1384499235.ppt

TRANSCRIPT

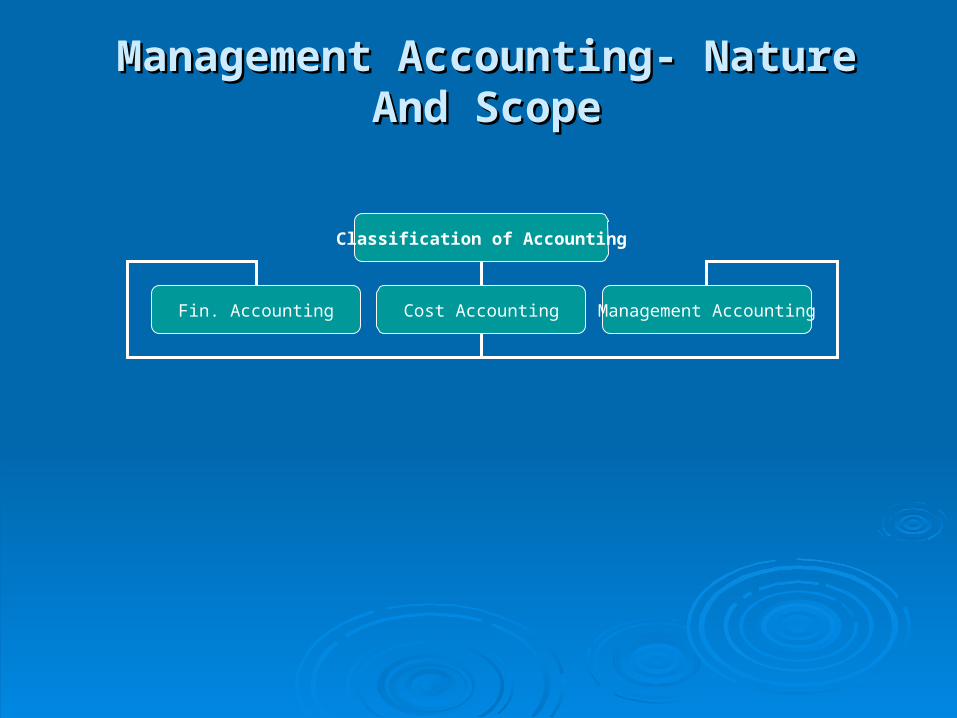

Management Accounting- Nature And Management Accounting- Nature And ScopeScope

Classification of Accounting

Fin. Accounting Cost Accounting Management Accounting

Financial AccountingFinancial Accounting – Fin. Acc is concerned with – Fin. Acc is concerned with recording, classifying and summarising the business recording, classifying and summarising the business transaction so that at the end of the year profit or loss transaction so that at the end of the year profit or loss can be calculated and its effect on owned capital, assets can be calculated and its effect on owned capital, assets and liabilities can be ascertained.and liabilities can be ascertained.

Principles of Financial AccountingPrinciples of Financial Accounting – – A. Accounting ConceptsA. Accounting Concepts Business Entity ConceptBusiness Entity Concept Going Concern ConceptGoing Concern Concept Money Measurement ConceptMoney Measurement Concept Cost ConceptCost Concept Dual Aspect ConceptDual Aspect Concept Realisation ConceptRealisation Concept Accounting Period ConceptAccounting Period Concept Matching ConceptMatching Concept

B. B. Accounting ConventionsAccounting Conventions :- :- Convention of ConsistencyConvention of Consistency Convention of Materiality and DisclosureConvention of Materiality and Disclosure Convention of ConservatismConvention of Conservatism

Limitations of Financial AccountingLimitations of Financial Accountingo Change in Nature of BusinessChange in Nature of Businesso Shift in EmphasisShift in Emphasiso Provision of Historical InformationProvision of Historical Informationo Fails to meet the information needs of Different levels of Fails to meet the information needs of Different levels of

ManagementManagemento Consideration of only Monetary informationConsideration of only Monetary informationo Less Importance of Budgeting and Planning Less Importance of Budgeting and Planning

Cost AccountingCost AccountingCost Accounting is the next stage in the development of Cost Accounting is the next stage in the development of accounting. Under cost accounting total cost of goods and accounting. Under cost accounting total cost of goods and the elements of total cost are studied.the elements of total cost are studied.Definition :- Definition :- ICWA London :- “Cost Accounting is the technique and ICWA London :- “Cost Accounting is the technique and

process of ascertainment of costs.”process of ascertainment of costs.”Objectives of Cost AccountingObjectives of Cost Accounting(1)(1) Cost DeterminationCost Determination(2)(2) To help Management in Cost ControlTo help Management in Cost Control(3)(3) To determine Selling Price To determine Selling Price (4)(4) To facilitate Management Decision MakingTo facilitate Management Decision Making

Management AccountingManagement AccountingManagement needs detailed information on different aspects to Management needs detailed information on different aspects to

arrive at meaningful decisions. Financial accounting provides arrive at meaningful decisions. Financial accounting provides some informations but these are not adequate. Management some informations but these are not adequate. Management accounting removes these limitations of financial accounting. accounting removes these limitations of financial accounting. Thus, management accounting means- “Accounting for Thus, management accounting means- “Accounting for Management to discharge its functions including organising, Management to discharge its functions including organising, planning, directing and controlling. planning, directing and controlling.

Definition :- According to American Accountng Association, Definition :- According to American Accountng Association, “Management accounting includes the methods and concepts “Management accounting includes the methods and concepts necessary for effective planning, for choosing among necessary for effective planning, for choosing among alternative business actions and for control through the alternative business actions and for control through the evaluation and interpretation of performance.” evaluation and interpretation of performance.”

R.N. Anthony :- “Management accounting is concerned with R.N. Anthony :- “Management accounting is concerned with accounting information that is useful to managementaccounting information that is useful to management

Functions of Management AccountingFunctions of Management Accounting1)1) Provides dataProvides data2)2) Modifies DataModifies Data3)3) Analysis and interpretation of dataAnalysis and interpretation of data4)4) Use of Qualitative Information alsoUse of Qualitative Information also5)5) To help in PlanningTo help in Planning6)6) To help in OrganisingTo help in Organising7)7) To help in MotivationTo help in Motivation8)8) To help in Co-ordinationTo help in Co-ordination9)9) CommunicationCommunication10)10) To help in ControlTo help in Control11)11) To help in Decision MakingTo help in Decision Making

Scope of Management Accounting Scope of Management Accounting

Cost Acc

Interim Reporting

Internal Audit

Revaluation Acc Taxation

Statistical

Inventory

Budgetary

Fin. Acc

Scope of Mgt Acc

Distinction Between Management Distinction Between Management Accounting and Financial AccountingAccounting and Financial Accounting

Mgt AccountingMgt Accounting ObjectivesObjectives :- To help mgt in :- To help mgt in

planning & decision-making. It is planning & decision-making. It is an Internal reporting system.an Internal reporting system.

2. 2. Subject MatterSubject Matter :- It reveals the :- It reveals the profitability or performance or profitability or performance or different departments products different departments products etc in detail.etc in detail.

3.3. Nature of Data usedNature of Data used :- Mgt Acc :- Mgt Acc uses detailed, statistical, uses detailed, statistical, relative, past and future data relative, past and future data and information.and information.

4.4. PeriodicityPeriodicity :- Small intervals :- Small intervals and quick information.and quick information.

5.5. AccuracyAccuracy :- Need not to be :- Need not to be completely accurate.completely accurate.

Fin. AccountingFin. Accounting1.1. Provides information to Provides information to

creditors, shareholders, banks, creditors, shareholders, banks, investors, govt. It is an external investors, govt. It is an external reporting system.reporting system.

2.2. Fin acc deals with the overall Fin acc deals with the overall position of business because fin. position of business because fin. Statements explain the position Statements explain the position the position of business in the position of business in totality.totality.

3.3. Fin acc presents monetary Fin acc presents monetary information of historic events information of historic events and transactions.and transactions.

4.4. Long time period.Long time period.

5.5. Completely accurate.Completely accurate.

Mgt. AccountingMgt. Accounting6. Compulsion : Mgt 6. Compulsion : Mgt

Accounting is voluntary Accounting is voluntary and has no legal and has no legal compulsion.compulsion.

7. Legal Formalities :- There 7. Legal Formalities :- There is no legal form or rules is no legal form or rules for the statements or for the statements or reports under mgt reports under mgt accounting.accounting.

8. Monetary Transactions :- 8. Monetary Transactions :- Mgt acc. Records Mgt acc. Records financial and non-financial and non-financial information.financial information.

Fin. AccountingFin. Accounting6. Fin. Acc is necessary for 6. Fin. Acc is necessary for

every business due to every business due to legal provisions.legal provisions.

7. Fin. Accounts are 7. Fin. Accounts are prepared under the prepared under the provisions of Company provisions of Company act, 1956.act, 1956.

8. Fin. Acc records only 8. Fin. Acc records only those transactions which those transactions which can e expressed in can e expressed in money formmoney form

Distinction between Cost Accounting and Distinction between Cost Accounting and Management Accounting Management Accounting

Cost AccountingCost Accounting1.1. Objective : to determine the Objective : to determine the

cost and control it.cost and control it.

2. Subject Matter :- Cost 2. Subject Matter :- Cost accounting deals mainly with accounting deals mainly with cost datacost data

3. Scope :- Cost accounting 3. Scope :- Cost accounting provides information relating provides information relating to cost of products only , so to cost of products only , so its scope is narrow.its scope is narrow.

Mgt AccountingMgt Accounting1.1. Mgt Acc helps the Mgt Acc helps the

management in decision management in decision making through cost and making through cost and financial information.financial information.

2.2. Mgt acc considers both cost Mgt acc considers both cost and income aspects.and income aspects.

3. Mgt acc has a wide scope as 3. Mgt acc has a wide scope as it collects information from it collects information from fin. Acc, cost acc and fin. Acc, cost acc and busine4ss finance.busine4ss finance.

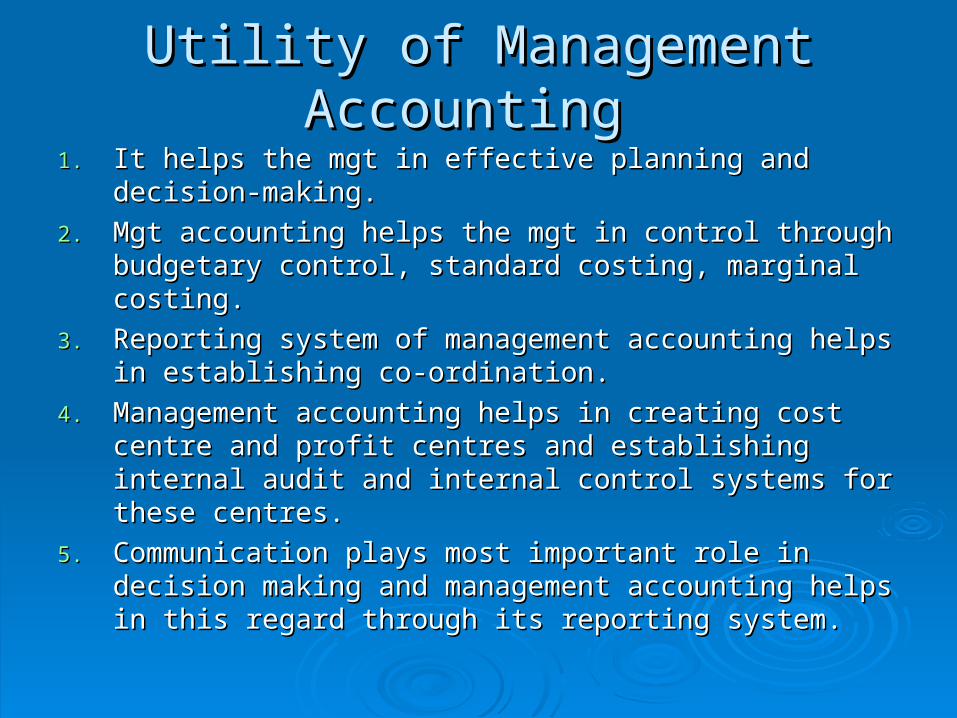

Utility of Management Accounting Utility of Management Accounting 1.1. It helps the mgt in effective planning and decision-It helps the mgt in effective planning and decision-

making.making.2.2. Mgt accounting helps the mgt in control through Mgt accounting helps the mgt in control through

budgetary control, standard costing, marginal costing.budgetary control, standard costing, marginal costing.3.3. Reporting system of management accounting helps in Reporting system of management accounting helps in

establishing co-ordination.establishing co-ordination.4.4. Management accounting helps in creating cost centre Management accounting helps in creating cost centre

and profit centres and establishing internal audit and and profit centres and establishing internal audit and internal control systems for these centres.internal control systems for these centres.

5.5. Communication plays most important role in decision Communication plays most important role in decision making and management accounting helps in this making and management accounting helps in this regard through its reporting system. regard through its reporting system.

Limitations of Management AccountingLimitations of Management Accounting

1.1. Limitations of Cost and Financial Accounting Limitations of Cost and Financial Accounting SystemSystem

2.2. Persistence of Intuitive DecisionPersistence of Intuitive Decision3.3. Wider ScopeWider Scope4.4. Costly SystemCostly System5.5. Psychological ResistancePsychological Resistance6.6. EvolutionaryEvolutionary7.7. It is not Alternative to ManagementIt is not Alternative to Management

Techniques of Management AccountingTechniques of Management Accounting

i.i. Analysis of Financial StatementsAnalysis of Financial Statementsii.ii. Ratio AnalysisRatio Analysisiii.iii. Fund Flow StatementFund Flow Statementiv.iv. Cash Flow StatementCash Flow Statementv.v. Marginal Costing and Cost-volume Profit AnalysisMarginal Costing and Cost-volume Profit Analysisvi.vi. Budgetary Control and standard costingBudgetary Control and standard costingvii.vii. Management ReportingManagement Reportingviii.viii. Statistical TechniquesStatistical Techniquesix.ix. Value Added Statement Value Added Statement x.x. Accounting Price Level ChangesAccounting Price Level Changesxi.xi. Human Resource AccountingHuman Resource Accounting