1q 2016 emea isg outsourcing index®

TRANSCRIPT

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

1

Hosted by:

John King

Bank of America Merrill Lynch

18 April 2016

The ISG Outsourcing Index®

First Quarter 2016

EMEA Market Data and Insights

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

2

Covering the state of the outsourcing industry for EMEA commercial contracts.*

Welcome to the 54th Quarterly ISG Outsourcing Index® Review

Bernd SchaeferPartner

John KeppelPartner & President

*Contracts with ACV ≥ €5M from the ISG Contracts Knowledgebase®

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

3

At a GlanceGLOBAL MARKET ACV UP 20% Y/Y

WITH SMALLER AWARDS DRIVING MARKET GROWTH

NUMBER OF RESTRUCTURING AWARDS SETS QUARTERLY RECORD,

WHILE RESTRUCTURING ACV SURGES ALMOST 50% Y/Y

AMERICAS UP 30% ON BEST QUARTERLY PERFORMANCE IN FOUR YEARS

EMEA UP 19% Y/Y WITH STRONG SHOWING IN THE RESTRUCTURING MARKET

ASIA PACIFIC ACV AND NUMBER OF AWARDS DOWN Y/Y;

EXTENDED WEAKNESS ACROSS MANY GEOGRAPHIC MARKETS

Scorecard 1Q16 1Q Y/Y 1Q Q/Q 1Q16 1Q Y/Y 1Q Q/Q

ACV (€B)* Change Change Counts Change Change

Global Market Totals € 4.9 20% -12% 404 32% 13%

Mega-relationships € 0.9 -3% -49% 5 -29% -38%

By Type New Scope € 2.6 4% 0% 231 11% 3%

Restructurings € 2.2 48% -23% 173 78% 31%

By Scope ITO € 3.4 24% -21% 301 51% 20%

BPO € 1.5 12% 17% 103 -4% -2%

By Region Americas € 2.2 30% 6% 217 49% 47%

EMEA € 2.2 19% -26% 160 28% -6%

Asia Pacific € 0.4 -13% -4% 27 -23% -29%

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

4

Global Market ACV is up 20% Y/Y, and smaller awards drive market growth;

ACV approaches €5B level, while number of awards exceeds the 400 mark.

Broader Market Quarterly ACV (€B)*

Broader Market Quarterly Contract Counts

Global Market Contract Award Trends

€ 4.9 € 5.5

€ 4.4 € 4.9

€ 4.1

€ 5.3 € 4.6

€ 5.4 € 5.2

€ 4.0

€ 5.1

€ 3.2

€ 4.9 € 4.6 € 4.8 € 5.2 € 5.9 € 6.1

€ 5.5

€ 3.8

€ 19.7 € 19.4 € 17.5

€ 19.6 € 21.2

1Q164Q3Q2Q1Q154Q3Q2Q1Q144Q3Q2Q1Q134Q3Q2Q1Q124Q3Q2Q11

Quarterly ACV TTM ACV Totals

404 356 336

446

306

387

295

376 358 325

378

233

323 313 263

313 370

332 313 275

15421364129412121290

1Q164Q3Q2Q1Q154Q3Q2Q1Q144Q3Q2Q1Q134Q3Q2Q1Q124Q3Q2Q11

Quarterly Counts TTM Count Totals

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

5

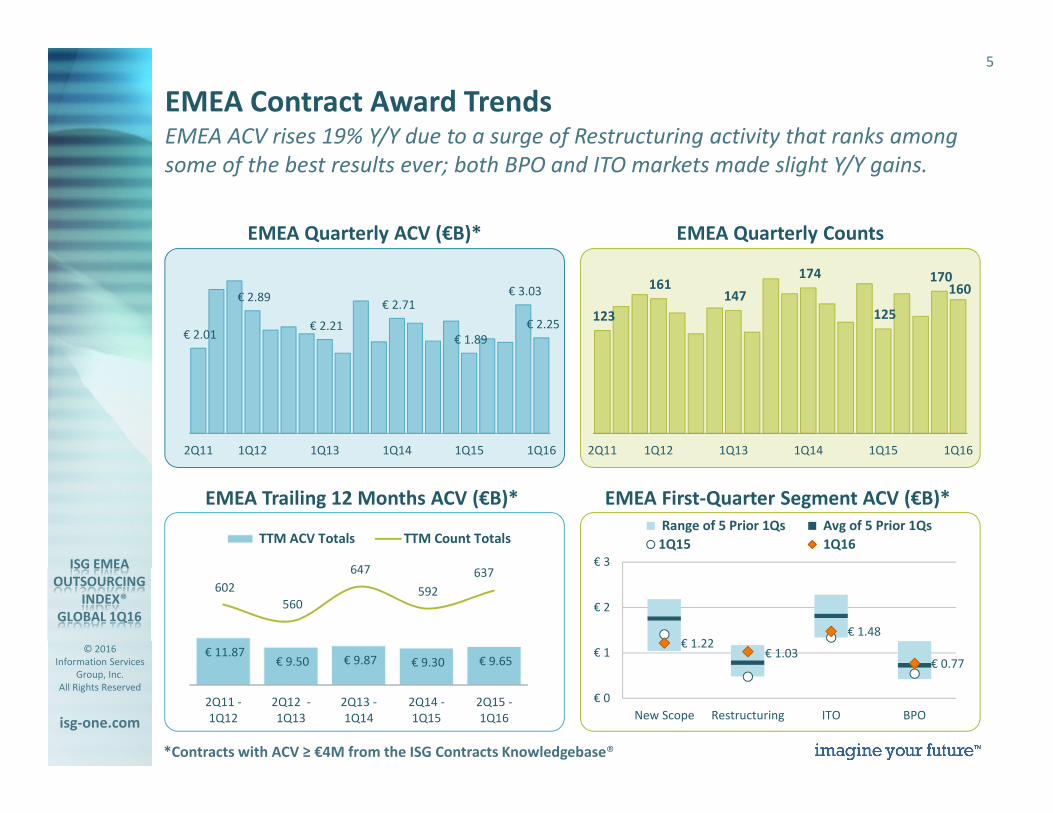

EMEA ACV rises 19% Y/Y due to a surge of Restructuring activity that ranks among

some of the best results ever; both BPO and ITO markets made slight Y/Y gains.

EMEA Quarterly Counts

EMEA Contract Award Trends

EMEA Quarterly ACV (€B)*

EMEA First-Quarter Segment ACV (€B)* EMEA Trailing 12 Months ACV (€B)*

€ 1.22 € 1.03

€ 1.48

€ 0.77

€ 0

€ 1

€ 2

€ 3

New Scope Restructuring ITO BPO

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs

1Q15 1Q16

€ 2.25

€ 3.03

€ 1.89

€ 2.71

€ 2.21

€ 2.89

€ 2.01

1Q161Q151Q141Q131Q122Q11

160 170

125

174

147 161

123

1Q161Q151Q141Q131Q122Q11

€ 9.65 € 9.30 € 9.87 € 9.50 € 11.87

637

592

647

560

602

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

TTM ACV Totals TTM Count Totals

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

6

U.K. and France inch up Y/Y, while Nordics and Southern Europe make larger gains.

DACH market ACV down Y/Y though number of DACH awards increases over 30% Y/Y.

EMEA Sub-Regions First-Quarter ACV (€B)*

EMEA Industry First-Quarter ACV (€B)*

EMEA Contract Award Trends Detail

€ 0.89

€ 0.28

€ 0.55

€ 0.09 € 0.12 € 0.10 € 0.22

€ 0.01 € 0.0

€ 0.2

€ 0.4

€ 0.6

€ 0.8

€ 1.0

€ 1.2

€ 1.4

U.K. & Ireland DACH Nordics Benelux France Africa &

Middle East

Southern

Europe

E. Europe &

Russia

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

€ 0.67

€ 0.50

€ 0.26 € 0.25 € 0.23

€ 0.05 € 0.10 € 0.12 € 0.08 € 0.0

€ 0.2

€ 0.4

€ 0.6

€ 0.8

€ 1.0

€ 1.2

Financial

Services

Manufacturing Telecom &

Media

Travel,

Transport &

Leisure

Energy Business

Services

Consumer

Packaged

Goods

Retail Healthcare &

Pharma

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

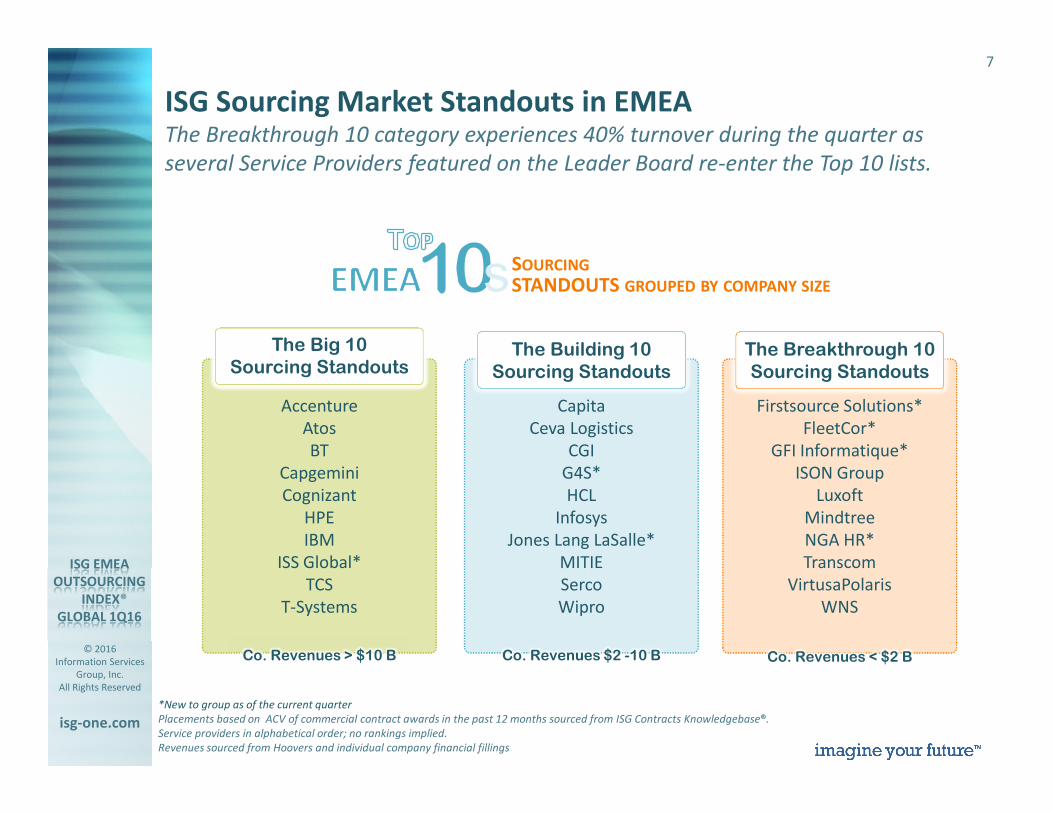

7

Firstsource Solutions*

FleetCor*

GFI Informatique*

ISON Group

Luxoft

Mindtree

NGA HR*

Transcom

VirtusaPolaris

WNS

Co. Revenues < $2 B

Capita

Ceva Logistics

CGI

G4S*

HCL

Infosys

Jones Lang LaSalle*

MITIE

Serco

Wipro

Co. Revenues $2 -10 B

Accenture

Atos

BT

Capgemini

Cognizant

HPE

IBM

ISS Global*

TCS

T-Systems

ISG Sourcing Market Standouts in EMEAThe Breakthrough 10 category experiences 40% turnover during the quarter as

several Service Providers featured on the Leader Board re-enter the Top 10 lists.

*New to group as of the current quarter

Placements based on ACV of commercial contract awards in the past 12 months sourced from ISG Contracts Knowledgebase®.

Service providers in alphabetical order; no rankings implied.

Revenues sourced from Hoovers and individual company financial fillings

Co. Revenues > $10 B

SOURCING

STANDOUTS GROUPED BY COMPANY SIZE

The Building 10Sourcing Standouts

The Breakthrough 10Sourcing Standouts

The Big 10Sourcing Standouts

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

8

Americas Quarterly Counts

Americas Contract Award Trends

Americas Quarterly ACV (€B)*

Americas First-Quarter Segment ACV (€B)* Americas Trailing 12 Months ACV (€B)*

Americas ACV rises 30% Y/Y as Restructuring activity achieves record-setting levels;

ITO ACV was best in four years, and number of ITO awards was second-best ever.

217

148 146 134 142

177

119

1Q161Q151Q141Q131Q122Q11

€ 2.2

€ 2.1

€ 1.7 € 1.7

€ 2.2

€ 2.6

€ 1.5

1Q161Q151Q141Q131Q122Q11

€ 8.4 € 7.9

€ 5.5 € 7.2 € 7.6

756

616

488 483 555

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

TTM ACV TTM Counts

€ 1.10 € 1.14

€ 1.71

€ 0.54 $0.5

$1.0

$1.5

$2.0

New Scope Restructuring ITO BPO

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs

1Q15 1Q16

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

9

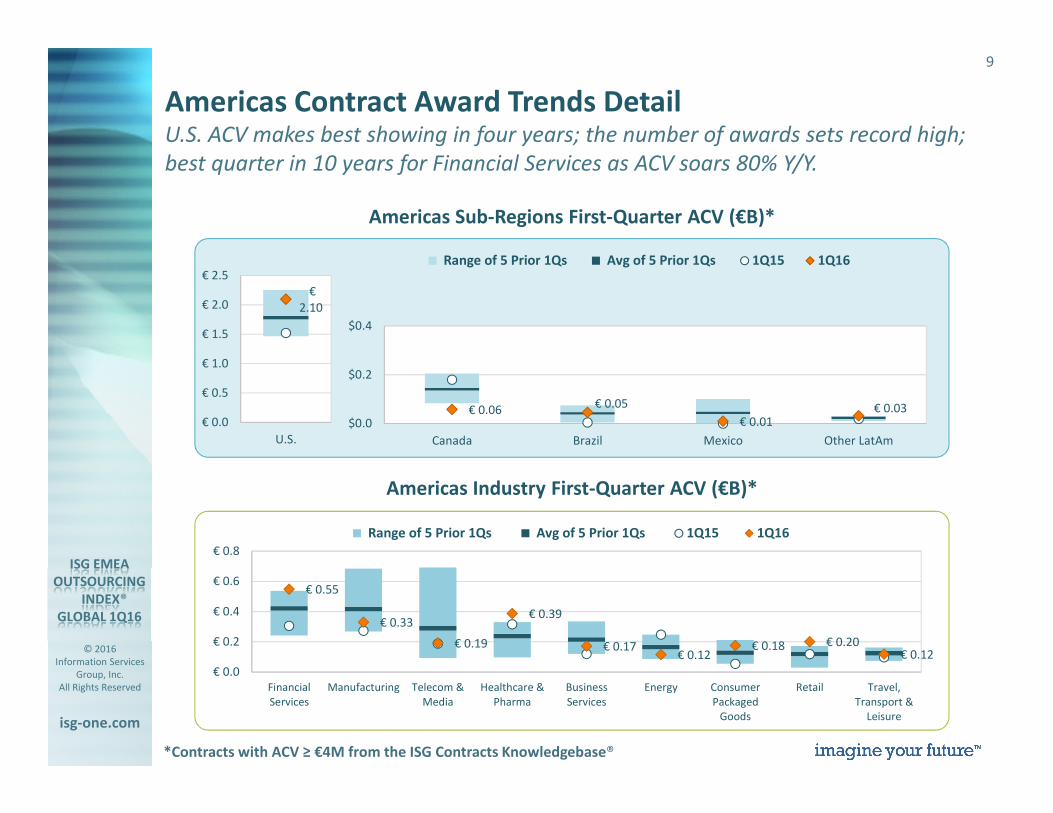

U.S. ACV makes best showing in four years; the number of awards sets record high;

best quarter in 10 years for Financial Services as ACV soars 80% Y/Y.

Americas Sub-Regions First-Quarter ACV (€B)*

Americas Industry First-Quarter ACV (€B)*

Americas Contract Award Trends Detail

€ 0.55

€ 0.33

€ 0.19

€ 0.39

€ 0.17 € 0.12

€ 0.18 € 0.20 € 0.12

€ 0.0

€ 0.2

€ 0.4

€ 0.6

€ 0.8

Financial

Services

Manufacturing Telecom &

Media

Healthcare &

Pharma

Business

Services

Energy Consumer

Packaged

Goods

Retail Travel,

Transport &

Leisure

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

€ 0.06 € 0.05

€ 0.01 € 0.03

$0.0

$0.2

$0.4

Canada Brazil Mexico Other LatAm

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

€

2.10

€ 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

€ 2.5

U.S.

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

10

Asia Pacific ACV slips 13% from a modest Q1 compare with number of contracts also

falling; both New Scope and Restructuring ACV lag Y/Y.

Asia Pacific Quarterly Counts

Asia Pacific Contract Award Trends

Asia Pacific Quarterly ACV (€B)*

Asia Pacific First-Quarter Segment ACV (€B)*Asia Pacific Trailing 12 Months ACV (€B)*

€ 1.69 € 2.20 € 2.15

€ 2.85

€ 1.67

149 156 159 169

133

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

TTM ACV TTM Counts

€ 0.33

€ 0.06

€ 0.19 € 0.19

€ 0.0

€ 0.2

€ 0.4

€ 0.6

€ 0.8

New Scope Restructuring ITO BPO

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs

1Q15 1Q16

€ 0.38 € 0.44

€ 0.84

€ 0.45 € 0.42 € 0.30

1Q161Q151Q141Q131Q122Q11

27

38 35

50

34 32 33

1Q161Q151Q141Q131Q122Q11

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

11

One large mega award helps support ANZ and Manufacturing short-term growth;

remaining geographic and vertical markets in Asia Pacific struggle to gain traction.

Asia Pacific Sub-Regions First-Quarter ACV (€B)*

Asia Pacific Industry First-Quarter ACV (€B)*

Asia Pacific Contract Award Trends Detail

€ 0.22

€ 0.02

€ 0.07

€ -

€ 0.06

€ -€ 0.00

€ 0.05

€ 0.10

€ 0.15

€ 0.20

€ 0.25

€ 0.30

ANZ India and South

Asia

Japan Greater China Southeast Asia South Korea

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

€ 0.05 € 0.04 € 0.01

€ 0.21

€ 0.04 € -

€ 0.03 € 0.01 € -€ 0.0

€ 0.1

€ 0.2

€ 0.3

Financial

Services

Telecom &

Media

Travel,

Transport &

Leisure

Manufacturing Energy Consumer

Packaged

Goods

Business

Services

Retail Healthcare &

Pharma

Range of 5 Prior 1Qs Avg of 5 Prior 1Qs 1Q15 1Q16

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

12

Special Topic First Quarter 2016

PUBLIC SECTOR OUTSOURCING

John Keppel

Partner & President

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

13

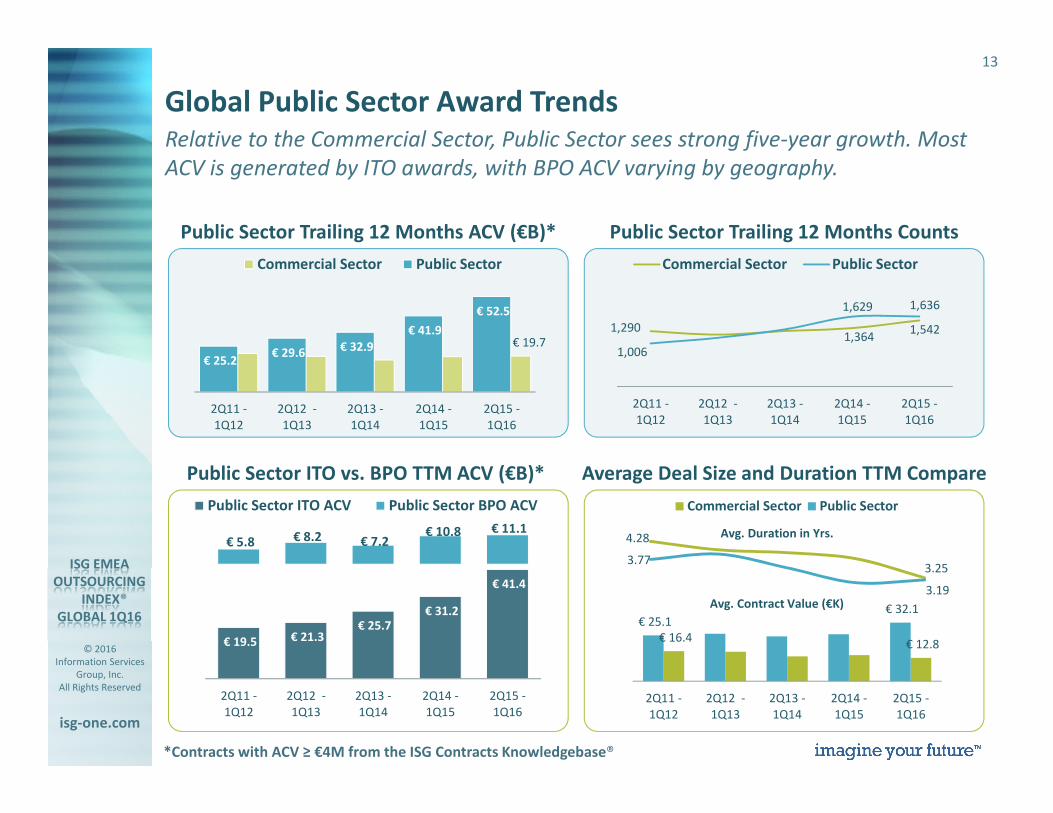

Relative to the Commercial Sector, Public Sector sees strong five-year growth. Most

ACV is generated by ITO awards, with BPO ACV varying by geography.

Public Sector Trailing 12 Months Counts

Global Public Sector Award Trends

1,542 1,364

1,290

1,636 1,629

1,006

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

Commercial Sector Public Sector

Public Sector Trailing 12 Months ACV (€B)*

Public Sector ITO vs. BPO TTM ACV (€B)*

3.25

4.28

3.19

3.77

Average Deal Size and Duration TTM Compare

Avg. Duration in Yrs.

Avg. Contract Value (€K)

€ 19.7

€ 52.5

€ 41.9

€ 32.9 € 29.6

€ 25.2

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

Commercial Sector Public Sector

€ 41.4

€ 31.2 € 25.7

€ 21.3 € 19.5

€ 11.1 € 10.8 € 7.2 € 8.2 € 5.8

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

Public Sector ITO ACV Public Sector BPO ACV

€ 12.8 € 16.4

€ 32.1 € 25.1

2Q15 -

1Q16

2Q14 -

1Q15

2Q13 -

1Q14

2Q12 -

1Q13

2Q11 -

1Q12

Commercial Sector Public Sector

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

14

Global Public Sector Award TrendsNorth America, led by federal government IT spending, accounts for a large share of

sourcing. Average deal values increase, whereas durations shorten.

Share of Public Sector ACV for Trailing 12 Months

Top Public Sector Providers

in Recent 12 Months

58%

17%5% 3%

17%

U.S. &

Canada

U.K. Continental

Europe

ANZ Other

*New to List for 2016

Service providers in alphabetical order; no rankings implied.

Placements based on counts of public sector contract awards sourced from ISG Contracts Knowledgebase ®.

U.S. & Canada ANZ

U.K. Continental Europe

Booz Allen Hamilton*

CACI*

HPE*

Lockheed Martin

Northrop Grumman

Raytheon

Science Applications

BT

Capgemini*

Capita

Carillion

CGI

Fujitsu*

G4S*

HPE

Accenture

Atea

Atos

BT*

Capgemini

HPE

Indra Sistemas

Accenture

Boeing

Harris Corp.

HPE*

IBM

Raytheon*

SingTel Optus*

Telstra*Public Sector Regional ITO vs. BPO % TTM

79%

31%

88%76%

21%

69%

12%24%

U.S. & Canada U.K. Continental

Europe

ANZ

ITO ACV BPO ACV

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

15

€ 31.4

€ 24.0

€ 15.4

€ 5.8 € 3.0

€ 4.7

€ 0.9 € 0.9 € 1.2

€ 0.3 € 0.7 € 0.6

€ 13.0

€ 6.1€ 4.1

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

Local

Government

Public

Healthcare

Other Federal

Government

Department of

Defense

U.S. Public Sector Contract Award DetailsDepartment of Defense (DoD) ITO dominates the U.S. Public Sector sourcing;

Health and Human Services (HHS) and Homeland Security (DHS) remain active.

% of DOD

Consortium

Contracts up

17 percentage pts

in Recent 12 Months

Local GovernmentCapgemini

Dell

Harris

HPE

Verizon

Public HealthcareAtos

Booz Allen Hamilton

HPE

ICF International

Kelly Services

Other Federal

GovernmentAccenture

CSC

HPE

Raytheon

Science Applications

DoD Single ProviderGeneral Dynamics

Lockheed Martin

Northrop Grumman

Science Applications

Raytheon

DoD Consortium

Participation**

BAE Systems

Booz Allen

General Dynamics

Leidos

Lockheed Martin

U.S. Activity Details by Sub-Sector

U.S. Public Sector Activity for Last 3 TTMs Top U.S. Public Sector Providers for the

Most Recent 12 Months*

*Service providers in alphabetical order; no rankings implied. Placements based on counts of contract awards in the ISG Contracts Knowledgebase ®.

**Providers who had the highest participation rates in consortiums who were awarded DOD contracts.

€ 38.4 € 28.6

€ 21.8

1,041 1,059

723

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

ACV €B Counts

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

16

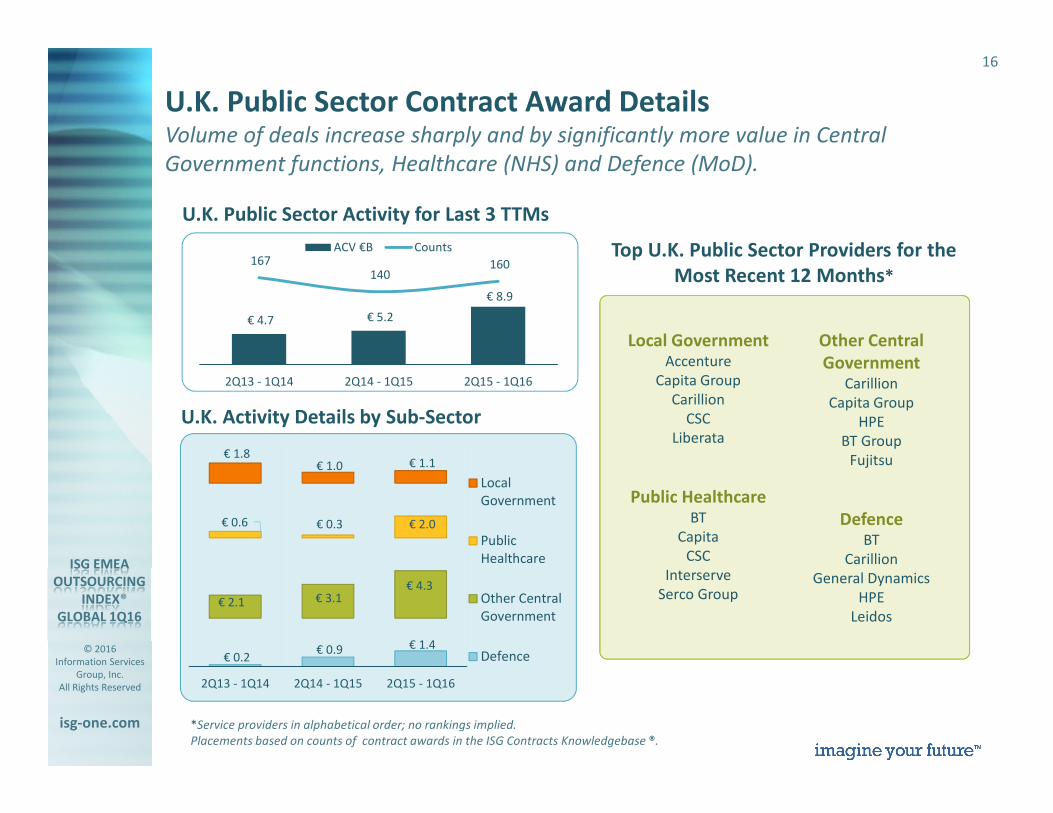

U.K. Public Sector Contract Award DetailsVolume of deals increase sharply and by significantly more value in Central

Government functions, Healthcare (NHS) and Defence (MoD).

Local GovernmentAccenture

Capita Group

Carillion

CSC

Liberata

Public HealthcareBT

Capita

CSC

Interserve

Serco Group

Other Central

GovernmentCarillion

Capita Group

HPE

BT Group

Fujitsu

DefenceBT

Carillion

General Dynamics

HPE

Leidos

U.K. Activity Details by Sub-Sector

U.K. Public Sector Activity for Last 3 TTMs

Top U.K. Public Sector Providers for the

Most Recent 12 Months*

*Service providers in alphabetical order; no rankings implied.

Placements based on counts of contract awards in the ISG Contracts Knowledgebase ®.

€ 1.4 € 0.9 € 0.2

€ 4.3 € 3.1 € 2.1

€ 2.0 € 0.3 € 0.6

€ 1.1 € 1.0 € 1.8

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

Local

Government

Public

Healthcare

Other Central

Government

Defence

€ 8.9

€ 5.2 € 4.7

160 140

167

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

ACV €B Counts

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

17

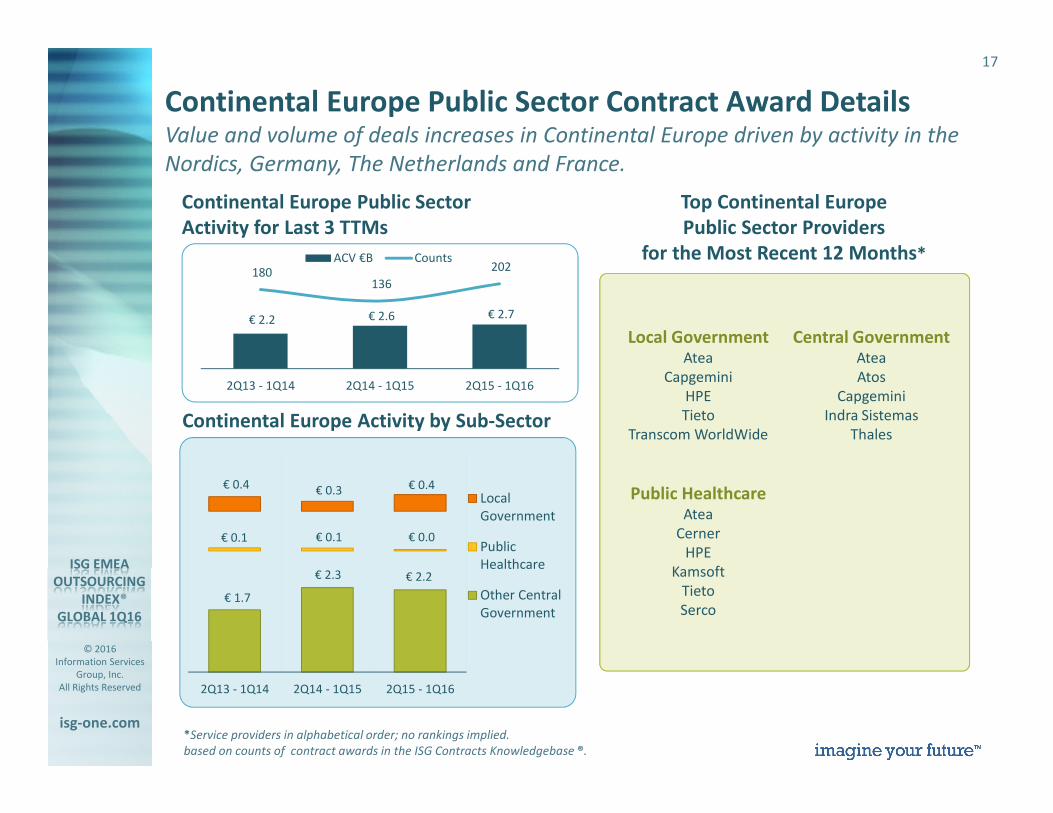

Continental Europe Public Sector Contract Award DetailsValue and volume of deals increases in Continental Europe driven by activity in the

Nordics, Germany, The Netherlands and France.

Local GovernmentAtea

Capgemini

HPE

Tieto

Transcom WorldWide

Public HealthcareAtea

Cerner

HPE

Kamsoft

Tieto

Serco

Central GovernmentAtea

Atos

Capgemini

Indra Sistemas

ThalesContinental Europe Activity by Sub-Sector

Continental Europe Public Sector

Activity for Last 3 TTMs

Top Continental Europe

Public Sector Providers

for the Most Recent 12 Months*

*Service providers in alphabetical order; no rankings implied.

based on counts of contract awards in the ISG Contracts Knowledgebase ®.

€ 2.2 € 2.3

€ 1.7

€ 0.0 € 0.1 € 0.1

€ 0.4 € 0.3 € 0.4

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

Local

Government

Public

Healthcare

Other Central

Government

€ 2.7 € 2.6 € 2.2

202

136 180

2Q15 - 1Q162Q14 - 1Q152Q13 - 1Q14

ACV €B Counts

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

18

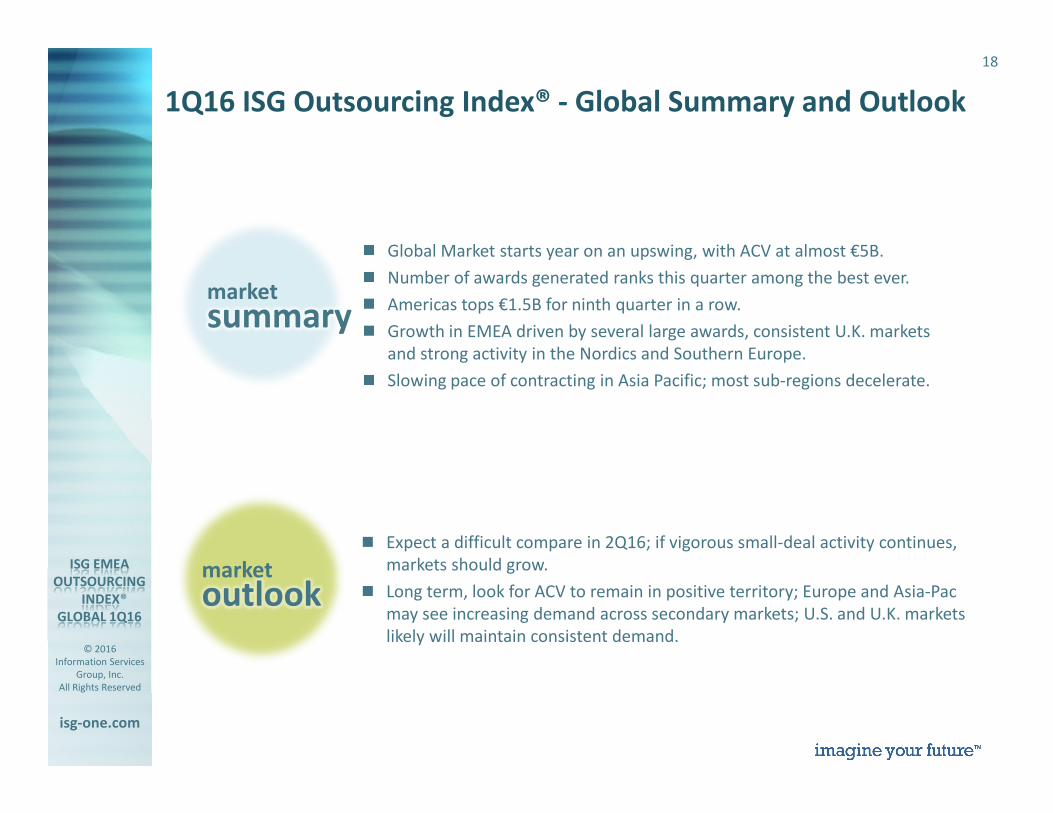

� Global Market starts year on an upswing, with ACV at almost €5B.

� Number of awards generated ranks this quarter among the best ever.

� Americas tops €1.5B for ninth quarter in a row.

� Growth in EMEA driven by several large awards, consistent U.K. markets

and strong activity in the Nordics and Southern Europe.

� Slowing pace of contracting in Asia Pacific; most sub-regions decelerate.

� Expect a difficult compare in 2Q16; if vigorous small-deal activity continues,

markets should grow.

� Long term, look for ACV to remain in positive territory; Europe and Asia-Pac

may see increasing demand across secondary markets; U.S. and U.K. markets

likely will maintain consistent demand.

1Q16 ISG Outsourcing Index® - Global Summary and Outlook

summarymarket

outlookmarket

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

19

Please contact us with your questions and comments.

Learn More

Paul ReynoldsPartner & Chief Research Officer,

ISG Momentum

+1 508 625 2194

www.isg-one.comJohn Keppel

Partner and President

+44 (0)7879 432 212

Denise Colgan

EMEA and AP Media Contact

+44 1737 371523

Bill McNeeCEO Saugatuck Technologies,

an ISG Business

+1 203 820 8987

Laura Mountain

Cohn & Wolfe for ISG

+44 (0) 20 7331 5372

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

20

First Quarter 2016

APPENDIX: SCORE CARD FOR TCV

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

21

The ISG Outsourcing Index has moved to ACV as the primary measure of the

Broader Market. We will continue to provide a high-level TCV view of the market via

a Scorecard analysis.

First Quarter 2016 TCV Scorecard

*Contracts with TCV ≥ €25M from the ISG Contracts Knowledgebase®

Scorecard 1Q16 1Q Y/Y 1Q Q/Q

TCV (€B)* Change Change

Global Market € 15.5 -12% -24%

New Scope € 10.9 -15% -4%

Restructurings € 4.6 -3% -49%

Mega-deals € 2.9 -26% -37%

ITO € 9.4 -28% -39%

BPO € 6.1 33% 22%

Americas € 5.6 -2% -25%

EMEA € 7.6 -21% -35%

Asia Pacific € 2.2 5% 107%

© 2016

Information Services

Group, Inc.

All Rights Reserved

isg-one.com

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase®

22

www.isg-one.com

Information Services Group is a leading technology insights, market intelligence and advisory services company, serving more than 500 clients around the

world to help them achieve operational excellence. ISG supports private and public sector organizations to transform and optimize their operational

environments through research, benchmarking, consulting and managed services, with a focus on information technology, business process transformation,

program management services and enterprise resource planning. Clients look to ISG for unique insights and innovative solutions for leveraging technology,

the deepest data source in the industry, and more than five decades of experience of global leadership in information and advisory services. Based in

Stamford, Conn., the company has more than 1,000 employees and operates in 21 countries.

imagine your future™

RESEARCH | CONSULTING | MANAGED SERVICES

let’s connect...