1.mtls q4'17 oppday-final 20.2.18

TRANSCRIPT

update

CAC Ratification

Financial Highlights

Unit: MB 4Q17 4Q16 YoY% 3Q17 QoQ%

New Loan Amount 16,834 11,524 46.07% 15,253 10.36%

Loan Receivables 35,622 23,541 51.32% 32,332 10.18%

Total Revenue 2,174 1,402 55.06% 1,968 10.47%

Net Profit 743 483 53.83% 650 14.30%

2014 2015 2016 2017 YoY

New Loan Amount 12,471 20,232 37,717 58,039 53.88%

Loan Receivables 7,448 12,630 23,541 35,622 51.32%

Total Revenue 1,856 2,559 4,471 7,470 67.07%

Net Profit 544 825 1,464 2,501 70.83%

1

Share Capital Information

Price (Dec 29, 2017) : 38.75 THB

Hi/Low : 43.75 / 27.50

No. of shares : 2,120 M

Market Capitalization : 82,150 MB

P/E (X) : 36.66P/BV (X) : 9.97

MSCI Global Small Cap Index

Major Shareholders (Nov 17, 2017)

Mr. Chuchat Petaumpai 33.97%

Mrs. Daonapa Petampai 33.96%

Others 11.38%

Public 20.69%

Board of Directors

1. Admiral Apichart Pengsritong Chairman

2. Mr. Chuchat Petaumpai Director

3. Mrs. Daonapa Petampai Director

4. Mr. Yodhin Anavil Director

5. Mrs. Kongkeaw Piamduaytham Director

6. Mr. Kampol Tatiyakavee Director

7. Mrs. Nongnuch Dawasuwan Director

Audit Committee

1. Mrs. Kongkeaw Piamduaytham Chairman of the Audit Committee

2. Mr. Kampol Tatiyakavee Audit Committee

3. Mrs. Nongnuch Dawasuwan Audit Committee

Ms. Monthon Onphan as Company Secretary

Mr. Chaloem Inhoum as Audit Committee Secretary

2

Contents

Company Profile

Business Operation

Industry Overview

Financial Highlights

3

2015

Company History

2003

1992

1998

2001

Established in May 22, 1992 to provide motorcycle hire purchase business under the name “D.S. Leasing Co.,Ltd.” by Mr. Chuchat Petaumpai and Mrs. Daonapa Petampai

Started providing Motorcycle Title Loans Terminated Motorcycle Hire Purchase business

Started providing Tractor Title Loans Changed name to “Muangthai Leasing Co.,Ltd.”

Started providing Car Title Loans

2006 Started operating Personal Loans under supervision of the Bank of Thailand Invested in 99.99% of “Muangthai Leasing Insurance Broker Co., Ltd.”

2014

2016

Expanded to 506 branches Listed in Stock Exchange of Thailand

Started Nano Finance Started Land Title Loans Expanded to 940 branches Received BBB Tris Rating

4

Expanded to 1,874 branches First branch in Bangkok Announced Anti corruption

Calculated in SET 50 Thailand Nominated for CNBC Asia Business Leaders Award Expanded to 2,424 branch CG 4 stars

2017

Type of Services

Motorcycle Title Loan Car Title Loan Tractor Title Loan Land Title Loan (June 2015)

Occupation Individuals Individuals Farmers Farmers

Vehicle Type

Credit Line Baht 3,000-30,000 Baht 30,000 – 400,000 Baht 10,000 – 200,000 Baht 5,000 – 200,000

Age of vehicle Not exceed 12 years Not exceed 25 years Depend on the condition of engine -

Installments 10-24 months 10-24 months : credit line < Baht 30,000 12-50 months : credit line ≥ Baht 30,000

4 months 12 – 50 momths

1. Secured Loan 2. Unsecured Loan■ Use vehicle title and land title as collateral■ The Company offers loan service to low income individuals

that have no access to financial services from commercial bank but have ownership in vehicle and land

■ Ownerships of vehicle and land are not transferred to the Company but the borrowers have to surrender their titles to the Company and sign in the transfer document (Blank Transfer) in exchange for loan granted

■ The borrowers can possess their assets as usual

Personal Loan■ The Company offers personal loan only to existing

customers who have good payment record■ Credit Line is limit at Baht 20,000■ Under supervision of Bank Of Thailand

Nano finance (July 2015)■ Credit Line is limit at Baht 30,000■ Under supervision of Bank Of Thailand

5

Loan Approval

Notification

Credit Approval Process

Qualification of Customer

Qualification of Guarantor

Collateral

Type of Vehicle

Brand and Model

Age of Vehicle

Vehicle Condition

Credit Approval Checklist

Loan Agreement

Ownership Transfer Memo

Ownership Transfer Form

Power of Attorney

In case of Car or Agricultural vehicle title loan or motorcycle title loan that value Baht 30,000 and more, the approval must be granted by branch manager or regional manager.

In case of Car or Agricultural vehicle title loan or motorcycle title loan that value Baht 30,000 and more, the approval must be granted by branch manager or regional manager.

LoanApproval

LoanApproval

Verify Customer,Guarantor and

Collateral

Verify Customer,Guarantor and

CollateralDetermineCredit LineDetermineCredit Line

DocumentPreparationDocument

Preparation

In case of motorcycle title loan value below Baht 30,000, credit analyst can approve such loan in accordance with credit approval table.

In case of motorcycle title loan value below Baht 30,000, credit analyst can approve such loan in accordance with credit approval table.

6

MTLS has 6 own auction centers for selling the collateral vehicle repossessed from

the customers.

Chonburi Auction Center

Ayudhya Auction Center

Khonkaen Auction Center

Phitsanulok Auction Center

Repossession and Auction Process

• Customer pasts due more than 2 months

• The Company could repossess the collateral vehicle from the customer (must be granted an approval from Branch Manager)

• Head of debt collection unit gathers the collateral vehicle from branches and deliver them to the auction centers.

• The auction centers are responsible for selling of the collateral vehicles.

7

Nakhon RatchasimaAuction Center

Distribution Channel and Target

2014

506

Total 2,424 Branches 2015

940

2016

1,664

2018(F)

2,800

6 million people 324 branches

22 million people 716 branches

28 million people 1,197 branches

10 million people 187 branches

Thailand’s Geography77 cities/877 towns/7,255 villages

• 4Q17 total 2,424 branches• All branches linked online, real time• Well positioned in urban and rural markets• Leading player across retail loan categories

Growing Potential

8

2017

2,424

2019(F)

2020(F)

3,400

4,000

Branches

Full Branch Service Center

Branch Sub Branch Service Center

CAPEX (Baht) 800,000 400,000 250,000

PAYBACK PERIOD 1 YR9

Sub Branch

Motocycle, 54.02%

Other Vehicles, 5.00%

Car, 40.98%

Vehicle Title Loan Industry & New Loan Lending

0

10

20

30

40

2013 2014 2015 2016 2017

19.95 20.31 20.50 20.47 20.69

13.02 13.79 14.42 15.00 15.70

1.63 1.74 1.81 1.86 1.92

Motorcycle Car Others

Million

Source : Department of Land transport

Proportion of Vehicle Registration as of December, 31 2017Accumulated Number of Vehicle Registration

New Loan Amount Number of New Contracts

0

20,000

40,000

60,000

2013 2014 2015 2016 2017

9,84012,471

20,232

6,95211,8508,75014,10210,491

15,25311,524

16,834

Q1 Q2 Q3 Q4

0

1,000,000

2,000,000

3,000,000

2013 2014 2015 2016 2017

717,790848,859

1,194,005

364,981538,627

432,079647,360

501,090

699,425534,185

761,871

Q1 Q2 Q3 Q4

Contracts +42.62% YoY+8.93% QoQMillion Baht

+46.07% YoY+10.36% QoQ

10

37,7171,832,335

2,647,28358,039

14.72 13.43 14.15 14.69 12.98 13.43 13.54 14.15 13.86 14.32 14.09 14.69

24.6521.52

27.17 26.8024.96

28.31 27.71 27.7025.29

27.56 26.5927.78

0

10

20

30

2014 2015 2016 2017 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17

Loan receivable per branch New loan per branch

Million Baht

Loan Receivables and No. of Branches

Million Baht Branches

0

6,000

12,000

18,000

24,000

30,000

36,000

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

5,083 5,903 7,526 10,555 10,876 11,758 12,564 13,440 609 1,310

3,862

7,779 8,558 9,589

10,553 11,671

134 200 538

1,136 1,280 1,463

1,649 1,733

10 34 340

1,037 1,324

1,667 2,234

2,844

252

2,583 3,331

4,057 4,483

4,921

111

451 603

772 849

1,013

Motorcycle Car Agricultural Vehicle Personal Loan Land Nano

Loan Receivables classified by Types of LoanMillion Baht

Loan Receivables

Personal Loan7.98%

Nano2.85%

Motorcycle37.73%

Car32.76%

Tractor4.86%

Land13.82%

Proportion of Loan Receivables as of December, 31 2017

(Figure is annualized)

Average New Loan and Loan Receivables per Branch

506 940

11

1,8741,664

7,448

12,630

23,54135,622

25,972

29,306

32,33235,622

506

940

1,664

2,4241,874

2,0462,294

2,424

-

1,000

2,000

3,000

0

9,000

18,000

27,000

36,000

45,000

2014 2015 2016 2017 1Q17 2Q17 3Q17 4Q17

Loan receivable Number of branch

1,664 1,5151,2361,114 2,046 2,294 2,4242,424

0

500

1,000

1,500

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

179.5 182.4 216.0419.3

466.7 550.6604.7 690.2

142.6 142.6 119.6

226.4 285.9372.4

435.9480.8

277.86%318.04%287.61% 257.35%265.32%267.11% 274.72% 265.41%

116 102 117 251 284 345 379 441

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

87.05% 89.57%91.89% 91.49%91.25% 90.88% 90.78% 90.77%

10.96% 9.06% 7.18% 7.44% 7.66% 7.94% 8.05% 7.99%

1.99% 1.37% 0.92% 1.07% 1.09% 1.18% 1.17% 1.24%

Overdue less than 30 days Overdue 31-90 days Overdue more than 90 days

Asset Quality Ratio

Loan Receivables Classified by Aging

Loan Receivables Quality

5.52%

4.36%

2.65% 2.74% 2.90% 3.15% 3.22% 3.29%

0%

2%

4%

6%

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

Credit cost = Allowance for doubtful / Total loans

Aging Rate of allowance for doubtful accounts

Current and past due for not more than 30 days

1%

Past due for 31 - 90 days 2%

Past due for more than 90 days 100%

Receivables transferred to litigation 100%

1. Allowance for Doubtful Account by Aging

2. Additional provision for potential uncollectible receivables (General Reserve) : calculated by PD x LGD

Allowance for Doubtful AccountMillion Baht

Allowance for doubtful account by Aging

Additional provision for uncollectible receivables Non performing loans

coverage ratio = allowance for doubtful / NPL

645.7

322.1 325.0 335.6

12

752.6923.0

Loan Receivables Classified by Aging calculated from Net Loan / Total Net Loan Net Loan = Loan receivables – unearned interest income

1,040.61,171.0

0

2,000

4,000

6,000

8,000

10,000

2013 2014 2015 2016 2017

1,548 1,8562,559

8651,5631,0031,7651,201

1,9681,402

2,174

Q1 Q2 Q3 Q4

Total Revenues Revenues Structure

Million Baht

Operating Results

Interest Income and Management Fee

Million Baht

0

2,000

4,000

6,000

8,000

2013 2014 2015 2016 2017

1,301 1,5672,225

7691,415

897

1,6001,083

1,7961,270

1,984

Q1 Q2 Q3 Q4

+55.06% YoY+10.47% QoQ

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

84.0% 84.5% 87.0% 90.6% 90.5% 90.7% 91.3% 91.3%

15.4% 15.1% 12.4% 9.1% 9.1% 8.7% 8.4% 8.3%

0.6% 0.5% 0.7% 0.3% 0.4% 0.6% 0.3% 0.4%

Interest Income & Management fee Fee and Service Income Other income

• Total Revenues are new high due to branch expansions

• Interest Income and Management Fee takes a significant portion in Revenue Structure

• Focus on Interest Income instead of Fee and Service Income

+56.22% YoY+10.47% QoQ

13

4,019

4,471

7,470

6,795

25.21% 23.97% 23.48% 23.91% 23.53% 23.88% 24.07% 24.15%

5.98% 4.96%2.83% 3.06% 2.74% 2.93% 3.27% 3.31%

19.23% 19.01%20.65% 20.85% 20.79% 20.95% 20.80% 20.84%

0%

5%

10%

15%

20%

25%

30%

2014 2015 2016 2017 1Q17 2Q17 3Q17 4Q17

Interest Income Ratio Interest Expense Ratio Interest Spread

Net Profit

Million Baht

Net Profit Margin and Return on EquityInterest Income Ratio, Interest Expense Ratioand Interest Spread

Operating Results-Profitable Growth

29.32%32.24% 32.74%

33.47%32.34%

29.94%33.37%34.45% 34.30%

32.37% 33.05%34.16%

15.45% 15.34%

23.72%

31.99%

19.34%20.46%

26.69%

29.94% 30.82% 30.84%32.88%

34.59%

0%

10%

20%

30%

40%

2014 2015 2016 2017 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17Net Profit Margin Return on Equity

Million Baht

Operating Expenses

0

1,000

2,000

3,000

2014 2015 2016 2017

544825

280

536300

571401

650483

743

Q1 Q2 Q3 Q4

+53.83% YoY+14.30% QoQ

* Calculated by averaging the four quarters.

Cost to income = (S&A + Loss on disposal of asset foreclosed) / (Total revenue – FC)

14

1,464

8961,275

2,000

2,994

392 459 541 608 628 710 805 869

56.35%54.68%

48.42%44.14% 49.05%

49.28%

48.58%

46.77%43.57%

43.96%

45.25%

44.28%

0%

20%

40%

60%

0

1,000

2,000

3,000

4,000

2014 2015 2016 2017 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17

Operational Expense % Cost to Income

**

2,501

*

0

10,000

20,000

30,000

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

15.73% 15.70% 46.95% 26.60% 36.09% 50.55%

64.64%61.34%

78.37% 78.40% 7.92%

13.65%13.54%

13.96%

12.48% 13.85%

5.90% 5.90%45.13%

59.75%50.37%

35.49%

22.88%24.81%

Long-term Loans Current of Long-term Loans Short-term Loans

Bank Loan Total Liabilities

Times

Debt to Equity RatioShareholders’ Equity

Million Baht

Financial Position – Low DE , Potential to Grow

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

4,079 3,671

7,431

17,73319,585

22,44725,062

28,009Million Baht Million Baht

-

5,000

10,000

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

1,937

5,1065,652

6,6927,228

7,588 8,2388,943

2.11

0.72

1.31

2.65 2.712.96 3.04 3.13

0.00

1.00

2.00

3.00

4.00

2013 2014 2015 2016 1Q17 2Q17 3Q17 4Q17

3,919 3,489

15

17,21718,838

7,135

21,85624,444

27,091

No. MTLS Year 17 Year 16 % 4Q17 4Q16 %

1. Net loan receivables 35,622.57 23,541.24 51.32 35,622.57 23,541.24 51.32

2. Allowance for doubtful account 1,170.98 645.64 81.37 1,170.98 645.64 81.37

3. NPL 441.20 250.88 75.86 441.20 250.88 75.86

4. Allowance/NPL (2/3) 265.41% 257.35% 265.41% 257.35%

5. NPL/ Net AR (3/1) 1.24% 1.07% 1.24% 1.07%

6. Write off 15.42 21.66 (28.81) 6.87 5.14 33.66

7. NPL+Write off (3+6) 456.62 272.54 67.54 448.07 256.02 75.01

8. NPL+Write off / Net AR (7/1) 1.28% 1.16% 1.26% 1.09%

9. Total asset 36,953.01 24,425.58 51.29 36,953.01 24,425.58 51.29

10. Total liabilities 28,009.69 17,733.29 57.95 28,009.69 17,733.29 57.95

11. Total equity 8,943.32 6,692.28 33.64 8,943.32 6,692.28 33.64

12. D/E ratio (10/11) 3.13 2.65 3.13 2.65

Summary of Significant Figure Year 16 & 4Q16 (Position)

Fundamental

16

Growth

No. MTLS Year 17 Year 16 % 4Q17 4Q16 %20. Doubtful account 665.69 310.07 114.69 161.87 86.60 86.92

21. Doubtful account & write off (6+20) 681.11 331.73 105.32 168.74 91.74 83.93

22. Total employees 5,880 4,185 40.50 5,880 4,185 40.5023. Total branches 2,424 1,664 45.67 2,424 1,664 45.6724. New loan per employee (annualized) (15/22)*4 9.87 9.01 9.52 11.45 11.01 3.9625. New loan per branch (annualized) (15/23)*4 23.94 22.67 5.63 27.78 27.70 0.27

26. Net loan receivables per employee (1/22) 6.06 5.63 7.70 6.06 5.63 7.70

27. Net loan receivables per branch (1/23) 14.70 14.15 3.88 14.70 14.15 3.88

Efficiency

Summary of Significant Figure Year 16 & 4Q16 (Position) continued

No. MTLS Year 17 Year 16 % 4Q17 4Q16 %

13. Net loan receivables 35,622.57 23,541.24 51.32 35,622.57 23,541.24 51.32

14. Total revenue 7,470.07 4,472.00 67.04 2,174.46 1,401.66 55.13

15. Accumulated new loan amount 58,038.73 37,716.72 53.88 16,833.64 11,524.44 46.07

16. Interest and fee income 6,794.92 4,019.34 69.06 1,984.33 1,270.31 56.21

17. Fee and service income 642.03 436.07 47.23 179.95 126.89 41.82

18. Net profit 2,500.60 1,464.14 70.79 742.97 482.91 53.85

19. % Net profit / Total revenue (18/14) 33.47 32.74 34.16 34.45

17

Missions

1. To grow 40% in all dimensions– New Loan to grow 40%– Account Receivables to grow 40%– Net Profit expected to follow

2. To hit a total of 2,800 branches 3. To maintain NPL not exceed 1.5%

18

Business Plan for 2018

4 Highest

• Highest New Loan• Highest Account

Receivables• Highest Number of

Branches• Highest Net Profit

Business Plan for 2018 : MTLS Highlights in Microfinance

19

2 Lowest

• Lowest NPL = 1.20%• Lowest affected by

IFRS9Coverage Ratio now > 260%

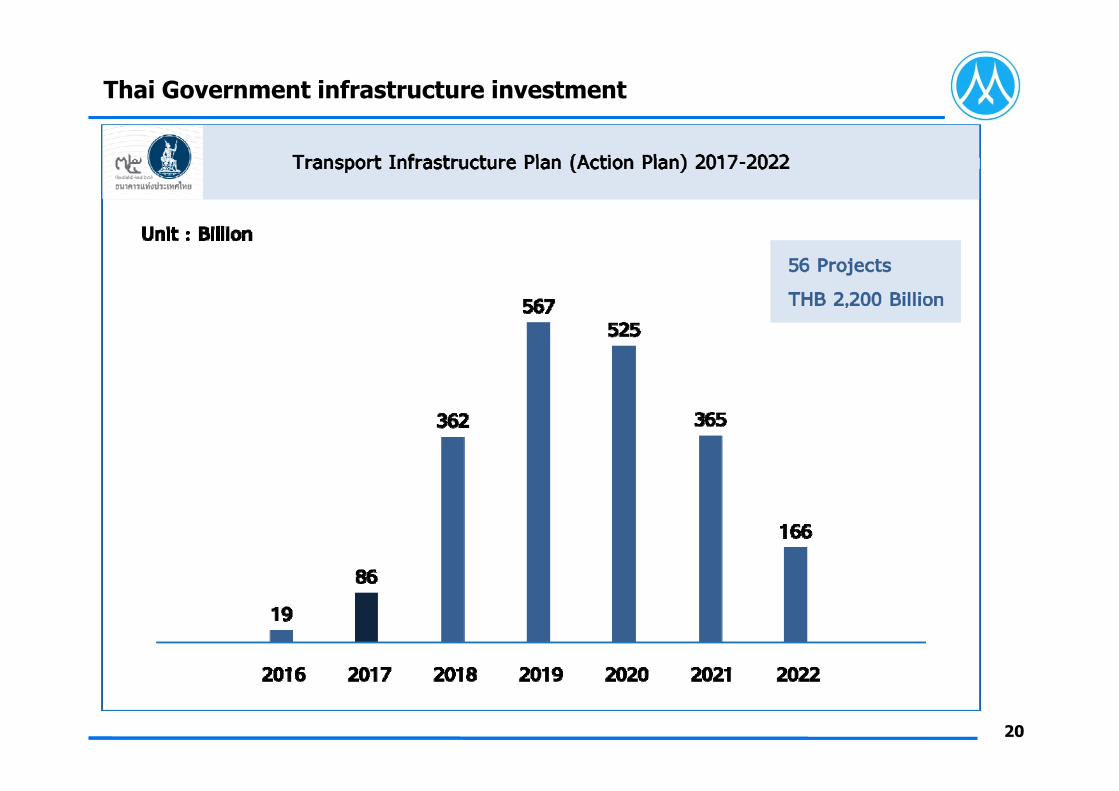

Thai Government infrastructure investment

20

Thailand’s Eastern Economic Corridor (EEC)

21

Social Responsibility

Corporate:Education: Construction of 2 rural schools in 4Q17 with a total cost of 2.25 MB. The project is called “My new home”, so far 9 schools have been built since 2011.

Family:Private donation of 40 MB in 2Q15 to a hospital in Sukhothai to build an Emergency Department and a Patient Building.

Private donation of 65 MB in 3Q16 to Chiang Mai University to construction a new Economic Department building.

Private donation of 50 MB in 1Q17 to a hospital in Sukhothai to purchase medical equipments.

22CG SCORE

Religion : A host for 4 temple constructions in 4Q17 with a total collected donation of 4.10 MB. The temple were in Khonkaen , Buriram , Kanchanaburi and Uttaradit. This annual event began in 1996.

CAC Ratification