2000 annual report - zonebourse.com · 2000 annual report asm ... 16-22 kung yip street kwai chung,...

TRANSCRIPT

The Process of Innovation™

20

00

An

nu

al R

eport

ASM InternationalThe Process of Innovation™

ASM International N.V.

Jan van Eycklaan 10

3723 BC Bilthoven

The Netherlands

®

ASM International®

20

00

With the exception of historical information, the information

in this annual report contains forward-looking statements

within the meaning of the United States federal securities

laws. These statements include, among others, statements

regarding future expenditures, sufficiency of cash generated

from operations, maintenance of majority interest in ASM

Pacific Technology, business strategy, product development,

product acceptance, market penetration, market demand,

return on investment in new products, facility completion

dates and product shipment dates, and any other non-

historical information in this annual report.

Forward-looking statements typically are identified by use

of terms such as “believe,” “anticipate,” “estimate,” “expect,”

“intend,” “plan,” “will,” “may” and similar words, although

some forward-looking statements are expressed differently.

You should be aware that our actual results could differ

materially from those contained in the forward-looking

statements due to a number of factors. These include, but

are not limited to: economic conditions in the semiconductor

industry, currency fluctuations, the timing of significant

orders, market acceptance of new products, competitive

factors, risk factors related to litigation, and other risks

indicated in filings from time to time with the SEC.

In the more than 30-year history of our

Company ASM International N.V. has

witnessed the evolution of the semiconductor

equipment industry, from 2” wafers of the

late 1960’s, to the 300 mm today. Symbolic

of these products is the silicon crystal...

the basis of the ASM International logo. JAPAN:

ASM Japan K.K.

23-1, 6-chome Nagayama

Tama-shi,

Tokyo 206-0025

Tel. (81) 42 337-6311

Fax (81) 42 389-7555

Osaka Sales Office

4F, Shin-Osaka

Ueno Toyo Building

7-4-17 Nishinakajima

Yodogawa-ku, Osaka-shi

Osaka 532-0011

Tel. (81) 6 6390-9913

Fax (81) 6 6390-9917

Nagaoka Factory

392-One Shimbo, Mishima-machi

Santoh-gun

Niigata 940-2311

Tel. (81) 258 42-2400

Fax (81) 258 41-2490

Daini Technology Center

2-7-2 Kurikii

Asao-ku, Kawasaki-shi

Kanagawa 215-0033

Tel. (81) 44-986-6811

Fax (81) 44-986-6812

Hiroshima Service Center

5F, Daihyaku-seimei Building

One-14 Higashi-Hiratsuka-cho,

Naka-ku, Hiroshima-shi

Hiroshima 730-0025

Tel. (81) 82 542-3055

Fax (81) 82 542-3056

Kumamoto Service Center

1-14-63 Kuwamizu

Kumamoto-shi

Kumamoto 862-0954

Tel. (81) 96 387-7300

Fax (81) 96 387-7301

Sendai Service Center

4F, Ami-Grande building

14-15, Futsuka-machi

Aoba-ku, Sendai-shi

Miyagi 980-0802

Tel. (81) 22 262-8333

Fax (81) 22 262-8334

Shonai Service Point

8-32-2 Asahishin-machi, Sakata-shi

Yamagata 998-0021

Tel. (81) 234-26-4536

Fax (81) 234-26-4537

ASM Assembly Technology Co. Ltd.

2nd Floor, MS Building 2-3

Shouwa-cho, Akishima-shi

Tokyo 196-0015

Tel. (81) 425 45-7041

Fax (81) 425 45-7085

SOUTH-EAST ASIA:

ASM Pacific Technology Ltd.

12/F, Watson Center

16-22 Kung Yip Street

Kwai Chung, Hong Kong

Tel. (852) 2424-2021

Fax (852) 2481-3367

ASM Assembly Automation Ltd.

4/F, Watson Center

16-22 Kung Yip Street

Kwai Chung, Hong Kong

Tel. (852) 2619-2000

Fax (852) 2619-2118

ASM Assembly Materials Ltd.

14/F, Block A, Wo Kee Hong

Building

585-609 Castle Peak Road

Kwai Chung, Hong Kong

Tel. (852) 2619-4000

Fax (852) 2480-5852

ASM Wafer Process Equipment Ltd.

12/F., Room 1202, Stanhope House

734-738 King’s Road,

Quarry Bay, Hong Kong

Tel. (852) 2881-7522

Fax (852) 2881-7516

Shen Zhen ASM Micro Electronic

Technology Co. Ltd.

6/F Block A, Hoi Peng

Industrial Estate

2052, Wu Tung Road

Sha Tou Jiao, Shenzhen

Peoples Republic of China

Tel. (86) 755-5552-433

Fax (86) 755-5552-434

ASM Precision Machinery

Manufactory Ltd.

2048, Wu Tung Road

Sha Tou Jiao, Shenzhen

Peoples Republic of China

Tel. (86) 755-5553-590

Fax (86) 755-5552-434

ASM Pacific KOR Limited

3F1, 628-6, Deung Chon Dong

Kangseo Gu, Seoul

157-030 Korea

Tel. (82)-2-659 4174

Fax (82)-2-659 4216

ASM Korea Ltd.

4F, DaeWoo Engineering Bldg.

9-3, SuNae-Dong, BunDang-Ku

SungNam-City, Kyonggi-Do

463-020 Korea

Tel. (82) 31-738-1011

Fax (82) 31-738-1012

ASM Taiwan - Taipei Office

2nd Floor, No. 70, Sec. 2

Chang Sha Street,

Taipei, Taiwan, R.O.C.

Tel. (886) 2-32312 6800

Fax (886) 2-32312 6899

ASM Taiwan - Kaohsiung Office

No. 4-2, East 3 Road Street

N.E.P.Z. Kaohsiung

Taiwan, R.O.C.

Tel. (886) 7-367 6300

Fax (886) 7-367 6399

ASM Taiwan - Hsin Chu Office

2F, No.9, Lane 379, Sec 1

Ching Kuo Road

Hsin-Chu Hsien,

Taiwan, R.O.C.

Tel. (886) 3-543 1500

Fax (886) 3-543 1555

ASM Far East Marketing Ltd.

Taiwan Branch

1F, Nr. 58, Hsien-Cheng

Liu Road, Chu-Pei 302

Hsin-Chu Hsien,

Taiwan, R.O.C.

Tel. (886) 3-551-5596

Fax (886) 3-551-5597

ASM Pacific Philippines

Unit 401, The Sycamore Building

Alabang-Zapote Road

Alabang, Muntinlupa City

Philippines 1770

Tel. (632) 850-4543809 3917

(632) 809 3919/809 3931

Fax (632) 850-4547

ASM Technology Singapore Pte Ltd.

2, Yishun Avenue 7

Singapore 768924

Tel. (65) 7526-311

Fax (65) 7582-287

ASM Wafer Process Equipment

Singapore Pte Ltd.

2, Yishun Avenue 7

Singapore 768924

Tel. (65) 7503-192

Fax (65) 7535-485

ASM Shanghai

Room H, 4/F, AI HE Building

629 Ling Ling Road

200030 Shanghai

Peoples Republic of China

Tel. (86) 21-6427 6928

Fax (86) 21-6486 5304

ASM Assembly Equipment

(M) Sdn. Bhd.

Bayan Point, Block A

No. 15-1-23, 15-1-24

Medan Kampung Relau

11900 Penang, Malaysia

Tel. (604) 644 9490/642 0291

Fax (604) 645 1294

ASM Assembly Equipment

(M) Sdn. Bhd.

17 Tingkat Satu,

Taman Sri Mulia Sungai Abong

84000, Muar, Johor, Malaysia

Tel. (606) 951 5713

Fax (606) 951 5786

ASM Assembly Equipment

Bangkok Ltd.

51/3, Vibhavadi Tower, 18/2 Floor

Ngamwongwan Road, Ladyao,

Chathuchak

Bangkok, 10900, Thailand

Tel. (66) 2-941 3181/2

Fax (66) 2-941 3183

®

ASM International N.V. dedicates its resources to the research, development,

manufacturing, marketing and servicing of equipment and materials used to produce

semiconductor devices.

The Company provides solutions for the main areas of semiconductor production:

wafer processing, assembly and packaging.

The Company’s principal facilities in Europe, the United States, South-East Asia and

Japan enable it to meet local specifications and to sell and service its products in the

world’s major semiconductor markets: Europe, the United States and the Far East.

To meet the semiconductor industry’s demand for capital intensive production

solutions, the Company’s design concepts emphasize superior quality, ease of

operation and maintenance, reliability, safety and system integration.

ASM International

4 Financial Highlights and Selected Comparative Financial Data

5 Report from the Supervisory Board

6 Letter to Shareholders

8 ASM, The Process of Innovation

12 Management’s Discussion and Analysis

20 Consolidated Financial Statements20 Consolidated Balance Sheets

21 Consolidated Statements of Operations

22 Consolidated Statements of Comprehensive Income

22 Consolidated Statements of Shareholders’ Equity

23 Consolidated Statements of Cash Flows

24 Notes to Consolidated Financial Statements

40 Independent Auditors’ Report

42 Statutory Financial Statements42 Statutory Balance Sheets

42 Statutory Statements of Operations

43 Notes to Statutory Financial Statements

46 Additional Information

47 Independent Auditors’ Report

48 Common Stock Information

49 Corporate Information

50 ASM Worldwide

Contents

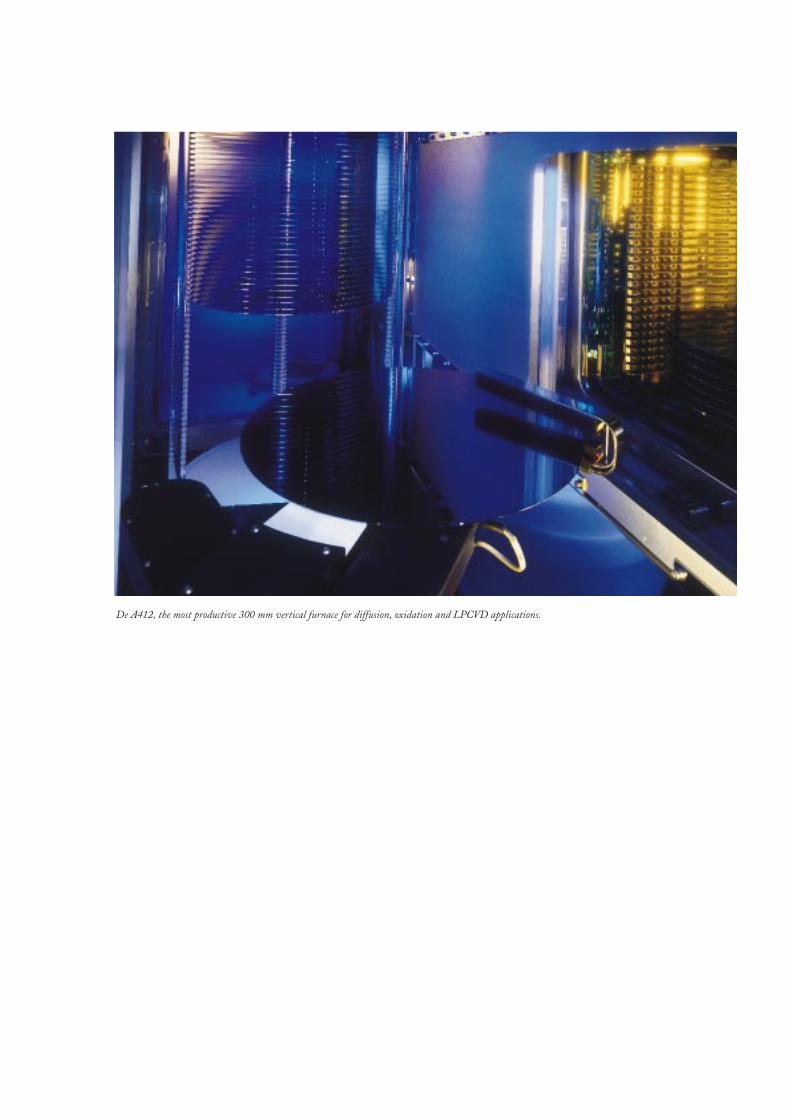

De A412, the most productive 300 mm vertical furnace for diffusion, oxidation and LPCVD applications.

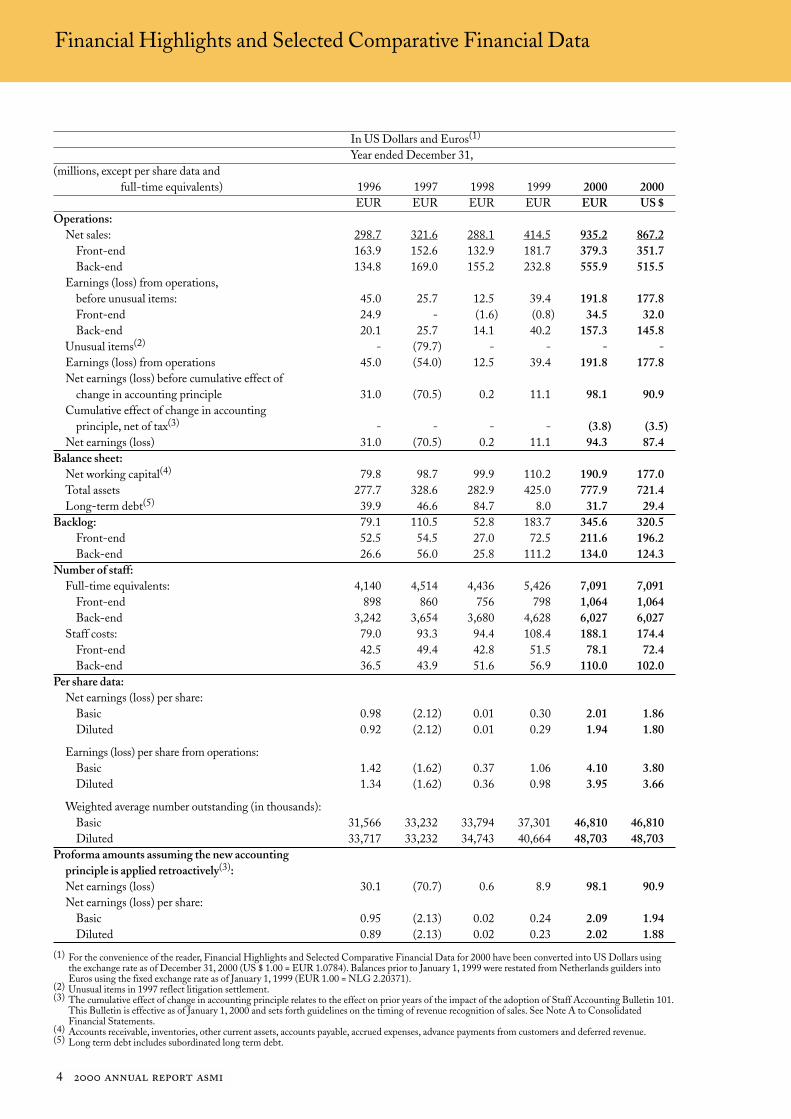

Financial Highlights and Selected Comparative Financial Data

In US Dollars and Euros(1)

Year ended December 31,

(millions, except per share data and

full-time equivalents) 1996) 1997) 1998) 1999) 2000) 2000)

EUR) EUR) EUR) EUR) EUR) US $)

Operations:

Net sales: 298.7) 321.6) 288.1) 414.5) 935.2) 867.2)

Front-end 163.9) 152.6) 132.9) 181.7) 379.3) 351.7)

Back-end 134.8) 169.0) 155.2) 232.8) 555.9) 515.5)

Earnings (loss) from operations,

before unusual items: 45.0) 25.7) 12.5) 39.4) 191.8) 177.8)

Front-end 24.9) -) (1.6) (0.8) 34.5) 32.0)

Back-end 20.1) 25.7) 14.1) 40.2) 157.3) 145.8)

Unusual items(2) -) (79.7) -) -) -) -)

Earnings (loss) from operations 45.0) (54.0) 12.5) 39.4) 191.8) 177.8)

Net earnings (loss) before cumulative effect of

change in accounting principle 31.0) (70.5) 0.2) 11.1) 98.1) 90.9)

Cumulative effect of change in accounting

principle, net of tax(3) -) -) -) -) (3.8) (3.5)

Net earnings (loss) 31.0) (70.5) 0.2) 11.1) 94.3) 87.4)

Balance sheet:

Net working capital(4) 79.8) 98.7) 99.9) 110.2) 190.9) 177.0)

Total assets 277.7) 328.6) 282.9) 425.0) 777.9) 721.4)

Long-term debt(5) 39.9) 46.6) 84.7) 8.0) 31.7) 29.4)

Backlog: 79.1) 110.5) 52.8) 183.7) 345.6) 320.5)

Front-end 52.5) 54.5) 27.0) 72.5) 211.6) 196.2)

Back-end 26.6) 56.0) 25.8) 111.2) 134.0) 124.3)

Number of staff:

Full-time equivalents: 4,140) 4,514) 4,436) 5,426) 7,091) 7,091)

Front-end 898) 860) 756) 798) 1,064) 1,064)

Back-end 3,242) 3,654) 3,680) 4,628) 6,027) 6,027)

Staff costs: 79.0) 93.3) 94.4) 108.4) 188.1) 174.4)

Front-end 42.5) 49.4) 42.8) 51.5) 78.1) 72.4)

Back-end 36.5) 43.9) 51.6) 56.9) 110.0) 102.0)

Per share data:

Net earnings (loss) per share:

Basic 0.98) (2.12) 0.01) 0.30) 2.01) 1.86)

Diluted 0.92) (2.12) 0.01) 0.29) 1.94) 1.80)

Earnings (loss) per share from operations:

Basic 1.42) (1.62) 0.37) 1.06) 4.10) 3.80)

Diluted 1.34) (1.62) 0.36) 0.98) 3.95) 3.66)

Weighted average number outstanding (in thousands):

Basic 31,566) 33,232) 33,794) 37,301) 46,810) 46,810)

Diluted 33,717) 33,232) 34,743) 40,664) 48,703) 48,703)

Proforma amounts assuming the new accounting

principle is applied retroactively(3):

Net earnings (loss) 30.1) (70.7) 0.6) 8.9) 98.1) 90.9)

Net earnings (loss) per share:

Basic 0.95) (2.13) 0.02) 0.24) 2.09) 1.94)

Diluted 0.89) (2.13) 0.02) 0.23) 2.02) 1.88)

(1) For the convenience of the reader, Financial Highlights and Selected Comparative Financial Data for 2000 have been converted into US Dollars using the exchange rate as of December 31, 2000 (US $ 1.00 = EUR 1.0784). Balances prior to January 1, 1999 were restated from Netherlands guilders into Euros using the fixed exchange rate as of January 1, 1999 (EUR 1.00 = NLG 2.20371).

(2) Unusual items in 1997 reflect litigation settlement.(3) The cumulative effect of change in accounting principle relates to the effect on prior years of the impact of the adoption of Staff Accounting Bulletin 101.

This Bulletin is effective as of January 1, 2000 and sets forth guidelines on the timing of revenue recognition of sales. See Note A to ConsolidatedFinancial Statements.

(4) Accounts receivable, inventories, other current assets, accounts payable, accrued expenses, advance payments from customers and deferred revenue.(5) Long term debt includes subordinated long term debt.

4

Financial Highlights and Selected Comparative Financial Data

In US Dollars and Euros(1)

Year ended December 31,

(millions, except per share data and

full-time equivalents) 1996) 1997) 1998) 1999) 2000) 2000)

EUR) EUR) EUR) EUR) EUR) US $)

Operations:

Net sales: 298.7) 321.6) 288.1) 414.5) 935.2) 867.2)

Front-end 163.9) 152.6) 132.9) 181.7) 379.3) 351.7)

Back-end 134.8) 169.0) 155.2) 232.8) 555.9) 515.5)

Earnings (loss) from operations,

before unusual items: 45.0) 25.7) 12.5) 39.4) 191.8) 177.8)

Front-end 24.9) -) (1.6) (0.8) 34.5) 32.0)

Back-end 20.1) 25.7) 14.1) 40.2) 157.3) 145.8)

Unusual items(2) -) (79.7) -) -) -) -)

Earnings (loss) from operations 45.0) (54.0) 12.5) 39.4) 191.8) 177.8)

Net earnings (loss) before cumulative effect of

change in accounting principle 31.0) (70.5) 0.2) 11.1) 98.1) 90.9)

Cumulative effect of change in accounting

principle, net of tax(3) -) -) -) -) (3.8) (3.5)

Net earnings (loss) 31.0) (70.5) 0.2) 11.1) 94.3) 87.4)

Balance sheet:

Net working capital(4) 79.8) 98.7) 99.9) 110.2) 190.9) 177.0)

Total assets 277.7) 328.6) 282.9) 425.0) 777.9) 721.4)

Long-term debt(5) 39.9) 46.6) 84.7) 8.0) 31.7) 29.4)

Backlog: 79.1) 110.5) 52.8) 183.7) 345.6) 320.5)

Front-end 52.5) 54.5) 27.0) 72.5) 211.6) 196.2)

Back-end 26.6) 56.0) 25.8) 111.2) 134.0) 124.3)

Number of staff:

Full-time equivalents: 4,140) 4,514) 4,436) 5,426) 7,091) 7,091)

Front-end 898) 860) 756) 798) 1,064) 1,064)

Back-end 3,242) 3,654) 3,680) 4,628) 6,027) 6,027)

Staff costs: 79.0) 93.3) 94.4) 108.4) 188.1) 174.4)

Front-end 42.5) 49.4) 42.8) 51.5) 78.1) 72.4)

Back-end 36.5) 43.9) 51.6) 56.9) 110.0) 102.0)

Per share data:

Net earnings (loss) per share:

Basic 0.98) (2.12) 0.01) 0.30) 2.01) 1.86)

Diluted 0.92) (2.12) 0.01) 0.29) 1.94) 1.80)

Earnings (loss) per share from operations:

Basic 1.42) (1.62) 0.37) 1.06) 4.10) 3.80)

Diluted 1.34) (1.62) 0.36) 0.98) 3.95) 3.66)

Weighted average number outstanding (in thousands):

Basic 31,566) 33,232) 33,794) 37,301) 46,810) 46,810)

Diluted 33,717) 33,232) 34,743) 40,664) 48,703) 48,703)

Proforma amounts assuming the new accounting

principle is applied retroactively(3):

Net earnings (loss) 30.1) (70.7) 0.6) 8.9) 98.1) 90.9)

Net earnings (loss) per share:

Basic 0.95) (2.13) 0.02) 0.24) 2.09) 1.94)

Diluted 0.89) (2.13) 0.02) 0.23) 2.02) 1.88)

(1) For the convenience of the reader, Financial Highlights and Selected Comparative Financial Data for 2000 have been converted into US Dollars using the exchange rate as of December 31, 2000 (US $ 1.00 = EUR 1.0784). Balances prior to January 1, 1999 were restated from Netherlands guilders into Euros using the fixed exchange rate as of January 1, 1999 (EUR 1.00 = NLG 2.20371).

(2) Unusual items in 1997 reflect litigation settlement.(3) The cumulative effect of change in accounting principle relates to the effect on prior years of the impact of the adoption of Staff Accounting Bulletin 101.

This Bulletin is effective as of January 1, 2000 and sets forth guidelines on the timing of revenue recognition of sales. See Note A to ConsolidatedFinancial Statements.

(4) Accounts receivable, inventories, other current assets, accounts payable, accrued expenses, advance payments from customers and deferred revenue.(5) Long term debt includes subordinated long term debt.

4

We submit herewith the 2000 Annual Report and

Accounts as prepared by the Management Board. As

Supervisory Directors, we have held several meetings

with the Management Board during the year and in our

assessment we have gained sufficient insight in the

Company’s strategy, the business risks, the ongoing

operations, market developments, its organization,

management and financials. The Board monitored the

compliance with the standards given by the Dutch

Corporate Governance Committee. The Board was also

actively involved in the refinancing activities during the

year. It continues to supervise the ongoing efforts to

change the maturity profile of the financing of the

Company into one with more emphasis on permanent

capital.

The Supervisory’s Board Audit Committee met

regularly with the Management Board and Deloitte &

Touche, the Company’s independent auditors. Matters

of discussion were the Company’s system of internal

control, the introduction of the Euro by the Company,

as well as the Company’s accounting principles

(including this year’s change to the new SAB 101 rules

for revenue recognition), the audit performed and its

findings and the 2000 Report and Accounts as prepared

by the Management Board. Deloitte & Touche has

issued an unqualified opinion on the 2000 Accounts

and we submit these Accounts to the General Meeting

of Shareholders for approval. We also recommend to

discharge the Managing Directors for their

management during the year 2000 and to discharge the

Supervisory Directors for their supervision during the

year 2000.

Mr. F.W. Saris retired from the Supervisory Board as of

May 30, 2000. The contributions he made to our

company since 1987 in the areas of technological know-

how and the facilitation of a dialogue with universities

and their students have been much appreciated.

On May 30, 2000 Mr. J.M.R. Danneels was appointed

as Supervisory Director. Mr. Danneels is Director of

Hardware Coordination and Chief Executive Officer of

Alcatel Microelectronics in Zaventem, Belgium.

We thank the staff of ASM International for their

commitment and support shown during the past year.

Supervisory Board,

P.C. van den Hoek

J.M.R. Danneels

J. den Hoed

F.C. Rauwenhoff

Bilthoven,

February 9, 2001

Report from the Supervisory Board

5

Letter to Shareholders

2000 was a breakthrough year for ASM International

- the best in our history. We not only achieved record

results that outperformed the industry for the fourth

consecutive year, we also realized our long-term vision

of market leadership through innovation. ASMI both

gained market share and solidified relationships with

most of the world’s top semiconductor manufacturers,

thus firmly establishing the company as a world-class

supplier of leading-edge capital equipment to the

semiconductor industry.

Of equal importance, ASMI substantially improved its

financial position. Net earnings of H 94.3 million

strengthened our equity position. Two successful

capital market transactions also improved our balance

sheet. In February 2000 we converted US $20 million

zero coupon convertible bonds. In April 2000 we

successfully completed a secondary offering that yielded

net proceeds of approximately H 120 million, which

was then used to substantially reduce our interest

bearing debt. As a result of the refinancing activities

that took place in 2000 and our dramatic growth over

the prior year, we now enjoy good financial health.

Industry outperformance

In a year when the industry had exceptional growth of

85%, our net sales surpassed that, growing 126% year

over year. Profits grew eight-fold from the prior year.

All major product lines in both Front-end and

Back-end businesses reported record sales for the year.

While we are proud of our financial performance this

year, we are equally enthusiastic that ASMI’s growth

has been organic, and stems from our broad range of

products and enabling technologies strategically

developed over the past several years. The increased

demand for all our products, the gain in new customers,

and expansion of market share validate our commitment

and our confidence in the quality of our core technology

platforms.

Meeting industry challenges:

The ASMI advantage

As a result of years of strategic initiatives and pioneering

new technologies, ASMI is strongly positioned to

capitalize on the semiconductor industry’s rapid evolution

toward smaller, faster and cheaper products. With

breakthrough technologies for 100 nanometer and

smaller device manufacturing, and system solutions for

the major assembly processes, ASMI holds a clear

competitive advantage in our industry today.

All of ASMI’s products directly address the major

drivers of our industry’s growth: shrinking feature sizes,

the move toward larger (300 mm) wafers, the need for

higher manufacturing productivity at lower costs, as

well as the demand for new materials and process

solutions, such as Silicon-Germanium epitaxy, copper

and low-k, “systems on a chip”, and “flash memory”.

Our leading-edge equipment and process technologies

enable the manufacture of advanced high speed and

high frequency devices used in wireless and broadband

applications, and other high growth semiconductor

markets including automotive applications, optical

networks, digital cameras and other hand-held devices.

Adding to ASMI’s competitive strength is our unique

position as world-class supplier to both the Front-end

and Back-end segments of the capital equipment market.

This not only enables us to participate dynamically in

the future of both segments, but due to the slightly

different demand cycles of wafer processing and

assembly and packaging, also helps stabilize our

company’s growth. Our ability to capitalize on our

diversification has clearly paid off, as is evident in our

outstanding results in 2000.

Assembly and packaging portfolio

ASM Pacific Technology Ltd. (‘ASMPT’), our

55-percent owned Back-end subsidiary, supplying

assembly and packaging products, contributed

significantly to 2000 first half year performance. This

year ASMPT became the world’s second-largest

Back-end equipment supplier, moving up from

number five. More importantly, ASMPT is the most

profitable company worldwide in its sector.

As a provider of both innovative low-cost solutions and

leading-edge technology, ASMPT is the only company

in the world today that manufactures equipment for all

6

major steps in assembly and packaging. In the year,

ASMPT’s award winning AB339 gold wire bonder

continued to gain major volume orders, as the next-

generation gold wire bonder entered the mass production

phase in the fourth quarter.

Wafer processing portfolio

In the second half of the year, while the chip assemblers

digested their extraordinarily high level of equipment

purchases, our Front-end wafer processing products

took the lead in order momentum.

Our epitaxial reactors, our plasma-enhanced chemical

vapor deposition (PECVD) product line and our vertical

furnaces increased market share across geographical

markets and with the top semiconductor producers.

Due to the success of our new applications in Silicon-

Germanium, our epitaxial line held its number one

market position, with over 70% market share. In

PECVD, we rank among the top three players, and

are the market leader in atomic layer deposition

(ALD). In vertical furnaces, ASMI became the world’s

third largest supplier, having added customers every

quarter since our market entry in 1993. We currently

maintain the largest installed base for 300 mm vertical

furnaces in the industry.

Financial management

On January 1, 2001, we welcomed Robert L. de Bakker

to our ASMI management team. He joins ASM

International as Chief Financial Officer, succeeding

Rinse de Jong, who retired early in 2001. Mr. de Bakker

brings extensive experience in financial management

of industrial companies. He was formerly Chief

Financial Officer of NKF Holding N.V., a Dutch

multinational industrial cable company.

Outlook

As we enter 2001, our markets are digesting record

capital equipment spending in 2000. At the same time,

the fundamental drivers of our industry remain

unchanged, fueling our optimism for stable long-term

growth.

Since the market for technology enabling solutions,

such as atomic layer deposition, copper, low-k and 300

mm is generally less susceptible than standard

products to market consolidations, these pockets of the

equipment market are expected to be relatively healthy

in the coming year.

Since ASMI’s portfolio of leading edge equipment for

these segments of the market is now stronger than ever,

we are confident that our company will use the

short-term negative market developments in 2001 to

further improve its competitive position.

While ASMI has gained significant market share over

the past 4 years, we feel that the years ahead present

abundant opportunities for our company, and our

industry. It is our intention to take every advantage of

those opportunities, building upon our record

achievements in 2000, to further enhance our company’s

value for our customers, our employees, and our

shareholders.

Arthur H. del Prado

President and Chief Executive Officer

Bilthoven,

February 9, 2001

7

ASM - The Process of Innovation

The basic driving forces behind continued industry

growth can be summarized as enhanced device

performance or speed, decreased size, and lower costs.

This is achieved mainly by:

• Decreasing the feature size or linewidth-device

scaling;

• Increasing wafer size;

• Improving yield and productivity.

The latter two points mainly affect the device cost,

while device scaling influences all the industry drivers.

By making the transistor - the basic building block of

the device - smaller, it also performs operations faster.

If transistors are smaller, a device with a certain

functionality becomes more compact. Thus, more

devices can be placed on a single wafer, and production

cost is reduced. But, as linewidths get smaller, layer

thickness must also decrease. With each generation,

this can lead to the introduction of new materials and

technologies such as atomic layer deposition (ALD),

and rapid thermal processing (RTP).

Historically, a change in the linewidth of 0.7x, meaning

about twice as many transistors can be placed on a

given wafer surface, occurred every three years.

Recently, however, the introduction of a new technology

generation has been accelerating, occurring every two

years. The industry is responding by introducing new

materials and technologies also at a faster rate.

ASMI has positioned itself to work within a two-year

generation cycle. Today, ASMI is leveraging its

capabilities to support 130 nm technology equipment,

beta testing for 100 nm technology, and the development

of 70 nm technology. For reference, 100 nm is 0.1

micron or 1/10000 of a millimeter.

To decrease costs, wafer sizes increase by a factor of 1.5

times approximately every 9-12 years. The industry is

currently transitioning from 200 mm to 300 mm wafers.

The number of devices that can be placed on a 300 mm

wafer is about 2.4 times greater than on a 200 mm or

8 inch wafer. The greater number of devices compensates

for the higher cost of 300 mm equipment. Presently, all

large semiconductor companies have committed to 300

mm facilities with about 25 plants already announced

for startup over the next two years. ASMI participates

in at least two out of every three 300 mm startups.

Pushing frontiers

Over the years, ASMI has invested heavily in both

core and new technologies. We continue to both pioneer

new technologies and push the frontiers of existing

technologies in order to move to smaller, better

performing and lower-cost transistors. What we are

seeing today is a merging of our long-term strategies

with our new competencies.

ASMI has followed a roadmap that includes both

Front-end and Back-end capabilities and batch and

single wafer processes.

Because of our position in both Front-end and Back-end

semiconductor equipment, we are the only company in

the industry that can address the complexities of copper

connection in both of these segments. Optimal

integration of these historically separate technologies

is crucial to yielding the best device performance at

the lowest cost.

ASMPT has now taken the technological lead in

leadframe-based alternatives for substrate-type chip

scale packages. With both equipment and materials

technology, ASMPT is perfectly positioned to provide

an integrated solution that affords a small footprint

package at a lower cost.

ASMI’s Front-end product portfolio includes both

batch and single wafer processing technologies. This

enables us to respond quickly to industry dynamics.

Due to the inherent robustness of batch systems, we

believe they will retain their desirability, particularly

where cycle time is not a major factor. On the other

hand, in selected applications, and especially those

where cycle time plays an important role, single wafer

processing may be preferred. ASMI’s flexibility and

experience in both processes ideally positions us to

address both markets.

In addition to our ability to respond to migrating

technologies and new materials in our existing

addressable markets, ASMI has an extensive record of

pioneering new technologies. Today, we are extending

our know-how into critical areas necessary to effect

solutions for the next generation of changes in the

microelectronics industry. The newest components of

our intellectual property portfolio, patent protected,

include systems and processes for ALD, RTP, copper

and low-k.

Unique production solutions

ASMI’s position in the accelerating technology scenario

has never been better. Our product portfolio supports

the industry’s changes. Productivity improvements and

the development of a complete set of 300 mm solutions

place our existing products such as the Advance 400,

Industry Trends

8

Epsilon and Eagle series reactors as major contenders

in the coming 300 mm investment waves for 130 and

100 nm technology devices.

At the same time, ASMI developed a new product

portfolio for next generation devices with linewidths

of 100 to 70 nm. These devices will enter mass

production in two to four years. The development of

our Pulsar ALD and RTP equipment is essential for

the production of those devices.

Smaller and faster transistors

As a CVD company, ASMI must match the shrinkage

in transistors, achievable by reducing linewidths from

current advanced levels of 0.18 micron through

successive steps down to sub 0.1 micron levels with the

ability to deposit thinner yet very uniform films. In

our Back-end group, we must supply smaller assembly

and packaging methods to protect the advantages

garnered in the Front-end processes.

Smaller transistors require extremely thin insulating

layers. Presently, standard silicon oxide can be used to

a thickness of six atoms, suitable for 130 to 100 nm

technology. These layers can be constructed with our

Advance 400 series reactors.

However, to get to a thickness of less than four atoms,

which is required for even smaller devices, new

materials and processes are required. ASMI’s solution

is Atomic Layer CVD™, depositing layers with atomic

control of flatness and composition, which satisfies

requirements of 100 to 70 nm transistors. ASMI,

IMEC and Philips Electronics have already

demonstrated the feasibility of such a thin dielectric

with very desirable properties. In addition to logic devices,

such thin insulating layers are also necessary for

memory devices such as flash memory and DRAMS.

ASMI’s market leadership in the area of atomic layer

deposition is firmly established with the ALCVD™

processes in the Pulsar and or Polygon cluster platform.

A breakthrough technology, for thin film applications,

atomic layer deposition is viewed as a successor

technology to many existing physical and chemical

vapor deposition processes.

Smaller transistors also require increasingly thinner

electrical contacts, or junctions, on the transistor. RTP,

which minimizes the time a wafer is exposed to high

temperatures, is essential to achieve such thin junctions.

ASMI’s Levitor RTP system uses gas-bearing principles

to hold a silicon wafer one-tenth of a millimeter

between the surface of two large refractory material

blocks for heating. With its floating wafer concept, it

has demonstrated heat-up rates that are twice as fast

as any radiantly heated systems. In addition, the

Levitor offers lower cost, reduced energy consumption

and high throughput.

Faster transistors, such as those required for wireless

devices, are being made with the Epsilon Silicon

Germanium processes. The Epsilon continues to hold

its dominant position in this growth market. Silicon

Germanium-Carbonfilms are the next step-up in chips

for wireless broadband applications and are now being

installed at customers for qualification.

A third area that ASMI has focused on is the

interconnections between the transistors. A greater

number of transistors must be electrically connected

with thinner and thinner wires. This has driven the

migration to copper as a conductor, replacing

aluminum, and a low-k insulator, which reduces

interaction between adjacent wires.

ASMI’s solution to reducing interaction between

adjacent wires is the Aurora low-k insulator. The

amount of interaction can be characterized by the

k-value. Aurora insulators with a k-value of 2.7

(compared to k=4 for conventional insulators) can be

deposited with our Eagle PECVD equipment. The

Aurora 2.7 process thus reduces interaction by 30% to

40%. A future generation, Aurora 2.0, currently in

development, is expected to provide a 50% reduction.

In order to provide adhesion and prevent interaction

between the copper and low-k insulator, a thin

so-called barrier and seed layer is required in-between

the copper and insulator. These layers need to uniformly

cover all surfaces. ALD films generally follow the

surface of the semiconductor perfectly. This makes

ASMI’s ALCVD technology ideal for this application.

Shrinking the dimension of chips and simultaneously

increasing their functionality affects the Back-end

production processes as well. We lead the industry

with fine pitch ball bonding capability. With successive

chip generations, the number of leads, or wires, must

increase on a smaller surface. This requires smaller

distances between the wires without the leads

interfering with each other. Our bonders have decreased

the physical distance between wires to 35 microns,

compared to an industry average of just 50 microns.

The complexities of copper connection extend also to

the assembly and packaging of devices. While studying

ways to reduce the impact of the high cost of new metal

�

9

ASM - The Process of Innovation (continued)

layers in the semiconductor structure of newer complex

devices, ASMI is looking for solutions both in the

semiconductor structure itself and the subsequent steps

where the semiconductor connects to the outside

world. ASMI is working on improved solutions for

copper, low-k and systems in a package by combining

its expertise in Front-end and Back-end competencies.

Wafer sizes and productivity

Wafer sizes affect the cost of semiconductor devices.

With 2.4 more dies derived per 300 mm wafer than

the prior generation, 300 mm equipment becomes

cost-effective despite the incremental cost.

ASMI was early in this generation change with a full

line of 300 mm equipment covering epitaxy,

LPCVD/diffusion/oxidation and PECVD. Our 300

mm vertical furnace, the A412, is in every 300 mm

pilot line in the world today, and it was the first 300

mm vertical furnace used in a production line.

For all newer offerings such as ALCVD and the Levitor

RTP system, 300 mm equipment is under development

and we expect to ship first products in 2001.

We have integrated metrology, measuring layer

thickness, uniformity and particle count, in our 300 mm

vertical furnace tool set. ASMI’s goal is to incorporate

metrology in all of its product offerings. Integrated

metrology allows the customer to reduce cycle time,

increase yield and throughput, and lower the overall

cost of production.

To satisfy the trend to automation in Back-end

processes, we offer a fully-automated Back-end

production line from die bonding and wire bonding,

to encapsulation and trim and form. This enables our

customers to meet their total system requirements by

offering the most innovative solution to assembly and

packaging, based on our own modular hardware and

software.

Research alliances

To expand and enhance our advanced research

capabilities beyond our own facilities located in the

principal semiconductor markets of the world, ASMI

is engaged in alliances with renowned customers and

institutes.

During 2000, we initiated a partnership with IHP, a

German research institute, to further enhance SiGe films.

These enhanced films will serve the rapidly expanding

need for more bandwidth in telecommunications

applications.

Our relationships with European research laboratories,

including IMEC in Belgium, LETI in France, and the

University of Helsinki in Finland, were strengthened

over the year. Such co-operations enable ASMI to not

only develop new films and process steps but also to

incorporate these steps in the process flow to complete

working devices.

Capacity additions

ASMI is at an exciting juncture in the company’s

history. 300 mm is a reality. As our 300 mm line

continues to gain broad customer acceptance, ASMI

took several steps in the year to expand our 300 mm

production capacity:

In Almere, the Netherlands, a new facility dedicated

to 300 mm furnace production is scheduled to open

Summer 2001, more than doubling ASMI’s furnace

capacity.

Our US subsidiary, ASM America, broke ground for a

demonstration laboratory and a Class-1 cleanroom to

showcase 300 mm and other leading-edge processes.

In June, 2000 ASM Japan opened a new Class-10

cleanroom facility at its Daini Technology Center, to

accommodate our growth in the Japanese market.

During the year, we also qualified additional

subcontractors and outsourced manufacturing of more

Front-end products to help balance production resources

with anticipated demand for our new product families.

ASMPT also took major steps in capacity expansion.

At its China factory, new equipment was added and

the construction of two nearby satellite plants was

completed.

To support ASMPT’s Singapore facility, a new

Malaysian factory came on stream early in 2000.

These additions not only strengthen ASMPT's ability

to meet rising demand for its products, but also help

maintain acceptable delivery lead times for its customers.

10

Floating wafer concept of the Levitor.

11

Management’s Discussion and AnalysisManagement’s Discussion and Analysis of Financial Condition and Results of Operations

We are a leader in the design, manufacture and sale

of equipment and solutions used to produce

semiconductor devices. Our production equipment

and solutions are used by both the Front-end and

Back-end segments of the semiconductor market. We

were incorporated under the laws of the Netherlands

in 1968. Throughout our history, we have conducted

business through subsidiaries located worldwide. We

established our operations in Hong Kong in 1975, in

the United States in 1976, in Japan in 1982, and in

Finland in 1999 through the acquisition of

Microchemistry Ltd. We completed our initial public

offering in the United States in 1981 and in the

Netherlands in 1996. We completed subsequent

public offerings in the United States in 1983 and in

the United States and the Netherlands in 2000. Our

common shares are listed on the Euronext

Amsterdam in the Netherlands and the Nasdaq

National Market in the United States.

We conduct our Back-end operations through ASM

Pacific Technology Ltd (‘ASMPT’), which was our

wholly-owned subsidiary until 1988, when we

completed an initial public offering of 25% of its

shares on the Hong Kong Stock Exchange. We have

since sold and purchased shares of ASMPT on the

open market, and as of December 31, 2000, we

owned 54.62% of its outstanding shares. ASMPT

expanded operations with significant new production

facilities in Shenzhen, China in 1989, Singapore in

1990, and completed new plants in China and

Malaysia in 2000.

The sales cycle from quotation to shipment for our

Front-end equipment generally ranges from five to

nine months, depending on capacity utilization and

the urgency of the order. The acceptance period after

installation may be as short as four to five weeks. If

customers are unfamiliar with our equipment or are

receiving new product models, the acceptance period

may take as long as ten weeks. The sales cycle is

longer for equipment which is installed at the

customer’s site for evaluation prior to sale. The typical

trial period ranges from six months to one year after

installation.

The sales cycle for Back-end products typically is

shorter than for Front-end. Generally, the majority of

our Back-end equipment is built in standard

configurations. We build Back-end products that are

approximately 85% complete in anticipation of

customer orders. Upon receipt of a customer’s order

and specifications, the remaining 15% of the

manufacturing is completed. This allows us to complete

the assembly of our equipment in a short period of

time. We therefore require between two to six weeks

for final manufacturing, testing, crating, and shipment

of our Back-end equipment. Our Back-end customers’

acceptance periods generally are shorter than those

for Front-end equipment. We provide installation,

training and technical support to our customers with

local staff in all of our major markets.

Effective January 1, 2000 the Company adopted new

guidance on revenue recognition as is described in

Staff Accounting Bulletin No. 101 “Revenue

Recognition in Financial Statements” (“SAB 101”),

issued by the staff of the Securities and Exchange

Commission (the “SEC”) in December 1999. See

Note A to Consolidated Financial Statements.

Net revenues include product revenues derived

primarily from sales of Front-end and Back-end

equipment used by both segments of the

semiconductor market. The Company recognizes

revenue from equipment sales upon shipment of its

products when it is proven prior to shipment that the

equipment has met all of the customers’ criteria and

specifications. The installation process is not believed

to be essential to the functionality of the Company’s

products. However, since under most of the Company’s

sales contracts, the timing of payment of a portion of

the sales price is coincident with installation, such

installation is not considered to be inconsequential or

perfunctory under the guidance of SAB 101.

Therefore, at the time of shipment, the Company

defers that portion of the sales price related to the

fair value of installation at the time of shipment. The

Company believes it has an enforceable claim for that

portion of the sales price not related to the fair value

of the installation should it not fulfill its installation

obligation. The fair value of the installation process is

measured based upon the per-hour amounts charged

by third parties for similar installation services. When

the Company can only satisfy the customer acceptance

criteria or specifications at the customer’s location,

revenue is deferred until final acceptance by the

customer or until contractual conditions lapse.

The Company provides training and technical support

to customers. Revenue related to such services are

recognized when the service is completed. Revenue

from the sale of spare parts and materials is recognized

when the goods are shipped.

The Company previously recognized revenue from

the sale of all equipment sales including installation

services at the time of transfer of title, and when no

Overview

12

significant contractual obligations remained. Revenue

recognition for sale of spare parts and services has not

been changed.

The adoption of the new accounting principle for

revenue recognition as of January 1, 2000 based on the

new guidance of SAB101 has an effect on the amounts

of revenue and net earnings reported in previous

periods. The effect of this change as of January 1,

2000 was to defer H 12.2 million net sales and H 3.8

million net earnings to future periods. The effect on

net earnings as of January 1, 2000 has been recorded

as a cumulative effect of change in accounting

principle in the Statement of Operations for the year

ended December 31, 2000.

Our Front-end sales are primarily concentrated in the

United States, Europe, Japan and South-East Asia.

During 2000, equipment shipped to destinations in

these regions accounted for sales of H 110.4 million,

H 87.0 million, H 108.7 million, and H 73.2 million,

respectively. Our Back-end sales, which approximated

H 555.9 million, are concentrated in Asia. Our ten

largest customers in 2000 accounted for approximately

45.2% of total sales.

We invested approximately H 73.8 million in research

and development during 2000. As part of our

research and development activities, we are engaged

in various development programs with customers and

institutes that allow us to develop products that meet

customer requirements and to obtain access to new

technology and expertise. We expense our research

and development costs. We charge to costs of sales

the costs which relate to prototype and experimental

models which we subsequently sell to customers.

Our reported research and development expenses are

after research and development credits, which

approximated H 2.2 million in 2000. Our Netherlands,

Belgium, Finnish and Singapore operations receive

research and development grants and credits from

various governmental sources. The research and

development grants we received in the Netherlands

are contingently repayable to the extent we recognize

sales of products to which the credit was related. These

repayments vary and range from 1.0% to 4.0% of the

realized sales, depending on the products sold. Our

actual and contingent repayments accrue interest at

rates ranging from 5.0% to 8.0% per annum. Our

contingent liability related to these possible repayments

approximated H 12.0 million at December 31, 2000.

During the first quarter of 1999, the Company

decided to close its manufacturing activities for wafer

processing equipment in the United States and in

combination therewith, to outsource to third parties

the manufacturing of substantially all parts previously

manufactured in-house. Concurrently, the United

States assembly and test activities were combined

with those in Europe. This resulted in a reduction in

employees in the United States by approximately 75

and in the vacating of certain facilities.

Approximately 50 new positions were created in

Europe. The Company incurred a restructuring

charge, covering employee terminations, write-offs

and occupancy costs of H 3.9 million associated with

these decisions.

The Company’s intention was to begin implementing

the steps necessary to complete the 1999 restructuring

program immediately on formalization thereof and to

substantially complete all necessary steps by the end

of 1999. At December 31, 1999, however, there was a

remaining accrual associated with the restructuring

program of H 2.5 million; implementation of certain

elements of the program had been delayed due to

longer than anticipated time taken to transfer certain

operations to Europe where plant modifications were

required. At December 31, 1999, the revised schedule

for completion of the program was mid 2000.

In the first half of 2000, the global demand for wafer

processing equipment and, as a consequence, the

assembly and final testing activities of such

equipment, increased sharply when compared to the

same period in 1999. The Company’s European

facilities and the Company’s third party subcontractors

had difficulty in coping with the significantly higher

volumes. Consequently, the Company decided to

partially reverse its earlier decision and reopened

facilities that were vacated under the 1999 restructuring

program. As a consequence, part of the restructuring

provision mainly related to legal contractual obligations

for leased properties in the amount of H 1.6 million

was reversed and credited to selling, general and

administrative expenses in the Consolidated Statement

of Operations in the second quarter of 2000.

Effective in July 1999, we purchased all of the

outstanding shares of Microchemistry, a company

located in Finland, for approximately H 3.9 million. In

September 1999 Microchemistry was renamed ASM

Microchemistry. Prior to our purchase, Microchemistry

developed the process to grow or deposit films one

layer at a time by means of ALCVD, and marketed

ALCVD processes to manufacturers of flat panel

displays and tape magnetic head products. Following

our acquisition, ASM Microchemistry is shifting its

focus to manufacturers of semiconductor devices.

�

13

In December 1999, we purchased a 24% interest in

NanoPhotonics AG, a German supplier of precision

thin film metrology equipment for H 338,000. The

technology supplied by NanoPhotonics allows for the

integration of high-resolution, ellipsometric thin film

metrology directly in a wafer-processing tool. We

believe that this investment will enable us to equip

our batch and single wafer equipment with integrated

thin film metrology.

In April 2000, the Company completed a public

offering of 4,250,000 common shares at a price of

US $ 29.00 per share. The net proceeds amounted to

H 119.7 million, which were used to repay

outstanding loans and funding of the Company’s

working capital needs.

Following the issuance of common shares under the

ASMPT Employee Incentive Scheme in March

2000, the Company’s shareholding in ASMPT

dropped slightly below 50%. In various transactions

in April and June, the Company acquired 0.3% of the

outstanding common shares of ASMPT, thereby

restoring its total shareholding in that company to

over 50%. Throughout this entire period, the

Company maintained control over ASMPT. On July 6,

2000, the Company completed a purchase of

approximately 4.7% of the outstanding common shares

in ASMPT from one institututional investor. At

December 31, 2000, the shareholding in ASMPT

amounts to 54.62% of the outstanding common shares.

As of December 31, 2000, we had net operating loss

tax carryforwards of H 260 million which we

can mainly apply against earnings reported in the

United States and the Netherlands.

The market value of our investment in ASMPT at

the end of 2000 was approximately H 318.4 million,

which is lower than the market value at the end of

1999, which was approximately H 333.9 million.

Results of Operations

Year Ended December 31, 2000 Compared to Year Ended

December 31, 1999

Net Sales. The market for semiconductor equipment

was strong in the first three quarters of the year and

started to become weaker at the end of the year.

Consolidated net sales increased 125.6% to

H 935.2 million in 2000 compared to H 414.5 in

1999. Front-end sales increased 108.8% from H 181.7

million in 1999 to H 379.3 million in 2000. Back-end

sales increased 138.8% from H 232.8 million in 1999

to H 555.9 million in 2000. The Front-end sales

increase was over all product lines. The Back-end sales

increase was primarily due to increased sales of

equipment and to a lesser extent, leadframes.

Gross Profit. Our consolidated gross profit increased

from 41.0% of net sales in 1999 to 44.6% of net sales

in 2000. The Front-end business gross profit decreased

slightly from 40.5% of net sales in 1999 to 40.3% of

net sales in 2000, while the Back-end division gross

profit grew from 41.4% of net sales in 1999 to 47.6%

of net sales in 2000. The decrease in gross profit as a

percentage of sales in Front-end is, despite efficiency

improvements in the manufacturing of existing product

lines, caused by initial lower margins on the introduction

of new technology in ALCVD and 300 mm

equipment. The improvement by our Back-end

segment was achieved through manufacturing

efficiencies related to the increased volumes and partly

through better pricing conditions for our products.

Selling, General and Administrative. Our selling,

general and administrative expenses increased from

H 83.2 million in 1999 to H 147.3 million in 2000.

Front-end and Back-end selling, general and

administrative expenses increased from H 48.6 million

and H 34.6 million in 1999 to H 66.2 million and

H 81.1 million in 2000. Throughout this year, we

have been investing in the expansion of our support

and overhead departments in order to handle

increased product and order volumes. Staff levels

increased from 2,387 as of December 31, 1999 to

2,895 as of December 31, 2000. As a percentage of

net sales, selling, general and administrative expenses

decreased from 20.1% for 1999 to 15.8% for 2000.

Amortization of Goodwill. The amortization of goodwill

increased from H 0.3 million in 1999 to H 4.3 million

in 2000. This increase relates to the amortization of

goodwill resulting from the acquisition of an additional

5.0% in ASMPT in 2000 and the acquisition of

Microchemistry and NanoPhotonics in 1999.

Research and Development. Research and development

expenses increased by 56.5% from H 47.1 million in

1999 to H 73.8 million in 2000. Front-end research

and development expenses increased by 63.4% from

H 29.3 million in 1999 to H 47.9 million in 2000

while Back-end research and development expenses

increased 45.2% from H 17.8 million in 1999 to

H 25.9 million in 2000. Net research and development

expenses declined from 11.4% of net sales in 1999 to

7.9% of net sales in 2000. The amounts of research

and development credits offset against research and

development expenses amounted to H 3.3 million in

Management’s Discussion and Analysis (continued)Management’s Discussion and Analysis of Financial Condition and Results of Operations

14

�

1999 and H 2.2 million in 2000. Investments in

research and development have been concentrated on

the products that have pushed our growth in the last

three years. In Front-end the concentration was on

high-k dielectrics, low-k dielectrics, ALD, RTP and

300 mm process applications while in Back-end our

concentration was on performance improvements and

the release of new or upgraded products.

Net Interest and Other Financial Income (Expenses).

Net interest and other financial income (expenses)

decreased by 81.5% from a net expense of H 8.6 million

in 1999 to a net expense of H 1.6 million in 2000 due

principally to the repayment of short-term loans with

the proceeds of the public offering of common shares

we completed in April 2000 and with cash generated

from operations. The strength of the US Dollar, the

Hong Kong Dollar versus the Euro, our reporting

currency, resulted in transaction exchange gains.

Income Taxes. We incurred H 22.8 million in income

taxes during 2000, compared to H 1.3 million in 1999.

As of December 31, 2000, we have a H 260 million

net operating loss carryforward which we mainly can

apply against future earnings reported in the United

States and the Netherlands.

Net Earnings. Our net earnings in 2000 were

approximately H 94.3 million compared to H 11.1

million in 1999. These 2000 net earnings were

influenced by a cumulative effect of change in

accounting principle of H 3.8 million due to the

adoption of new accounting guidelines for revenue

recognition. Our Front-end operation reported net

earnings before the cumulative effect of change in

accounting principle of H 16.8 million in 2000

compared to a net loss of H 7.8 million in 1999. Our

portion of our Back-end operation's net earnings

before the cumulative effect of change in accounting

principle was H 81.3 million compared to H 18.9 mil-

lion in 1999.

Year Ended December 31, 1999 Compared to Year Ended

December 31, 1998

Net Sales. While the market for semiconductor

equipment was still weak in the first quarter of 1999,

net sales increased in both Front-end and Back-end

segments during the second through fourth quarters

of 1999 and consolidated sales increased by 43.9% in

1999 compared to 1998. Front-end sales increased

36.8% from H 132.9 million in 1998 to H 181.7 million

in 1999. Back-end sales increased 49.9% from

H 155.2 million in 1998 to H 232.8 million in 1999.

The Front-end sales increase was primarily due to

higher sales of our Eagle 10 products. The Back-end

sales increase was primarily due to increased sales of

equipment and to a lesser extent, leadframes. Pricing

in the leadframe market, which was depressed in

1998, improved in 1999.

Gross Profit. Our consolidated gross profit increased

from 37.8% of net sales in 1998 to 41.0% of net sales

in 1999. The Front-end business gross profit increased

from 39.4% of net sales in 1998 to 40.5% of net sales

in 1999, while the Back-end division gross profit grew

from 36.4% of net sales in 1998 to 41.4% of net sales

in 1999. Semiconductor equipment market growth in

the second half of 1999 led to an easing of pricing

pressures experienced during 1998. In addition, our

introduction of new process technology helped

improve our margins.

Selling, General and Administrative. To keep pace with

the general semiconductor market expansion and to

meet increasing customer orders in 1999, selling, general

and administrative expenses increased from H 60.0

million in 1998 to H 83.2 million in 1999. Front-end

and Back-end selling, general and administrative

expenses increased from H 30.2 million and H 29.8

million in 1998 to H 48.9 million and H 34.6 million

in 1999. Increased costs primarily reflected expansion

in personnel and the restructuring of the ASM America

manufacturing related operations. However, selling,

general and administrative expenses as a percentage of

net sales declined from 20.8% in 1998 to 20.1% in 1999.

Research and Development. Research and development

expenses increased by 30.0% from H 36.3 million in

1998 to H 47.1 million in 1999. Front-end research

and development expenses increased by 23.4% from

H 23.7 million in 1998 to H 29.3 million in 1999

while Back-end research and development expenses

increased 42.3% from H 12.6 million in 1998 to

H 17.8 million in 1999. Net research and

development expenses declined from 12.6% of net

sales in 1998 to 11.4% of net sales in 1999. The

amounts of research and development credits offset

against research and development expenses amounted

to H 5.2 million in 1998 and H 3.3 million in 1999.

Net Interest and Other Financial Income (Expenses).

Net interest and other financial income (expenses)

increased by 60.9% from H 5.4 million in 1998 to

H 8.6 million in 1999 due to the repayment of a non-

interest bearing short-term loan which became due in

November 1998 with an interest-bearing, longer term

loan with warrants. In addition, in October 1999 we

issued a zero-coupon US $14.9 million debenture

with a maturity value of US $20.0 million which

15

accrued interest at 6% per annum, and which had

warrants attached. We also borrowed more frequently

on our revolving lines of credit to finance receivables

and work-in-process which, on average, were larger

in 1999 than in 1998.

Income Taxes. We paid H 1.3 million in income taxes

during 1999, compared to H 0.6 million in 1998. As of

December 31, 1999, we had a H 275 million net

operating loss carryforward which we can apply

against future earnings reported in the United States

and the Netherlands.

Net Earnings. Our net earnings in 1999 were

approximately H 11.1 million compared to H 0.2 million

in 1998. Our Front-end operation reported a net loss

approximating H 7.8 million in 1999, including the

H 3.9 million restructuring charge incurred in

connection with moving manufacturing operations from

ASM America to ASM Europe. Our Front-end

operation’s net loss in 1999 was larger than its net loss

in 1998 approximating H 6.6 million. Our portion of

our Back-end operation’s net earnings approximated H

18.9 million compared to H 6.8 million in 1998.

Backlog

Our backlog of orders booked increased from

approximately H 183.7 million at December 31, 1999

to approximately H 345.6 million at December 31,

2000, of which a substantial majority was for

deliveries in the first and second quarter of 2001.

Our backlog consists of orders of products by

purchase orders or letters of intent for future periods,

typically for up to the next twelve months. In

markets such as Japan it is common practice for

letters of intent to be used in place of firm purchase

orders. We sometimes allow customers to cancel or

reschedule deliveries. In addition, purchase orders are

subject to price negotiations and changes in

quantities of products ordered as a result of changes

in customers’ requirements. Depending on the

complexity of an order, we generally ship our

products from one to six months after receipt of an

order. We include in the backlog only orders for

which a delivery schedule has been specified and to

which the customer has assigned an order number.

Liquidity and Capital Resources

Our liquidity is affected by many factors, some of

which are related to our ongoing operations and

others of which are related to the semiconductor and

semiconductor equipment industries and to the

economies of the countries in which we operate.

Although our cash requirements will fluctuate based

on the timing and extent of these factors, we believe

that cash generated by operations, together with the

liquidity provided by our existing cash resources and

the arrangements governing our current indebtedness,

will be sufficient to fund working capital, capital

expenditures and other ongoing business requirements.

In addition, we have equipment in the field that is

being evaluated by customers. This ‘seeding’ of new

equipment is an important tool for us to enlarge our

customer base and our installed base, requiring

significant capital during the evaluation period.

At December 31, 2000 our principal sources of

liquidity consisted of H 106.8 million in cash and

cash equivalents and H 68.5 million in undrawn bank

lines. H 89.7 million of the cash and cash equivalents

and H 48.8 million of the undrawn bank lines are res-

tricted to use in our Back-end operations.

During 2000, operating activities generated a net

cash inflow of H 153.1 million as compared to H 46.9

million during 1999. The increase was primarily due

to higher cash flow from operations, which was

partially offset by a net outflow of H 72.7 million in

other assets and liabilities in 2000 compared to a

H 7.9 million outflow in 1999. These outflows

resulted primarily from an increase in accounts

receivable and inventories due to the increase in

business activities in 2000. Cash flow used in

investment activities amounted to H 136.4 million

during 2000, an increase compared to H 26.8 million

in 1999. Those investments were made to increase

our manufacturing and assembly capacity, particularly

to complete new plants in Malaysia and China.

In April 2000, we completed a public offering of

common shares, which gave us net proceeds of

approximately H 119.7 million. We used H 76.8 million

of these proceeds for repayment of loans. Following

the repayment, the assets securing these loans have

been released from their liens.

In July 2000, we completed the purchase of

approximately 4.7% of the outstanding shares in

ASMPT, bringing our total shareholding in this

company to 54.88% at that date. The investment,

including some smaller purchases of shares in April

and June of this year, amounted to H 75.5 million.

The purchase was funded with cash and with the

proceeds of a two-year loan facility with Canadian

Imperial Bank of Commerce (“CIBC”). We borrowed

US $ 69 million under the loan facility. The loan is

secured by our shareholding in ASMPT.

The excess of the purchase price over the fair market

Management’s Discussion and Analysis (continued)Management’s Discussion and Analysis of Financial Condition and Results of Operations

16

�

value of the underlying net assets acquired in the

amount of H 65.0 million has been recorded as

goodwill and is amortized over a period of ten years,

on a straight line basis. The fair market value approxi-

mates the bookvalue of such net assets of ASMPT.

On October 6, 2000 the Company repaid US $ 10

million in principle amount under the CIBC loan

facility consisting of US $ 5.5 million installment and

US $ 4.5 million partial prepayment. On December

21, 2000 a second partial prepayment of US $ 13.0

million was made. The outstanding balance as of

December 31, 2000 is US $ 46.0 million.

In connection with the CIBC loan facility, we entered

into an equity line of credit with Canadian Imperial

Holdings, Inc. (“CIHI”), an affiliate of CIBC, pursuant

to which we have the right to sell up to an aggregate

of US $ 65 million of newly issued shares to CIHI

from time to time over a two year period. Pursuant to

the equity line, we are required to register with the

US Securities and Exchange Commission (“SEC”)

US $ 65 million of our common shares for offer and

sale pursuant to the equity line. The registration

statement must remain in effect for the duration of

the equity line. CIHI is under no obligation to

purchase our newly issued common shares under the

equity line if effectiveness of our registration statement

is withdrawn, certain conditions precedent to the

equity line are not satisfied or certain covenants are

not complied with.

We have filed a registration statement with the SEC

for these shares on March 9, 2001. Until the registration

statement is declared effective by the SEC, we are

unable to issue shares under this equity line of credit.

Registration must be effective by April 23, 2001. If it

is not effective by that date, we must pay CIHI a

monthly fee of 3/4% of the outstanding CIBC loan

amount and 1% per month if the registration statement

is not effective by June 8, 2001.

In April 2000 we repaid a term loan of H 25.0 million

to the Nationale Investeringsbank N.V. (‘NIB’) from

the proceeds of the share offering and during the year

2000 we repaid the remaining installments of a

subordinated loan to the NIB in the amount of H 2.0

million and a H 1.4 million subordinated loan to a

related party.

During 2000 we negotiated an increase of the term

loans with our banks in Japan and increased our loans

with our bank in Finland and repaid outstanding

bank loans in Hong Kong.

During 1998 we negotiated an extension of an

original US $ 80.0 million convertible note provided

by Applied Materials following the settlement of the

patent dispute in 1997. After paying Applied

Materials US $ 15.0 million in 1997 and US $ 20.0

million in 1998, the remaining balance of US $ 45.0

million of the initial interest-free subordinated

convertible loan was replaced by an interest-bearing

note for which we provided security. In addition, we

issued a warrant to Applied Materials to purchase

1.5 million of our common shares at a price of

US $ 5.375 per share. The note was repayable in two

installments: US $ 10.0 million was paid in 1999 and

the remaining US $ 35.0 million was due in 2000 which

was repaid from the the proceeds of the exercise of

the 1.5 million warrants in March 2000 and from the

proceeds of the share offering in April 2000.

On October 1, 1999, we placed 6% zero-coupon

debentures with a maturity value of US $ 20.0 million

with a group of United States institutional investors.

The debentures had a five year maturity. The

debentures were discounted by 6% annual interest

for a net purchase value of approximately US $ 14.9

million. As part of the debenture agreement, the

investors received 2,037,957 non-detachable warrants

and 200,000 supplemental warrants on common shares

of the Company with an exercise price of US $ 9.81

per share, a premium to market at the date of issuance

of 20%. In February 2000, the 2,037,957 warrants

were exercised and the debentures were cancelled in

partial payment of the exercise price of the warrants.

The remaining portion of the exercise price of the

warrants was fulfilled by the investors contributing

US $ 4.8 million in cash.

In 1998 we entered into a H 20.4 million, 6%

subordinated convertible loan with three lenders.

During 1999, all three lenders converted their loan

into common shares.

The Front-end business finances its operations from

the cash flows derived from its business activities and

from collateralization of fixed and current assets.

Back-end operations are entirely self-financed by

ASM Pacific Technology. The cash resources and

borrowing capacity of ASM Pacific Technology are

not available to our Front-end operations.

We support borrowings of our Front-end subsidiaries

with guarantees. We have also mortgaged certain

land and buildings to secure our Front-end

borrowings. We have also pledged all of our

shareholding in ASMPT. The market value of our

investment in ASMPT at the end of 2000 was

17

Management’s Discussion and Analysis (continued)Management’s Discussion and Analysis of Financial Condition and Results of Operations

approximately H 318.4 million, which is slightly

lower than the market value at the end of 1999,

which was approximately H 333.9 million.

Market Risk Disclosure

We are exposed to currency fluctuations, most notably

fluctuations of the United States dollar, the Hong

Kong dollar and the Japanese yen against the Euro.

To the extent that these fluctuations affect the value

of our investments in our affiliates, they are not

hedged. The cumulative effect of these fluctuations

are separately reported in shareholders’ equity and

2000 showed a negative movement of H 0.9 million.

Currency

Currency fluctuations that affect operating cash flows

are hedged as a policy. We view exposures on a

consolidated basis and sell off or cover excess or short

positions, using spot or forward contracts which are

entered into with commercial banks of good standing.

At December 31, 2000 we had outstanding forward

exchange contracts in which we agreed to buy foreign

currencies in the amount of H 5,5 million and to sell

foreign currencies in the amount of H 7,5 million. At

December 31, 2000 the fair market value of these

exchange contracts were H 5,8 million and

H 7,2 million respectively.

The operations of our subsidiaries are generally financed

with debt issued in our subsidiaries’ respective functional

currencies. Thus, we believe we do not have significant

currency exposure related to our borrowings.

Interest Rates

A considerable percentage of our outstanding debt

bears interest which are typically variable in nature.

We are exposed to interest rate risk primarily through

our borrowing activities. We do not enter into

financial instrument transactions for trading or

speculative purposes or to manage interest rate

exposure. Therefore, a 1% adverse change in interest

rates on the portion of our debt bearing interest at

variable rates would result in an annual increase in

interest expense of approximately H 0.8 million at

December 31, 2000 borrowing levels.

Euro

The Netherlands, our country of domicile, is one of

the countries that participates in the use of the Euro,

the new currency unit that has been available since

January 1, 1999. Until 2002, the participating

countries will allow both the Euro and local

currencies as legal tender. Our European operations

will therefore use the Euro as their functional

currency as soon as possible after its introduction. The

actual introduction is not critical for our business but

will depend on availability of reliable software for

accounting, payroll and other internal functions and

will be achieved over a period of time, but before 2002.

The introduction of the Euro will not significantly

affect our currency profile or risk as the Euro has a

fixed exchange rate against the Netherlands guilder.

Effective beginning of fiscal year 1999, we changed

our reporting currency from Netherlands guilders to

Euros. Prior year balances have been restated based

on the fixed exchange rate of H 1.00 to NLG 2.20371.

The comparative balances reported in Euros depict

the same trends as would have been presented if we

had continued to present balances in Netherlands

guilders. Balances for periods prior to January 1, 1999