12 december 2012 report research specialmedia.rtl.nl/media/financien/rtlz/2012/rabolist.pdf · food...

TRANSCRIPT

1 | Rabobank International – GFM Equity Research Please note the disclaimer on the last page of this document

Wednesday 12 December 2012 Report

Research Special

Conviction List 2013

Our conviction list generated a healthy 660bps alpha in 2012. For 2013, key themes

are (i) limited cyclical European exposure, (ii) balance sheet strenght, (iii) M&A

fantasy and (iv) attractive valuation and/or dividend yield. In light of a weakening

European macro picture, stock picking is key. We are not necessarily bearish on

equity markets given a relatively attractive return versus other asset classes.

Figure 1: Rabo Conviction List (last price 12 December 2012)

Company Entry date Entry price

(EUR)

Last price

(EUR)

α generation

since entry (%)

Price target

12-m (EUR)

Upside

(%)

Ahold (entry) 12-Dec-2012 10.2 10.2 11.0 8

ABInbev (exit) 31-Jan-2012 45.7 68.5 30.3 76.0 11

Barco 1-Aug-2012 46.5 53.6 7.5 63.0 18

CSM 10-Sept-2012 13.7 16.4 15.3 18.0 10

Fugro (re-entry) 12-Dec-2012 45.3 45.3 60.0 35

ING Group 10-Sept-2012 6.7 7.2 4.1 9.5 42

Reed Elsevier 9-Nov-2012 10.6 11.3 2.5 12.0 6

TomTom (entry) 12-Dec-2012 3.8 3.8 5.8 51

UNIT4 (entry) 12-Dec-2012 22.4 22.4 25.0 12

Average (incl. closed positions) 6.6

Performance since 6 January 2012

AEX 312.5 344.1 10.1

AMX 472.0 529.7 13.2

AScX 377.6 394.8 2.8

Bel-20 2,095.5 2431 16.7

Total return Rabo conviction list (%) 21.2

Source: Company data, Rabobank International

New entries in Rabobank Conviction List: Ahold, Fugro, TomTom and UNIT4

We add Ahold as a true value play, given its handsome FCF (10%) and attractive valuation, while the

ICA exit could imply a further increase in cash returns to shareholders. Fugro returns on our list, as we

feel that market concerns on recent management changes are overdone. We flag the still healthy

growth prospects for the subsea markets, while FCF should improve hugely. TomTom is primarily on

our list, as its maps and mapping expertise could be crucial to solve Apple’s map issues. This should

lead to significant benefits. UNIT4 is one of the very few European IT software plays to capture the

large SaaS opportunity, while remaining a prime M&A target also given its compelling valuation.

Barco, CSM, ING Group and Reed Elsevier remain top picks

We reiterate our preference for Belgian Barco, given triggers like (i) expected dividend pay-out

increases (in 13H1), (ii) confirmation of growth prospects in digital projector markets and

Entertainment (iii) add-on acquisitions, combined with a highly attractive valuation (< 7x P/E 2013)

Special sit CSM offers a number of triggers: (i) disposal of Bakery Supplies, (ii) substantial return of

cash to shareholders, (iii) new contracts in PLA and (iv) remaining ingredients business becoming

Analysts

David Tailleur

+31 30 7124474

Philip Scholte

+31 30 7124471

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

Research special

B runel *Rating:B uy (unchanged)

*Price as of 11 December 2 012 : EUR 3 6.83 (+1.08% ) *Price target: EUR 42 .00 (unchanged)

*EPS 2 012 E: EUR 2 .3 4 (unchanged)

an M&A target. ING offers upside from (i) multiple divestments, which so far generated sound take-

out prices leading to an enhanced capital base and (ii) a compelling valuation. The recent EC deal

markedly improved ING’s negotiation position. Reed Elsevier remains an ultimate safe play with

upside coming from (i) earnings revisions and (ii) potential room for extra cash returns.

Research special - 12 December 2012

2 | Rabobank International – GFM Equity Research

Overview closed ideas Rabo Conviction List in 2012

Figure 1: Overview closed ideas Rabo Conviction List

Company Open date Close date Open price Close price Alpha (%)

Fugro 6-1-2012 25-1-2012 45.97 48.85 3.5

Arcadis 6-1-2012 31-1-2102 12.84 14.85 7.0

Delhaize 6-1-2012 31-1-2012 43.99 42.17 -9.2

Wolters Kluwer 6-1-2012 3-7-2012 12.12 12.74 1.1

TenCate 6-1-2012 20-7-2012 22.01 19.54 -20.9

DSM 31-1-2012 6-3-2012 39.08 42.9 9.7

SBM Offshore 31-1-2012 23-3-2012 12.67 15.19 16.6

TKH 31-1-2012 29-6-2012 16.34 16.75 -1.4

Ahold 31-1-2012 1-8-2012 9.76 9.87 -4.5

Beter Bed 31-1-2012 30-8-2012 15.56 14.35 -4.9

Akzo Nobel 26-3-2012 30-7-2012 43.38 45.25 2.2

Aalberts Industries 10-9-2012 30-10-12 13.93 14.09 -0.6

Philips 01-08-2012 23-10-12 17.95 19.86 10.3

Wolters Kluwer 01-08-2012 8-11-2012 13.57 14.88 7.4

Fugro 22-5-2012 19-11-2012 47.65 42.02 -20.5

ABInbev 31-1-2012 12-12-2012 45.65 68.45 30.3

Source: Rabobank International

- 12 December 2012

3 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

Ahold Please note the disclaime r on the last page of this

Safe value play in troubled sector

Despite the Macro backdrop, we expect Ahold to continue to generate strong

FCF in both the US and the Netherlands. A balanced and disciplined approach

to the allocation of FCF likely implies the re-initiation of SBBs. Although the

market has not factored in an ICA exit, we see it is a key trigger for H1, offering

an additional upside of c. 10%.

Source: Company data, Rabobank International Year to December, fully diluted

More ambitious towards growth and in maximizing FCF

During the last 2 years, Ahold has become more transparent and more ambitious towards

maximising FCF and to invest in sustainable and profitable growth. Moreover, balance sheet

efficiency is to improve further and management will remain disciplined regarding CF allocation.

Strong ability to generate cash. Disciplined approach to CF allocation

The recent Capital Markets Day confirmed our view that Ahold is a true value stock, in terms of its

ability to generate EUR 1bn in FCF as well as towards the allocation of this. Whereas growth in

Europe will be driven by a combination improved customer loyalty, store openings and

remodels, growth in the US should come from optimisation of the existing network and further

add ons. We also believe that online expansion will accelerate, offering incremental sales with a

decent ROIC. On several occasions, management has stressed the disciplined approach towards

CF allocation. Annual FCF of EUR 1bn implies a combination of further add on deals and that

substantial cash will continue to be returned to SHs. We regard a major M&A deal as unlikely.

An ICA exit is the key trigger we expect to materialize by H1 2013

The share’s valuation has hardly factored in an exit from ICA. Part of the sceptic relates to

previous intentions to exit JMR, but the ICA case is different related to its size and Hakon being

much more cooperative. Based on a fair value of Ahold’s 60% stake in ICA of EUR 1.9bn and a

share split, Ahold trades at attractive 2013 multiples: 8.8x PER, an EV/EBITDA of 4.1x and a FCF

yield of 12.8%. Hakon’s 40% stake is implicitly valued at EUR 1.7bn, translating into 7.4x EBITDA

and a 27% premium vs Ahold’s stake. Such valuation is a reflection of ICA Sweden and the

baking by RE, while Axfood trades at 7x EV/EBITDA. An alternative scenario is a separate listing or

sale to Hakon, which proceeds are to be allocated to M&A (EUR 1bn) and SBB’s (EUR 1bn).

Analysts

Patrick Roquas

+31 (0)30 712 4470

Karel Zoete

+31 (0)30 712 4476

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

Ahold

*Rating:B uy (unchanged) *Price as of 05 December 2 012 : EUR 9.96 (+0.94% )

*Price target: EUR 11.00 (unchanged) *EPS 2 012 E: EUR 0.79 (unchanged)

Forecast 2011 2012E 2013E 2014E

Sales (EURm) 30,271 33,059 34,378 35,377

EBITDA (EUR m) 2,143 2,247 2,330 2,436

EBIT before exceptionals (EUR m) 1,346 1,371 1,426 1,506

Recurring net income (EUR m) 1,031 865 1,084 1,161

EPS Recurring New (EUR) 0.88 0.79 0.99 1.06

EPS Recurring Old (EUR) 0.88 0.79 0.99 1.06

P/E 10.6 12.6 10.0 9.4

EV/EBITDA 5.3 5.3 4.9 4.5

FCF Yield (%) 7.4 10.4 11.0 11.1

Dividend Yield (%) 4.0 4.5 4.7 5.1

Rating Buy =

Price target (12m) EUR 11.00 =

Price 05-Dec-2012 EUR 9.96

Up-/downside 10.5%

Food & Staples Retailing

Netherlands

Market capitalisation

EUR 10,562m

Avg (3month) daily turnover

3,373,625

Reuters

AHLN.AS

Bloomberg

AH NA

Web site

www.ahold.com

Share Performance

1m 3m 12m

Ahold 1.9 -1.3 4.5

AEX 1.1 3.0 11.1

Agenda

None --

- 12 December 2012

4 | Rabobank International – GFM Equity Research

Financial Information

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2008 2009 2010 2011 2012E 2013E 2014E 2015EIncome Statement (EUR mln)Revenues 25,722 27,926 29,518 30,271 33,059 34,378 35,377 36,410Cost of sales -18,777 -20,338 -21,601 -22,152 -24,193 -25,158 -25,889 -26,645Gross profit 6,945 7,587 7,917 8,119 8,866 9,220 9,488 9,765Operating costs 0 0 0 0 0 0 0 0EBITDA 1,866 2,053 2,148 2,143 2,247 2,330 2,436 2,535Depreciation -662 -756 -812 -797 -876 -904 -930 -958EBITA (before exceptionals) 1,204 1,297 1,336 1,346 1,371 1,426 1,506 1,577Exceptional items 0 0 0 0 0 0 0 0Amortisation of goodwill & other ITA 0 0 0 0 0 0 0 0EBIT 1,204 1,297 1,336 1,346 1,371 1,426 1,506 1,577Net financial result -216 -283 -259 -316 -223 -214 -206 -197Other pre-tax items 0 0 0 0 0 0 0 0EBT 988 1,014 1,077 1,030 1,148 1,212 1,300 1,380Income taxes -226 -148 -271 -140 -277 -304 -326 -347Minority interests -5 0 0 0 0 0 0 0Other post-tax items / participation 124 106 57 141 -6 176 187 197Extraordinary Items & Discontinued Operations 0 0 0 0 0 0 0 0Net income 881 972 863 1,031 865 1,084 1,161 1,231Extraordinary Items & Amortisation 0 0 0 0 0 0 0 0Net income recurring (cash) 881 972 863 1,031 865 1,084 1,161 1,231Balance Sheet (EUR mln)Cash & Cash equivalents 2,863 2,688 2,600 2,438 1,587 2,166 2,798 3,468Current assets 2,433 2,417 2,594 2,755 N/A N/A N/A N/ATangible fixed assets 5,532 5,407 5,827 5,984 6,103 6,161 6,222 6,283Goodwill 251 619 762 836 1,663 1,663 1,663 1,663Other Intangible assets 0 0 0 0 0 0 0 0Other non-current assets 2,513 2,802 2,942 2,967 N/A N/A N/A N/ATotal Assets 13,591 13,933 14,725 14,980 14,899 15,543 16,328 17,156

Short-term debt 271 564 216 648 384 384 384 384Current liabs 3,867 3,461 3,876 3,966 4,020 4,180 4,302 4,427Long-term debt 3,924 3,413 3,577 3,302 3,380 3,380 3,380 3,380Other non-current liabs 853 1,055 1,146 1,187 1,260 1,233 1,258 1,284Minority interest 0 0 0 0 0 0 0 0Total equity 4,687 5,440 5,910 5,877 5,768 6,365 7,003 7,680Total liabs & equity 13,602 13,933 14,725 14,980 14,813 15,543 16,328 17,156

Net debt 1,586 725 977 1,086 1,615 1,123 688 13Invested capital 19,246 19,476 19,651 19,814 19,649 19,580 19,587 19,593Invested capital excl. hitorical goodwill 3,705 3,935 4,110 4,273 4,108 4,039 4,045 4,052Off balance lease liabilities 2,927 3,178 3,359 3,445 3,762 3,913 4,026 4,144Net pension assets -113 -96 -129 -94 N/A N/A N/A N/ACash Flow Statement (EUR mln)Operating income 1,204 1,297 1,336 1,346 1,371 1,426 1,506 1,577Depreciation & Amortisation 662 756 812 797 876 904 930 958Other non-cash Items 0 0 0 0 0 0 0 0Change in Working Capital -629 -433 326 -83 138 -20 25 26Change in Provisions 109 144 87 19 -12 -27 25 26Cash taxes -226 -148 -271 -140 -277 -304 -326 -347Cash interest -216 -283 -259 -316 -223 -214 -206 -197Cash impact associates & minorities 129 106 57 141 -6 176 187 197Other cash expectionals / cash flow assets held for sale 0 0 0 0 1 2 2 2Operating cash flow 1,070 1,498 2,092 1,786 1,953 1,944 2,143 2,242

CAPEX 1,080 632 1,100 938 926 963 991 1,019Acquisitions & Disposals 0 0 0 0 790 0 0 0Other Investments 38 289 140 25 -49 -154 12 12Cash Flow from Investments 1,118 921 1,240 963 1,667 808 1,003 1,032

Cash dividend -176 -292 -345 -412 -433 -488 -522 -554Change in Equity 0 0 0 -523 -568 0 0 0Change in Bank Debt -473 -218 -184 157 -186 0 0 0Other adjustments -82 0 0 0 0 0 0 0Cash Flow from Financing -731 -510 -529 -778 -1,186 -488 -522 -554FX effect N/A N/A N/A N/A N/A N/A N/A N/AChange in Cash -780 68 323 44 -901 646 616 654

Free Cash Flow -49 577 852 823 1,076 1,134 1,139 1,208

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

5 | Rabobank International – GFM Equity Research

Source: Rabobank International

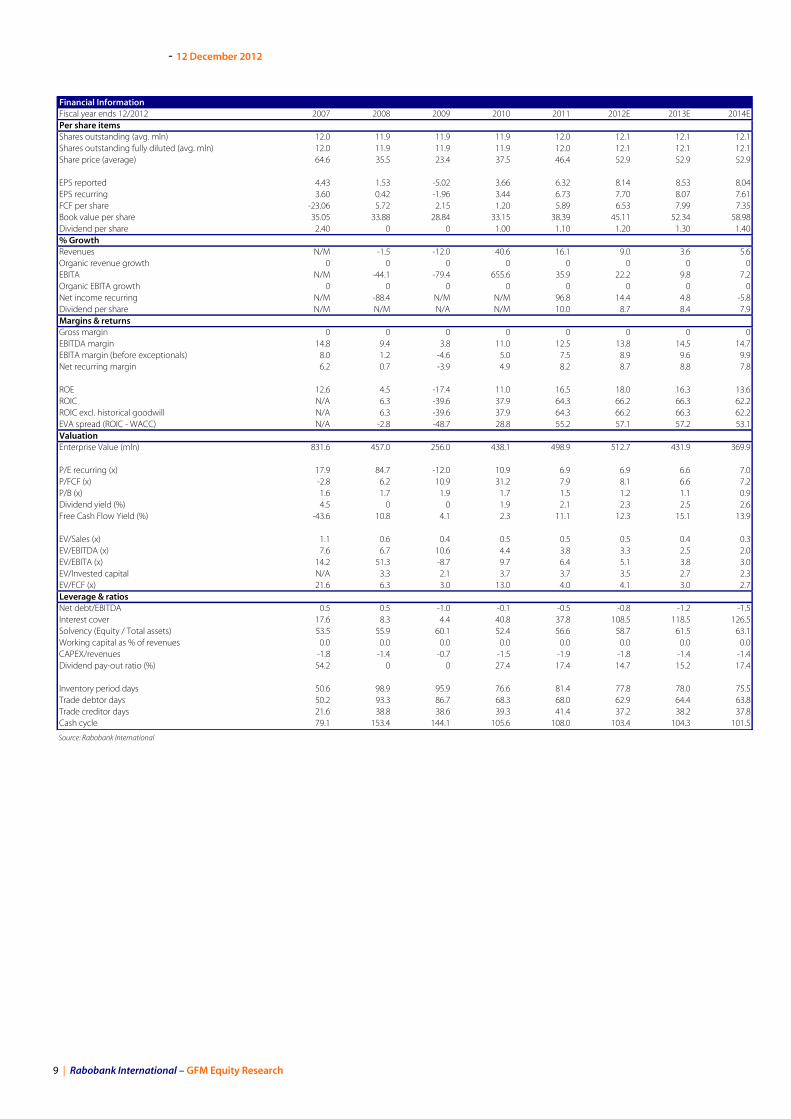

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EPer share itemsShares outstanding (avg. mln) 22.7 22.9 23.1 23.2 23.4 23.7 23.8 24.0Shares outstanding fully diluted (avg. mln) 22.7 22.9 23.1 23.2 23.5 24.0 24.2 24.4Share price (average) 22.3 13.9 15.8 25.1 27.6 35.8 35.8 35.8

EPS reported 1.59 1.96 1.34 1.08 1.83 2.37 2.74 3.21EPS recurring 1.59 1.96 1.34 1.15 1.82 2.34 2.70 3.16FCF per share 1.15 0.72 2.41 0.02 0.30 1.38 2.25 1.47Book value per share 5.94 7.12 7.81 8.69 10.10 11.16 12.47 14.01Dividend per share 0.70 0.80 0.80 0.80 0.90 1.17 1.35 1.58% GrowthRevenues 16.2 23.2 3.4 -2.4 35.9 25.9 4.7 12.2Organic revenue growth 16.2 23.2 3.4 -2.4 35.9 25.9 4.7 12.2EBITA 44.9 21.1 -27.3 -12.5 63.1 29.8 15.6 17.7Organic EBITA growth 44.9 21.1 -27.3 -12.5 63.1 29.8 15.6 17.7Net income recurring 51.8 24.2 -30.8 -14.2 61.0 31.1 16.0 18.0Dividend per share 90.5 14.9 -0.2 -0.9 13.3 29.8 15.1 17.1Margins & returnsGross margin 23.5 23.4 20.8 21.1 19.7 18.5 18.7 18.5EBITDA margin 9.4 9.1 6.6 6.0 7.0 7.3 8.0 8.4EBITA margin (before exceptionals) 8.8 8.7 6.1 5.5 6.6 6.8 7.5 7.9Net recurring margin 6.2 6.3 4.2 3.7 4.4 4.6 5.0 5.3

ROE 26.8 27.6 17.2 12.5 18.1 21.3 21.9 22.9ROIC 40.6 43.0 29.5 22.4 30.5 32.8 32.7 34.9ROIC excl. historical goodwill 42.5 44.7 31.1 23.8 32.1 34.2 33.9 36.0EVA spread (ROIC - WACC) 31.6 34.0 20.5 13.4 21.5 23.8 23.7 25.9ValuationEnterprise Value (mln) 468.8 280.7 294.1 523.6 568.1 791.5 773.6 775.2

P/E recurring (x) 14.0 7.1 11.7 21.9 15.2 15.3 13.3 11.3P/FCF (x) 19.4 19.2 6.5 1,256.6 91.0 25.9 15.9 24.3P/B (x) 6.2 5.2 4.7 4.2 3.6 3.2 2.8 2.5Dividend yield (%) 2.0 2.3 2.2 2.2 2.5 3.3 3.8 4.4Free Cash Flow Yield (%) 3.2 2.0 6.8 0.1 0.8 3.9 6.3 4.1

EV/Sales (x) 0.8 0.4 0.4 0.7 0.6 0.6 0.6 0.5EV/EBITDA (x) 8.6 4.3 6.1 12.1 8.3 8.8 7.5 6.4EV/EBITA (x) 9.1 4.5 6.5 13.3 8.8 9.5 8.0 6.8EV/Invested capital 5.2 2.7 2.7 4.5 4.1 4.7 3.9 3.6EV/FCF (x) 17.9 16.9 5.3 1,126.6 79.5 23.9 14.2 21.6Leverage & ratiosNet debt/EBITDA -0.7 -0.6 -1.5 -1.5 -1.3 -0.8 -0.9 -0.8Interest cover -719.7 -168.0 N/M -41.5 -78.3 -130.0 -97.8 -84.9Solvency (Equity / Total assets) 68.2 69.1 70.8 68.7 60.8 62.2 63.9 64.1Working capital as % of revenues 13.8 14.7 10.8 15.5 12.4 13.7 13.7 14.5CAPEX/revenues -0.7 -0.6 -0.8 -0.5 -0.7 -0.5 -0.5 -0.5Dividend pay-out ratio (%) 44.0 41.0 59.7 73.5 49.2 49.4 49.2 49.1

Inventory period days 0 0 0 0 0 0 0 0Trade debtor days 87.3 80.1 78.9 85.2 84.2 83.7 88.1 86.7Trade creditor days 9.6 7.8 7.3 8.5 29.2 25.5 10.7 10.4Cash cycle 77.7 72.3 71.6 76.7 54.9 58.2 77.4 76.4

- 12 December 2012

6 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

Barco Please note the disclaime r on the last page of this

An acquired taste

Besides further growth of Barco’s business, for H1 2013, we see several share

price triggers, especially shareholder payout increases and additional insight in

the digital projector market. Furthermore, in our view Barco’s valuation remains

attractive at below 7x 2013 earnings, also as we see several initiatives in place

to partly counter the effects of lower cinema digitalization revenue in 2015.

Source: Company data, Rabobank International Year to December, fully diluted

Continued strong growth and lot’s of new order wins

Besides continued news regarding (smaller sized) project wins and new initiatives, the main

news items for Barco are: (i) Chinese cinema market. In December Barco announced that they

will supply 800 digital cinema projectors to the China Film Group. In addition, they announced

that the annual number of devices purchased from Barco will increase each year. China is still a

growing market in which Barco has a market share over 60%. We note that Barco is able to

produce around 10k screens per annum, so this order represents around one month of

production capacity, and (ii) Q3 2012 reported figures. Barco reported very strong revenue

growth, supported by all divisions. Q3 2012 revenues came in at EUR 285m, up 13% compared to

last year. We note that the growth in the Healthcare division was only 4.8%, as the announced

acquisitions and investments currently do not contribute. Q3 2012 order intake was very strong

at EUR 291m, increasing the order book to EUR 503. (75% relates to orders for Q4 2012 and Q1

2013). In addition, Barco stated that the EBITDA margin increased compared to last year,

consistent with the progress reported for H1 2012 (EBITDA margin 13.5%). Barco’s net cash

position further increased, at Q3 2012 we anticipate > EUR 80m of cash (> EUR 6.5 ps).

Many share price triggers for H1 2013

Besides further growth, in our view the main triggers for Barco’s share price are: (i) Shareholder

payout increases. We anticipate more news regarding a possible share buyback program and

dividend increase in H1 2013, (ii) Additional insight in the digital projector (replacement) market

and new products in the Entertainment division. We also anticipate more insight in this market

during H1 2013, which should take some uncertainty regarding a possible strong decrease of

revenues related to the saturation of the cinema market regarding the transformation to

digitalization, (iii) Add-on acquisitions, i.e. in line with the JAOtech and FIMI acquisitions and in

line with Barco’s strategy as set out during its 2012 CMD, and (iv) A take-out bid.

Analysts

Micha Tiekink

+31 (0)30 712 4475

Philip Scholte

+31 (0)30 712 4471

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

B arco

*Rating:B uy (unchanged) *Price as of 10 December 2 012 : EUR 52 .91 ( -3 .10% )

*Price target: EUR 63 .00 (unchanged) *EPS 2 012 E: EUR 7.70 (unchanged)

Forecast 2011 2012E 2013E 2014E

Sales (EURm) 1,041 1,135 1,176 1,242

EBITDA (EUR m) 130 157 171 182

EBIT before exceptionals (EUR m) 78 101 113 123

Recurring net income (EUR m) 86 98 103 97

EPS Recurring New (EUR) 6.73 7.70 8.07 7.61

EPS Recurring Old (EUR) 6.73 7.70 8.07 7.61

P/E 6.9 6.9 6.6 7.0

EV/EBITDA 3.8 3.3 2.5 2.0

FCF Yield (%) 11.1 12.3 15.1 13.9

Dividend Yield (%) 2.1 2.3 2.5 2.6

Rating Buy =

Price target (12m) EUR 63.00 =

Price 10-Dec-2012 EUR 52.91

Up-/downside 19.1%

Electronic Equipment, Instruments & Components

Belgium

Market capitalisation

EUR 670m

Avg (3month) daily turnover

18,131

Reuters

BARBt.BR

Bloomberg

BAR BB

Web site

www.barco.com

Share Performance

1m 3m 12m

Barco -5.8 2.5 52.2

BEL MID 1.2 5.9 18.5

Agenda

None --

- 12 December 2012

7 | Rabobank International – GFM Equity Research

Valuation still looks very appealing, Buy reiterated

Although we recognize the temporarily strong demand from the entertainment industry as a result of the

transition to digital cinema, Barco is attractively valued at below 7x 2013 earnings, as (i) In our view several

measures are in place to partly counter the effects of the decrease of revenues in the Entertainment division after

2014/2015, i.e. (a) Laser technology, which could be a catalyst for the replacement cycle, (b) mid-market

initiatives, (c) strong growth of the Entertainment business unrelated to the digitalization of cinema’s, we

understand that the growth in 2012 mainly stems from this part of the Entertainment business, and (d) finally the

replacement market, (ii) Barco currently has a net cash position of > EUR 80m, (iii) Barco is not capital intensive,

and (iv) Barco has a FCF yield >10%. We reiterate our Buy rating and a PT of EUR 63.

Dependency on economic developments seems to be limited at Barco

YTD Q3 2012 Barco has shown revenue growth of 10%, driven by all businesses, but predominantly by the

Control Rooms & Simulation (+13%), Defense & Aerospace (21%) and Ventures (+17%) businesses. Despite this

strong growth so far, we note that part of Barco’s business is affected by the difficult mature European markets

and austerity measures by governments. As a result, the growth has come mainly from Latin American, Asian and

the Middle Eastern markets, offset by more difficult North American and European markets. Furthermore, as a part

of Barco’s business supports the efficiency and effectiveness of certain end markets, f.i. in Healthcare markets

Barco’s products are relevant for the growth of endoscopic surgery and in Defense markets Barco’s products are

supportive to the development towards unmanned drones, Barco should be able to partly grow its business

despite (more) difficult mature European markets and additional austerity measures by governments.

- 12 December 2012

8 | Rabobank International – GFM Equity Research

Financial Information

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EIncome Statement (EUR mln)Revenues 736 725 638 897 1,041 1,135 1,176 1,242Cost of sales 736 725 638 897 1,041 1,135 1,176 1,242Gross profit 0 0 0 0 0 0 0 0Operating costs N/A N/A N/A N/A N/A N/A N/A N/AEBITDA 109 68 24 99 130 157 171 182Depreciation -11 -13 -13 -13 -14 -15 -15 -15EBITA (before exceptionals) 98 55 11 85 116 142 156 167Exceptional items 0 0 0 0 -0 0 0 0Amortisation of goodwill & other ITA -40 -46 -41 -40 -38 -41 -43 -45EBIT 59 9 -30 45 78 101 113 123Net financial result -6 -8 -5 -2 -3 -1 -1 -1Other pre-tax items 4 4 4 1 1 3 4 5EBT 56 5 -31 44 75 103 115 126Income taxes -10 0 6 0 10 -5 -12 -29Minority interests -0 0 0 0 0 0 0 0Other post-tax items / participation 0 0 0 0 0 0 0 0Extraordinary Items & Discontinued Operations 8 13 -35 0 -10 0 0 0Net income 53 18 -60 44 76 98 103 97Extraordinary Items & Amortisation -8 -13 35 0 10 0 0 0Net income recurring (cash) 46 5 -25 44 86 98 103 97Balance Sheet (EUR mln)Cash & Cash equivalents 73 72 46 46 79 143 224 296Current assets 493 418 323 472 465 501 513 536Tangible fixed assets 65 62 54 56 58 63 65 67Goodwill 48 57 32 53 44 44 44 44Other Intangible assets 81 71 60 68 84 90 95 100Other non-current assets 27 40 58 59 85 85 85 85Total Assets 788 721 572 755 815 927 1,027 1,128

Short-term debt 112 91 11 27 8 8 8 8Current liabs 236 207 200 306 318 347 359 379Long-term debt 15 14 12 13 19 19 19 19Other non-current liabs 4 6 5 13 8 9 9 10Minority interest 0 0 0 0 0 0 0 0Total equity 422 403 344 396 461 544 632 712Total liabs & equity 788 721 572 755 815 927 1,027 1,128

Net debt 53 33 -23 -9 -62 -126 -207 -269Invested capital 147 134 114 124 142 154 161 167Invested capital excl. hitorical goodwill 147 134 114 124 142 154 161 167Off balance lease liabilities 0 0 0 0 0 0 0 0Net pension assets 0 0 0 0 0 0 0 0Cash Flow Statement (EUR mln)Operating income 59 9 -30 45 78 101 113 123Depreciation & Amortisation 50 59 54 54 52 55 58 60Other non-cash Items 0 0 31 1 11 0 0 0Change in Working Capital -61 39 80 -47 31 -8 0 -3Change in Provisions 4 2 -0 8 -5 1 0 1Cash taxes -16 -17 0 0 -11 -5 -12 -29Cash interest -2 -4 -2 -1 -3 2 2 3Cash impact associates & minorities -0 0 0 0 0 0 0 0Other cash expectionals / cash flow assets held for sale 18 -5 -43 -12 -6 0 0 0Operating cash flow 52 83 90 47 145 146 161 155

CAPEX -13 -10 -5 -13 -20 -20 -17 -17Acquisitions & Disposals 0 -36 0 -10 -9 0 0 0Other Investments -52 -47 -52 -41 -55 -47 -48 -49Cash Flow from Investments -55 -33 -33 -62 -83 -67 -65 -66

Cash dividend -28 -29 0 0 -13 -14 -16 -17Change in Equity -10 -1 0 0 4 0 0 0Change in Bank Debt 33 -22 -83 15 -20 0 0 0Other adjustments 1 1 0 0 1 0 0 0Cash Flow from Financing -4 -51 -83 15 -28 -14 -16 -17FX effect N/A N/A N/A N/A N/A N/A N/A N/AChange in Cash -8 -1 -26 0 33 64 81 72

Free Cash Flow 39 73 85 34 125 126 144 138

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

9 | Rabobank International – GFM Equity Research

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EPer share itemsShares outstanding (avg. mln) 12.0 11.9 11.9 11.9 12.0 12.1 12.1 12.1Shares outstanding fully diluted (avg. mln) 12.0 11.9 11.9 11.9 12.0 12.1 12.1 12.1Share price (average) 64.6 35.5 23.4 37.5 46.4 52.9 52.9 52.9

EPS reported 4.43 1.53 -5.02 3.66 6.32 8.14 8.53 8.04EPS recurring 3.60 0.42 -1.96 3.44 6.73 7.70 8.07 7.61FCF per share -23.06 5.72 2.15 1.20 5.89 6.53 7.99 7.35Book value per share 35.05 33.88 28.84 33.15 38.39 45.11 52.34 58.98Dividend per share 2.40 0 0 1.00 1.10 1.20 1.30 1.40% GrowthRevenues N/M -1.5 -12.0 40.6 16.1 9.0 3.6 5.6Organic revenue growth 0 0 0 0 0 0 0 0EBITA N/M -44.1 -79.4 655.6 35.9 22.2 9.8 7.2Organic EBITA growth 0 0 0 0 0 0 0 0Net income recurring N/M -88.4 N/M N/M 96.8 14.4 4.8 -5.8Dividend per share N/M N/M N/A N/M 10.0 8.7 8.4 7.9Margins & returnsGross margin 0 0 0 0 0 0 0 0EBITDA margin 14.8 9.4 3.8 11.0 12.5 13.8 14.5 14.7EBITA margin (before exceptionals) 8.0 1.2 -4.6 5.0 7.5 8.9 9.6 9.9Net recurring margin 6.2 0.7 -3.9 4.9 8.2 8.7 8.8 7.8

ROE 12.6 4.5 -17.4 11.0 16.5 18.0 16.3 13.6ROIC N/A 6.3 -39.6 37.9 64.3 66.2 66.3 62.2ROIC excl. historical goodwill N/A 6.3 -39.6 37.9 64.3 66.2 66.3 62.2EVA spread (ROIC - WACC) N/A -2.8 -48.7 28.8 55.2 57.1 57.2 53.1ValuationEnterprise Value (mln) 831.6 457.0 256.0 438.1 498.9 512.7 431.9 369.9

P/E recurring (x) 17.9 84.7 -12.0 10.9 6.9 6.9 6.6 7.0P/FCF (x) -2.8 6.2 10.9 31.2 7.9 8.1 6.6 7.2P/B (x) 1.6 1.7 1.9 1.7 1.5 1.2 1.1 0.9Dividend yield (%) 4.5 0 0 1.9 2.1 2.3 2.5 2.6Free Cash Flow Yield (%) -43.6 10.8 4.1 2.3 11.1 12.3 15.1 13.9

EV/Sales (x) 1.1 0.6 0.4 0.5 0.5 0.5 0.4 0.3EV/EBITDA (x) 7.6 6.7 10.6 4.4 3.8 3.3 2.5 2.0EV/EBITA (x) 14.2 51.3 -8.7 9.7 6.4 5.1 3.8 3.0EV/Invested capital N/A 3.3 2.1 3.7 3.7 3.5 2.7 2.3EV/FCF (x) 21.6 6.3 3.0 13.0 4.0 4.1 3.0 2.7Leverage & ratiosNet debt/EBITDA 0.5 0.5 -1.0 -0.1 -0.5 -0.8 -1.2 -1.5Interest cover 17.6 8.3 4.4 40.8 37.8 108.5 118.5 126.5Solvency (Equity / Total assets) 53.5 55.9 60.1 52.4 56.6 58.7 61.5 63.1Working capital as % of revenues 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0CAPEX/revenues -1.8 -1.4 -0.7 -1.5 -1.9 -1.8 -1.4 -1.4Dividend pay-out ratio (%) 54.2 0 0 27.4 17.4 14.7 15.2 17.4

Inventory period days 50.6 98.9 95.9 76.6 81.4 77.8 78.0 75.5Trade debtor days 50.2 93.3 86.7 68.3 68.0 62.9 64.4 63.8Trade creditor days 21.6 38.8 38.6 39.3 41.4 37.2 38.2 37.8Cash cycle 79.1 153.4 144.1 105.6 108.0 103.4 104.3 101.5

- 12 December 2012

10 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

CSM Please note the disclaime r on the last page of this

A Sure Fire Win

Since announcing its strategic repositioning, the shares gained almost 50%.

More time might be required to sell BS, but we have become more optimistic

regarding the potential for cash returns and new contracts in PLA. Combined

with a target multiple of 7.5x EBITDA for Ingredients, these factors provide

further upside to EUR 20-25.

Source: Company data, Rabobank International Year to December, fully diluted

Fair value Bakery Supplies estimated at EUR 0.8 – 1.2bn

Our base case values BS at EUR 1bn, or 5.4x post synergies, justified by the options CSM has in

selling the assets and the financial and strategic upside for the acquirer. Although we assume

sound interest for the US assets, selling Europe might require more time or an exit in several

pieces. The key risk remains that Bakery is sold for EUR 800m, only 4.4x EBITDA post synergies.

Combined with a target multiple for Ingredients of 7.5x EBITDA, generates a PT of EUR 12.

However, selling below EUR 800m would: (i) provide little comfort for new M&A, (ii) weaken the

position of the team, and thus, (iii) make CSM vulnerable for a hostile take-over or a full break up.

In such event, we apply a target multiple of 10-11x, translating into a SOTP of EUR 17. Our worst

case PT therefore arrives in the midst at c. EUR 14. Our blue sky PT offers 56% upside: (i) Bakery is

sold for EUR 1.2bn, (ii) up to EUR 350m in cash is returned, (iii) Ingredients becomes a prey.

From niche to mainstream in PLA could be imminent

Rumours are that Purac will become a partner of PTT in the development of PLA. Such would be

excellent news, albeit that the market is skeptic given previews delays and disappointments: (i)

how likely is it for PPT and Purac to team up, (ii) how fast will PTT and Purac scale up? For three

reasons, we believe a partnership is realistic: (i) it would provide PTT improved security of supply,

(ii) we hear ongoing rumours that PTT is not satisfied with the quality of the PLA supplied by

Natureworks, while Purac’s PLA would give way to high end applications.

Sequence of triggers for the next 12 months

We anticipate the following triggers: (i) news in Q4 2012 might already provide an indication of

the potential disposal price, followed by a preliminary agreement, (iii) the announcement of a

SBB in H1 2013, (iv) the strategy for the remaining business being presented in H1 2013.

Analysts

Patrick Roquas

+31 (0)30 712 4470

Karel Zoete

+31 (0)30 712 4476

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

CSM

*Rating:B uy (unchanged) *Price as of 05 December 2 012 : EUR 15 .93 (+4.05% )

*Price target: EUR 17.5 0 (unchanged) *EPS 2 012 E: EUR 1.3 6 (unchanged)

Forecast 2011 2012E 2013E 2014E

Sales (EURm) 3,113 3,312 3,388 3,585

EBITDA (EUR m) 223 235 249 265

EBIT before exceptionals (EUR m) -129 137 157 178

Recurring net income (EUR m) -174 59 96 118

EPS Recurring New (EUR) 0.89 1.36 1.54 1.94

EPS Recurring Old (EUR) 0.89 1.36 1.54 1.94

P/E 21.8 11.7 10.3 8.2

EV/EBITDA 8.4 7.0 6.3 5.8

FCF Yield (%) 4.0 7.6 11.1 8.5

Dividend Yield (%) 4.4 4.4 4.4 4.4

Rating Buy =

Price target (12m) EUR 17.50 =

Price 05-Dec-2012 EUR 15.93

Up-/downside 9.9%

Food Products

Netherlands

Market capitalisation

EUR 1,114m

Avg (3month) daily turnover

261,506

Reuters

CSMNc.AS

Bloomberg

CSM NA

Web site

www.csm.nl

Share Performance

1m 3m 12m

CSM 2.1 18.0 40.4

AMX 0.2 4.6 12.7

Agenda

None --

- 12 December 2012

11 | Rabobank International – GFM Equity Research

Financial Information

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2008 2009 2010 2011 2012E 2013E 2014E 2015EIncome Statement (EUR mln)Revenues 2,599 2,556 2,990 3,113 3,312 3,388 3,585 3,725Cost of sales -2,079 -2,045 -2,392 -2,490 -2,650 -2,710 -2,868 -2,980Gross profit 520 511 598 623 662 678 717 745Operating costs N/A N/A N/A N/A N/A N/A N/A N/AEBITDA 192 212 287 223 235 249 265 288Depreciation 59 61 72 72 73 69 66 68EBITA (before exceptionals) 113 151 215 151 162 180 199 220Exceptional items 0 0 -21 -21 -34 -4 0 0Amortisation of goodwill & other ITA -7 -8 -36 -280 -25 -23 -21 -21EBIT 107 143 158 -149 103 153 178 199Net financial result -28 -29 -28 -30 -26 -25 -19 -17Other pre-tax items 0 0 0 0 0 0 0 0EBT 78 114 131 -179 77 128 159 183Income taxes 12 -27 -31 5 -18 -32 -41 -48Minority interests 0 0 0 0 0 0 0 0Other post-tax items / participation 0 0 0 0 0 0 0 0Extraordinary Items & Discontinued Operations 0 0 0 0 0 0 0 0Net income 90 87 99 -174 59 96 118 134Extraordinary Items & Amortisation 0 0 0 0 0 0 0 0Net income recurring (cash) 90 87 99 -174 59 96 118 134Balance Sheet (EUR mln)Cash & Cash equivalents 84 120 119 116 126 193 236 281Current assets 662 554 718 740 736 744 787 817Tangible fixed assets 513 500 575 583 590 592 615 659Goodwill 774 766 1,147 912 928 905 884 863Other Intangible assets 0 0 0 0 0 0 0 0Other non-current assets 74 64 70 64 62 62 62 62Total Assets 2,107 2,004 2,627 2,415 2,443 2,497 2,584 2,683

Short-term debt 5 4 4 5 8 8 8 8Current liabs 473 444 638 623 629 637 655 669Long-term debt 607 445 746 727 723 723 723 723Other non-current liabs 80 111 123 113 107 107 107 107Minority interest 0 0 0 0 0 0 0 0Total equity 942 1,000 1,117 948 976 1,023 1,091 1,176Total liabs & equity 2,107 2,004 2,627 2,415 2,443 2,497 2,584 2,683

Net debt 528 328 631 616 605 538 495 450Invested capital 622 498 532 588 590 593 640 701Invested capital excl. hitorical goodwill 622 498 532 588 590 593 640 701Off balance lease liabilities 70 68 80 83 89 91 96 100Net pension assets 0 0 0 0 0 0 0 0Cash Flow Statement (EUR mln)Operating income 107 143 158 -149 103 153 178 199Depreciation & Amortisation -52 -54 -36 208 -48 -46 -45 -47Other non-cash Items 0 0 0 0 0 0 0 0Change in Working Capital -37 80 21 -40 7 -2 -28 -20Change in Provisions -52 31 12 -10 -6 0 0 0Cash taxes 12 -27 -31 5 -18 -32 -41 -48Cash interest -28 -29 -28 -30 -26 -25 -19 -17Cash impact associates & minorities 0 0 0 0 0 0 0 0Other cash expectionals / cash flow assets held for sale 3 4 5 6 7 8 8 8Operating cash flow 70 271 244 133 164 195 184 211

CAPEX 52 48 146 92 80 72 89 112Acquisitions & Disposals 0 0 0 0 0 0 0 0Other Investments 16 -10 6 -6 -1 0 0 0Cash Flow from Investments 69 38 152 86 79 72 89 112

Cash dividend -54 -57 -44 77 -26 -42 -52 -59Change in Equity 0 0 0 0 0 0 0 0Change in Bank Debt 118 -163 301 -18 -1 0 0 0Other adjustments 0 0 0 0 0 0 0 0Cash Flow from Financing 64 -220 257 59 -26 -42 -52 -59FX effect N/A N/A N/A N/A N/A N/A N/A N/AChange in Cash 62 9 344 100 52 73 36 32

Free Cash Flow -2 229 87 42 79 115 88 92

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

12 | Rabobank International – GFM Equity Research

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2008 2009 2010 2011 2012E 2013E 2014E 2015EPer share itemsShares outstanding (avg. mln) 61.8 64.8 65.9 67.6 68.8 68.8 68.8 68.8Shares outstanding fully diluted (avg. mln) 61.8 65.0 68.0 68.0 68.0 68.0 68.0 68.0Share price (average) 18.2 12.8 22.6 19.4 15.9 15.9 15.9 15.9

EPS reported 1.46 1.34 1.51 -2.58 0.85 1.40 1.71 1.95EPS recurring 1.86 1.40 1.84 0.89 1.36 1.54 1.94 2.18FCF per share -0.03 3.53 1.34 0.64 1.21 1.77 1.35 1.41Book value per share 15.22 15.42 16.96 14.04 14.18 14.48 21.56 23.72Dividend per share 0.88 0.88 0.90 0.70 0.70 0.70 0.70 0.70% GrowthRevenues 4.6 -1.7 17.0 4.1 6.4 2.3 5.8 3.9Organic revenue growth N/A N/A N/A N/A N/A N/A N/A N/AEBITA 73.2 32.9 42.9 -29.9 7.4 11.2 10.6 10.6Organic EBITA growth N/A N/A N/A N/A N/A N/A N/A N/ANet income recurring -55.6 -3.6 14.4 N/M N/M 64.5 22.5 14.0Dividend per share 0 0 2.3 -22.2 0 0 0 0Margins & returnsGross margin 20.0 20.0 20.0 20.0 20.0 20.0 20.0 20.0EBITDA margin 7.4 8.3 9.6 7.2 7.1 7.4 7.4 7.7EBITA margin (before exceptionals) 4.1 5.6 6.0 -4.1 4.1 4.6 5.0 5.4Net recurring margin 3.5 3.4 3.3 -5.6 1.8 2.8 3.3 3.6

ROE 9.6 8.7 8.9 -18.4 6.0 9.4 10.8 11.4ROIC 20.3 19.8 23.4 -20.3 13.3 19.4 21.7 22.3ROIC excl. historical goodwill 20.3 19.8 23.4 -20.3 13.3 19.4 21.7 22.3EVA spread (ROIC - WACC) 10.7 10.1 13.7 -30.0 3.6 9.8 12.0 12.6ValuationEnterprise Value (mln) 1,654.6 1,158.1 2,101.9 1,874.9 1,640.0 1,572.6 1,530.4 1,485.3

P/E recurring (x) 9.8 9.2 12.3 21.8 11.7 10.3 8.2 7.3P/FCF (x) -570.6 3.6 16.9 30.3 13.2 9.0 11.8 11.3P/B (x) 1.2 1.1 1.0 1.2 1.1 1.1 1.0 0.9Dividend yield (%) 5.5 5.5 5.6 4.4 4.4 4.4 4.4 4.4Free Cash Flow Yield (%) -0.2 22.1 8.4 4.0 7.6 11.1 8.5 8.9

EV/Sales (x) 0.6 0.5 0.7 0.6 0.5 0.5 0.4 0.4EV/EBITDA (x) 8.6 5.5 7.3 8.4 7.0 6.3 5.8 5.1EV/EBITA (x) 15.5 8.1 11.7 -14.5 12.0 10.0 8.6 7.4EV/Invested capital 2.8 2.1 4.1 3.3 2.8 2.7 2.5 2.2EV/FCF (x) -838.2 5.1 24.1 45.1 20.9 13.6 17.4 16.2Leverage & ratiosNet debt/EBITDA 2.8 1.5 2.2 2.8 2.6 2.2 1.9 1.6Interest cover 6.8 7.3 10.4 7.5 9.0 10.0 13.6 17.2Solvency (Equity / Total assets) 44.7 49.9 42.5 39.3 39.9 41.0 42.2 43.8Working capital as % of revenues 7.3 4.3 2.7 3.8 3.2 3.2 3.7 4.0CAPEX/revenues 2.0 1.9 4.9 2.9 2.4 2.1 2.5 3.0Dividend pay-out ratio (%) 60.5 65.7 59.7 -27.1 82.3 50.0 40.8 35.8

Inventory period days 39.8 40.1 35.8 39.5 37.3 36.4 35.3 35.6Trade debtor days 46.2 45.0 40.5 43.5 42.4 42.9 42.2 42.5Trade creditor days 32.6 32.9 31.8 35.7 34.6 34.4 33.8 34.1Cash cycle 53.4 52.3 44.6 47.3 45.1 44.8 43.6 44.0

- 12 December 2012

13 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

Fugro Please note the disclaime r on the last page of this

Turbulent times, but fundamentals unchanged

In our view, the divestment of the majority of the Geoscience division to CGG

improves the business mix. We anticipate that Fugro’s remaining activities will

show robust organic growth in 2013E and beyond. The almost debt free balance

sheet will enable the company to continue with add-on acquisitions and we do

not rule out a modest extra cash pay-out to shareholders. Buy reiterated.

Source: Company data, Rabobank International Year to December, fully diluted

Recent news flow: change at the top and lowering of the FY outlook

In November, Fugro surprised the market with the announcement that CEO Mr. Steenbakker will

leave the company “because of a difference of opinion with respect to the vision regarding the

direction for the company”. Mr. Steenbakker will be replaced by Mr. Van Riel, a Fugro board

member with a strong track record and a background as entrepreneur. In addition, Fugro

lowered its FY net income guidance to EUR 280m (was at least EUR 310m). The new net income

outlook, adjusted for one-off elements, is at least EUR 26m below the former outlook provided

by Fugro. Important to note, the company stated that EUR 15-20m relates to lower utilization

rates for the marine seismic data acquisition vessels, which implies that only EUR 5-10m relates

to the core activities of Fugro (mainly the slow start of Subsea projects in Brazil, part of the

Survey division).

Several eminent triggers for the share price

In our view, there are at least five triggers for the share price: 1) The final close of the divestment

of the majority of the Geoscience division to CGG for EUR 1.2bn. We anticipate more news

before February, 2) Healthy growth of the remaining activities within Fugro. We anticipate an

improvement of the Subsea activities (ROV’s) based on the many tree awards in 2012. Looking to

the past, teh ROV market improves with a time lag of 6-18 months on the actual tree award3)

Solid revenues from the multi-client seismic data library. Many investors are still questioning the

quality of the data library. Fugro indicated that the total book value will be approximately EUR

500m end 2012. 4) Add-on acquisitions. In the past, Fugro added on average 5% to revenues per

annum, and finally 5) We do not completely rule out that Fugro will increase the pay-out to

investors. The company is almost debt free by the end of 2013E, which implies that there is room

to change the dividend policy towards cash only, increase the dividend payout or buy back

shares. We anticipate more news at the publication of the FY results or in August 2013.

Analysts

Michel Aupers

+31 (0)30 712 4462

Micha Tiekink

+31 (0)30 712 4475

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

Fugro

*Rating:B uy (unchanged) *Price as of 10 December 2 012 : EUR 46.3 7 (+1.11% )

*Price target: EUR 60.00 (unchanged) *EPS 2 012 E: EUR 3 .68 (unchanged)

Forecast 2011 2012E 2013E 2014E

Sales (EURm) 2,578 2,904 2,852 3,015

EBITDA (EUR m) 581 677 710 781

EBIT before exceptionals (EUR m) 349 418 480 536

Recurring net income (EUR m) 298 297 336 382

EPS Recurring New (EUR) 3.78 3.68 4.10 4.67

EPS Recurring Old (EUR) 3.78 3.68 4.10 4.67

P/E 13.4 12.6 11.3 9.9

EV/EBITDA 9.1 6.3 6.1 5.2

FCF Yield (%) -2.0 18.1 11.6 11.2

Dividend Yield (%) 3.2 3.2 3.5 3.9

Rating Buy =

Price target (12m) EUR 60.00 =

Price 10-Dec-2012 EUR 46.37

Up-/downside 29.4%

Energy Equipment & Services

Netherlands

Market capitalisation

EUR 3,774m

Avg (3month) daily turnover

555,103

Reuters

FUGRc.AS

Bloomberg

FUR NA

Web site

www.fugro.nl

Share Performance

1m 3m 12m

Fugro -10.8 -7.0 8.2

AEX 3.3 2.2 12.6

Agenda

08 March FY 2012 results

- 12 December 2012

14 | Rabobank International – GFM Equity Research

Valuation: FCF yield of 10% in 2013E and beyond

In our view, the valuation of Fugro is very attractive. Looking to price earnings and EV/EBITDA multiples, the

shares are trading slightly below the valuation of many good quality European mid- and small caps and clearly

below the valuation of oil services peers (however, there is not a peer with a comparable activity mix). However,

we conclude that the underlying quality of the assets is clearly above average (see the investment case below).

We conservatively forecast the FCF from the MC data library at EUR 100m per annum for the 2013-2017 period

and estimate the net income generated by the core-activities of Fugro at EUR 280m in 2013E, which implies a FCF

yield above 10%. In addition, we anticipate that there is some room for working capital improvement. However,

at this moment we do not take this into account.

Dependency on economic developments is relatively low

Approximately 75% of Fugro’s activities are related to the oil and gas industry, which implies that global E&P

spend is the main driver for revenue and margin growth. Fugro is generating approximately 25% of revenues

onshore, which is somewhat under pressure due to the budget constraints of governments. However, we

observe that large and complicated infrastructure projects are seen as investments in the future. In addition,

Fugro is good positioned in regions which continue to grow and onshore the company is also active for private

clients which continue to invest.

Investment case: Buy, price target EUR 60

The annual depletion rate of oil reserves is 6-8% and global demand continues to increase by 1.5% We anticipate

that the demand for deep water services (20-25% of Fugro’s total group revenues) is growing even faster. Fugro is

excellently positioned to benefit from the structural growth trend towards deep water oil explorations.

Furthermore, Fugro is a consultant, which implies that its operational risk is much lower than most other oil

services companies. The company is a global market leader in Geotechnical (80% global market share) and Survey

(50% global market share) and Seabed Geophysics (40% global market share, in joint venture with CGG which has

a 40% stake in these activities) In our view, the operational leverage within Fugro is high: we anticipate that an

improved fleet/ROV utilisation will be followed by a more attractive pricing environment. In our view, the outlook

is bright. In addition, Fugro will continue to strengthen its market position by add-on acquisitions (historically

adding on average 5% to group revenues per annum) and we do not rule out that the company will decide to

increase the cash pay out to shareholders. We decided to add Fugro to our conviction buy list, because we

believe that the recent decline of the share price (after the CEO change and lowering of the FY net income

guidance) is overdone. We reiterate our price target at EUR 60.

- 12 December 2012

15 | Rabobank International – GFM Equity Research

Financial Information

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EIncome Statement (EUR mln)Revenues 1,803 2,154 2,053 2,280 2,578 2,904 2,852 3,015Cost of sales 1,363 1,619 1,502 1,719 1,997 2,228 2,141 2,234Gross profit 0 0 0 0 0 0 0 0Operating costs 0 0 0 0 0 0 0 0EBITDA 440 536 551 561 581 677 710 781Depreciation -108 -140 -174 -201 -221 -248 -220 -235EBITA (before exceptionals) 332 395 378 360 360 429 490 546Exceptional items 0 0 0 0 0 0 0 0Amortisation of goodwill & other ITA -7 -9 -10 -8 -11 -11 -10 -10EBIT 325 386 367 351 349 418 480 536Net financial result -35 -7 -28 -22 -43 -57 -49 -43Other pre-tax items 4 5 7 28 29 1 9 11EBT 294 384 347 358 336 362 440 504Income taxes -71 -95 -74 -79 -45 -72 -88 -100Minority interests -6 -6 -10 -8 -8 -8 -30 -35Other post-tax items / participation -0 -0 0 1 5 4 4 4Extraordinary Items & Discontinued Operations 0 0 0 0 0 296 0 0Net income 216 283 263 272 288 582 326 373Extraordinary Items & Amortisation 7 9 10 8 11 -285 10 10Net income recurring (cash) 223 292 274 280 298 297 336 382Balance Sheet (EUR mln)Cash & Cash equivalents 72 113 108 81 170 876 1,082 1,286Current assets 595 668 672 1,052 1,310 1,575 1,394 1,468Tangible fixed assets 599 859 1,043 1,291 1,483 1,190 1,202 1,232Goodwill 408 452 493 576 782 700 690 681Other Intangible assets 0 0 0 0 0 0 0 0Other non-current assets 26 31 51 89 116 69 69 69Total Assets 1,700 2,123 2,366 3,090 3,862 4,410 4,437 4,735

Short-term debt 85 221 193 324 248 150 150 150Current liabs 412 505 453 571 622 669 588 722Long-term debt 450 395 441 591 1,215 1,215 1,050 900Other non-current liabs 47 66 79 81 103 103 102 103Minority interest 7 7 12 15 18 22 35 51Total equity 700 928 1,188 1,508 1,656 2,252 2,512 2,810Total liabs & equity 1,700 2,123 2,366 3,090 3,862 4,410 4,437 4,735

Net debt 463 503 527 833 1,292 489 118 -236Invested capital 1,410 1,703 2,000 2,609 3,223 3,078 2,989 2,960Invested capital excl. hitorical goodwill 784 1,023 1,269 1,787 2,184 2,110 2,022 1,992Off balance lease liabilities 0 0 0 0 0 0 0 0Net pension assets -30 -52 -73 -76 -98 -98 -98 -98Cash Flow Statement (EUR mln)Operating income 325 386 367 351 349 418 480 536Depreciation & Amortisation 115 149 184 210 232 259 230 245Other non-cash Items 0 0 0 22 -5 0 0 0Change in Working Capital -6 70 -46 -244 -286 -219 101 60Change in Provisions -6 19 13 2 4 0 -1 1Cash taxes -71 -89 -92 -98 -72 -72 -88 -100Cash interest -24 -31 -14 -17 -25 -57 -40 -32Cash impact associates & minorities 6 6 10 9 8 12 34 39Other cash expectionals / cash flow assets held for sale 0 0 0 0 0 296 0 0Operating cash flow 329 499 413 231 192 625 669 694

CAPEX -338 -406 -315 -335 -266 46 -232 -265Acquisitions & Disposals 0 0 0 0 -203 0 0 0Other Investments -43 -58 -71 -131 -35 119 0 0Cash Flow from Investments -381 -464 -385 -465 -504 165 -232 -265

Cash dividend -23 -40 -58 -62 -64 -60 -131 -150Change in Equity -23 -67 -2 -10 -80 73 66 75Change in Bank Debt 93 82 18 280 548 -98 -165 -150Other adjustments 6 7 9 0 -2 0 0 0Cash Flow from Financing 52 6 -33 208 401 -84 -231 -225FX effect 0 0 0 0 0 0 0 0Change in Cash 1 41 -5 -26 89 706 206 204

Free Cash Flow -8 94 98 -104 -74 671 437 428

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

16 | Rabobank International – GFM Equity Research

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EPer share itemsShares outstanding (avg. mln) 69.6 73.0 76.2 78.4 79.2 80.0 81.4 82.6Shares outstanding fully diluted (avg. mln) N/A N/A N/A N/A N/A N/A N/A N/AShare price (average) 46.2 43.6 31.0 47.0 50.5 46.4 46.4 46.4

EPS reported 3.11 3.88 3.46 3.47 3.63 7.28 4.00 4.52EPS recurring 3.17 3.82 3.55 3.59 3.78 3.68 4.10 4.67FCF per share -0.12 1.28 1.29 -1.32 -0.94 8.39 5.37 5.19Book value per share 10.06 12.71 15.58 19.23 20.91 28.15 30.87 34.03Dividend per share 1.25 1.50 1.50 1.50 1.50 1.50 1.60 1.80% GrowthRevenues 25.7 19.5 -4.7 11.1 13.1 12.7 -1.8 5.7Organic revenue growth 22.9 23.4 -5.6 6.0 7.6 9.1 -15.8 5.7EBITA 52.4 19.1 -4.5 -4.7 0.1 19.2 14.2 11.3Organic EBITA growth 0 0 0 0 0 0 0 0Net income recurring 51.7 31.0 -6.5 2.5 6.4 -0.3 13.0 13.9Dividend per share 50.6 20.0 0 0 0.0 -0.0 6.8 12.3Margins & returnsGross margin 0 0 0 0 0 0 0 0EBITDA margin 24.4 24.9 26.8 24.6 22.5 23.3 24.9 25.9EBITA margin (before exceptionals) 18.0 17.9 17.9 15.4 13.5 14.4 16.8 17.8Net recurring margin 12.4 13.6 13.3 12.3 11.6 10.2 11.8 12.7

ROE 30.9 30.5 22.2 18.0 17.4 25.9 13.0 13.3ROIC 19.2 18.8 15.7 12.0 10.4 10.7 12.7 14.5ROIC excl. historical goodwill 36.0 32.5 25.4 18.1 15.3 15.7 18.7 21.5EVA spread (ROIC - WACC) 10.9 10.5 7.4 3.7 2.1 2.4 4.4 6.2ValuationEnterprise Value (mln) 3,681.6 3,777.2 2,972.0 4,567.1 5,290.3 4,233.9 4,362.1 4,064.2

P/E recurring (x) 14.6 11.4 8.7 13.1 13.4 12.6 11.3 9.9P/FCF (x) -385.3 34.0 24.1 -35.5 -53.9 5.5 8.6 8.9P/B (x) 5.4 4.1 3.2 2.5 2.3 1.7 1.5 1.3Dividend yield (%) 2.7 3.2 3.2 3.2 3.2 3.2 3.5 3.9Free Cash Flow Yield (%) -0.3 2.8 2.8 -2.9 -2.0 18.1 11.6 11.2

EV/Sales (x) 2.0 1.8 1.4 2.0 2.1 1.5 1.5 1.3EV/EBITDA (x) 8.4 7.1 5.4 8.1 9.1 6.3 6.1 5.2EV/EBITA (x) 11.3 9.8 8.1 13.0 15.1 10.1 9.1 7.6EV/Invested capital 2.9 2.4 1.6 2.0 1.8 1.3 1.4 1.4EV/FCF (x) -440.7 40.4 30.3 -44.0 -71.3 6.3 10.0 9.5Leverage & ratiosNet debt/EBITDA 1.1 0.9 1.0 1.5 2.2 0.7 0.2 -0.3Interest cover 12.6 79.7 20.0 25.4 13.7 11.9 14.5 18.1Solvency (Equity / Total assets) 41.2 43.7 50.2 48.8 42.9 51.1 56.6 59.3Working capital as % of revenues 10.2 7.6 11.0 21.7 27.2 31.7 28.8 25.2CAPEX/revenues -18.7 -18.8 -15.3 -14.7 -10.3 1.6 -8.1 -8.8Dividend pay-out ratio (%) 40.2 38.7 43.4 43.2 41.3 20.6 40.0 39.8

Inventory period days 9.3 7.2 10.8 24.0 41.3 56.0 59.8 43.9Trade debtor days 84.5 66.4 88.3 110.1 119.5 117.4 122.5 121.8Trade creditor days 18.9 16.7 39.9 66.0 69.9 67.0 66.6 65.8Cash cycle 74.9 56.9 59.3 68.1 91.0 106.4 115.7 99.9

- 12 December 2012

17 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

ING Group Please note the disclaime r on the last page of this

Positive newsflow to continue

The last few months there has been quite some positive newsflow from ING

Group, and we expect this to continue the next few months. At a PE of 6x and a

moderate risk profile the company is attractively valued. Economic conditions

have some impact on the stock, but ING reduced its PIIGS exposure clearly. The

restructuring might not take as long as the market expects. Buy.

Source: Company data, Rabobank International Year to December, fully diluted

Recent news flow was all positive

11 Oct: ING announced the sale of its Malaysia business for EUR 1.3bn;

19 Oct: ING announced the sale of its Hong Kong, Macau, Thailand business for EUR 1.64bn;

19 Nov: ING reached agreement on an amended EC restructuring plan which prevents that

ING has to sell Westland Utrecht bank and gives it more time for the insurance divestments;

26 Nov: ING paid back EUR 1,125m to the Dutch state, being EUR 750m + 50% penalty.

Many positive triggers for the share price to come

Going forward we expect the following items to be positive for the share price:

Divestment of the South Korean life insurance business for about EUR 1.6bn;

Possible other divestments like the Eastern European Insurance business and maybe the in

the press rumourd Turkey banking business (both are our view, and are not based on ING’s

statements);

Continuing good earnings figures, mostly driven by the bank operations;

Upstreaming of the cash flow and divestment proceeds will clearly reduce the remaining

EUR 7bn holding debt increasing the chance for a spin off, and increasing transparency;

Starting of the US Insurance IPO process in 13Q1 to be executed in 13Q2.

Valuation attractive at PE of 6

ING Group’s valuation is actually not so difficult as by end 2013 the current excess capital +

retained profits + divestment proceeds are estimated to be enough to fully redeem the holding

debt and government capital. So the remaining business is the bank plus the Dutch insurer

which generate an EPS14 of EUR 1.15 which is a PE of 6.3x for a company which is for 90% a bank

and 10% a Dutch insurer. This is quite attractively valued. Maybe the growth of the business is

not so high as other financials, but a bank in the more stable Benelux market with 80% of the

revenues from the understandable net interest income is also attractive in this respect.

Analysts

Cor Kluis

+31 (0)30 712 4467

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

IN G Group

*Rating:B uy (unchanged) *Price as of 06 December 2 012 : EUR 7.19 (+0.8 4% )

*Price target: EUR 9.5 0 (unchanged) *EPS 2 012 E: EUR 0.92 (unchanged)

Forecast 2011 2012E 2013E 2014E

Net income (EURm) 3,796.2 3,464.1 4,614.6 4,921.2

EPS Reported New 1.00 0.92 1.22 1.30

EPS Reported Old 1.00 0.92 1.22 1.30

Dividend per share 0 0 0 0.20

Book value per share 10.13 10.06 11.28 12.38

P/E 7.2 7.9 5.9 5.5

P/B 0.7 0.7 0.6 0.6

Dividend Yield (%) 0 0 0 2.8

Rating Buy =

Price target (12m) EUR 9.50 =

Price 06-Dec-2012 EUR 7.19

Up-/downside 32.2%

Diversified Financials

Netherlands

Market capitalisation

EUR 27,532m

Avg (3month) daily turnover

20,262,386

Reuters

ING.AS

Bloomberg

INGA NA

Web site

www.ing.com

Share Performance

1m 3m 12m

ING Group 4.5 12.6 14.1

AEX 1.2 1.4 12.0

Stoxx 600 Insurance 3.7 8.0 26.9

Agenda

None --

- 12 December 2012

18 | Rabobank International – GFM Equity Research

Dependency on economic developments

As being mostly a Benelux bank the economic conditions in the Benelux are important for ING Group.

Although also in the Benelux there is an impact of the European austerity measures, the conditions in the

Benelux are better than in most of Europe.

The Euro developments are important for ING Group as it has some banking activities in Southern Europe

(ING Direct Spain and Italy). ING has been actively reducing their net funding exposure towards Spain to EUR

11bn end October (from EUR 22bn end 2011) and we expect this to decline to EUR 5bn end 2013. The net

funding exposure of ING Italy was EUR 7bn end 12Q3.

The general economic and capital market sentiment has some influence on the prices ING can receive for

exiting the insurance operations. However, this is mitigated as ING has extra time to do the divestments

under the adjusted European Commission agreeement.

Wild card: the restructuring does not have to take many years

The market has been expecting that ING remains a restructuring story for quite a few years because the European

Commission has given ING Group more time for the insurance divestments. However, we believe that if market

conditions enable it, that ING will still finish the restructuring as soon as possible. The extra time improves the

negotiation position of ING Group, as it does not have to make the divestments deals if the price and terms are

not satisfactory.

- 12 December 2012

19 | Rabobank International – GFM Equity Research

Financial Information

Source: Company data, Rabobank International

05 06 07 08 09 10 11 12E 13E 14E 15E

ING Insurance

Life 2,647 3,509 5,009 -1,691 -670 -948 -34 357 1,237 1,321 1,409

Non-life 1,331 1,377 1,144 470 266 244 171 45 185 192 199

Combined ratio 94.6% 90.4% 97.1% 96.5% 101.5% 100.5% 100.5% 99.5% 99.5% 99.5% 99.5%

Asset management 169 212 207 219 229 239

Profit before tax insurance 3,978 4,886 6,152 -1,221 -404 -535 349 609 1,641 1,741 1,846

ING Bank

Interest 9,162 9,334 9,063 11,084 12,539 13,420 13,491 12,022 11,627 12,151 12,573

(% of average RWAs) 3.1% 2.9% 2.6% 3.0% 3.7% 4.1% 4.1% 3.9% 4.0% 4.0% 4.0%

Commission 2,401 2,675 2,927 2,896 2,678 2,628 2,484 2,164 2,238 2,337 2,439

Other revenues 2,285 2,191 2,627 -2,249 -1,904 1,281 219 921 1,316 1,112 1,113

Total income 13,848 14,200 14,617 11,731 13,313 17,329 16,194 15,107 15,181 15,600 16,125

Total costs 8,844 9,063 9,521 10,003 10,134 9,712 9,668 8,715 8,709 8,883 9,218

Gross profit 5,004 5,137 5,096 1,728 3,179 7,617 6,526 6,393 6,472 6,716 6,907

Addition to loan loss provision 88 103 125 1,280 2,972 1,751 1,670 2,072 1,394 1,298 1,334

Profit before tax 4,916 5,034 4,971 448 207 5,866 4,856 4,321 5,077 5,418 5,572

ING Group

Commercial Banking (excl. real estate) 2,028 1,856 1,736 907 2,083 2,379 2,048 1,909 2,472 2,482 2,485

Real estate 631 664 -297 -1,388 -40 66 0 0 0 0

Retail Banking 1,815 1,932 2,062 1,688 1,536 2,177 1,967 1,967 2,252 2,390 2,476

ING Direct 617 717 531 -1,123 -666 1,450 999 493 583 788 854

Other banking 107 -102 -22 -727 -1,358 -99 -223 -48 -230 -242 -242

Insurance Europe 2,021 2,328 1,882 650 649 1,029 541 257 1,108 1,150 1,194

Insurance Americas 1,986 1,992 2,058 -517 68 -1,145 -574 408 786 833 883

Insurance Asia/Pacific 452 609 575 116 245 519 588 250 0 0 0

Asset management 0 0 0 0 0 169 212 207 219 229 239

Other insurance -481 -53 1,637 -1,471 -1,378 -1,107 -417 -513 -472 -471 -470

Group pre-tax profit 8,545 9,910 11,123 -774 -209 5,332 5,207 4,929 6,719 7,159 7,419

ING Group

ING Insurance 3,978 4,886 6,152 -1,221 -404 -535 349 609 1,641 1,741 1,846

ING Bank 4,916 5,034 4,971 448 207 5,866 4,856 4,321 5,077 5,418 5,572

Profit before tax 8,894 9,920 11,123 -773 -197 5,331 5,205 4,929 6,719 7,159 7,419

Taxation -1,930 -2,193 -2,268 577 149 -1,355 -1,329 -1,349 -2,016 -2,144 -2,218

Third-party interests -305 -341 -267 37 119 -100 -82 -116 -88 -94 -97

Dividend on core tier 1 capital + yield on this cash -425

Operational net profit (from 2005 net profit) 6,659 7,386 8,588 -159 -355 3,876 3,794 3,464 4,615 4,921 5,104

Insurance cleaning

-/- insurance equity capital gains/losses 532 761 2,714 -558 -331 164 110 159 100 100 100

-/- insurance real estate capital gains/losses 217 286 156 -315 -337 -38 -12 -48 86 87 88

-/- Capital gains fixed income (insurance) 98 -7 -33 0 0 163 165 73 93 95 95

-/- Release provisions insurance 69 131 67 32 0 123 -91 -20 0 0 0

-/- Derivatives that do not qualify for hedge accounting 23 44 -83 -338 53 199 25 -606 0 0 0

-/- Estimated one time tax effect 400 115 50 0 0 40 135 172 0 0 0

DAC write offs (25% tax) 0 9 0 767 475 1,223 1,069 -83 0 0 0

Minimum guarantees (27% tax) (insurance) 0 0 0 58 -8 347 0 0 0 0 0

Bond defaults (27% tax) 1 8 49 750 358 477 830 44 180 185 190

Extra provision/charges in insurance 20 44 58 0 225 37 -36 169 0 0 0

Bank cleaning

-/- Capital gains fixed income (bank) 40 65 57 -1,680 -1,072 -6 -501 -204 0 50 60

-/- Capital gains equities (bank) 113 119 292 -264 -25 113 35 15 62 62 62

-/- Revaluations real estate (bank) 42 47 66 -491 -506 -72 -34 -18 0 0 80

-/- Derivatives that do not qualify for hedge accounting 96 53 4 -156 0 4 92 -302 0 0 0

-/- Release of provision 0 46 0 0 0 0 0 25 0 0 0

-/- Estimated one time tax effect 173 30 90 0 26 0 0 0 0 0 0

Cost provision bank 135 144 67 -16 628 21 32 0 0 0 0

Cleaned net group profit 4,631 5,942 5,381 5,169 3,505 5,100 5,764 4,025 4,453 4,713 4,811

Tax rate 21.7% 22.1% 20.4% 74.6% 75.3% 25.4% 25.5% 27.4% 30.0% 29.9% 29.9%

Average number of shares (m) 3,071 3,048 3,030 2,905 3,095 3,784 3,784 3,785 3,785 3,785 3,785

EPS (EUR) 2.17 2.42 2.83 -0.05 -0.11 1.02 1.00 0.92 1.22 1.30 1.35

Dividend per share 0.83 0.93 1.05 0.52 0.00 0.00 0.00 0.00 0.00 0.20 0.30

RWA Bank 319,653 314,286 387,206 343,387 332,374 321,101 330,420 283,878 297,425 309,500 322,923

Value adj. To receivables / avg RWA 0.03% 0.03% 0.04% 0.35% 0.88% 0.54% 0.51% 0.67% 0.48% 0.43% 0.42%

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

20 | Rabobank International – GFM Equity Research

Source: Company data, Rabobank International

Valuation of ING Group (estimated after exiting the insurance business) (EUR m)

base case fair

value

15% discount

on insurance

fair value

30% discount

on insurance

fair value

Net profit ING bank 2014E 3,641 3,641 3,641

-/- Est. net profit effect of Westland Utrecht divestment -30 -30 -30

+/+ Est. net profit effect of redemption of holding leverage (est 3% interest cost) 169 169 169

Net profit of the new recurring ING bank 2014E 3,780 3,780 3,780

+/+ Net profit of Dutch insurance activities 657 559 460

Net profit new ING after transactions 2014E 4,437 4,339 4,240

Number of shares (m) 3 ,784 3,784 3,784

EPS 2014E (EUR) 1.17 1.15 1.12

Share price (EUR) 7.22 7.22 7.22

PE 2014 6.2 6.3 6.4

- 12 December 2012

21 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

Reed Elsevier Please note the disclaime r on the last page of this

Risk on the upside

Reed Elsevier is a Conviction Buy as we continue to see room for small EPS

upgrades due to (1) Growth acceleration for the Risk Solutions business; (2)

Additional share buy backs; (3) Balance sheet refinancing benefits; (4)

Continuing operational improvements. We also believe that the open access

threat is clearly manageable for the Science & Technology unit.

Source: Company data, Rabobank International Year to December, fully diluted

50bpos lower interest rate benefit

The refinancing of the balance sheet through redeeming the expensive Choicepoint debt (8.0-

8.5% rates) and issuing new debt at much lower rates (2.8%!) will bring the blended interest

percentage down with 50bps in 2013. Reed Elsevier’s gross debt stood at EUR 4.8bn at 30 June

2012, so this could lead to EUR 20-25m lower interest charges in 2013.

Room for even more cash returns in 2013

Due to higher disposal proceeds as a result of the Variety transaction and some other small

disposals, Reed raised the amount of share buy backs in 2012 towards EUR 310m, up from EUR

193m previously. Given the de-leveraging of the balance sheet, the highly FCF generative

character of the business and the focus on organic growth, we expect to see a more positive

stance towards share buy-backs out of the FCF in the next 6-12 months. At the interims leverage

stood at 2.3x on a pension and lease adjusted basis. We believe there is potential room for a EUR

500m SBB program in 2013.

Acceleration Risk business is a key positive

As expected Reed Elsevier reaffirmed the 2012FY forecasts. A key positive was that the high-

margin Risk business accelerated in terms of growth from 5% in 12H1 towards 7% in 12Q3 (Rabo

12Q3 estimate: 5%). Organic growth trends for Legal (+ 1%), STM (+ 2%) and Reed Exhibitions (+

7%) were in line with our expectations.

Analysts

Hans Slob

+31 (0)30 712 4472

Philip Scholte

+31 (0)30 712 4471

Rabobank International GFM

Equity Sales

Equity Sales Trading

+ 31 30 216 9101

+31 30 216 9123

www.rabotransact.com

Reed Elsevier

*Rating:B uy (unchanged) *Price as of 05 December 2 012 : EUR 11.3 0 (+0.53% )

*Price target: EUR 12 .00 (unchanged) *EPS 2 012 E: EUR 0.95 (unchanged)

Forecast 2011 2012E 2013E 2014E

Sales (EURm) 6,902 7,509 7,633 7,950

EBITDA (EUR m) 2,108 2,359 2,487 2,643

EBIT before exceptionals (EUR m) 1,457 1,683 1,768 1,873

Recurring net income (EUR m) 1,219 1,387 1,477 1,568

EPS Recurring New (EUR) 0.83 0.95 1.01 1.07

EPS Recurring Old (EUR) 0.83 0.95 1.01 1.07

P/E 10.7 11.8 11.2 10.5

EV/EBITDA 8.1 8.0 7.7 7.1

FCF Yield (%) 8.0 6.9 8.5 9.8

Dividend Yield (%) 3.9 4.3 4.5 4.7

Rating Buy =

Price target (12m) EUR 12.00 =

Price 05-Dec-2012 EUR 11.30

Up-/downside 6.2%

Media

Netherlands

Market capitalisation

EUR 8,193m

Avg (3month) daily turnover

2,166,412

Reuters

ELSN.AS

Bloomberg

REN NA

Web site

www.reed-elsevier.com

Share Performance

1m 3m 12m

Reed Elsevier 7.3 6.1 29.8

AEX 1.1 3.0 11.1

Agenda

None --

- 12 December 2012

22 | Rabobank International – GFM Equity Research

Steady growth for Science & Technology

RBI continued to grow 1% in 12Q3 (Rabo estimate: - 1%) in spite of weakness for US construction related data

services and weakening print advertising trends (13% of RBI sales). With the fast growing Accuity business

becoming part of organic growth from 2013 onwards, the RBI growth profile will further shift towards fast

growing data services and analytics.

In spite of the open access threat, Science & Technology continued to show healthy 5% organic sales growth in

12Q3. Double digit growth for usage and article submissions continued. Health Sciences remained a flat liner, as

growth for medical research and e-tools was offset by lower medical print book sales and a decrease for the

pharma promotional business. Due to the reorganized management structure with Ron Mobed now also

responsible for Health, we hope to see a sale of the pharma promotional business in order to improve the growth

and margin profile of Health.

In a flat market, Legal continued to grow 1% in 12Q3. We estimate that the North American business grew 1-2%

organically, with Europe being flat to slightly down. This is a major outperformance when compared to Wolters

Kluwer, which saw its sales falling 7-8% in 12Q3 for Legal & Regulatory Europe.

The LexisNexis Legal & Professional CMD in London confirmed our view that that organic growth and margins

will recover slowly and that capital expenditure has peaked for this division (27% of sales; 14% of EBITA).

Management expects to see recovery of the business in line with GDP growth, but was not willing to make any

statements about whether it expects to be able to gain share after the massive investment program in recent

years. Growth is gradually returning back to the business. After 5% and 2% organic sales declines in 2009/2010,

the business returned to 1% growth in 2011 and 12H1. Some 60% of the business is now coming from Legal

Digital Solutions which is growing low to mid-single digits. The other 40% of the business (print information;

news & business; directory listings) is declining low to mid-single digits. After a period of underinvestment in the

2007/2008 period, capital expenditure has been ramped up from 4% of sales in 2008 towards 12% of sales in

2011. It has now peaked and it is expected to level off in the medium term towards high single digits as

percentage of sales.

As we expected organic growth (ex biennial cycling) for Reed Exhibitions decelerated from 8% in 12H1 towards

6% in 12Q3. Growth in Europe (48% of sales) is slowing down mainly due to increasing weakness in France lately,

which is the largest single country in Europe. Double-digit growth outside the US and Europe continued.

Compelling 8.5% FCF yield

The 8.5% FCF yield remains compelling. Quick de-leveraging of the balance sheet resulting from strong FCF

generation and subdued acquisition activity create ample room for additional cash return in 2013/2014 on top of

the solid dividend (4.5% yield).

- 12 December 2012

23 | Rabobank International – GFM Equity Research

Financial Information

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EIncome Statement (EUR mln)Revenues 6,694 6,721 6,800 7,084 6,902 7,509 7,633 7,950Cost of sales N/A N/A N/A N/A N/A N/A N/A N/AGross profit N/A N/A N/A N/A N/A N/A N/A N/AOperating costs N/A N/A N/A N/A N/A N/A N/A N/AEBITDA 1,876 1,948 2,008 2,096 2,108 2,359 2,487 2,643Depreciation -216 -211 -250 -277 -238 -263 -305 -358EBITA (before exceptionals) 1,660 1,737 1,758 1,819 1,870 2,096 2,181 2,286Exceptional items 0 0 0 0 0 0 0 0Amortisation of goodwill & other ITA -378 -412 -610 -408 -413 -413 -413 -413EBIT 1,282 1,325 1,148 1,411 1,457 1,683 1,768 1,873Net financial result -203 -219 -326 -326 -270 -264 -229 -212Other pre-tax items 0 0 0 0 0 0 0 0EBT 1,079 1,106 822 1,085 1,187 1,420 1,540 1,661Income taxes -344 -355 -328 -339 -373 -440 -469 -498Minority interests -4 -5 -4 -7 -8 -6 -7 -8Other post-tax items / participation 267 0 0 0 0 0 0 0Extraordinary Items & Discontinued Operations 0 -153 -53 19 68 0 0 0Net income 998 593 437 758 874 974 1,064 1,155Extraordinary Items & Amortisation 428 565 663 389 345 413 413 413Net income recurring (cash) 1,426 1,158 1,100 1,147 1,219 1,387 1,477 1,568Balance Sheet (EUR mln)Cash & Cash equivalents 3,355 386 822 868 871 1,928 2,256 2,712Current assets 1,929 2,094 2,058 2,149 2,187 2,294 2,332 2,429Tangible fixed assets 325 339 327 341 346 519 633 673Goodwill 6,189 9,584 8,928 9,241 9,867 9,454 9,041 8,628Other Intangible assets 0 0 0 0 0 0 0 0Other non-current assets 1,059 848 559 456 533 533 533 533Total Assets 12,857 13,251 12,694 13,055 13,804 14,728 14,795 14,975

Short-term debt 1,533 461 759 604 1,178 1,178 1,178 1,178Current liabs 4,672 5,475 4,993 5,350 5,614 5,620 5,689 5,864Long-term debt 2,723 5,865 4,511 4,430 3,960 3,960 3,960 3,960Other non-current liabs 209 425 446 366 395 401 403 408Minority interest 15 15 15 0 0 4 0 0Total equity 3,705 1,010 1,970 2,305 2,657 3,565 3,565 3,565Total liabs & equity 12,857 13,251 12,694 13,055 13,804 14,728 14,795 14,975

Net debt 901 5,940 4,448 4,166 4,267 3,210 2,882 2,426Invested capital 13,682 17,490 17,739 18,172 19,078 19,352 19,435 19,397Invested capital excl. hitorical goodwill -1,473 -1,472 -1,177 -1,465 -1,598 -1,324 -1,241 -1,279Off balance lease liabilities 0 0 0 0 0 0 0 0Net pension assets -181 -537 -386 -263 -290 -290 -290 -290Cash Flow Statement (EUR mln)Operating income 1,282 1,325 1,148 1,411 1,457 1,683 1,768 1,873Depreciation & Amortisation 594 623 860 685 651 676 718 771Other non-cash Items 0 0 0 0 0 0 0 0Change in Working Capital 1,295 13 -301 296 138 -101 31 78Change in Provisions -172 216 21 -80 29 6 2 5Cash taxes -344 -355 -328 -339 -373 -440 -469 -498Cash interest -203 -219 -326 -326 -270 -264 -229 -212Cash impact associates & minorities 271 5 4 7 8 6 7 8Other cash expectionals / cash flow assets held for sale 0 -153 -53 19 68 0 0 0Operating cash flow 2,398 2,075 876 1,636 1,788 1,561 1,822 2,016

CAPEX 212 217 271 364 403 436 420 398Acquisitions & Disposals -2,748 3,037 0 0 0 0 0 0Other Investments N/A N/A N/A 1,286 N/A N/A N/A N/ACash Flow from Investments -2,536 3,254 271 1,650 403 436 420 398

Cash dividend -700 -573 -550 -600 -640 -693 -739 -784Change in Equity -1,061 36 1,000 0 297 -310 0 0Change in Bank Debt -223 2,070 -1,056 -236 104 0 0 0Other adjustments -9 -5 -4 -22 -8 -3 -11 -8Cash Flow from Financing -1,993 1,528 -610 -858 -247 -1,006 -749 -791FX effect 0 0 0 0 0 0 0 1Change in Cash 1,458 -1,056 450 562 422 417 644 814

Free Cash Flow 1,828 1,963 873 1,382 1,319 1,126 1,402 1,619

|

R

a

b

o

b

a

n

k

I

n

t

e

r

n

a

t

i

o

n

a

l

–

E

q

u

i

t

y

R

e

s

e

a

r

c

h

- 12 December 2012

24 | Rabobank International – GFM Equity Research

Source: Rabobank International

Financial InformationFiscal year ends 12/2012 2007 2008 2009 2010 2011 2012E 2013E 2014EPer share itemsShares outstanding (avg. mln) 1,642.0 1,420.0 1,390.0 1,466.8 1,466.8 1,452.2 1,458.0 1,463.8Shares outstanding fully diluted (avg. mln) 1,642.0 1,420.0 1,390.0 1,466.8 1,466.8 1,452.2 1,458.0 1,463.8Share price (average) 13.5 11.0 8.2 9.1 8.9 11.3 11.3 11.3

EPS reported 0.61 0.42 0.31 0.52 0.60 0.67 0.73 0.79EPS recurring 0.88 0.87 0.79 0.78 0.83 0.95 1.01 1.07FCF per share 1.13 1.48 0.63 0.94 0.90 0.78 0.96 1.11Book value per share 2.29 0.76 1.42 1.57 1.81 2.45 2.45 2.44Dividend per share 0.43 0.40 0.40 0.41 0.44 0.49 0.51 0.54% GrowthRevenues -15.6 0.4 1.2 4.2 -2.6 8.8 1.7 4.1Organic revenue growth 5.8 4.0 -6.0 2.0 1.7 3.9 2.0 4.2EBITA -6.7 4.7 1.2 3.5 2.8 12.1 4.1 4.8Organic EBITA growth N/A N/A N/A N/A N/A N/A N/A N/ANet income recurring 16.9 -18.8 -5.0 4.3 6.3 13.8 6.5 6.2Dividend per share 3.3 -5.3 -1.9 3.4 6.7 11.7 3.9 5.7Margins & returnsGross margin N/A N/A N/A N/A N/A N/A N/A N/AEBITDA margin 28.0 29.0 29.5 29.6 30.5 31.4 32.6 33.3EBITA margin (before exceptionals) 19.1 19.7 16.9 19.9 21.1 22.4 23.2 23.6Net recurring margin 21.3 17.2 16.2 16.2 17.7 18.5 19.4 19.7

ROE 26.9 58.7 22.2 32.9 32.9 27.3 29.8 32.4ROIC 8.4 8.5 7.7 7.8 7.7 8.3 8.5 8.9ROIC excl. historical goodwill -165.5 -90.4 -102.4 -106.4 -93.6 -109.0 -129.3 -137.9EVA spread (ROIC - WACC) 0.3 0.5 -0.4 -0.2 -0.4 0.3 0.5 0.9ValuationEnterprise Value (mln) 22,054.6 19,886.1 16,105.9 17,267.0 17,049.7 18,985.1 19,050.6 18,660.8

P/E recurring (x) 15.3 12.6 10.3 11.6 10.7 11.8 11.2 10.5P/FCF (x) 12.0 7.4 13.0 9.7 9.9 14.6 11.8 10.2P/B (x) 2.2 8.1 4.2 3.6 3.1 2.3 2.3 2.3Dividend yield (%) 3.8 3.6 3.5 3.6 3.9 4.3 4.5 4.7Free Cash Flow Yield (%) 10.0 13.1 5.6 8.3 8.0 6.9 8.5 9.8

EV/Sales (x) 3.3 3.0 2.4 2.4 2.5 2.5 2.5 2.3EV/EBITDA (x) 11.8 10.2 8.0 8.2 8.1 8.0 7.7 7.1EV/EBITA (x) 17.2 15.0 14.0 12.2 11.7 11.3 10.8 10.0EV/Invested capital 1.5 1.3 0.9 1.0 0.9 1.0 1.0 1.0EV/FCF (x) 12.1 10.1 18.4 12.5 12.9 16.9 13.6 11.5Leverage & ratiosNet debt/EBITDA 0.5 3.0 2.2 2.0 2.0 1.4 1.2 0.9Interest cover 9.2 8.9 6.2 6.4 7.8 8.9 10.9 12.5Solvency (Equity / Total assets) 28.8 7.6 15.5 17.7 19.2 24.2 24.1 23.8Working capital as % of revenues -26.9 -26.9 -22.2 -25.5 -28.2 -24.5 -24.5 -24.5CAPEX/revenues 3.2 3.2 4.0 5.1 5.8 5.8 5.5 5.0Dividend pay-out ratio (%) 70.1 96.7 125.8 79.1 73.2 72.7 69.4 67.9

Inventory period days 35.7 19.7 17.9 14.8 13.1 11.4 11.7 11.5Trade debtor days 101.2 89.5 91.4 87.5 92.7 88.5 89.8 88.7Trade creditor days 151.5 150.0 150.8 149.2 164.2 159.8 163.3 161.3Cash cycle -14.6 -40.8 -41.5 -46.9 -58.5 -59.8 -61.8 -61.1

- 12 December 2012

25 | Rabobank International – GFM Equity Research

Wednesday 12 December 2012 Report

TomTom Please note the disclaime r on the last page of this

A sweet Apple?

Due to the problems of Apple with its mapping app, we see a 30% chance on a

take-out by Apple for EUR 9-10 per share. Just as Nokia acquired Navteq, we

believe Apple needs to go “all in” with mapping through acquiring TomTom.

Our stand alone value is EUR 4.20 per share. As we incorporate a 30% chance on

a take-out at EUR 9-10, we lift our SPT from EUR 4.20 EUR 5.80 (> 50% upside).

Source: Company data, Rabobank International Year to December, fully diluted

Apple might have to go “all in” with mapping

Just as Nokia acquired Navteq, Apple might have to go “all in” with mapping technology

through acquiring TomTom. Because of Apple’s major issues with its mapping app, we see an

increasing logic for a complete tie-up between Apple and TomTom.

Ten reasons for Apple to consider an acquisition of TomTom

We see ten reasons for Apple to consider an acquisition of TomTom: 1) Crowd-surfing

functionality (Mapshare). TomTom has the procedures and tools (MapShare) in place to make

map corrections faster than Apple can. 2) Apple has not enough mapping experts to solve its

issues quickly. 3) TomTom HD Traffic is an excellent differentiator to improve the map

functionality. 4) Apple can leverage TomTom POI database outside USA; 5) Apple could use IQ

routes, as Apple has limited historical traffic data. 6) Sharing of source codes to faster develop

apps and location based services; 7) Faster map updates; 8) Entry into leading carmakers; 9)

Apple needs the know-how of TomTom; 10) It’s a royal way out for the four TomTom founders.