©2003 prentice hall business publishing, cost accounting 11/e, horngren/datar/foster an...

TRANSCRIPT

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster ©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

An Introduction to CostTerms and Purposes

Chapter 2

2 - 1

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 1

2 - 2

Define and illustratea cost object.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Cost and Cost Terminology

2 - 3

Cost is a resource sacrificed or forgone to achievea specific objective.

An actual cost is the cost incurred (a historical cost)as distinguished from budgeted costs.

A cost object is anything for which a separatemeasurement of costs is desired.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 2

2 - 4

Distinguish between direct costsand indirect costs.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Direct and Indirect Costs

2 - 5

Direct CostsExample: Paper on whichSports Illustrated magazineis printed

Indirect CostsExample: Lease cost forTime-Warner buildinghousing the senior editorsof its magazine

COST OBJECT

Example: Sports Illustrated magazine

COST OBJECT

Example: Sports Illustrated magazine

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

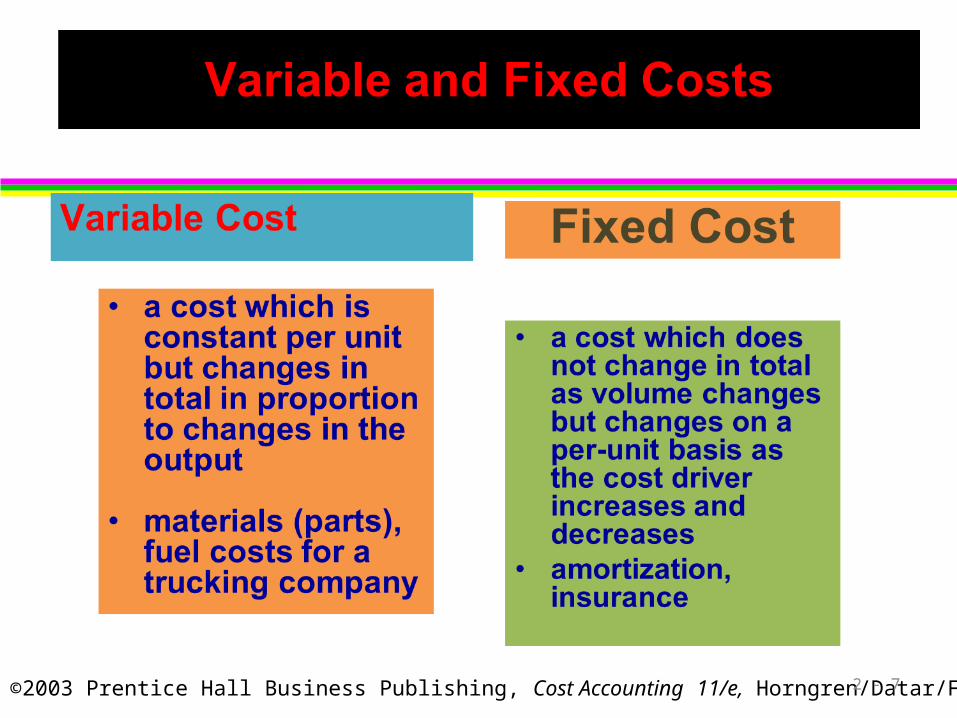

Learning Objective 3

2 - 6

Explain variable costsand fixed costs.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster 2 - 7

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster 2 - 8

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Relationships of Types of Costs

2 - 9

Direct

Indirect

Variable Fixed

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 4

2 - 10

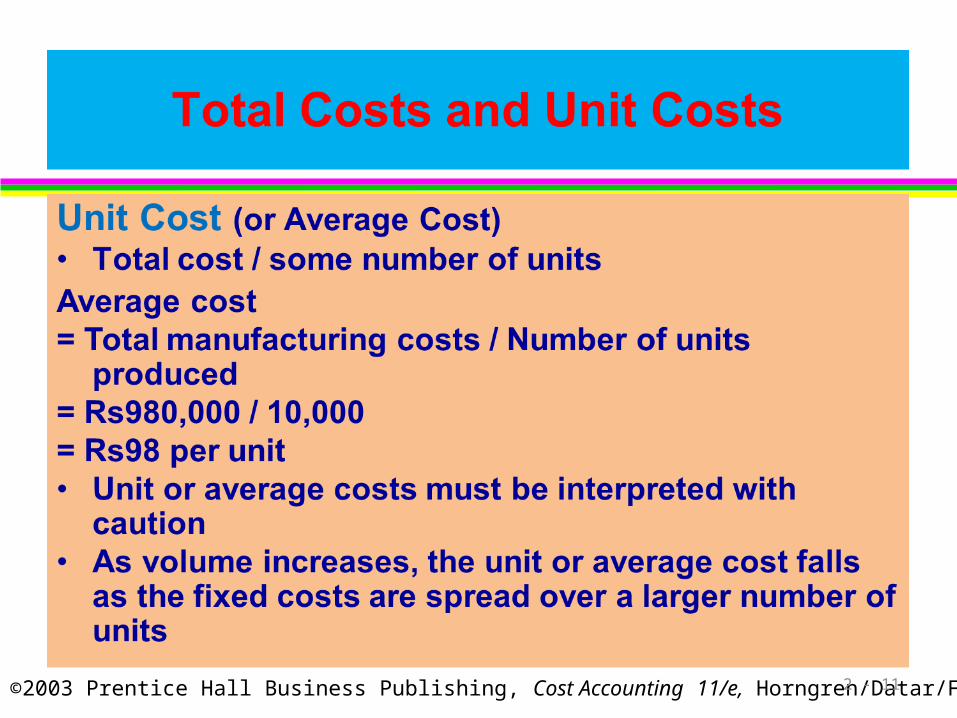

Interpret unit costs cautiously.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster 2 - 11

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 5

2 - 12

Distinguish amongmanufacturing companies,

merchandising companies, andservice-sector companies.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

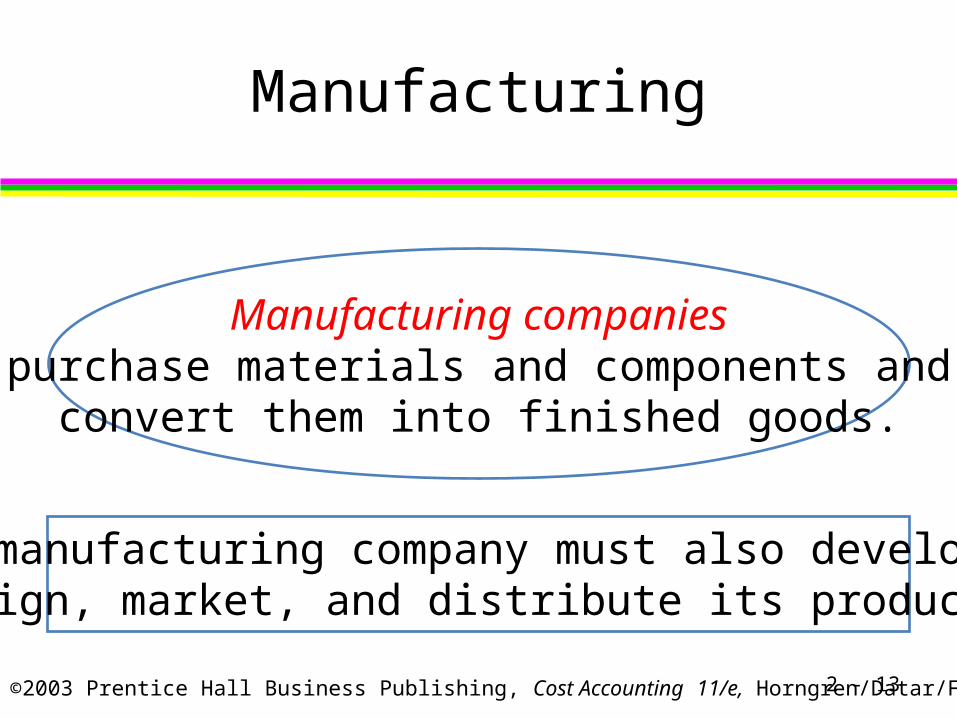

Manufacturing

2 - 13

Manufacturing companiespurchase materials and components and

convert them into finished goods.

A manufacturing company must also develop,design, market, and distribute its products.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Merchandising

2 - 14

Merchandising companiespurchase and then sell tangible products

without changing their basic form.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Merchandising

2 - 15

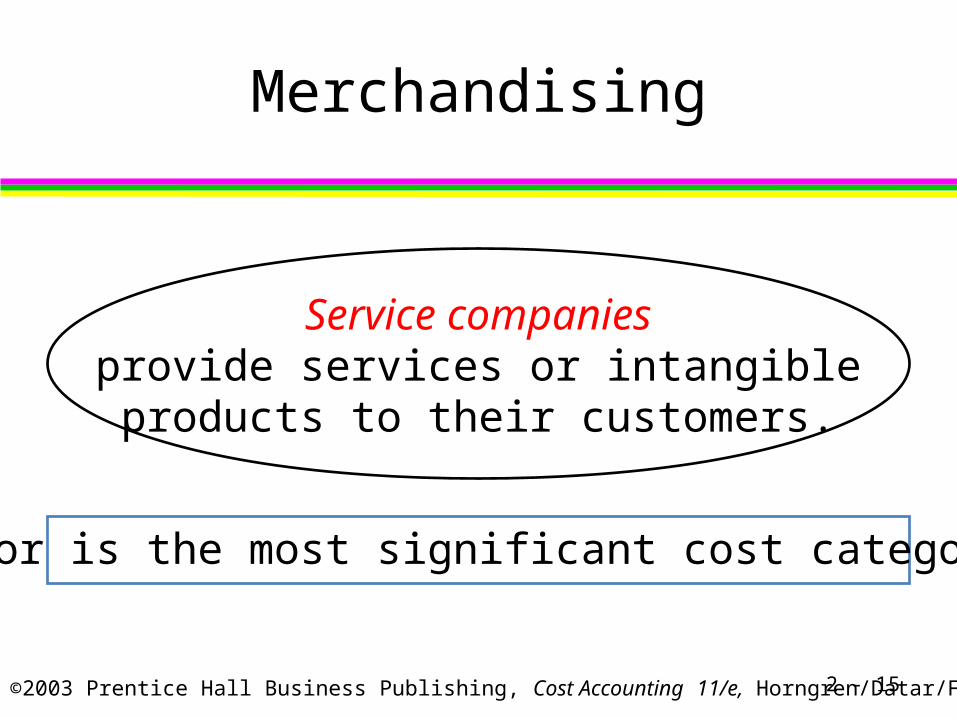

Service companiesprovide services or intangibleproducts to their customers.

Labor is the most significant cost category.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 6

2 - 16

Differentiate betweeninventoriable costsand period costs.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

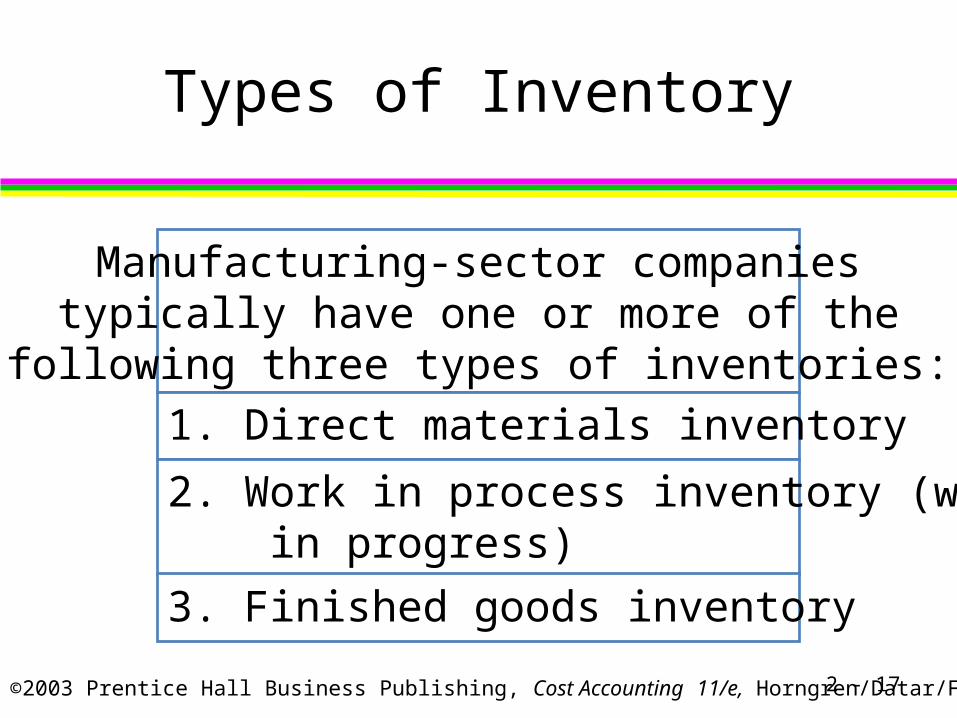

Types of Inventory

2 - 17

Manufacturing-sector companiestypically have one or more of the

following three types of inventories:

1. Direct materials inventory

2. Work in process inventory (work in progress)

3. Finished goods inventory

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Types of Inventory

2 - 18

Merchandising-sector companies holdonly one type of inventory – the

product in its original purchased form.

Service-sector companies do nothold inventories of tangible products.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

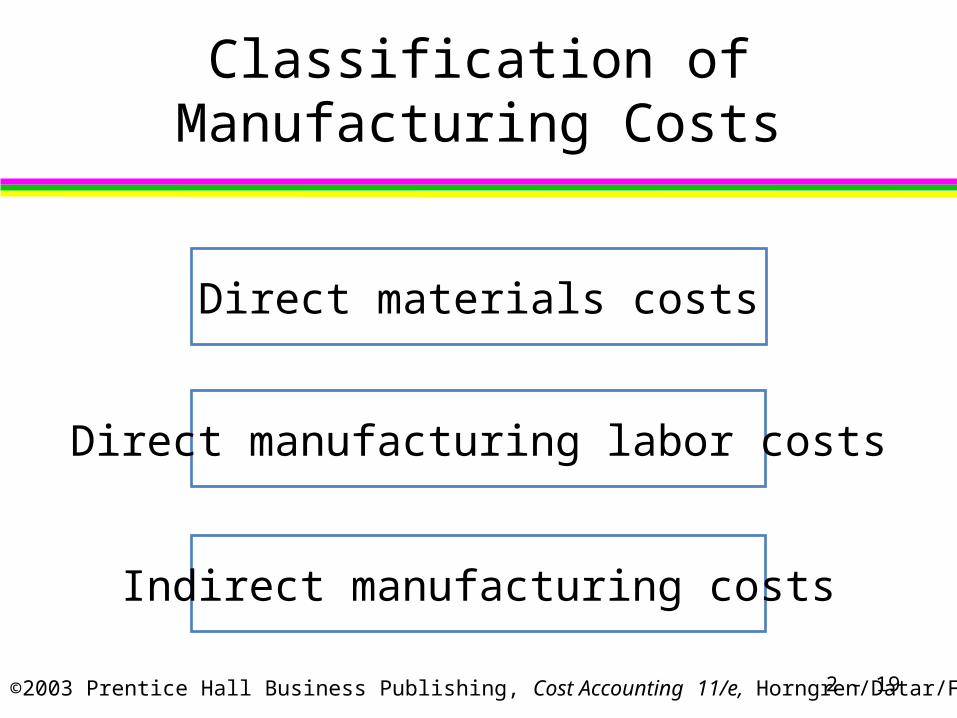

Classification ofManufacturing Costs

2 - 19

Direct materials costs

Direct manufacturing labor costs

Indirect manufacturing costs

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Learning Objective 7

2 - 20

Describe the three categories ofinventories commonly foundin manufacturing companies.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Inventoriable Costs

2 - 21

Inventoriable costs (assets)…

become cost of goods sold…

after a sale takes place.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Period Costs

2 - 22

Period costs are all costs in the incomestatement other than cost of goods sold.

Period costs are recorded as expenses of theaccounting period in which they are incurred.

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Manufacturing Company

2 - 23

MaterialsInventory

FinishedGoods

Inventory

Revenues

Cost ofGoods Sold

INCOME STATEMENT

PeriodCosts

InventoriableCosts

BALANCE SHEET

Equals Operating Income

whensalesoccur

deduct

Equals Gross Margindeduct

Work inProcess

Inventory

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

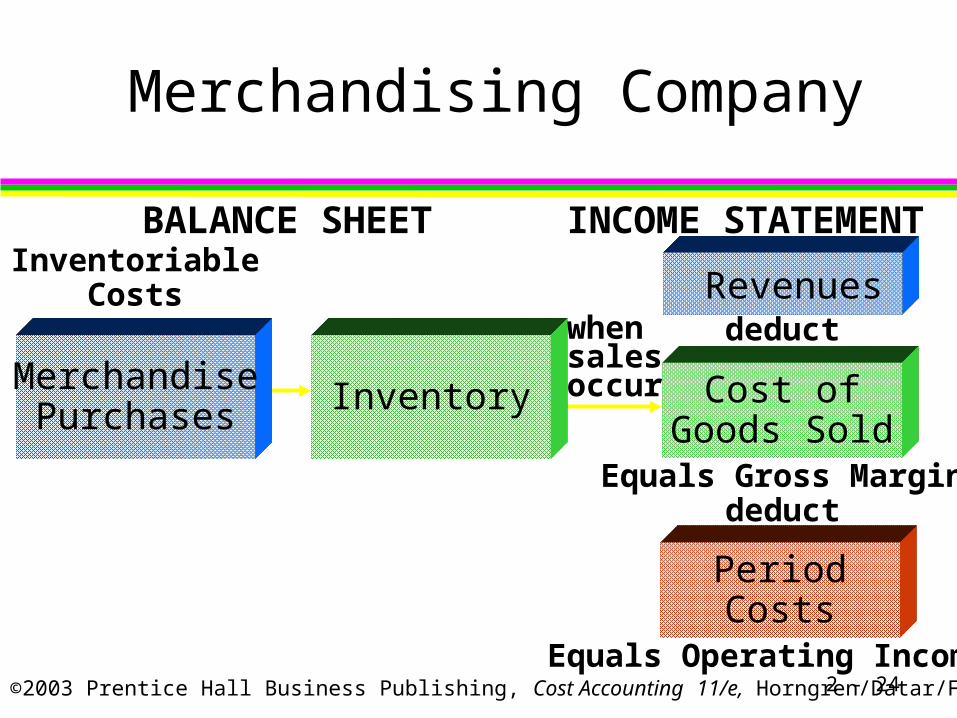

Merchandising Company

2 - 24

INCOME STATEMENTBALANCE SHEET

whensalesoccur

InventoriableCosts

MerchandisePurchases Inventory

Revenuesdeduct

Cost ofGoods Sold

Equals Gross Margindeduct

PeriodCosts

Equals Operating Income

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

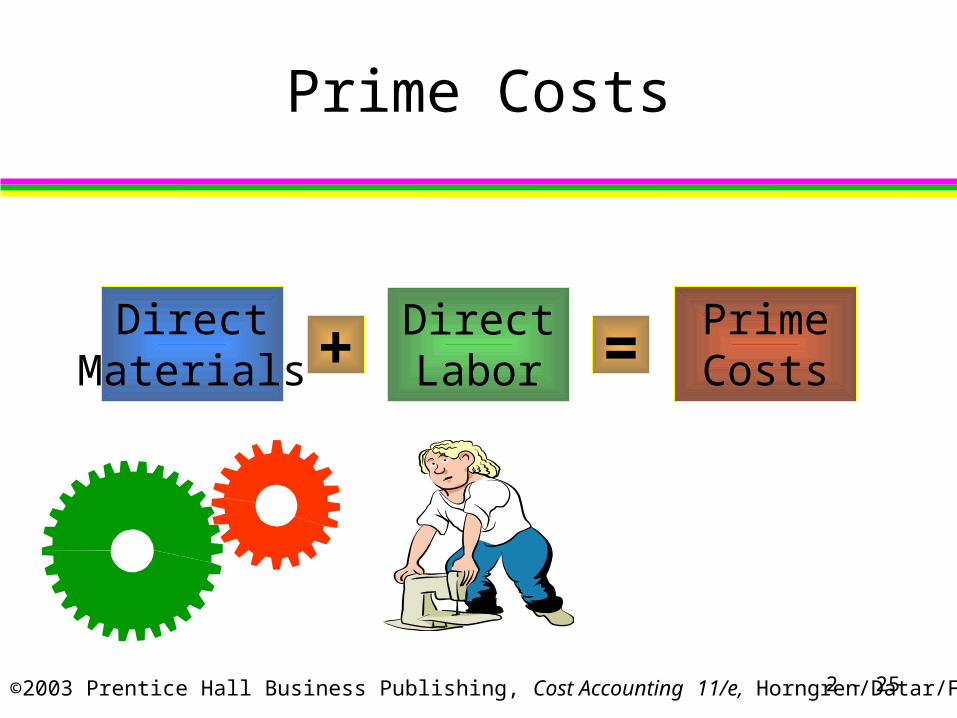

Prime Costs

2 - 25

DirectMaterials

DirectLabor

PrimeCosts+ =

©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

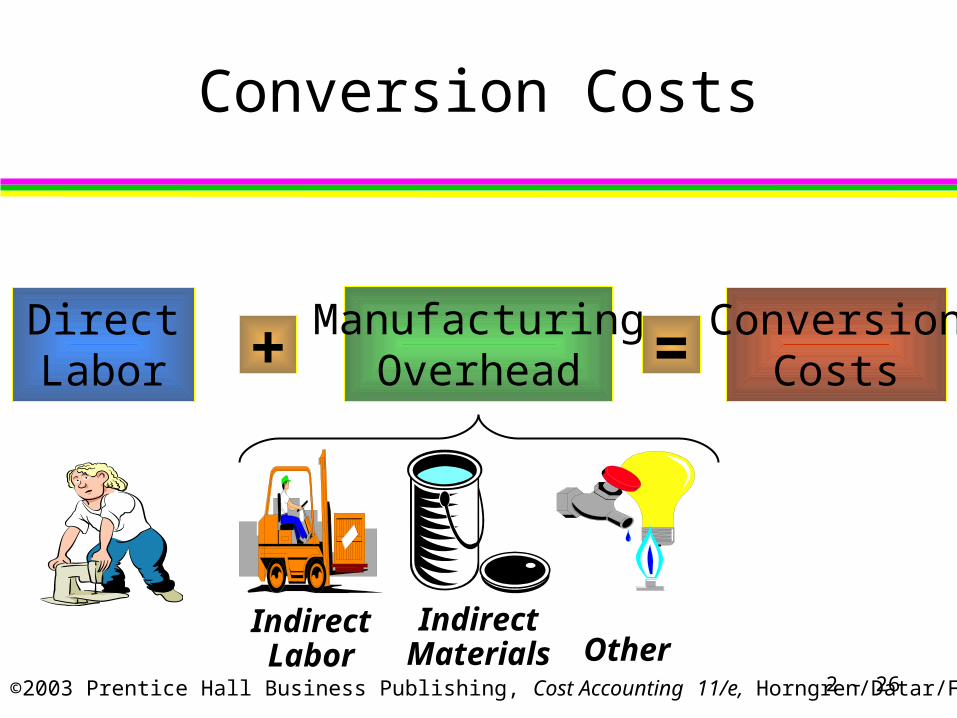

Conversion Costs

2 - 26

DirectLabor

ManufacturingOverhead+ =

ConversionCosts

IndirectLabor

IndirectMaterials Other