2006 annual report

DESCRIPTION

the 2006 KMBI Annual ReportTRANSCRIPT

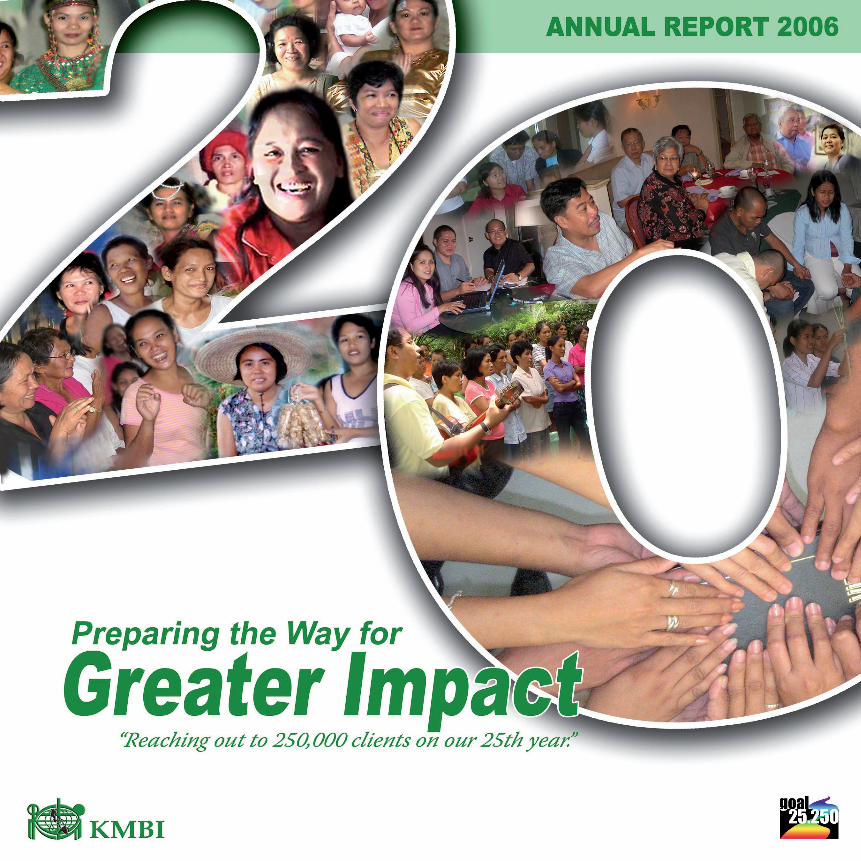

PREPARING THE WAY FOR GREATER IMPACT g 1

g KMBI ANNUAL REPORT 2006 2

transforming

OUR VISION is to see people in communities live in abundance with strengthened faith in God and in right

relationship with their fellowmen and the rest of creation.

OUR MISSION is to help transform the lives of our clients and develop our human resources who will provide

sustainable microfi nance, training and demand-driven non-fi nancial services.

OUR CORE VALUES are respect, integrity, stewardship, commitment to the poor, discipline, innovation

and excellence.

g KMBI ANNUAL REPORT 06 2

PREPARING THE WAY FOR GREATER IMPACT g �

lives

OUR GOAL is to reach out 250,000 clients by 2011.

ContentsMessage 4Highlights 62006 at a Glance 8Philippine Poverty 10Pro-active Response to Poverty 11The Catalysts 12Road map: Goal 25.250 1�Financials 14History �1The People Behind �2Directory �5

g KMBI ANNUAL REPORT 2006 4

ENVISIONING TRANSFORMATION

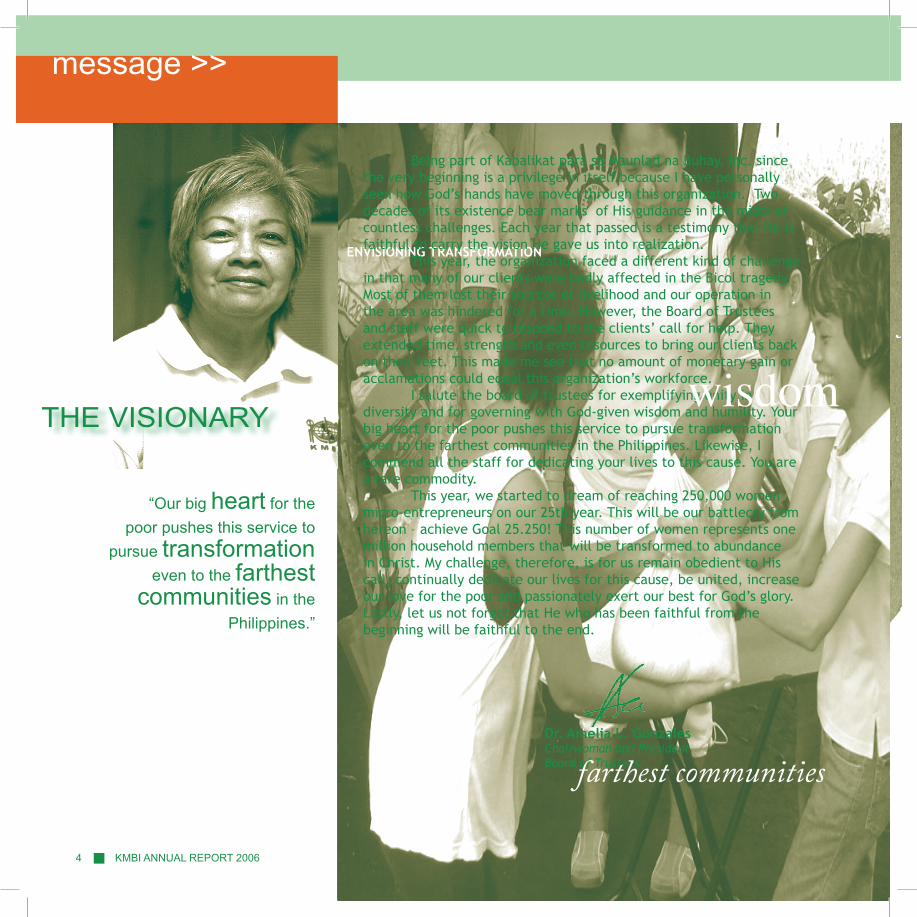

THE VISIONARY

message >>

Dr. Amelia L. GonzalesChairwoman and PresidentBoard of Trustees

“Our big heart for the poor pushes this service to

pursue transformation even to the farthest

communities in the Philippines.”

Being part of Kabalikat para sa Maunlad na Buhay, Inc. since the very beginning is a privilege in itself because I have personally seen how God’s hands have moved through this organization. Two decades of its existence bear marks of His guidance in the midst of countless challenges. Each year that passed is a testimony that He is faithful to carry the vision He gave us into realization. This year, the organization faced a different kind of challenge in that many of our clients were badly affected in the Bicol tragedy. Most of them lost their sources of livelihood and our operation in the area was hindered for a time. However, the Board of Trustees and staff were quick to respond to the clients’ call for help. They extended time, strength and even resources to bring our clients back on their feet. This made me see that no amount of monetary gain or acclamations could equal this organization’s workforce. I salute the board of trustees for exemplifying unity in diversity and for governing with God-given wisdom and humility. Your big heart for the poor pushes this service to pursue transformation even to the farthest communities in the Philippines. Likewise, I commend all the staff for dedicating your lives to this cause. You are a rare commodity. This year, we started to dream of reaching 250,000 women micro-entrepreneurs on our 25th year. This will be our battlecry from hereon – achieve Goal 25.250! This number of women represents one million household members that will be transformed to abundance in Christ. My challenge, therefore, is for us remain obedient to His call, continually dedicate our lives for this cause, be united, increase our love for the poor and passionately exert our best for God’s glory. Lastly, let us not forget that He who has been faithful from the beginning will be faithful to the end.

PREPARING THE WAY FOR GREATER IMPACT g 5

message >>

“We believe that access to a well-functioning financial system, predicated in positive values and divine life purpose, can economically and socially empower individuals...”

THE LEADER

Edgardo S. MercedesExecutive Director

Life is a journey, and a journey has its beginning and end. Man’s journey, regardless of how far he had traveled will not be remembered for so long without it being chronicled. KMBI, of which the Almighty God has breathed life into, has its beginnings and ends as well. Thus, this Annual Report 2006 is a chronicle that accounts God’s moving in KMBI’s journey. This is a journal that records in its pages the light and heavy treks we had done during the year. Certainly the treks we started will have their ends; such also maybe the time to start another one. But our intention, as we anticipate modification or replacement of the initiatives we started in due time, is to see the treks we made serve their respective purposes. The year was an era of new calling, new image and new wave for all the stakeholders of KMBI geared towards realizing bilateral aspirations. These include seeing in the near future a more significant and deliberate social and spiritual impacts through relevant programs and interventions, as well as financial independence characterized by abundance and stability. We believe that access to a well-functioning financial system, predicated in positive values and divine life purpose, can economically and socially empower individuals, in particular the impoverished people, allowing them to better integrate into the economy, actively contribute to development and protect themselves against economic shocks. The stratagem is to capacitate our workforce in the area of personal and professional growth and equip them with life skills essential to the work of development. Another is to over-deliver financial and non-financial products, and entrepreneurial services that fit the business needs of the program members. Finally, we will augment the integrated programs en route for holistic transformation. As we close 2006 and unfold 2007, we are ending a very fruitful year and beginning a new and promising journey headed to the realization of Goal 25.250 -- that is reaching to 250,000 clients on our 25th year of existence. All the strategies cited remain in drawing board until such time you choose to involve proactively in preparing the way for greater impact. Join me in this journey!

g KMBI ANNUAL REPORT 2006 6

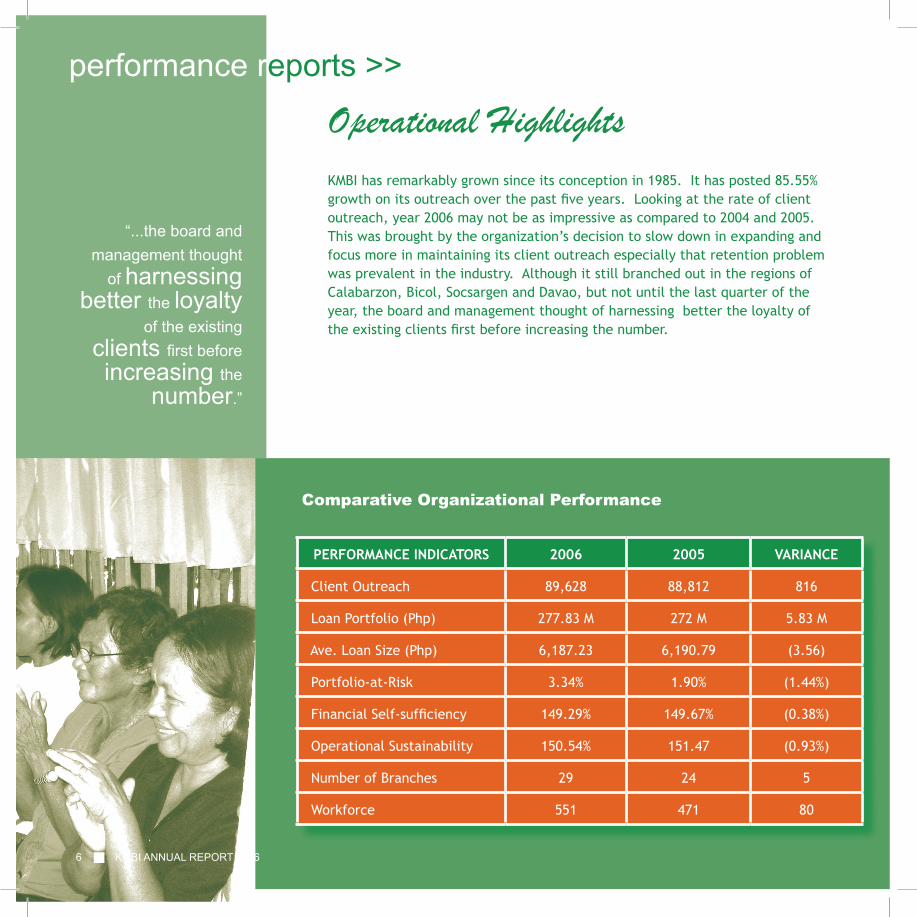

KMBI has remarkably grown since its conception in 1985. It has posted 85.55% growth on its outreach over the past five years. Looking at the rate of client outreach, year 2006 may not be as impressive as compared to 2004 and 2005. This was brought by the organization’s decision to slow down in expanding and focus more in maintaining its client outreach especially that retention problem was prevalent in the industry. Although it still branched out in the regions of Calabarzon, Bicol, Socsargen and Davao, but not until the last quarter of the year, the board and management thought of harnessing better the loyalty of the existing clients first before increasing the number.

Operational Highlights

PERFORMANCE INDICATORS 2006 2005 VARIANCE

Client Outreach 89,628 88,812 816

Loan Portfolio (Php) 277.83 M 272 M 5.83 M

Ave. Loan Size (Php) 6,187.23 6,190.79 (3.56)

Portfolio-at-Risk 3.34% 1.90% (1.44%)

Financial Self-sufficiency 149.29% 149.67% (0.38%)

Operational Sustainability 150.54% 151.47 (0.93%)

Number of Branches 29 24 5

Workforce 551 471 80

Comparative Organizational Performance

“...the board and management thought

of harnessing better the loyalty

of the existing clients first before increasing the

number.”

performance reports >>

g KMBI ANNUAL REPORT 2006 6

PREPARING THE WAY FOR GREATER IMPACT g �PREPARING THE WAY FOR GREATER IMPACT g �

reports >>

In 2005, the Microfinance Information Exchange (MIX) released a review on the profitability of over 500 MFI’s worldwide. With 21.39% return on asset, KMBI was declared to be the third most profitable microfinance institution all over the world.

KMBI’s operations in 2006 was tested by natural and man-made disasters, especially in Bicol region which was hit by two super typhoons. Despite the odds, KMBI managed to thrive both on its operational and financial performances. The minimal growth on its client outrach was cushioned by the high 96.66% repayment rate on the loans it extended to microentrepreneurs. This translated an 11.86 percent increase on the organization’s total asset.

With the financial growth obtained, although there is still a long way to go, KMBI sees more prospects and opportunities to facilitate holistic transformation to an increasing number of women microentrepreneurs and their families.

performance reports >>

PERFORMANCE INDICATORS 2006 2005

Operational Income 71,055,236 89,779,928

Asset 452,085,485 404,055,124

Liability 209,225,538 232,250,413

Fund Balance 242,859,947 171,804,711

Grants 5,231,000 17,125,000

Comparative Financial Performance

Financial Highlights

“With the financial growth obtained, although there is still a long way to go, KMBI sees more prospect to facilitate holistic transformation...“

PERFORMANCE INDICATORS 2006 2005 VARIANCE

Client Outreach 89,628 88,812 816

Loan Portfolio (Php) 277.83 M 272 M 5.83 M

Ave. Loan Size (Php) 6,187.23 6,190.79 (3.56)

Portfolio-at-Risk 3.34% 1.90% (1.44%)

Financial Self-sufficiency 149.29% 149.67% (0.38%)

Operational Sustainability 150.54% 151.47 (0.93%)

Number of Branches 29 24 5

Workforce 551 471 80

g KMBI ANNUAL REPORT 2006 8

2006 at a glance >>

g KMBI ANNUAL REPORT 2006 8

Being twenty prompted the organization to review systems and movements made in the past years. A transparent internal assessment exposed previous years as time well-spent on organizational growth and maintenance. This moved the organization to devise clear goals and systematized directions to strategically achieve the triple bottom-line goal: deepened and widened outreach, self-sufficiency and increased impact. These goals promise stability for the next five years. Hence, 2006 defined where the organization has been to shape its strategic road map towards poverty alleviation.

Areas of Transformation WidenedTo widen the organization’s sphere for community transformation, it expanded its operations through the establishment of new branches and splitting some of the current branches. New branches were established in Biñan, Daet, Tacurong and Koronadal City. On the other hand, Metro Davao branch was split into Metro Davao 1 and 2. This horizontal expansion also prompted the splitting of Southern Mindanao operations into North and South Cotabato and Davao operations to better serve the microentrepreneursin the area. With this, KMBI ended 2006 with 29 branches.

Program Impact DeepenedDeveloping the potential of more than a hundred household beneficiaries for community enterprise in Koronadal, South Cotabato, the community-based enterprise development program (CBEDP) was commenced in early December. The project seeks to build the economic landscape of the community which is deprived of access to financing, market, common infrastructure and support services. Ongoing sessions involve beneficiaries on participatory planning and capacity building until viability of the enterprise is achieved. Once the community is ready, microfinance program will be offered to the locale’s microentrepreneurs to further boost economic activities. This project is done in coordination with AusAID through Opportunity International Australia and is closely monitored by the Enterprise Development Unit until 2009.

Structure Fortified

Edgardo Mercedes succeeded Rosemarie Castro who stirred KMBI during her last five-year stint. Alongside this was the further fortification of the organization’s structure brought by the following movements: (a) splitting of transformation focus to schematize programs that cater to its two internal clients - the staff and program members; (b) putting up separate offices for Luzon and Mindanao operations for better monitoring and supervision; (c) extracting publications from the Research and Development department for it to concentrate more on product development and other studies that will inform the organization’s decisions;

PREPARING THE WAY FOR GREATER IMPACT g �

2006 at a glance >>

(d) defining market development as Enterprise Development Services unit’s major role; (e) creation of the Resource Mobilization and Communications department; and (f) branching out of the Training unit from the Human Resource Development department to fully focus on skills and capacity-building of the staff.

Systems ModifiedReviews of the previous system revealed areas that obstruct effective facilitation of transformation in the lives of the clients. This led to the modification of the system in the aspects of recording, reporting, branch and center structures, loan application and processing, human resource management, among others. Since its implementation in November, the program assistants’ clerical load was lessened giving them ample time to conduct transformational activities in the communities. Likewise, number of forms was significantly reduced to 58% resulting to fast application processing time. To ensure efficient implementation of the modified system, branch staff were re-oriented and provided with developmental training.

Workforce BoostedThe organization believes that transformation starts from within. Because of this, the mission statement was revised and made two-fold to give emphasis on the development of the clients and its human resources. People underwent internal and external trainings during the course of the year. Ninety-seven percent of the board of trustees and staff participated in the quarterly Leadership Enrichment and Development (LEaD) sessions with a purpose of becoming pro-active servant-leaders in the communities. Moreso, 33 staff enrolled in the graduate program of the Microfinance

Success Institute. Aside from this educational advancement, the branch managers, program unit supervisors and branch accountants were equipped through in-house training on management and operations. Selected staff members were also sent to external training on public speaking, leadership, management development, stewardship, human development, among others. In the middle of the year, the staff was gathered in regional retreats to ignite their commitment and dedication to the cause of the organization.

Manpower count at year-end increased by 85%, from 471 to 551 staff members, as new branches were opened.

Partnerships ForgedTo pool financing and expertise towards poverty reduction, the organization forged new partnerships with Landbank Countryside Development Foundation and People Power against Poverty through Micro Enterprise (PPP-ME or PinoyME). These two organizations share the mission of integrating the working and entrepreneurial poor into the mainstream economy. Specific actions achieved through this partnership were provision of microcredit, capacity-building services, research, publication and other innovative approaches.

Transformation Activities StrengthenedBuilding up the social and biblical foundations of the

internal and external clients has always been the focus of KMBI’s transformation programs. Among the programs were the formulation of the discipleship groups and distribution of Bibles to the staff, facilitation of seminar on biblical parenting, mass weddings, and implementation of four immediate post disaster responses to clients affected by disasters.

g KMBI ANNUAL REPORT 2006 10

Poverty is hunger. Poverty is lack of shelter. Poverty is being sick and not being able to see a doctor. Poverty

is not having access to school and not knowing how to read. Poverty is not having a job, is fear for the future, living one day at a time. Poverty is losing a

child to illness brought about by unclean water. Poverty is powerlessness, lack of representation and freedom.

– World Bank

HOW POOR ARE THE FILIPINOS?• At least 14.8 million Filipinos

lives on less than $1 a day, accounting for 1.5 percent of the people in the world currently trapped in extreme poverty.

• 19% of the population or 76.5 million lived on the $1-a-day international poverty line as of May 2000.

• Most of the poor Filipinos live in rural areas. Bicol and Central Mindanao are considered two of the poorest regions.

• Approximately 13.9% to 16.9% of the population sleep in hunger in 2006.

• About 72.8% are worried that food would run out before they get money to buy more.

• Approximately 3.67 million children under five years of age are chronically underweight.

• 2 out of 10 Filipino families do not have access to safe drinking water.

• About 2.9 million Filipinos are unemployed and 7.8 million are underemployed.

Sources: World Bank, Annual Poverty Indicators Survey (APIS), National Statistics Office (NSO), Social Weather Stations (SWS), Government Census, Food and Nutrition Research Institute (FNRI), and Central Intelligence Agency (CIA).

poverty >>

g KMBI ANNUAL REPORT 2006 10

PREPARING THE WAY FOR GREATER IMPACT g 11

OuOour response >>

HOW POOR ARE THE FILIPINOS?• At least 14.8 million Filipinos lives on less than $1

a day, accounting for 1.5 percent of the people in the world currently trapped in extreme poverty.

• 19% of the population or 76.5 million lived on the $1-a-day international poverty line as of May 2000.

• Most of the poor Filipinos live in rural areas. Bicol and Central Mindanao are considered two of the poorest regions.

• Approximately 13.9% to 16.9% of the population sleep in hunger in 2006.

• About 72.8% are worried that food would run out before they get money to buy more.

• Approximately 3.67 million children under five years of age are chronically underweight.

• 2 out of 10 Filipino families do not have access to safe drinking water.

• About 2.9 million Filipinos are unemployed and 7.8 million are underemployed.

Sources: Annual Poverty Indicators Survey (APIS), National Statistics Office (NSO), Social Weather Stations (SWS), Government Census, Food and Nutrition Research InstitutFood and Nutrition Research Institute (FNRI), and Central Intelligence Agency (CIA).

Build inclusive financial productsKMBI ushers women microentreprenuers to its holistic transformational program, which incorporates financial and non-financial products and services. The financial package includes microcredit with a range of PhP4,000 to PhP20,000,

microinsurance and client build-up (CBU), to increase the clients’ capital accumulation over time.

Build healthy communitiesThe organization’s approach to fighting poverty and facilitating holistic transformation is community-based. Clients are grouped from 30 to 40 members in a trustbank (or center). Every week, clients gather as a community and openly interact with fellow micro-entrepreneurs, developing sense of social responsibility and accountability within their sphere.

Intervene thru enterprise developmentThrough the Enterprise Development Services (EDS), clients are subjected to different training curriculum and programs, such as Improve Your Business and Success Circle, where clients are given continuous entrepreneurial inputs, alternative livelihood training, technical assistance, market linkage and increased opportunities for promotions and product brokerage toward achieving development or diversification in their businesses. Deepening of outreach is also achieved through the Community-based Enterprise Development Program (CBEDP).

Maximize women capacitiesDoors of opportunities are seldom open for microentrepreneurs because they do not possess proper training. This, aside from developing their enterprise, KMBI maximizes client capacities through additional training and projects towards educating them on values formation, health care, personality development and caring for the environment. These inputs lead to women being catalysts of transformation, firstly, in their homes, then, in their communities.

WHAT KMBI DOES TO HELP REDUCE POVERTY

KMIBI pro-actively invests on holistic transformation or integral mission believing that it would reduce poverty slowly among the communities it serves.

g KMBI ANNUAL REPORT 2006 12

GENERAL SANTOS CITY. Belle sustained the family when her husband left them. However, she rose above her problems and worked her way up as a dressmaker with a big heart to share to others. Aside from being responsible for generating special projects for her trustbank group in General Santos City, she also helped disabled persons in her barangay continue a rag-making project which is their source of living. Belle bought the rags they produced with her small amount of savings. With this, she was able to help others even with the little she got. She also encouraged her group members to do the same and be good stewards of money, time and skills.

BUTUAN CITY. For trouble-free cooking, Filipino households opt the usage of liquefied petroleum gas (LPG). But when Helenita Servas could not afford to buy LPG, she improvised a local charcoal stove. Together with her husband, they placed electricity-operated blower to the stove and made the entire package convenient, presentable and durable. Her usage of the stove did add savings to her pocket plus extra time to vend snack items. Upon realizing this, she introduced the product to her neighbors. Like she did, they were able earn the benefits of using it. Helenita desired that more and more people would get to use the product, so she acquired financial assistance through KMBI to increase her production. Today, she caters to more locales of Butuan City and other municipalities of Agusan del Norte. With increasing sales, she diversified her product into double-burner charcoal stove for large occasions and charcoal stove with battery-operated blower to cater communities without electricity.

GENERAL SANTOS CITY. Cindy joined KMBI’s team because she was captivated by its vision of seeing transformed lives in Filipino communities. Accepting KMBI’s job offering made her enthusiastic for further developments and adventures in her young life. As program assistant, Cindy began facilitating transformation activities. Today, she gathers 314 program members in ten different trustbanks (or centers) in a week. She oversees their RoadSigns discussions and inputs her learning on business, marketing, finances and spiritual matters to these microentrepreneurs.

Milabelle “Belle” ManingoInitiator of Special Projects

Helenita “Helen” ServasInnovator

Butuan City

Candelaria “Cindy” LopezFacilitator of Transformation

the catalysts >>

PREPARING THE WAY FOR GREATER IMPACT g 1�

In 2006, the organization set seven strategic directions to chart its path for full action leading to greater impact in the next five years. This is through GOAL 25.250: Reaching 250,000

our road map >>

complementary financial products and services in 2008. By that

year also, automation of head office and branch recording system is

realized. This greatly speeds up processes and transactions. On 2011,

preparations for international expansion are commenced.

DIRECTION 4>> Establish bank and transfer sufficient and profitable portfolio from the NGO. In 2006, studies and preparations for banking have been initiated. By

2007, the bank is already established and fully-operational. Towards

the end of 2008, KMBI is starting to transfer sufficient and profitable

portfolio to the bank, ensuring efficient transfer and transition of

personnel from NGO to Bank.

DIRECTION 5>> Train and equip board and staff of both the NGO and the Bank on leadership and management toward technical expertise and social responsibility. Starting 2007, development and implementation

of responsive competency-based training programs for the board

and staff are continued to produce a pool of world class leaders and

trainers for the NGO and the bank.

DIRECTION 6>> Provide opportunities for personal development of board and staff of both the NGO and the bank. Starting 2007, provision of opportunities for

educational advancement is continued. On the same year, additional

benefits packages benchmarked against MF industry standards are

provided for the staff and their families.

DIRECTION 7>> Establish a training institute that will offer consultancy services and courses on microfi-nance, business management, research and rela-ted fields locally and internationally. By 2008, prepara-

tions for the establishment of the training institute is commenced.

By the second semester of 2009, the training institute is already

established.

women microentrepreneurs on its 25th year of service.

DIRECTION 1>> Actively share Christ and promote Christian values. By year 2011, all members of the board,

staff and clients have heard the gospel and given the opportunity

to receive Christ as personal savior towards becoming responsible

and productive citizens. This is through ensuring the presentation

of gospel through the integration of evangelism strategies into

mainstream operations and programs, and promotion of Christian

values by revitalizing and fortifying discipleship programs.

DIRECTION 2>> Deliver demand-driven and sustainable non-financial services for clients. Starting 2007, sustainable non-financial services for clients based

on extensive market research shall be provided, such as enterprise

development, social and environmental awareness programs, and

other capacity building-related services.

DIRECTION 3>> Maintain microfinance operations of the NGO. By the end of 2011, 250,000 clients nationwide

are reached while additional 31 branches are established. The

organization shall open four branches in Metro Manila and four

branches in Central Luzon in 2007, eight branches in Northern Luzon

in 2008, open four branches in Northern Mindanao in 2009, seven

branches in Visayas in 2010, four branches in Western Mindanao in

2011. By 2007, Resource Mobilization & Publication (RM&C) and

Research and Development (R&D) units are fully operationalized.

R&D focuses on market development, market penetration, product

development, and product diversification, while RM&C augments

communication and generation of resources. This operationalization

leads to the development and implementation of relevant

Milabelle “Belle” ManingoInitiator of Special Projects

g KMBI ANNUAL REPORT 2006 14

financials >>

REPORT OF INDEPENDENT AUDITORS

The Board of TrusteesKabalikat Para Sa Maunlad Na Buhay, Inc.(A Non-Stock, Non-Profit Organzation)

We have audited the accompanying financial statements of Kabalikat Para Sa Maunlad Na Buhay, Inc. (a non-stock, non-profit organization), which comprise the statements of assets, liabilities and fund balance as at December 31, 2006 and 2005, and the statements of revenues and expenses, statements of changes in fund balance and statements of cash flows for the years then ended, and a summary of significant accounting policies and other explanatory notes.

Management is responsible for the preparation and fair presentation of these financial statements in accordance with Philippine Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Philippine Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

In our opinion, the financial statements present fairly, in all material respects, the assets, liabilities and fund balance of Kabalikat Para Sa Maunlad Na Buhay, Inc. as of December 31, 2006 and 2005, and its financial performance and its cash flows for the years then ended in accordance with Philippine Financial Reporting Standards.

MANABAT SANAGUSTIN & CO. March 30, 2007EMERITA H. ESCUETA Makati City, Metro ManilaPartner Philippines

Manabat Sanagustin & Co.Certified Public Accountants22/F, Philamlife Tower, 8�6� Paseo de RoxasMakati City 1226, Metro Manila, Philippines

Telephone +6� (2) 885 �000 +6� (2) 8�� 850�Fax +6� (2) 8�4 1�85 +6� (2) 816 65�5Internet www.kpmg.com.phe-Mail [email protected]

PRC-BOA Registration No. 000�SEC Accreditation No. 0004-FR-1BSP Accredited

financials >>

PREPARING THE WAY FOR GREATER IMPACT g 15

financials >>financials >>

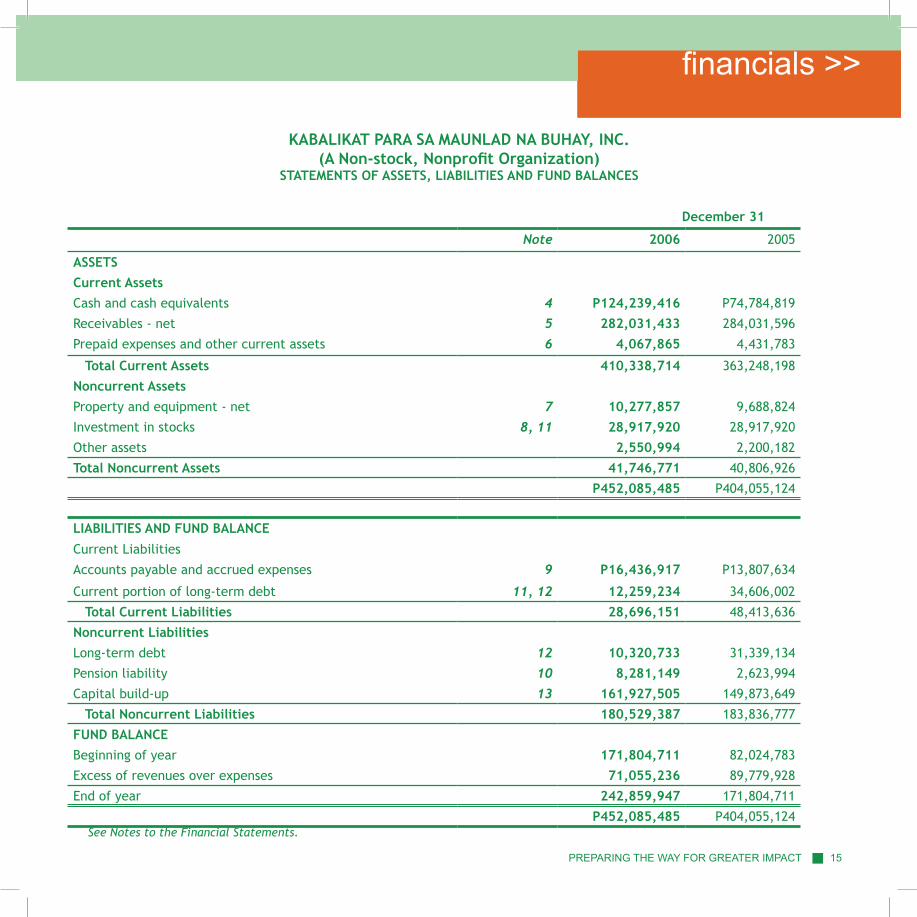

December 31

Note 2006 2005

ASSETSCurrent AssetsCash and cash equivalents 4 P124,239,416 P74,784,819

Receivables - net 5 282,031,433 284,031,596

Prepaid expenses and other current assets 6 4,067,865 4,431,783

Total Current Assets 410,338,714 363,248,198

Noncurrent AssetsProperty and equipment - net 7 10,277,857 9,688,824

Investment in stocks 8, 11 28,917,920 28,917,920

Other assets 2,550,994 2,200,182

Total Noncurrent Assets 41,746,771 40,806,926

P452,085,485 P404,055,124

LIABILITIES AND FUND BALANCE

Current Liabilities

Accounts payable and accrued expenses 9 P16,436,917 P13,807,634

Current portion of long-term debt 11, 12 12,259,234 34,606,002

Total Current Liabilities 28,696,151 48,413,636

Noncurrent LiabilitiesLong-term debt 12 10,320,733 31,339,134

Pension liability 10 8,281,149 2,623,994

Capital build-up 13 161,927,505 149,873,649

Total Noncurrent Liabilities 180,529,387 183,836,777

FUND BALANCEBeginning of year 171,804,711 82,024,783

Excess of revenues over expenses 71,055,236 89,779,928

End of year 242,859,947 171,804,711

P452,085,485 P404,055,124

KABALIKAT PARA SA MAUNLAD NA BUHAY, INC.(A Non-stock, Nonprofit Organization)

STATEMENTS OF ASSETS, LIABILITIES AND FUND BALANCES

See Notes to the Financial Statements.

g KMBI ANNUAL REPORT 2006 16

financials >>

2006 2005

FUND BALANCE

Balance at beginning of year P171,804,711 P82,024,783

Excess of revenues over expenses 71,055,236 89,779,928

P242,859,947 P171,804,711

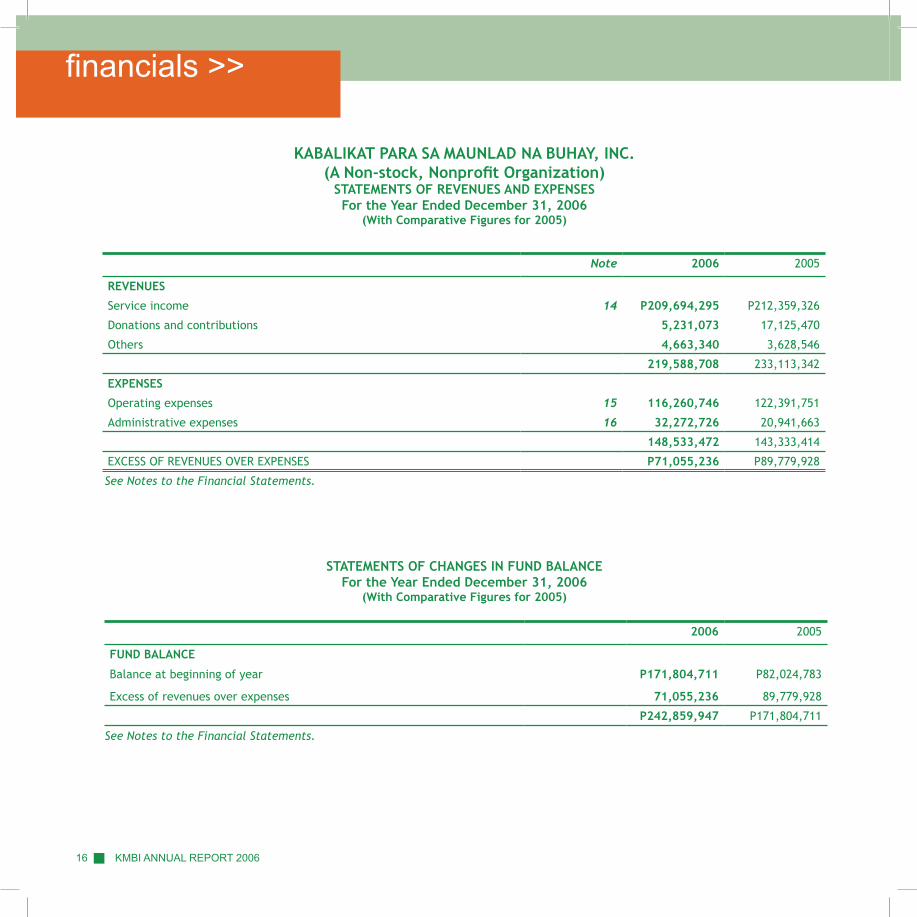

KABALIKAT PARA SA MAUNLAD NA BUHAY, INC.(A Non-stock, Nonprofit Organization)

STATEMENTS OF REVENUES AND EXPENSESFor the Year Ended December 31, 2006

(With Comparative Figures for 2005)

Note 2006 2005

REVENUES

Service income 14 P209,694,295 P212,359,326

Donations and contributions 5,231,073 17,125,470

Others 4,663,340 3,628,546

219,588,708 233,113,342

EXPENSES

Operating expenses 15 116,260,746 122,391,751

Administrative expenses 16 32,272,726 20,941,663

148,533,472 143,333,414

EXCESS OF REVENUES OVER EXPENSES P71,055,236 P89,779,928

See Notes to the Financial Statements.

STATEMENTS OF CHANGES IN FUND BALANCEFor the Year Ended December 31, 2006

(With Comparative Figures for 2005)

See Notes to the Financial Statements.

PREPARING THE WAY FOR GREATER IMPACT g 1�

financials >>

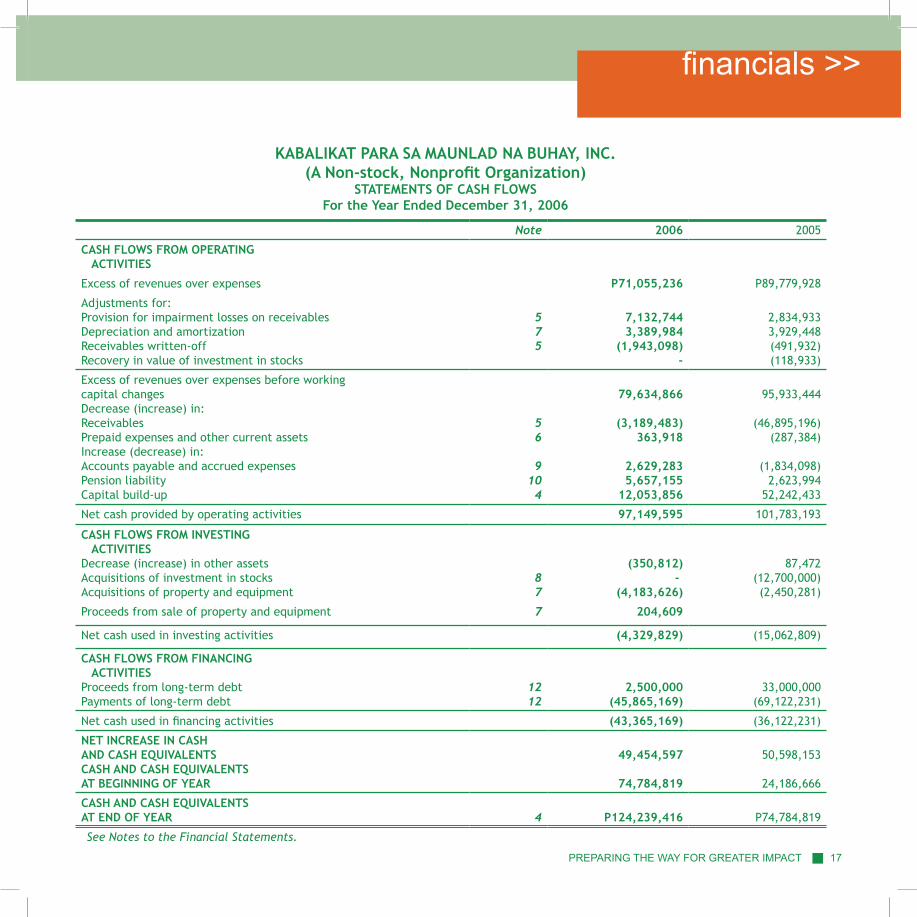

Note 2006 2005

CASH FLOWS FROM OPERATING ACTIVITIES

Excess of revenues over expenses P71,055,236 P89,779,928

Adjustments for:Provision for impairment losses on receivables Depreciation and amortization Receivables written-off Recovery in value of investment in stocks

575

7,132,7443,389,984

(1,943,098) -

2,834,9333,929,448(491,932)(118,933)

Excess of revenues over expenses before working capital changesDecrease (increase) in:Receivables Prepaid expenses and other current assetsIncrease (decrease) in:Accounts payable and accrued expensesPension liabilityCapital build-up

56

9104

79,634,866

(3,189,483)363,918

2,629,2835,657,155

12,053,856

95,933,444

(46,895,196)(287,384)

(1,834,098)2,623,994

52,242,433

Net cash provided by operating activities 97,149,595 101,783,193

CASH FLOWS FROM INVESTING ACTIVITIESDecrease (increase) in other assetsAcquisitions of investment in stocks Acquisitions of property and equipment

87

(350,812) -

(4,183,626)

87,472(12,700,000)(2,450,281)

Proceeds from sale of property and equipment 7 204,609

Net cash used in investing activities (4,329,829) (15,062,809)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from long-term debt Payments of long-term debt

1212

2,500,000(45,865,169)

33,000,000(69,122,231)

Net cash used in financing activities (43,365,169) (36,122,231)

NET INCREASE IN CASH AND CASH EQUIVALENTSCASH AND CASH EQUIVALENTSAT BEGINNING OF YEAR

49,454,597

74,784,819

50,598,153

24,186,666

CASH AND CASH EQUIVALENTS AT END OF YEAR 4 P124,239,416 P74,784,819

KABALIKAT PARA SA MAUNLAD NA BUHAY, INC.(A Non-stock, Nonprofit Organization)

STATEMENTS OF CASH FLOWSFor the Year Ended December 31, 2006

See Notes to the Financial Statements.

g KMBI ANNUAL REPORT 2006 18

financials >>

KABALIKAT PARA SA MAUNLAD NA BUHAY, INC.(A Non-stock, Non-profit Organization)

NOTES TO THE FINANCIAL STATEMENTS

1. Reporting Entity

Kabalikat Para Sa Maunlad Na Buhay, Inc. (“the Organization”) is a non-stock, non- profit organization which was organized on November 4, 1986 with the objective of assisting the low-income Filipinos in their pursuit for education, culture, civic, physical and economic advancement with the end view that they will become responsible members and assets of society. To attain these objectives, the Organization conducts seminars, lectures and trainings by inviting resource persons who have expertise and knowledge in specialized fields and extends financial assistance at reasonable interest rates to economically active poor people.

On March 12, 2003, the Organization was certified by the Philippine Council for NGO Certification as a qualified donee institution in accordance with Revenue Regulations No. 13-98 for a period of three years. Accordingly, it is exempt from payment of income tax on income it received and the filing of income tax return covering such income. Such exemption, however, does not apply to income of whatever kind and character derived from the use of the Organization’s properties, real and personal, or from any of its activities conducted for profit regardless of the dispositions made of such income.

The registered address of the Organization is No. 12 San Francisco Street, Karuhatan, Valenzuela City.

2. Basis of Preparation

Statement of ComplianceThe accompanying financial statements have been prepared in conformity with the accounting principles generally accepted in the Philippines as set forth in Philippine Financial Reporting Standards (PFRS).

The Organization’s financial statements as of December 31, 2006 were authorized for issue by the Board of Trustees’ authorized representative on March 30, 2007.

Basis of MeasurementThe Organization’s financial statements have been prepared on the historical cost basis.

Functional and Presentation CurrencyThe financial statements of the Organization are presented in Philippine peso, which is the Organization’s functional currency.

Use of Judgments and EstimatesThe preparation of the Organization’s financial statements requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses.Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised and in future period affected.

Impairment of assetsIn accordance with the Organization’s policy on impairment of assets, the Organization performs an impairment test when certain

PREPARING THE WAY FOR GREATER IMPACT g 1�

financials >>

impairment indicators are present. In determining the present value of future cash flows expected to be generated from the continued use of the assets, the Organization is required to make estimates and assumptions that can materially affect the financial statements.

Estimated allowance for impairment of receivablesThe Organization maintains allowances for impairment losses at a level considered adequate to provide for potential uncollectible receivables. The level of this allowance is evaluated by management on the basis of factors that affect the collectibility of the accounts. These factors include, but are not limited to, the length of the Organization’s relationship with the client, the client’s payment behavior and known market factors. The Organization reviews the age and status of receivables, and identifies accounts that are to be provided with allowances on a continuous basis.

Estimated useful lives of property and equipmentThe Organization reviews annually the estimated useful lives of property and equipment based on the period over which the assets are expected to be available for use and are updated if expectations differ from previous estimates due to physical wear and tear, technical or commercial obsolescence. It is possible that future results of operations could be materially affected by changes in these estimates brought about by changes in the factors mentioned. A reduction in the estimated useful lives of property and equipment would increase the recorded depreciation expenses and decrease noncurrent assets.

Pension and other employee benefitsThe determination of the obligation and cost of pension and other employee benefits is dependent on the selection of certain assumptions used by the actuary in calculating such amounts. Those assumptions include among others, discount rates, expected returns on plan assets and salary increase rates (see Note 10). In accordance with PFRS actual results that differ from the Organization’s assumptions are accumulated and amortized over future periods and therefore, generally affect the recognized expense and recorded obligation in such future period.

While the Organization believes that the assumptions are reasonable and appropriate, significant differences between actual experience and assumptions may materially affect the cost of employee benefits and related obligations.

3. Summary of Significant Accounting Policies

The accounting policies set-out below have been applied consistently to all periods presented in these financial statements.

Adoption of New Standards, Amendments to Standards and Interpretations The Financial Reporting Standards Council, or FRSC, (the successor body to the Accounting Standards Council) approved the adoption as part of PFRSs a number of new standards, amendments to standards and interpretations issued by the International Financial Reporting Interpretations Committee (IFRIC).

Amendment to Standard and Interpretation Adopted in 2006Effective January 1, 2006, the Organization adopted the following amendment to standard and interpretation:

Amendment to PAS 39, Financial Instruments: Recognition and Measurement – The Fair Value Option limits the fair value option to only those financial instruments that meet certain conditions. The conditions that are required to be met under the amendment are: where such designation eliminates or significantly reduces an accounting mismatch, when a group of financial assets, financial liabilities or both are managed and their performance is evaluated on a fair value basis in accordance with a documented risk management or investment strategy, and when an instrument contains an embedded derivative that meets particular conditions.

IFRIC 4, Determining Whether an Arrangement Contains a Lease provides guidance for determining whether an arrangement,

g KMBI ANNUAL REPORT 2006 20

financials >>

comprising a transaction or a series of related transactions, that does not take the legal form of a lease but conveys a right to use an asset in return for a payment or series of payments, is or contains, a lease that should be accounted for in accordance with PAS 17, Leases.

The adoption of the above amendment to standard and interpretation did not have a material effect on the Organization’s financial statements.

New Standard and Amendment to Standard Not Yet AdoptedThe following are the new standard and amendment to standard which are not yet effective for the year ended December 31, 2006, and have not been applied in preparing these financial statements:

PFRS 7, Financial Instruments: Disclosures requires extensive disclosures about the significance of financial instruments for an entity’s financial position and performance, and quantitative and qualitative disclosures on the nature and extent of risks.

Amendment to PAS 1, Presentation of Financial Statements – Capital Disclosures adds requirements to disclose the entity’s objec-tives, policies and processes for managing capital; quantitative data about what the entity regards as capital; whether the entity has complied with any capital requirements; and if it has not complied, the consequences of such non-compliance.

The Organization has not yet determined the potential effect of the adoption of the above standards and amendment to standard.

Cash and Cash EquivalentsCash includes cash on hand and deposits held at call with banks which earn interest at the respective bank deposit rates. Cash equivalents are short-term highly liquid instruments purchased with the maturity of three (3) months or less from date of acquisition and are subject to an insignificant risk of change in value.

Investment in StocksInvestment in equity securities is initially recognized at transaction price or the fair value of the stocks at acquisition date.

Held for trading equity securities are measured at fair value with gains or losses being recognized in the statements of revenues and expenses. Available for sale equity securities are measured at fair value with gains or losses being recognized as a separate component of equity until the investment is derecognized or until the investment is determined to be impaired at which time the cumulative gain or loss previously reported in equity is included in the statements of revenues and expenses. Stocks for which fair value cannot be reliably measured are recorded at cost.

ReceivablesReceivables are stated at face value, net of allowance for impairment losses maintained at a level considered adequate to provide for potential uncollectible account.

Revenue RecognitionRevenue is recognized when it is probable that the economic benefits associated with the transaction will flow to the Organization and the amount of the revenue can be measured reliably. Revenues from loans and other related fees are recognized based on the accrual method of accounting.

Property and EquipmentProperty and equipment, except for land, are carried at cost less accumulated depreciation, amortization and impairment losses, if

PREPARING THE WAY FOR GREATER IMPACT g 21

financials >>

any. Land is stated at cost less any impairment losses.

Initially, an item of property and equipment is measured at its cost, which comprises its purchase price and any directly attributable costs of bringing the asset to the location and condition for its intended use. Subsequent costs that can be measured reliably are added to the carrying amount of the asset when it is probable that future economic benefits associated with the asset will flow to the Organization. The costs of day-to-day servicing of an asset are recognized as an expense in the period in which they are incurred.

Depreciation is computed using the straight-line method over the estimated useful lives of the assets. Leasehold improvements are amor-tized over the estimated useful life of the improvements or the term of the lease, whichever is shorter. The estimated useful lives are as follows:

The useful lives and depreciation and amortization method are reviewed at each balance sheet date to ensure that the period and method of depreciation and amortization are consistent with the expected pattern of economic benefits from those assets.

When an asset is disposed of, or is permanently withdrawn from use and no future economic benefits are expected from its disposal, the cost and accumulated depreciation, amortization and impairment losses, if any, are removed from the accounts and any resulting gain or loss arising from the retirement or disposal is recognized in the statements of revenues and expenses.

Impairment of AssetsFinancial AssetsA financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.

An impairment loss in respect of a financial asset measured at amortized cost is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate.

Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed col-lectively in groups that share similar credit risk characteristics.

Impairment losses are recognized in the statements of revenues and expenses.

Non-Financial AssetsNon-financial assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. If any such indication exists and where the carrying amount of an asset exceeds its recoverable amount, the asset or cash-generating unit is written down to its recoverable amount. The estimated recoverable amount is the higher of an asset’s net selling price and value in use. The net selling price is the amount obtainable from the sale of an asset in an arm’s length transaction less the costs of disposal while value in use is the present value of estimated future cash flows expected to arise from the continuing use of an asset and from its disposal at the end of its useful life. In assessing value in use, the estimated future cash flows are discounted to

Number of Years

Building and improvements 40

Leasehold improvements 3

Furniture and equipment 3

Transportation equipment 5

g KMBI ANNUAL REPORT 2006 22

financials >>

their present value using a pre-tax discount rate that reflects current market assessments of time value of money and the risks spe-cific to the asset. For an asset that does not generate largely independent cash inflows, the recoverable amount is determined for the cash-generating unit to which the asset belongs. Impairment losses are recognized in the statements of revenues and expenses.

Recovery of impairment losses recognized in prior years is recorded when there is an indication that the impairment losses recog-nized for the asset no longer exist or have decreased. The recovery is recorded in the statements of operations. However, the in-crease in carrying amount of an asset due to a recovery of an impairment loss is recognized to the extent that it does not exceed the carrying amount that would have been determined (net of depreciation and amortization) had no impairment loss been recognized for that asset in prior years.

Operating Leases Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating lease. Payments made under operating leases are recognized in the statements of revenues and expenses on a straight-line basis over the term of the lease.

Foreign Currency TransactionsForeign currency transactions are recorded in Philippine peso based on the exchange rates prevailing at the transaction dates. Mon-etary assets and liabilities denominated in foreign currencies are translated to their Philippine peso values using the exchange rates prevailing at the balance sheet date. Translation gains or losses are recognized in the statements of revenues and expenses. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates at dates of initial transactions.

Related PartiesParties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise signifi-cant influence over the other party in making financial and operating decisions. Parties are also considered to be related if they are subject to common control or common significant influence. Related parties may be individuals or corporate entities. Transactions between related parties are based on terms similar to those offered to non-related parties.

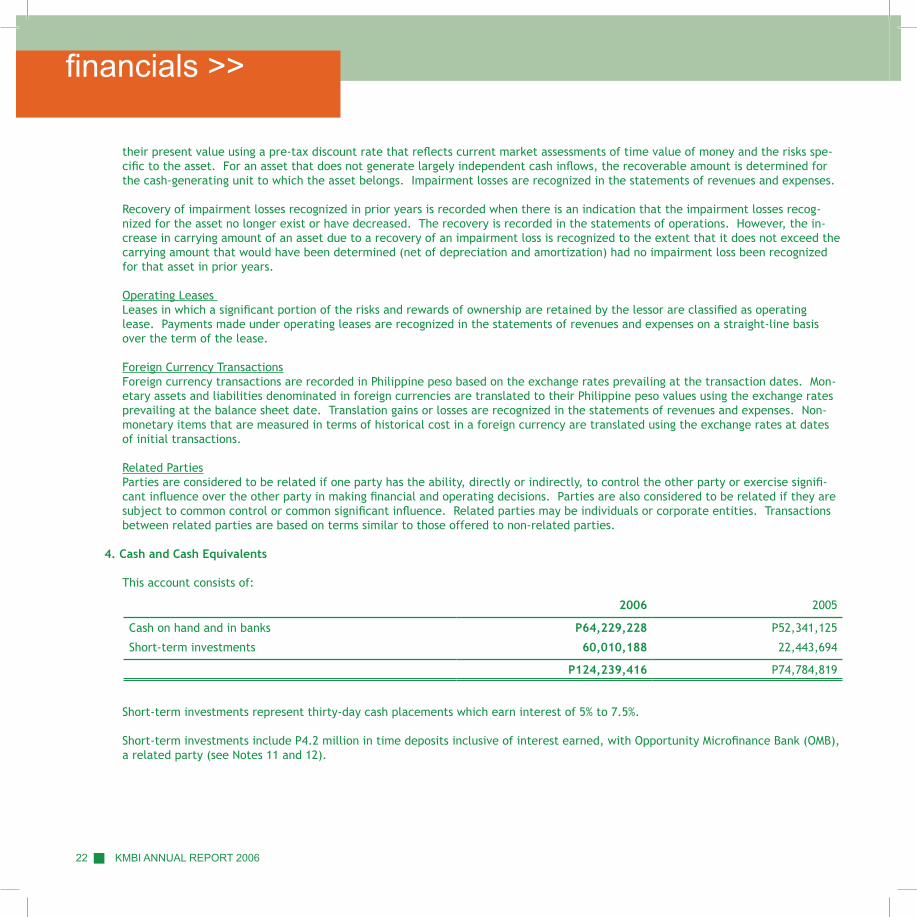

4. Cash and Cash Equivalents

This account consists of:

Short-term investments represent thirty-day cash placements which earn interest of 5% to 7.5%.

Short-term investments include P4.2 million in time deposits inclusive of interest earned, with Opportunity Microfinance Bank (OMB), a related party (see Notes 11 and 12).

2006 2005

Cash on hand and in banks P64,229,228 P52,341,125

Short-term investments 60,010,188 22,443,694

P124,239,416 P74,784,819

PREPARING THE WAY FOR GREATER IMPACT g 2�

financials >>

5. Receivables

This account consists of:

Certain loans receivable are used as collateral for the Organization’s long-term debt (see Note 12).

6. Prepaid Expenses and Other Current Assets

This account consists of:

2006 2005

Loans receivable P278,064,840 P271,753,760

Other receivable 8,475,310 10,119,505

Interest receivable 3,275,448 4,752,850

289,815,598 286,626,115

Less allowance for impairment losses 7,784,165 2,594,519

P282,031,433 P284,031,596

2006 2005

Unused office suppliesPrepaid expenses

P2,949,8511,118,014

P3,258,0791,173,704

P4,067,865 P4,431,783

g KMBI ANNUAL REPORT 2006 24

financials >>

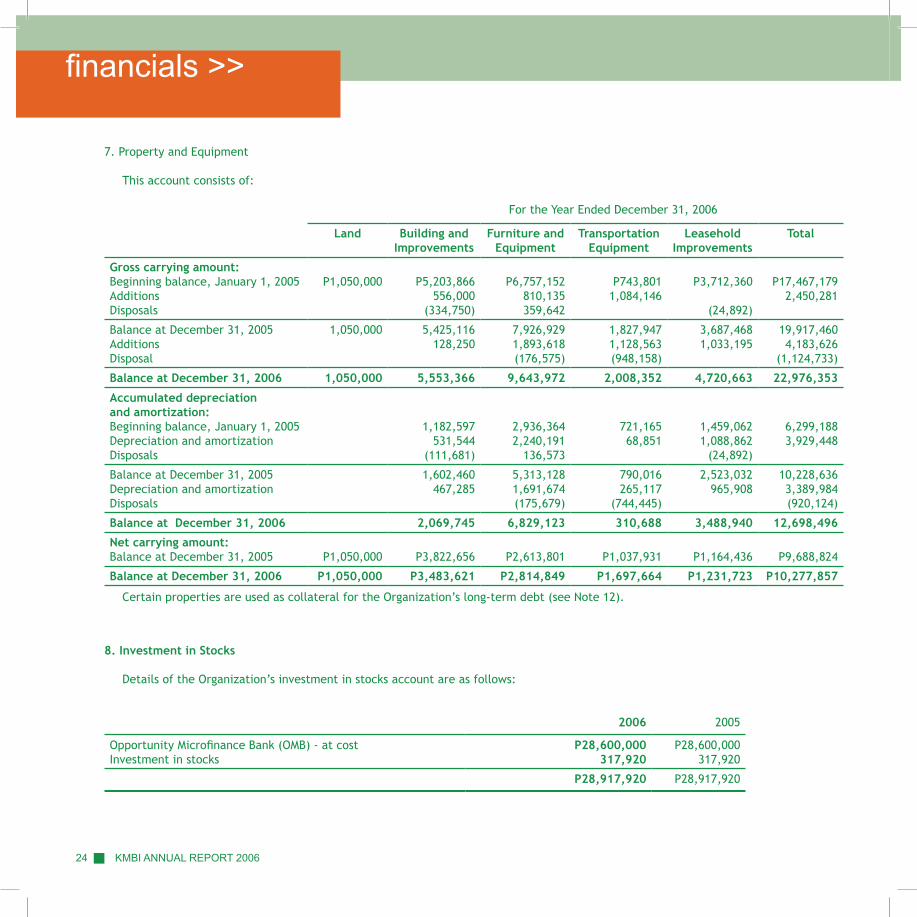

7. Property and Equipment

This account consists of:

Certain properties are used as collateral for the Organization’s long-term debt (see Note 12).

Land Building and Improvements

Furniture and Equipment

Transportation Equipment

Leasehold Improvements

Total

Gross carrying amount:Beginning balance, January 1, 2005AdditionsDisposals

P1,050,000 P5,203,866556,000

(334,750)

P6,757,152810,135359,642

P743,8011,084,146

P3,712,360

(24,892)

P17,467,1792,450,281

Balance at December 31, 2005AdditionsDisposal

1,050,000 5,425,116128,250

7,926,9291,893,618(176,575)

1,827,9471,128,563(948,158)

3,687,4681,033,195

19,917,4604,183,626

(1,124,733)

Balance at December 31, 2006 1,050,000 5,553,366 9,643,972 2,008,352 4,720,663 22,976,353

Accumulated depreciationand amortization:Beginning balance, January 1, 2005Depreciation and amortizationDisposals

1,182,597531,544

(111,681)

2,936,3642,240,191

136,573

721,16568,851

1,459,0621,088,862

(24,892)

6,299,1883,929,448

Balance at December 31, 2005Depreciation and amortizationDisposals

1,602,460467,285

5,313,1281,691,674(175,679)

790,016265,117

(744,445)

2,523,032965,908

10,228,6363,389,984(920,124)

Balance at December 31, 2006 2,069,745 6,829,123 310,688 3,488,940 12,698,496

Net carrying amount:Balance at December 31, 2005 P1,050,000 P3,822,656 P2,613,801 P1,037,931 P1,164,436 P9,688,824

Balance at December 31, 2006 P1,050,000 P3,483,621 P2,814,849 P1,697,664 P1,231,723 P10,277,857

8. Investment in Stocks

Details of the Organization’s investment in stocks account are as follows:

For the Year Ended December 31, 2006

2006 2005

Opportunity Microfinance Bank (OMB) - at costInvestment in stocks

P28,600,000317,920

P28,600,000317,920

P28,917,920 P28,917,920

PREPARING THE WAY FOR GREATER IMPACT g 25

financials >>

Land Building and Improvements

Furniture and Equipment

Transportation Equipment

Leasehold Improvements

Total

Gross carrying amount:Beginning balance, January 1, 2005AdditionsDisposals

P1,050,000 P5,203,866556,000

(334,750)

P6,757,152810,135359,642

P743,8011,084,146

P3,712,360

(24,892)

P17,467,1792,450,281

Balance at December 31, 2005AdditionsDisposal

1,050,000 5,425,116128,250

7,926,9291,893,618(176,575)

1,827,9471,128,563(948,158)

3,687,4681,033,195

19,917,4604,183,626

(1,124,733)

Balance at December 31, 2006 1,050,000 5,553,366 9,643,972 2,008,352 4,720,663 22,976,353

Accumulated depreciationand amortization:Beginning balance, January 1, 2005Depreciation and amortizationDisposals

1,182,597531,544

(111,681)

2,936,3642,240,191

136,573

721,16568,851

1,459,0621,088,862

(24,892)

6,299,1883,929,448

Balance at December 31, 2005Depreciation and amortizationDisposals

1,602,460467,285

5,313,1281,691,674(175,679)

790,016265,117

(744,445)

2,523,032965,908

10,228,6363,389,984(920,124)

Balance at December 31, 2006 2,069,745 6,829,123 310,688 3,488,940 12,698,496

Net carrying amount:Balance at December 31, 2005 P1,050,000 P3,822,656 P2,613,801 P1,037,931 P1,164,436 P9,688,824

Balance at December 31, 2006 P1,050,000 P3,483,621 P2,814,849 P1,697,664 P1,231,723 P10,277,857

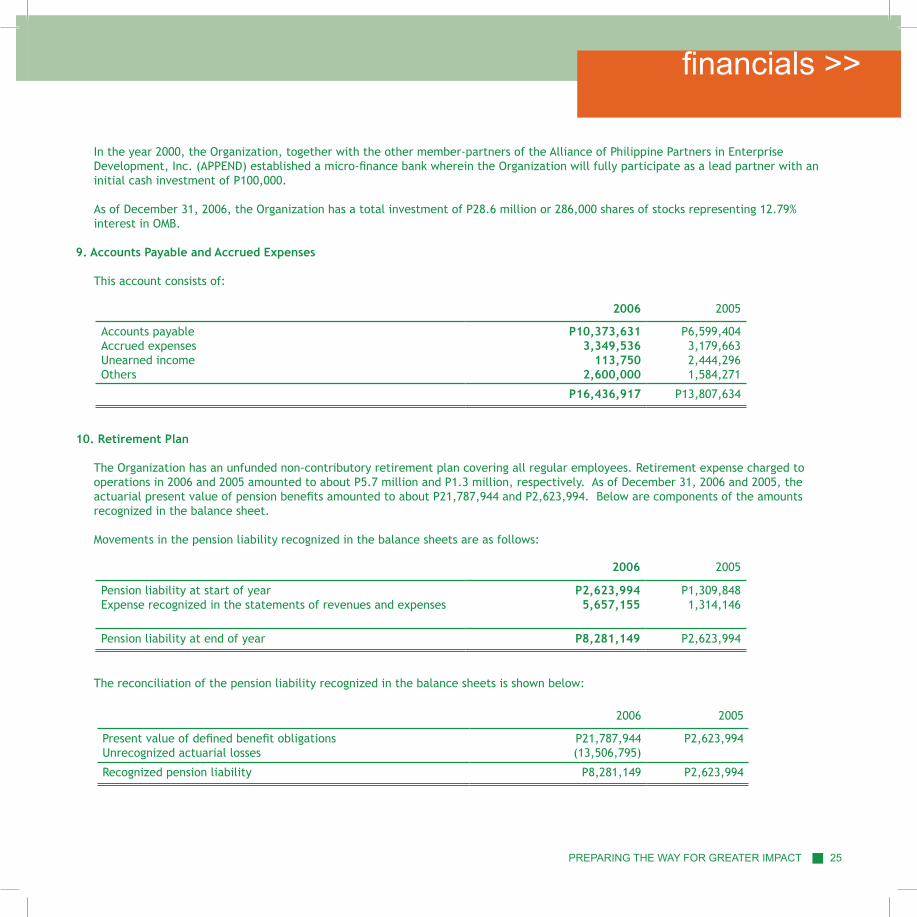

In the year 2000, the Organization, together with the other member-partners of the Alliance of Philippine Partners in Enterprise Development, Inc. (APPEND) established a micro-finance bank wherein the Organization will fully participate as a lead partner with an initial cash investment of P100,000.

As of December 31, 2006, the Organization has a total investment of P28.6 million or 286,000 shares of stocks representing 12.79% interest in OMB.

9. Accounts Payable and Accrued Expenses

This account consists of:

10. Retirement Plan

The Organization has an unfunded non-contributory retirement plan covering all regular employees. Retirement expense charged to operations in 2006 and 2005 amounted to about P5.7 million and P1.3 million, respectively. As of December 31, 2006 and 2005, the actuarial present value of pension benefits amounted to about P21,787,944 and P2,623,994. Below are components of the amounts recognized in the balance sheet.

Movements in the pension liability recognized in the balance sheets are as follows:

The reconciliation of the pension liability recognized in the balance sheets is shown below:

For the Year Ended December 31, 2006

2006 2005

Accounts payableAccrued expensesUnearned incomeOthers

P10,373,6313,349,536

113,7502,600,000

P6,599,4043,179,6632,444,2961,584,271

P16,436,917 P13,807,634

2006 2005

Pension liability at start of yearExpense recognized in the statements of revenues and expenses

P2,623,9945,657,155

P1,309,8481,314,146

Pension liability at end of year P8,281,149 P2,623,994

2006 2005

Present value of defined benefit obligationsUnrecognized actuarial losses

P21,787,944(13,506,795)

P2,623,994

Recognized pension liability P8,281,149 P2,623,994

g KMBI ANNUAL REPORT 2006 26

financials >>

The amounts recognized in the statements of revenues and expenses are as follows:

Principal actuarial assumptions at the balance sheet date (expressed as weighted averages):

11. Related Parties

a. Significant transactions with OMB during 2006 and 2005 are as follows:

As of December 31, 2006 and 2005, the outstanding balances of accounts with OMB are as follows:

b. The key management personnel compensations representing short-term employee benefits amount to about P8.2 million in 2006, and P6.1 million in 2005.

c. Total remuneration of key management personnel included in “Salaries and Wages” amount to about P1.2 million in 2006 and P1.3 million in 2005.

12. Long-Term Debt

Loans from Oikocredit Foundation Philippines, Inc. In a meeting held on April 1, 2002, the Board of Trustees approved the availment of a P33 million loan from Oikocredit Foundation

Note 2006 2005

Short-term investments Subscription of additional shares of stock Loan availment Others (rentals & utilities)

4

812

P4,000,000 P4,000,000

12,700,0005,500,000

744,000

Note 2006 2005

Short-term investments Loan payable

412

P4,409,967 P4,192,721P5,500,000

2006 2005

Interest costCurrent service costTransitional liability recognized during the year

P5,289,796367,359

P262,101489,744562,301

Retirement expense P5,657,155 P1,314,146

2006 2005

Discount rateExpected rate of return on plan assetsFuture salary increases

8% p.a8% p.a

10% p.a

14% p.a.8% p.a.

10% p.a.

PREPARING THE WAY FOR GREATER IMPACT g 2�

financials >>

Philippines, Inc., (Oikocredit) payable in three (3) years at 10.67% interest per annum on the first year; succeeding annual interest rate shall be the average interest rate paid on the 91-day Philippine Treasury Bills for all issues during the 6 months period preceding Oikocredit’s review plus five percent (5%) provided that the interest rate for the loan shall at no point be lower than 10%. The loan was used to fund the expansion projects of the Organization.

The loan is secured by the following:

a. a first mortgage on real estate property of the Organization located in Karuhatan, Valenzuela with an area of three (300) square meters and improvements thereon;

b. a first mortgage on the shares of capital stock of OMB, a partner, equivalent to 158,999 total shares with a par value of P100 each;

c. assignment of loan portfolio and related securities which, at all times, shall have a face value of at least P9 million;

d. a promissory note in form and substance acceptable to the lender.

On June 23, 2004, another loan was availed from Oikocredit Foundation Philippines, Inc. amounting to P55 million. The interest for the loan during the first year is 12.16% while the succeeding interest will be calculated based on the treasury bills rate. The loan is payable semi-monthly over a period of three years.

The loan is secured by the securities enumerated above, as well as the following:

a.Continuing deed of assignment of loan portfolio and related securities equivalent to 120% of the outstanding loan balance; and

b.Promissory note in form and in substance acceptable to the lender.

As of December 31, 2006, the initial loan amounting to P33 million has been fully paid.

Loan from People’s Credit and Finance Corporation (PCFC)As of December 31, 2005, the Organization has an outstanding loan from PCFC amounting to P15 million which was pre-terminated on August 8, 2006.

In February 2006, the Organization obtained an institutional loan from PCFC amounting to P2.5 million which bears 3% annual interest and is payable quarterly until February 14, 2008. Proceeds of the loan shall be used for granting of sub-loans to micro finance-enterprise or livelihood projects of qualified sub-borrowers. As of December 31, 2006, the outstanding balance of the loan amounted to P1.6 million.

The loan is secured by the post-dated checks issued by the Organization on behalf of PCFC. Loan from Taytay sa Kauswagan, Inc. (TSKI)On May 1, 2004, the Organization obtained a loan facility from TSKI amounting to P11 million of which P10 million was already received as of December 31, 2004. The interest rate is at 10% for the first two (2) years, 11% for the third year and 12% for the fourth and fifth years. The agreement requires the Organization to open a microfinance branch in Parañaque in behalf of TSKI, named Kabalikat sa Kaunlaran Project.

Loan from OMBOn February 28, 2005, the Organization obtained a loan from OMB amounting to P5.5 million at 9% interest per annum for a period of

g KMBI ANNUAL REPORT 2006 28

financials >>

one year, payable in four (4) equal quarterly payments. The loan is secured by the Organization’s short-term time deposit with OMB amounting to about P4.2 million as of December 31, 2006. On February 28, 2006, the loan from OMB was fully paid.

Details of the outstanding long-term debts follow:

13. Capital Build-Up

This represents initial membership contribution of P200 and the mandatory weekly capital build - up amounting to P40 per client that earn interest at the current bank rate on savings deposit plus 1% per annum. Capital build-up will be returned to clients when they leave the program.

14. Service Income

Service income consists of loan fees, interest on loans, membership and processing fee from clients.

15. Operating Expenses

This account consists of:

2006 2005

Salaries and wagesEmployee benefits and allowancesFinancing costRent Transportation and travelImpairment losses on receivablesCommunication, light and waterSSS, Medicare, ECC and HDMF contributionMeetings, trainings and conferences

P44,988,39520,308,4398,736,4787,682,5287,429,6137,132,7444,723,8283,720,2443,037,011

P45,443,92222,939,91814,366,6917,088,6977,505,7482,834,9335,057,1773,477,9654,381,131

Forward

2006 2005

Oiko Foundation Philippines, Inc.Taytay sa Kauswagan, Inc.People’s Credit and Finance CorporationOpportunity Microfinance Bank

P11,000,00010,000,0001,579,967

P35,750,00010,000,00014,695,1365,500,000

Less current portion of long-term debt 22,579,96712,259,234

65,945,13634,606,002

P10,320,733 P31,339,134

PREPARING THE WAY FOR GREATER IMPACT g 2�

financials >>

2006 2005

Meetings, trainings and conferencesSalaries and wagesRetirement expense Employee benefits and allowances Transportation and travelCommunication, light and waterDepreciation and amortization SuppliesNon MED expenseMembership duesRepresentation and entertainmentDonations and contributionsSSS, Medicare, ECC and HDMF contributionsSecurity servicesGasoline and oilInsuranceAdvertisement and promotionLegal, audit and other professional feesRepairs and maintenanceTaxes and licensesPrintingMiscellaneous

P6,194,5126,055,1255,657,1553,333,0192,811,5411,973,4211,515,259

822,657639,399563,745518,133448,823342,730150,000139,40295,42494,10684,31771,30062,2771,237

699,143

P2,361,8675,104,2961,314,1463,012,2752,246,2221,933,7001,182,097

613,2931,069,857

- 330,15946,251

279,256151,778132,54572,907

133,26056,821

106,38858,06334,168

702,314

P32,272,726 P20,941,663

2006 2005

SuppliesPrintingDepreciation and amortization InsuranceTaxes and licensesLegal, audit and other professional feesRepairs and maintenanceSecurity servicesDonations and contributionsAds & Promotions ExpenseMembership duesRepresentation and entertainmentMiscellaneous

2,768,6711,913,4361,874,725

638,047403,897123,555

P241,22776,24237,0519,8613,0002,912

408,841

2,184,4072,191,4742,747,351

942,547187,288305,890

P263,67152,51220,3388,988

- 1,193

389,910

P116,260,746 P122,391,751

16. Administrative Expenses

This account consists of:

g KMBI ANNUAL REPORT 2006 �0

financials >>

17. Lease Commitments

The Organization leases office spaces for its 24 branches in Luzon and Mindanao for a period of two to three years, with options to renew the lease. Rent expense in 2006 and 2005 amounted to P7,706,053 and P7,088,697, respectively.

The future minimum lease payments under the above lease contracts are as follows:

18. Financial Instruments

Financial Risk Management Objectives and PoliciesThe Organization’s financial instruments consist of cash and cash equivalents, investments, loans receivable and bank loans. The main risk arising from the use of these financial instruments are interest rate risk, credit risk and liquidity risk.

Interest Rate RiskThe Organization’s exposure to the risk for changes in market rate relates primarily to its long-term debt obligations with variable interest rates. However, most of the Organization’s existing debt obligations are based on fixed interest rates with relatively small component of the debts that are subject to interest rate fluctuation.

Credit RiskCredit risk represents the loss that the Organization would incur if counterparty failed to perform under its contractual obligations. The Organization has established controls and procedures in its credit policy to determine and monitor the credit worthiness of cus-tomers and counterparties.

Liquidity RiskThe Organization manages liquidity risk by maintaining a balance between continuity of funding and flexibility. Treasury controls and procedures are in place to ensure the sufficient cash is maintained to cover daily operational and working capital requirements. Management closely monitors the Organization’s future and contingent obligations and sets up required cash services as necessary in accordance with internal policies.

2006 2005

Less than one yearBetween one and five years

P2,078,209 P3,549,5022,078,209

P2,078,209 P5,627,711

PREPARING THE WAY FOR GREATER IMPACT g �1

Kabalikat Para sa Maunlad na Buhay, Inc., now with 29 branches

and expanding, planted its first seeds in Valenzuela, Metro Manila.

Starting out as a small, church-based credit program, it opened

a six-square-meter choir room to poor neighbors. Its vision

was to see them live in abundance with strengthened faith in

God. Even with only one worker, 37 neighbors were assisted into

microentrepreneurship through loans amounting to Php 145,000.

Twenty of them were trained on cash management. Now the vision

cuts through geographical barriers, sowing the same seeds to as far

as Southern Mindanao.

Climbing up

Retracing its steps, we find KMBI hurdling through challenges of

growth and fortification from 1986 to 1997. With guidance and

wisdom from God, through the leadership of the Board of Trustees,

it grew to become a full-scale microfinance organization. From

Valenzuela, it expanded its borders to Bulacan, Caloocan and

Quezon City, catering to more poor families than before. Constant

reengineering and strategic planning lead the organization to

embrace the “branch scale-up” model. With this effective and

efficient system, a significant number of clients were reached.

However, its vigor didn’t stop there.

From 1998 to 2000 KMBI’s scaling up was witnessed as it treaded

higher grounds towards further expansion and strengthening. It

started to apply the daily branch reporting and monitoring system

based on SEEP and CGAP standards, conceptualize and implement

a tool for transformation which is the Road Signs book series, open

new branches in General Santos and Marbel, and sign a Memorandum

of Agreement to establish the Opportunity Microfinance Bank (OMB).

Strengthening its stride

2001 to 2004 were the years when KMBI needed to strengthen its

stride. Among the courses that it took during these years were the

following:

* creation of a research and development / publication department

* decentralization of the training department and centralization of

the finance, administrative and human resource departments

* putting up of 17 branches in Bicol, Quezon, Batangas, Laguna,

Cavite, Metro Manila, and Southern Mindanao areas

* reconfiguration of existing Southern Mindanao branches

* standardization of MF operations

* provision of national and international exposures and trainings for

staff

* recognition from both national and international networks.

It was also in 2004 that Opportunity International Network

hailed KMBI as the number one microfinance practitioner among

international partners in the large-scale category, as well as the top

advocate for gender excellence.

history >>

With guidance

and wisdom

from God, through

the leadership of the Board of Trustees, it grew to become a full-scale

microfinance organization.

With guidance

and wisdom

from God, through

the leadership of the Board of Trustees, it grew to become a full-scale

microfinance organization.

g KMBI ANNUAL REPORT 2006 �2

Dr. Amelia L. Gonzales Chairman & President

Emmanuel M. de Guzman Vice Chairman & Vice President

Atty. Servillano C. Mendoza Trustee & Corporate Secretary

Aurelio C. Llenado, Jr. Trustee & Corporate Treasurer

Damiana D. Exiomo Trustee

Eduardo C. Jimenez Trustee

Dr. Ricardo B. Jumawan Trustee

the board of trustees >>

PREPARING THE WAY FOR GREATER IMPACT g ��

the management >>

Edgardo S. MercedesExecutive Director

Liza D. EcoDeputy Director - SSG

Annalie D. ConcepcionAdministration Manager

Rizaldy R. DuqueRes. Mob. & Communications Manager

Vencent A. AbrahamOperations Manager (Mindanao)

Carmela N. PorrasOperations Manager (Luzon)

Arthur N. Gonzaga Training Manager & OIC - HRD

Sancho A. Montaos IIFinance & Accounting Manager

Selven A. RaguroResearch & Development Manager

Hazel Christine Z. RosaciaEnterprise Development Services Head

Charis Ken C. Layawan Transformation Coordinator

Madelyn P. FrijillanoSenior Auditor

g KMBI ANNUAL REPORT 2006 �4

“We are beginning a new and promising

journey heading to the realization of

Goal 25.250... Join me in this journey!”

Edgardo S. MercedesExecutive Director

g KMBI ANNUAL REPORT 2006 �4

g KMBI ANNUAL REPORT 2006 34