15.401 finance theory i, options - mit opencourseware · a brief history of option-pricing theory...

TRANSCRIPT

15.401

15.401 Finance Theory15.401 Finance TheoryMIT Sloan MBA Program

Andrew W. LoAndrew W. LoHarris & Harris Group Professor, MIT Sloan SchoolHarris & Harris Group Professor, MIT Sloan School

Lectures 10Lectures 10––1111: Options: Options

© 2007–2008 by Andrew W. Lo

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 2

Critical ConceptsCritical ConceptsMotivationPayoff DiagramsPayoff TablesOption StrategiesOther Option-Like SecuritiesValuation of OptionsA Brief History of Option-Pricing TheoryExtensions and Qualifications

Readings:Brealey, Myers, and Allen Chapters 27

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 3

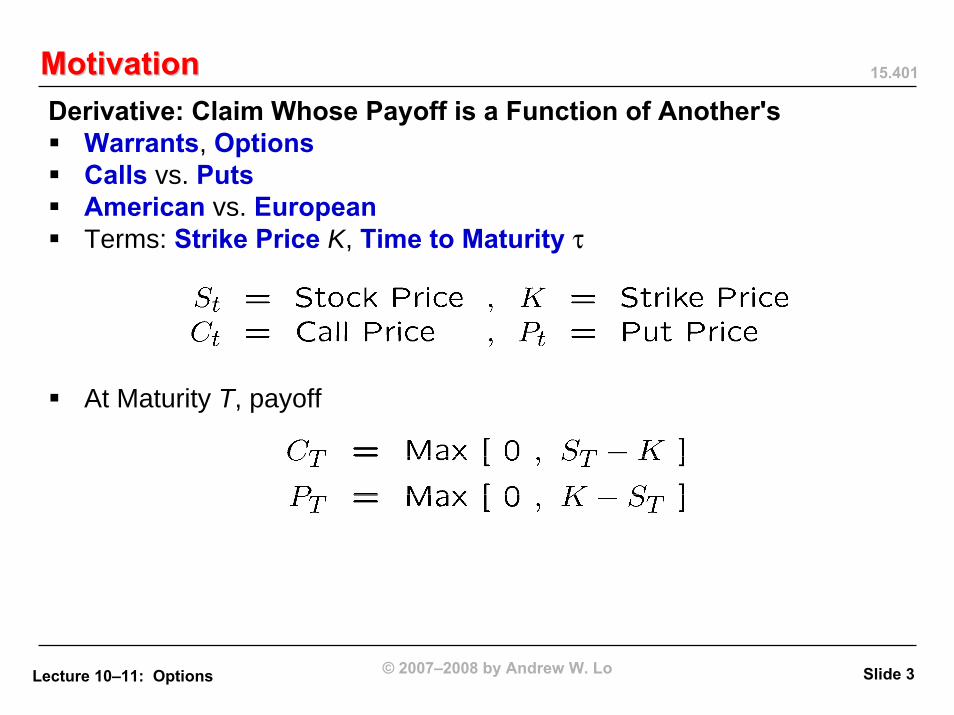

MotivationMotivationDerivative: Claim Whose Payoff is a Function of Another's

Warrants, OptionsCalls vs. PutsAmerican vs. EuropeanTerms: Strike Price K, Time to Maturity τ

At Maturity T, payoff

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 4

MotivationMotivationPut Options As Insurance

Differences– Early exercise– Marketability– Dividends

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 5

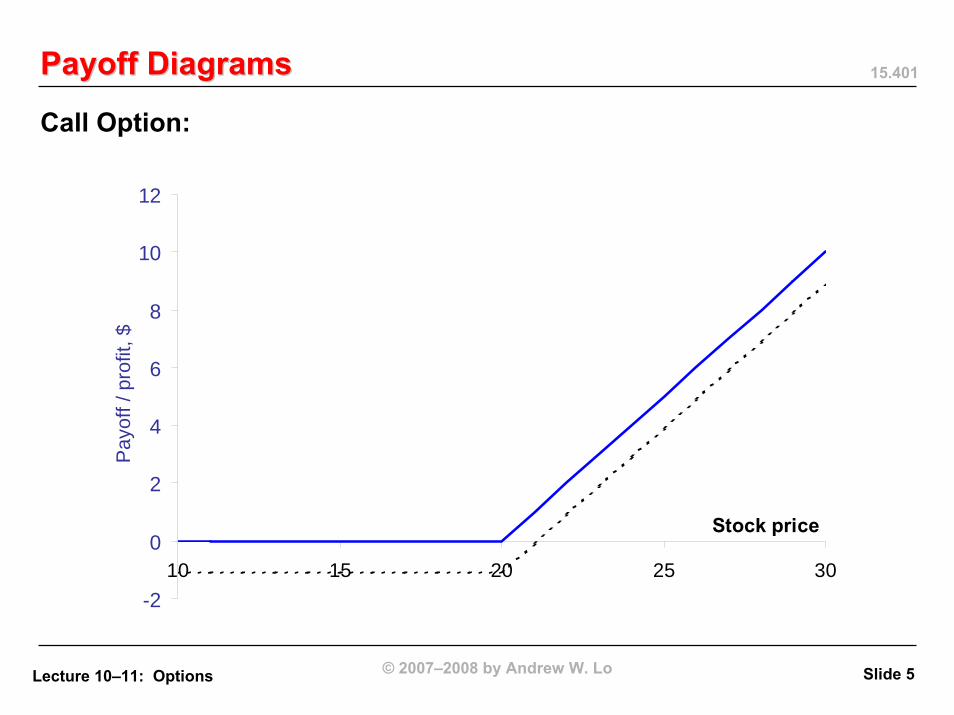

Payoff DiagramsPayoff Diagrams

Call Option:

-2

0

2

4

6

8

10

12

10 15 20 25 30

Stock price

Pay

off /

pro

fit, $

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 6

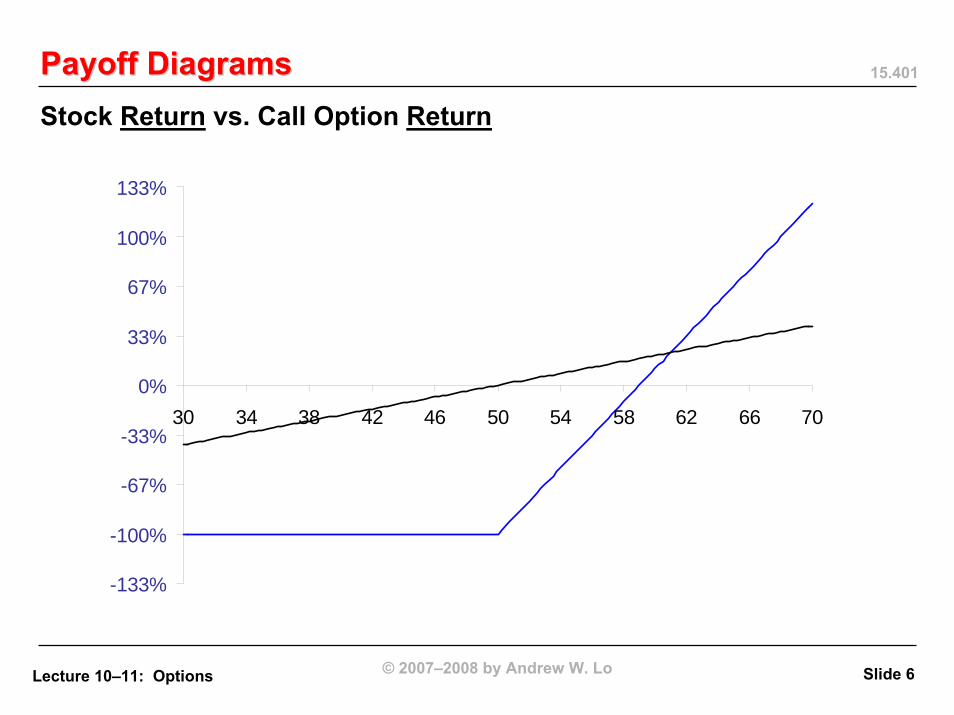

Payoff DiagramsPayoff DiagramsStock Return vs. Call Option Return

-133%

-100%

-67%

-33%

0%

33%

67%

100%

133%

30 34 38 42 46 50 54 58 62 66 70

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 7

Payoff DiagramsPayoff Diagrams

Put Option:

-4

-2

0

2

4

6

8

10

12

10 15 20 25 30

Stock price

Pay

off /

pro

fit, $

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 8

Payoff DiagramsPayoff Diagrams

-5

0

5

10

15

20

25

30 40 50 60 70

Stock price-5

0

5

10

15

20

25

30 40 50 60 70Stock price

-25

-20

-15

-10

-5

0

5

30 40 50 60 70

Stock price

-25

-20

-15

-10

-5

0

5

30 40 50 60 70

Stock price

Long Call

Short Put

Long Put

Short Call

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 9

Payoff TablesPayoff TablesStock Price = S, Strike Price = X

Call option (price = C) if S < X if S = X if S > XPayoff 0 0 S – XProfit –C –C S – X – C

Put option (price = P)

if S < X if S = X if S > XPayoff X – S 0 0Profit X – S – P –P –P

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 10

Option StrategiesOption StrategiesTrading strategies

Options can be combined in various ways to create an unlimited number of payoff profiles.

ExamplesBuy a stock and a putBuy a call with one strike price and sell a call with anotherBuy a call and a put with the same strike price

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 11

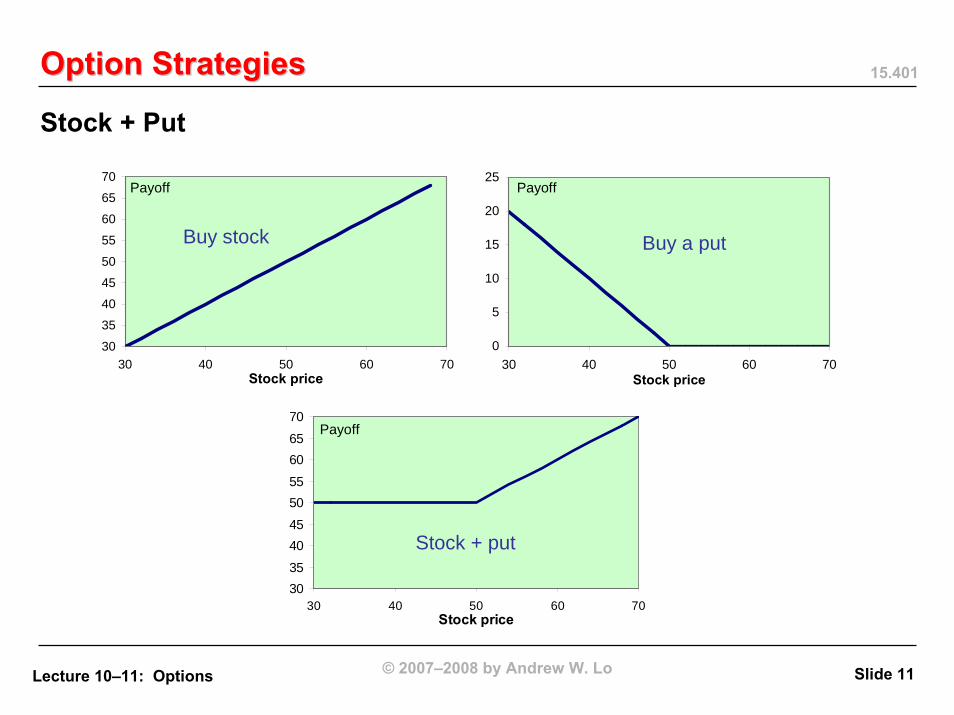

Option StrategiesOption Strategies

Stock + Put

30

35

40

45

50

55

60

65

70

30 40 50 60 70Stock price

0

5

10

15

20

25

30 40 50 60 70Stock price

3035

4045

5055

6065

70

30 40 50 60 70Stock price

Buy stock Buy a put

Payoff Payoff

Stock + put

Payoff

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 12

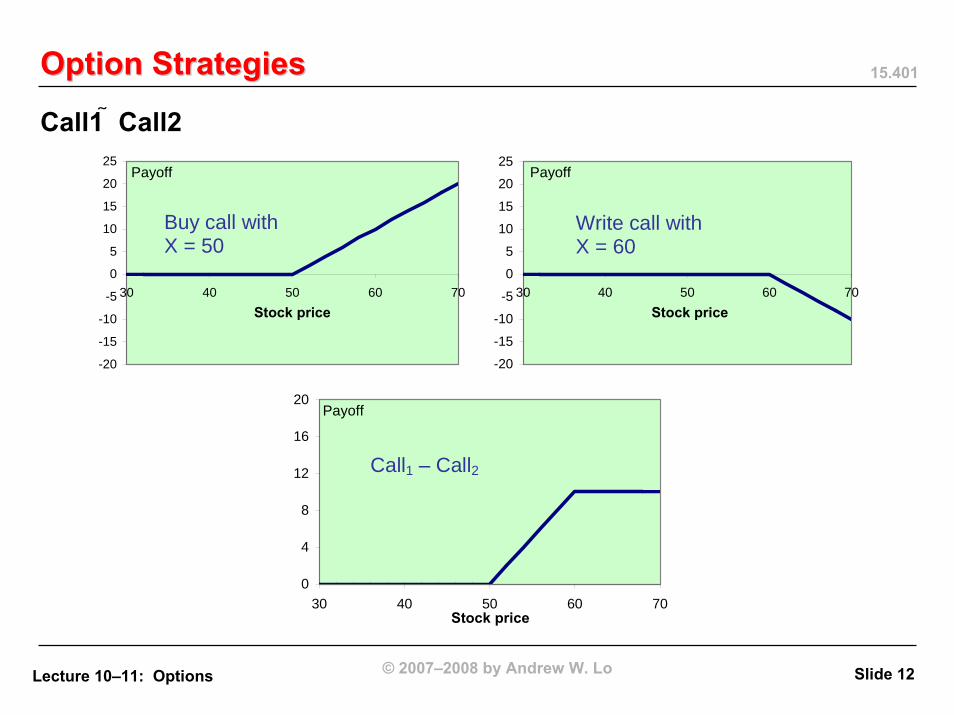

Option StrategiesOption Strategies

Call1 Call2

-20

-15

-10

-5

0

5

10

15

20

25

30 40 50 60 70Stock price

-20

-15

-10

-5

0

5

10

15

20

25

30 40 50 60 70Stock price

0

4

8

12

16

20

30 40 50 60 70Stock price

Buy call with X = 50

Write call with X = 60

Payoff Payoff

Call1 – Call2

Payoff

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 13

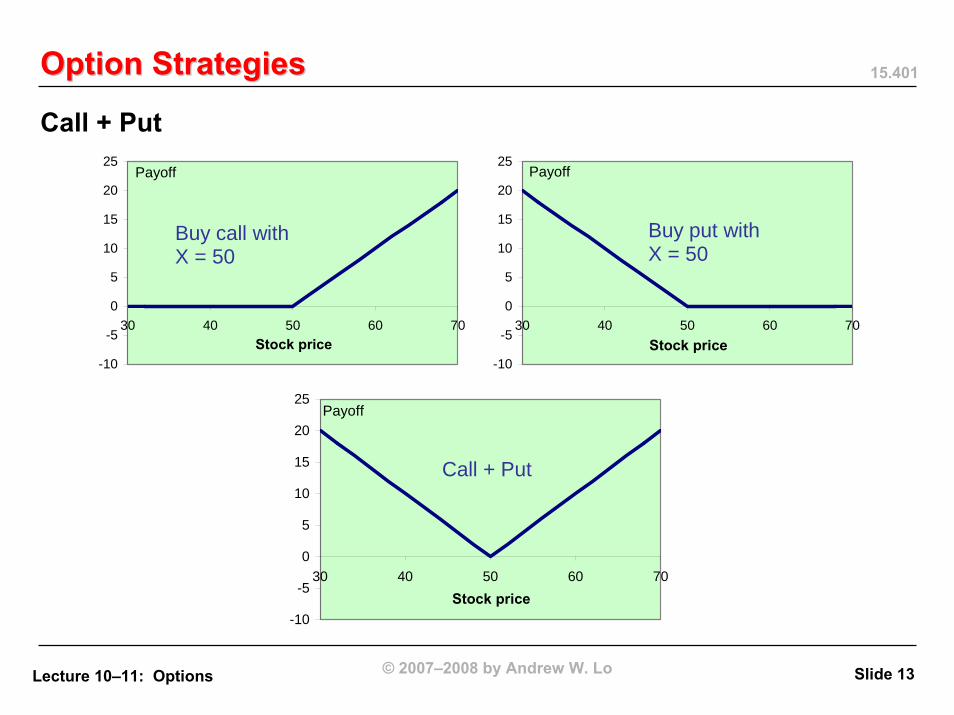

Option StrategiesOption Strategies

Call + Put

-10

-5

0

5

10

15

20

25

30 40 50 60 70Stock price

-10

-5

0

5

10

15

20

25

30 40 50 60 70Stock price

-10

-5

0

5

10

15

20

25

30 40 50 60 70Stock price

Buy call with X = 50

Buy put with X = 50

Payoff Payoff

Call + Put

Payoff

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 14

Other OptionOther Option--Like SecuritiesLike Securities

Corporate Liabilities:

Equity: hold call, or protected levered putDebt: issue put and (riskless) lendingQuantifies Compensation Incentive Problems:– Biased towards higher risk– Can overwhelm NPV considerations– Example: leveraged equity

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 15

Other OptionOther Option--Like SecuritiesLike SecuritiesOther Examples of Derivative Securities:

Asian or “Look Back” OptionsCallables, ConvertiblesFutures, ForwardsSwaps, Caps, FloorsReal Investment OpportunitiesPatentsTenureetc.

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 16

Valuation of OptionsValuation of Options

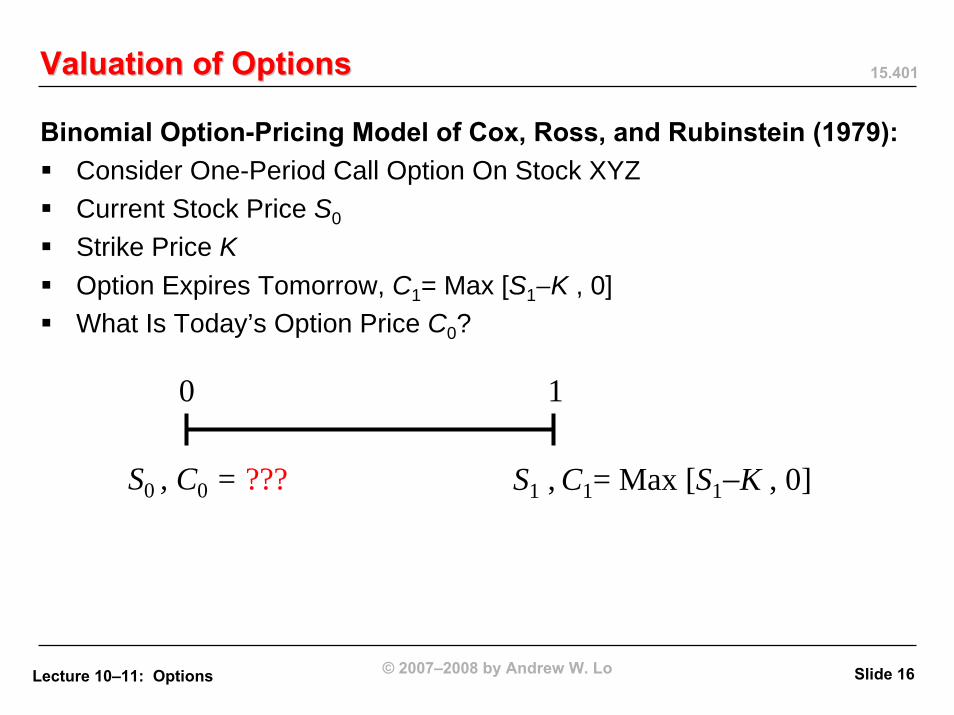

Binomial Option-Pricing Model of Cox, Ross, and Rubinstein (1979):Consider One-Period Call Option On Stock XYZCurrent Stock Price S0

Strike Price KOption Expires Tomorrow, C1= Max [S1−K , 0]What Is Today’s Option Price C0?

S0 , C0 = ???

0 1

S1 , C1= Max [S1−K , 0]

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 17

Valuation of OptionsValuation of Options

Suppose S0 → S1 Is A Bernoulli Trial:

S1

uS0

dS0

p

1− p

u > d

C1

Max [ uS0 − K , 0 ] == Cu

Max [ dS0 − K , 0 ] == Cd

p

1− p

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 18

Valuation of OptionsValuation of Options

Now What Should C0 = f (⋅) Depend On?Parameters: S0 , K , u , d , p , r

Consider Portfolio of Stocks and Bonds Today:∆ Shares of Stock, $B of BondsTotal Cost Today: V0 == S0∆ + BPayoff V1 Tomorrow:

V1

uS0∆ + rB

dS0 ∆ + rB

p

1− p

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 19

Valuation of OptionsValuation of Options

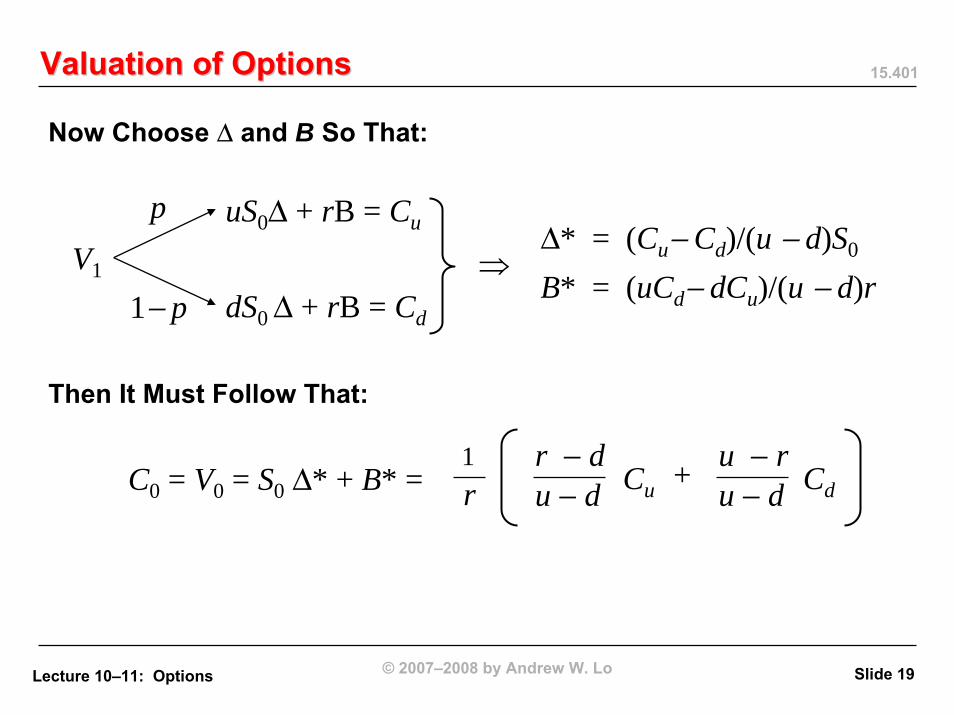

Now Choose ∆ and B So That:

V1

uS0∆ + rB = Cu

dS0 ∆ + rB = Cd

p

1− p⇒

∆* = (Cu− Cd)/(u − d)S0

B* = (uCd− dCu)/(u − d)r

Then It Must Follow That:

C0 = V0 = S0 ∆* + B* = 1r

r − du − d Cu

u − ru − d Cd+

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 20

Valuation of OptionsValuation of Options

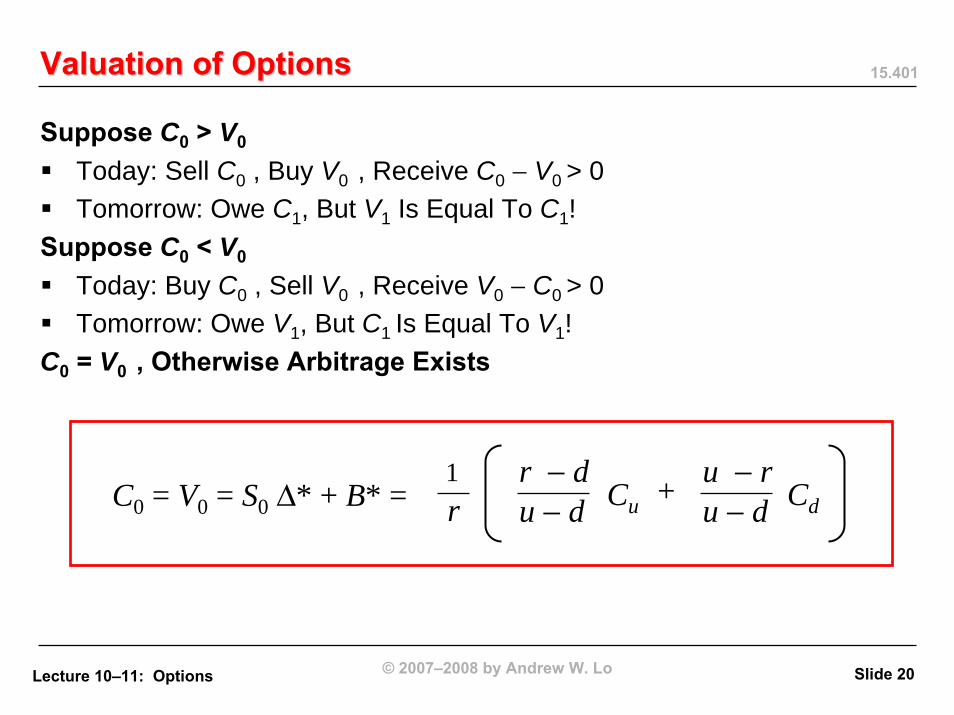

Suppose C0 > V0

Today: Sell C0 , Buy V0 , Receive C0 − V0 > 0Tomorrow: Owe C1, But V1 Is Equal To C1!

Suppose C0 < V0

Today: Buy C0 , Sell V0 , Receive V0 − C0 > 0Tomorrow: Owe V1, But C1 Is Equal To V1!

C0 = V0 , Otherwise Arbitrage Exists

C0 = V0 = S0 ∆* + B* = 1r

r − du − d Cu

u − ru − d Cd+

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 21

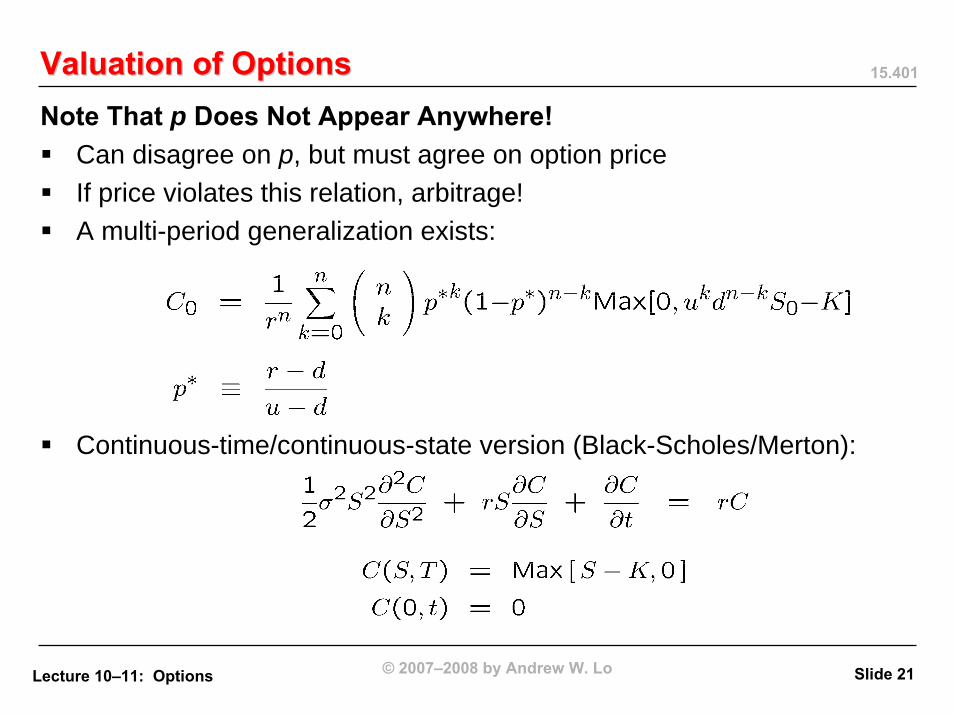

Valuation of OptionsValuation of OptionsNote That p Does Not Appear Anywhere!

Can disagree on p, but must agree on option priceIf price violates this relation, arbitrage!A multi-period generalization exists:

Continuous-time/continuous-state version (Black-Scholes/Merton):

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 22

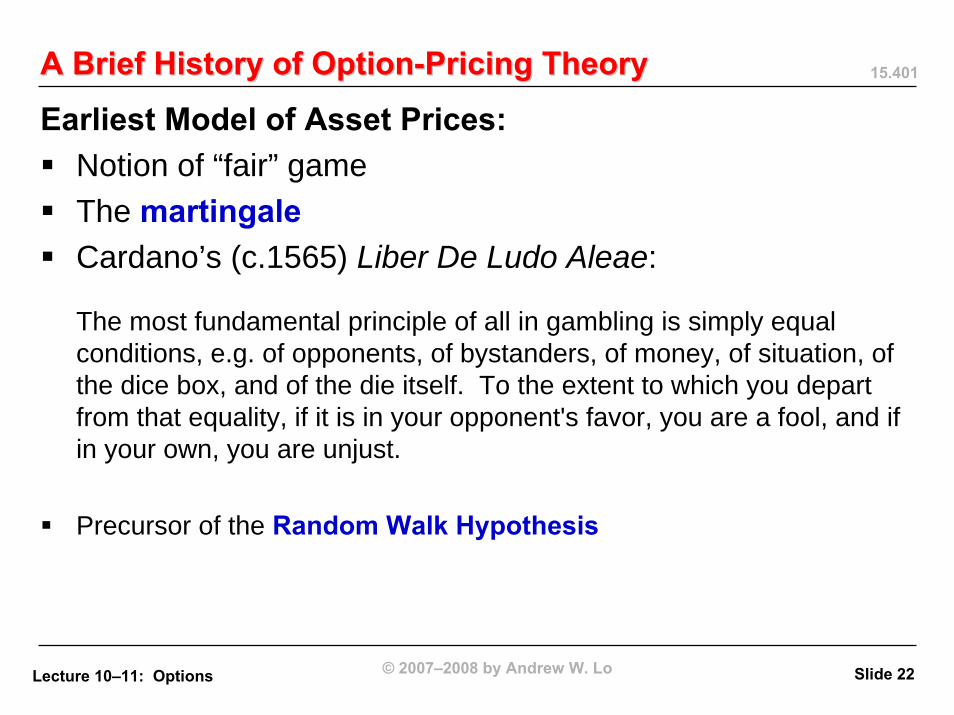

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing Theory

Earliest Model of Asset Prices:Notion of “fair” gameThe martingaleCardano’s (c.1565) Liber De Ludo Aleae:

The most fundamental principle of all in gambling is simply equal conditions, e.g. of opponents, of bystanders, of money, of situation, of the dice box, and of the die itself. To the extent to which you depart from that equality, if it is in your opponent's favor, you are a fool, and if in your own, you are unjust.

Precursor of the Random Walk Hypothesis

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 23

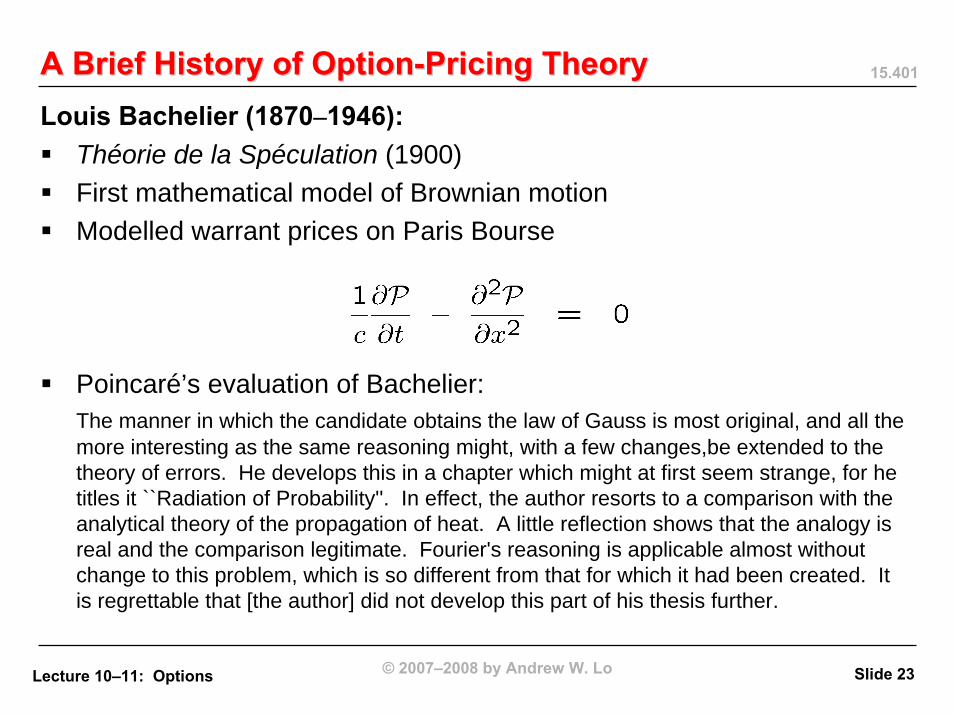

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing TheoryLouis Bachelier (1870–1946):

Théorie de la Spéculation (1900)First mathematical model of Brownian motionModelled warrant prices on Paris Bourse

Poincaré’s evaluation of Bachelier:The manner in which the candidate obtains the law of Gauss is most original, and all the more interesting as the same reasoning might, with a few changes,be extended to the theory of errors. He develops this in a chapter which might at first seem strange, for he titles it ``Radiation of Probability''. In effect, the author resorts to a comparison with the analytical theory of the propagation of heat. A little reflection shows that the analogy is real and the comparison legitimate. Fourier's reasoning is applicable almost without change to this problem, which is so different from that for which it had been created. It is regrettable that [the author] did not develop this part of his thesis further.

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 24

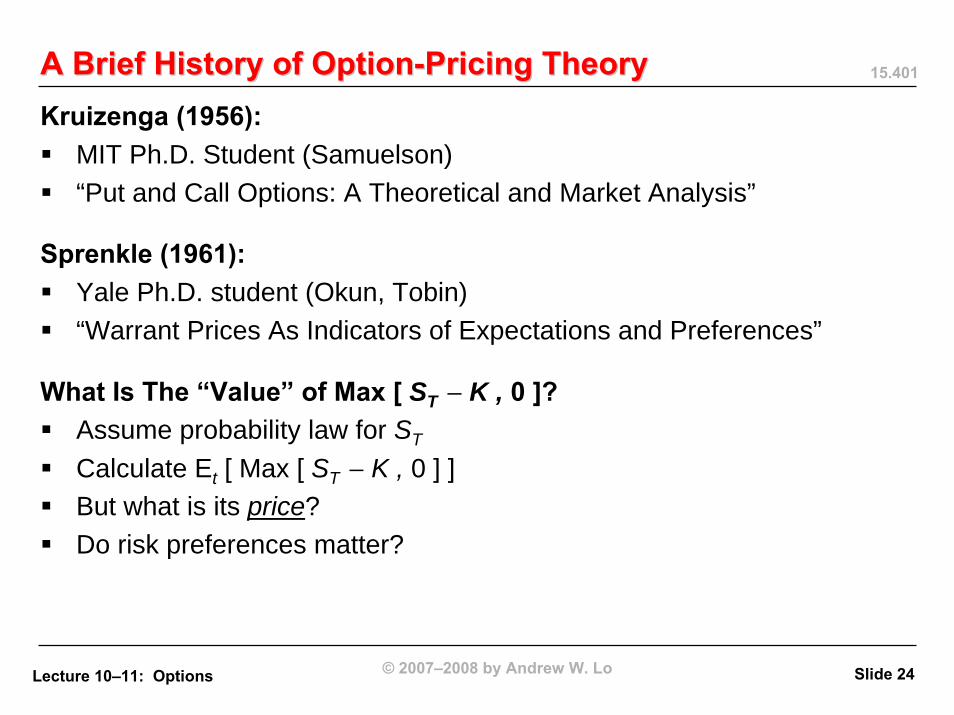

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing TheoryKruizenga (1956):

MIT Ph.D. Student (Samuelson)“Put and Call Options: A Theoretical and Market Analysis”

Sprenkle (1961):Yale Ph.D. student (Okun, Tobin)“Warrant Prices As Indicators of Expectations and Preferences”

What Is The “Value” of Max [ ST − K , 0 ]?Assume probability law for ST

Calculate Et [ Max [ ST − K , 0 ] ]But what is its price?Do risk preferences matter?

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 25

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing TheorySamuelson (1965):

“Rational Theory of Warrant Pricing”“Appendix: A Free Boundary Problem for the Heat Equation Arising from a Problem in Mathematical Economics”, H.P. McKean

Samuelson and Merton (1969):“A Complete Model of Warrant Pricing that Maximizes Utility”Uses preferences to value expected payoff

Black and Scholes (1973):Construct portfolio of options and stockEliminate market risk (appeal to CAPM)Remaining risk is inconsequential (idiosyncratic)Expected return given by CAPM (PDE)

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 26

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing TheoryMerton (1973):

Use continuous-time framework– Construct portfolio of options and stock– Eliminate market risk (dynamically)– Eliminate idiosyncratic risk (dynamically)– Zero payoff at maturity– No risk, zero payoff ⇒ zero cost (otherwise arbitrage)– Same PDE

More importantly, a “production process” for derivatives!Formed the basis of financial engineering and three distinct industries:– Listed options– OTC structured products– Credit derivatives

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 27

A Brief History of OptionA Brief History of Option--Pricing TheoryPricing TheoryThe Rest Is Financial History:

Photographs removed due to copyright restrictions.

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 28

Extensions and QualificationsExtensions and Qualifications

The derivatives pricing literature is HUGEThe mathematical tools involved can be quite challengingRecent areas of innovation include:– Empirical methods in estimating option pricings– Non-parametric option-pricing models– Models of credit derivatives– Structured products with hedge funds as the underlying– New methods for managing the risks of derivatives– Quasi-Monte-Carlo methods for simulation estimators

Computational demands can be quite significantThis is considered “rocket science”

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 29

Key PointsKey Points

Options have nonlinear payoffs, as diagrams showSome options can be viewed as insurance contractsOption strategies allow investors to take more sophisticated betsValuation is typically derived via arbitrage arguments (e.g., binomial)Option-pricing models have a long and illustrious history

© 2007–2008 by Andrew W. LoLecture 10–11: Options

15.401

Slide 30

Additional ReferencesAdditional ReferencesBachelier, L, 1900, “Théorie de la Spéculation”, Annales de l'Ecole Normale Supérieure 3 (Paris, Gauthier-Villars).Black, F., 1989, “How We Came Up with the Option Formula”, Journal of Portfolio Management 15, 4–8.

Bernstein, P., 1993, Capital Ideas. New York: Free Press.Black, F. and M. Scholes, 1973, “The Pricing of Options and Corporate Liabilities”, Journal of Political Economy 81, 637–659.Kruizenga, R., 1956, Put and Call Options: A Theoretical and Market Analysis, unpublished Ph.D. dissertation, MIT.Merton, R., 1973, “Rational Theory of Option Pricing”, Bell Journal of Economics and Management Science 4, 141–183.Samuelson, P., 1965, “Rational Theory of Warrant Pricing”, Industrial Management Review 6, 13–31.Samuelson, P. and R. Merton, 1969, “A Complete Model of Warrant Pricing That Maximizes Utility”, Industrial Management Review 10, 17–46.Sprenkle, C., 1961, “Warrant Prices As Indicators of Expectations and Preferences”, Yale Economic Essays 1, 178–231.

MIT OpenCourseWarehttp://ocw.mit.edu

15.401 Finance Theory I Fall 2008

For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms.