1337161382 an overview of the pharmaceutical sector in bangladesh (may 2012)

TRANSCRIPT

Introduction

The pharmaceutical market in Bangladesh is pretty small compared to the

population size of the country, mainly because of the lack of spending power

of the population. Pharmaceutical spending is also amongst the lowest in the

world in per capita terms. Healthcare expenditures consist of only 3.35% of

GDP. However, increased awareness of healthcare, increase in per capita

income, emergence of private healthcare services and the government’s

increased expenditure in this sector, together with other factors, have caused

the demand to rise in recent years. The sector is also protected from external

competition as imports are completely restricted for similar drugs that are

manufactured locally. This sector reports provides an overview of the

pharmaceutical sector in Bangladesh and highlights the top performers that

are listed in the Dhaka Stock Exchange (DSE).

Pharmaceutical Sector in Bangladesh

Pharmaceutical sector is technologically the most developed manufacturing

industries in Bangladesh and the third largest industry in terms of contribution

to government’s revenue. The industry contributes about 1% of the total

GDP. There are about 250 licensed pharmaceutical manufacturers in the

country; however, currently a little over 100 companies are in operation. It is

highly concentrated as top 20 companies produce 85% of the revenue.

According to IMS, a US-based market research firm, the retail market size is

estimated to be around BDT 84 billion as on 2011.

Bangladesh pharmaceutical companied focus primarily on branded generic

final formulations, mostly using imported APIs (Active Pharmaceuticals

Ingredient). Branded generics are a category of drugs, including prescription

products, that are either novel dosage forms of off-patent products produced

by a manufacturer that is not the originator of the molecule, or a molecule

copy of an off-patent product with a trade name. About 85% of the drugs sold

in Bangladesh are generics and 15% are patented drugs - the structure

differs significantly from the international market. Branded generic drugs

represent about 25% on average of worldwide pharmaceuticals sales’;

however, given the popularity in emerging markets like China, India and Latin

America, branded generic drugs may well dominate the total sales within a

decade.

Bangladesh manufactures about 450 generic drugs for 5,300 registered

brands which have 8,300 different forms of dosages and strengths. These

include a wide range of products from anti-ulcerants, flouroquinolones, anti-

rheumatic non-steroid drugs, non-narcotic analgesics, antihistamines, and

oral anti-diabetic drugs. Some larger firms have also started producing anti-

cancer and anti-retroviral drugs. Domestic manufacturers account for 97% of

the drug sales in the local market while the remaining 3% are imported. This

is a complete turnaround over from two/three decades back when imports

There are about 250 licensed

pharmaceutical companies in

Bangladesh. The industry contributes

1% to the country's GDP and is the

third largest industry in terms of

contribution to government revenue

Analyst:

Khandakar Safwan Saad [email protected]

(880) 173 035 7779

An Overview of the Pharmaceutical Sector in Bangladesh May 2012

The market is dominated by branded

generics, accounting for 85% of the

total sales in the country

The market is almost self-sufficient in

meeting local demand as 97% of the

drugs are manufactured locally

Pharmaceutical Sector in Bangladesh May 2012

2

used to dominate the market. The imported drugs include essential live

saving drugs and other high quality drugs. The ratio will further increase in

favor of the local production as some of the big players are poised to

manufacture these high quality drugs in-house in the future.

Market Size and Growth

As stated earlier, the size of the retail market reached BDT 84.0 billion as on

2011 based on IMS report. The report further stated that, retail sales in the

domestic market achieved 23.6% growth in 2011 following 23.8% and 16.8%

growth in 2010 and 2009 respectively. High growth in the last three years

(78.8% cumulative and 21.4% CAGR) meant that the Bangladesh

Pharmaceutical market doubled in just over four years. The retail market also

crossed USD 1.0 billion in size in 2011. It is one of the fastest growing

sectors in the country with an annual average growth rate of 17.2% over the

last five years and 13.1% over the last decade.

However, considering that IMS does not include rural market in their survey,

the actual size of the market will vary slightly (5%-10%). It is estimated that

the retail market represent 90% of the total market; in that respect the total

market size (including the rural market) is expected to be over BDT 90.0

billion at present.

Drivers behind Market Growth

The table above shows some selected health indicators for Bangladesh. Most

of the indicators improved over the last decade which are among some of the

factors that contributed to the growth of the sector.

There has been a gradual demographic shift - life expectancy improved

from 64.7 in 2000 to 68.3 in 2009 which highlights the increased health

consciousness among the people. Also the income level of the

population increased over the last decade which allowed them to spend

more for healthcare.

The base was also low as healthcare expenditure was less than 3% of

GDP in 2000 with total pharmaceutical sector size of BDT 24.5 billion

only in that year.

Increased medical coverage of population with new hospitals.

Emergence of private healthcare service - a number of top class

hospitals started operating which includes Apollo Hospitals, Square

Hospitals, United Hospitals and others. These hospitals became very

Increased life expectancy, increased

medical coverage of population,

emergence of private healthcare

services, growing income base of

population and popularization of

wellness drug are some of the

factors contributing to high industry

growth in recent times

Retail market registered 21.4%

CAGR over the last three years,

17.2% over the last five years and

13.1% over the last decade

Health Indicators 2009 2008 2005 2000

Life Expectancy 68.3 68 66.9 64.7

Government % in total health exp. 31.7% 31.4% 34.9% 39.0%

Health exp. as % of GDP 3.35% 3.32% 3.21% 2.82%

GDP per Capita (Current US$) 607.8 546.9 428.8 363.6

Health exp. per capital (Current US$) 18.4 16.5 12.1 9.1

Median Age (2011 estimate) 23.3 - - -

Poverty Level 31.5% NA 40.0% 48.9%

Source: World Bank

Table 2: Selected Health Indicators for Bangladesh

Year Size (BDT b) Growth

2011 84.0 23.6%

2010 68.0 23.8%

2009 54.9 16.8%

2008 47.0 6.9%

2007 44.0 15.8%

2006 38.0 4.1%

2005 36.5 17.5%

2004 31.1 8.6%

2003 28.6 5.9%

2002 27.0 10.2%

2001 24.5

Source: Square Pharmaceuticals Annual Reports & IMS Report

Table 1: Retail Market Size & Growth

Pharmaceutical Sector in Bangladesh May 2012

3

popular with the mass population due to their quality service; they have

been a major factor contributing to increased healthcare expenditure.

Although government expenditure as a % of total healthcare expenditure

did not improve in the last decade, there has been increased expenditure

in in absolute terms. Growth in private expenditure was the primary

reason behind fall in public % of expenditure.

Income base of the population has been growing over the last decade.

Health expenditure per capita doubled in the last decade, indicating

people’s willingness to spend more to remain healthy.

Drivers for Future Growth

Table 4 compares the indicators with other regions of the world and shows

that Bangladesh is way behind other countries. Government spending

proportion is much lower than that in other regions - it is one possible area

where future growth may come from. Moreover, the total health expenditure

to GDP ratio and health expenditure per capita of Bangladesh (both of which

gradually increased from 2000) is very low in comparison to developed and

developing countries. Since the base is still very low, we expect the recent

growth in the local retail market to continue in the current decade. Some

other factors that will also boost the industry growth includes:

Increase in number of modern hospitals

Increase in level of service/treatment provided in the hospitals with

improved/more modern diagnostic equipments

General people are getting more health conscious

Growing income level of the people

Export of pharmaceutical products

Growth Projections

Table 3 shows the healthcare expenditure as % of GDP for neighboring

countries to Bangladesh as well as some other developed countries as well.

Bangladesh is way below in the list of countries with only Pakistan below in

terms of healthcare expenditure percentage. If we assume that Bangladesh is

going to achieve 6.5% real GDP growth rate over the next five years and

healthcare expenditure to reach 5% of GDP by that time, then healthcare

expenditure in nominal value will grow at 15.4% annually over the next five

years.

Health Indicators Bangladesh World

South

Asia EU USA

Life Expectancy 68.3 69.4 65 79.4 78.1

Government % in total health exp. 31.7% 60.8% 32.9% 76.1% 48.6%

Health exp. as % of GDP 3.35% 10.03% 3.99% 10.31% 16.21%

Health exp. per capital (Current US$) 18.4 863.6 40.2 3,370.7 7,410.2

Source: World Bank

Table 4: Comparison of health indicators (2009) with other regions

Region 2009 2005 2000

USA 16.21% 14.72% 13.41%

World 10.03% 9.73% 9.23%

UK 9.34% 8.25% 7.04%

Japan 8.35% 8.16% 7.69%

Afghanistan 7.36% 8.76% 8.29%

Nigeria 5.82% 6.60% 4.56%

Nepal 5.81% 5.91% 5.06%

Thailand 4.31% 3.55% 3.40%

India 4.17% 4.03% 4.61%

Sri Lanka 3.96% 4.04% 3.72%

Bangladesh 3.35% 3.21% 2.82%

Pakistan 2.62% 2.78% 3.02%

Source: World Bank

Table 3: Healthcare exp as % of GDP

Increase in government spending,

increase in number of modern

hospitals and increase in health

consciousness of the people are

some of the drivers for future growth

Pharmaceutical Sector in Bangladesh May 2012

4

Bangladesh has been achieving around 6% GDP growth rate over the last

decade. The current government has set target to achieve even higher

growth rate in this decade, with a vision to achieve double-digit growth within

2018. As such, it is likely that the actual growth in GDP in the next five years

will be greater than the projected 6.5% - in that case the growth in healthcare

expenditure is likely to be more than our simple estimated value of ~15%.

At present, the retail pharmaceutical market size is about 1% of GDP and

health expenditure is about 3.35% of GDP. Therefore, the pharmaceutical

sector revenue accounts for ~30% of the healthcare expenditure. If we

assume that the ratio will remain constant over the years, pharmaceutical

revenue will also grow at par - at 15.4% annually over the next five years.

Major Players

Based on the IMS report for the fourth quarter 2011, Square Pharmaceuticals

(DSE: SQURPHARMA) holds the top market share in the retail market -

18.7%, followed by Incepta Pharmaceuticals (INCEPTA) - 9.3%, Beximco

Pharmaceuticals (DSE: BXPHARMA) - 8.8%, Opsonin Pharma (OPSONIN) -

5.1% and Renata (DSE: RENATA) - 4.9%. The top five companies held

46.8% market share in 2011, slightly more than their 46.2% market holding in

2010 - indicating cumulative revenue growth in excess of the sector growth.

Among the top five, three are listed in DSE – Square, Beximco and Renata.

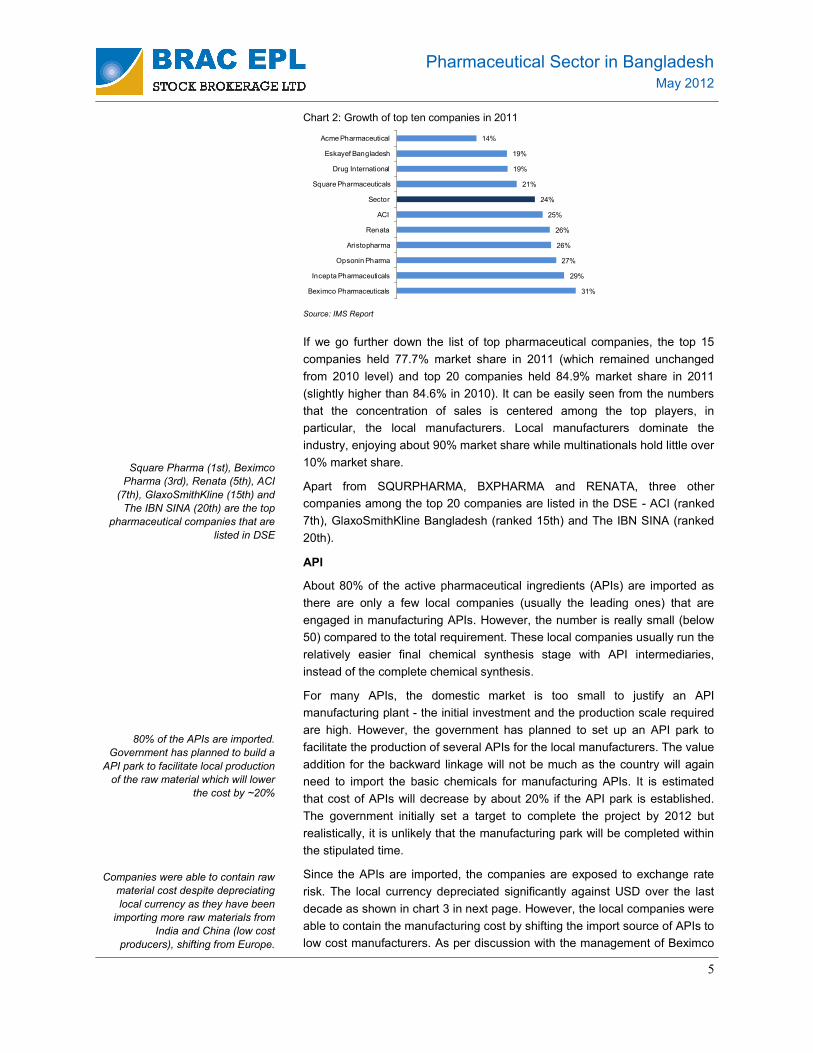

Top 10 companies held 67.7% of the market in 2011 as shown in chart 1.

Growth at par with the entire market meant that there cumulative holding did

not change from 2010 level. However, the market share shifted among the

top players. SQURPHARMA lost 0.5% market share in the last year (from

19.2% in 2010) while the next four companies gained 1.1% market share in

the same period. Growth in local sales of these four companies – INCEPTA,

BXPHARMA, OPSONIN and RENATA – was 28.5% in 2011, increasing their

market share from 27.0% in 2010 to 28.1% in 2011. Chart 2 in the next page

compares the growth rate for the top companies.

Market Size

(BDT m)

Growth in

2011

Market Share Company

2011 2010

Square Pharmaceuticals 15,725.8 20.5% 18.7% 19.2%

Incepta Pharmaceuticals 7,851.5 28.6% 9.3% 9.0%

Beximco Pharmaceuticals 7,415.0 30.5% 8.8% 8.4%

Opsonin Pharma 4,275.4 27.2% 5.1% 4.9%

Renata 4,076.8 26.1% 4.9% 4.8%

Eskayef Bangladesh 3,980.3 18.9% 4.7% 4.9%

ACI 3,578.2 24.9% 4.3% 4.2%

Acme Pharmaceutical 3,500.7 13.7% 4.2% 4.5%

Aristopharma 3,412.8 26.3% 4.1% 4.0%

Drug International 3,070.2 18.9% 3.7% 3.8%

Top 10 Companies 56,886.5 23.6% 67.7% 67.7%

Top 20 Companies 71,382.5 24.1% 84.9% 84.6%

Others Companies 12,661.6 20.7% 15.1% 15.4%

Total Sector 84,044.1 23.6%

Source: World Bank

Table 5: Major players in the retail market

Square Pharmaceuticals holds the

top market share, followed by

Incepta Pharmaceuticals and

Beximco Pharmaceuticals

Top 10 companies hold 67.7%

market share while top 15

companies hold 77.7% market share

With 6.5% forecasted GDP growth in

the next five years and healthcare

expenditure estimated to reach 5%

of GDP in that time, domestic market

is poised to grow over 15% annually

in the next five years

67.7%

32.3%

Top 10 Others

Source: IMS Report

Chart 1: Market Share

Pharmaceutical Sector in Bangladesh May 2012

5

If we go further down the list of top pharmaceutical companies, the top 15

companies held 77.7% market share in 2011 (which remained unchanged

from 2010 level) and top 20 companies held 84.9% market share in 2011

(slightly higher than 84.6% in 2010). It can be easily seen from the numbers

that the concentration of sales is centered among the top players, in

particular, the local manufacturers. Local manufacturers dominate the

industry, enjoying about 90% market share while multinationals hold little over

10% market share.

Apart from SQURPHARMA, BXPHARMA and RENATA, three other

companies among the top 20 companies are listed in the DSE - ACI (ranked

7th), GlaxoSmithKline Bangladesh (ranked 15th) and The IBN SINA (ranked

20th).

API

About 80% of the active pharmaceutical ingredients (APIs) are imported as

there are only a few local companies (usually the leading ones) that are

engaged in manufacturing APIs. However, the number is really small (below

50) compared to the total requirement. These local companies usually run the

relatively easier final chemical synthesis stage with API intermediaries,

instead of the complete chemical synthesis.

For many APIs, the domestic market is too small to justify an API

manufacturing plant - the initial investment and the production scale required

are high. However, the government has planned to set up an API park to

facilitate the production of several APIs for the local manufacturers. The value

addition for the backward linkage will not be much as the country will again

need to import the basic chemicals for manufacturing APIs. It is estimated

that cost of APIs will decrease by about 20% if the API park is established.

The government initially set a target to complete the project by 2012 but

realistically, it is unlikely that the manufacturing park will be completed within

the stipulated time.

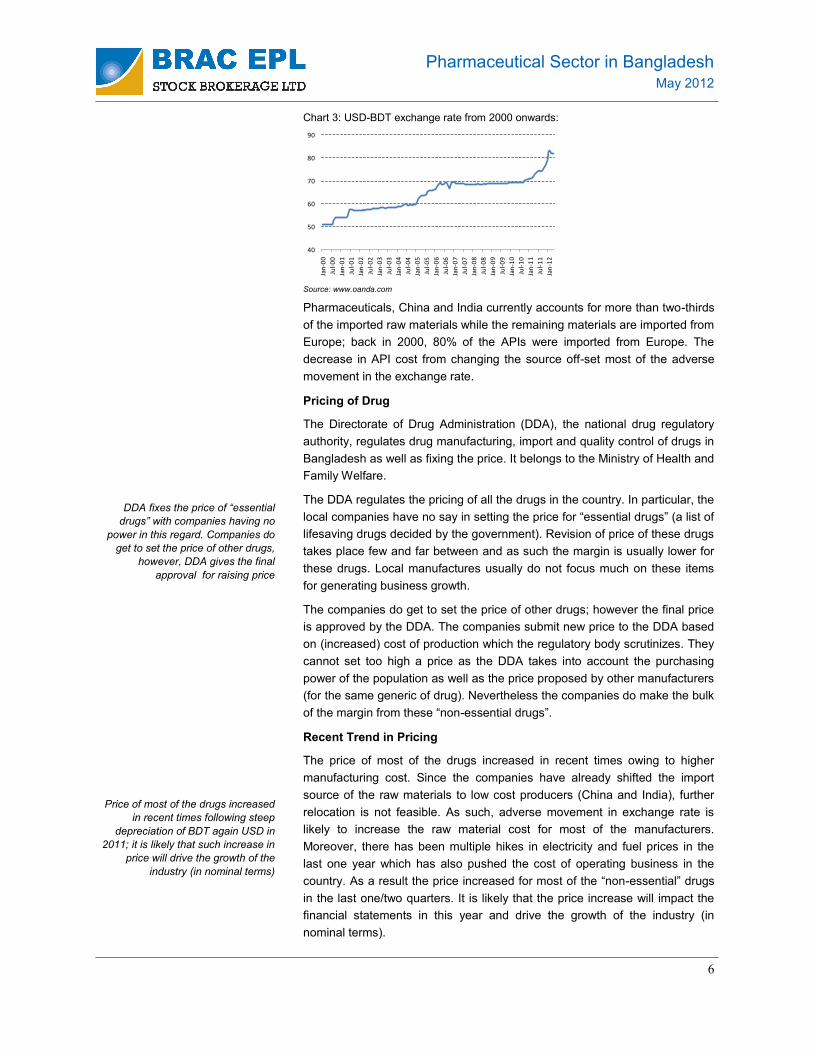

Since the APIs are imported, the companies are exposed to exchange rate

risk. The local currency depreciated significantly against USD over the last

decade as shown in chart 3 in next page. However, the local companies were

able to contain the manufacturing cost by shifting the import source of APIs to

low cost manufacturers. As per discussion with the management of Beximco

Square Pharma (1st), Beximco

Pharma (3rd), Renata (5th), ACI

(7th), GlaxoSmithKline (15th) and

The IBN SINA (20th) are the top

pharmaceutical companies that are

listed in DSE

80% of the APIs are imported.

Government has planned to build a

API park to facilitate local production

of the raw material which will lower

the cost by ~20%

Companies were able to contain raw

material cost despite depreciating

local currency as they have been

importing more raw materials from

India and China (low cost

producers), shifting from Europe.

31%

29%

27%

26%

26%

25%

24%

21%

19%

19%

14%

Beximco Pharmaceuticals

Incepta Pharmaceuticals

Opsonin Pharma

Aristopharma

Renata

ACI

Sector

Square Pharmaceuticals

Drug International

Eskayef Bangladesh

Acme Pharmaceutical

Chart 2: Growth of top ten companies in 2011

Source: IMS Report

Pharmaceutical Sector in Bangladesh May 2012

6

Pharmaceuticals, China and India currently accounts for more than two-thirds

of the imported raw materials while the remaining materials are imported from

Europe; back in 2000, 80% of the APIs were imported from Europe. The

decrease in API cost from changing the source off-set most of the adverse

movement in the exchange rate.

Pricing of Drug

The Directorate of Drug Administration (DDA), the national drug regulatory

authority, regulates drug manufacturing, import and quality control of drugs in

Bangladesh as well as fixing the price. It belongs to the Ministry of Health and

Family Welfare.

The DDA regulates the pricing of all the drugs in the country. In particular, the

local companies have no say in setting the price for “essential drugs” (a list of

lifesaving drugs decided by the government). Revision of price of these drugs

takes place few and far between and as such the margin is usually lower for

these drugs. Local manufactures usually do not focus much on these items

for generating business growth.

The companies do get to set the price of other drugs; however the final price

is approved by the DDA. The companies submit new price to the DDA based

on (increased) cost of production which the regulatory body scrutinizes. They

cannot set too high a price as the DDA takes into account the purchasing

power of the population as well as the price proposed by other manufacturers

(for the same generic of drug). Nevertheless the companies do make the bulk

of the margin from these “non-essential drugs”.

Recent Trend in Pricing

The price of most of the drugs increased in recent times owing to higher

manufacturing cost. Since the companies have already shifted the import

source of the raw materials to low cost producers (China and India), further

relocation is not feasible. As such, adverse movement in exchange rate is

likely to increase the raw material cost for most of the manufacturers.

Moreover, there has been multiple hikes in electricity and fuel prices in the

last one year which has also pushed the cost of operating business in the

country. As a result the price increased for most of the “non-essential” drugs

in the last one/two quarters. It is likely that the price increase will impact the

financial statements in this year and drive the growth of the industry (in

nominal terms).

DDA fixes the price of “essential

drugs” with companies having no

power in this regard. Companies do

get to set the price of other drugs,

however, DDA gives the final

approval for raising price

Price of most of the drugs increased

in recent times following steep

depreciation of BDT again USD in

2011; it is likely that such increase in

price will drive the growth of the

industry (in nominal terms)

Chart 3: USD-BDT exchange rate from 2000 onwards:

Source: www.oanda.com

40

50

60

70

80

90

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Pharmaceutical Sector in Bangladesh May 2012

7

TRIPS

The World Trade Organization's (WTO) Trade-Related Aspects of Intellectual

Property Rights (TRIPs) agreement permits Bangladesh to reverse-engineer

patented generic pharmaceutical products to sell locally and export to

markets around the world. The 1994 WTO agreement TRIPS requires

signatories to implement patent protection for almost all products, including

pharmaceuticals. However, article 66 provides Least Developed Countries

(LDCs) with a breathing space before introducing full product patent

protection. Bangladesh is therefore exempt until 2016 from the requirement to

observe patent protection on reverse-engineered generic products destined

for the local market. Bangladesh imports approximately 80% of its APIs for

domestic production, ~20% of which are patented.

Bangladesh also enjoys some export advantages from TRIPS with regards to

exporting pharmaceutical goods:

Bangladesh can export generic drugs to markets where the patent owner

has not filed for protection. Most drugs on WHO’s Model List of Essential

Drugs are not patented, as affordability is one of the criteria used in

designating medicines as “essential.”

Bangladesh can export to other LDCs or non-WTO members which have

not implemented product patent protection, for example Myanmar.

Bangladesh can also export to a country which has issued a compulsory

drug license and awarded the production contract to Bangladesh. TRIPS

grants governments the right to issue a compulsory license for public

health purposes, which occurs when a government overrides a patent

and grants another entity the right to produce the patented product. It

may do all of this without paying royalties to the patent owner.

The cost of importing APIs will most likely rise as TRIPS phases in. However,

it is likely that WTO would extend the facility for another 10 years on ground

of public health situation and technology transfer issue for producing patent

drugs in the LDCs. WTO will review extension of TRIPS agreement waivers

by the end of 2013. In case the TRIPS agreement is not extended beyond

2015, the local manufacturer will face a number of constraints including:

Import cost of patented APIs are likely to increase.

The cost of manufacturing patented drugs will also increase as the

companies are likely to pay royalty to the original manufacturer.

Export of patented products will become costly.

However, the cost pressure is likely to be associated with a lower proportion

of drugs as less than 20% drugs are patented in the current market.

Moreover, a number of blockbuster drugs have already lost patent or are

about to lose patent in the international market within this year, including

Plavix, Lipitor, Seroquel, Actos, Enbrel, Singulair, Levaquin, Zyprexa and

Concerta. With passage of time, more drugs are set to lose patent rights, as

such the post TRIPS era (if it happens in 2016), is not likely to have a

devastating impact in the pharmaceutical market in Bangladesh.

In case the TRIPS agreement is not

extended beyond 2015, Bangladeshi

companies will face cost pressure in

importing patented APIs and

producing patent drugs. However,

the impact may not be devastating

as proportion of patent drugs is very

small in our market

Bangladesh is exempted till

December 31, 2015 to implement

patent protection for pharmaceuticals

and other products

Pharmaceutical Sector in Bangladesh May 2012

8

Underlying Threat

The advantages that TRIPS provide for Bangladesh are somewhat offset by

the pace and competitiveness of the Indian and Chinese generic markets. In

both the countries, companies can produce drugs at highly competitive

pricing, even with higher costs associated with buying patented APIs or

paying royalties. Bangladesh will have to rely on the standard business

practices of producing the highest quality product at the lowest price to

compete on the international market which may be difficult to achieve in the

near term.

Bangladesh has a competitive disadvantage (when compared to India and

China), since the local pharmaceutical industry is not backward-integrated.

Most of the APIs have to be imported, and even if the APIs are manufactured

in the country, the basic raw materials still have to be imported. As such

construction of API Park is not likely to add too high a value in the

pharmaceutical manufacturing value chain. This results into higher factor

costs, especially in cases where the provider of the API is a competitor in

selling the finished product. Building up backward-integration for all relevant

APIs is also not a realistic option because of scale disadvantages and

infrastructure constraints. The reliance on importing API remains to be the

only significant threat for the pharmaceutical industry in Bangladesh.

Cost structure and Margins for Pharma Industry

Production cost is about 50%-55% for the pharmaceutical companies in

Bangladesh, which results into 45%-50% gross margin for most of the

companies. Raw materials, including API, excipients, packaging materials

and others, account for 75% of the production cost while the remaining 25%

is the conversion cost. Operating cost is about 25% of sales for an average

pharmaceutical company, most of which is dominated by selling and

marketing expenses (more than three-fourth of the operating cost).

Operating margin is about 20%-25% and net profit margin (NPM) varies

around 15% for the industry. The NPM is usually better for the listed

companies as they enjoy significant tax rebate for listing. 37.5% corporate tax

is applicable for non-listed companies in Bangladesh while it goes down to

27.5% for listing in the stock exchange. Listed companies further enjoy 10%

rebate for paying out more than 20% of paid-up capital as cash dividend -

corporate tax rate is only 24.75% for them. Table 6 shows the cost structure

& margin for the top three listed companies (pharmaceutical business only).

The reliance on imported APIs

remain as the major threat to the

industry

37.50%

27.50%24.75%

Non-Listed Listed Listed with 20% cash dividend

Chart 4: Tax Rates for Companies

Source: BRAC EPL Research

Square Beximco Renata

Gross Margin 42.8% 48.9% 52.7%

Operating Exp to sales 20.4% 23.7% 27.1%

Marketing Exp to sales 15.7% 20.1% NA

Operatinf Margin 22.4% 25.2% 25.7%

PBT Margin 25.3% 21.0% 22.2%

Tax expense to sales 6.5% 4.8% 5.5%

Net Margin 18.8% 16.2% 16.7%

Effective tax rate 25.8% 22.8% 24.6%

Table 6: Cost Structure of Top 3 listed companies

Source: BRAC EPL Research

Pharmaceutical Sector in Bangladesh May 2012

9

Export and Import

Bangladesh’s overall export earnings from pharmaceuticals reached USD

46.0 billion for the calendar year 2011, recording a growth of 16.1% over

USD 39.6 billion in calendar year 2010. Exports earnings in Q1’2012 was

USD 10.9 billion, 5.7% up from the same period previous year. Table 6

shows the quarter wise export earnings for the last three years while Chart 5

shows the total export over the last eight fiscal years*.

Pharmaceutical export from Bangladesh recorded 25.5% growth annually

over the last seven years. However, the growth was not steady across all the

years - in fact in FY2009 pharmaceutical export dropped 1.8% following the

global financial crisis. In FY2011 also, the growth was only 1.0% because of

sovereign debt crisis in Europe. Apart from these two years where trade

slowed down significantly worldwide, pharmaceutical export was robust in all

other years.

We expect the export growth to pick up from 2012 onwards given that the

world trade is likely to recover from the sovereign debt crisis. However, the

growth rate is likely to peak four/five years from now. Most of the top

pharmaceutical companies are gearing up for the export market as most of

them have been establishing GMP (Good Manufacturing Practice)

compliance plants. Some of the top companies have already received UK-

MHRA Certificate (Square Pharmaceuticals being the first company to do so

in 2007) while most of them are awaiting for US FDA approval. Apart from

these two major GMP certificate, most of the top companies have already

received GMP clearance from a number of countries, including Turkey,

Yemen, Kenya, Congo, Uganda, Sudan, Ethiopia, etc. Once the growth in the

domestic market becomes steady, companies are likely to focus heavily in

the export market. Earlier, we forecasted domestic market to grow at around

15% annually over the next five years. Top companies can easily achieve

more than 15% growth by attaining higher export sales. Going beyond 2016,

export is likely to be the major driver behind company’s top line growth.

Chart 5: Pharmaceutical Export and Growth (BDT m)

Source: Bangladesh Bank and Export Promotion Bureau

-20%

0%

20%

40%

60%

80%

100%

120%

0.0

400.0

800.0

1,200.0

1,600.0

2,000.0

2,400.0

2,800.0

2004 2005 2006 2007 2008 2009 2010 2011

Pharmaceuticals (LHS) Growth (RHS)

Chart 6: Pharmaceutical and Organic Chemical Import (USD m)

Source: Bangladesh Bank

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2003 2004 2005 2006 2007 2008 2009 2010 2011

Pharmaceuticals Organic Chemical

Export Sales is likely to drive

companies„ revenue once domestic

market reaches steady growth

Some of the top companies already

received the UK-MHRA Certificate

while the US FDA approval is waiting

in the pipeline for many companies

2011 2010 2009

Q1 10.4 9.4 8.8

Q2 12.4 8.7 8.5

Q3 12.3 10.1 10.2

Q4 10.9 11.4 12.7

Total 46.0 39.6 40.1

Table 7: Pharma Export (USD m)

Source: Export Promotion Bureau

* Fiscal Year (FY) is from July to June; FY 2012 means July 2011 to June 2012

Pharmaceutical Sector in Bangladesh May 2012

10

Chart 6 in the previous page shows the import data for pharmaceutical

products and organic chemicals. Over the last eight years, import of

pharmaceutical products grew at 12.9% annually while organic chemical grew

at 15.8%. Unlike export data, pharmaceutical and chemical imports have

been steady over the last four years as the domestic market has been bullish

is the same period.

Budget Directives for FY2012

The government lowered import duties for the FY2012 to provide support to

the pharmaceutical companies. They proposed the following changes to

promote further growth of the sector:

Lower import duty for certain raw materials, from 12% to 5%.

Lower duty for importing certain capital machineries used in the

pharmaceutical industry - for instance a sandwich panel that had a duty

of 12% applied on it would now have a 3% duty.

Withdrawal of existing 5% import duty and 15% VAT on leucocytes filter

used in purification of blood of thalasamia patients

Withdrawal of 20% supplementary duty and reduction of import duty from

25% to 12% on cartridge/membrane filter used for pharmaceuticals

industry.

Extended eligibility for tax holiday for both pharmaceutical and API firms.

Regulatory Assistance

The government has given support to the manufacturing industry for

decades. It adopted The Drug Act 1940 in 1974, originally adopted by the

Indian government in 1940, and later by the Pakistani Government in 1957.

The Drug Act gave protection to the local manufacturers by restricting import

of pharmaceutical products that are manufactured in the country. It

successfully prevented the Indian manufacturers, who could serve the market

at competitive price, from entering the country. Going forward there is no

regulatory risk that import restriction will be removed and local companies are

likely to continue on dominating the pharmaceutical market.

The government has planned to set up the API park by 2012 to facilitate API

production and lower reliance on API import. In the last budget also,

government provided various incentives to lower the import cost of the

pharmaceutical manufacturers. In this coming budget for FY 2013, it is

expected that the government is going to provide incentive to export - in

particular easing up the documentation procedures and removing bottleneck

for exporting goods.

Performance of Listed Companies

Of the six listed companies, only BXPHARMA and IBNSINA reports stand-

alone statements while the other four reports consolidated numbers. For

SQURPHARMA and RENATA, the pharmaceutical business generates bulk

of the consolidated revenue (80% and 94% respectively for the two

companies) while for ACI and GLAXOSMITH the proportion is much lower

Year Rebate

Year 1 100%

Year 2 100%

Year 3 50%

Year 4 50%

Year 5 25%

Source: Budget Speech for FY12

Table 8: Tax Holiday Structure

Pharmaceutical Sector in Bangladesh May 2012

11

(about 50%). Among the six companies, SQURPHARMA, BXPHARMA and

RENATA present investors with prospective investment opportunities. For

IBNSINA the market capitalization is very small for investment.

The sector P/E ratio (comprising of these six companies only) stands at

21.2x. Because of the market weight of the top two, the P/E ratio is heavily

tilted towards Square Pharmaceuticals (20.0x) and Beximco Pharmaceuticals

(19.7x). Renata has the highest P/E ratio of 26.0x.

DSE Ticker Market Price

(BDT)

Market Cap

(BDT m)

Profit in 2011

(BDT m) P/E

SQURPHARMA 268.7 71,161.1 3,565.4 20.0x

BXPHARMA 93.9 23,641.0 1,198.4 19.7x RENATA 981.2 27,710.9 1,066.7 26.0x

ACI 247.8 4,885.3 238.1 20.5x

GLAXOSMITH 605.2 7,290.5 282.1 25.8x

IBNSINA 135.5 1,756.1 70.8 24.8x

MCAP Weighted P/E 21.2x

Source: DSE Website and BRAC EPL Research

Table 9: Comparison of listed pharmaceuticals companies

* Market price and market capitalization given as on May 10, 2012

Pharmaceutical Sector in Bangladesh May 2012

12

IMPORTANT DISCLOSURES

Analyst Certification: Each research analyst and research associate who authored this document and whose name appears herein certifies that the recommendations and opinions expressed in the research report accurately reflect their personal views about any and all of the securities or issuers discussed therein that are within the coverage universe. Disclaimer: Estimates and projections herein are our own and are based on assumptions that we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation of the purchase or sale of any security. As it acts for public companies from time to time, BRAC-EPL may have a relationship with the above mentioned company(s). This report is intended for distribution in only those jurisdictions in which BRAC-EPL is registered and any distribution outside those jurisdictions is strictly prohibited. Compensation of Analysts: The compensation of research analysts is intended to reflect the value of the services they provide to the clients of BRAC-EPL. As with most other employees, the compensation of research analysts is impacted by the overall profitability of the firm, which may include revenues from corporate finance activities of the firm's Corporate Finance department. However, Research analysts' compensation is not directly related to specific corporate finance transaction. General Risk Factors: BRAC-EPL will conduct a comprehensive risk assessment for each company under coverage at the time of initiating research coverage and also revisit this assessment when subsequent update reports are published or material company events occur. Following are some general risks that can impact future operational and financial performance: (1) Industry fundamentals with respect to customer demand or product / service pricing could change expected revenues and earnings; (2) Issues relating to major competitors or market shares or new product expectations could change investor attitudes; (3) Unforeseen developments with respect to the management, financial condition or accounting policies alter the prospective valuation; or (4) Interest rates, currency or major segments of the economy could alter investor confidence and investment prospects.

BRAC EPL Research www.bracepl.com 121/B Gulshan Avenue Gulshan-2, Dhaka Phone: +880 2 881 9421-5 Fax: +880 2 881 9426 E-Mail: [email protected]

BRAC EPL Stock Brokerage Capital Markets Group

Institutional Sales and Trading

Delwar Hussain (Del) Head of International Trade & Sales

[email protected] 01755 541 252

Ali Imam Head of Research [email protected] 01730 357 153

Khandakar Safwan Saad Research Associate [email protected] 01730 357 779

Farjad Siddiqui Research Associate [email protected] 01730 727 924

Kallol Biswas Research Associate [email protected] 01730 727 930

Nafees Mohammed Badruddin Research Associate [email protected] 01730 727 931

Sajid Huq Amit Head of Strategic Sales [email protected] 01755 541 254

Strategic Sales