2. strategic performance measures in the private sector txt strategic...costing, target costing,...

TRANSCRIPT

D. STRATEGIC PERFORMANCE MEASUREMENT

2. Strategic Performance measures in the private sector

a) Demonstrate why the primary objective of financial performance should be (primarily) concerned with the benefits to

shareholders. [2]

Focus notes - What is financial performance?

- Financial performance is about managing for value i.e. shareholder value measured by the value of shares which is under pinned by the assets of the business.

- Strategic performance management begins when shareholder invest in order to achieve this end. They make a choice and trade-off risk for return in their investments in the organisation that

exceeds returns that can be obtained from similar risk investments elsewhere in the market.

- It is argued that the company does not create value and justify the investment unless it produces returns that exceed the cost of capital. This is the argument of EVA.

What is financial performance? 1. Specifically, financial performance is a measure of how well an organisation uses its assets to generate revenue from its core business model.

Examples of such measures are asset turnover (Sales/total assets), inventory turnover (cost of goods sold/average inventory).

2. Financial performance is also a measure of the financial health of an organisation over a period of time. Examples of performance measures

are ROCE, ROI, EVA, etc. These measures can be used to compare the performance of one firm with another or others in the same

industry. Each of these measures relates the returns to the investments in the organisation to obtain returns that can be compared with

benchmark returns on similar risk investments elsewhere in the market. This is essential in order to evaluate whether the returns adequately

compensate shareholders for the risks they have undertaken in investing in the organisation.

Why financial performance is primarily concerned with benefits to shareholders 3. Financial performance is about managing for shareholder value - income and capital growth, which is the primary objective of investment.

Investors make choices which involve trade-offs of risk for an acceptable return to compensate them for that risk. These returns must exceed

what can be obtained elsewhere in the market from similar risk investments. If these criteria are not met investors may not invest in the

organisation or may divest if they have already invested.

4. To be effective therefore financial performance management must focus on the drivers of value in the organisation. It is argued that the

organisation does not create wealth unless it can produce returns that exceed the cost of capital invested in it. This is the argument of EVA

(Economic value added). This argument is consistent with the assumption of rational economic behaviour which underpins the investor’s

decision to trade-off higher risks for higher returns in undertaking to invest in the organisation.

What is financial performance management? 5. Financial performance management consists of setting clear financial objectives that reflect the generic strategy, setting a financial strategy

to achieve the objectives, implementing the strategy, monitoring and controlling the implementation so as to achieve the objectives in a

changing environment that achieves sustainable competitive advantage in the long term.

6. For example, if the generic strategy is to be a cost leader, the financial objective would be to minimise costs. This could translate into an

operational planning objective to reduce costs by say 5%. The financial strategy to achieve this would consist of kaizen budgeting, kaizen

costing, target costing, lean management techniques, etc. In terms of production the strategy would be to achieve economies of scale, JIT

(procurement and production). In terms of investments the strategy would be to reduce the absolute amounts of investments, invest to

enhance productivity, achieve improved market share and reduce labour costs. In terms of financing the strategy would be to minimise

financing as far as possible by say forging strategic alliances rather than go for outright acquisition.

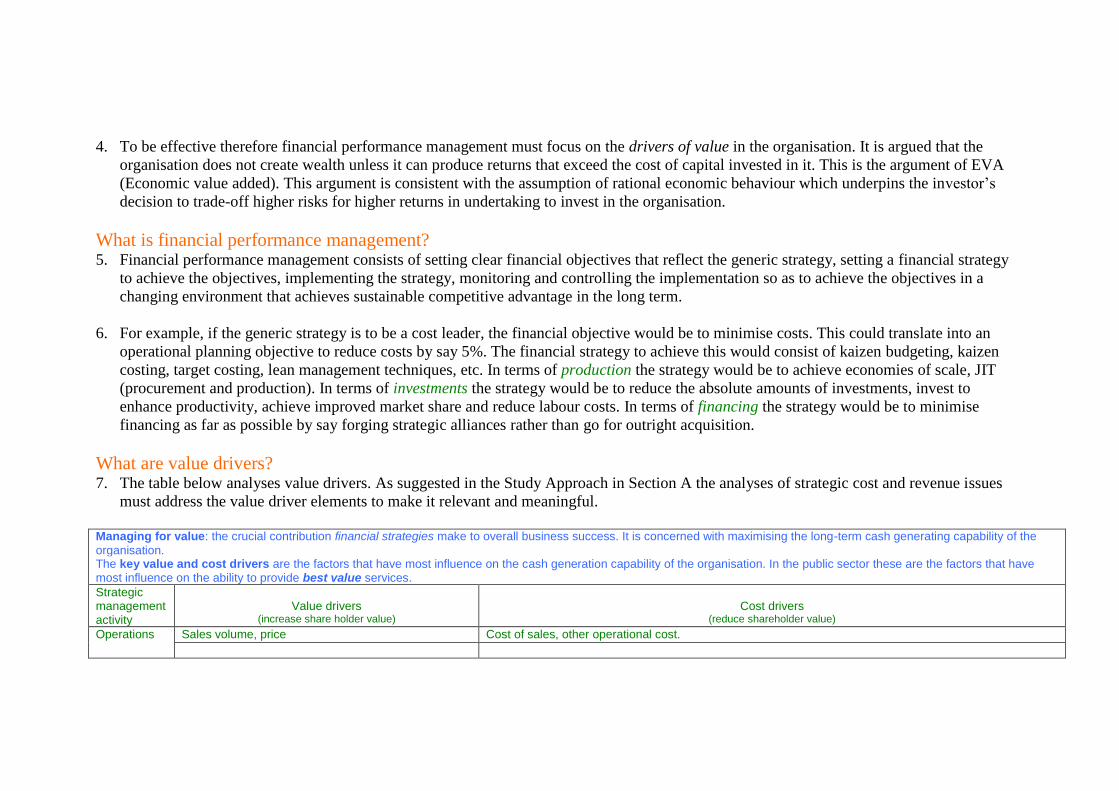

What are value drivers? 7. The table below analyses value drivers. As suggested in the Study Approach in Section A the analyses of strategic cost and revenue issues

must address the value driver elements to make it relevant and meaningful.

Managing for value: the crucial contribution financial strategies make to overall business success. It is concerned with maximising the long-term cash generating capability of the

organisation. The key value and cost drivers are the factors that have most influence on the cash generation capability of the organisation. In the public sector these are the factors that have most influence on the ability to provide best value services.

Strategic management activity

Value drivers

(increase share holder value)

Cost drivers

(reduce shareholder value)

Operations Sales volume, price Cost of sales, other operational cost.

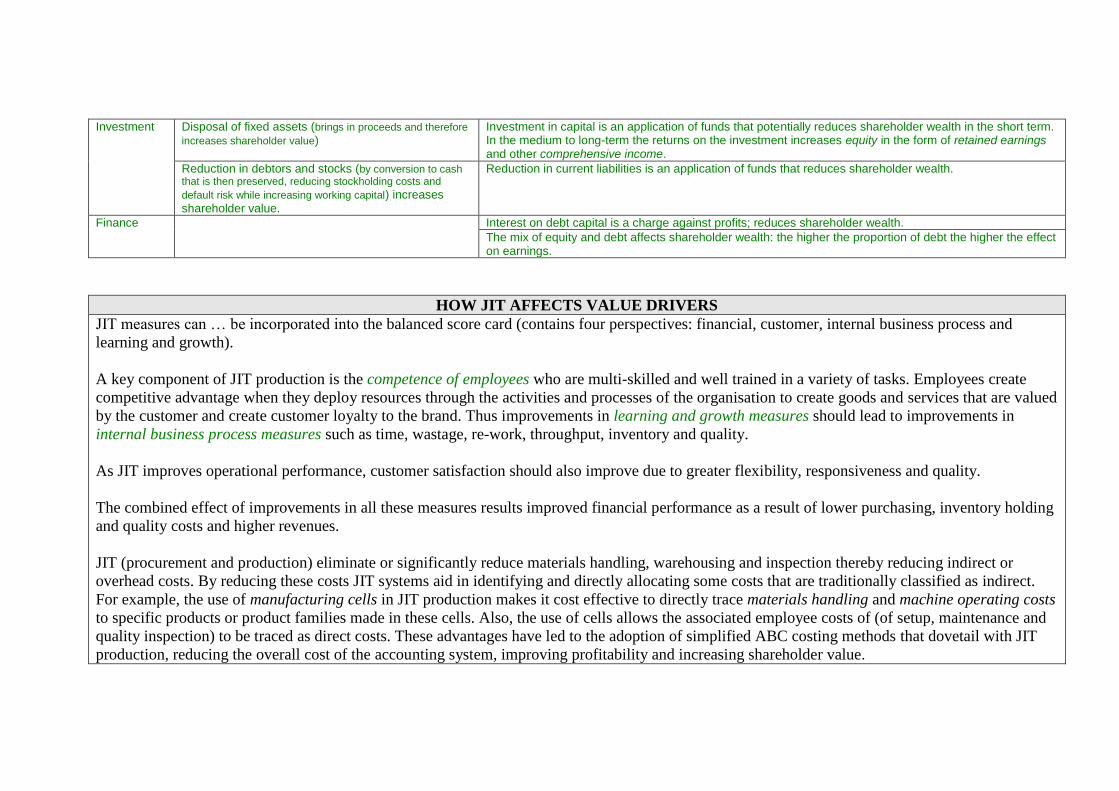

Investment Disposal of fixed assets (brings in proceeds and therefore

increases shareholder value) Investment in capital is an application of funds that potentially reduces shareholder wealth in the short term. In the medium to long-term the returns on the investment increases equity in the form of retained earnings and other comprehensive income.

Reduction in debtors and stocks (by conversion to cash that is then preserved, reducing stockholding costs and

default risk while increasing working capital) increases shareholder value.

Reduction in current liabilities is an application of funds that reduces shareholder wealth.

Finance Interest on debt capital is a charge against profits; reduces shareholder wealth.

The mix of equity and debt affects shareholder wealth: the higher the proportion of debt the higher the effect on earnings.

HOW JIT AFFECTS VALUE DRIVERS

JIT measures can … be incorporated into the balanced score card (contains four perspectives: financial, customer, internal business process and

learning and growth).

A key component of JIT production is the competence of employees who are multi-skilled and well trained in a variety of tasks. Employees create

competitive advantage when they deploy resources through the activities and processes of the organisation to create goods and services that are valued

by the customer and create customer loyalty to the brand. Thus improvements in learning and growth measures should lead to improvements in

internal business process measures such as time, wastage, re-work, throughput, inventory and quality.

As JIT improves operational performance, customer satisfaction should also improve due to greater flexibility, responsiveness and quality.

The combined effect of improvements in all these measures results improved financial performance as a result of lower purchasing, inventory holding

and quality costs and higher revenues.

JIT (procurement and production) eliminate or significantly reduce materials handling, warehousing and inspection thereby reducing indirect or

overhead costs. By reducing these costs JIT systems aid in identifying and directly allocating some costs that are traditionally classified as indirect.

For example, the use of manufacturing cells in JIT production makes it cost effective to directly trace materials handling and machine operating costs

to specific products or product families made in these cells. Also, the use of cells allows the associated employee costs of (of setup, maintenance and

quality inspection) to be traced as direct costs. These advantages have led to the adoption of simplified ABC costing methods that dovetail with JIT

production, reducing the overall cost of the accounting system, improving profitability and increasing shareholder value.

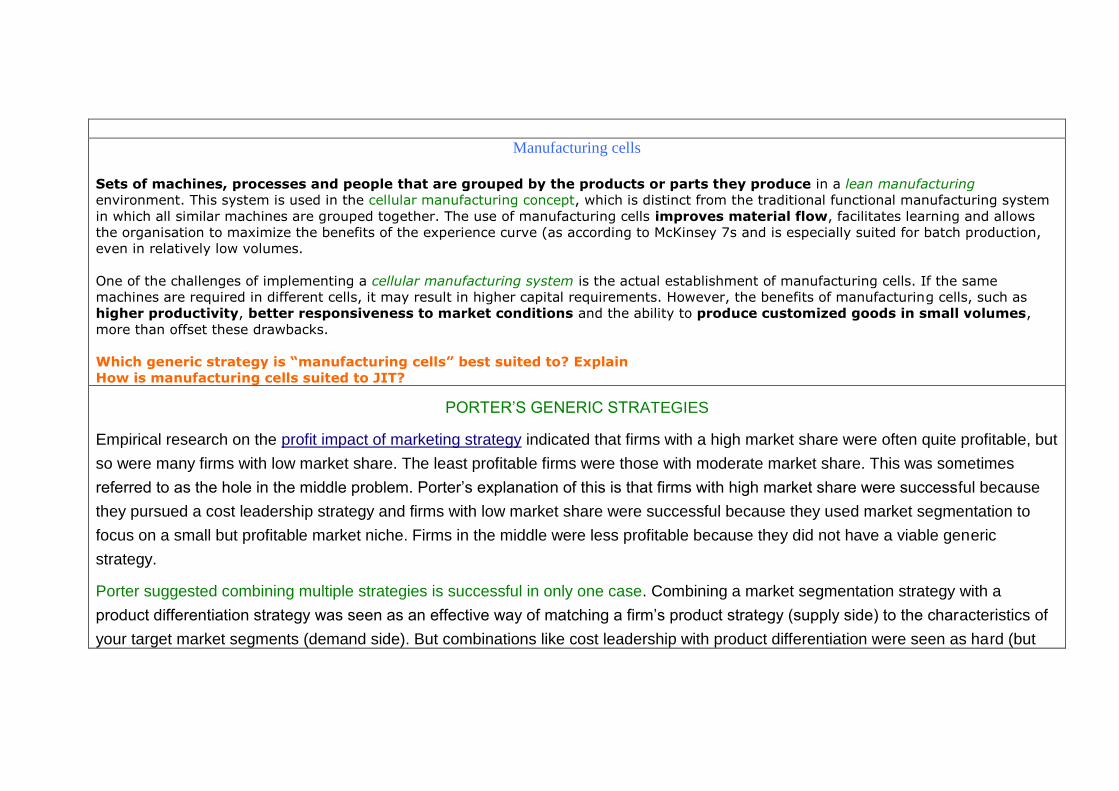

Manufacturing cells

Sets of machines, processes and people that are grouped by the products or parts they produce in a lean manufacturing

environment. This system is used in the cellular manufacturing concept, which is distinct from the traditional functional manufacturing system

in which all similar machines are grouped together. The use of manufacturing cells improves material flow, facilitates learning and allows

the organisation to maximize the benefits of the experience curve (as according to McKinsey 7s and is especially suited for batch production,

even in relatively low volumes.

One of the challenges of implementing a cellular manufacturing system is the actual establishment of manufacturing cells. If the same

machines are required in different cells, it may result in higher capital requirements. However, the benefits of manufacturing cells, such as

higher productivity, better responsiveness to market conditions and the ability to produce customized goods in small volumes,

more than offset these drawbacks.

Which generic strategy is “manufacturing cells” best suited to? Explain

How is manufacturing cells suited to JIT?

PORTER’S GENERIC STRATEGIES

Empirical research on the profit impact of marketing strategy indicated that firms with a high market share were often quite profitable, but

so were many firms with low market share. The least profitable firms were those with moderate market share. This was sometimes

referred to as the hole in the middle problem. Porter’s explanation of this is that firms with high market share were successful because

they pursued a cost leadership strategy and firms with low market share were successful because they used market segmentation to

focus on a small but profitable market niche. Firms in the middle were less profitable because they did not have a viable generic

strategy.

Porter suggested combining multiple strategies is successful in only one case. Combining a market segmentation strategy with a

product differentiation strategy was seen as an effective way of matching a firm’s product strategy (supply side) to the characteristics of

your target market segments (demand side). But combinations like cost leadership with product differentiation were seen as hard (but

not impossible) to implement due to the potential for conflict between cost minimization and the additional cost of value-added

differentiation.

Since that time, empirical research has indicated companies pursuing both differentiation and low-cost strategies may be more

successful than companies pursuing only one strategy.[1]

Some commentators have made a distinction between cost leadership, that is, low cost strategies, and best cost strategies. They claim

that a low cost strategy is rarely able to provide a sustainable competitive advantage. In most cases firms end up in price wars. Instead,

they claim a best cost strategy is preferred. This involves providing the best value for a relatively low price.

Examples of Cost Leadership & Strategy Marketing by Michael Smith, Demand Media

When it comes to marketing your business, there are three generic strategies you can use: focus, differentiation and cost leadership. While the cost

leadership strategy can be highly successful, it can be difficult to employ. It involves marketing your company as the cheapest source for a good or

service. This means that you need to minimize your costs and pass the savings on to your customers. By looking at examples of firms that have

employed this strategy successfully, you can see how it can benefit your own business.

Wal-Mart

Wal-Mart Stores Inc. has been successful using its strategy of everyday low prices to attract customers. The idea of everyday low prices is to

offer products at a cheaper rate than competitors on a consistent basis, rather than relying on sales. Wal-Mart is able to achieve this due to its large

scale and efficient supply chain. They source products from cheap domestic suppliers and from low-wage foreign markets. This allows the company

to sell their items at low prices and to profit off thin margins at a high volume.

McDonald's The restaurant industry is known for yielding low margins that can make it difficult to compete with a cost leadership marketing strategy. McDonald's

has been extremely successful with this strategy by offering basic fast-food meals at low prices. They are able to keep prices low through a division of

labour that allows it to hire and train inexperienced employees rather than trained cooks. It also relies on few managers who typically earn higher

wages. These staff savings allow the company to offer its foods for bargain prices.

Ikea The Swedish furniture retailer Ikea revolutionized the furniture industry by offering cheap but stylish furniture. Ikea is able to keep its prices low by

sourcing its products in low-wage countries and by offering a very basic level of service. Ikea does not assemble or deliver furniture; customers must

collect the furniture in the warehouse and assemble at home themselves. While this is less convenient than traditional retailers, it allows Ikea to offer

lower prices that attract customers.

Southwest Airlines The airline industry has typically been an industry where profits are hard to come by without charging high ticket prices. Southwest Airlines

challenged this concept by marketing itself as a cost leader. Southwest attempts to offer the lowest prices possible by being more efficient than

traditional airlines. They minimize the time that their planes spend on the tarmac in order to keep them flying and to keep profits up. They also offer

little in the way of additional thrills to customers, but pass the cost savings on to them.

8.

b) Justify the crucial objectives of survival and business growth. [3] Focus notes

- The reasoning that is done: explain why survival and growth are imperatives of organisations

- Analyse the implications of this in terms of performance management e.g. organisations needing to be outward and forward looking (feedforward) as well as being

backward looking (feedback).

- Discuss the use of certain performance management techniques in terms of how they contribute to survival and growth. Examples: strategic planning, strategic

management accounting, beyond budgeting, lifecycle costing, lean accounting, backflush costing,

Why survival and growth are imperative strategic objectives pursued by organisations 9. The stakeholders of an organisation, e.g. investors in a profit making enterprise, have expectations of continued growth and long-term

survival. The value investor expects her investment to grow in value. The income investor expects her income to grow over the long term. To

achieve these objectives the business needs to be competitive by continuously improving value propositions to the customer at a price the

customer is willing to pay. To secure customer loyalty these value propositions need to be superior to those of competitors. This superiority

needs to be sustained over the long term otherwise customers will switch loyalty to competitors, particularly in an industry such as grocery,

motor cars, merchandising and IT that provides commodities. Sustaining superiority requires maintenance of strategic capabilities such as

plants, staff competences and IT infrastructure. This requires that the business is adequately profitable and is generating adequate operating

cash flows to provide for renewal and working capital. This is achieved only if the business survives and grows in a controlled and managed

way so it does not overtrade and run out of cash.

The implications of the survival and growth imperatives for performance management 10. The implications of the above for performance management are that the firm needs to be forward and outward looking (feedforward) as

well as backward looking (feedback) to learn lessons from previous performance management practices. In terms of strategy the business

needs to avoid strategic drift (the incremental adjustments by bargaining and negotiation of past strategies to fit current circumstances

without taking adequate account of environmental changes. In such a situation there is “culture capture” – the taken for granted assumptions

of the organisation such as “growth will happen as a matter of course” significantly influence strategy formulation). According to Porter the

firm needs to analyse the environment rigorously and develop adequate strategies that respond to the challenges adequately (select generic

strategy by design that achieves advantage over the long term). It then needs to choose its competitive strategy to execute its generic

strategy. At the implementation stage it needs to analyse and manage its value chain effectively (value chain analysis) to ensure it achieves

sustainable competitive advantage.

11. In terms of performance management the firm needs strategic management information to allow continuous monitoring of the competitive

environment. Performance indicators are measured relative to competitors to assess the firm’s performance relative to its competitors so that

adequate control action can be taken to achieve objectives, overcome threats and take advantage of opportunities. Frameworks such as the

balanced scorecard are used to provide comprehensive information for effective strategic management. The performance pyramid is used

to ensure strategic alignment between mission, objectives, strategies and resources and the support systems contingent on the culture to

maximise organisational effectiveness.

12. Survival and growth imply an explicit focus on understanding stakeholders and their needs. The performance prism is an essential tool to

identify all the stakeholders, their needs, what the organisation expects from them and the resources and competences that would be needed

(strategic capabilities) to fulfil their expectations. In terms of value proposition to the customer in order to maintain strategic capability all

the techniques designed to achieve quality and promote efficiency are deployed appropriately, depending on the generic strategy being

pursued. Examples of techniques are lean accounting, JIT, lifecycle costing, target costing, ABC, six sigma, value engineering, obsolescence

planning, etc.

13.

c) Discuss the appropriateness of, and apply different measures of performance, including: [3]

Tesco plc 2012 http://www.tescoplc.com/files/pdf/reports/tesco_annual_report_2012.pdf

http://www.tesco.com/investorInformation/report97/review/page11.html

Comparative analysis of Tesco plc and Wal-mart http://essaybank.degree-essays.com/accounting/business-report-of-tesco-and-wal-mart.php

Investor investigates food and retailing sector to assess

investment prospects

http://www.scribd.com/doc/39455198/TESCO-Financial-Analysis

i) Return on Capital Employed (ROCE)

ii) Return on Investment (ROI)

iii) Earnings Per Share (EPS)

iv) Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA)

v) Residual Income (RI)

vi) Net Present value (NPV)

vii) Internal rate of return and modified internal Rate of Return (IRR, MIRR)

viii) Economic Value Added (EVA TM)

Focus notes:

- The key idea to bear in mind as you study the measures is that the measures need to be appropriate and used in combination because no one measure fully depicts the

performance of the organisation to its various stakeholders.

- The other thing to bear in mind is that the measures to be meaningful they need to be interpreted relative to i) a benchmark e.g. industry average, ii) the environment e.g.

constraints, iii) other conditions e.g. PESTEL factors, events, etc

- Above all the measures need to be appropriate to the strategy and its objectives.

- Each of the measures has limitations that need to be discussed and evaluated in terms of whether they matter to the interpretation of performance. If so to what extent and

how can these limitations be overcome either by using a combination of measures or by using a modified version as in MIRR.

- Therefore it is good learning practice to always ask (as with the various frameworks, concepts and tools): i) what does this measure give me that the other does not? ii)

which measure is most crucial and why? And to which of the stakeholders? iii) how can I best combined the measures to present the performance of the business?

14. The above measures are all relevant to shareholders the principal stakeholders in an organisation.

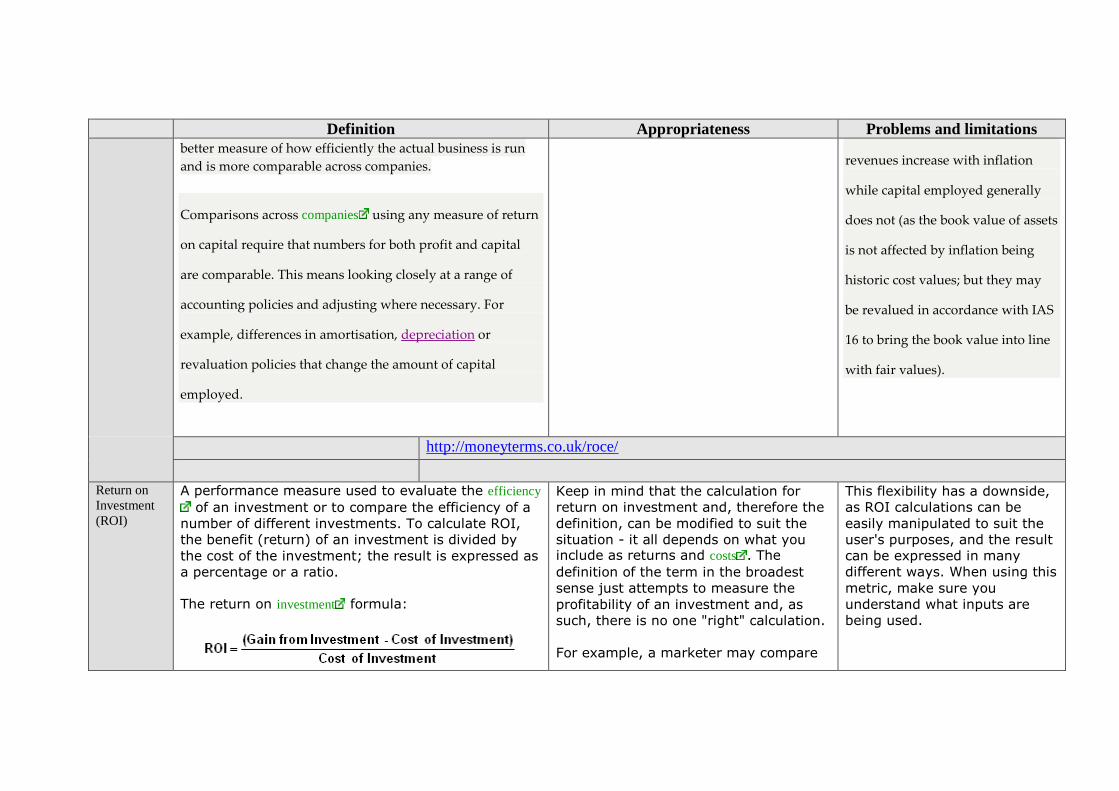

Definition Appropriateness Problems and limitations Return on

Capital

Employed

(ROCE)

Return on capital employed (ROCE) is the rate of return a

business is making on the total capital employed in the

business. Capital will include all sources of funding

(shareholders funds + debt). To be consistent with this the return

should be taken prior to interest (the return to lenders) and tax. It is

therefore:

EBIT ÷ (shareholders funds + debt)

RoE is a similar measure which looks only at the returns to

shareholders. Return on equity (RoE) is normally higher than

ROCE and is affected by the level of debt because the interest

charge is deducted to arrive at the return.

Return on operating capital employed is a variant of ROCE

that looks at the operations of the business only, ignoring

the effects of cash holdings and provisions. It is therefore a

Appropriate for evaluating the efficiency of asset

utilisation where the company’s asset base is large

and fixed e.g. manufacturing.

Not appropriate for service industries that don’t

rely on asset base to create value. The value

determinants in such industries are predominantly

people whose value is not measured and

recognised in the balance sheet. Hence ROCE

would be misleading in such circumstances.

Not appropriate for technology companies that rely

on intangibles such as intellectual property rights.

Royalties, patents and brands generate income

passively i.e. income accrues based on contracts

rather than from active use. Therefore, the

efficiency measure of ROCE is not meaningful.

The main drawback of ROCE is that

it measures return against the book

value of assets in the business. As

these are depreciated the ROCE

may increase even though cash

flow has remained the same has

reduced. Thus, older businesses

with depreciated assets will tend to

have higher ROCE than newer,

possibly better businesses. In

addition, while cash flow is affected

by inflation, the book value of

assets is not. Consequently,

Definition Appropriateness Problems and limitations

better measure of how efficiently the actual business is run

and is more comparable across companies.

Comparisons across companies using any measure of return

on capital require that numbers for both profit and capital

are comparable. This means looking closely at a range of

accounting policies and adjusting where necessary. For

example, differences in amortisation, depreciation or

revaluation policies that change the amount of capital

employed.

revenues increase with inflation

while capital employed generally

does not (as the book value of assets

is not affected by inflation being

historic cost values; but they may

be revalued in accordance with IAS

16 to bring the book value into line

with fair values).

http://moneyterms.co.uk/roce/

Return on

Investment

(ROI)

A performance measure used to evaluate the efficiency

of an investment or to compare the efficiency of a

number of different investments. To calculate ROI,

the benefit (return) of an investment is divided by

the cost of the investment; the result is expressed as

a percentage or a ratio.

The return on investment formula:

Keep in mind that the calculation for

return on investment and, therefore the

definition, can be modified to suit the

situation - it all depends on what you include as returns and costs . The

definition of the term in the broadest

sense just attempts to measure the

profitability of an investment and, as

such, there is no one "right" calculation.

For example, a marketer may compare

This flexibility has a downside,

as ROI calculations can be

easily manipulated to suit the

user's purposes, and the result

can be expressed in many

different ways. When using this

metric, make sure you

understand what inputs are

being used.

Definition Appropriateness Problems and limitations

In the above formula "gains from investment", refers

to the proceeds obtained from selling the investment

of interest. Return on investment is a very popular

metric because of its versatility and simplicity. That

is, if an investment does not have a positive ROI, or

if there are other opportunities with a higher ROI,

then the investment should not be undertaken.

Another way to calculate ROI is to divide net profit by

total assets thus:

ROI = Net Profit/Total assets

two different products by dividing

the gross profit that each product has

generated by its respective marketing

expenses. A financial analyst, however,

may compare the same two products

using an entirely different ROI

calculation, perhaps by dividing the net

income of an investment by the total value of all resources that have been

employed to make and sell the product.

Definition Appropriateness Problems and limitations Earnings Per

Share (EPS) Earnings per share (EPS) is a commonly used phrase in the financial world. Earnings per share represents a portion of a company's profit that is allocated to one share of stock. Although there are many online calculators available that will calculate an EPS sum automatically, many investors find it important to be able to do these calculations on their own.

Calculated as:

When calculating, it is more accurate to use

a weighted average number of shares outstanding

over the reporting term, because the number of

shares outstanding can change over time. However,

data sources sometimes simplify the calculation by

using the number of shares outstanding at the end of

the period.

Diluted EPS expands on basic EPS by including the

shares of convertibles or warrants outstanding in the

outstanding shares number.

Earnings per share is generally

considered to be the single

most important variable in determining

a share's price. It is also a major

component used to calculate the price-

to-earnings valuation ratio.

For example, assume that a company

has a net income of $25 million. If the

company pays out $1 million in

preferred dividends and has 10 million

shares for half of the year and 15 million

shares for the other half, the EPS would

be $1.92 (24/12.5). First, the $1 million

is deducted from the net income to get

$24 million, then a weighted average is

taken to find the number of shares

outstanding (0.5 x 10M+ 0.5 x 15M =

12.5M).

EPS can be further subdivided according to the time period involved. Profitability can be assessed by prior (trailing) earnings, recent (current) earnings, or projected future

Though earning per share is widely considered to be the most popular method of quantifying a firm's profitability, it's important to remember that earnings themselves can often be susceptible to manipulation, accounting changes, and restatements. For that reason, free cash flow is seen by some to be a more reliable indicator than EPS. Nevertheless, Earnings per share remains the industry standard in determining corporate profitability for shareholders.

Definition Appropriateness Problems and limitations

Shares outstanding refers to all shares currently owned by

stockholders, company officials, and investors in the public domain,

but does not include shares repurchased by a company.

How It Works/Example:

Shares outstanding is also referred to as outstanding shares,

or issued shares.

Shares that are outstanding include stock owned by the firm's

shareholders and owners. Shares outstanding does not

include treasury stock, which are stock shares that are repurchased

by the company. It also does not include unissued shares.

The number of shares outstanding is listed on a company's balance

sheet as "Capital Stock" and is reported on the company's quarterly

filings with the US Securities and Exchange Commission. The

number of shares outstanding can also be found in the capital

section of a company's annual report.

Why It Matters:

Shares Outstanding is included in the market capitalization formula

(outstanding shares multiplied by current share price)

and earnings per share formula (EPS calculated as outstanding

shares divided by earnings), two major measures of a company's

value and performance used by investors.

(forward) earnings.

An important aspect of EPS that's often

ignored is the capital that is required to

generate the earnings (net income) in

the calculation. Two companies could

generate the same EPS number, but one

could do so with less equity

(investment) - that company would be more efficient at using its capital to

generate income and, all other things

being equal, would be a "better"

company. Investors also need to be

aware of earnings manipulation that will

affect the quality of the earnings

number. It is important not to rely on

any one financial measure, but to use it

in conjunction with statement analysis

and other measures.

Free cash flow (FCF) is a

measure of how much cash a

business generates

after accounting for capital

expenditures such as buildings or

equipment. This cash can be used

for expansion, dividends, reducing

debt, or other purposes.

How It Works/Example:

The formula for free cash flow is:

FCF = Operating Cash Flow -

Capital Expenditures

The data needed to calculate a

company's free cash flow is

usually on its cash flow statement.

For example, if Company XYZ's

cash flow statement reported $15

million of cash from operations

and $5 million of capital

expenditures for the year, then

Company XYZ's free cash flow

was $15 million - $5 million = $10

million.

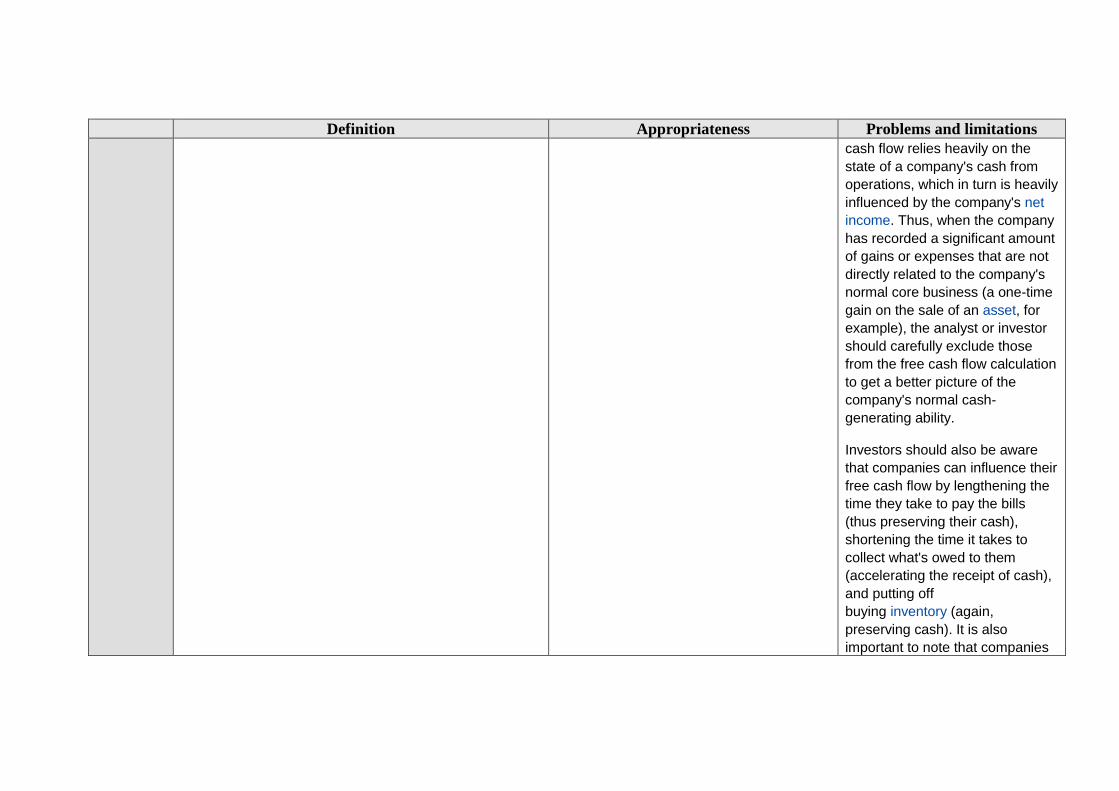

It is important to note that free

Definition Appropriateness Problems and limitations

cash flow relies heavily on the

state of a company's cash from

operations, which in turn is heavily

influenced by the company's net

income. Thus, when the company

has recorded a significant amount

of gains or expenses that are not

directly related to the company's

normal core business (a one-time

gain on the sale of an asset, for

example), the analyst or investor

should carefully exclude those

from the free cash flow calculation

to get a better picture of the

company's normal cash-

generating ability.

Investors should also be aware

that companies can influence their

free cash flow by lengthening the

time they take to pay the bills

(thus preserving their cash),

shortening the time it takes to

collect what's owed to them

(accelerating the receipt of cash),

and putting off

buying inventory (again,

preserving cash). It is also

important to note that companies

Definition Appropriateness Problems and limitations

have some leeway about what

items are or are not considered

capital expenditures, and the

investor should be aware of this

when comparing the free cash

flow of different companies.

Why It Matters:

The presence of free cash

flow indicates that a company has

cash to expand, develop new

products, buy back stock, pay

dividends, or reduce its debt. High

or rising free cash flow is often a

sign of a healthy company that is

thriving in its current environment.

Furthermore, since FCF has a

direct impact on the worth of a

company, investors often hunt for

companies that have high or

improving free cash flow but

undervalued share prices -- the

disparity often means the share

price will soon increase.

Free cash flow measures a

company's ability to generate

cash, which is a fundamental

Definition Appropriateness Problems and limitations

basis for stock pricing. This is why

some people value free cash flow

more than just about any other

financial measure out there,

including earnings per share.

How to calculate EPS http://www.wikihow.com/Calculate-Earnings-Per-Share Interpreting PE ratio http://economics.about.com/cs/finance/l/aa030503a.htm

Earnings

Before

Interest,

Tax,

Depreciation

and

Amortisation

(EBITDA)

Earnings Before Interest, Taxes, Depreciation and Amortization. A

measure of a company's ability to produce income on its

operations in a given year. (it can be an approximate measure

of a company's operating cash flow based on data from the

company's income statement).

EBITDA is calculated by looking at earnings before

Apart from the use mentioned above, EBITDA is widely

used in loan covenants, mostly in the following two

metrics:

Leverage: Debt/EBITDA. This metric measures the

amount of debt in relation to the EBITDA, i.e. how does

the debt relate to the operational profit generating ability

Why EBITDA may be risky

and inappropriate

EBITDA can be used to analyze and compare profitability between companies and industries because it eliminates the effects of financing and accounting decisions. However, this is a non-GAAP measure that allows for greater discretion in terms of what is

Definition Appropriateness Problems and limitations

the deduction of interest expenses, taxes, depreciation, and

amortization. (It is important to note that EBITDA does not

account for one-off or otherwise unusual revenues and

expenses, only recurring ones.)

This earnings measure is of particular interest in cases

where companies have large amounts of fixed assets which

are subject to heavy depreciation charges (such as manufacturing

companies) or in the case where a company has a large amount of

acquired intangible assets on its books and is thus subject to large

amortization charges (such as a company that has purchased

a brand or a company that has recently made a large acquisition).

Since the distorting accounting and financing effects on company

earnings do not factor into EBITDA, it is a good way of comparing

companies within and across industries. This measure is also of

interest to a company's creditors, since EBITDA is essentially

the income that a company has free for interest payments.

In general, EBITDA is a useful measure only for large companies

with significant assets, and/or for companies with a significant

amount of debt financing. It is rarely a useful measure for

evaluating a small company with no significant loans.

of the company. Whilst there is no absolute target and

whilst leverage ratios differ widely, it can probably be

argued that a leverage >3 is unhealthy for most

businesses.

Interest Cover (EBITDA/Interest Expense). This metric

measures the ability of a company to generate profit out of

its operations to cover the interest payments. Again there

is no absolute target for this value as the ratio that is

required obviously depends on taxes, working capital

needs, capital expenditures and the repayment needs of

the principal. However, it is clear that a ratio <1 is not

sustainable for long.

(and is not) included in the calculation. This also means that companies often change the items included in their EBITDA calculation from one reporting period to the next.

EBITDA came on the scene during the leveraged buyout boom of the 1980s, when it was used to indicate the ability of a company to service debt. As time passed, it became popular in industries with expensive assets that had to be written down over long periods. EBITDA now is quoted commonly by many companies, especially in the tech sector, even when it is not warranted. (Why do tech companies like this measure and why may it not be warranted within the tech industry?)

A common misconception is that EBITDA represents cash earnings. EBITDA is a good metric to evaluate profitability but not cash flow.

EBITDA also leaves out the cash required to fund working capital and the replacement of old equipment, which can be significant. Consequently, EBITDA often is used as an accounting gimmick to dress up a company's earnings (P2: management of earnings, the moral hazard problem). Investors

should not look at EBITDA alone but also look at other performance measures to help identify whether a company is hiding something in its

Definition Appropriateness Problems and limitations

Sometimes also called operational cash flow.

EBITDA results.

- Makes companies look cheaper than they really are

- Ignores quality of earnings

- No substitute for cash flow

- Skews interest coverage

A Clear Look At EBITDA (analysis and evaluation of benefits

and pitfalls) http://www.investopedia.com/articles/06/ebitda.asp#axzz296KaQNQr

Related terms http://financial-dictionary.thefreedictionary.com/EBITDA

Residual

Income (RI) The concept of residual income dates back to Alfred Marshall in the

late 1880s. In 1920s General Motors used the concept to evaluate

its business segments. Residual income is often called

Economic Value Added (EVA) as copyrighted by Stern Stewart &

Co, a consulting firm, in 1994.

Residual income is a company or division performance measure. It

can also be used to evaluate investment alternatives. 2. Residual come formula

Definition Appropriateness Problems and limitations

To calculate the residual income, the following formula can be used:

Residual Income = Income from Operations – Minimum Acceptable Income

Residual income is a dollar amount, which can be either positive

or negative:

When a positive residual income takes place, a company (division,

segment, investment) is creating wealth.

When a negative residual income takes place, a company (division,

segment, investment) is consuming capital.

The following residual income calculations exist:

Income from operations less minimum acceptable income (i.e.,

minimum return on operational assets)

Net income less equity charge

Net operating profits after tax (NOPAT) less capital charge

Companies can use the following income values: income from

operations (IFO) or earnings before interest and taxes (EBIT), net

operating profit after tax (NOPAT), net income, etc.

The minimum acceptable income is usually determined by

multiplying average operating assets by a minimum rate of return

(i.e., weighted average cost of capital). For example, if division A

has $200,000 of average operating assets and the top management

established 10% as the minimum acceptable rate of return (i.e.,

based on the cost of financing the business operations), then the

Definition Appropriateness Problems and limitations

minimum acceptable income for division A is $20,000 (i.e.,

$200,000 x 10%).

Instead of the minimum return on operational assets, companies

can use an equity charge or capital charge. The equity charge is

the estimated cost of equity capital. It is determined by multiplying

equity capital by the cost of equity capital. The capital charge is the

estimated total cost of capital: it includes both the debt charge and

the equity charge.

Net Present

value (NPV) The difference between the present value of the future cash

flows from an investment and the amount of investment.

Present value of the expected cash flows is computed

by discounting them at the required rate of return.

For example, an investment of $1,000 today at

10 percent will yield $1,100 at the end of the year; therefore, the

present value of $1,100 at the desired rate of return (10 percent)

is $1,000. The amount of investment ($1,000 in this example) is

deducted from this figure to arrive at net present value which here

is zero ($1,000-$1,000).

A zero net present

value means the project repays original investmen

t plus the required rate of return. A positive net

present value means a better return, and a

negative net present value means a worse return,

than the return from zero net present value. It is

one of the two discounted cash flow

techniques (the other is internal rate of return)

used in comparative appraisal of investment

proposals where the flow of income varies over

time.

Internal rate

of return and

modified

internal Rate

of Return

(IRR,

The discount rate often used in capital budgeting that

makes the net present value of all cash flows from a

particular project equal to zero. Generally speaking,

the higher a project's internal rate of return, the

more desirable it is to undertake the project. As

such, IRR can be used to rank several prospective

You can think of IRR as the rate of

growth a project is expected to

generate. While the actual rate of return

that a given project ends up generating

will often differ from its estimated IRR

rate, a project with a substantially

Internal rate of return (IRR) has never

had a good academic press.

Compared with net present value

(NPV), IRR has many drawbacks: it is

only a relative measure of value

creation, it can have multiple answers,

Definition Appropriateness Problems and limitations MIRR) projects a firm is considering. Assuming all other

factors are equal among the various projects, the

project with the highest IRR would probably be

considered the best and undertaken first.

higher IRR value than other available

options would still provide a much better

chance of strong growth.

IRRs can also be compared against

prevailing rates of return in the

securities market. If a firm can't find

any projects with IRRs greater than the

returns that can be generated in the

financial markets, it may simply choose

to invest its retained earnings into the

market.

it’s difficult to calculate, and it appears

to make a reinvestment

assumption that is unrealistic. But

financial managers like it. IRR

expresses itself as a percentage

measure of project performance; it also

provides a useful tool to measure

‘headroom’ when negotiating with

suppliers of funds.

IRR example calculations and relationship to NPV http://office.microsoft.com/en-us/excel-help/irr-HP005209146.aspx

MODIFIED IRR

While the internal rate of return (IRR) assumes the cash flows from a project are reinvested at the IRR, the modified IRR assumes that positive cash flows are reinvested at the firm's cost of capital, and the initial outlays are financed at the firm's financing cost. Therefore, MIRR more accurately reflects the cost and profitability of a project.

The formula for MIRR is:

Definition Appropriateness Problems and limitations example

For example, say a two-year project with an initial

outlay of $195 and a cost of capital of 12%, will

return $121 in the first year and $131 in the second

year. To find the IRR of the project so that the net

present value (NPV) = 0:

NPV = 0 = -195 + 121/(1+ IRR) + 131/(1 +

IRR)2 NPV = 0 when IRR = 18.66%

To calculate the MIRR of the project, we have to

assume that the positive cash flows will be reinvested

at the 12% cost of capital. So future value of the

positive cash flows is computed as:

$121(1.12) + $131 = $266.52 = Future Value of

positive cash flows at t = 2

Now you divide the future value of the cash flows by

the present value of the initial outlay, which was

$195, and find the geometric return for 2 periods.

=sqrt ($266.52/195) -1 = 16.91% MIRR

You can see here that the 16.91% MIRR is materially lower than

the IRR of 18.66%. In this case, the IRR gives a too optimistic

picture of the potential of the project, while the MIRR gives a more

realistic evaluation.

MIRR examples http://office.microsoft.com/en-gb/excel-help/mirr-HP005209180.aspx

Definition Appropriateness Problems and limitations

Modified IRR ACCA http://www.accaglobal.com/content/dam/acca/global/PDF-students/2012/sa_apr08_ryan_revised.pdf

Economic

Value

Added

(EVA TM)

Economic value added (EVA) is an internal management performance

measure that compares net operating profit to total cost of capital. Stern

Stewart & Co. is credited with devising this trademarked concept.

How It Works/Example:

Economic value added (EVA) is also referred to as economic profit.

The formula for EVA is:

EVA = Net Operating Profit After Tax - (Capital Invested x WACC)

As shown in the formula, there are three components necessary to solve

EVA: net operating profit after tax (NOPAT), invested capital, and

the weighted average cost of capital (WACC) operating profit after

taxes (NOPAT) can be calculated, but can usually be easily found on

the corporation's income statement.

The next component, capital invested, is the amount of money used to fund

a particular project. We will also need to calculate the weighted-average cost

of capital (WACC) if the information is not provided.

The idea behind multiplying WACC and capital investment is to assess a

charge for using the invested capital. This charge is the amount that

investors as a group need to make their investment worthwhile.

Let's take a look at an example.

Assume that Company XYZ has the following components to use in the EVA

Why It Matters:

Economic Value Added (EVA) is important because it is

used as an indicator of how profitable company projects

are and it therefore serves as a reflection of management

performance.

The idea behind EVA is that businesses are only truly

profitable when they create wealth for their shareholders,

and the measure of this goes beyond calculating net

income. Economic value added asserts that businesses

should create returns at a rate above their cost of capital

The economic value calculation has many advantages. It

succinctly summarizes how much and from where a

company created wealth. It includes the balance sheet in

the calculation and encourages managers to think about

assets as well as expenses in their decisions.

However, the seemingly infinite cash

adjustments associated with calculating

economic value can be time-consuming. And

accrual distortions can still affect the

measure, particularly when it comes to

depreciation and amortization differences.

Also, economic value added only applies to

the period measured; it is not predictive of

future performance, especially for companies

in the midst of reorganization and/or about to

make large capital investments.

The EVA calculation depends heavily on

invested capital, and it is therefore most

applicable to asset-intensive companies that

are generally stable. Thus, EVA is more

useful for auto manufacturers, for example,

than software companies or service

companies with a lot of intangible assets.

http://www.investinganswers.com/financial-dictionary/financial-statement-

analysis/economic-value-added-eva-2925

Definition Appropriateness Problems and limitations

formula:

NOPAT = $3,380,000

Capital Investment = $1,300,000

WACC = .056 or 5.60%

EVA = $3,380,000 - ($1,300,000 x .056) = $3,307,200

The positive number tells us that Company XYZ more than covered its cost of

capital. A negative number indicates that the project did not make enough profit to

cover the cost of doing business.

ACCA examples

15.

d) Discuss why indicators of liquidity and gearing need to be considered in conjunction with profitability. [3] Focus notes: -

Definition of liquidity

16. Cash, cash equivalents and other assets (liquid assets) that can be easily converted into cash (liquidated). In the case of a market, a stock or a commodity, the extent to which there are sufficient buyers and sellers to ensure that a few buy or sell orders would not move prices very much. Some markets are highly liquid; some are relatively illiquid.

The term also means how easy it is to perform a transaction in a particular security or instrument. A liquid security, such as a share in a large listed company or a sovereign bond, is easy to price and can be bought or sold without significant price impact. With an illiquid instrument, trying to buy or sell may change the price, if it is even possible to transact. Example Banks need to hold enough to cover expected demands from depositors, creditors and counterparties. During the global financial crisis it became clear that many assets were a lot harder to sell than banks had expected. Now the Basel Committee plans to require banks to keep enough liquid assets, such as cash and government bonds, to get through a 30-day market crisis. There will also be a second ratio that tries to match a bank's overall liquidity needs to its liabilities over a longer timeframe.

Indicators of liquidity

17. For a corporation with a published balance sheet there are various ratios used to calculate a measure of liquidity. These include the following:

the current ratio, which is the simplest measure and is calculated by dividing the total current assets by the total current liabilities. A value of over 100% is normal in a non-banking corporation. However, some current assets are more difficult to sell at full value in a hurry.

the quick ratio - calculated by deducting inventories and prepayments from current assets and then dividing by current liabilities - gives a measure of the ability to meet current liabilities from assets that can be readily sold. A better way for a trading corporation to meet liabilities is from cash flows, rather than through asset sales, so;

the operating cash flow ratio can be calculated by dividing the operating cash flow by current liabilities. This indicates the ability to service current debt from current income, rather than through asset sales.

18. For different industries and differing legal systems the use of differing ratios and results would be appropriate. For instance, in a country with a legal system that gives a slow or uncertain result a higher level of liquidity would be appropriate to cover the uncertainty related to the valuation of assets. A manufacturer with stable cash flows may find a lower quick ratio more appropriate than an Internet-based start up corporation.

Definition of gearing

19. Gearing focuses on the capital structure of the business – that means the proportion of finance that is provided by debt relative to the finance

provided by equity (or shareholders). The gearing ratio is also concerned with liquidity. However, it focuses on the long-

term financial stability of a business. Gearing (otherwise known as "leverage") measures the proportion of assets

invested in a business that are financed by long-term borrowing. In theory, the higher the level of borrowing

(gearing) the higher are the risks to a business, since the payment of interest and repayment of debts are not

"optional" in the same way as dividends. However, gearing can be a financially sound part of a business's capital

structure particularly if the business has strong, predictable cash flows.

Indicators of gearing

20. The formula for calculating gearing is:

Long-term liabilities include loans due more than one year + preference shares + mortgages

Capital employed = Share capital + retained earnings + long-term liabilities

The gearing calculation can be calculated like this:

2012

£’000

2011

£’000

Long-term liabilities 1,200 1,450

Capital employed 5,655 4,675

Gearing ratio 21.2% 31.0%

21. According to the data the gearing ratio at 31 December 2012 was 21.2%, a reduction from 31.0% a year

earlier. This was largely because the business reduced long-term borrowings by £200,000 and added over

£1million to retained earnings.

How can the gearing ratio be evaluated?

A business with a gearing ratio of more than 50% is traditionally said to be “highly geared”.

A business with gearing of less than 25% is traditionally described as having “low gearing”

Something between 25% - 50% would be considered normal for a well-established business which is happy to

finance its activities using debt.

For the above business, that would suggest that the business is relatively lowly-geared and that the capital structure of

the business is pretty safe and cautious.

It is important to remember that financing a business through long-term debt is not necessarily a bad thing! Long-

term debt is normally cheap, and it reduces the amount that shareholders have to invest in the business.

What is a sensible level of gearing? Much depends on the ability of the business to grow profits and generate positive

cash flow to service the debt. A mature business which produces strong and reliable cash flows can handle a much

higher level of gearing than a business where the cash flows are unpredictable and uncertain.

LIQUIDITY, GEARING AND PROFITABILITY

22. The profitability objective requires that the funds of the firm are used to maximize profits. Thus liquidity and profitability are very closely

related and may conflict in some of the decisions of the organisation. For example, if levels of raw material inventory are increased to hedge

against expected price increases , the profitability objective may be achieved at the cost of increased liquidity. Similarly, the firm may

relax credit policy (increasing risk) in order to boost sales, but its liquidity would decrease as a result.

23. A company may increase its profitability by having a very high debt to equity ratio e.g. where sales are increased and per unit cost of sales is

reduced at the same time as a result of increased volumes made possible by a large plant financed by a loan. However, when the company

secures a loan, it is committed to making regular payments of interest and capital, thus reducing its liquidity. Efficient financial management

means that increased profitability as a result of the loan has to exceed expected decreases in liquidity as a result of servicing the loan.

24. In all areas of financial management, the financial manager is faced with the choice of risk and profit and generally he seeks to achieve the

right balance between the two. This requires a clear financial strategy and proactive cash and profitability management e.g. forecasting

income and cash flows and modelling the effects of various scenarios to determine safe and affordable levels of debt compatible with the

anticipated levels of profitability.

25. Affordability of debt may be indicated by the interest cover - Profit/Interest, the number of times interest can be afforded by the amount of

profit.

Functions of finance http://www.managementstudyguide.com/finance-functions.htm

Aims and functions of

finance

http://www.newagepublishers.com/samplechapter/001541.pdf

e) Compare and contrast short and long run financial performance and the resulting management issues. [3] Focus notes:

- Short term priorities are crucial to long term health

- Financial health is crucial to turning the firm’s future prospects into actual performance: cash flows. Profits, etc.

- Given that expectation of future performance is the main driver of returns on shareholder investments, and given that short term performance is a determinant of future

performance e.g. EPS and PE ratio, then it is imperative that short term-performance management is undertaken with clarity of and commitment to its implications for

long-term strategic development. In terms of staff career tracks and incentives need to be structured to reflect the time it takes to achieve long-term objectives. In terms

of strategic management information appropriate metrics should be developed to track the production of goods and services and other value metrics that evidence

strategic development of the organisation over the long term. In terms of competence it should be recognized that managing for health requires different skill and mind

set than those required for managing for value. Accordingly, managers with the requisite competences should be selected and allocated responsibilities appropriately.

Short term financial performance

26. Short-term financial performance is driven by financial markets listing requirements and covers quarterly time horizons focusing on earnings

and sales as evidence of the underlying competitive capability of the organisation. Better than forecast performance gives a boost to share

price while less than forecast performance is punished by a fall in the share price. Naturally, managers are obsessed with this short-term goal,

tilting them towards an unbalanced focused on achieving short term results to the detriment of the organisation’s long-term health, as the

following quotes testify:

“In one recent survey, a majority of managers said that they would forgo an investment that offered a decent return on capital if it meant missing quarterly earnings expectations. In another, more than 80 percent of the executives responding said that they would cut expenditure on R&D and marketing to ensure that they hit quarterly earnings targets—even if they believed that the cuts were destroying value over the long term.” McKinsey Quarterly, April 2005 How to escape the short-term trap

“Regulatory and legal reforms have also been major contributors to "short-termism." Management teams have struggled to cope with a wealth of new regulations, many of which focus on the reporting of historical financial results. The same is true of board directors, who have been distracted from their role as stewards of a company's health. So despite an average 50 percent increase in the time

commitments required of directors, many boards don't have the time to understand the kind of strategic trade-offs needed to get the appropriate balance between short-term performance and long-term health. A recent McKinsey survey of over 1,000 directors around the world found that more than half admitted to having only a "limited" understanding of where the company's long-term objectives would position it in five to ten years. The good news is that our respondents told us that they are now eager to devote more time to these issues.” McKinsey Quarterly, April 2005 How to escape the short-term trap

27. According to McKinsey short-term obligations are important, of course, and only by fulfilling them will management build confidence in longer-term strategies. But the health of a company is crucial not just to its customers, suppliers, and employees but to its investors as well. It's crucial to turning the company's growth prospects, capabilities, relationships, and assets into future cash flows. Contrary to conventional wisdom, markets recognize this.

Long term financial performance

28. Long term financial performance is about the health of the company the generic components of which are: a robust and credible strategy;

productive, well-maintained assets; innovative products, services, and processes; a fine reputation with customers, regulators, governments,

and other stakeholders; the ability to attract, retain, and develop high-performing talent; maintaining and improving competitive position and

generating sustainable returns that are acceptable to investors.

29. According to McKinsey thinking about health, as opposed to short-term performance, helps management teams understand how to look after

companies today in a way that will ensure that they remain strong in the future. It focuses the mind on what must be done today to deliver the

outcome of long-term performance. Companies are not focusing enough on managing the health of their businesses. This was evidenced by

the underlying causes of the 2008 financial crises.

30. An examination of share prices demonstrates that expectations of future performance are the main driver of shareholder returns. In almost all

industry sectors and almost all stock exchanges, up to 80 percent of a share's market value can be explained only by cash flow

expectations beyond the next three years. These longer-term expectations are in turn driven by judgments on growth and long-term

profitability, a lesson relearned after the dot-com bust. For example, cash flows in the global semiconductor industry need to grow at more

than 10 percent a year during the next ten years to justify current market valuations. In retailing and consumer packaged goods, that growth

rate is between 3 and 6 percent. In electric utilities, it is around 2 percent.

31. Future expectations clearly drive the stock price of individual companies too, thus explaining the often widely differing P/E or market-to-

book ratios of companies with similar reported earnings. In the pharmaceutical sector, for example, the market ascribes significant value to a

healthy drug pipeline even though it will not affect short-term earnings.

32. Even in the private equity sector, renowned for its focus on short-term operational improvements, health matters. Most private equity

companies look to realize their investments in a five-year time frame. But they must still have a credible proposition for future earnings and

cash flow growth to underpin a sale or IPO.

The strategic management implications of differing short-term and long-term requirements

33. Given that expectation of future performance is the main driver of returns on shareholder investments, and given that short term performance

is a determinant of future performance e.g. EPS and PE ratio, then it is imperative that short term-performance management is undertaken

with clarity of and commitment to its implications for long-term strategic development. This is hard to achieve because it requires resilience

in delivering for the short-term as well as the long-term. This requires i) suitable strategies and processes that work over the short and long-

term, ii) appropriate dialogue with powerful and influential stakeholders

Robust strategies that allow the company to adapt to changes in the environment

34. First, a company's strategy should consist of a portfolio of initiatives that consciously embraces different time horizons. Companies do, of course, have different business units with distinct strategies. But few strategies direct a company in a way that will enable it to adapt to events and capitalize on opportunities as they arise. Some initiatives in the portfolio will influence short-term performance. Others will create options for the future—the development of new products or services, entry into new markets, or the restructuring of processes or value chains. A key management challenge is to design and select those initiatives and options to ensure, on a risk-adjusted basis, that the company's underlying health remains strong. Management seeks to address this challenge by setting a generic strategy (that gives scope and direction to the organisation); this informs the business strategy that defines how the business will compete and the criteria for project selection and performance evaluation.

Adequate organizational processes (support systems) that align with short term and long-term performance (Performance Prism)

35. Second, companies need organizational processes to support a focus on both performance and health. Companies with a long-term-value

orientation are always relentless about setting short-term-performance commitments and delivering on them. But such companies also define

what they are doing to ensure their health and how they will measure their efforts to do so. Reckitt Benckiser, the leading household-

cleaning-products business, emphasizes innovation as the key to its long-term strategy and specifically measures the proportion of

sales coming from new products.

36. Different companies will identify the health and performance metrics—product development, customer satisfaction, or the retention of

talent—appropriate to their industry or situation. But executives should insist on a balance of metrics that cover all areas of the business

while grabbing every opportunity to talk about these metrics, both internally and to analysts and investors.

37. Career tracks and incentives—money, recognition, promotion—should reflect the time required to deliver on longer-term goals; the current

trend of rotating people in roles every two or three years isn't necessarily good for corporate health. Moreover, companies ought to be

mindful of the different leadership qualities needed to manage for performance and health. Corporate health typically requires new skills, not

necessarily the reinforcement of the capabilities and leadership traits that worked in the past. (Performance Prism – Stakeholder

Expectations, Stakeholder Satisfaction)

Communicate the company’s vision, strategy and goals with stakeholders (shared values as in McKinsey 7s)

38. Third, companies need to change the nature of their dialogue with key stakeholders, particularly the capital markets and employees. That

means first identifying investors who will support a company's strategy and then attracting them. There is no point, for example, talking

about the company's health to court arbitrageurs or hedge fund managers looking for the next bid.

39. A management team should then quality time with analysts, explaining its views on the outlook for the industry and on how the company's

strategic stance will create a source of sustainable advantage. Management will also need to highlight the metrics it has developed to track

the company's performance and health. Just talking vaguely about shareholder value without a time frame or without addressing the specifics

of the business is not meaningful.

40. Companies might also be wise to separate discussions about quarterly results from those that focus on strategic development, as BP has done

recently. And they should ensure that analysts spend time with operational managers. When it comes to forming judgments about sustained

performance, the calibre of these managers is often the crucial factor.

41. Communicating with employees is just as important. The complaint that "we don't know what is going on" often reflects an emphasis on

communicating results rather than long-term intent. It is no coincidence that a hallmark of great, enduring companies is that they make their

future leadership generations feel involved in their long-term development.

Conclusion

42. The current focus on short-term performance is understandable given the recent economic and regulatory environment. Survival and the avoidance of risk have been of primary concern. But the focus is nevertheless unbalanced. Financial markets, as well as employees and all other stakeholders, place a real value on a company's future. Corporate managements and boards should square up to the challenge of managing for performance and health. And they should communicate loud and clear that this is exactly what they are doing.

43. How to escape the short-term trap

https://www.mckinseyquarterly.com/How_to_escape_the_short-term_trap_1611#

Long term financial plan http://www.bayside.vic.gov.au/long_term_financial_plan_2010_2021.pdf

Financial Statements analysis and long-

term planning

http://highered.mcgraw-hill.com/sites/dl/free/007353059x/335637/Sample_Chapter_03.pdf

Monitoring financial performance http://www.nachc.com/client/documents/GBG%206.pdf

44.

f) Explore the traditional relationship between profits and share value with the long term profit expectations of the stock market

and recent financial performance of new technology companies. [3] (The examiner has read the McKinsey article - it pays to read widely) Focus notes: -

45. An examination of share prices demonstrates that expectations of future performance are the main driver of shareholder returns. In almost all

industry sectors and almost all stock exchanges, up to 80 percent of a share's market value can be explained only by cash flow

expectations beyond the next three years. These longer-term expectations are in turn driven by judgments on growth and long-term

profitability, a lesson relearned after the dot-com bust. For example, cash flows in the global semiconductor industry need to grow at more

than 10 percent a year during the next ten years to justify current market valuations. In retailing and consumer packaged goods, that growth

rate is between 3 and 6 percent. In electric utilities, it is around 2 percent.

46. Future expectations clearly drive the stock price of individual companies too, thus explaining the often widely differing P/E or market-to-

book ratios of companies with similar reported earnings. In the pharmaceutical sector, for example, the market ascribes significant value to a

healthy drug pipeline even though it will not affect short-term earnings.

47. Even in the private equity sector, renowned for its focus on short-term operational improvements, health matters. Most private equity

companies look to realize their investments in a five-year time frame. But they must still have a credible proposition for future earnings and

cash flow growth to underpin a sale or IPO.

48. The P/E ratio is an important indicator of the value of a company’s stock because it measures how much the market is willing to pay for 1

dollar of earnings of the company. This interpretation reflects the way the ratio is calculated: P is the current price of the share, say $30 (per

share). E is the earnings per share (12 months earnings after tax/number of shares outstanding, say $3 per share). Therefore, P/E ratio is 10.

This is also known as the “earnings” multiple, representing the number of times the share price pays for a dollar of earnings. (Earnings could

be trailing, current or forward).

49. As with all ratios the P/E ratio is only meaningful if it is compared with other ratios. For example, the earnings multiple can be compared

with the organisation’s own earnings multiple for the previous or succeeding periods to asses how its market capitalization is changing.

i) If earnings and price move in sympathy, the P/E ratio stays the same

ii) If earnings increase but price stays the same, then P/E ratio declines

iii) If earnings decline but share price increases then the P/E ratio increases

50. At the time of the dot.com bubble the average P/E ratio of listed companies was around 20 whereas the P/E ratio of dot.com was above 60

reflecting a huge profit hike in future. There was clearly an over valuation of the dot.com shares which eventually crashed. But this disparity

in valuation reflects the expected earnings basis of valuation of shares as described above (para 30). Because the share price already factors

in the expected long term earnings, when earnings increased subsequently, this did not result in an immediate change in the share price thus

the P/E ration declined sharply.

g) Assess the relative financial performance of the organisation compared to appropriate benchmarks. [3]

Focus notes:

- Inter-firm comparisons. Requires consistency of definitions of indicators, policies and measurement basis.

- Do not calculate for the sake of it. First decide what you want to investigate and then select the relevant ratios, models and arguments. Put them together in a coherent

narrative. Reach your conclusion. - Relate analysis to models to enrich and improve the quality of the reasoning.

General remarks about assessing financial performance relative to a benchmark

51. Financial Ratio Analysis is the calculation and comparison of main indicators - ratios which are derived from the information given in a

company's financial statements(which must be from similar points in time and preferably audited financial statements and developed in the

same manner). It involves methods of calculating and interpreting financial ratios in order to assess a firm's performance and status. This

Analysis is primarily designed to meet informational needs of investors, creditors and management. The objective of ratio analysis is the

comparative measurement of financial data to facilitate wise investment, credit and managerial decisions.

52. Some examples of analysis, according to the needs to be satisfied, are:

Horizontal Analysis - the analysis is based on a year-to-year comparison of a firm's ratios,

Vertical Analysis - the comparison of Balance Sheet accounts either using ratios or not, to get useful information and draw useful

conclusions, and

Cross-sectional Analysis - ratios are used and compared between several firms of the same industry in order to draw conclusions about an

entity's profitability and financial performance. Inter-firm Analysis can be categorized under Cross-sectional, as the analysis is done by using

some basic ratios of the Industry in which the firm under analysis belongs to (and specifically, the average of all the firms of the industry) as

benchmarks or the basis for our firm's overall performance evaluation.

53. The informational needs and appropriate analytical techniques needed for specific investment and credit decisions are a function of the

decision maker’s time horizon (short versus long term investors and creditors). A pervasive problem when comparing a firm’s performance

over time (trend or time series analysis) or with other firms (cross sectional or common size analysis) is changes in the firm’s size over time

and the different sizes of firms which are being compared. However, one approach to this problem is to use common size statements in which

the various components of the financial statements are standardized by expressing them as a percentage of some base (base in the income

statement is sales and base in the balance sheet is total assets). See sample file below for further understanding.

54. In general, a process of standardization is being achieved by the use of ratios. They can be used to standardize financial statements allowing

for comparisons over time, industry, sector and cross-sectionally between firms and further facilitate the evaluation of the efficiency of

operations and/or the risk of the firm’s operations regarding the scope and purpose of evaluation. Ratios measure a firm’s crucial

relationships by relating inputs(costs) with output(benefits) and facilitate comparisons of these relationships over time and across firms.

55. Many attractive categories of financial ratios and numerous individual ratios have been proposed in the literature. The most prominent

literature on financial analysis - though non-exhaustive - indicates the following categories of ratios:

Profitability

Gross Profit Ratio = ( Gross Profit / Sales) * 100

Operating Profit = ( Operating profit / Sales) * 100

Return on capital employed (ROCE) , in times = ( Profit before interest and tax / Capital Employed) or

Return on Equity (ROE), in times = Net Income ÷ (Average Equity during the period)

Very often, the reported profits are adjusted to reflect sustainable levels of performance and thus instil more meaning to the computation

and interpretation of the financial ratios. In this context, EBITDA is used, which is calculated by excluding from the profit figure the tax,

interest, depreciation and amortisation amount. Non-recurring expenses or income is also excluded when this can be substantiated to

enhance the interpretation of the derived ratio figures. EBITDA figure can be used as an approximation of the underlying cash flows

which at the same time incorporate the future potentials of the company's profitability rather than just the cash generation of a financial

year.

Activity or Management Efficiency ratios

Debtor days, in days = ( Av. Debtors / Sales ) * 365

Creditor days, in days = ( Av. Creditors / COGS ) * 365, where COGS is the Cost of Goods Sold by the firm

Stock days, in days = ( Av. Stock / COGS ) * 365