2006 annual ownership report

TRANSCRIPT

i

2006 Annual Ownership Report

ii

2006 Annual Ownership Report

iii

2006 ANNUAL OWNERSHIP REPORT

Contact Information

Comments and suggestions about the report

can be submitted to

Undersecretariat of Treasury

General Directorate of State Owned Enterprises

via phone numbers ++90 – 312 (204 61 90 - 204 61 88)

or via e-mail [email protected]

2006 Annual Ownership Report

iv

2006 Annual Ownership Report

v

MINISTER’S PREAMBLE

Public resource usage in an effective and efficient manner and informing the public about this issue within the context of accountability is one of the main policies of our government.

In this context, it is important for the general public to be informed about the activities of state owned enterprises which operate in agriculture, transportation, communication, energy and mining industries and have a great impact on the economy via utilization of public resources.

Although the main objective of our government is to create a free market economy and sustain economic growth through private sector operations by privatizing state owned enterprises, it is also among our priorities to make public enterprises operate according to modern corporate governance principles.

The Undersecretariat of Treasury, which exercise the ownership function of the State, has taken on great reponsibillity by publishing the review of performances of enterprises and by informing the public about them besides creating policies in order to make them operate effectively and efficiently.

I hope this first Annual Ownership Report fullfills the information needs of the public and I thank to all of the Treasury staff which takes part in the preparation process of this report.

Ali BABACAN

Minister of State and Chief Negotiator

2006 Annual Ownership Report

vi

2006 Annual Ownership Report

vii

UNDERSECRETARY’S PREAMBLE

The adoption of corporate governance principles and improvement of accountability and transparency level are very important for attaining a competitive market and for carrying out the responsibilities of public bodies to all stakeholders.

The Undersecretariat of Treasury exercising the ownership function of the State in a large number of public enterprises is expected not to deviate from this point of view. This standpoint requires informing the public about the operations, financial stance, directors and performance of public enterprises.

As the shareholder of the SOEs which comprise a significant part of the current economic program, our main objective of publishing this annual report is to introduce the SOE system to the public, to convey the developments and restructuring efforts in 2006 and to contribute to the development of corporate governance.

The Undersecretariat of Treasury endeavors for SOEs in its portfolio to be managed in an efficient and effective manner, to create more value added to the economy and consequently to increase their values. In this regard, some provisions related to corporate governance were included in the 2007 General Investment and Financing Program Decree for the first time. With contribution of State Planning Organization, Privatization Administration and Capital Markets Board, we embarked on a project which aims to improve the corporate governance of State Owned Enterprises.

I hope this Annual Ownership Report prepared for the first time with the governance concerns will be useful and I would like to express my thanks to my colleagues who devoted their efforts to this report

İbrahim H. ÇANAKCI Undersecretary

2006 Annual Ownership Report

viii

2006 Annual Ownership Report

ix

GENERAL DIRECTOR’S PREAMBLE

Public agencies which exercise the ownership function of the State and public enterprises which operate in different sectors constitute a very scattered picture in our country. Besides some non-financial and financial public enterprises wholly owned by the Undersecretariat of Treasury, there are also other enterprises and subsidiaries performing in the market, which are owned by Privatisation Administration, other central government bodies and local governments.

As of December 31st 2006, there are 20 state owned enterprises and 4 subsidiaries in the Treasury’s portfolio. These enterprises constitute a very important role in the real economy with the total gross sale figure of 44 Billion YTL corresponding to 7,7% of the GDP in 2006. Furthermore, these enterprises still maintain their importance in terms of executing current economic program.

The Undersecretariat of Treasury finds it useful and regards it as a duty to disclose the results of the operations of the enterprises under its portfolio in terms of improving the corporate governance principles.

So as to improve the accountability and transperancy level, the Treasury has started to announce periodically the financial accounts of SOEs on its web page within the context of national announcement program conducted by Turkish Statistical Institute.

2006 Annual Ownership Report is divided into three parts. The first one covers the problems of managing state owned enterprises in Turkey and the position of the Treasury as a shareholder. The second part includes the aggregated analysis about the accounts of SOEs under the Treasury Portfolio and the last part assesses the 2006 performances of SOEs seperately.

The data in the report consists of the inputs which are collected from the financial and other tables sent by SOEs. The data between 2002 and 2004 had been audited by High Auditing Board and approved by the Parliament. Whereas, the accounts concerning 2005 and 2006 has not been audited yet. However, it is not expected that the financial figures will change too much.

I express my thanks to my colleagues who prepared this Report for the first time and I wish the Report would be beneficial for our stakeholders.

M. Sefa PAMUKSUZ General Director

2006 Annual Ownership Report

x

1

CONTENTS

MINISTER’S PREAMBLE .......................................................................................................................... V EXECUTIVE’S PREAMBLE .................................................................................................................... Vİİ GENERAL DIRECTOR’S PREAMBLE .....................................................................................................İX CONTENTS ................................................................................................................................................. 1 LIST OF TABLES ........................................................................................................................................ 3 LIST OF GRAPHS ....................................................................................................................................... 3 LIST OF BOXES.......................................................................................................................................... 3 ABBREVIATIONS ....................................................................................................................................... 4 CHAPTER 1: INTRODUCTION ................................................................................................................... 5 CHAPTER 2: PUBLIC ENTERPRISES AND SOES .................................................................................. 6 CHAPTER 3: TREASURY PORTFOLIO ..................................................................................................... 8

3.1. OUR PORTFOLIO ................................................................................................................................. 8 3.2. OUR TASK .......................................................................................................................................... 8 3.3. OUR OBJECTIVES AND GOALS ............................................................................................................ 10 3.4. SOE – CENTRAL BUDGET RELATION................................................................................................... 11

3.4.1. Transfers from Budget to SOEs.............................................................................................. 11 3.4.2. Transfers from SOEs to Budget.............................................................................................. 11

CHAPTER 4: 2006 PERFORMANCE OF ALL SOES............................................................................... 13 4.1. FINANCIAL ANALYSIS ......................................................................................................................... 13

4.1.1. Income Statement .................................................................................................................. 13 4.1.2. Balance Sheet ........................................................................................................................ 14 4.1.3. Ratio Analysis......................................................................................................................... 15 4.1.4. Value Added ........................................................................................................................... 16

4.2. EMPLOYMENT ................................................................................................................................... 17 4.2.1. Personnel Numbers................................................................................................................ 18 4.2.2. Personnel Costs ..................................................................................................................... 18 4.2.3.Average Personnel Costs ........................................................................................................ 19 4.2.4. Personnel Profile .................................................................................................................... 19

4.3. OTHER INDICATORS ........................................................................................................................... 20 4.4. MAIN PROBLEMS OF SOES ................................................................................................................ 20

CHAPTER 5: PERFORMANCES OF THE SOES .................................................................................... 22 5.1. ENERGY AND MINING SECTORS ................................................................................................ 23

5.1.1. BOTAŞ ................................................................................................................................... 25 5.1.2. EÜAŞ...................................................................................................................................... 28 5.1.3. TEİAŞ ..................................................................................................................................... 31 5.1.4. TETAŞ .................................................................................................................................... 34 5.1.5. TKİ.......................................................................................................................................... 36 5.1.6. TTK......................................................................................................................................... 38 5.1.7. TPAO...................................................................................................................................... 40 5.1.8. ETİ MADEN ............................................................................................................................ 43

2006 Annual Ownership Report

2

5.2. TELECOMMUNICATION & TRANSPORTATION SECTORS......................................................... 45 5.2.1. TCDD ..................................................................................................................................... 47 5.2.2. DHMİ ...................................................................................................................................... 51 5.2.3. KIYEM .................................................................................................................................... 54 5.2.4. PTT......................................................................................................................................... 57

5.3. AGRICULTURE SECTOR .............................................................................................................. 59 5.3.1. EBK ........................................................................................................................................ 61 5.3.2. TİGEM .................................................................................................................................... 63 5.3.3. TMO ....................................................................................................................................... 66 5.3.4. ÇAYKUR ................................................................................................................................ 70 5.3.5. TŞFAŞ .................................................................................................................................... 74

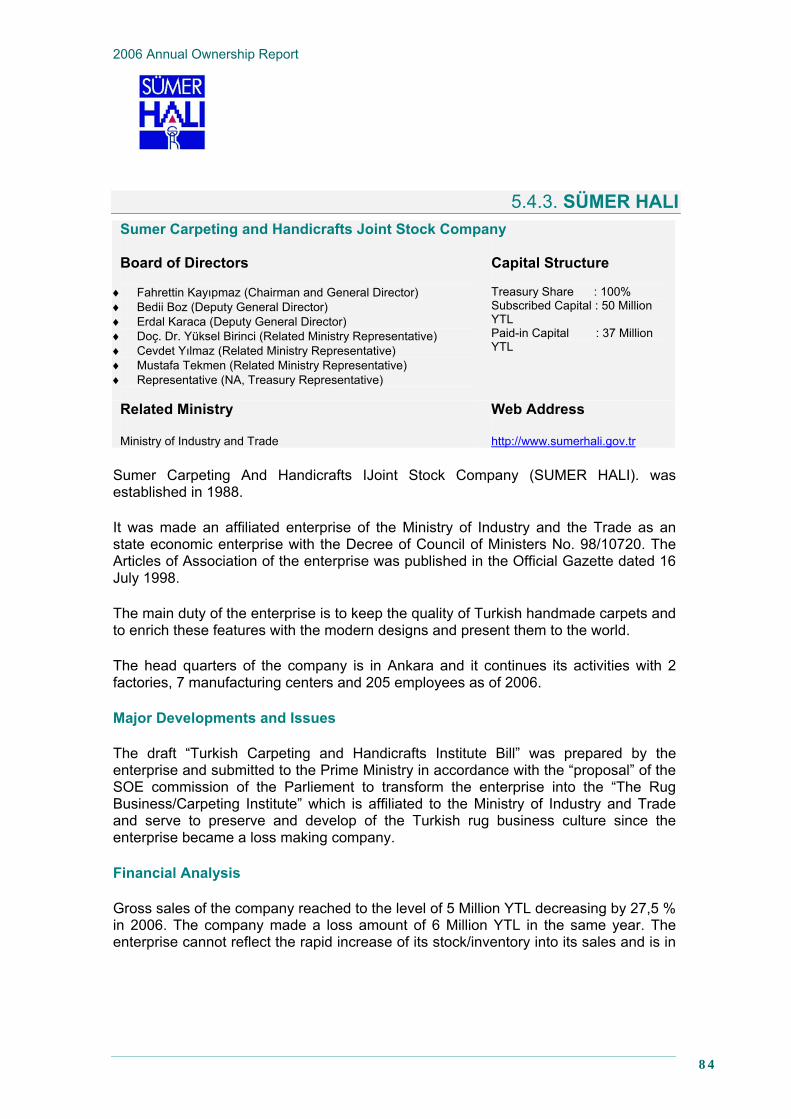

5.4. OTHER SECTORS......................................................................................................................... 78 5.4.1. DMO ....................................................................................................................................... 80 5.4.2. MKEK ..................................................................................................................................... 82 5.4.3. SÜMER HALI.......................................................................................................................... 84

CHAPTER 6: APPENDICES ..................................................................................................................... 86 APPENDIX 1: LIST OF PUBLIC ENTERPRISES AND THEIR SUBSIDIARIES........................................ 88 ANNEX 2: FINANCIAL TABLES OF SOES UNDER TREASURY PORTFOLIO ........................................ 92

Income Statement ............................................................................................................................ 94 Balance Sheet .................................................................................................................................. 95 Financial Ratios ................................................................................................................................ 96 Non Tax Revenues........................................................................................................................... 97

APPENDIX 3: EMPLOYMENT DATA OF SOES UNDER TREASURY PORTFOLIO ................................. 98 SOE Personnel Numbers and Costs .............................................................................................. 100 Personnel Profile ............................................................................................................................ 101

APPENDIX 4: OTHER SELECTED INDICATORS OF SOES UNDER TREASURY PORTFOLIO........... 104 E APPENDIX 5: AGGREGATED FINANCIAL TABLES (TREASURY AND PRİVATİZATİON ADMINISTRATION

PORTFOLİO)............................................................................................................................................ 108 Income Statement .......................................................................................................................... 110 Balance Sheet ................................................................................................................................ 111 Financial Ratios .............................................................................................................................. 112

2006 Annual Ownership Report

3

LIST OF TABLES Tables PageTable 3.1: Capital Structure of Treasury Portfolio 9Table 3.2: SOE – Central Government Budget Relation 11Table 4.1: Income Statements 13Table 4.2: Balance Sheets 14Table 4.3: Financial Ratios 15Table 4.4: Personnel Numbers 18Table 4.5: Personnel Costs 18Table 4.6: Personnel Costs / (Cost of Sales + General and Administrative Expenses)

(%) 19

Table 4.7: Average Personnel Costs 19Table 4.8: Other Indicators (YTL) 20Table 4.9: Other Indicators (%) 20Table 5.1: BOTAŞ’s Receivables 26Table 5.2: TPAO – Domestic Investment Expenditures 41Table 5.3: KIYEM Breakdown of Sales 55Table 5.4: TMO Purchases 67Table 5.5: TMO Sales (Selected Crops) 68Table 5.6: ÇAYKUR Sales and Production 70Table 5.7: TŞFAŞ Sales, Production and Purchases 74Table 5.8: DMO Sales & Revenue Data 79

LIST OF GRAPHS Graphs PageGraph 1: Value Added 16Graph 2: Tea Leaf Purchases 70Graph 3: Tea Leaf Support Payments 71

LIST OF BOXES Box PageBox 1: What is an SOE? 5Box 2: Corporate Governance 10Box 3: Primary Balance of SOEs 12Box 4: Status Change of Temporary Workers into Permanent Workers 17

2006 Annual Ownership Report

4

ABBREVIATIONS AOÇ Atatürk Farm and Forest Enterprise SÜMER HALI Carpeting Company

BO Build-Operate TCDD Turkish State Railways

BOT Build-Operate-Transfer TEDAŞ Electricity Distribution Co.

BOTAŞ Petroleum Pipeline Corporation TEİAŞ Electricity Transmission Co.

CPM Capital Markets Board of Turkey TEKEL Tobacco Co.

ÇAYKUR Tea Enterprise TEMSAN Turkish Electromechanics Industry

DHMİ State Airports Authority TETAŞ Electricity Trading and Contracting Co.

DMO State Supply Office TİGEM Agriculture Enterprises

EBK Meat and Fish Board TKİ Turkish Coal Enterprise

EMRA Energy Market Regulatory Authority TMO Turkish Grain Board

ETİ MADEN Eti Mine Works TOR Transfer of Rights

EÜAŞ Electricity Generation Co. TPAO Turkish Petroleum Corporation

KBİ Blacksea Copper Company TRT Turkish Radio and Television

KIYEM Coastal Safety TSKGV Turkish Armed Forces Foundation

MARA Ministry of Agriculture and Rural Affairs TŞFAŞ Turkish Sugar Factories Corporation

MKEK Mechanical and Chemical Industry Corporation TTK Turkish Hard Coal Enterprise

PA Privatisation Administration TÜDEMSAŞ Turkish Railway Machines Co.

PB Primary Balance TÜİK Turkish Statistical Institute

PEI Public Economic Institution TÜLOMSAŞ Turkish Locomotive Co.

PMUM Balance and Settlement Market TÜVASAŞ Turkish Wagon Co.

PTT Post and Telegraph Organization UT The Undersecretariat of Treasury

SEE State Economic Enterprise YDK Prime Ministry High Auditing Board

SOE State Owned Enterprise YPK High Planning Council

SPO State Planning Organization

*Information about the SOEs and the subsidiaries can be obtained from the address below; http://www.hazine.gov.tr/stat/kit_ist.htm.

2006 Annual Ownership Report

5

CHAPTER 1: INTRODUCTION

State owned enterprises (SOE) have been contributing to the economic growth since the initial years of the Turkish Republic by using the natural resources for the benefit of the economy, giving opportunity to industrial investments, increasing the employment and providing the capital accumulation via State1.

The precedence of SOEs in the Turkish economy have been sustained for years particularly in the capital-intensive sectors. However, when the private sector has managed to make investments by gaining enough capital accumulation and experience and when the liberal economy policies have started to gain importance, the contribution of SOEs to the economy has decreased. Furthermore, the turmoils in the Turkish economy and the problems attached to the characteristics of public enterprises have affected the SOEs adversely.

While the value added of SOEs to the economy was around 7% of the GDP during 1990s, this figure decreased to the 2% of GDP mostly because the number of SOEs has decreased as a result of privatisation and the private sector has started to operate within the sectors open to the competition.

Public enterprises have difficulties while competing with the private companies because they are subject to strict rules and regulations and their managers have limited role while making operational decisions such as employment, investment and pricing.

In this framework, as it is mentioned in the 9th development Plan, an initiative for a new legislation has been started in order to eliminate problems in the SOE system. Moreover, a project about the implementation of the corporate governance principles in the public enterprises has been conducted with the cooperation of Undersecretariat of Treasury, State Planning Organization, Privatization Administration and Capital Markets Board.

1 The idea of founding SOEs in our country arised at İzmir Economic Congress (17 February 1923) in accordance with the aim of “Strenghtening the Economical Domination”

Box 1: What is an SOE?

In Turkish acquis, state owned enterprises (SOEs) are those subject to the Decree Law No. 233 and the common name of the SEEs and PEIs whose whole capital belong to the state.

State Economic Enterprises (SEE): The enterprises which operate in a free market with profit making motive. Such as, MKEK (Military Equipment), EÜAŞ (Electric Generation), ÇAYKUR (Tea), BOTAŞ (Natural Gas), TTK (Hard Coal) and TKİ (Lignite)

Public Economic Institutions (PEI): The institutions which produce public goods and services carrying monopolistic characteristics by taking into account the public welfare. TCDD (Railways), KIYEM (Coastal Safety), PTT (Post Office) and DHMİ (Airport Administration) are the PEIs.

In this context, even there is a state ownership in state banks and the enterprises in the privatisation program, they are not included in the SOE classification because they are not subject to Decree-Law No. 233.

2006 Annual Ownership Report

6

CHAPTER 2: PUBLIC ENTERPRISES AND SOEs

According to the international definition, public enterprises are “the enterprises in which the capital ratio of central authority and local government is more than 50 percent or in which the capital ratio of central authority and local government is less than 50 percent but the government controls the management” 2. As it is defined in the former section, SOEs in Turkey are the subcategory of public enterprises.

In our country, different public administrations exercise the ownership function of the state in public enterprises. Moreover, there is not any public institution/agency responsible for coordination of state’s ownership functions in public enterprises and collecting their data.

It is also common to encounter with a situation in which the public enterprises are associated with a public body other than the shareholder administration. In this dual structure, to set the priorities of the enterprises and to coordinate the performances compatible with general economic policies become much more important.

On the other hand, public enterprises have many subsidiaries. Also, it is not possible to reach the consolidated data of all subsidiaries.

So, the public enterprises and their subsidiaries which are subject to different laws can be classified as follows3:

The Ones Related To Central Government

SOEs and Subsidiaries subject to Decree Law 233 4 and of which UT owns the whole capital,

The state banks which UT owns the whole capital (Ziraat Bank, Eximbank and Kalkınma Bank (99,08%)),

Enterprises subject to Turkish Commercial Law and UT owns the whole capital (TURKSAT),

Enterprises which UT owns the fraction of the capital (Türk Telekomünikasyon A.Ş.),

Enterprises under the portfolio of PA which exercises the ownership function of the state (such as TEKEL, TEDAŞ)

2 2006/111/EC EU Commission Transparency Directive. 3 Please look at Annex-1 for the detailed list of public enterprises and their subsidiaries. 4 Decree Law 233 published in the Official Gazette (date:18.06.1984; number:18435)

2006 Annual Ownership Report

7

Public enterprises where it is not clear which government agncy exercises the ownership function (such as AOÇ and TRT),

Enterprises whose shareholder is the Undersecretariat of Defence Industries5.

Housing Development Administration and its subsidiaries

Social Security Institutions’ subsidiaries

Enterprises under the control of The Savings Deposit Insurance Fund (SDIF)

Revolving funds

Non – Budgetary Funds (Defense Industry Support Fund, Fund for the Encouragement of Social Assistance and Solidarity, Privatisation Fund etc)

The Ones Related To Local Governments

Local governments’ enterprises and their subsidiaries are established to conduct the local activities in a simple and flexible way. Local governments exercise the shareholder function in these enterprises.

As it is seen above, there are many enterprises and subsidiaries which are under the control of central and local governments. The list in the Annex-1 includes the names of the enterprises which are gathered by the working group within the context of Coordination Council for the Improvement of the Investment Environment (YOİKK) Project.

The public sector accounts are constituted of the accounts of the general government and public enterprises. In order to improve fiscal transperancy and accountability, Public Financial Management And Control Law No: 5018 forces the public instutions within the general government (central government, social security institutions and local government) to monitor and report their accounts and annual reports. This Law also distributes the responsibilities between various public administrations.

From this point of view, it will be useful to monitor, report and disclose the accounts of the public enterprises for fiscal transperancy. UT monitors and reports the accounts of its enterprises and PA’s companies. However, it is very important to define the public enterprises in a broder terms and to collect and to disclose their accounts.

5 The enterprises, their subsidiaries and indirect subsidiaries of Turkish Armed Forces Foundation are not included in this list though they can be classified as public enterprises because the management control is at the hands of government officials. This Foundation has a special status.

2006 Annual Ownership Report

8

CHAPTER 3: TREASURY PORTFOLIO

There were 26 enterprises in 2006, of which 20 were SOEs, 4 public banks and 2 other under Treasury portfolio.6 The UT performs the state ownership function through General Directorate of State Owned Enterprises.

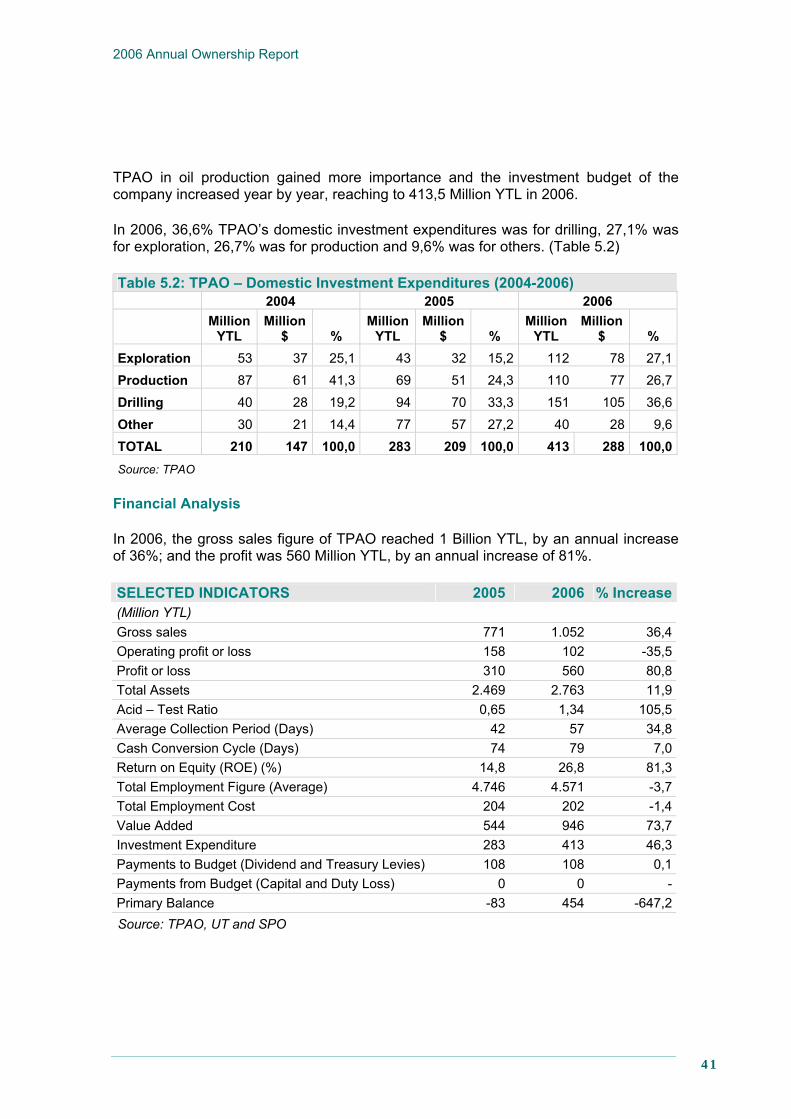

3.1. Our Portfolio

List and capital structures of SOEs, public banks and others in our portfolio as of 2006 are presented in Table 3.1.

All enterprises except TPAO, TŞFAŞ, Kalkınma Bankası and Türk Telekomünikasyon A.Ş. are wholly owned by the state. As of 2006, YTL 27 billion of YTL 31 billion subscribed capital was paid.

3.2. Our Task

According to Law No. 4059, the duty of UT regarding the SOEs are as follows:

♦ Exercising the ownership functions of the state,

♦ Manage the relations between Treasury and the SOEs,

♦ Prepare the general financing and investment program of the SOEs together with SPO, present the program for Council of Ministers approval, monitor the course of the program and make necessary revisions according to developments during the year,

♦ Monitor the SOEs’ operations whether they comply to related legislation or not,

♦ Provide that SOEs operate effectively and efficiently; or fulfill duties given by High Planning Council, High Privatisation Council or other authorities related to preparation for privatization of an SOE.

6 In our portfolio, there are also some public participations. The shares in these participations, including heritages to Treasury, are negligible in terms of percentages; therefore they are not included in this report.

2006 Annual Ownership Report

9

Table 3.1: Capital Structure of the Treasury Portfolio (as of 31.12.2006 - Million YTL) Subscribed

CapitalPaid-in Capital

Treasury’s Share (%)

MKEK 300 231 100,0 ETİ MADEN 100 89 100,0 TTK 3.000 2.926 100,0 TKİ 360 360 100,0 EÜAŞ 1.300 1.300 100,0 TEİAŞ 330 326 100,0 TETTAŞ 179 73 100,0 TPAO 950 950 97,0 BOTAŞ 1.830 1.830 100,0 TMO 961 961 100,0 ÇAYKUR 469 465 100,0 TİGEM 300 269 100,0 DMO 26 26 100,0 TCDD 8.000 6.089 100,0 PTT 800 731 100,0 DHMİ 1.700 376 100,0 KIYEM 42 42 100,0 SÜMER HALI 50 37 100,0 EBK 400 332 100,0 TŞFAŞ 1.600 1.534 99,9 SOE TOTAL 22.697 18.947

T.C.ZİRAAT BANK 2.500 2.222 100,0 T.H.T.EMLAK BANK 750 749 100,0 T. KALKINMA BANK 160 160 99,0 EXİMBANK 1.000 929 100,0 PUBLIC BANKS TOTAL 4.410 4.060

TÜRKSAT 438 438 100,0 TÜRK TELEKOM 3.500 3.500 45,0

GRAND TOTAL 31.046 26.945 Source: UT

2006 Annual Ownership Report

10

3.3. Our Objectives and Goals

The UT aims to improve the efficiency and value of SOEs by fulfilling its duties effectively. The policies are implemented by setting annual investment and financing program, monitoring SOE performance and ensure that they operate with conformity to this program. In the long term, SOEs are expected to operate efficiently and effectively under market conditions and achieve a status that can compete with private firms.

Box 2: Corporate Governance

OECD Principles of Corporate Governance

OECD Guidelines on Corporate Governance of State Owned Enterprises

Organisation for Economic Cooperation and Development (OECD) prepared Principles of Corporate Governance in 1999 and Guidelines on Corporate Governance of State Owned Enterprises in 2005. The guidelines is available at www.oecd.org. The guidelines cover six main topics:

I. Ensuring an Effective Legal and Regulatory Framework for State-Owned Enterprises: The legal and regulatory framework for state-owned enterprises should ensure a level-playing field in markets where state-owned enterprises and private sector companies compete in order to avoid market distortions.

II. The State Acting as an Owner: The state should act as an informed and active owner and establish a clear and consistent ownership policy, ensuring that the governance of state-owned enterprises is carried out in a transparent and accountable manner, with the necessary degree of professionalism and effectiveness.

III. Equitable Treatment of Shareholders: The state and state-owned enterprises should recognise the rights of all shareholders and in accordance with the OECD Principles of Corporate Governance ensure their equitable treatment and equal access to corporate information.

IV. Relations with Stakeholders: The state ownership policy should fully recognise the state-owned enterprises’ responsibilities towards stakeholders and request that they report on their relations with stakeholders.

V. Transparency and Disclosure: State-owned enterprises should observe high standards of transparency in accordance with the OECD Principles of Corporate Governance.

VI. The Responsibilities of the Boards of State-Owned Enterprises: The boards of state-owned enterprises should have the necessary authority, competencies and objectivity to carry out their function of strategic guidance and monitoring of management. They should act with integrity and be held accountable for their actions.

The Project on Corporate Governance of SOEs in Turkey

Studies regarding the governance of SOEs started in 2002 and several drafts have been prepared. However, those studies have not gone beyond the phase of compilation of public institutions‘ suggestions on draft law. The last draft law prepared in 2005 has become absolute.

In the scope of YOİKK objectives, a project on Corporate Governance of SOEs in Turkey has been initiated again, this time with contribution of SPO, PA and CMB.

List of public enterprises has been compiled, corporate governance of public enterprises in other countries has been surveyed and SOEs in Turkey are evaluated in the framework of good governance principles.

With the help of the findings in this study, we will set an SOE model suitable for our country and prepare a draft law. It is foreseen that, the draft will be finalized and project will be completed by the end of December 2008.

2006 Annual Ownership Report

11

3.4. SOE – Central Government Budget Relation

The financial relation between SOEs and Central Government Budget comprises transfers from SOEs to budget and transfers from budget to SOEs. (See Table 3.2)

3.4.1. Transfers from Budget to SOEs

Transfers from Treasury Budget to SOEs in our portfolio occur by two means.

Capital Transfers: Regarding our responsibilities towards SOEs and public banks, capital transfers are performed in accordance with related budget laws.

Duty Loss / Income Loss Payments: Duties given by Council of Ministers to SOEs in accordance with Decree Law No. 233 and to public banks in accordance with Law No. 4603 are compensated from the budget in compliance with the legislation mentioned.

3.4.2. Transfers from SOEs to Budget

Other than tax and other legal liabilities, transfers from SOEs to budget are made by two means.

Dividend Payments: Those payments are calculated in accordance with related legislation and paid to the Treasury.

Treasury Levy Payments: In reference to the Law No. 5018 Article 78, up to 15 percent of gross sales of some specific SOEs is paid to the budget7.

Table 3.2: SOE –Central Government Budget Relations (Million YTL) 2005 - 2006

2005 2006 Amount % Increase

Transfers from Budget to SOEs Capital Transfers 921 1.917 996 108Duty Loss / Income Loss Payments 502 710 208 41Total 1.423 2.627 1.204 85 Transfers from SOEs to Budget Dividend Payments 1 2.128 3.428 1.301 61Treasury Levy Payments 166 191 25 15Total 2.294 3.619 1.325 581 Including Telekom Source: UT

7 The SOEs to pay Treasury Levy and the payment ratio are determined by Decree of Council of Ministers No: 2005/9916. Those SOEs are TPAO, DHMİ, KIYEM and DMO.

2006 Annual Ownership Report

12

In 2006, YTL 2,6 Billion were transferred to SOEs, which contributed an amount of YTL 3.6 Billion to the budget8. (Table 3.2)

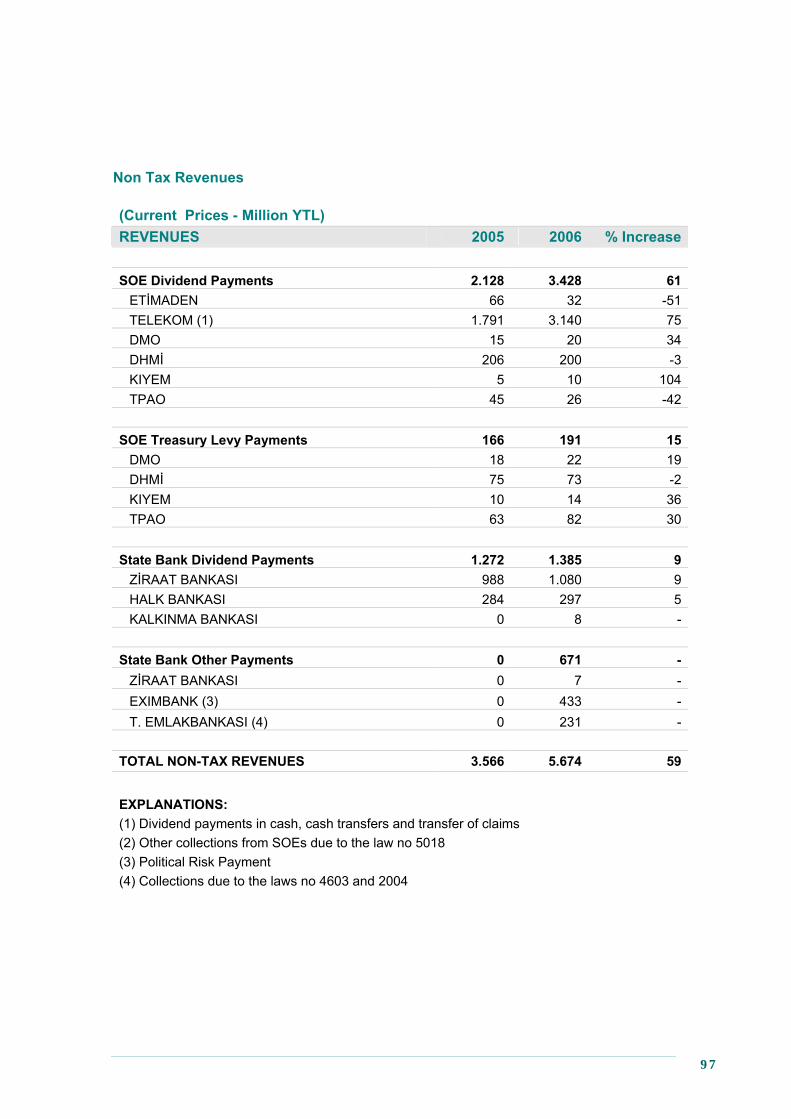

8 For details, see Annex 1- Non - Tax Revenues Table or Table 7: Non - Tax Revenues Table available at http://www.hazine.gov.tr/stat/kit_ist.htm.

Box 3: Primary Balance of SOEs One of the fundamental objectives of the economic program being implemented is the realization of Primary Balance (PB) targets for public sector. Our Undersecretariat is responsible for target setting and monitoring of SOEs and some companies in the privatization portfolio, which are a part of the Consolidated Government Sector monitored and reported in this respect. PB of SOEs is calculated starting from the Profit / Loss figure and subtracting some non - cash revenue and expenses and adding some non – revenue and non – expense cash recipts and disbursements and exclusion of interest related accounts. PB is calculated annually based on above the line method and it is monitored monthly based on below the line method. In this respect, calculation method of SOE PB is on accrual basis; therefore it has some differences from that of the central government. Above the line PB Below the line PB (+) Profit / Loss (+) Increase in financing (-) Non-cash revenues (-) Increase in debts (+)Non-cash expenses (+) Increase in receivables (+) Non-revenue cash inflows (-) Interest Income (-) Non-expense cash outflows (+) Interest expense (-) Interest Income (+) Interest expense

2006 Annual Ownership Report

13

CHAPTER 4: 2006 PERFORMANCE OF ALL SOEs

In this section the aggregated data and analysis of the SOEs under Treasury portfolio are presented. 9

4.1. Financial Analysis

4.1.1. Income Statement

The gross sales of 20 SOEs and 4 subsidiaries under Treasury portfolio has reached to 44 Billion YTL with an increase of 26%. But their net profit has declined to 1,2 Billion YTL with a decrease of 23% 10 .

Table 4.1: Aggregated Income Statement (Current Prices - Billion YTL)

2004 2005 2006 Change (%)

(1) (2) (3) (2)/(1) (3)/(2)Gross Sales 29.332 34.886 44.061 19 26

Domestic Sales 27.264 31.893 39.924 17 25 Export Sales 1.156 1.383 1.614 20 17 Duty Losses 692 1.364 1.408 97 3

Discounts From Sales 192 218 529 14 143Cost of Goods Sold 25.145 30.865 39.928 23 29Operating Expenses 1.738 1.885 2.159 8 15Operating Profit or Loss 2.258 1.917 1.445 -15 -25Ordinary Revenues From Other Operations 3.449 1.175 3.775 -66 221Ordinary Expenses From Other Operations 2.159 552 2.271 -74 311

Provisions 72 266 218 271 -18Financing Expenses 719 428 992 -40 132

Interest Expenses 405 279 437 -31 57Exchange Rate Differences 310 146 552 -53 277

Extra Ordinary Revenues and Profit 371 1.159 642 213 -45Extra Ordinary Expenses And Losses 1.437 1.755 1.434 22 -18Profit – Loss 1.762 1.516 1.166 -14 -23Net Profit – Loss 1.232 1.028 799 -17 -22Net Profit – Loss / GDP 0,29 0,21 0,14 Source: SOEs and UT

9 The tables in this report cover the data of last three years. Data of last five years can be seen in the annexes. Financial data of 2005 and 2006 are not officially audited and so temporary figures. Data used in the report covers the figures of the SOEs in the Treasury Portfolio as of 2006. In other words, the tables do not cover the figures of the SOEs transferred to the Privatization Administration’s Portfolio before 2006 like TEDAŞ and TEKEL. 10 The accounts of TÜVASAŞ, TÜLOMSAŞ, and TÜDEMSAŞ which are the subsidiaries of TCDD and TEMSAN, one of the subsidiaries of EÜAŞ, are monitored separately from the main SOE. In 2007 TEMSAN’s status is turned to an SOE.

2006 Annual Ownership Report

14

The main reason for the profit shrinkage is the increase in ‘the cost of goods sold’ by 29% despite to the increase in the gross sales by 23%. The sudden depreciation of YTL in May and June of 2006 has affected the input costs of energy SOEs, namely EÜAŞ, TEİAŞ, TPAO and BOTAŞ.

The main reason of 97% increase in the duty loss amounts which is a part of the gross sales in 2005 figures is the high grain purchases of TMO.

Financial expenses are reduced by 40% in 2005 but increased by 132% in 2006. The main reasons behind this issue are the fluctuation in the exchange rates occurred in May and June of 2006 and the financial expenses of the BOTAŞ.

The increases of the other ordinary revenues and ordinary expenses in 2006 are respectively 221% and 311% and composed of the exchange profit and losses from the exchange rates, especially of TPAO and BOTAŞ.

4.1.2. Balance Sheet

The consolidated balance sheet figures of 20 SOEs and 4 subsidiaries in the Treasury portfolio has reached to 73 Billion YTL with an increase of 18% in 2006 from 62 Billion YTL in 2005. In this period the ratio of balance sheet figures to the GDP remained unchanged. (Table 4.2)

One of the most important points in the balance sheet figures is the 4% decrease in stocks. The main reason in this case is the transfer of 3 sugar factories of TŞFAŞ to the PA portfolio from Treasury Portfolio. Table 4.2: Aggregated Balance Sheet (Current Prices - Billion YTL)

2004 2005 2006 Change (%)

(1) (2) (3) (2)/(1) (3)/(2)TOTAL ASSETS 56.072 61.834 72.784 10 18Current Assets 24.647 29.980 38.835 22 30 Liquid assets and Securities 2.238 2.632 3.009 18 14 Trade and Other Receivables 15.495 18.839 26.866 22 43 Inventories 4.464 5.422 5.194 21 -4Fixed Assets 31.425 31.854 33.949 1 7 Trade and Other Receivables 1.478 2.035 1.845 38 -9 Financial Fixed Assets 1.209 1.187 1.219 -2 3 Tangible Fixed Assets 28.105 27.724 29.423 -1 6Short Term Liabilities 17.074 19.728 25.693 16 30 Financial Liabilities 2.654 2.267 3.776 -15 67 Trade and Other Liabilities 9.700 12.187 16.046 26 32 Taxes Payable and Other Fiscal Liabilities 983 1.018 1.212 4 19Long Term Liabilities 6.252 7.075 8.494 13 20 Financial Liabilities 5.547 5.548 6.175 0 11 Trade and Other Liabilities 61 50 556 -17 1011Equity 32.746 35.030 38.596 7 10 Nominal Capital 16.603 19.175 22.952 15 20 Paid in Capital 13.862 16.830 18.825 21 12TOTAL ASSESTS / GDP 13,0 12,7 12,6 Source: SOEs and UT

2006 Annual Ownership Report

15

Increases in the balance sheet are mainly composed of the increases in receivables and the Short term liabilities. SOEs had to fulfill their financial obligations with debts (lending or not-paying some taxes) due to the unability to collect their receivables.

4.1.3. Ratio Analysis

Current Ratio: Current ratio, which shows the capability of paying short term liabilities and sufficiency of net working capital, has not changed much from 2005 to 2006. It was 1,52 in 2005 and 1,51 in 2006.

Table 4.3: Financial Ratios 2004 2005 2006Liquidity Ratios

Current Ratio 1,44 1,52 1,51Acid-Test Ratio 0,84 0,95 1,01Cash Ratio 0,10 0,13 0,11Inventory Turnover 1,52 1,56 1,88Cash Collection Period (Days) 149 166 190Cash Conversion Cycle (Days) 99 100 101

Capital Structure and Long Term Financing Position Financial Leverage 0,42 0,43 0,47Long Term Liabilities / Capital 0,19 0,20 0,22Equity / Assets 0,58 0,57 0,53Interest Coverage Ratio 3,45 4,54 2,18

Rate of Investment Returns Return on Assets (ROA) (%) 3,43 2,25 2,22Return on Equity (ROE) (%) 4,26 3,03 2,17

Operational Ratios Gross Sales Profit Ratio 0,14 0,11 0,08Operating Profit / Sales 0,08 0,06 0,03Profit Before Tax / Sales 0,06 0,04 0,03Net Profit / Sales 0,04 0,03 0,02

Asset Utilization Ratios Sales / Liquid Assets 17,50 13,72 15,91Sales / Receivables 2,42 2,16 1,90Sales / Assets 0,52 0,56 0,60

Source: UT

Acid-Test Ratio: The ratio of the liquid assets, securities and current receivables to the short term liabilities gives the acid-test ratio which was 0,95 in 2005 rose up to 1,01 in 2006

2006 Annual Ownership Report

16

Stock Turnover Ratio: This ratio which shows how many times the firm turns over its stocks along a year rose up to 1,88 in 2006 from 1,56 of 2005.

Cash Collection Period (Days): The length of collecting receivables was 166 days in 2005 and it rose up to 190 days in 2006 due to collecting problems of especially energy SOEs (electricity and natural gas)

Cash Conversion Cycle (Days): This ratio which is around 100 days in both 2005 and 2006, measures in how many days the cash is spent and collected..

Financial Leverage: This ratio shows the percentage of total assets financed by liabilities. In 2005 the financial leverage was 0,43 and it rose up to 0,47 in 2006

Interest Coverage Ratio: This ratio which was 4,54 in 2005 and fell down to 2,18 in 2006, is used to determine how easily a company can pay interest on outstanding debt. The lower the ratio, the more the company is burdened by debt expense.

Return on Assets (ROA) (%): This ratio which was 2,25 in 2005 has fallen down to 2,22 in 2006, measures if the assets in the firm used effectively.

Return on Equity (ROE) (%): This ratio measures the profit per share that the shareholders transfer to the firm. This ratio was 3,03% in 2005 and fallen down to 2,17% in 2006. This ratio rises up to 5% if the SOEs receiving budgetary capital injections (TTK and TCDD) are excluded.

Operation and Asset Utilization Ratios: A downward trend is observed. As an example, the ratio of operating profit to the sales has fallen down to 3% from 6% in 2006 compared to the 2005 figures.

4.1.4. Value Added

The value added is calculated as the sum of net profit, interest payments, provisions, current year’s amortization and the employment costs. The ratio of the value added was 2,4% of the GDP in 2003 and it falls down to 1,7% in 2006.

Chart 1: Value Added

8.800

9.0009.200

9.4009.600

2004 2005 20060,00,51,01,52,02,5

Current Prices (Billion YTL) % GDP (Right Axis)

2006 Annual Ownership Report

17

Box 4: Status Change of Temporary Workers Into Permanent Workers

Although the employment of temporary workers was foreseen as temporary, seasonal or campaign jobs that are needed to be done for a certain period of time in a year, ongoing employment policies in public sector have caused either employment of temporary workers in permanent tasks or periodic jobs that need to be done at certain time intervals. Thus, the temporary workers have turned into permanent workers or workers of continuously repeated contracts.

With Law No: 5620, the statute of temporary workers has been rearranged according to their de facto duties and/or the total work days they have been employed in a financial year. The Law covers SOEs, firms that are in the portfolio of Privatization Administration, central governments and local administrations. In SOEs, temporary workers that were employed more than 6 months in 2006 and temporary workers that worked in the same conditions in 2005 or 2006 with the excuses described in the Law who are currently unemployed due to their temporary worker status, have become permanent workers. On the other hand, from now on, SOEs can only employ temporary workers for seasonal or periodic jobs if they work less than 6 months. The contracts of temporary workers, who have reached 56 in women and 58 in men and have deserved to get a pension, are ended with all their financial legal rights paid.

26.000 temporary workers in SOEs are expected to turn to permanet worker status.

4.2. Employment

Personnel regime of the SOEs has been regulated by Decree Law No.399. Three different kinds of employee statute exist within SOEs.11.

Civil Servant

Civil servants are either subject to Law No. 657 or Decree Law No: 399. These personnel are generally employed as administrative staff who is responsible for performing fundamental and permanent tasks. The titles of civil servants that are subject to Decree Law No: 399, are listed in the first table attached to the Decree.

Contracted Personnel

Contracted personnel are subject to Decree Law No: 399. The titles of contracted personnel are listed in the second table attached to the Decree. The contracted personnel are not qualified as workers. Their main duty is to perform non-administrative tasks.

Workers

The workers are employed according to the Labor Law No: 4857. There are three different statuses for workers.

Union Workers: These workers have the right to involve in collective bargaining processes.

Non-Union Workers: Non-union workers are employed according to Labor Law No:4857 but they are not allowed to involve in collective bargaining processes due to their administrative duties.

11 The statistics of firms that are in the portfolio of Undersecretariat of Treasury and Privatization Authority can be reached at http://www.hazine.gov.tr/stat/kit_ist.htm.

2006 Annual Ownership Report

18

Temporary Workers: Temporary workers are employed in periodic or seasonal for a maximum time of 11 months in a year. Law No: 5620 that passed in 2007 has rearranged the statute of temporary workers. (Box 4)

In SOEs, the salaries of civil servants and contracted personnel are determined with Budget Laws, High Planning Council Decisions and Decrees of Council of Ministers. On the other hand, the wages of workers is determined by collective bargaining.

4.2.1. Personnel Numbers

The policy of decreasing the number of personnel has been adopted with the aim of rationalization of employment, improvement of personnel profile by replacement of redundant workers with qualified workers and improving the competition ability of SOEs. The Annual Decree of Council of Ministers on SOEs allows them to hire 10% of previous year’s attritions, with some exceptions on expert and internationally-enforced positions . The priority in new employment is to hire highly qualified personnel in order to increase the average qualifications of the staff.

In 2000, the average number of personnel employed in Treasury Portfolio was 229.000. The number has been reduced to 171.000 employees in 2006. The number of average personnel employed by SOEs has decreased in 2005 and 2006 by 3,9% and 2,9% respectively. (Table 4.4).

Table 4.4: Personnel Numbers (Yearly Average)

2004 2005 2006 Change(%)

(1) (2) (3) (2)/(1) (3)/(2)Civil Servant + Contracted 84.446 80.190 79.179 -5,0 -1,3Worker 98.898 95.987 91.847 -2,9 -4,3Total 183.344 176.177 171.026 -3,9 -2,9

Source: SOEs and UT

4.2.2. Personnel Costs

In line with the policy of decreasing the number of personnel, personnel costs are also in a declining trend. The employment costs of SOEs that are in the Treasury Portfolio have only increased by 4% and reached a total amount of 5,2 Billion YTL.

Table 4.5: Personnel Costs (Million YTL)

2004 2005 2006 Change(%)

(1) (2) (3) (2)/(1) (3)/(2)Civil Servant + Contracted 1.659 1.763 1.912 6,2 8,4Worker 2.837 3.211 3.260 13,2 1,5Total 4.497 4.974 5.171 10,6 4,0

Source: SOEs and UT

2006 Annual Ownership Report

19

Another indicator for this decrease is the share of personnel costs in total operating costs that are reflected in income statement. The share of personnel costs in the operating costs fell from 36% in 2000 (Appendix 3) to 12% in 2006. (Table 4.6).

Table 4.6: Total Personnel Costs / Total Operating Cost (%)

2004 2005 2006

Civil Servant + Contracted 6,2 5,4 4,5Worker 10,6 9,8 7,7Total 16,7 15,2 12,3Source: UT

4.2.3.Average Personnel Costs

The average personnel cost in SOEs is higher than that of public and private sector. Per month average cost of civil servants and contracted personnel employed in SOEs was 2,012 YTL in 2006. The average cost for workers in the same period realized as 2,957 YTL (Table 4.7).

Table 4.7: Average Personnel Costs (YTL/Month)

2004 2005 2006 Change (%)

(1) (2) (3) (2)/(1) (3)/(2)Civil Servant + Contracted 1.638 1.832 2.012 11,9 9,8

Worker 2.391 2.788 2.957 16,6 6,1

Total 2.044 2.353 2.520 15,1 7,1Source: UT

4.2.4. Personnel Profile

The efforts to reduce the number of personnel while upgrading their quality have not yet given desired results in profile outcomes. The statistics on the personnel profile are presented at the end of the Report. (Appendix 3). According to data collected from SOEs, personnel profile is summarized below:

♦ Average working duration, 16 years

♦ Average age, 42

♦ High school or lower education level, 79%

♦ Women participation, 7,2%

♦ Foreign language skill, 0,7%

2006 Annual Ownership Report

20

♦ The personnel employed for social responsibility and legal obligations are

3% disabled, 1,7% convicted previously 0,3% veteran-martyr relatives 0,5% from Social Services and Child Protection Agency 6,4% special security personnel.

4.3. Other Indicators

The Investment expenditures of SOEs have constantly increased over the last 3 years and reached to the 0,48% of GDP from 0,35% of GDP. The main reasons behind this increase are the new oil wells of TPAO and the investments made by TCDD for high – speed trains (Table 4.8 and Table 4.9.)

Table 4.8: Other Indicators (Billion YTL)

2004 2005 2006 Change (%)

(1) (2) (3) (2)/(1) (3)/(2)Investment Expenditures 1.494 2.229 2.746 49,2 23,2Primary Balance 1.958 546 2.270 -72,1 315,6Budgetary Transfers (Capital, Duty Loss) 1.303 1.423 2.627 9,2 84,6Source: UT and SPO

The Primary balance figure rose up to 2.270 million YTL in 2006 from 546 million YTL in 2005. The most important part in this improvement is the increases in the budgetary transfers figures and improvement of primary balance of TMO in 2006 compared to that of in 2005.

Table 4.9: Other Indicators (Percentage to GDP - %)

2004 2005 2006

Investment Expenditures 0,35 0,46 0,48Primary Balance 0,45 0,11 0,39Budgetary Transfers* 0,30 0,29 0,46*Capital, Duty Loss Source: UT and SPO

4.4. Main Problems of SOEs

Although they operate in a competitive environment and are expected to make profit, SOEs have to face with various problems just because they are state enterprises.

The primary problems can be summarized as followings below:

2006 Annual Ownership Report

21

♦ Pricing Policy: In the Annual Investment and Financing Program Decree12, it is stated that the SOEs “are free to set their prices of goods and services in line with the principles and policies of the ongoing economic program by taking the necessary measures needed for cost efficiency”. However, in practice they have to cope with some problems to realize it.

♦ Duty Losses: Although SOEs do not have any financial problems on accrual basis caused by duty loss mechanism, they usually have problems on cash basis because of the late payments from the central budget.

♦ Non flexible employment policies: SOEs do not have the flexibility on employment issues as much as the private companies, like hiring – firing personnel and wage policies. Additionally, many public institutions other than SOEs are involved in the hiring process.

♦ Investment: investment decisions are one of the most important issues for a company. The Boards of Directors of the SOEs are not independent in decision making process. Their investment projects have to be approved by the SPO.

♦ Procurement Rules: SOEs are subject to the public procurement law unlike their rival firms in private sector. Because of the restrictions in procurement legislation they do not have enough flexibility required for commercial operations.

♦ Board of Directors: Current legal structure of the board of directors is far from modern corporate governance principles.

♦ Auditing: The official auditing process of High Auditing Board takes a long time, around 18 months. Moreover, there are many other institutions like related ministry, State Supervisory Council, Prime Ministry Inspection Board which also have the right to audit and inspect them. SOEs are not subject to the external independent auditing.

12 Decree of Council of Ministers No: 2006/11106 of date September,16, 2006

2006 Annual Ownership Report

22

CHAPTER 5: PERFORMANCES OF THE SOEs

In this section, general introductory information about 20 SOEs in the Treasury portfolio has been presented, and their performance in 2006 is summarized separately.

In analyzing SOEs’ 2006 performances, their operation areas, problems and 2006 developments have been summarized, and financial analysis has been done through several financial ratios.

More detailed data can be reached at the firms’ web sites or in their annual reports.

The list of Board of Directors consists of members as of 31 July 2007, whereas subscribed and paid-in capital amounts represent the figures in Treasury accounts as of 31 December 2006.

SOEs have been classified by their sectors, namely energy and mining, transportation and communication, agriculture and other.

2006 Annual Ownership Report

23

5.1. ENERGY AND MINING SECTORS

2006 Annual Ownership Report

24

2006 Annual Ownership Report

25

5.1.1. BOTAŞ Petroleum Pipeline Corporation Board of Directors ♦ Hüseyin Saltuk Düzyol (Chairman and General Director) ♦ Osman Göksel (Deputy General Director) ♦ Rıza Çiftçi (Deputy General Director) ♦ Representative (NA – Related Ministry Representative) ♦ Representative (NA – Related Ministry Representative) ♦ Representative (NA – Treasury Representative)

Capital Structure Treasury Share : 100% Subscribed Capital:1,83 Billion YTL Paid-in Capital : 1,83 Billion YTL

Related Ministry Ministry of Energy and Natural Resources

Web Address http://www.botas.gov.tr

Petroleum Pipeline Corporation (BOTAŞ) was founded on August 15, 1974 by the Turkish Petroleum Corporation (TPAO) as a subsidiary company under the auspices of the Decree No 7/7871. The primary founding mission of BOTAŞ was the transportation of petroleum through pipelines. Due to Turkey's increasing need for clean and cheap energy sources, the importance of natural gas has increased. Therefore, BOTAŞ has been assigned to expand the pipelines and make natural gas agreements.

Considering the company's existing and future tasks, BOTAŞ was restructured in 1995 by the authority of the Decree of Council of Ministers No. 95/6526 as an SEE obtaining therefore the status of an independent company. BOTAŞ's monopoly rights on natural gas import, distribution, sales and pricing that were granted by Decree No.397 dated February 9, 1990, was abolished by the Natural Gas Market Law No. 4646 which was enacted on May 2, 2001. The Law covers the import, transmission, distribution, storage, marketing, trade and export of the natural gas and the rights and obligations of all real and legal entities related to these activities.

BOTAŞ’s market share in internal transportation is 98%; and its share in natural gas importation is 100%.

Major Developments and Issues

As a result of expansion of natural gas use in the country, new pipelines have been instructed. At the end of the year 2006; the length of the pipelines has reached to 10 km with a supply to 43 provinces. Thus; the consumption of natural gas has increased to 30 billion m3 by 13% rise compared to the previous year.

Today, BOTAŞ imports 32 billion m3 natural gas from different countries including Russia. In order to improve the participation of private sector; BOTAŞ has tendered import contracts for 16 billion m3 natural gas. However, only 250 million m3 of the tendered amount has been transferred yet.

2006 Annual Ownership Report

26

Due to the increasing petroleum prices; natural gas purchase price has also increased by 122% in 2002-2006 periods. Nevertheless, in that time period, the rise in sales prices could be reflected by 82% to households, and 60% to the industry. The price for EÜAŞ, Build-Operate-Transfer (BOT) and Build-Operate (BO) power stations is calculated by adding a margin on purchase price.

On the other hand; BOTAŞ has been experiencing financial difficulties because of collection problems (EGO and EÜAŞ). As a result, to fulfill its financial obligations from abroad, BOTAŞ has begun to get commercial bank loans which has rise to 1.74 billion YTL. The interest for the credit is 197.5 million YTL at the end of 2006; and it is 500 million YTL until May 15, 2007.

Financial Analysis

BOTAŞ experienced operating loss in 2006. The problems related to price adjustment mechanism and collection and the decrease in expected revenue from Iraq-Turkey Natural Gas Pipeline have also triggered BOTAŞ’s financial difficulties. However, with the help of company’s other revenues, its profit has reached to 45 million YTL for this period.

BOTAŞ’s receivables excluding interest is over 4 billion YTL. Due to the problems in energy sector related to collection, street lighting, high loss/leakage and timely pricing, BOTAŞ can not collect cash from EÜAŞ; and the receivables from that company increased continuously.

Receivables of BOTAŞ on July 13, 2007 can be seen in Table 5.1.

Table 5.1: Receivables of BOTAŞ (Million YTL) COMPANY Principle Interest Total %

EGO 677 0 677 6,5EÜAŞ 3.201 5.547 8.748 83,4HEAŞ 299 489 788 7,5EÜAŞ+HEAŞ 3.500 6.036 9.536 90,9İZGAZ(Treasury) 40 0 40 0,4İZGAZ (In effect) 20 0 20 0,2BOT+BO 58 9 66 0,6İGDAŞ 0 2 2 0,0TÜGSAŞ 4 18 22 0,2Other 84 15 99 1,2TOTAL 4.383 6.080 10.464 100,0Source: BOTAŞ

2006 Annual Ownership Report

27

Law No: 5669, which aims to expedite for the collection of receivables from EGO, was accepted in Parliament on May 25th, 2007. It is stipulated that the minimum 80% of the Ankara’s natural gas distribution company which the Metropolitan Municipality (EGO) owns will be privatized within 2 years. Moreover, it is envisaged in the Law that within one month following the completion of privatization date, outstanding receivables of EGO to BOTAŞ will be paid.

SELECTED INDICATORS 2005 2006 % Increase(Million YTL) Gross sales 8.155 12.307 50,9Operating profit or loss 232 -150 -164,6Profit or loss 245 45 -81,8Total Assets 8.400 11.742 39,8Acid – Test Ratio 0,81 0,81 -0,2Average Collection Period (Days) 156 160 2,5Cash Conversion Cycle (Days) 96 97 1,2Return on Equity (ROE) (%) 6,7 1,2 -81,7Total Employment Figure (Average) 2.745 3.110 13,3Total Employment Cost 116 159 36,6Value Added 905 655 -27,5Investment Expenditure 573 543 -5,2Payments to Budget (Dividend and Treasury Levies) 0 0 -Payments from Budget (Capital and Duty Loss) 0 0 -Primary Balance 55 -424 -876,5Source: BOTAŞ, UT and SPO

Employment cost of the company has increased parallel to the new staffing; but the value added figure has decreased. Furthermore, whereas the primary surplus of the company was 55 million YTL for the year 2005, it became -424 Million YTL in 2006.

2006 Annual Ownership Report

28

5.1.2. EÜAŞ Electricity Generation Incorporated Company Board of Directors ♦ Sefer Bütün (Chairman and General Director) ♦ Nurettin Kulalı (Deputy General Director) ♦ M.Ahmet Dere (Related Ministry Representative) ♦ Mehmet Faruk Akşit (Related Ministry Representative) ♦ Member (Empty – Related Ministry Representative) ♦ Edip Yılmaz (Treasury Representative)

Capital Structure Treasury Share : 100% Subscribed Capital: 1,3 Billion YTL Paid-in Capital : 1,3 Billion YTL

Related Ministry Ministry of Energy and Natural Resources

Web address http://www.euas.gov.tr

Electricity Generation Incorporated Company (EÜAŞ) was established to carry out its generation activities as an SOE according to the Decree Law No. 233 and 399, the Decree of Council of Ministers No. 2001/2026 and Electricity Market Law No. 4628. Its Articles of Association was published in Official Gazette No. 26241on 27th of July in 2006.

EÜAŞ is an SEE which is established to generate electricity efficiently and profitably under the guidance of economic and energy policies of the State. Other functions of EÜAŞ are:

♦ to contract electrical energy sales and /or sub sevices ♦ to take over the due facilities, to operate the generation facilities of which have

not taken over by the private sector, via by herself and/or subsidiaries, or to take out the system when necessary.

♦ to get the licences from the Energy Market Regulatory Authority (EMRA) according to its field of activity and to pay licences costs to EMRA. To act according to these licences.

♦ to procure all kinds of studies, projects, constructions and facilities needed for electricity generation.

♦ to procure all kinds of goods and services for maintenance, repair, rehabilitation, operation and development of the generation facilities domestically and/or via import.

♦ To operate , the mines to be used for electricity generation at the existing or future thermal power plants and other resources or to make it generated via service procurement.

In 2006 EÜAŞ’s market share was 48%.

2006 Annual Ownership Report

29

Major Developments and Issues

In the year 2006 there were both structural and legal changes in the electricity energy sector. A Loan Agreement of “Electricity Generation Rehabilitation and Restructuring Project” was signed on 12.09.2006 between World Bank and EÜAŞ. The rehabilitation of Afşin Elbistan A thermic plant started with this loan agreement. On the other hand, with the exception of hydroelectric plants held in EÜAŞ body, 6 portfolio generation groups were established. On 12.02.2006 Afşin Elbistan-B plant with 1440 MW installed capacity became operational. It is expected that the production figure will be 8 billion kwh in a year, if it goes into a full capacity production.

The efforts on the preparation of regulation for “Hand over of hydro plants which were built by DSİ to EÜAŞ” continued in 2006.

In June 2006, transition period contracts about energy purchase and sale were signed between EÜAŞ’s portfolio generation groups and distribution companies which have retail sale licence. The period is set not to exceed 5 years.

EÜAŞ’s thermic plants working by natural gas was affected from increased natural gas prices (Price of natural gas is linked to price of petroleum). In addition to this private sector producers gave up producing electricity due to the high natural gas prices. Thus EÜAŞ had to produce more than it had planned.

Moreover EÜAŞ has been still negatively effected from the debt and receivable problem among energy SOEs.

Financial Analysis

In 2005 EÜAŞ’s total assets were 16,1 billion YTL. In 2006 it increased by 20% and reached to 19,3 billion YTL. High increases in” Commercial and other receivables” and “short term loan capital” figures are caused by the increase of EÜAŞ’s short term debts to other energy SOEs .

In 2006 gross sales increased by 41.7% and reached to 5,7 billion YTL, profit of the period decreased to 269 million YTL by 42.4%. (In 2006 EÜAŞ’s total energy production was 84.4 billion kwh, total energy sales was 80.5 billion kwh)

Despite 42 % increase in sales, 59% increase in cost of goods sold lowered the profitability. In 2005 financing costs decreased 47% but in 2006 it increased 261%. This high increase was due to the fluctuation of foreign exchange rates occured in May 2006.

Current ratio has been 1.4 for the last 3 years. Acid test ratio has been increasing since 2004, and in 2006 it became 1.1.

2006 Annual Ownership Report

30

Due to the fact that average average collection day of its receivables increased from 327 days in 2005 to 400 days in 2006. Since the company can’t collect its receivables on time from distribution companies and TETAŞ, cash conversion cycle increased rapidly in 2006.

SELECTED INDICATORS 2005 2006 % Increase(Million YTL) Gross sales 4.024 5.702 41,7Operating profit or loss 1.119 923 -17,5Profit or loss 468 269 -42,4Total Assets 16.116 19.337 20,0Acid – Test Ratio 0,98 1,07 8,4Average Collection Period (Days) 327 400 22,3Cash Conversion Cycle (Days) -5 44 -1.009,5Return on Equity (ROE) (%) 3,6 2,2 -38,0Total Employment Figure (Average) 11.910 13.134 10,3Total Employment Cost 392 427 8,9Value Added 1.708 1.955 14,4Investment Expenditure 415 244 -41,3Payments to Budget (Dividend and Treasury Levies) 0 0 -Payments from Budget (Capital and Duty Loss) 0 0 -Primary Balance 984 1.055 7,2Source: EÜAŞ, UT and SPO

In 2006 EÜAŞ’s value added was around 1,9 billion YTL and primary surplus was 1 billion YTL. In 2006 EÜAŞ was the third company in the Istanbul Chamber of Industry’s (ISO) biggest industrial company list according to the sales from production.

2006 Annual Ownership Report

31

5.1.3. TEİAŞ Electricity Transmission Company Board of Directors ♦ İlhami Özşahin (Chairman and General Director) ♦ Halil Alış (Deputy General Director) ♦ Kemal Yıldır (Deputy General Director) ♦ Bilal Eryılmaz (Related Ministry Representative) ♦ Mehmet Kamil Şani (Related Ministry Representative) ♦ İrfan Tokgöz (Treasury Representative)

Capital Structure Treasury Share : 100% Subscribed Capital : 330 Million YTL Paid in Capital : 326 Million YTL

Related Ministry Ministry of Energy and Natural Resources

Web Address http://www.teias.gov.tr

Electricity Transmission Company (TEİAŞ) started its operations in 01.10.2001 in order to take over the transmission lines and to provide electricity transmission and balancing and settlement services. The Articles of Association of TEİAŞ was published in Offical Gazette No. 24447 on 26.06.2001.

The company is subject to Decree Laws No.233 and 399 which concerns SOEs. It has obtained the transmission license from EMRA in 2003 and it operates in accordance with regulations envisaged in new market model.

TEİAŞ is the sole owner of the transmission license in Turkey. Main responsibilities of the company are; planning, operating and rehabilitating the 400 and 154 kV transmission lines to provide high quality and continuous energy supply, preparing necessary tariffs, overseeing the central dispatch system and undertake the required balancing and international interconnection operations and preparing the electricity generation capacity projection report in line with the demand projections of distribution companies.

The company’s market share is 100%.

Major Developments and Issues

The balancing and settlement market which was in virtual mode between November 2004 and August 2006 became operational starting from 01.08.2006. Recently, the share of this market ranges 5% - 10% subject to the degree of discrepancy between demand and supply for each distribution company.

In July 2007, Turkey’s Electricity Energy Generation Capacity Projection for 10 Year (2007-2016) has been published. This report is revised annually based on the recent market data.

2006 Annual Ownership Report

32

In 2007, the increase in electricity demand is 8,5% compared to previous year. The annual consumption is 189.4 TWh and installed capacity is 40.7 GW.

Regarding interconnections with Europe, Turkey aims to become a member of Union for the Co-ordination of Transmission of Electricity (UCTE). The necessary work has been started in 2005 and is projected to be completed in 2008.

TEİAŞ faces significant receivables problem as other energy SOEs have. Owing to the arrears of EÜAŞ and its affiliates, TEİAŞ has to get external financing in order to undertake its investments. Transmission lines require expropriation which may extend the time for the completion of necessary investments.

Furthermore, the company lacks enough technical personnel compared to other countries. For example, number of personnel per kilometer is 0.026 in Turkey, whereas this figure is 0.081 in France and 0.043 in Spain. Therefore, the priority is given to the hiring of the technical personnel.

Financial Analysis

Main cost items of TEİAŞ include transmission investments and expenditures related with providing transmission services, such as operating expenses, replacement costs and ancillary service costs. The tariffs to finance these costs are; Connection and Use of System Tariff and Transmission Tariff. These tariffs are regulated by EMRA which envisages a ceiling on income of TEİAŞ.13 The tariffs are differential for consumers and producers. Furthermore, there is also tariff differential among different regions in Turkey.

80% of the sales revenue proceeds from public companies, whereas private sector’s share is only 20%.

The sales revenue of TEİAŞ is related with installed capacity of producers and consumption capacity of consumers rather than electricity transmitted through lines.

The revenue from Balancing and Settlement Market is reflected to financial tables of TEİAŞ. Accordingly, the gross sales revenue in 2005 was 787 Million YTL whereas it is 1.730 Million YTL in 2006. On the other hand, cost of the goods sold increased 821 Million YTL between 2005 and 2006.

The total value of assets is 7.32 Billion YTL.

In 2006, Average collection period was 304 days. This is mainly due to the receivables from EUAS and its affiliates. The total amount of receivables is 753 Million YTL.

13 Income ceiling is adjusted every year according to the energy price index, preset efficiency factor and realization of deficit or surplus of the previous years income.

2006 Annual Ownership Report

33

SELECTED INDICATORS 2005 2006 % Increase(Million YTL) Gross sales 787 1.730 119,7Operating profit or loss 83 150 81,5Profit or loss 112 89 -20,9Total Assets 6.491 7.318 12,8Acid – Test Ratio 3,45 1,74 -49,5Average Collection Period (Days) 274 304 10,9Cash Conversion Cycle (Days) 197 128 -34,9Return on Equity (ROE) (%) 1,9 1,1 -43,2Total Employment Figure (Average) 8.604 8.500 -1,2Total Employment Cost 262 278 6,1Value Added 764 847 10,9Investment Expenditure 230 276 20,1Payments to Budget (Dividend and Treasury Levies) 0 0 -Payments from Budget (Capital and Duty Loss) 0 0 -Primary Balance 242 218 -9,8Source: TEİAŞ, UT and SPO

In 2005, the profit margin was 14% whereas in 2006 this ratio decreased to 4%. On the other hand, return on capital was 1,1% in 2006, decreasing from 1,9% in 2005.

The company provided primary surplus both in 2005 and 2006.

2006 Annual Ownership Report

34

5.1.4. TETAŞ Turkish Electricity Trading and Contracting Incorporated Company Board of Directors ♦ Hacı Duran Gökkaya (Chairman and General Director ) ♦ Selahattin Çimen (Related Ministry Representative) ♦ Hüseyin Karakaya (Related Ministry Representative) ♦ Member (Empty-Related Ministry Representative ) ♦ Member (Empty-Related Ministry Representative) ♦ Nevzat BAHRAN (Treasury Representative)

Capital Structure Treasury Share :100% Subscribed Capital:179 Million YTL Paid-in Capital : 73 Million YTL

Related Ministry Ministry of Energy and Natural Resources

Web Address http://www.tetas.gov.tr

Turkish Electricity Trading and Contracting Incorporated Company (TETAŞ) was established to do electricity trading and contracting activities depending on Decree Laws No. 233 and 399, The Decree of Council of Ministers No. 2001/2026 and Electricity Market Law No. 4628. Its Articles of Association was published in Official Gazette No. 24447 on 29th of June in 2001.

TETAŞ is an SEE which is founded to trade electricity under the guidance of economic and energy policies of the State. Other functions of TETAŞ are: to take over the energy purchase and sale contracts from TEAŞ and TEDAŞ which were signed in according to related legislation, under the restriction of the Law No. 4628 to do energy sale contracts and energy purchase contracts (last for less than one year), to import / export electricty from / to countries which has suitable interconnection conditions, to prepare the wholesale tariffs and implement the approved tariffs, to take electricity from the hydro plants which EÜAŞ owns, to take the necessary measures to obtain consistent, low-cost electricity, to modify the energy sale and purchase agreements according to changing sectoral and legal conditions within the approval of the UT.

In 2006 TETAŞ’s market share was 100%.

Major Developments and Issues

According to the Law No: 5496, transitional period contracts concerning energy purchase and sale were signed between TETAŞ and distribution companies in June 2006.

Within the context of these contracts EÜAŞ’s hydro plants would sell 25 billion kwh electricity to TETAŞ in a year. TETAŞ would provide electricity both from EÜAŞ’s hydro plants and BOT, BO, Transfer of Rights (TOR) plants which would lead to a decrase in the average purchasing costs. TETAŞ would sell this electricty to 20 distribution companies with the price approved by EMRA.

2006 Annual Ownership Report

35

Since BOT, BO, TOR contracts which lasts 15-20 years were not signed under the competitive conditions and since these plants mostly depend on natural gas (85% of sales of BO, 100% of sales of BOT are Treasury guaranteed) TETAŞ’s purchasing cost increases.

Financial Analysis

SELECTED INDICATORS 2005 2006 % Increase(Million YTL) Gross sales 10.077 10.726 6,4Operating profit or loss 38 96 152,1Profit or loss 66 48 -26,6Total Assets 6.415 7.587 18,3Acid – Test Ratio 1,00 1,01 1,3Average Collection Period (Days) 221 250 13,4Cash Conversion Cycle (Days) 46 49 6,9Return on Equity (ROE) (%) 40,2 27,7 -31,1Total Employment Figure (Average) 213 215 0,9Total Employment Cost 5,4 5,1 -4,7Value Added 91 55 -39,6Investment Expenditure 0,0 0,3 31.516,2Payments to Budget (Dividend and Treasury Levies) 0 0 -Payments from Budget (Capital and Duty Loss) 10 14 38,5Primary Balance 63 32 -49,7Source: TETAŞ, UT and SPO

In 2005 TETAŞ’s total assets were 6,4 billion YTL. In 2006 it increased 18% and reached to 7,6 billion YTL. In 2006 commercial and other receivables item increased 21% and reached to 7,4 billion YTL. Problems arising from unability to collect the receivables increased the amount of short term liabilities.

In 2006 TETAŞ’s gross sales increased 6.4% and reached to 10,7 billion YTL (In 2006 total energy sales were 118 billion kwh). In 2006 profit of the period decreased 27% to 48 million YTL.

Current ratio and acid test ratio of TETAŞ was around 1. Average collection period of its receivables which was 221 days in 2005, increased to 250 days in 2006. Moreover its financial structure mostly depended on short and long term liabilities. Equity/Liability ratio was 0,02.

In 2006 TETAŞ’s primary surplus decreased 50% and realized 32 million YTL.

2006 Annual Ownership Report

36

5.1.5. TKİ Turkish Coal Enterprise Board of Directors ♦ Selahaddin Anaç (Chairman and General Director ) ♦ Yaşar Topçuoğlu (Deputy General Director) ♦ Ziya Coşar (Related Ministry Representative) ♦ Mehmet Tombul (Related Ministry Representative) ♦ Representative (NA - Related Ministry Representative) ♦ Nurşen Demirbilek (Treasury Representative)

Capital Structure Treasury Share : 100% Subscribed Capital : 360 Million YTL Paid-in Capital : 360 Million YTL

Related Ministry Ministry of Energy and Natural Resources

Web Address http://www.tki.gov.tr

The coal production units that were under the control of Etibank Company, had been transferred to Turkish Coal Enterprise (TKİ) in 1957 by the Law No. 6974. As an SEE, TKİ started its activities after its Articles of Association was published in Official Gazette No.18588 on November, 1984. TKİ is also subject to the Mining Law No. 3213

In accordance with the Government’s general energy policy, TKİ has been assigned to produce lignite and some other types of coal and to meet the country’s coal demand.

55% of the total lignite production capacity of Turkey comes from TKİ. The Company’s production depends on the requirements of the power generation companies and the demands of heating and industry. 22% of total Electricity Generation Company (EÜAŞ)’s electricity production in 2006 was performed by the input that TKİ has provided.

Major Developments and Issues

The Company distributes coal, not less than 500 kg, to poor families by Governorships, since 2003. In the period of 2005-2006 1,3 million tones of coal were distributed through out the country.

TKİ can not collect its receivables from EÜAŞ. The receivables from EÜAŞ were 135 million YTL in December, 2006.

Financial Analysis

The sales revenue of the company has increased by 17% to 1,4 billion YTL, and the profit of the period has increased by 38% to 40 million YTL in 2006. However, to meet its financial needs, TKİ get commercial bank loans and the interest expense of this loans came up to 13 million YTL at the end of 2006.