2008 global assignment policies and practices (gapp) survey tax international executive services

TRANSCRIPT

2008 Global Assignment Policies and Practices (GAPP) Survey

TAX

INTERNATIONAL EXECUTIVE SERVICES

2

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials.

3

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Objectives

• To explore current issues in international assignment management

• Discuss and review the results from KPMG’s International Assignment Policy and Practices Survey

• Consider the potential applicability of these concepts within your own organization

4

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

With You Today

• John McLearie, Principal, KPMG• Jeannette Wistner, Senior Manager, KPMG

5

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Agenda

• 2008 Global Assignment Practices and Policies Survey− Background− Participants− Benchmarking and Surveys

• Issues in international assignment management− Expatriate Return on Investment (ROI)− In Your opinion− Family Issues− Tax policy & tax equalization− Home leave− Housing IssuesHousing Issues− Wills and estate planningWills and estate planning− In Your opinionIn Your opinion

6

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Background and Participants

• Survey is dynamic• More than 400 multinational companies participated

over the past 5 years• Results are frozen as of February 2008• Divided into three broad categories:

− Organization Profile

− Program Profile

− Policy

• Real-time information is available at www.kpmglink.com

7

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Program Demographics of the Survey Participants

501 to 1,0005%

More than 1,000

8%

Fewer than 1020%

10 to 5033%

51 to 10012%

101 to 2009%

201 to 50013%

How many assignees does your organization have?

8

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008:Benchmarking and Surveys

• Appropriate comparisons:− Company location

− Size

− Industry

• Integrity of data:− Age

− Methodology

− Input error

− Interpretations

− Multiple policies

9© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Expatriate Return on Investment (ROI)

10

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

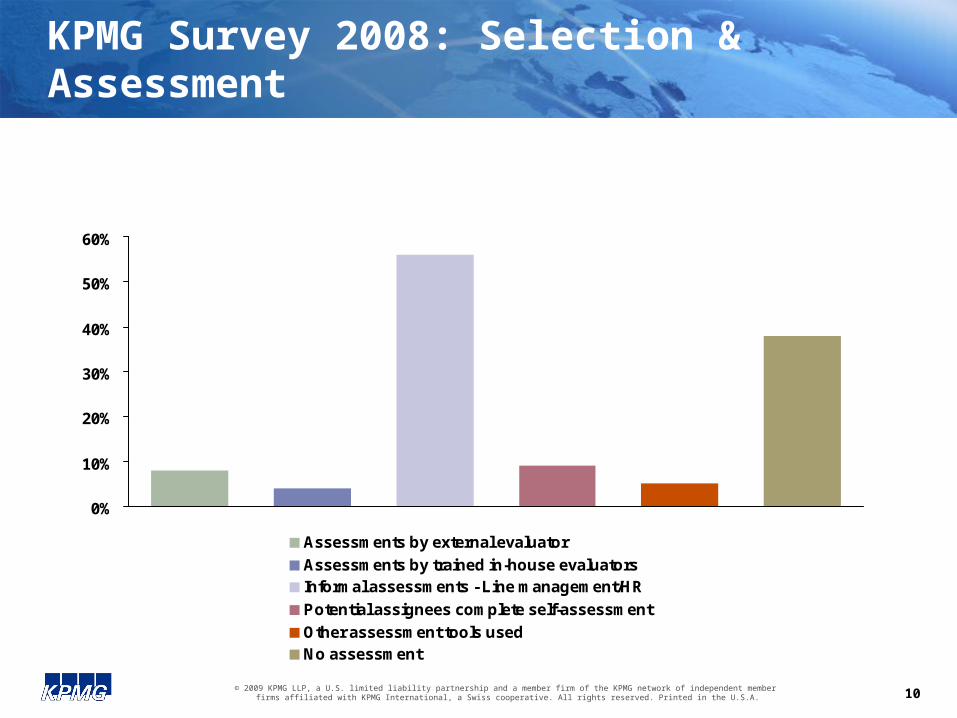

KPMG Survey 2008: Selection & Assessment

0%

10%

20%

30%

40%

50%

60%

Assessments by external evaluator

Assessments by trained in-house evaluatorsInformal assessments - Line management/HR

Potential assignees complete self-assessment

Other assessment tools usedNo assessment

Which statement best describes your approach to assessing a potential assignee's suitability?

11

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Selection & Assessment

• Pool of candidates− Performance review / self nominating

− Data base

• Assessment− “I know Jane. She’ll do a good job.”

• Primary factors in the selection of most assignees by managers are: − Work experience

− Technical skills

12

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

• According to advocates of selection and assessment methodologies, assignment success factors are:− Flexibility/adaptability

− Cross-cultural skills (language, sensitivity, open-mindedness)

− Strong family relationships

• How are business managers convinced of the importance of the “soft factors?”

• Risk that business managers may not ‘buy in” to validity of selection methodology or vendors and therefore may not accept the results

KPMG Survey 2008: Selection & Assessment (Con’t.)KPMG Survey 2008: Selection & Assessment (Con’t.)

13

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Selection and Retention

• Succession planning− Train locals

− Expatriate position

• Repatriation / career planning− ROI versus OOSOOM*

− Integration of assignments into career plan / performance management process

− Collaboration with Organizational Development group

*out of sight out of mind*out of sight out of mind

14

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

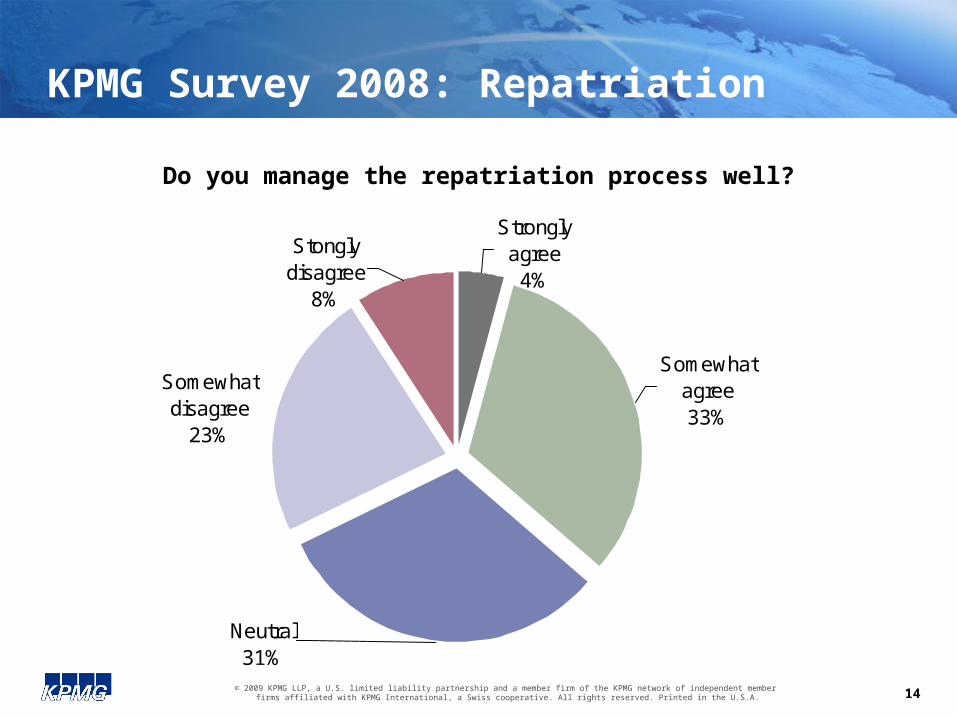

KPMG Survey 2008: Repatriation

Strongly agree

4%

Somewhat agree33%

Neutral31%

Somewhat disagree

23%

Stongly disagree

8%

Do you manage the repatriation process well?

15

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Assignment Success

0%

5%

10%

15%

20%

25%

30%

35%

40%

No appropriate job available in the home countryLocal employee compensation perceived as insufficientFamily issuesDifficulty in adjusting to local employee statusOffered a better job/career in another organizationOtherDo not know

The main reason assignees terminate after repatriation

16

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

In Your Opinion

In your opinion:

• Do assignees take too much time to administer?• Are assignees over-compensated?

17

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: In Your Opinion

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

...are over-compensated ...take too much administration

Yes No

In Your Opinion, Assignees...

18© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Family Issues

19

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Families

0%

10%

20%

30%

40%

50%

60%Unmarried domesticpartners/companions of oppositegender

Unmarried domesticpartners/companions of samegender

Dependent parents/extendedfamily of assignee

Other

None of the above

Does your organization include any of the following in its definition of family?

20

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Defining Families

• Strong social, cultural, and legal considerations− “Partners,” same- and opposite-sex

• Differing definitions of marriage

• Domestic partner legislation

• Non-discrimination requirements

• Visa/residency permit limitations

• Also complex:− Dependent parents and extended families

− Step-children, children from previous marriages, children-not-at-post

21

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Families

0%

5%

10%

15%

20%

25%

30%

35%

40% Allowance or payment that must be usedfor designated expenses

Allowance or payment for any expense

Job search assistance at host country

Work Visa assistance at host country

Reimbursement of education expenses

Partial financial compensation for lostsalary

Full financial compensation for lostsalary

Other

None of the above

Does your organization provide any assistance to accompanying spouses/partners?

22

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Trailing Spouses

• Limited menu of options available− Money can only do so much

• Challenges− Visas and work permits

− Transferability of licenses and certificates

− Loss of place on the corporate ladder

− Loss of practice (clients) that takes years to build (lawyers, doctors, accountants, etc.)

• If a spouse interrupts a rewarding career, will resentment result?

23© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Home Leave

24

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Home Leave

Do not provide6%

Free to go wherever

47%

Required to go to headquarters

country4%

Required to go to home country

42%

Which of the following best describes your organization’s home leave policy?

25

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Home Leave

• Trend toward laissez-faire and/or lump-sum administrative approach

• Upside: − Less administration and tracking

− Greater flexibility for assignees

• Downside: − Potential resentment from host locals regarding “company-paid

vacation”; confusion of purpose

− Missed opportunity for repatriation planning

− Missed potential opportunity for cost savings

26© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Taxes

27

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Taxes

Which statement best describes your approach to tax costs related to the assignee's earnings?

Assignees pay tax on base &

IC, organization pays tax on IA compensation

6%

Laissez-faire9%

Other3%

Tax Protect8%

Tax Equalize74%

28

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Tax Equalization Versus Tax Protection

• Tax Equalization: Assignee pays no more or no less than approximate home country burden

• Tax Protection: Assignee pays no more than home country burden; might pay less

• Differentiators− Assignee mobility

− Equity among locations

− Cost effectiveness to the organization

− Fairness to the employee

− Cost, effort, and complexity of the process

29© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Housing

30

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Housing

Do you deduct a housing norm?

No- we never withhold

39%

Issue treated on a case-by-

case basis8%

Yes- in all minority cases

4%

Yes- in most cases with

rare or specific

exceptions23%

Yes- in all cases26%

31

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Home Housing Norm

• Elements:− Interest on a mortgage (not principal!)

− Utilities

− Property taxes

− Repairs (roofs, windows, boilers, pools, fences, etc.)

− Maintenance

− Common charges

• Less common among non-US multinationals

• Do you want to determine “actual costs”?

32

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

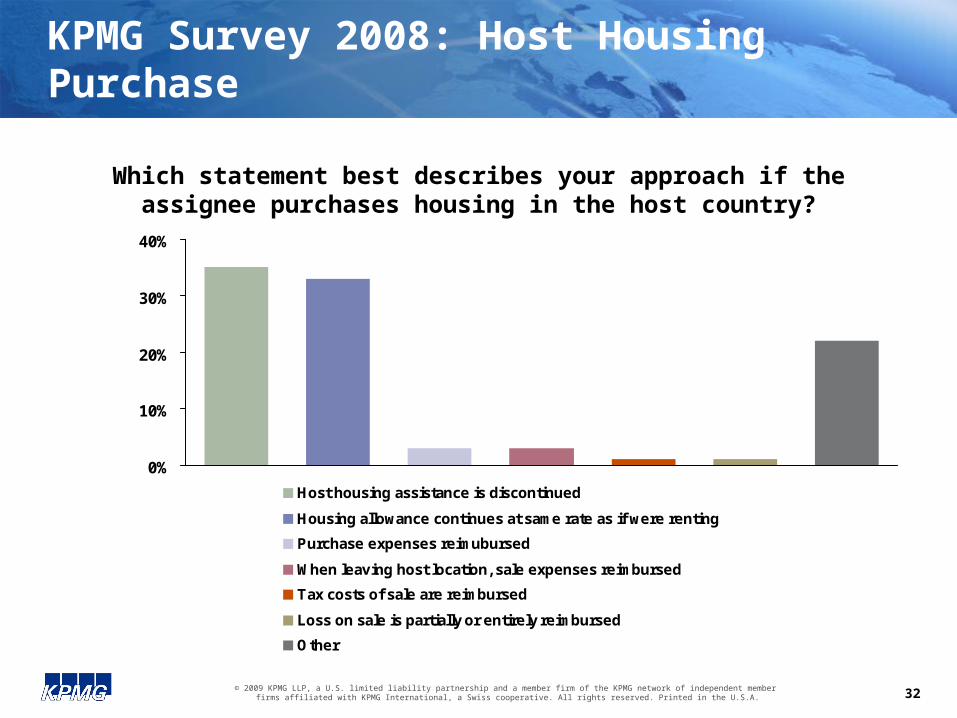

KPMG Survey 2008: Host Housing Purchase

0%

10%

20%

30%

40%

Host housing assistance is discontinued

Housing allowance continues at same rate as if were renting

Purchase expenses reimubursed

When leaving host location, sale expenses reimbursed

Tax costs of sale are reimbursed

Loss on sale is partially or entirely reimbursed

Other

Which statement best describes your approach if the assignee purchases housing in the host country?

33

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Host Housing Purchase

• Short-term financial impact for the employer: minimal

• Long-term: potential for large negative impact− Inequitable treatment of employees

− Loss of mobility

− Capital gains and exchange rate gain and loss issues

− Financial risks to both employees and employers

34© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Will Preparation

35

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: Will Preparation/Review

Other3%

Assignee is informed and organization

reimburses all costs 2%

Assignee is informed and organization

reimburses cost to predetermined limit

6%

Assignee is informed, but organization does

not pay for costs36%

Issue is not addressed; assignee not informed

53%

Which statement best describes your organization’s approach to the preparation of wills?

36

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Wills and Estate Planning

• Assignees may be at greater risk of life and health when on assignment

− Increased stress

− Lower standard of health facilities in many parts of the world, and (often) inability to communicate with medical professionals in their native tongue

− Terrorism and economic targeting (e.g., kidnap and ransom)

− Driving on “the wrong side” of the road

• Rules change when you cross borders (state and national)

− Taxes

− Disposition of estate

− Custody of children

• To whom will the grieving spouse turn to for help?

37

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

In Your Opinion

• In your opinion

• How frequently will assignees be used in five years?− Considerably less

− Somewhat less

− About the same

− Somewhat more

− Considerably more

38

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

KPMG Survey 2008: In Your Opinion

How frequently will assignees be used in 5 years?

Considerably more10%

Somewhat more30%

About the same44%

Somewhat less11%

Considerably less5%

39

© 2009 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. Printed in the U.S.A.

Contact Information

John McLeariePrincipalInternational Executive ServicesKPMG LLP(714) [email protected]

Jeannette WistnerSenior ManagerInternational Executive ServicesKPMG LLP(714) [email protected]