2. final accounts - adjustments

TRANSCRIPT

FINAL ACCOUNTS

ADJUSTMENT ENTRIES

The adjustments relates to the following:

Closing stock Outstanding expenses Prepaid expenses Outstanding or accrued income Income received in advance or unearned income Depreciation Bad debts Provision for bad debts Provision for discount on debtors Reserve for discount on creditors Interest on capital Interest on drawings

Rule: Any item given outside the Trial Balance will be recorded at two places on account of Dual Aspect concept.

Closing stock .The journal entry would be:Closing stock A/c Dr. To Trading A/c

Ex: Trial Balance

Stock at the end of the period is Rs 15000

Dr. Trading Account Cr.

Balance Sheet

Particulars Dr. Amt. Cr. Amt.

Opening stock

Purchases

Sales

10000

30000

40000

Particulars Amount (Rs) Particulars Amount (Rs)

To, Opening Stock

To, Purchase

To, Gross Profit

10000

30000

15000

55000

By, Sales

By Closing Stock

40000

15000

55000

Liabilities Amount Assets Amount

Closing Stock 15000

Outstanding Expenses: Expenses which have become due during the a/cing period but not paid till the end of the year. In order to ascertain true profit and loss made during the year, it is necessary that such outstanding expenses are taken into account.

Trial Balance

Additional Information:Salary for the month of December Rs 2000 has yet not been paid

Rent amounting to Rs 1000 is still outstanding.

Journal Proper

Particulars Dr. Amount Cr. Amount

Salaries A/c

Office Rent A/c

10000

5000

Date Particulars Dr. Amount Cr. Amount

Salaries A/c Dr

To Outstanding Salaries A/c

(Being Salary due but not paid)

Office Rent A/c Dr

To Outstanding Rent A/c

(Being Rent due but not paid)

2000

1000

2000

1000

Prepaid Expenses: Expenses of next accounting period paid in advance in the current accounting period.

Ex: Trial Balance

Additional Information: Insurance Premium has been paid in advance amounting to Rs.1000 for the

next year Rent Rs 500 has been paid for the next year

Journal Proper

Particulars Dr. Amount Cr. Amount

Insurance

Store Rent

8000

4000

Date Particulars Dr. Amount Cr. Amount

Prepaid Insurance A/c Dr.

To, Insurance A/c

(being Insurance Premium paid in advance)

Prepaid Rent A/c Dr.

To, Store Rent A/c

(Being Rent paid in advance)

1000

500

1000

500

Profit and Loss Account

Balance Sheet

Particulars Amount Particulars Amount

To, Salaries 10000

Add: Outstanding Salaries 2000

To, Office Rent 5000

Add: Outstanding Rent 1000

To, Insurance 8000

Less: Prepaid 1000

To, Store Rent 4000

Less Prepaid 500

12000

6000

7000

3500

Liabilities Amount Assets Amount

Outstanding Expenses:

Outstanding Salaries 2000

Outstanding O. Rent 1000 3000

Prepaid Insurance

Prepaid S. Rent

1000

500

Outstanding Income: Income which has become due but not received yet. (Asset)

Treatment: Added to the income received in the credit side of the Profit and Loss account and then shown as an asset in the Balance sheet.

Accrued Income: Income which has been earned by the business but has not become due and therefore not received yet. (Asset)

Treatment: Similar to Outstanding Income

Income Received in advance: income which has been received by the business before being earned by it. (liability)

Treatment: Subtracted from the Income received in the Credit side of the Profit and Loss account and then shown as a liability in the Balance sheet.

Ex: Trial Balance (as on 31st December,1998)

Additional Information: Interest on M.T. Loan has been received in advance to the . extent of Rs 500

Particulars Dr. Amount Cr. Amount

6% L.T. Loan

Investment in 6% Debentures in B Ltd. (Interest payable on 31/3 & 30/9)

Interest on L.T. Loan received up to 31st October, 1998

Interest on Investment

Rent received for 12 months ending 31st March, 1999

Interest on M.T. Loan

20000

30000

1000

900

1200

2000

Journal Entries:

Outstanding Interest A/c Dr. 200 To, Interest on L.T. Loan account 200Accrued Interest A/c Dr. 450 To, Interest on investment A/c 450Rent A/c Dr. 300 To, Rent received in advance A/c 300Interest on M.T. Loan A/c Dr. 500 To, Interest received in advance A/c 500

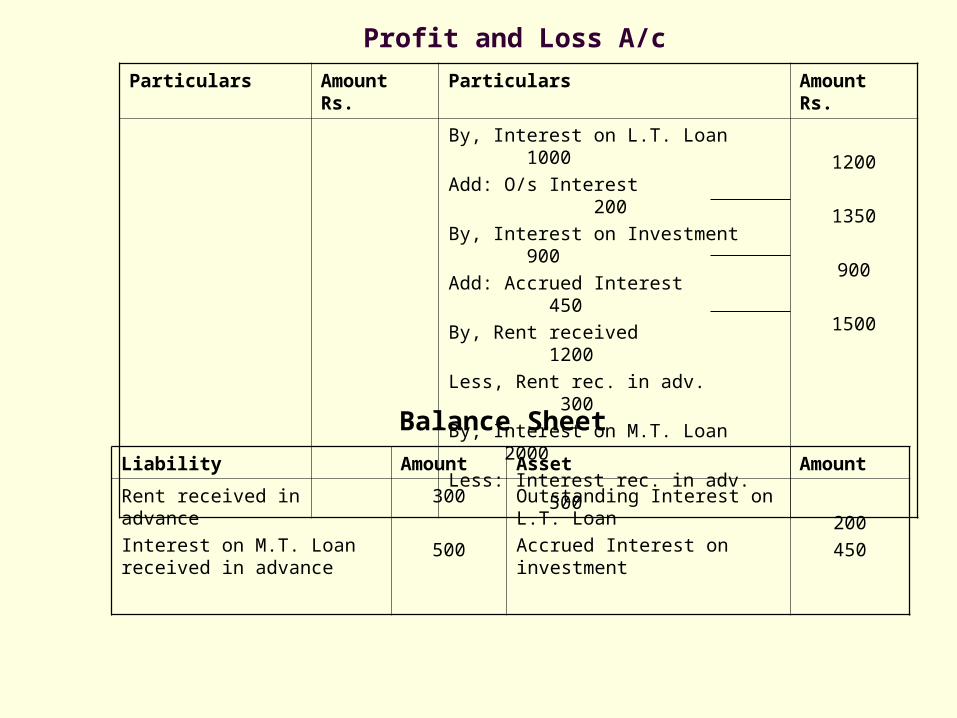

Profit and Loss A/c

Balance Sheet

Particulars Amount Rs. Particulars Amount Rs.

By, Interest on L.T. Loan 1000

Add: O/s Interest 200

By, Interest on Investment 900

Add: Accrued Interest 450

By, Rent received 1200

Less, Rent rec. in adv. 300

By, Interest on M.T. Loan 2000

Less: Interest rec. in adv. 500

1200

1350

900

1500

Liability Amount Asset Amount

Rent received in advance

Interest on M.T. Loan received in advance

300

500

Outstanding Interest on L.T. Loan

Accrued Interest on investment200

450

Depreciation:

Depreciation A/c Dr. To, Fixed Asset A/cTreatment: Calculate depreciation on the basis of the rate given. Charge this amount to the debit side of the Profit and Loss account. In the Balance Sheet, reduce the value of that asset by this amount.

Bad debts and Provision for Bad debts Bad debts A/c Dr. Profit & Loss Dr. To, Debtor’s personal A/c To, Provision for Bad debts Treatment: Charge this amount (additional bad debts) to the Debit side of the P&L A/c. If the

Trial balance already has an entry of Bad debts, ‘additional bad debts’ should be added to this amount . In the Balance Sheet, reduce the value of the Debtors by this ‘additional Bad debts’.

Add this amount (new provision for bad debts) to the ‘Bad debts’ in the Debit side of the P&L A/c. If the Trial balance already has an entry of Provision for Bad debts, this old provision should be subtracted from the total. In the Balance sheet, reduce the value of Debtors by this new ‘provision for bad debts’.

Discount to Debtors: Similar treatment like Bad debts Provision for Discount on Debtors: Similar treatment like Provision for Bad debts

Trial Balance

Additional Bad debts = 1000, Additional Discount = 500Create Provisions: Bad debts @10% & Discount @5% on Debtors

Journal Entries:

Particulars Dr. Amount Cr. Amount

Sundry Debtors

Provision for Bad debts

Provision for Discount

Bad debts

Discount

50000

3000

1000

5000

2000

Date Particulars Amount (Dr.) Amount (Cr.)

Bad debts A/c Dr.

Discount A/c Dr.

To, Sundry Debtors

Provision for Bad debts A/c Dr.

To, Bad debts A/c

Provision for Discount on debtors A/c Dr.

To, Discount A/c

Profit and Loss A/c Dr.

To, Provision for Bad Debts

To, Provision for Discount A/c

1000

500

4000

1500

5532.50

1500

4000

1500

3850

1682.50

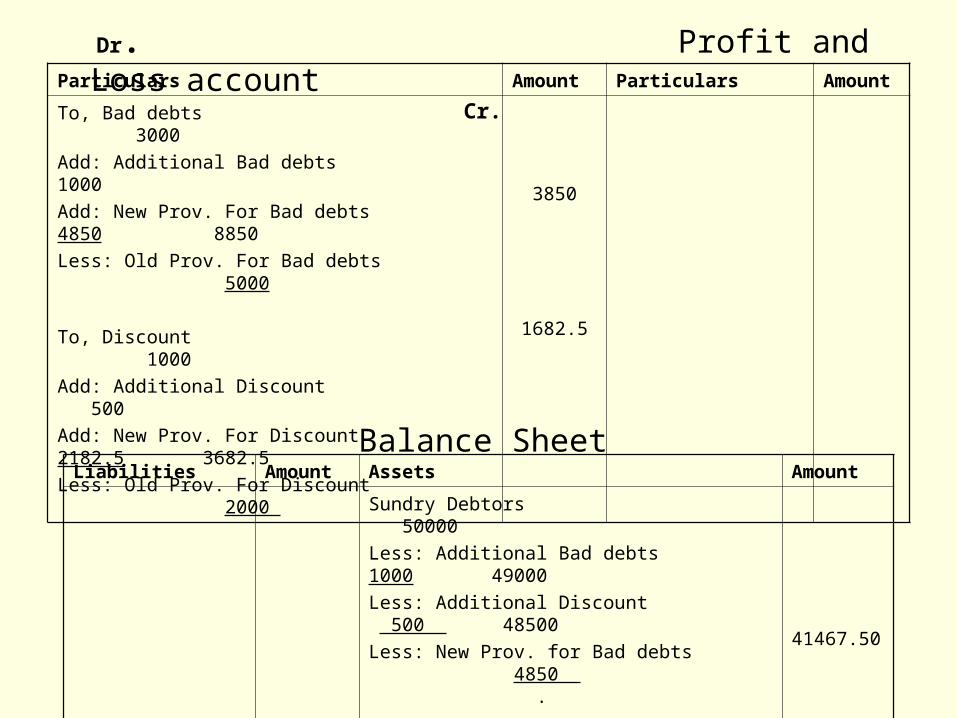

Liabilities Amount Assets Amount

Sundry Debtors 50000

Less: Additional Bad debts 1000 49000

Less: Additional Discount 500 48500

Less: New Prov. for Bad debts 4850 . 43650

Less: New Prov. For Discount 2182.5

41467.50

Particulars Amount Particulars Amount

To, Bad debts 3000

Add: Additional Bad debts 1000

Add: New Prov. For Bad debts 4850 8850

Less: Old Prov. For Bad debts 5000

To, Discount 1000

Add: Additional Discount 500

Add: New Prov. For Discount 2182.5 3682.5

Less: Old Prov. For Discount 2000

3850

1682.5

Dr. Profit and Loss account Cr.

Balance Sheet