2007 namm global report music usa

TRANSCRIPT

�

2007 NAMM GLOBAL REPORTMUSIC USAA STATISTICAL REVIEW

OF THE MUSIC PRODUCTS INDUSTRY

�

2007 NAMM GLOBAL REPORTMUSIC USAA STATISTICAL REVIEW

OF THE MUSIC PRODUCTS INDUSTRY

�

A MessAge froM the ChAirMAn & President/Ceo

The state of the music products industry continues to change rapidly, and making good business decisions in today’s turbulent environment depends on having the latest information. The 2007 NAMM Global Report, Featuring Music USA provides N�MM Members with the most current statistics of various market segments and countries, as well as commentary from leaders of the global music products market.

This edition presents a stronger focus on our global portion of the report than in previous years, as our international section has grown. We now feature 1� countries, adding Norway and Switzerland to the fold.

This year we see industry trends changing: the continued emergence of China and India, slowing sales in the United States and mixed results in most categories across all countries. Electric and acoustic guitars, which have been one of the main driving forces globally in recent years, only showed increased sales in about half of the regions surveyed. Piano purchases were slow in almost all markets, whereas digital piano sales showed upward movement in several countries. One successful segment is the stringed instrument category, which enjoyed increased sales in nearly every market. �ll in all, �006 was a year of changing times and varied markets across most regions.

N�MM has compiled this information from many sources in an effort to support you in your business. So whether you’re using this report to shed light on your local market or to plan a multinational product launch, we hope that this information will help you identify trends and directions that can assist you in making good decisions for your business.

We hope you will take advantage of this valuable information to help position your business for success, overcome today’s challenges and seek out the opportunities offered by change.

Sincerely,

dennis houlihan, Chairman Joe Lamond, President/CEO

�

MANAGING EDITORKen Wilson

INTERNATIONAL AFFAIRSBetty Heywood

RESEARCH ANALYSTErin Block

LAYOUT/DESIGNMegan Nelson

COPY EDITORLaurie Gibson

Contents

2 Message from the Chairman & President/CEO 4 Understanding the U.S. Data 5 U.S. Industry Revenue at a Glance 7 Introduction the U.s. segment data

9 The Fretted Instrument Market 12 The Organ Market 13 The Piano Market 15 The School Music Market 17 The �udio Products Market 20 The Signal Processing Market 22 The Percussion Market 25 The DJ Market 27 The Electronic Music Market 31 The Printed Music Market 31 The Portable Keyboard Market 33 The Karaoke Market 34 The �ccessory Market

Music and sound U.s. industry summary & imports and exports

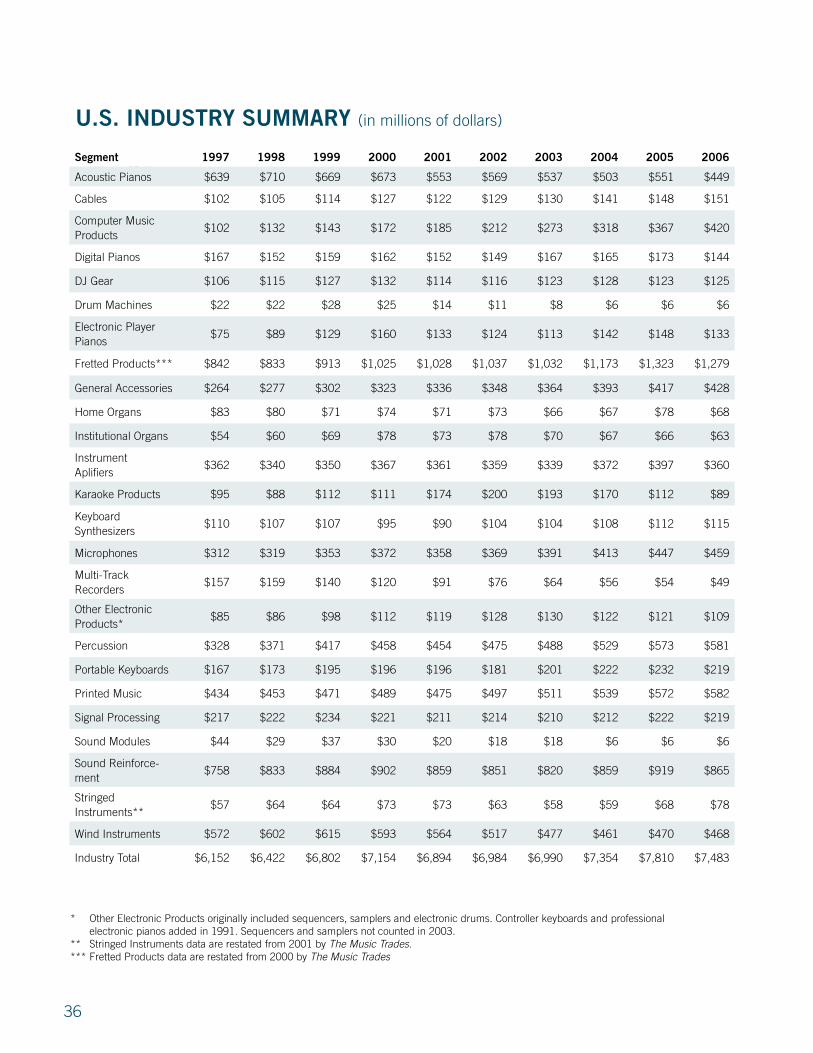

36 U.S. Industry Summary 42 U.S. Imports and Exports of Music and Sound Products

the nAMM global report

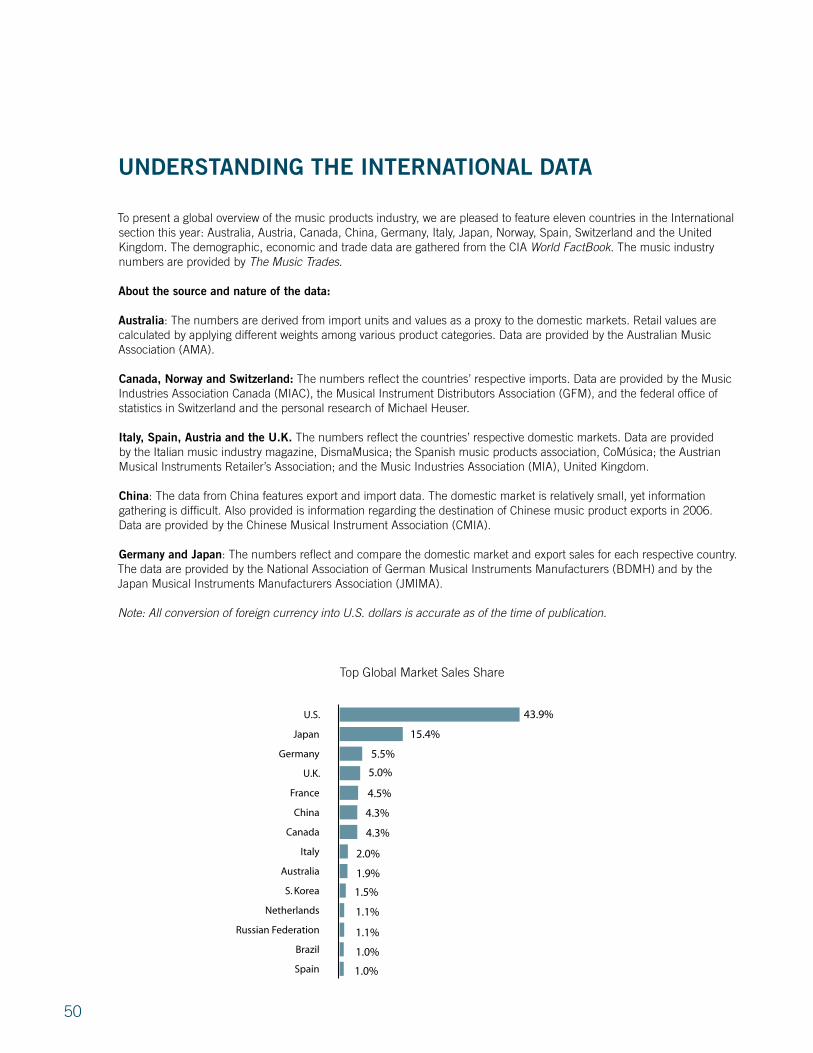

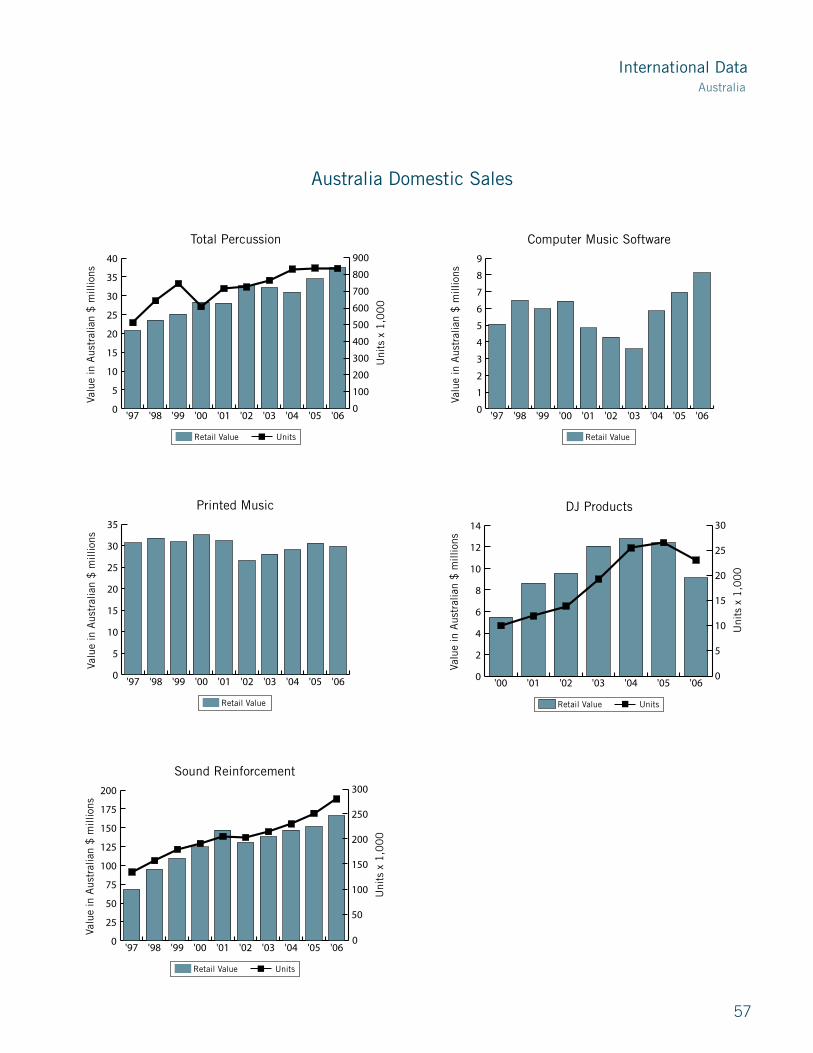

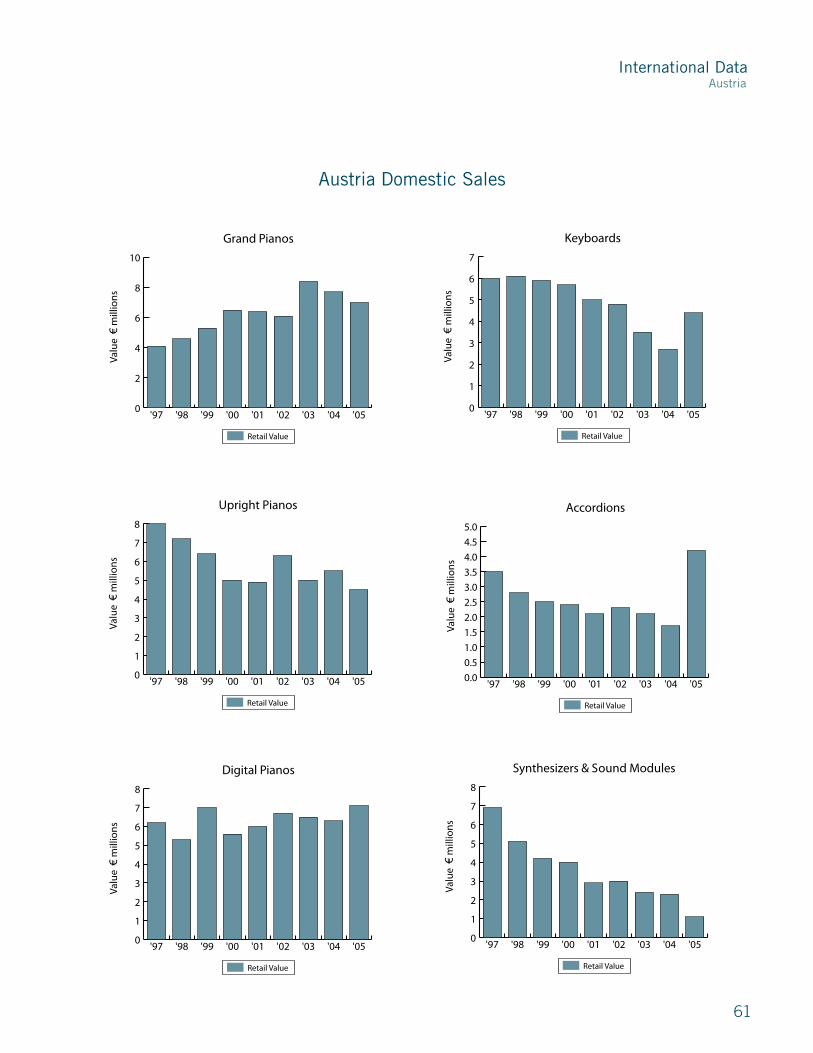

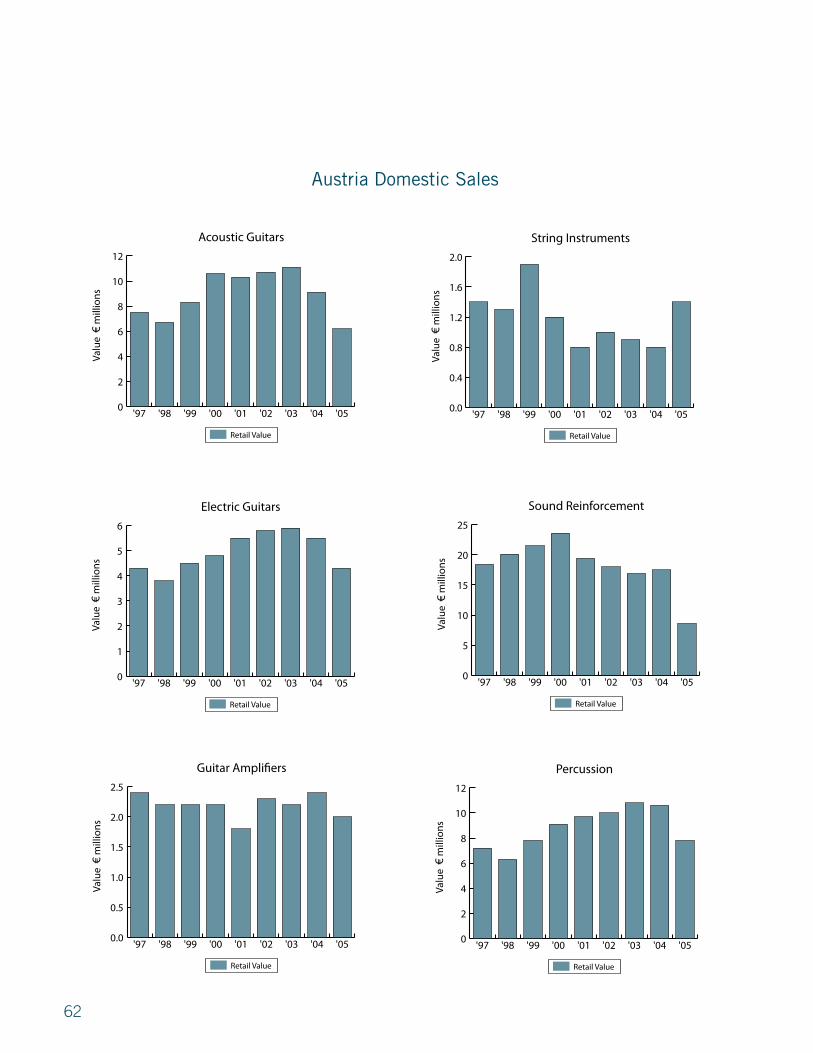

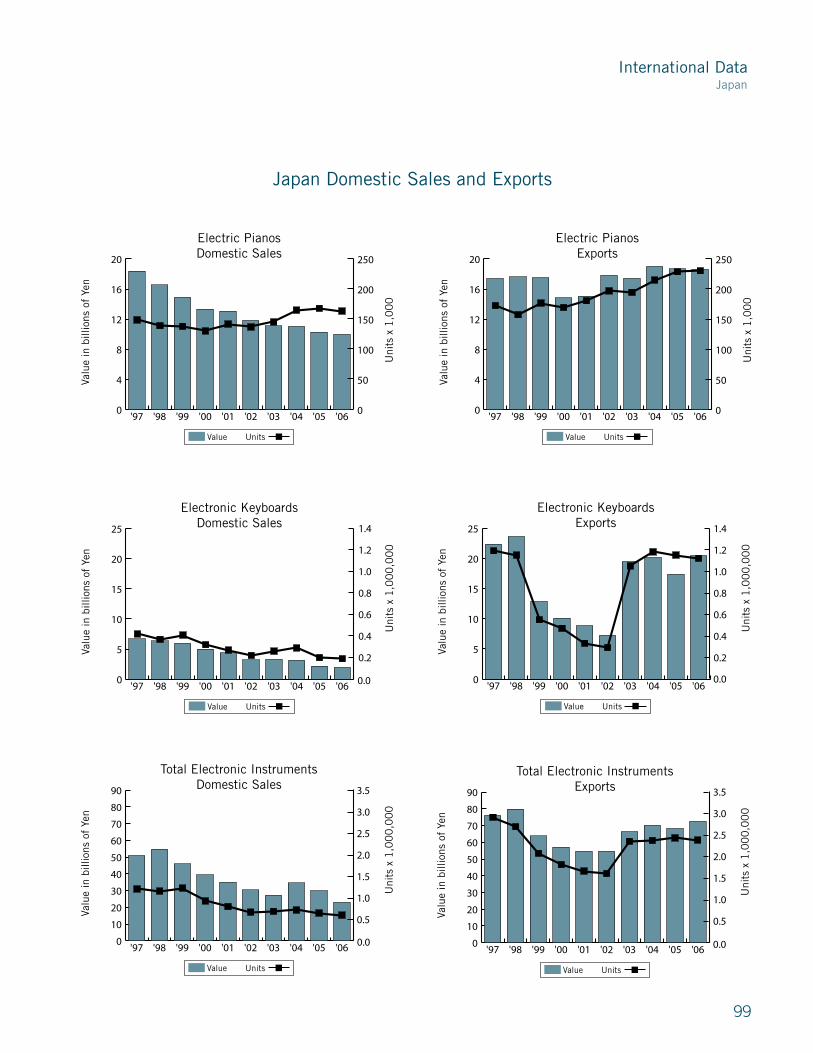

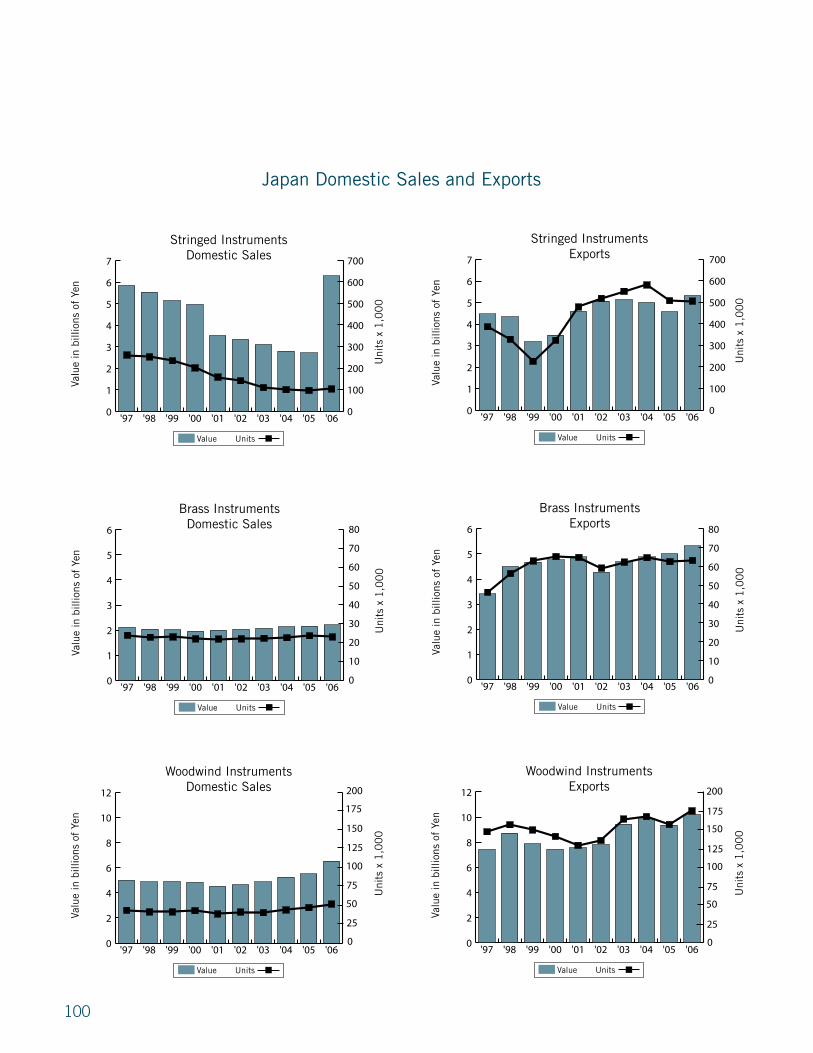

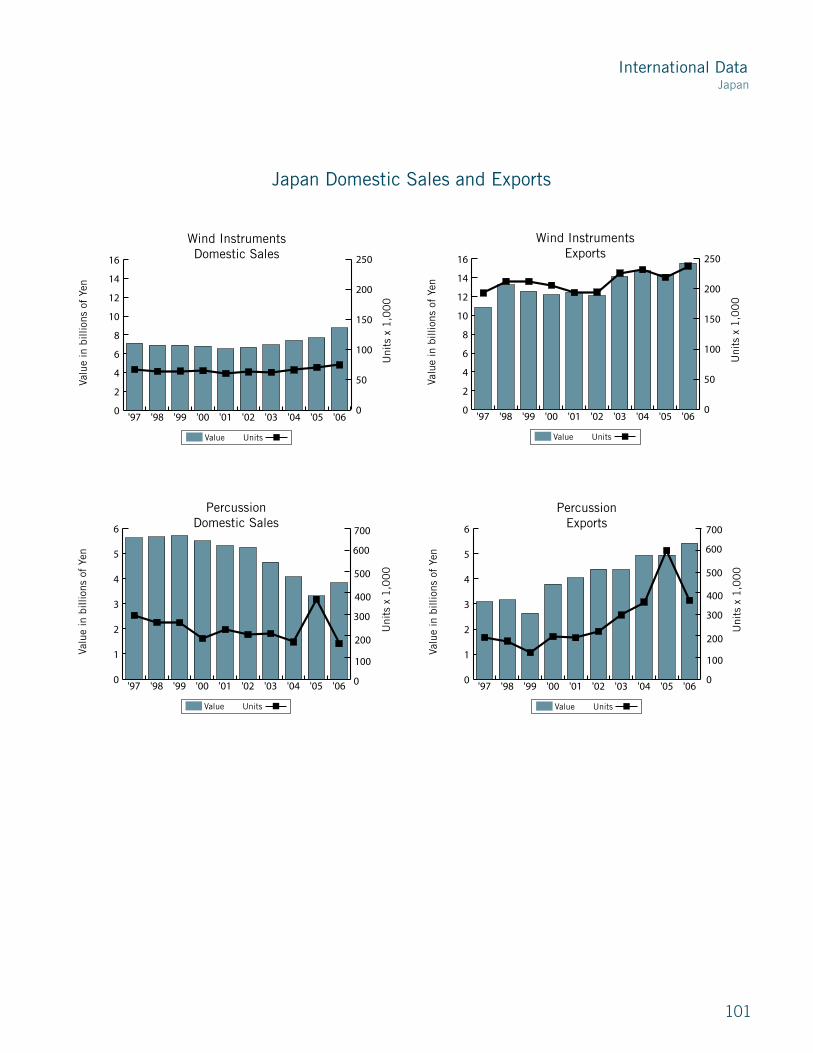

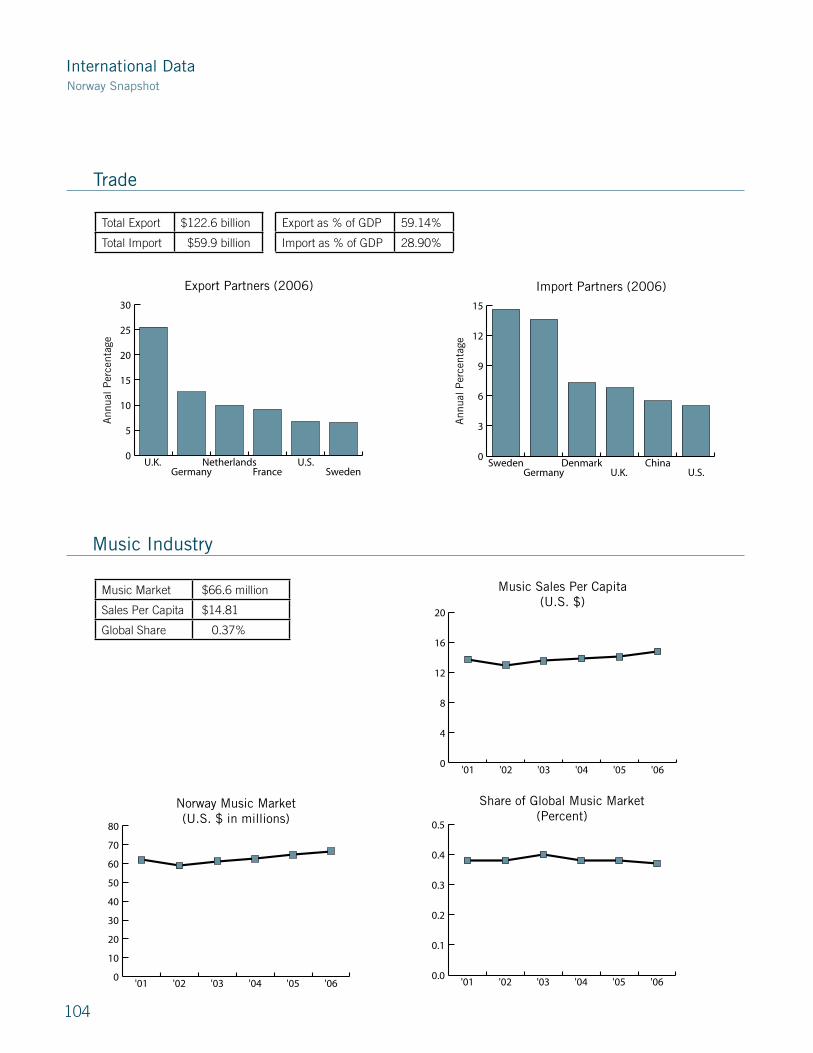

50 Understanding the International Data 51 �ustralia 58 �ustria 64 Canada 70 China 80 Germany 88 Italy 94 Japan102 Norway107 Spain112 Switzerland117 United Kingdom

People’s Attitudes toward Music

123 United States Gallup Poll136 �ustralian Nexus Survey146 United Kingdom Nexus Survey159 Combined Survey Comparison

Music retailing

169 Music Retailing Cost of Doing �usiness181 N�MM Executive Committee & �oard of Directors182 �cknowledgments

�

MethodoLogy

The NAMM Global Report is a collection of information gathered from many sources, agencies and associations around the world. N�MM does not verify any of the information and cannot and does not guarantee the accuracy of the data.

The statistics N�MM receives are summaries; N�MM personnel do not see or manipulate any individual company information. Sources for each piece of data are listed at the beginning of each section and can be summarized as follows:

U.S. sales information and commentary is provided by The Music Trades magazine; import and export numbers are collected by the U.S. Census �ureau. The Cost of Doing �usiness Survey is a program funded by N�MM in which N�MM Members contribute business information to Industry Insights (a third party research company), which aggregates the information and provides N�MM with the summary and commentary published in this edition. N�MM personnel do not see any individual company information.

Sales information and commentaries in the International section are provided by associations in each country. International economic, demographic and trade data are gathered from the CIA World Fact Book, and the International music industry numbers are provided by The Music Trades magazine.

The U.S. data in the People’s �ttitude Toward Music section is from a survey funded by N�MM and conducted every three years by the Gallup Organization. Information from the U.K. and �ustralia reflect the results of surveys conducted by Nexus Research Pty Ltd.

UnderstAnding the U.s. dAtA

The unit sales and retail values in this report were compiled by the staff of The Music Trades magazine, which provides the following overview of the methodology used:

Dollar and unit figures represent the quantity of product shipped to retailers in the United States, not actual sell-through volumes. Unit and dollar volumes are derived from a combination of import and export data gleaned from government agencies in the United States, China, Japan, Korea, Indonesia and the European Union; European, Japanese and U.S. trade association reports; financial filings of publicly traded companies in the United States and abroad; sales data provided by a cross-section of U.S. retailers, and informed estimates. Initially, the wholesale value of product shipped to retailers is computed. Then retail values are computed by adding an average margin, which varies among product categories.

Please note that data on the following pages does not include any figures on the used instrument market, which is extremely substantial, but difficult to measure with any accuracy.

�

U.s. indUstry revenUe At A gLAnCe

Product Sales Totals(Retail 2005–2006)

0 300 600 900 1200 1500

Drum Machines

Sound Modules

Multi Track Recorders

Institutional Organs

Home Organs

Stringed Instruments

Karaoke Products

Other Electronic Products

Keyboard Synthesizers

DJ Gear

Electronic Player Pianos

Digital Pianos

Cables

Signal Processing

Portable Keyboards

Instrument Amplifiers

Computer Music Products

General Accessories

Acoustic Pianos

Microphones

Wind Instruments

Percussion

Printed Music

Sound Reinforcement

Fretted Products

$123.14

$111.83$115.32

$111.91$89.19

$77.85$68.01

$68.43$77.73

$66.14$63.14

$53.97$48.75

$6.04$5.81

$5.92$6.26

$124.60

$147.90

$132.65

$172.80$143.75

$147.68$151.37

$120.47$108.86

$221.65$218.54

$232.03$218.78

$397.09$360.36

$365.62

$420.34

$416.58$427.83

$550.57$449.28

$446.73$458.65

$470.37$485.59

$571.99$581.71

$572.68$580.86

$919.30$865.43

$1,322.62

$1,279.41

2005 2006

(in millions of dollars)

6

U.s. indUstry revenUe At A gLAnCe

-25 -20 -15 -10 -5 0 5 10 15

Karaoke Products

Acoustic Pianos

Digital Pianos

Home Organs

Electronic Player Pianos

Multi Track Recorders

Other Electronic Products

Instrument Amplifiers

Sound Reinforcement

Portable Keyboards

Institutional Organs

Drum Machines

Fretted Products

Signal Processing

DJ Gear

Percussion

Printed Music

Cables

Microphones

General Accessories

Keyboard Synthesizers

Wind Instruments

Sound Modules

Stringed Instruments

Computer Music Products

2006 Industry Sales Gains and Declines

14.97%

13.59%

5.74%

3.12%

3.24%

2.70%

2.67%

2.50%

1.70%

1.43%

1.19%

-1.40%

-3.27%

-3.81%

-4.54%

-5.71%

-5.86%

-9.25%

-9.64%

-9.67%

-10.31%

-12.64%

-16.81%

-18.40%

-20.30%

�

introdUCtion

�006 Industry �nalysis Since 199�, there have been only two years where sales actually declined from the previous year. Last year was one of them, as the aggregate sales of instruments, audio gear, accessories and printed music dipped �.� percent to $�.� billion from the record level of $�.8 billion, set in �00�. In �000, the industry’s other

“down” year, causality was easily identified: that year the stock market tanked, wiping out an estimated $� trillion of the nation’s net worth. The source of the industry’s woes in �006, however, is not so clear-cut.

Current macro economic data makes for confusing and downright contradictory headlines. In March �00�, the Department of Commerce noted that new housing starts had dropped �� percent and that median housing prices were off � percent. In the same month, though, the Federal Reserve issued a study indicating that household net worth was at record levels. The respected Conference �oard study has recently placed the often-cited “Consumer Confidence Index” at a five-year high, yet voters in the recent mid-term elections expressed obvious displeasure with the current state of affairs. While unemployment levels hover near �0-year lows, opinion polls show high levels of consumer uncertainty. What to make of a situation where information gatherers seem to be working in different universes?

In a large, dynamic and diverse place like the United States, broad generalities are to be taken with a liberal grain of salt. If predicting the outlook, attitudes and behavior of a single teenager strains the ability of even the most concerned parent, is it possible for anyone to neatly sum up how �00 million people are going to behave from one day to the next? Sweeping generalities are also not too helpful in assessing what we call the music products industry. This is a highly fragmented business made up of diverse product categories that serve very different consumers, face different challenges and operate in different competitive environments. For example, the difficulties facing the church organ market have very little to do with the difficulties facing guitar makers. �ut for all the diversity, there do appear to be a few larger issues that have applied downward pressure on industry sales.

Unlike the stock market crash of �000, the magnitude and impact of the drop in housing prices has been much harder to measure. That doesn’t mean it hasn’t had an impact, however. With appraised values off anywhere between � percent and

�� percent (depending on the region), many homeowners no doubt feel less flush, and less in the mood to spring for big-ticket discretionary items. �s noted elsewhere in this report, the sale of home keyboards has closely followed the trajectory of new housing starts.

Over the past 1� months, the price of commodities, from copper to petroleum, has risen at a fast clip. Shipping costs have also moved up, particularly on freight from �sia to the United States. It would stand to reason that these rising costs would translate into price increases on most music products. In reality, however, prices on most Chinese goods either remained flat or fell slightly. We interpret this as a sign of major over-capacity issues in China that have prompted factories to sharpen prices in an effort to hang on to business.

Methodology also helps explain some of the slowdown in industry sales last year. The dollar and unit figures in this report represent the quantity of product shipped to retailers in the United States, not actual sell-through volumes. �ssessments from the largest to the smallest retailers in the country indicate that the entire distribution channel spent the better part of �006 struggling to work down excess inventory. The over-inventorying was particularly acute in the fretted instrument category. From this we conclude that the decline in consumer activity was not as acute as our sales data indicates.

Over the years, we have continually looked (with little success) for economic indicators that can be used to forecast music product sales. The problem is, unlike mass consumer goods (e.g., autos or home appliances) the specialized music business is somewhat insulated from the larger economy. The industry has prospered in some economically challenging times and floundered in boom times. That said, the best forecasting tool we have encountered, and it’s far from perfect, is the U.S. Census.

Much has been made about baby boomers and their interest in music making, and the industry’s broadening demographic appeal. In reality however, the 1�-to-��-year-old age group buys about �� percent of everything we sell. That’s where the Census provides some good news. If Census projections are to be believed, this vital age window is set to expand by 1.� to � percent a year until �0�0, after which they stop making

U.S. Segment Data

8

0

1

2

3

4

5

6

7

8

'06'05'04'03'02'01'00'99'98'97'96'95

Industry Total

Ret

ail V

alue

in $

bill

ions

2005–06 4.19% 10-Year 21.63%

Introduction, continued

predictions. If past economic progress is any guide, a larger potential market with more money to spend is grounds for optimism and reason to think that it will be at least another 1� years before industry sales turn down again.

� few words about the methodology underlying the sales numbers in this report. Unit and dollar volumes are derived from a combination of import and export data gleaned from government agencies in the United States, China, Japan, Korea, Indonesia and the European Union; European, Japanese and U.S. trade association reports; financial filings of publicly traded companies in the United States and abroad; sales data provided by a cross-section of U.S. retailers; and informed estimates. We initially compute a wholesale value of product shipped to retailers. Retail values are computed by adding an average margin, which varies among product categories.

9

U.s. segMent dAtA

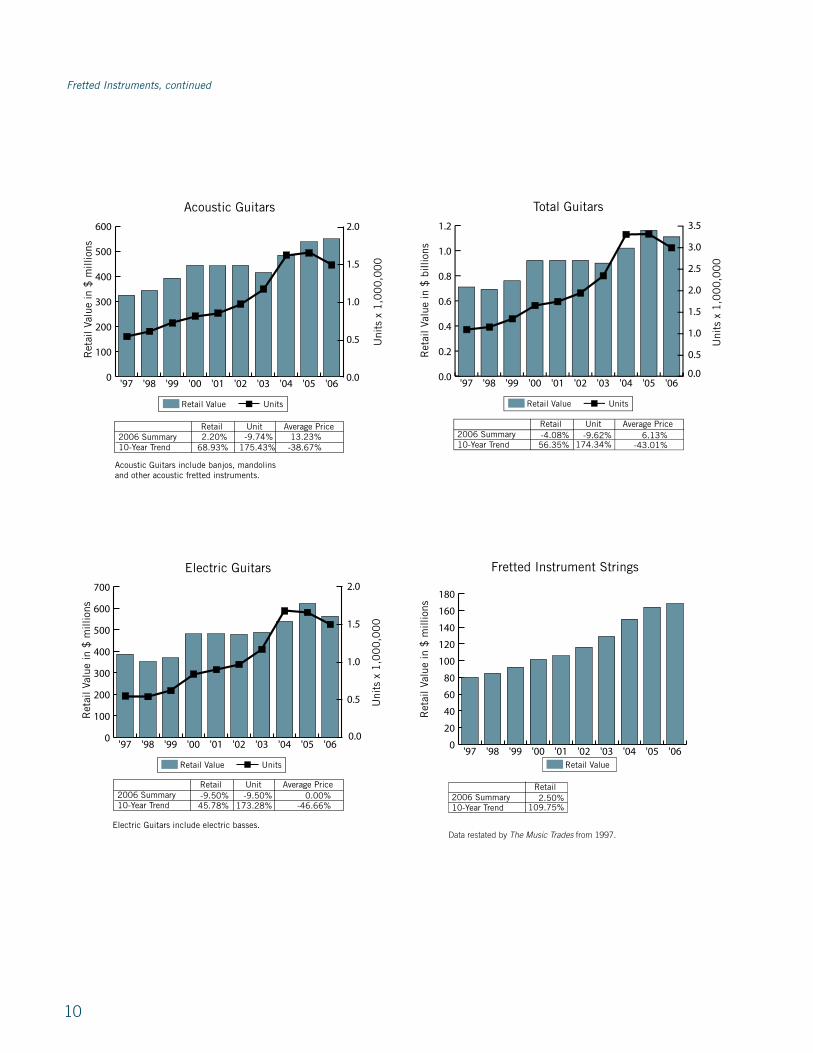

Fretted InstrumentsThe guitar industry’s growth streak came abruptly to a halt in �006 as sales of both electric and acoustics trended down. In both electrics and acoustics, the sales declines were concentrated exclusively in the entry-level price points. In price points over $�00, unit sales either held their own or advanced. �s previously mentioned, �006 saw major increases in all commodity prices, including wood, metal and energy. However, Chinese factories, scrambling to hold on to volume, actually cut prices during the year. The average landed unit value of guitars entering the United States from China dropped �.� percent during the year, suggesting a highly competitive manufacturing environment.

In dollars and units, the guitar is the single largest product category in the industry by a fairly wide margin. �ut the sales numbers don’t tell the entire story. In addition to spending on instruments, amplifiers, strings and stomp boxes, guitarists purchase a disproportionate amount of sound and recording gear, not to mention accessories, generating close to �0 percent of total industry revenue. Consequently, any slippage in guitar sales is cause for serious concern.

�ssessing a sales trend is not exactly like conducting a science experiment where cause and effect can be easily isolated and quantified. �s a result, it’s impossible to determine with precision exactly why guitar sales headed south after 10 years of brisk growth. Certainly, macro social and economic conditions weren’t particularly helpful. Higher gas prices for much of �006 took a bite out of discretionary income, falling hardest on the critical 1�-to-��-year-old demographic. This provides a plausible explanation for the disproportionate decline in entry-level price points. Unit sales of acoustic guitars retailing for under $��0 fell by 1� percent (dollar volume held steady, due to an increase in slightly higher-priced instruments with onboard pickups) while electrics in the under-$��0 price point were off by 11 percent. Popular music didn’t help things much, either. In �006, hip-hop music, which makes little use of the guitar, dominated the �illboard charts. (�ut after the first of the year, rap and hip-hop sales unexpectedly cratered, while sales from guitar-centric country acts increased.)

The numbers in this report reflect the instruments sold through the channel of specialized music retailers, and do not include sales figures from mass merchants. Extensive anecdotal evidence, ranging from comments by Guitar Center management to surveys by The Music Trades of the other �,000 MI retailers indicate that expanded distribution of guitars and related products through the mass market channel adversely impacted entry-level sales in the MI channel. However, total imports of acoustic guitars with a retail price

of under $�99 dropped by �0 percent in �006 and imports of electrics were off by 1�.6 percent, suggesting that mass merchants didn’t have a stellar year with guitars in �006, either. Obviously, the decline is not just a case of one distribution channel gaining market share at the expense of another.

The best-case scenario is that the decline in guitar sales was the result of temporary economic conditions and will reverse as consumers gain confidence. The worst-case suggests that the industry may be approaching something of a saturation point. If manufacturers’ warranty cards are any guide, about �0 percent of all guitars are purchased by males in the 1� to �6 year-old age range, a group that numbered approximately �� million at the end of �00�. Over the past decade the industry has sold well over �0 million guitars. Is it possible that most of the potential guitar prospects already have an instrument? �s noted earlier, given that we can’t test any of these hypotheses with a controlled experiment, they are just speculation.

U.S. Segment Data

Retail Value Market Share

Fretted Instrument

Strings10.3%

Instrument Amplifiers

22.0%

Electric Guitars34.3%

Acoustic Guitars33.4%

10

0

100

200

300

400

500

600

700

'06'05'04'03'02'01'00'99'98'97

Electric Guitars

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

,00

0

Retail Value Units

0.0

0.5

1.0

1.5

2.0

0605'04'03'02'01'00'99'98'97

0

200

400

600

800

1000

1200

1400

1600

1800

'04 '03 '02 '01 '00 '99 '98 '97 '96

2006 Summary10-Year Trend

Retail Unit Average Price-9.50%45.78%

-9.50%173.28%

0.00%-46.66%

Electric Guitars include electric basses.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

'06'05'04'03'02'01'00'99'98'97

Total Guitars

Ret

ail V

alue

in $

bill

ions

Retail Value Units

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0605'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

Import Value Units

Uni

ts x

1,0

00

,00

0

2006 Summary10-Year Trend

Retail Unit Average Price-4.08%56.35%

-9.62%174.34%

6.13%-43.01%

0

100

200

300

400

500

600

'06'05'04'03'02'01'00'99'98'97

Acoustic Guitars

0.0

0.5

1.0

1.5

2.0

0605'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

,00

0

Retail Value Units

-9.74%2.20% 13.23% 175.43%68.93% -38.67%

2006 Summary10-Year Trend

Retail Unit Average Price

Acoustic Guitars include banjos, mandolins and other acoustic fretted instruments.

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Fretted Instrument Strings

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Retail Value

2006 Summary10-Year Trend

Retail 2.50%

109.75%

Data restated by The Music Trades from 1997.

Fretted Instruments, continued

11

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01'00'99'98'97

Instrument Amplifiers

Ret

ail V

alue

in $

mill

ions

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0605'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

,00

0

-12.00% -9.25% 3.13%90.16%-0.45% -47.65%

2006 Summary10-Year Trend

Retail Unit Average Price

Instrument Amplifiers include tube, digital and solid-state amplifier heads, speaker enclosures and other self-contained amplifiers for guitars, basses and other musical instruments.

Retail Value Units

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

'06'05'04'03'02'01'00'99'98'97

Total Fretted Instruments

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

bill

ions

Retail Value

2006 Summary10-Year Trend

Retail-4.65%42.23%

Total Fretted Instruments include acoustic guitars, electricguitars, fretted instrument strings and instrument amplifiers.

U.S. Segment Data

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

'06'05'04'03'02'01'00'99'98'97

Fretted Instrument Market

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

bill

ions

Retail Value

2006 Summary10-Year Trend

Retail-3.27%61.76%

Fretted Instrument Market includes acoustic guitars, electricguitars and fretted instrument strings.

1�

Home and Church Organs�oth segments of the organ market recorded disappointing results in �006. �s retailers have long noted, there never has been a true “market” for home organs. Demand has been generated almost exclusively by the industry’s creative efforts, which have long centered on lesson programs offered by retailers. Last year’s decline in unit sales appears to be the result of fewer retailers doing the necessary work in the field to cultivate the demand for home organs.

The church market has been adversely affected by an ongoing shift from a traditional style of worship service utilizing an organ and choir toward a more contemporary service that uses guitars, keyboards and other instruments.

-12.64%

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Home Organs

0

2

4

6

8

10

12

14

16

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

2

4

6

8

10

12

14

16

0605'04'03'02'01'00'99'98'97

-19.77% 8.89%-49.18%-17.68% 61.98%

2006 Summary10-Year Trend

Retail Unit Average Price

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Institutional Organs

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0605'04'03'02'01'00'99'98'97

-8.01%-4.54% 3.77%-7.42%16.39% 25.71%

2006 Summary10-Year Trend

Retail Unit Average Price

Retail Value Market Share

Institutional Organs48.1%

Home Organs51.9%

0

20

40

60

80

100

120

140

160

'06'05'04'03'02'01'00'99'98'97

Total Organs

0

2

4

6

8

10

12

14

16

18

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

2

4

6

8

10

12

14

16

18

0605'04'03'02'01'00'99'98'97

-16.65%-8.92% 9.28%-41.45%-4.17% 63.67%

2006 Summary10-Year Trend

Retail Unit Average Price

1�

Retail Value Market Share

ElectricPlayer Pianos

18.3%

Digital Pianos19.8%

Grand Pianos44.1%

Vertical Pianos17.8%

0

50

100

150

200

250

300

350

400

450

500

'06'05'04'03'02'01'00'99'98'97

Grand Pianos

0

5

10

15

20

25

30

35

40

'05'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

5

10

15

20

25

30

35

40

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-23.50%-19.98% 4.61%

-5.01%-22.12% -18.01%

U.S. Segment Data

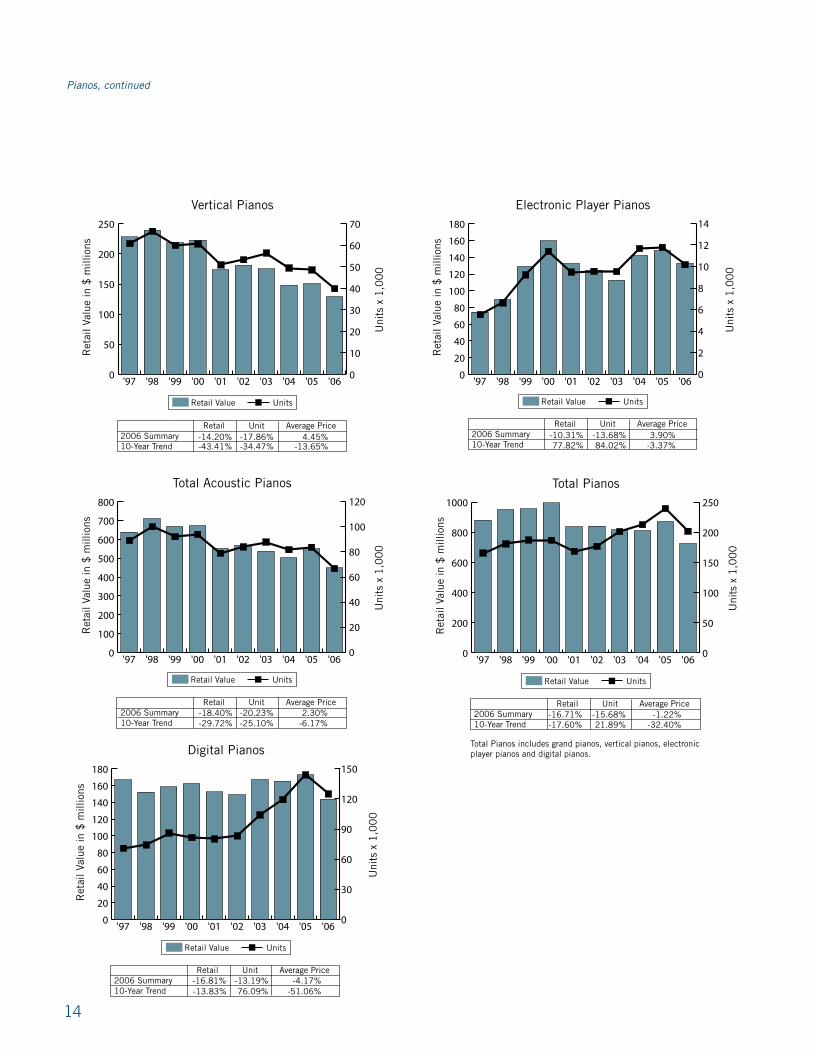

The Piano MarketSales of existing homes dropped 9 percent to 6.� million units in �006, versus sales of �.1 million in �00�. The drop in the sale of new homes was even greater, sinking �1 percent to just over 1 million units, compared with 1.�8 million in �00�. These numbers help explain the significant sales decline in all piano categories. Grand unit sales dropped ��.� percent; verticals were off 1�.9 percent; player-equipped units fell 19.� percent; and even digitals dropped 1�.� percent. Fewer people buying new homes or moving apparently translated into fewer piano sales. �lthough it provides little comfort to piano makers and retailers, it’s worth noting that manufacturers of furniture and home appliances blamed their disappointing sales results on the housing slowdown.

�ssessing the sales data by country of origin, size and price point, it’s clear that the slowdown affected every segment of the market. Lower price points generally suffered a steeper decline, but every category showed double-digit declines.

�lthough the slowdown in the housing market, whether in crimping consumers’ sense of wealth or reducing their need for a new piano, had a huge, negative effect on the market, retailers cite other factors as well. � common lament is that an over-reliance on out-of-store promotional events has conditioned consumers to avoid stores and wait for “blowout” sales before considering a purchase. �nother complaint is that excessive price focus in promotions has “commoditized” pianos in the eyes of buyers to the point that they assess only price without examining the underlying value.

1�

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Vertical Pianos

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

-17.86%-14.20% 4.45%-34.47%-43.41% -13.65%

2006 Summary10-Year Trend

Retail Unit Average Price

0

100

200

300

400

500

600

700

800

'06'05'04'03'02'01'00'99'98'97

Total Acoustic Pianos

0

20

40

60

80

100

120

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

20

40

60

80

100

120

'06'05'04'03'02'01'00'99'98'97

-20.23%-18.40% 2.30%-25.10%-29.72% -6.17%

2006 Summary10-Year Trend

Retail Unit Average Price

0

200

400

600

800

1000

'06'05'04'03'02'01'00'99'98'97

Total Pianos

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Total Pianos includes grand pianos, vertical pianos, electronic player pianos and digital pianos.

-15.68%-16.71% -1.22%21.89%-17.60% -32.40%

2006 Summary10-Year Trend

Retail Unit Average Price

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Digital Pianos

0

30

60

90

120

150

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

30

60

90

120

150

'06'05'04'03'02'01'00'99'98'97

-13.19%-16.81% -4.17%76.09% -13.83% -51.06%

2006 Summary10-Year Trend

Retail Unit Average Price

Pianos, continued

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Electronic Player Pianos

0

2

4

6

8

10

12

14

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

2

4

6

8

10

12

14

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-13.68%-10.31% 3.90%84.02%77.82% -3.37%

1�

School Music

Retail Value Market Share

WoodwindInstruments

48.9%

Stringed Instruments

13.8%

Brass Instruments

37.3%

U.S. Segment Data

0

200

400

600

800

1000

'06'05'04'03'02'01'00'99'98'97

Total Pianos

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Total Pianos includes grand pianos, vertical pianos, electronic player pianos and digital pianos.

-15.68%-16.71% -1.22%21.89%-17.60% -32.40%

2006 Summary10-Year Trend

Retail Unit Average Price

Unit sales of band and orchestral instruments edged up �.6 percent in �006, driven by the beneficial combination of increased school enrollments and flush state coffers. Dollar volume advanced at a similar pace, reflecting a stable pricing climate. �006 saw a 1.9 percent increase in the number of children enrolled in grades � through 1�, which created an increased market for all types of rental instruments. The fact that all but two of the �0 states enjoyed record tax receipts and budget surpluses was reflected in the increased sale of background brass instruments and educational percussion, products that are typically purchased directly by school systems.

Despite budgetary pressures in schools and an increased emphasis on basic curricula—often at the expense of arts education—music programs are surprisingly durable. This durability is reflected by the fact that unit sales of brass and woodwind instruments over the past five decades have closely tracked enrollment levels. If demographics are any indication, this facet of the industry has another five years (at least) of potential sales growth. � bulge in the number of �- to 10-year-olds will increase school enrollments through �0�0.

Public school music programs have represented the primary market for brass and woodwind instruments since school music programs became popular in the ’�0s. They are somewhat less significant for stringed instruments, due to the fact that recently there has been considerable growth in the number of string programs outside public school systems, whether in private music schools or various community centers. This increase in “private” stringed music programs provides one explanation for why growth in stringed instrument sales has outpaced wind instruments. Lower price points, largely due to imports from China, have also contributed to the sales growth, as students are now more likely to purchase, rather than rent, an instrument.

�lthough computer software and recording systems are considered in this report as two distinct product categories, they in fact are simply two different ways of addressing the same issue: capturing and editing music. Over the past five years, spending on recording has expanded significantly. However, growth in software-based products has come at the expense of self-contained hardware systems.

Virtually no one in the United States under the age of �0 has experienced life without a computer. Unlike preceding generations that modified behaviors and practices to take advantage of readily accessible computing power, this younger demographic has viewed the computer as an indispensable appendage since birth. This generational difference helps the trend.

� shift in the way consumers make use of self-contained recording systems has led to a significant decline in the category. Where the multi-track units were once viewed as a central component of a project studio, they have since been downgraded to the status of a “musical sketch pad”: devices used for capturing musical ideas on the fly, but not for recording and editing a full-range project. �s a result, the most popular units are now low-cost portable units, many of which are only slightly larger than an iPod.

However, declines in the sale of self-contained units have been more than offset by increases in recording software and components designed for use with a personal computer. Sales of recording and sequencing software advanced 11 percent in the past year, despite the continued prevalence of piracy. (Some manufacturers estimate that for every program sold, at least eight are illegally copied.) Sound cards, input/output boxes and various control surfaces enjoyed even more robust growth, advancing 19 percent for the year.

16

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01

Stringed Instruments

0

50

100

150

200

250

300

350

400

450

'04'03'02'01'00

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01

Data restated by The Music Trades from 2001.

6-Year Trend13.60% 7.01%

6.32% 17.51%6.16%

-9.52%2006 Summary

Retail Unit Average Price

0

100

200

300

400

500

600

700

'06'05'04'03'02'01

Total School Music

0

200

400

600

800

1000

1200

'04'03'02'01'00

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

200

400

600

800

1000

1200

'06'05'04'03'02'01

2006 Summary6-Year Trend

Retail Unit Average Price4.55% 4.58%

-11.53% 5.13%-0.02%

-15.85%

School Music, continued

0

50

100

150

200

250

300

350

400

'06'05'04'03'02'01'00'99'98'97

Woodwind Instruments

0

50

100

150

200

250

300

350

400

450

'04 '03 '02 '01 '00 '99 '98 '97 '96 '95

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01'00'99'98'97

10-Year Trend1.48% 2.03%

-13.47% 3.72%-0.53%

-16.57%2006 Summary

Retail Unit Average Price

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

Brass Instruments

0

50

100

150

200

250

300

'04'03'02'01'00'99'98'97'96'95

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price5.63% 4.52%

-17.06% -9.38%1.06%

-8.48%

Retail Value Units

1�

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

Power Amplifiers

0

100

200

300

400

500

600

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

100

200

300

400

500

600

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-6.83% -11.32%5.32% 15.98%

5.06%-9.20%

Retail Value Market Share

Non-Powered Mixers9.8%

Powered Mixers5.8%

Speaker Enclosures

28.3% Cables10.3%

Cabled Microphones

22.6%

Wireless Microphones

8.5%

Power Amplifiers

14.8%

Audio Products�006 was a challenging year in the sound reinforcement market. Slowing economic conditions took a toll on unit sales as the general public tightened its spending. Rising costs of raw materials and �sian labor brought the eight-year deflationary trend to a halt. However, in a market where copper prices surged by 80 percent, sheet steel advanced by �0 percent and hourly labor in China was up 1� percent, the average selling prices of most sound gear was up in the mid-single digits at best. This suggests significant over-capacity in �sia and brutal price competition. �t some point in the near term, expect prices to advance at a somewhat faster pace.

The type of audio products that are the staple of the MI distribution channel revolve around what can best be described as “mature technology.” The electro-magnetic paper-coned speaker has been with us for almost a century; analog mixers are based on technology that is nearly as venerable; and the digital switching technology that has made power amps more efficient is approaching its �0th anniversary. Despite the comparative lack of core innovation, improved packaging of these basic technologies has resulted in ongoing shifts in the product mix. The increasing popularity of powered speakers, which are easier to configure and less likely to malfunction, have come at the expense of power amp and powered mixer sales. Unit volumes in both amps and powered mixers trended down last year.

From powering a U� stadium concert to making political pronouncements audible, line-array speakers have long been used for their combination of sound clarity and efficiency. Once employed only in high-end installations and top tour sound systems, line-array technology is now more affordable and is being embraced by the broader market. These products have contributed to the modest increase in enclosure sales.

The bright spot in the sound business has been the continued upward trend in microphone sales, both wired and cable. Two factors seem to be at work here. Top recording engineers have long recognized that individual microphones have special characteristics that color tonal qualities. Musicians who have set up project studios at home have made the same discovery, which has prompted them to add to their collection of microphones. Increasing availability of affordable, high-quality mics from China has also helped spur demand. Secondly, from church sanctuaries to health clubs, to school auditoriums to corporate meeting rooms, the use of microphones is simply on the rise.

U.S. Segment Data

With fewer venues for live music, churches play an increasingly important role in the total sound market. End-user data is sketchy at best, but several manufacturer surveys indicate that houses of worship represent approximately �0 percent of sound reinforcement sales. Given that there are more than �00,000 churches in the United States alone, this should not be a surprise.

18

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01'00'99'98'97

Speaker Enclosures

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail-0.80%40.98%

0

20

40

60

80

100

120

140

160

180

200

'06'05'04'03'02'01'00'99'98'97

Non-Powered Mixers

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

300

350

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-14.90% -6.40%

8.54% 203.77%-9.09%

-64.27%

0

20

40

60

80

100

120

140

160

'06'05'04'03'02'01'00'99'98'97

The Cable Market

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail2.50%

48.76%

Audio Products, continued

0

20

40

60

80

100

120

140

160

'06'05'04'03'02'01'00'99'98'97

Powered Mixers

0

50

100

150

200

250

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-9.69% -10.58%

-29.63% -3.15%1.00%

-27.34%

19

0

50

100

150

200

250

300

350

'06'05'04'03'02'01'00'99

Cabled Microphones

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary8-Year Trend

Retail2.00%

29.69%

0

20

40

60

80

100

120

140

'06'05'04'03'02'01'00'99

Wireless Microphones

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

Data represents estimates of only those microphones sold by the approximately 7,000 MI retailers in the United States, and excludes products aimed at broadcast markets.

2006 Summary8-Year Trend

Retail4.50%

30.89%

U.S. Segment Data

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'06'05'04'03'02'01'00'99

Total Sound Reinforcement

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

bill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary8-Year Trend

Retail-2.53%9.19%

All data represents an estimate of sound reinforcement products sold by the approximately 7,000 MI retailers in the United States. Excluded from data are sound products for the cinema, tour sound, broadcast and large fixed-installation markets. Data includes non-powered mixers, power amplifiers, powered mixers, speaker enclosures, cable, cable microphones and wireless microphones.

�0

The Signal Processing MarketComputer-based recording systems have continued to adversely impact the sale of rack-mounted signal processing. Rather than buy a metal box, with compression, delay, reverb or EQ functions, consumers are now just as likely to buy a software

“plug-in” to use with their recording software. �s a result, actual hardware is more and more limited to live performance applications.

Multi-effect floor units and stomp boxes, by contrast, are almost exclusively the province of the guitar market. Despite a down year in guitars, both of these categories advanced, reflecting a continued stream of new products and a larger user base.

Retail Value Market Share

Rack-Mounted Processors

43.7%

Stomp Boxes25.1%

Multi-Effect Floor Processors

31.2%

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

Multi-Effect Floor Processors

0

50

100

150

200

250

300

350

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

50

100

150

200

250

300

350

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price3.30% -1.50%

79.73% 150.81%4.88%

-28.34%

0

20

40

60

80

100

120

140

160

'05'05'04'03'02'01'00'99'98'97

Rack-Mounted Processors

0

100

200

300

400

500

600

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

0

100

200

300

400

500

600

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-6.44% -8.00%

-26.83% 11.79%1.69%

-34.55%

�1

0

10

20

30

40

50

60

'06'05'04'03'02'01'00'99'98'97

Stomp Boxes

0.0

0.2

0.4

0.6

0.8

1.0

1.2

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

,00

0

Retail Value

Retail Value Units

Retail Value Units

0.0

0.2

0.4

0.6

0.8

1.0

1.2

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price2.41% -3.50%

12.91% 95.51%6.12%

-42.25%

0

40

80

120

160

200

240

'06'05'04'03'02'01'00'99'98'97

Total Signal Processing

0.0

0.5

1.0

1.5

2.0

2.5

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

,00

0

Retail Value

Retail Value Units

Retail Value Units

0.0

0.5

1.0

1.5

2.0

2.5

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-1.40% -4.48%0.68% 66.78%

3.22%-39.63%

U.S. Segment Data

��

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Drum Kits

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

Retail Value Units

2006 Summary10-Year Trend

Retail Unit Average Price-3.33% -3.80%96.84% 178.69%

0.49%-29.37%

0

10

20

30

40

50

60

'06'05'04'03'02'01'00'99'98'97

Educational Percussion

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

Educational Percussion includes timpani, marching percussion, mallet instruments, snare drum kits and orchestral percussion instruments.

2006 Summary10-Year Trend

Retail5.20%

31.98%

Retail Value Market Share

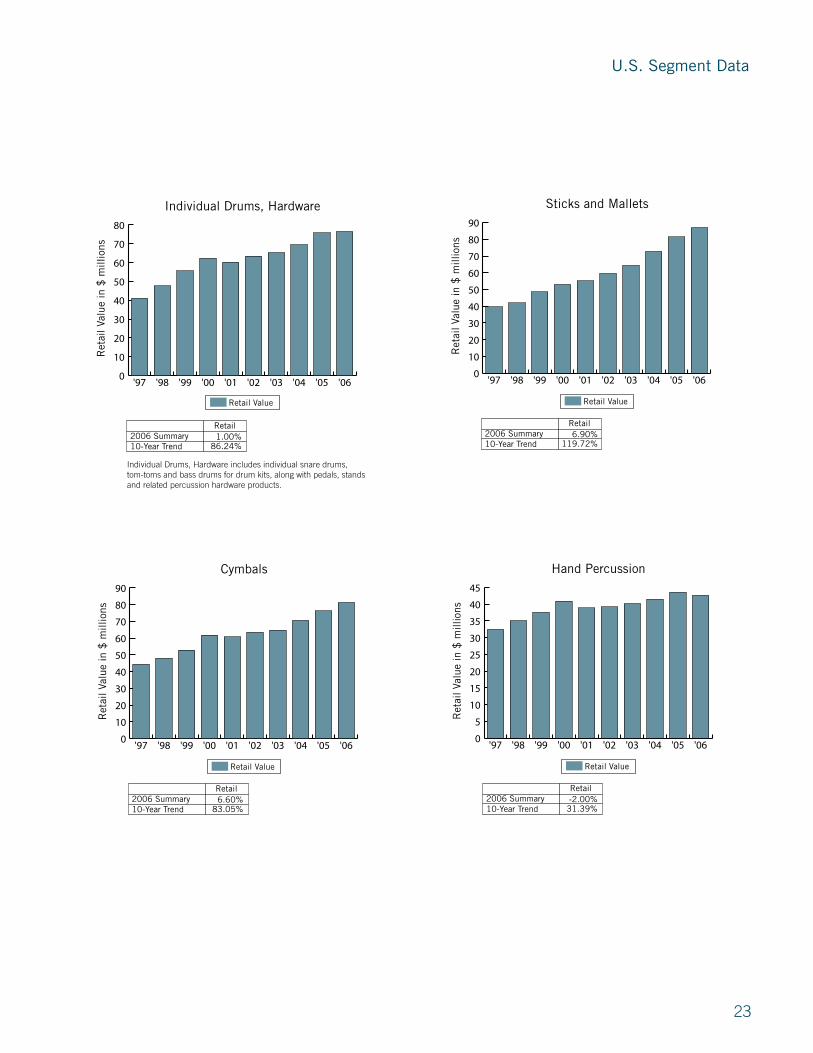

Educational Percussion

10.1%

Sticks & Mallets15.0%

Individual Drums, Hardware

13.2%

Drumheads11.6%

Cymbals14.0%

Hand Percussion

7.3%

Drum Kits28.8%

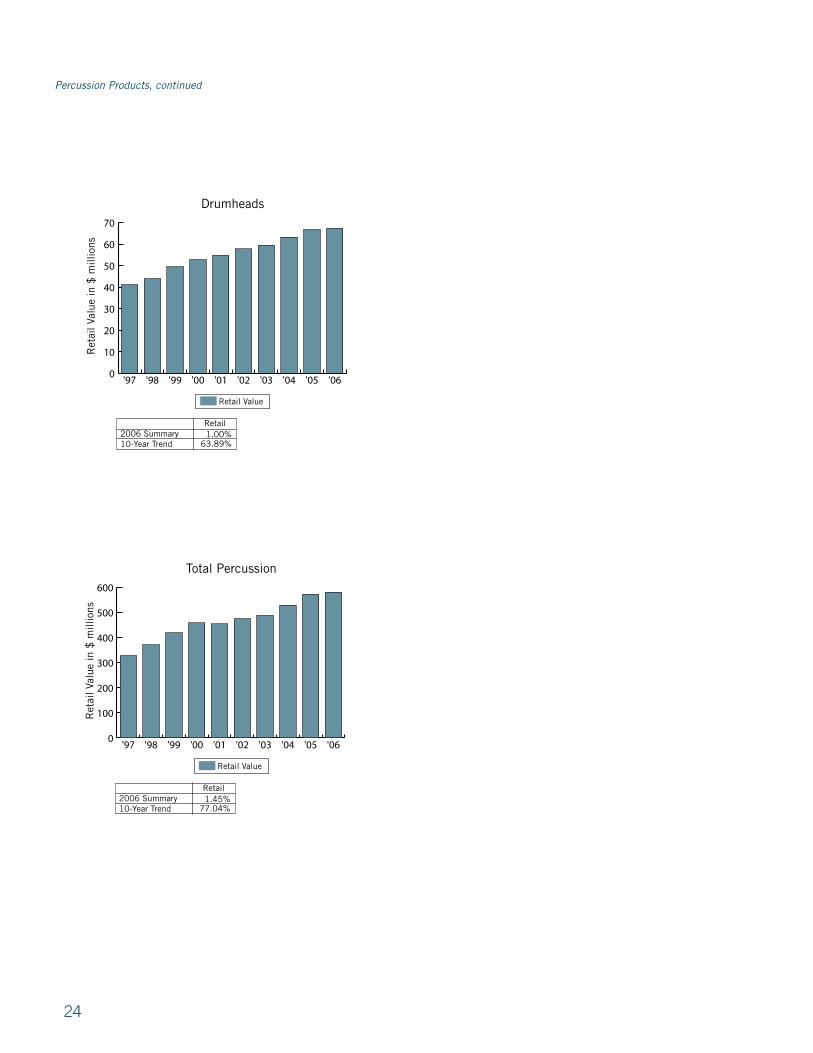

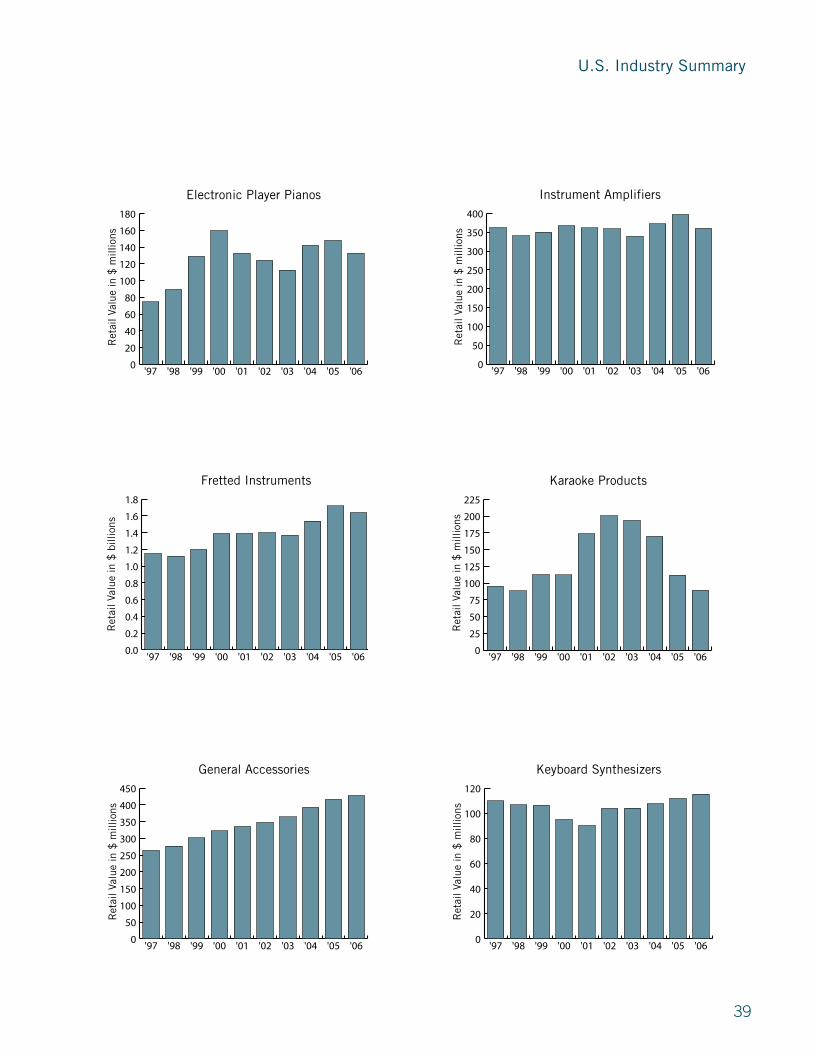

Percussion ProductsSales of percussion products moved in two directions in �006. �ccessory products including sticks, cymbals and hardware trended up, while sales of drums decreased slightly. To explain the drop-off in sales of drum kits and hand percussion, retailers cite a number of factors, including unease among the buying public and competition from non-musical items like the top-selling Nintendo and Microsoft gaming consoles and widescreen televisions. The user base of percussionists continues to expand however, which helps account for the increase in the sale of “consumable” items like drumsticks, heads and cymbals.

One surprising bright spot has been the increase in the sale of educational percussion—bass drums, marching percussion, timpani and mallet instruments—which are typically purchased by schools. Despite widely publicized fears of budget cuts, states are apparently in the process of outfitting their music rooms with new percussion instruments. It doesn’t hurt that nationwide surging tax collections pushed state revenues up 10 percent last year. State spending advanced at an even faster pace, up 11.� percent.

��

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Cymbals

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units 2006 Summary10-Year Trend

Retail6.60%

83.05%

0

10

20

30

40

50

60

70

80

'06'05'04'03'02'01'00'99'98'97

Individual Drums, Hardware

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

Individual Drums, Hardware includes individual snare drums, tom-toms and bass drums for drum kits, along with pedals, stands and related percussion hardware products.

2006 Summary10-Year Trend

Retail1.00%

86.24%

0

5

10

15

20

25

30

35

40

45

'06'05'04'03'02'01'00'99'98'97

Hand Percussion

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units 2006 Summary10-Year Trend

Retail-2.00%31.39%

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Sticks and Mallets

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units 2006 Summary10-Year Trend

Retail6.90%

119.72%

U.S. Segment Data

��

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

Drumheads

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units 2006 Summary10-Year Trend

Retail1.00%

63.89%

0

100

200

300

400

500

600

'06'05'04'03'02'01'00'99'98'97

Total Percussion

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units 2006 Summary10-Year Trend

Retail1.45%

77.04%

Percussion Products, continued

��

DJ Products

0

5

10

15

20

25

30

35

'06'05'04'03'02'01'00'99'98'97

CD Players

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price16.39% 2.06%

132.17% 191.53%14.05%

-20.36%

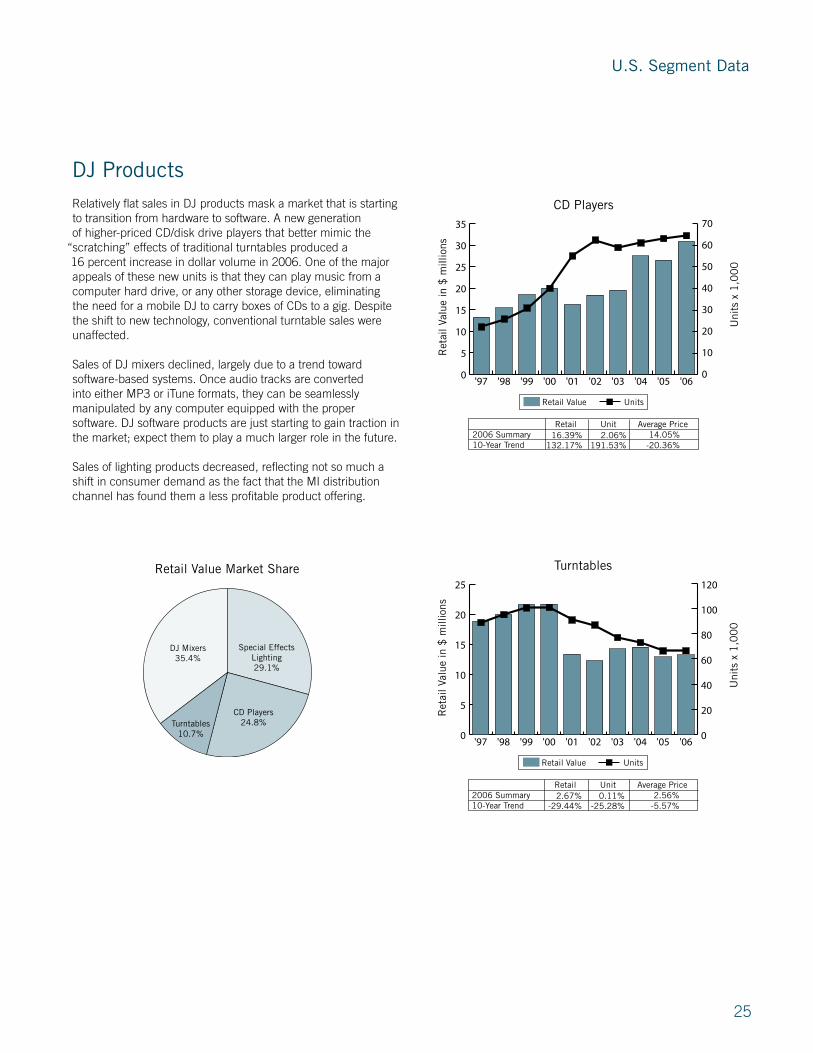

Special Effects Lighting29.1%

DJ Mixers35.4%

Turntables10.7%

CD Players24.8%

Retail Value Market Share

0

5

10

15

20

25

'06'05'04'03'02'01'00'99'98'97

Turntables

0

20

40

60

80

100

120

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

20

40

60

80

100

120

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price2.67% 0.11%

-29.44% -25.28%2.56%

-5.57%

Relatively flat sales in DJ products mask a market that is starting to transition from hardware to software. � new generation of higher-priced CD/disk drive players that better mimic the

“scratching” effects of traditional turntables produced a 16 percent increase in dollar volume in �006. One of the major appeals of these new units is that they can play music from a computer hard drive, or any other storage device, eliminating the need for a mobile DJ to carry boxes of CDs to a gig. Despite the shift to new technology, conventional turntable sales were unaffected.

Sales of DJ mixers declined, largely due to a trend toward software-based systems. Once audio tracks are converted into either MP� or iTune formats, they can be seamlessly manipulated by any computer equipped with the proper software. DJ software products are just starting to gain traction in the market; expect them to play a much larger role in the future.

Sales of lighting products decreased, reflecting not so much a shift in consumer demand as the fact that the MI distribution channel has found them a less profitable product offering.

U.S. Segment Data

�6

0

5

10

15

20

25

30

35

40

45

50

'06'05'04'03'02'01'00'99'98'97

Special Effects Lighting Units

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

2006 Summary10-Year Trend

Retail-7.16%-0.10%

0

20

40

60

80

100

120

140

'05'05'04'03'02'01'00'99'98'97

Total DJ Sales

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

2006 Summary10-Year Trend

Retail1.18%

17.49%

0

10

20

30

40

50

'06'05'04'03'02'01'00'99'98'97

DJ Mixers

0

50

100

150

200

250

300

'04 '03 '02 '01 '00 '99 '98 '97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-.99% -6.49%

17.44% 29.06%5.88%

-2.69%

DJ Products, continued

��

0

10

20

30

40

50

60

70

80

90

100

'06'05'04'03'02'01'00'99'98'97

Total Multi-Track Sales

0

20

40

60

80

100

120

140

160

180

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

2006 Summary10-Year Trend

Retail Unit Average Price-9.67% -10.57%

-43.99% 1.58%1.01%

-44.87%

Multi-Track

0

5

10

15

20

25

30

35

40

'06'05'04'03'02'01'00'99'98'97

Cassette Tape Multi-Track

0

20

40

60

80

100

120

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

20

40

60

80

100

120

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price0.00% -19.48%

-75.88% -39.94%24.19%

-62.92%

0

10

20

30

40

50

60

70

80

'06'05'04'03'02'01'00'99'98'97

Hard Disk Multi-Track

0

10

20

30

40

50

60

70

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

Retail Value Units

2006 Summary10-Year Trend

Retail Unit Average Price-11.37% 1.01%-24.03% 143.09%

-12.26%-68.75%

Retail Value Market Share

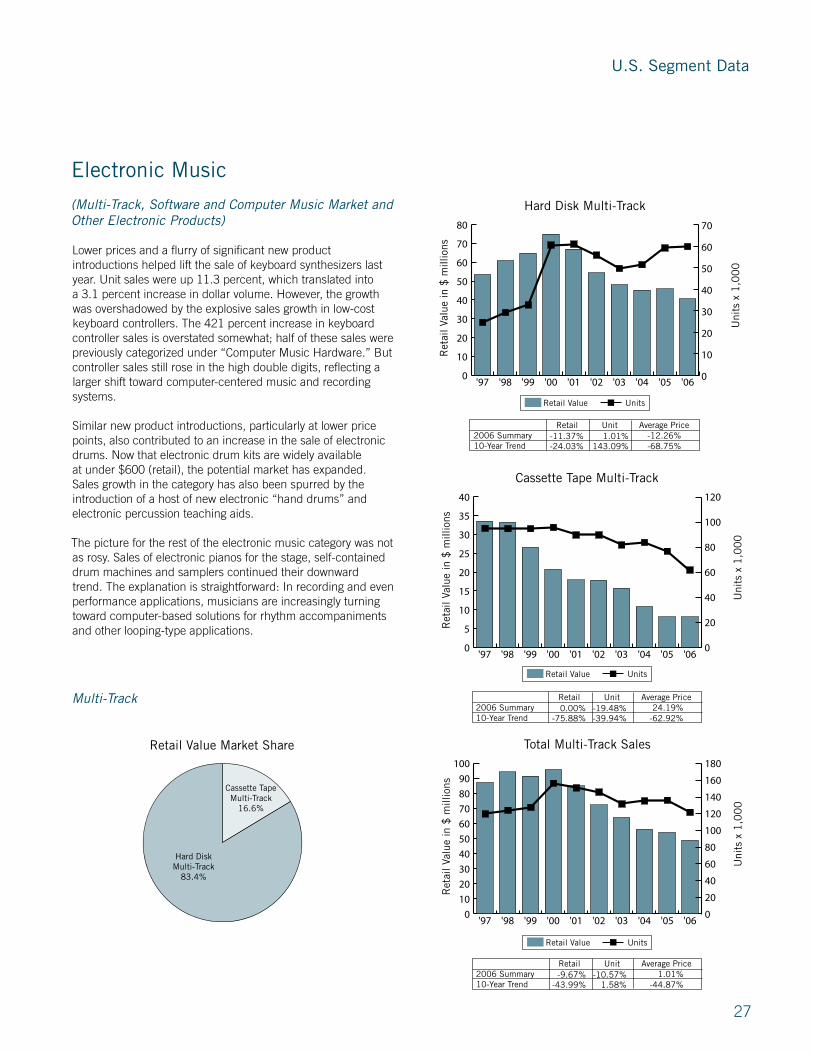

Cassette Tape Multi-Track

16.6%

Hard Disk Multi-Track

83.4%

Electronic Music

(Multi-Track, Software and Computer Music Market and Other Electronic Products)

Lower prices and a flurry of significant new product introductions helped lift the sale of keyboard synthesizers last year. Unit sales were up 11.� percent, which translated into a �.1 percent increase in dollar volume. However, the growth was overshadowed by the explosive sales growth in low-cost keyboard controllers. The ��1 percent increase in keyboard controller sales is overstated somewhat; half of these sales were previously categorized under “Computer Music Hardware.” �ut controller sales still rose in the high double digits, reflecting a larger shift toward computer-centered music and recording systems.

Similar new product introductions, particularly at lower price points, also contributed to an increase in the sale of electronic drums. Now that electronic drum kits are widely available at under $600 (retail), the potential market has expanded. Sales growth in the category has also been spurred by the introduction of a host of new electronic “hand drums” and electronic percussion teaching aids.

The picture for the rest of the electronic music category was not as rosy. Sales of electronic pianos for the stage, self-contained drum machines and samplers continued their downward trend. The explanation is straightforward: In recording and even performance applications, musicians are increasingly turning toward computer-based solutions for rhythm accompaniments and other looping-type applications.

U.S. Segment Data

�8

Sound Cards & Related Hardware

44.4%

Software55.6%

Retail Value Market Share

0

40

80

120

160

200

240

'06'05'04'03'02'01'00'99'98'97

Software

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail11.94%

168.54%

Software includes recording software packages, plug-in modules, loops, sampling software, notation software and educational software.

0

20

40

60

80

100

120

140

160

180

200

'06'05'04'03'02'01'00'99'98'97

Sound Cards and Related Hardware

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail19.00%

1,144.74%

Sound Cards and Related Hardware includes sound cards and related input/output devices, digital audio work surfaces (DAWS) and keyboard controllers designed expressly for use with computers.

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01'00'99'98'97

Total Computer Music Market

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail14.97%

312.10%

Electronic Music, continued

�9

0

5

10

15

20

25

30

'06'05'04'03'02'01'00'99'98'97

Drum Machines

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-3.77% -14.00%

-73.30% -42.05%11.89%

-53.93%

0

20

40

60

80

100

120

'06'05'04'03'02'01'00'99'98'97

Keyboard Synthesizers

0

10

20

30

40

50

60

70

80

90

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

Retail Value Units

2006 Summary10-Year Trend

Retail Unit Average Price3.11% 11.29%4.93% 16.87%

-7.35%-10.22%

Keyboard Synthesizers48.8%

Electronic Drums22.0%

Electronic Pianos/Professional Organs

18.8%

Sound Modules2.6%

Controller Keyboards5.3%Drum Machines

2.5%

Retail Value Market Share

0

5

10

15

20

25

30

35

40

45

50

'06'05'04'03'02'01'00'99'98'97

Sound Modules

0

10

20

30

40

50

60

70

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value UnitsU

nits

x 1

,00

0

Retail Value Units

0

10

20

30

40

50

60

70

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price5.77% -34.28%

-85.90% -83.45%60.95%

-14.79%

Other Electronic Products

U.S. Segment Data

�0

0

5

10

15

20

25

30

'06'05'04'03'02'01'00'99'98'97

Controller Keyboards

0

10

20

30

40

50

60

70

80

'04'03'02'01'00'99'98'97'96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0.000000

8.888889

17.777778

26.666667

35.555556

44.444444

53.333333

62.222222

71.111111

80.000000

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price21.60% 421.13%

-55.22% 439.75%-76.67%-91.70%

0

10

20

30

40

50

60

70

80

90

'06'05'04'03'02'01'00'99'98'97

Electronic Pianos / Professional Organs

0

5

10

15

20

25

30

35

40

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

Retail Value Units

0

5

10

15

20

25

30

35

40

'06'05'04'03'02'01'00'99'98'97

2006 Summary10-Year Trend

Retail Unit Average Price-27.08% -19.70%169.56% 236.94%

-9.19%-20.00%

0

10

20

30

40

50

60

'06'05'04'03'02'01'00'99'98'97

Electronic Drums

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail5.50%

434.56%

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

Total Electronic Music Sales

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail-3.28%2.69%

Electronic Music, continued

�1

U.S. Segment Data

0

50

100

150

200

250

300

'06'05'04'03'02'01'00'99'98'97

Total Electronic Music Sales

0

10

20

30

40

50

60

70

'04 '03 '02 '01 '00 '99 '98 '97 '96

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Retail Value Units

2006 Summary10-Year Trend

Retail-3.28%2.69%

Printed MusicPrinted music sales advanced modestly in �006, due to a host of factors. � decline in the sale of entry-level guitars and pianos slowed the sales of method books. These issues were exacerbated by the problem of unauthorized online music sales, particularly in the guitar “tab” category. Web sites such as fret�fret.com and Ultimateguitar.com, which offer free tabulatures online, report traffic of over ��0,000 unique visitors per week. In a year where the �illboard charts were dominated by hip-hop and R&� songs, publishers also suffered from a dearth of high-selling hit songs.

Offsetting these negatives, school programs apparently increased their purchases of printed music.

0

100

200

300

400

500

600

'06'05'04'03'02'01'00'99'98'97

Printed Music

0

200

400

600

800

1000

1200

1400

1600

'04 '03 '02 '01 '00 '99 '98

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

2006 Summary10-Year Trend

Retail1.70%

34.35%

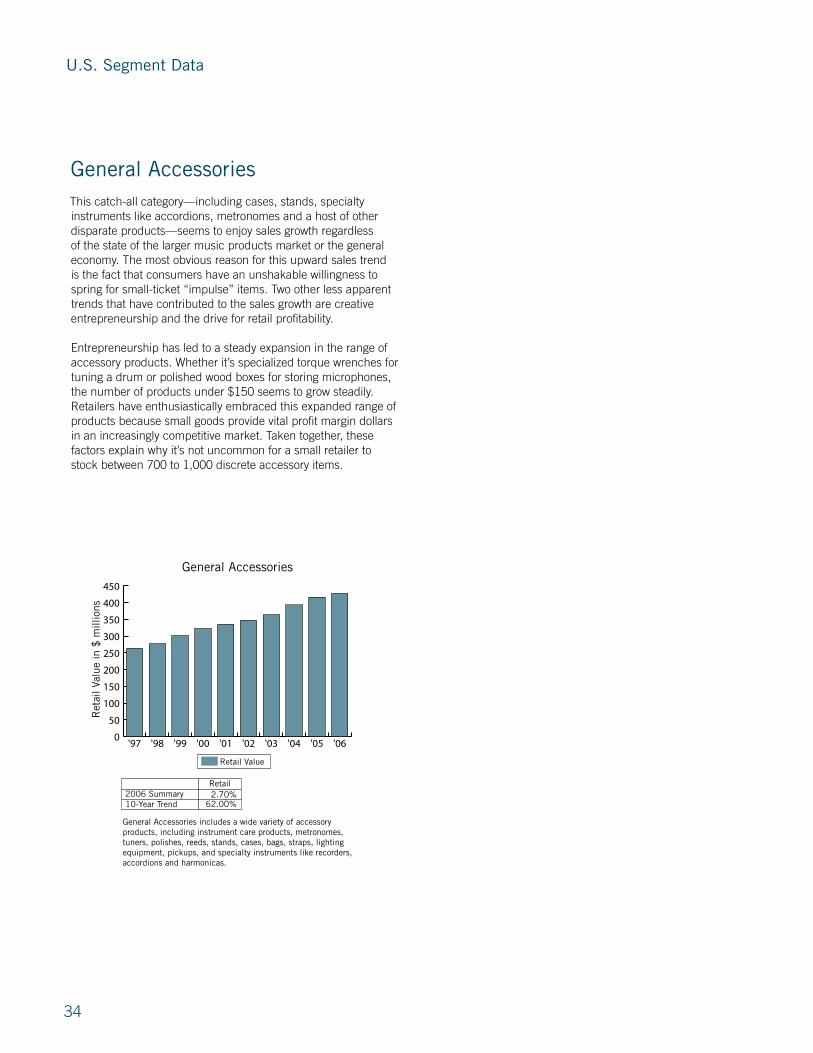

Retail Value Market Share

Keyboards Under $199

44.7%

Keyboards Over $199

55.3%

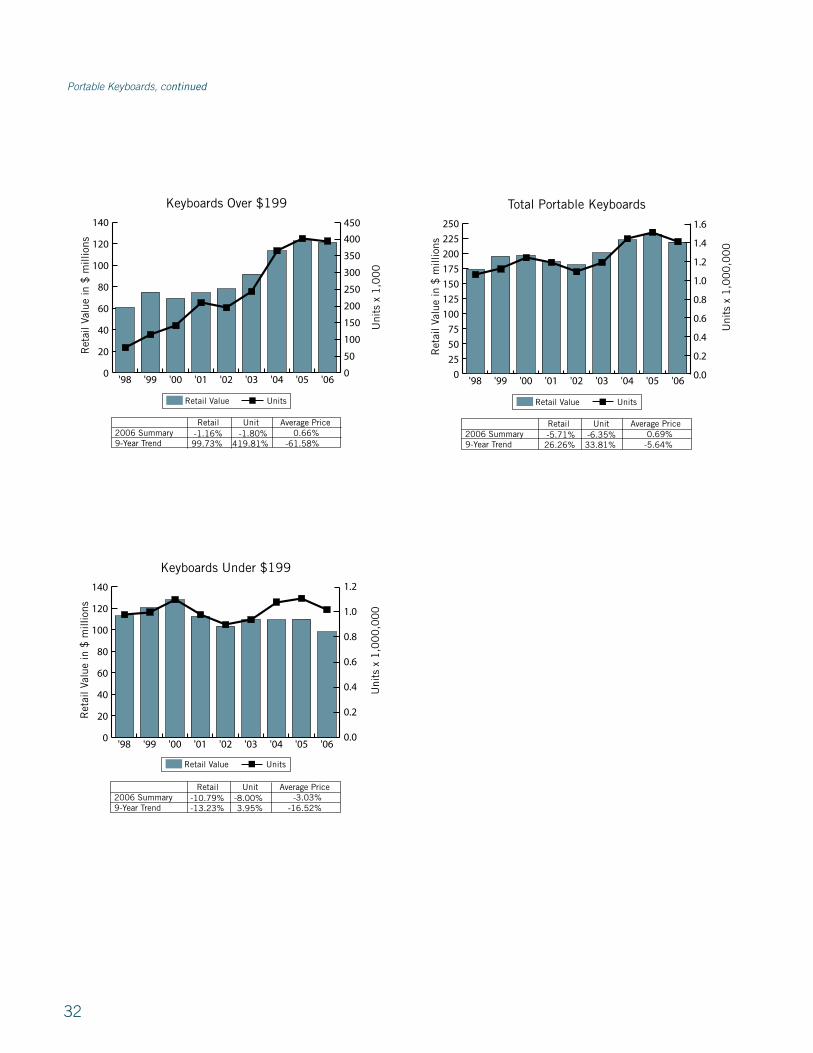

Portable KeyboardsSales of portable keyboards, both those sold by mass merchants and those by specialized MI retailers, declined, but for different reasons. Now in their �6th season, portable keyboards in the mass merchant channel face stiff competition from newer and more novel forms of electronic entertainment, ranging from electronic games to slick new cell phones. Manufacturers of keyboards now face the challenge of fighting for shelf space at mega retailers ranging from �est �uy to Wal-Mart.

The higher-end keyboards, which are the province of specialized MI retailers, suffered declines primarily because of competition from keyboard controllers. Given that teen access to computers in the United States nears 90 percent, the growing inclination is to buy a keyboard that works in conjunction with a computer, rather than a self-contained unit.

��

0

20

40

60

80

100

120

140

'06'05'04'03'02'01'00'99'98

Keyboards Under $199

0.0

0.2

0.4

0.6

0.8

1.0

1.2

'06'05'04'03'02'01'00'99'98

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

,00

0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

'06'05'04'03'02'01'00'99'98

Uni

ts x

1,0

00

2006 Summary9-Year Trend

Retail Unit Average Price-10.79% -8.00%-13.23% 3.95%

-3.03%-16.52%

0

25

50

75

100

125

150

175

200

225

250

'06'05'04'03'02'01'00'99'98

Total Portable Keyboards

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'04'03'02'01'00'99'98

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

Uni

ts x

1,0

00

,00

0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'06'05'04'03'02'01'00'99'98

Uni

ts x

1,0

00

2006 Summary9-Year Trend

Retail Unit Average Price-5.71% -6.35%26.26% 33.81%

0.69%-5.64%

0

20

40

60

80

100

120

140

'06'05'04'03'02'01'00'99'98

Keyboards Over $199

0

50

100

150

200

250

300

350

400

'04 '03 '02 '01 '00 '99 '98

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value

Retail Value Units

0

50

100

150

200

250

300

350

400

450

'06'05'04'03'02'01'00'99'98

Uni

ts x

1,0

00

2006 Summary9-Year Trend

Retail Unit Average Price-1.16% -1.80%99.73% 419.81%

0.66%-61.58%

Portable Keyboards, continued

��

U.S. Segment Data

KaraokeThe ongoing sales decline in the karaoke market reflects both shifting consumer tastes, and the dynamic of the mass merchant distribution channel. Three years ago, when fourth-quarter sales of karaoke machines and software failed to meet the expectations of large retailers (including Wal-Mart, Target, �est �uy and Costco), their immediate response was to reduce the number of units they stocked and to move the karaoke inventory to a less prominent position in the store. Not surprisingly, sales the following year were also disappointing, which triggered yet another inventory reduction and banishment to an even more remote piece of retail real estate. �arring some abrupt resurgence in the popularity of karaoke products, this downward spiral is destined to continue for the near term.

There is however, a core karaoke software market, roughly �0 percent, that is sold to serious singers, largely through the specialized MI distribution channel. This market remains largely stable.

0

20

40

60

80

100

120

140

160

180

'06'05'04'03'02'01'00'99'98'97

Karaoke Machines

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'06'05'04'03'02'01'00'99'98'97

Ret

ail V

alue

in $

mill

ions

Uni

ts x

1,0

00

Retail Value Units

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'06'05'04'03'02'01'00'99'98'97

Uni

ts x

1,0

00

,00

0

Import Value Units

2006 Summary10-Year Trend

Retail Unit Average Price-24.81% -54.37%-11.74% -26.96%

64.77%20.83%

0

5

10

15

20

25

30

35