2011 annual ifta business meeting virginia beach, virginia

TRANSCRIPT

Annual IFTA Business Meeting August 2011 Page 1 of 11

2011 Annual IFTA Business Meeting

Virginia Beach, Virginia August 16 – 17, 2011

Call to Order Mr. Scott Greenawalt (OK), IFTA, Inc. Board of Trustees (Board) President, called the meeting to order and welcomed everyone to the business meeting. The Virginia Beach Police Department Honor Guard presented the colors of the United States and Canada as well as those of Virginia. Following the singing of the National Anthems by Ms. MaryAnn Rayment (VA), Mr. Greenawalt introduced the Honorable Sean T. Connaughton, Virginia Secretary of Transportation. Welcome The Honorable Sean Connaughton welcomed the delegates of the 18th Annual IFTA Business Meeting on behalf of Virginia Governor Bob McDonnell. As Secretary, Mr. Connaughton oversees seven state agencies with more than 9,700 employees and combined annual budgets of $5 billion. Prior to joining the McDonnell administration, he served as Corporate Vice President, Government Affairs for the American Bureau of Shipping, one of the world's leading ship and marine classification societies. Secretary Connaughton explained the large military and naval presence in the area and reminded everyone of why flags were flying at half-mast. He asked for a moment of silence for those who died in a recent helicopter crash. Many were members of a Navy SEAL team based in the area. Secretary Connaughton thanked the membership for coming to Virginia. Roll Call Mrs. Tammy Trinker (IFTA, Inc.), Events Coordinator, called the roll of the membership. Following the roll call, Mrs. Trinker announced a quorum of the membership was present to conduct the business of the association. Fifty-three (53) jurisdictions were present either in person or by proxy. President’s Report Mr. Greenawalt gave the President’s report. The focus of his report was the importance of jurisdiction participation in the activities of the membership through participation on the Standing and Special Committees. He recognized eight (8) jurisdictions that participate on four (4) or more committees: Indiana, Nevada, Kansas, Kentucky, Missouri, North Carolina, Saskatchewan, and Virginia. He thanked each of these jurisdictions for their commitment to the membership and the association. He stated that sixteen (16) jurisdictions do not participate on any committees or on the Board. He stated that IFTA, Inc. is a living and breathing association and stressed the importance of getting involved to show and share ideas. IFTA, Inc. Strategic Plan Mr. Hester presented an update on the IFTA, Inc. strategic plan. He reviewed several projects that were underway or had been completed to meet the goals of the association. Some of these projects are webinars for the clearinghouse and audit, developing a complete history of IFTA,

Annual IFTA Business Meeting August 2011 Page 2 of 11

combined training opportunities with IRP, developing a commissioner training, quality control reviews of the clearinghouse data, the development of electronic reviews and the establishment of the Re-Audit and Re-Examination Working Group. Approval of the 2010 Minutes Mr. Greenawalt asked for changes or corrections to the minutes of the 2010 Annual IFTA Business Meeting. Hearing none, Mr. Greenawalt asked for a motion to approve. Motion: Mr. James Poe (IN) moved to accept the minutes as written. Mr. Roland Marr (IL) seconded. The motion passed with no opposition. Election Committee Report and Board Election Chair of the Election Committee, Mrs. Platt presented this report. Each year, the Board president selects an Election Committee to seek nominations for election to the Board. Mrs. Platt reported that four (4) current Board members were seeking re-election: Mr. Greenawalt, Mr. Hester, Ms. Sheila Rowen (TN), and Mr. Stuart Zion (CO). Due to term limitations, Ms. Rena Hussey (VA) could not seek re-election. In order to meet the Bylaws requirement of a single board member region, the Election Committee sought a nominee from the Northeast Region. Mrs. Platt announced that Mr. Chuck Ulm (MD) was included in the slate of nominees with the four current Board members. Mrs. Platt then asked for nominations from the floor. Motion: Mr. Julian Fitzgerald (NC) moved to close the nominations. Mr. Bill Kron (MS) seconded. The motion passed without objection. Motion: Mr. Garry Hinkley (ME) moved to approve the nominations of Mr. Greenawalt, Mr. Hester, Ms. Rowen, Mr. Zion, and Mr. Ulm by acclamation. Mr. Gary Frohlick (SK) seconded. The motion passed without objection. Proposed Bylaws Changes Ms. Lonette Turner (IFTA, Inc.), Executive Director, presented a proposed amendment to the IFTA, Inc. Bylaws. The purpose of the proposed amendment was to change the provision that requires the Election Committee to follow a particular regional rotation for the single board member region. The problem arises when there are mid-term resignations. The proposed amendment would also require the Election Committee to determine the single board member region in a fair and equitable manner. Motion: Mr. Scott Bryer (NH) moved to accept the amendment to the IFTA, Inc. Bylaws. Ms. Hussey seconded the motion. The motion passed 51:7. Jurisdictions not voting were counted as dissenting votes. Clearinghouse Update Ms. Turner reported that there are fifty (50) full participating members and three (3) jurisdictions that have signed the non-participating member agreement to view transmittals and demographic data. For the 2010 funds netting year, IFTA, Inc. collected and distributed over $325,600,000 USD and nearly $2,600,000 CAD. Through the first six (6) clearinghouse transmittal periods of 2011, IFTA, Inc. had collected and distributed almost $180,000,000 USD and over $1,200,000 CAD.

Annual IFTA Business Meeting August 2011 Page 3 of 11

Ms. Turner showed a comparison of the first six (6) clearinghouse transmittal periods in 2010 to 2011. For those periods in 2010, IFTA, Inc. transmitted $159,971,156 USD. In 2011, the amount for the same time period was $179,927,949 USD. For those same periods, IFTA, Inc. transmitted $1,385,837 CAD in 2010 and $1,225,470 CAD in 2011. Ms. Turner stated that issues were faced during the implementation year. These issues included checks being inadvertently sent by the jurisdictions; payments not received timely resulting in two prorate periods; payments not received timely resulting in checks being required from a jurisdiction; other types of payments being sent to the funds netting accounts; and data not being uploaded timely. In 2011, the number of issues has reduced and it appears the funds netting process is working. Ms. Turner also reported that the AICPA had changed its requirements regarding SAS 70 audits. No longer are these types of audits being conducted for services such as those provided by the IFTA, Inc. Clearinghouse and funds netting processes. IFTA, Inc. will have an audit completed in which its auditors will utilize Statement of Standards for Attestation Engagements or SSAE 16. In an attestation report, a CPA attests to subject matter or an assertion about something other than the fairness of the presentation of financial statements. The SSAE 16 is applicable when an entity (like the member jurisdictions) outsources a business task or function to another entity (IFTA, Inc.) and the data resulting from that task or function is incorporated into financial statements. So, IFTA, Inc. is the service organization and the jurisdictions are known as user entities. Based on the review of these documents with IFTA, Inc. auditors, these requirements for IFTA, Inc. were identified. Establishing a Funds Netting System Timeliness of the Funds Netting Process Confidentiality Requirements Assignment of Clearinghouse Users Reporting to Jurisdictions Monitoring the Funds Netting Account and Tracking Funds Distribution of Funds Controls (security of data, backups, etc.)

The required description of the IFTA, Inc. funds netting system has been written and includes examples of each type of record kept. Ms. Turner also presented the new screens designed by Jason DeGraf (IFTA, Inc.), Information Systems Administrator. Program Compliance Review Update Mrs. Debora Meise (IFTA, Inc.), Program Director gave an update regarding program compliance reviews. No reviews are being conducted in 2011 due to the five-year review cycle. During 2011, the on-site review procedures were revised and the e-review procedures were written, the volunteer database was updated, preparations are underway for the 2012 reviews, assistance has been given to the Program Compliance Review Committee (PCRC) with revisions to the Review Guide, and training is being developed for e-review volunteers. In 2012, eleven (11) jurisdictions have elected to undergo e-reviews and 4 will be reviewed on-site.

Annual IFTA Business Meeting August 2011 Page 4 of 11

Membership was reminded of the requirement to participate in reviews. A list of all volunteer jurisdictions is maintained at IFTA, Inc. If jurisdictions do not participate on a review they could be found out of compliance when their jurisdiction is reviewed. Committee Reports Agreement Procedures Committee Mrs. Cindy Arnold (NV), Chair of the Agreement Procedures Committee (APC) presented a list of the APC members and reported on the activities of the committee since the 2010 ABM: the committee hosted the 2010 IFTA Managers’ and Law Enforcement Workshop, has held monthly teleconferences, has reviewed the 2011 ballots, and the committee ballot sponsored in 2010 passed and was effective July 1, 2011. On the APC’s action item list are reviewing the Best Practices Guide, its charter, the committee member terms and a new APC Member Guide. Mrs. Arnold then reviewed the agenda for this year’s workshop. Clearinghouse Advisory Committee Mr. Kron, Chair of the Clearinghouse Advisory Committee (CAC) reported on the committee’s activities and announced the committee members. The CAC holds monthly teleconferences which include an update from the Information Technology Advisory Committee (ITAC) and review of enhancement requests. Two subcommittees were created this year; one for quality control review of the clearinghouse data and the other to establish the 2013 funds netting calendar for the Board’s approval. Richard L. Reeves IFTA Leadership Award The presentation of the 2011 Richard L. Reeves IFTA Leadership Award was made. Ms. Turner, Ms. Donna Burch (Ryder, Inc.), Mr. Dan Eisinger (Supervalu, Inc.), Chair of the Industry Advisory Committee (IAC), and Mr. Robert Pitcher (ATA), presented this unique award. This year’s recipient was Mr. Gary Frohlick (SK) who accepted the award graciously. Attorneys’ Section Steering Committee Ms. Carolee Johnstone (CA), Chair, gave the report of the Attorneys’ Section Steering Committee (ASSC). Ms. Johnstone reported that the ASSC members had contacted the member jurisdictions requesting they update their Jurisdiction Communication List to include a current legal contact. Several jurisdictions have done so. The committee is planning to create a newsletter for distribution to these contacts. The ASSC also plans to conduct two webinars in the near future. Additionally the committee hopes to hold another face-to-face meeting as it has been a few years since the last one. Audit Committee Mrs. Meise gave a report on behalf of the Audit Committee (AC) Chair, Ms. Dawn Lietz (NV). The AC is working with the IRP Audit Committee to organize the agenda for the 2012 IFTA / IRP Audit Workshop. The focus of the workshop will be “Auditing in the 21st Century”. The committee has created a subcommittee to review the Audit Manual; has conducted webinars with IRP; and has representatives serving on the ITAC and the Re-Audit and Re-Examination Working Group (RRWG). Mrs. Meise also reported that the Audit Committee has sponsored Full Track Preliminary Ballot Proposal (FTPBP) #2-2011 which is a proposed amendment to A310 and changes the term

Annual IFTA Business Meeting August 2011 Page 5 of 11

“registration” year to “license” year. During discussion a suggestion was made that a definition of license year be added to the Articles of Agreement to coincide with this proposed change. Motor Carrier Technology Demonstration Mrs. Hussey then announced the Motor Carrier Technology Demonstration. The Virginia Department of Motor Vehicles presented six (6) different stations. They provided “MO”, a mobile DMV office that provides driver and vehicle services. This gives the DMV the ability to journey out to remote locations and customers. There was also a vehicle weighing station. The DMV was also showing IRIS. This is an infrared inspection technology which identifies vehicles running with bad brakes and other problems such as under-inflated tires. A station was also set up so the attendees could look at the ARS – Automated Routing Service. This is a tool for oversize and overweight permits. Carriers can get these permits instantaneously on line. A review station was provided for the traffic crash database, an evaluation of road service. Registrants were also given the opportunity to review Virginia’s IFTA and IRP on-line services which includes tax reporting. CBI 62-11 Mr. Zion then presented CBI #62-11. The issues for interpretation were received by the Board from the jurisdiction of Connecticut. Connecticut was seeking clarification of language that was approved in Full Track Final Ballot Proposal (FTFBP) #2-2010. This language is effective July 1, 2013:

For a fleet based in a U.S. jurisdiction, interest shall be set at an annual rate of two (2) percentage points above the underpayment rate established under Section 6621(a)(2) of the Internal Revenue Code, adjusted on an annual basis on January 1 of each year. Interest shall accrue monthly at 1/12 this annual rate. The Repository shall notify Jurisdictions of the new rate by December 1.

Connecticut’s questions were:

1. Is it the Board’s interpretation that it (the Board) has the discretionary authority to assign the duty of calculating the interest rate?

Connecticut pointed out that Ballot #2-2010 does not establish who is responsible for determining the effective interest rate. Therefore, it would seem that the responsibility rests with each member jurisdiction. They also stated that the Bylaws of the International Fuel Tax Association, Inc. do not appear to provide for such authority to be exercised by the Board of Trustees. Article Four, Section One (1) of the Bylaws defines the General Powers of the Board of Trustees. The language is very general (“The affairs of IFTA, Inc. shall be managed by the Board”) and does not seem to include the calculation of an interest rate to be implemented by the member jurisdictions.

2. What consequences exist if the member jurisdictions are not notified on or before December 1? If the member jurisdictions are not notified timely, what is their obligation to impose the correct rate (there are provisions in Section P1120.300 which relieve jurisdictions from taking extraordinary measures to implement a change of tax rate when the rate is not reported timely)?

Annual IFTA Business Meeting August 2011 Page 6 of 11

3. How will interest be imposed, for example, in the following situation? The taxpayer is audited for the periods of October 1, 2010 through September 30, 2013. The audit is completed in late December 2013. Interest is being calculated through January 31, 2014.

Connecticut pointed out that under Article R1230 (effective 7/1/13), the effective rate for the year 2014 will be reported to the member jurisdictions on or before December 1, 2013. How will the member jurisdictions be able to program their systems properly to result in the correct calculation of the January 2014 interest? While the imposition of interest for a late filed first quarter 2014 return will likely have the correct interest application (the rate will have been known to the base jurisdiction on or before December 1 of the year preceding), the audit situation described above is entirely different. As to Question 1, the Board determined that its interpretation of the language from FTFBP #2-2010 would answer Connecticut’s first question. Based on that interpretation, the Board is making no assignment of duties. Therefore, this question is outside of the scope of this Proposed Consensus Board Interpretation. The proposed Consensus Board Interpretation stated:

The rate established by the language in FTFBP 2-2010, effective July 1, 2013, is clearly stated: “an annual rate of two (2) percentage points above the underpayment rate established under Section 6621(a)(2) of the Internal Revenue Code, adjusted on an annual basis on January 1 of each year. Per the current ballot language, IFTA, Inc. would notify the member jurisdictions, by December 1 of each year, of the calculated rate: the IRS underpayment rate + 2%. The ballot states: “Interest shall accrue monthly at 1/12 this annual rate.” The calculation for the monthly rate is the responsibility of each jurisdiction. The notification by IFTA, Inc. is provided as a convenience and does not relieve the jurisdictions from imposing the correct interest rate. The interest rate applies for the calendar year for all deficiencies. Several interest rates may be in effect successively during the period that an underpayment remains outstanding.

Following the presentation and discussion, Mr. Greenawalt asked for a motion to accept the Board’s interpretation of CBI 62-11. Motion: Mr. Hinkley moved to accept the proposed Consensus Board Interpretation. Mr. Julian Fitzgerald (NC) seconded the motion. A roll call vote was taken and the motion passed by a vote of 49 to 9. Jurisdictions not voting were counted as dissenting votes. Short Track Preliminary Ballot Proposal 4-2011 Mr. Zion presented Short Track Preliminary Ballot Proposal (STPBP) #4-2011. This ballot is sponsored by the Board and would remove the language approved in FTFBP #2-2011 which requires: “The Repository shall notify Jurisdictions of the new rate by December 1.”

Annual IFTA Business Meeting August 2011 Page 7 of 11

Motion: Ms. Hussey moved to accept STPBP 4-2011. Mr. Hinkley seconded the motion. Following a roll call vote the motion failed 27 to 31. Jurisdictions not voting were counted as dissenting votes. STPBP 4-2011 will not continue. Closed Session The second day of the business meeting started with a closed session for jurisdiction representatives only. The purpose of the closed session was for the presentation of the financial report and the discussion of a dues increase. Before the session was closed, a roll call was taken to ensure that a quorum was present to conduct the business of the association. Fifty-three (53) jurisdictions were present in person or by proxy. The session was then closed. During the closed session the following motions were made. Motion: Mr. Kron moved to accept the proposed dues increase as presented. Mrs. Hussey moved to second. A roll call vote was taken and the motion was defeated by a vote of 32 to 22. Jurisdictions not voting were counted as dissenting votes. Motion: Mr. Bryer moved to raise the dues to $18,000 per year beginning in fiscal year ending June 30, 2014. Mrs. Arnold seconded the motion. Following discussions, Mr. Bryer rescinded his motion and Mrs. Arnold withdrew her second. Motion: Ms. Kitty Decker (AZ) moved to increase the dues to $18,000 per year beginning in fiscal year ending June 30, 2014. Mr. Kron seconded the motion. Discussion followed this motion. Motion: Mr. Kron moved to table the motion by Ms. Decker. Mrs. Arnold seconded the motion. This motion passed with no opposition. Committee Reports Re-Audit and Re-Examination Working Group The open session resumed with Mr. Frohlick presenting reports on behalf of the RRWG and the Dispute Resolution Committee (DRC). Mr. Frohlick is the Chair of the RRWG and Vice Chair of the DRC. For the RRWG, Mr. Frohlick listed the committee members and reviewed the working group objectives. He stated that the committee has moved toward recommending that the “re-audit” and “re-examination” become part of a single audit process. The group will be drafting a ballot for next year and is currently reviewing the Board’s latest comments to the working group’s response to its charge. Dispute Resolution Committee For the Dispute Resolution Committee (DRC), Mr. Frohlick stated that there had been no disputes since the 2010 ABM. The committee is currently working on a charge from the Board. The Board gave the DRC six (6) action items to review. Three (3) have been completed and the committee continues to work on the other three (3). The remaining action items include the authority of the DRC and the Board and whether there should be an intermediate step by a third party. The committee continues to discuss whether that step is warranted.

Annual IFTA Business Meeting August 2011 Page 8 of 11

Industry Advisory Committee Mr. Eisinger presented the IAC report. He reported that the committee has had extensive discussions regarding the IFTA decals and would like to see them eliminated. He also reported that the IAC has an active role in the planning of the 2012 Audit Workshop. A representative of the committee will also attend the IFTA Managers’ and Law Enforcement Workshop. Information Technology Advisory Committee Mr. John Poole (TX), ITAC member, gave the committee report and listed the members of the committee. Mr. Poole reported that the committee continues its monthly conference calls and has also extensively used the committee message board to exchange information. The ITAC has completed its charge from the Board regarding investigating, analyzing and reporting on the current capabilities of GPS and other vehicle tracking systems as they apply to commercial trucking operations. A second charge has been received from the Board that asks the ITAC to provide the Audit Committee with support as it completes its review of the ITAC’s work product regarding vehicle tracking systems and proposed revisions to P600. A third charge asks the ITAC to identify and analyze existing motor carrier data information systems to determine whether there is a viable method to provide roadside law enforcement a snapshot of all pertinent data. Law Enforcement Committee Lt. Jennifer Brown (AZ), Chair, gave the Law Enforcement Committee (LEC) report. Lt. Brown stated that the committee continues its monthly conference calls. Due to committee member retirements, vacancies from the Northeast, Southeast, and Western regions need to be filled. She reported that more jurisdictions participated in the March and May (M&M) enforcement activities and that a database was developed by IFTA, Inc. to allow the LEC to collect enforcement statistics from these activities. The LEC co-sponsored a ballot with the Jurisdiction of Illinois. Full Track Preliminary Ballot Proposal 1-2011 Mr. Trent Knoles (IL), and a member of the LEC, presented FTPBP #1-2011 for discussion. This ballot proposes the addition of the issue date to the IFTA license. Mr. Knoles stated that there is a distinction between the issue date of the license and the effective date of the license. The membership discussed whether the issue date should be defined. During discussions it was explained that the issue date is important for roadside enforcement that could lead to a possible audit. Furthermore the issue date could affect post-violation actions such as possible waiving of a penalty assessment. Program Compliance Review Committee Mr. Jay Starling (AL), Past-Chair of the Program Compliance Review Committee (PCRC), presented this report on behalf of the current Chair, Mr. John Szilagyi (CT). The PCRC is recruiting for administrative representatives from two regions; Northeast and Southeast. Projects of the committee include reviewing the program, conference calls, a subcommittee with the APC to address electronic filing and its impact on the Agreement, and a face-to-face meeting regarding the impact of FTFBP 1-2009 and E-reviews. The committee has also updated the Program Compliance Review Guide to include and accommodate both on-site and electronic reviews (E-reviews). It was explained that the review process itself is not affected by these changes except for the initial jurisdiction review which will be revised from 90 to 120 days prior to the actual review.

Annual IFTA Business Meeting August 2011 Page 9 of 11

Mr. Greenawalt called for a vote to ratify the PCR Guide by a show of hands. With a vote of 49 in favor membership ratified the document. IFTA, Inc. Financial Report Following the committee reports, the discussions returned to the financial report. Discussions then returned to the membership dues increase. Motion: Ms. Platt moved to have the dues increase motion un-tabled. Mr. Doug Miller (MI) seconded the motion. The motion passed. Mr. Greenawalt asked for the motion to be restated. Motion: Ms. Kitty Decker (AZ) moved to increase the dues to $18,000 per year beginning in fiscal year ending June 30, 2014. Mr. Kron seconded the motion. Discussion followed this motion. Following a roll call vote the motion failed by a vote of 32 to 22. Jurisdictions not voting were counted as dissenting votes. Motion: Mr. Bryer moved to increase the membership dues to $17,000 beginning fiscal year ending June 30, 2014, including travel costs for the jurisdictions’ voting representative to attend the Annual IFTA Business Meeting. Mr. Bernie Meagher (NS) seconded this motion. Discussion was had regarding the trust of the Board in regards to inserting the travel expenses into the motion. It was explained that the additional wording would assist members in their travel requests. Following a roll call vote the motion passed by a vote of 40 to 16 with two jurisdictions abstaining. Jurisdictions not voting were counted as dissenting votes. 2012 Invitational Mr. Miller invited those in attendance to the 29th Annual IFTA Business Meeting in Grand Rapids, Michigan in 2012. The dates of this meeting have been set for July 18 – 19. THE IFTA NEWS will contain additional details about the business meeting throughout the coming year. Full Track Preliminary Ballot Proposal 3-2011 Mr. Meagher, Ms. Virginia Barnett (ON), and Ms. Angelina Leung (AB) presented FTPBP #3-2011 for discussion. This ballot proposes a pilot project for the sponsoring jurisdictions regarding number of audits completed. The number of audits completed would include, for the five-year pilot project period, compliance activities, roadside enforcement activities, and education and outreach activities. The purpose of the ballot is the recognition that enforcement, educational, and compliance efforts contribute toward audit coverage. During the pilot project, the jurisdictions would consult with the IAC and the LEC ensuring alternative measures are clearly defined, consistent and measurable. The pilot jurisdictions may apply alternative measures for up to 1% of audit coverage. The remaining 2% must be traditional audits. It was pointed out that in many jurisdictions, audit resources are allocated to higher risks, such as sales and use tax. It was also stated that audit alone is not the most efficient effort for compliance. In the pilot, the participants would calculate average hours per audit; specify alternative activities; and one hour of an alternative activity would equal one audit hour.

Annual IFTA Business Meeting August 2011 Page 10 of 11

Those in attendance offered feedback on the ballot. It was suggested that the sponsors should consider conducting a pilot project without including it in the governing documents. It was also suggested that such a pilot need not be limited to only the sponsors of this ballot proposal. It was further suggested that only those jurisdictions currently meeting the number of audits requirement should participate. IRP and IRP, Inc. Update Ms. Mary Pat Paris (IRP, Inc.), CEO, presented a report concerning the activities of IRP and IRP, Inc. There were 158 in attendance at the IRP Annual Meeting in May. The IRP, Inc. Board funded one person from each jurisdiction to attend. IRP is working with IFTA for the planning of the Managers’ and Law Enforcement Workshop. IRP conducted 20 webinars which included 1,500 participants. There were three (3) ballot proposals: full reciprocity, charter buses, and the audit manual rewrite. The charter bus ballot failed. IRP has many other activities and projects underway. FHwA Mr. Michael Dougherty, Program Analyst with the Federal Highway Administration (FHwA) gave a presentation that covered the Surface Transportation Program at the Federal level and the way that IFTA data factors into the apportionment of funds to the States. The presentation began with an overview of the current authorization (which is currently operating under an extension) and what is being proposed for the next program which would probably last about 5 years or so. The various taxes and fees that went into the Federal Highway Trust Fund (HTF) were explained and issues that are causing a reduction not only in the balance, but also future revenue were discussed. Included in the presentation was a description of what data is collected by FHwA, including IFTA gallons, and how it is used to compute the amount of fuel used on the highways in each state, so that there was a common basis for distributing funds from the HTF into several Federal programs. The presentation concluded with a review of the Congressional proposals to date for a new authorization, with some discussion as to how it may affect the reporting of IFTA data to the FHwA. Alternative to Decals Survey Mr. Hinkley presented the results of a survey taken of the membership regarding alternatives to decals. Forty-two jurisdictions responded, representing 170,000 accounts and 1.8 million decals. Twenty-eight jurisdictions suspend other credentials when IFTA decals are not displayed. If there was a reliable system available, twenty-three jurisdictions would give up decals. Only sixteen jurisdictions would be in favor of no decals for larger carriers only. United States / Mexican Motor Carrier Long-Haul Pilot Project Mr. Poole presented a report regarding the US/Mexico Cross-Border Long-Haul Pilot Program. Negotiations for this project began in March 2011. Applications are being accepted by FMCSA now from Mexican carriers. The pilot will last up to three (3) years. The IRP International Committee has established a subcommittee for this project. IFTA is participating. Two conference calls have been held and action items were established. New Business Items Mr. Marr announced that over the course of the following year Illinois would be contacting membership to address Agreement issues that have impacted the decisions made this year,

Annual IFTA Business Meeting August 2011 Page 11 of 11

specifically the issue of voting and jurisdictions not in attendance at the business meeting. It is the view of Illinois that those who opt not to attend the business meeting, or not provide a voting proxy, should not have an impact on the outcome of a vote. Adjournment Mr. Greenawalt thanked the staff of the Virginia Department of Motor Vehicles for all of their work toward making the meeting so successful. Concluding the business discussions of the organization Mr. Greenawalt asked for a motion to adjourn. Motion: Mr. Kron moved to adjourn the 28th Annual IFTA Business Meeting. Ms. Platt seconded the motion. The motion passed with no objections.

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 1 of 10

BYLAWS OF THE INTERNATIONAL FUEL TAX ASSOCIATION, INC.

An Arizona Nonprofit Corporation

Article One - Offices

The principal office of the International Fuel Tax Association, Inc. (hereinafter referred to

as “IFTA, Inc.”) in the State of Arizona is located in the City of Chandler, County of Maricopa.

IFTA, Inc. may have such other offices, either within or out of the State of Arizona as may be

necessary to conduct the business of the corporation. The principal office of IFTA, Inc. may be

changed from time to time in the manner provided in the Arizona Revised Statutes and without

amending the Articles of Incorporation.

Article Two - Membership

Section 1. Eligibility and Requirements. Membership in IFTA, Inc. shall be open to any

state of the United States of America, the District of Columbia, any province or territory of Canada

or a state of the United Mexican States. Any such entity desiring membership must submit an

application to IFTA, Inc. The application must be in accordance with Article XIV of the

International Fuel Tax Agreement (hereinafter referred to as the “Agreement”). All members must

pay the annual membership fee adopted at an annual meeting of IFTA, Inc. and required by the

Agreement. Continued membership in IFTA, Inc. is contingent upon compliance with all terms of

the Agreement.

Section 2. Expulsion. Any member failing to properly comply with the terms of the

Agreement may be expelled as provided in Article XV of the Agreement.

Section 3. Withdrawal. Any member may withdraw from IFTA, Inc. upon compliance

with Article XIV of the Agreement.

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 2 of 10

Article Three - General Membership Meetings

Section 1. Quorum. A two-thirds majority of the active member jurisdictions of IFTA, Inc.

shall constitute a quorum. A quorum is required to conduct the business of IFTA, Inc. at a

meeting of the members of the corporation. For the purposes of determining whether a quorum is

established, active member jurisdictions present and/or represented by proxy shall be considered

present at the meeting.

Section 2. Annual Meeting. An annual meeting of the members of IFTA, Inc. shall be

held once each year for the purpose of electing Trustees to the Board of Trustees (hereinafter

referred to as the “Board”) and for the transaction of such other business as may come before the

meeting. The annual meeting shall be held at such time and place as determined by the Board.

Section 3. Special Meetings. Special meetings of the members of IFTA, Inc. may be

called by the Board. Such meetings shall be held at such time and place as determined by the

Board.

Section 4. Notice of Meetings. Written notice stating the place, day, and hour of any

meeting of the members of IFTA, Inc. shall be delivered by mail to each member entitled to vote

at such meeting, not less than ten days before the date of such meeting. In the case of a special

meeting, the notice shall contain a statement of the purpose of the meeting. Notice shall be

deemed delivered on the date that same is deposited in the national post office of the country of

origin of the notice addressed to the members at the address last appearing in the records of

IFTA, Inc., with postage thereon prepaid.

Section 5. Voting Rights. Each active member jurisdiction of IFTA, Inc. shall be entitled

to one vote on each matter submitted to a vote of the members at a meeting, except for a vote to

elect Trustees to the Board, and on such votes each active member jurisdiction shall have one

vote for each Trustee to be elected. Each active member jurisdiction shall use all votes available

to it when electing Trustees, but may not use more than one vote for a single candidate. A simple

majority of active member jurisdictions is required to elect a trustee to the board. Each active

member jurisdiction may cast their vote by an authorized representative in person, or by proxy.

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 3 of 10

Article Four - Board of Trustees

Section 1. General Powers. The affairs of IFTA, Inc. shall be managed by the Board.

Section 2. Number and Tenure. There shall be nine Trustees on the Board. The term

of office for a Trustee shall be two years, with five Trustees elected in years ending in an odd

number and the other four Trustees elected in years ending in an even number, so as to provide

for staggered terms of the Trustees. No Trustee may serve more than three complete two-year

consecutive terms.

Section 3. Qualifications and Requirements. Any commissioner of a member

jurisdiction, or their designee, is eligible to serve as a Trustee. However, at least one Trustee

shall be from each of the five geographic regions outlined in these bylaws (see Appendix A). No

more than two trustees shall be from a single geographic region with the region represented by

one trustee rotating among the geographical regions in a fair and equitable manner. At least one

Trustee shall be a member where fuel taxes are administered by a tax or revenue department,

and at least one Trustee shall be a member where fuel taxes are administered by a department of

transportation or department of motor vehicles. At least one Trustee shall be a woman or

minority. A single Trustee on the Board may satisfy more than one criterion.

Section 4. Regular Meetings. The Board shall meet each calendar quarter unless the

President of IFTA, Inc. determines otherwise. These meetings shall be at such times and at such

places as designated by the President of IFTA, Inc.

The first regular annual meeting of the Board shall be the second meeting of the Board

held after the annual meeting of IFTA, Inc. The purpose of this meeting will be to elect officers of

IFTA, Inc., in addition to such other business as may come before the Board at said meeting.

The Board may provide by resolution for the time and place of the regular annual meeting and

such additional regular meetings of the Board necessary to manage the business of IFTA, Inc.

without any notice other than such resolution.

Section 5. Special Meetings. Special meetings of the Board may be called by the

President of IFTA, Inc. The time and place of special meetings shall be fixed by the President,

and if desirable, may be held via teleconference and/or e-mail.

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 4 of 10

Section 6. Notice. Notice of any special meeting of the Board shall be given at least two

days prior to the meeting if sent via facsimile or e-mail, or seven days prior if sent via the national

post office of the country of origin of the notice. Notice shall be deemed delivered on the day of

the facsimile or e-mail transmission or the day same is deposited in the mail with prepaid

postage. Any Trustee may waive notice of a meeting. The attendance of a Trustee at a meeting

shall constitute a waiver of notice of such meeting, unless said Trustee appears solely to object to

the transaction of business at the meeting due to improper notice and also refuses to take part in

any of the business transacted at such meeting because of the improper notice.

Section 7. Quorum. A two-thirds majority of the Trustees shall constitute a quorum for

the transaction of business at any meeting of the Board; but, if less than a two-thirds majority of

the Trustees are present at a meeting, a majority of the Trustees present may adjourn the

meeting from time to time without providing any further notice of said meeting.

Any one or more members of the Board may participate in a meeting of the Board by

means of conference telephone or similar communications equipment by means of which all

persons participating in the meeting can communicate with each other, and participation in a

meeting by such means shall constitute presence in person at such meeting.

Section 8. Voting Rights. Each Trustee shall have one vote.

Section 9. Manner of Acting. Except as otherwise provided in these bylaws, the act of a

two-thirds majority of the Trustees shall be the act of the Board. A Trustee present at a meeting

of the Board at which action on any matter of IFTA, Inc. is taken shall be presumed to have

assented to the action unless a dissent is entered in the minutes of the meeting, or unless a

dissent has been filed with the Executive Director of IFTA, Inc. No Trustee who votes in favor of

any action may file a dissent or have same entered in the minutes of the meeting.

Section 10. Vacancies

Full Term Vacancies - The President of IFTA, Inc. shall direct that nominations be sought

from member jurisdictions for election to the Board. Nominations including those of trustees

wishing re-election may be made prior to the annual meeting or from the floor at the Annual

Business Meeting.

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 5 of 10

The President of IFTA Inc. shall each year establish an Election Committee consisting of

the Trustees whose terms are not expiring. The Election Committee shall select a Chair. The

duties of this committee are to ensure the Qualifications and Requirements set forth in Article

Four, Section 3 herein are met, to ensure equitable geographic representation is maintained and

to conduct the election at the Annual Business Meeting.

All nominees for the Board of Trustees will be voted upon by the member jurisdictions at

the Annual Business meeting.

Mid-term Vacancies - Any mid-term vacancy occurring on the Board shall be filled by

nominations from jurisdictions in the regions in which the vacancy occurred. Nominations shall

be received within 20 days of being solicited and commissioners from all member jurisdictions will

have a further 20 days to vote. If only one nominee is received by the nomination deadline, the

Board of Trustees may accept the nominee by acclamation. The nominees receiving the most

votes or being named by acclamation will take a seat on the Board of Trustees effective with the

next scheduled Board of Trustees meeting. A Trustee elected to fill a vacancy shall serve the

unexpired term of his or her predecessor Trustee provided the vacancy occurred in the last 18

months of the term being vacated. A Trustee elected to fill a vacancy which occurred in the first

six months of the vacated term will be considered to be serving her/his first two year term.

To expedite the replacement of mid-term vacancies, nominations and elections will be

conducted using electronic means.

Section 11 Standing Committees. No member of the Board shall serve as the chair,

vice-chair, or as a member of a Standing Committee established by the International Fuel Tax

Agreement.

Section 12. Resignation. A Trustee who misses is absent from two consecutive board

meetings shall have deemed to have resigned from the Board unless an absence is excused by a

majority of the Board. A Trustee who has so resigned may be reappointed in accordance with

Section 10 of this Article.

Article Five - Officers

Section 1. Titles and Duties. The officers of IFTA, Inc. shall be the President, the First

Vice-President, the Second Vice-President, and the Secretary/Treasurer. The President shall be

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 6 of 10

the principal executive officer of IFTA, Inc. The President shall preside at all meetings. The

President shall prepare and present an annual report of the work of IFTA, Inc. to the members at

the annual meeting. The President shall see that all books, reports, and certificates required by

law are properly kept or filed. The President shall have such other powers that may be

reasonably necessary to the performance of the office. The First Vice-President, the Second

Vice-President, and the Secretary/Treasurer shall perform such duties as the President may from

time to time assign or delegate to them.

Section 2. Election and Term of Office. The President, First Vice-President, and the

Second Vice-President shall be elected by majority vote of the Trustees. Only Trustees shall be

eligible to be President, First Vice-President, and the Second Vice-President. The Executive

Director of IFTA, Inc. shall be appointed by the Board to serve as Secretary/Treasurer. The

Executive Director of IFTA, Inc. shall be an ex officio member of the Board with no voting rights.

The President, First Vice-President, and the Second Vice-President shall serve a one year term,

but may serve more than one term. The Secretary/Treasurer shall serve as long as that person

remains Executive Director of IFTA, Inc.

Section 3. Vacancies. Should the office of President become vacant, the First Vice-

President shall fill the vacancy. Should the office of First Vice-President become vacant, the

Second Vice-President shall fill the vacancy. A vacancy in the office of Second Vice-President

shall be filled by a two-thirds majority vote of the remaining Trustees. Should the office of

Secretary/Treasurer become vacant, the Board shall appoint the incoming Executive Director of

IFTA, Inc. to fill the vacancy. Officers who fill vacancies shall serve the unexpired portion of the

term of the predecessor in that office.

Section 4. Resignation. The President, First Vice-President, and Second Vice-President

may resign from the office without having to resign from the Board.

Section 5. Compensation. The President, First Vice-President, and Second Vice-

President shall not, by virtue of the office, be entitled to receive any salary or compensation from

IFTA, Inc., but nothing shall be construed to prevent any officer from receiving reimbursement for

any expenses incurred on behalf of IFTA, Inc. The Secretary/Treasurer shall not be entitled to

any compensation from IFTA, Inc. by virtue of the office, other than that paid as salary and

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 7 of 10

benefits to the Executive Director of IFTA, Inc. No reimbursement for expenses shall be paid to

the President, First Vice-President, and the Second Vice-President unless approved by the Board

by a two-thirds majority vote. No reimbursement for expenses shall be paid to the

Secretary/Treasurer unless approved by a majority of the Executive Committee.

Article Six – Committees Section 1. Executive Committee. The President, First Vice-President, and Second Vice-

President shall constitute the Executive Committee. The Executive Committee shall have such

powers and duties as assigned to it by a two-thirds majority vote of the Trustees.

Section 2. Agreement Procedures Committee. The Agreement Procedures Committee

shall have the responsibility of maintaining the Articles of Agreement and the Procedures Manual,

and such other responsibilities assigned to it by the Board. In discharging these responsibilities,

the Agreement Procedures Committee shall seek input from the Audit Committee, Law

Enforcement Committee, Program Compliance Review Committee, and the Industry Advisory

Committee. The President, with the approval of the Board, shall appoint an Agreement

Procedures Committee Chair. The chair shall select the committee members to serve on the

Agreement Procedures Committee, subject to approval by the Board. The committee members

shall be selected from the membership of IFTA, Inc.

Section 3. Audit Committee. The Audit Committee has the responsibility for the Audit

Manual, and such other responsibilities assigned to it by the Board. In discharging these

responsibilities, the Audit Committee shall seek input from the Agreement Procedures

Committee, Law Enforcement Committee, Program Compliance Review Committee, and the

Industry Advisory Committee. The President, with the approval of the Board, shall appoint an

Audit Committee Chair. The Chair shall select the committee members to serve on the Audit

Committee, subject to approval by the Board. The committee members shall be selected from

the membership of IFTA, Inc.

Section 4. Industry Advisory Committee. The Industry Advisory Committee has the

responsibility of advising the Agreement Procedures Committee, Audit Committee, Law

Enforcement Committee, and Program Compliance Review Committee, as well as such other

responsibilities assigned to it by the Board. The President, with the approval of the Board, shall

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 8 of 10

appoint an Industry Advisory Committee Chair. The Chair shall select the committee members to

serve on the Industry Advisory Committee, subject to approval by the Board. The committee

members shall be selected from the Industry representatives who have expressed an interest in

working with the Board.

Section 5. Law Enforcement Committee. The Law Enforcement Committee has the

responsibility of advising the IFTA membership regarding law enforcement matters, and such

other responsibilities as specified in the International Fuel Tax Agreement or assigned to it by the

Board. In discharging these responsibilities, the Law Enforcement Committee shall seek input

from the Agreement Procedures Committee, the Audit Committee, the Program Compliance

Review Committee, and the Industry Advisory Committee. The President, with the approval of

the Board shall appoint a Law Enforcement Committee Chair. The Chair shall select the

committee members to serve on the Law Enforcement Committee, subject to approval by the

Board. The committee members shall be selected from the membership of IFTA, Inc.

Section 6. Program Compliance Review Committee. The Program Compliance

Committee has the responsibility of maintaining the IFTA Program Compliance Review Guide,

establishing and maintaining a pool of qualified individuals to conduct compliance reviews,

reviewing all program compliance review reports to determine any needs for reassessment, to

make findings of compliance or non-compliance, and such other responsibilities as specified in

the International Fuel Tax Agreement or assigned to them by the Board. In discharging these

responsibilities, the Program Compliance Review Committee shall seek input from the Agreement

Procedures Committee, the Audit Committee, the Law Enforcement Committee, and the Industry

Advisory Committee. The President, with the approval of the Board, shall appoint a Program

Compliance Review Committee Chair. The Chair shall select the committee members to serve

on the Program Compliance Review Committee, subject to approval by the Board. The

committee members shall be selected from the members of IFTA, Inc.

Section 7. Dispute Resolution Committee. The Dispute Resolution Committee has the

responsibility for hearing disputes pursuant to the IFTA Dispute Resolution Process. The Dispute

Resolution Committee facilitates dispute resolution in a fair, impartial, effective, and expeditious

manner. The President, with the approval of the Board shall appoint a Dispute Resolution

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 9 of 10

Committee Chair. The Chair shall select the committee members to serve on the Dispute

Resolution Committee, subject to approval by the Board. The committee members shall be

selected from the members of IFTA, Inc. and the Industry Advisory Committee as set forth in the

Dispute Resolution Committee Charter approved by the Board.

Section 8. Other Committees. The President, with the approval of the Board, may

establish such other committees as from time to time are deemed necessary or desirable, and

may, with the approval of the Board, appoint Chairs to such Committees.

Article Seven - Employees

The Board may hire and fix the compensation and fringe benefits of any and all

employees which they may, in their discretion, determine to be necessary to conduct the

business of IFTA, Inc.

Article Eight - Contracts, Loans, Checks, and Deposits

Section 1. Contracts. The Board may authorize any officer to enter into any contract or

execute and deliver any instrument in the name of and on behalf of IFTA, Inc. and such authority

may be general or confined to specific instances.

Section 2. Loans. No loans shall be contracted on behalf of IFTA, Inc. and no evidence

of indebtedness shall be issued in its name unless authorized by the Board. Such authority may

be general or confined to specific instances.

Section 3. Checks, Drafts, etc. All checks, drafts or other orders for the payment of

money, notes, or other evidences of indebtedness issued in the name of IFTA, Inc. shall be

signed by such officers or agents of the corporation and in such manner as shall from time to time

be determined by the Board.

Section 4. Deposits. All funds of IFTA, Inc. not otherwise employed shall be deposited

from time to time to the credit of the corporation in such banks, trust companies, or other

depositories as the Board may select.

Article Nine - Definitions and Waiver of Notice

Section 1. Definitions. Except as provided by Article Three – Section 5, when the term

majority is used in these bylaws it shall mean a two-thirds majority of the active member

jurisdictions when referring to votes of members or a two-thirds majority of the Trustees, unless

IFTA, Inc. Bylaws Proposed Amendment for 2012 Annual Business Meeting

July 2012 Page 10 of 10

otherwise specified, when referring to votes on the Board. Any other terms used in these bylaws,

not defined herein, shall have the same meaning as provided in the Agreement if the terms are

defined therein.

Section 2. Waiver of Notice. When any notice is required to be given under these

bylaws, a waiver thereof, in writing, signed by the member or Trustee entitled to such notice,

whether before or after the time stated therein, shall be deemed equivalent to the giving of proper

notice.

FOR DISCUSSION AT THE ANNUAL IFTA BUSINESS MEETING

IFTA Full Track Preliminary Ballot Proposal #01-2012

February 1, 2012 Page 1 of 3

IFTA FULL TRACK PRELIMINARY BALLOT PROPOSAL

#01-2012 Sponsor IFTA Agreement Procedures Committee IFTA Program Compliance Review Committee Date Submitted January 17, 2012 Proposed Effective Date January 1, 2014 Manual Sections to be Amended (January 1996 Version, Effective July 1, 1998, as revised) IFTA Procedures Manual P700 Standard Tax Returns Subject To clarify the requirements for filing an IFTA Tax Return. History/Digest As technology advances, requests from licensees to file their quarterly IFTA tax returns online have increased. Jurisdictions have increasingly accommodated licensees in this regard; some even requiring what licensees file online. It was determined that P700 does not adequately address what is required to be included or captured. Therefore, the IFTA Agreement Procedures Committee and the IFTA Program Compliance Review Committee formed a subcommittee, the Electronic Filing Subcommittee to ballot language that would provide guidance and consistency among the jurisdictions, regarding data elements that shall be captured on IFTA tax returns. Intent The intent of this ballot is to provide an update to the IFTA Procedures Manual to include the necessary requirements for filing an IFTA tax return, regardless of the manner filed.

IFTA Full Track Preliminary Ballot Proposal #01-2012

February 1, 2012 Page 2 of 3

Interlining Indicates Deletion; Underlining Indicates Addition P700 STANDARD TAX RETURNS 1 2 The data elements listed in P720 are to be data captured regardless of the method of completion of the 3 tax return (manually, electronically prepared or electronically prepared and filed) and must be provided on 4 the appropriate transmittal. 5 6 {SECTIONS P710 AND P730 REMAIN UNCHANGED} 7 8 *P720 REQUIRED INFORMATION 9 10 Each jurisdiction shall use a standard tax return that shall contain, but not be limited to, the elements 11

listed below: 12 13 .050 Name and mailing address of the jurisdiction issuing the tax return; 14 15 .100 A space for the IFTA license number of the licensee; 16 17 .150 A space for the Name and address of the licensee; 18 19 .200 A space for the Tax reporting period of the tax return; 20 21 .250 A space for the Total distance traveled in all jurisdictions during the tax reporting period, 22

including operations with trip permit; 23 24 .300 A space for Total fuel consumed in all jurisdictions during the tax reporting period; 25 26 .350 A space for the Average fuel consumption factor (to two decimal places) for the tax reporting 27

period; 28 29 .400 A space for the Fuel type(s) consumed during the tax reporting period; 30 31 .450 Columns for the jurisdictions in the Agreement; 32 33 .500 Columns for reporting for each jurisdiction in order (with rounding provided to the nearest 34

whole unit); 35 36 .010 Tax rate; 37 38 .015 Total miles or kilometers; 39 40 .020 Total taxable miles or kilometers; 41 42 .025 Taxable gallons or liters; 43 44 .030 Tax paid gallons or liters; 45 46 .035 Net taxable gallons or liters; 47 48 .040 Tax due; 49 50

IFTA Full Track Preliminary Ballot Proposal #01-2012

February 1, 2012 Page 3 of 3

.045 Interest due; and 51 52 .050 Total due; 53 54 .550 Totals for the columns that are listed under P720.500 with the exception of 55

P720.500.010 and P720.500.045; 56 57 .600 A space for Penalty or late filings fees ($50.00 or 10 percent of the tax, whichever is greater); 58 59 .650 A space for the Total remittance of the tax return; 60 61 .700 A space for the Date of the submitted tax return; 62 63 .750 A space for the Signature of the person filing the licensee’s tax return, unless the licensee 64

is filing electronically in accordance with R940.300 and P160. 65 66 .800 A space for the Title of the person filing the licensee's tax return; and 67 68 .850 A space for the Telephone number of the person filing the licensee's tax return. 69 70 A space for previous balances may be included. 71 72 73

NO REVISIONS FOLLOWING THE FIRST COMMENT PERIOD

FTPBP #1-2012 First Comment Period Ending May 16, 2012

FTPBP #1-2012 First Comment Period Ending May 16, 2012 Page 1 of 5

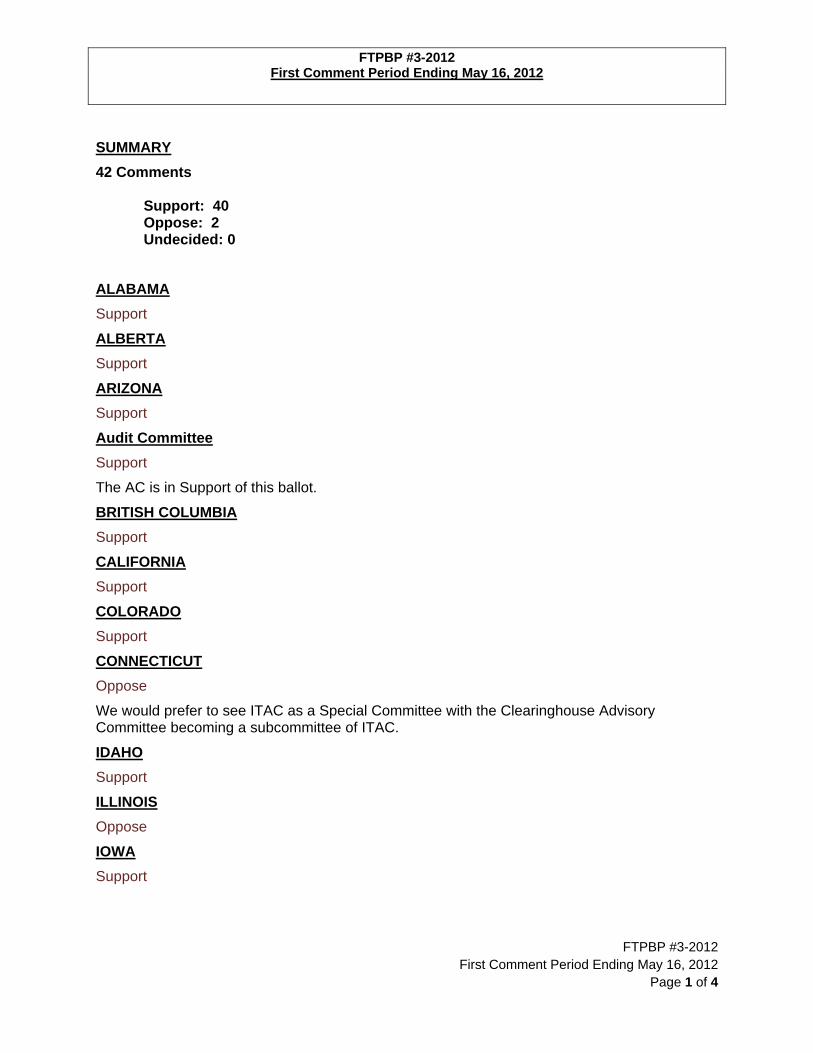

SUMMARY

42 Comments

Support: 34 Oppose: 3 Undecided: 5

ALABAMA

Support

ALBERTA

Undecided

Alberta has some concerns. Our online system currently captures the demographic information at the registration stage, eg, who can file the return, their name, phone number and email address, etc. Each filer is assigned an ID so that we will know who actually files the return. Redesigning a return for electronic filing that contains information we already obtain at our registration stage may cause us problems.

ARIZONA

Support

Audit Committee

Undecided

The AC Supports the intent of this ballot but is concerned that the removal of providing “A space for the….” will change the meaning of P720 and will require each jurisdiction to “pre-populate” all of the data fields. This is not possible as it would require the jurisdiction to fill in information that it does not have like “total distance traveled” etc. Recommend revising the language to remove “Each jurisdiction shall use” from the Required Information in P720 to read, “A standard tax return shall contain, but not be limited to, the elements listed below.”

BRITISH COLUMBIA

Support

BC Supports the ballot but finds the wording confusing/problematic and would suggest the following.

P700 – A standard tax return shall contain the elements listed in P720 regardless of how the tax return (e.g., manually or electronically) is prepared and filed. These elements must also be provided on the appropriate transmittal.

Unrelated but another suggestion within P720:

“P720.550 – Totals for the columns that are listed under P720.500 with the exception of P720.500.010, P720.500.035; and P720.500.045.”

There appears to be no value in carriers calculating the total “net taxable gallons or liters” for all jurisdictions.

FTPBP #1-2012 First Comment Period Ending May 16, 2012

FTPBP #1-2012 First Comment Period Ending May 16, 2012 Page 2 of 5

CALIFORNIA

Support

COLORADO

Support

CONNECTICUT

Support

IDAHO

Support

ILLINOIS

Undecided

IOWA

Support

KANSAS

Support

Kansas Supports this ballot our paper and electronic filed returns already capture all the needed data. We would also like to suggest that e-mail addresses and total interest column may be included as an optional field.

MAINE

Support

MANITOBA

Support

MARYLAND

Support

MASSACHUSETTS

Support

MICHIGAN

Support

Language subject to changes

MINNESOTA

Undecided

Minnesota is unsure of the unintended consequences of the proposal. The concern is “data captured” . The paper tax return contains the base jurisdiction name and address, an

FTPBP #1-2012 First Comment Period Ending May 16, 2012

FTPBP #1-2012 First Comment Period Ending May 16, 2012 Page 3 of 5

electronically filed tax return does not capture the base jurisdiction name and address. The P700 Proposal states the data “must be provided on the appropriate transmittal.” This appears to be a change to the transmittal data as currently the transmittal data does not capture the items in P700.750,P720.800, and P700.850.

MISSOURI

Support

Missouri's MCE system captures the required information at our common customer and IFTA fleet levels, however, it does not capture the information on the tax return if it is filed online. Missouri has approximately 1600 customers, per quarter, that file via paper.

MONTANA3

Support

NEBRASKA

Oppose

Nebraska has some concerns regarding the language used in this ballot. To state that the "data elements listed in P720 are to be data captured....." poses a problem in our view. IF the term 'data captured' implies that the carrier is keying in this data or that the on-line process somehow stores this data per tax return - we would have problems with that. For example, while we do have our jurisdicton name and address printed on the paper tax return - we do not store nor do we capture that information on an electronically filed tax return.

NEVADA

Oppose

Nevada would like the language changed in P720 to state "A standard tax return that shall capture, but not be limited to, the elements listed below" to remove the responsibility of the jurisdiction from providing the elements on the tax return. The former language simply required 'a space' for each element. Additionally, R950 should be changed from 'a standard tax return form that contains...' to 'a standard tax return that captures...' since the intent of the ballot was to move to the electronic world. Nevada does not want the tax returns to be required to be pre-printed.

NEW BRUNSWICK

Support

NEW HAMPSHIRE

Support

NEW JERSEY

Support

NEW MEXICO

Support

FTPBP #1-2012 First Comment Period Ending May 16, 2012

FTPBP #1-2012 First Comment Period Ending May 16, 2012 Page 4 of 5

NEW YORK

Oppose

New York feels that the language does not reflect what the intent of this ballot.

NORTH CAROLINA

Support

NORTH DAKOTA

Undecided

NOVA SCOTIA

Support

OHIO

Support

ONTARIO

Support

Ontario Supports the proposed language as it provides guidance and consistency among the jurisdictions regarding data elements to be captured on IFTA tax returns.

PENNSYLVANIA

Support

PRINCE EDWARD ISLAND

Support

QUEBEC

Support

SASKATCHEWAN

Support

TEXAS

Support

Suggest this ballot also delete P720.550 requiring totals for each column on the return. Having a total for each column should be optional.

UTAH

Support

VERMONT

Support

VIRGINIA

Support

FTPBP #1-2012 First Comment Period Ending May 16, 2012

FTPBP #1-2012 First Comment Period Ending May 16, 2012 Page 5 of 5

WEST VIRGINIA

Support

WYOMING

Support

FOR DISCUSSION AT THE ANNUAL IFTA BUSINESS MEETING

IFTA Full Track Preliminary Ballot Proposal #02-2012

February 1, 2012 Page 1 of 3

IFTA FULL TRACK PRELIMINARY BALLOT PROPOSAL

#02-2012 Sponsor Jurisdiction of Colorado Date Submitted January 31, 2012 Proposed Effective Date July 1, 2013 Manual Sections to be Amended (January 1996 Version, Effective July 1, 1998, as revised) IFTA Articles of Agreement R1200 ASSESSMENT AND COLLECTION R1230.100 US Jurisdiction Interest Rate Subject An amendment to the US jurisdiction interest rate. History/Digest IFTA Full Track Ballot #02-2010 established an interest rate of 2% above the IRS rate. Intent The intent of this ballot is to amend the IFTA Articles of Agreement to minimize the number of interest rate changes from year to year for minor fluctuations in the IRS rate and to make it easier for the carrier to calculate interest on a monthly basis. The ballot would establish a monthly interest rate for the year based on the IRS interest rate from the prior year. Example:

IRS rate IFTA monthly rate 0% - 3% 0.25% or 0.0025 3.1% - 6% 0.5% or 0.005 6.1% - 9% 0.75% or 0.0075 9.1% - 12% 1.0% or 0.01 12.1% - 15% 1.25% or 0.0125 15.1% - 18% 1.5% or 0.015 18.1% - 21% 1.75% or 0.0175 21.1% - 24% 2% or 0.02

IFTA Full Track Preliminary Ballot Proposal #2-2012

February 1, 2012 Page 2 of 3

Interlining Indicates Deletion; Underlining Indicates Addition ARTICLES OF AGREEMENT 1 R1200 ASSESSMENT AND COLLECTION 2 3 [SECTIONS R1210 AND R1220 REMAIN UNCHANGED] 4 5 *R1230 INTEREST 6 7

The base jurisdiction, for itself and on behalf of the other jurisdictions, shall assess interest on all 8 delinquent taxes due each jurisdiction except taxes collected directly by other jurisdictions in 9 accordance with IFTA Procedures Manual Sections P1000 and P1120.300. 10

11 .100 U.S. Jurisdiction Interest Rate 12

13 For a fleet based in a U.S. jurisdiction, interest shall be set at an annual monthly rate of 14 two (2) percentage points above as specified below, based on the underpayment rate 15 established under Section 6621(a)(2) of the Internal Revenue Code, adjusted on an 16 annual basis on January 1 of each year. Interest shall accrue monthly at 1/12 this annual 17 rate. The Repository shall notify Jurisdictions of the new rate by December 1. 18 (Emphasis added.) 19 20 Interest shall accrue at a rate of one forth of a percent per month if the underpayment rate 21 established under Section 6621(a)(2) of the Internal Revenue Code is equal to or greater 22 than zero percent and equal to or less than three percent. 23 24 Interest shall accrue at a rate of one half of a percent per month if the underpayment rate 25 established under Section 6621(a)(2) of the Internal Revenue Code is greater than three 26 percent and equal to or less than six percent. 27 28 Interest shall accrue at a rate of three forth of a percent per month if the underpayment 29 rate established under Section 6621(a)(2) of the Internal Revenue Code is greater than 30 six percent and equal to or less than nine percent. 31 32 Interest shall accrue at a rate of one percent per month if the underpayment rate 33 established under Section 6621(a)(2) of the Internal Revenue Code is greater than nine 34 percent and equal to or less than twelve percent. 35 36 Interest shall accrue at a rate of one and one forth of a percent per month if the 37 underpayment rate established under Section 6621(a)(2) of the Internal Revenue Code is 38 greater than twelve percent and equal to or less than fifteen percent 39 40 Interest shall accrue at a rate of one and one half of a percent per month if the 41 underpayment rate established under Section 6621(a)(2) of the Internal Revenue Code is 42 greater than fifteen percent and equal to or less than eighteen percent 43 44 Interest shall accrue at a rate of one and three forth of a percent per month if the 45 underpayment rate established under Section 6621(a)(2) of the Internal Revenue Code is 46 greater than eighteen percent and equal to or less than twenty one percent 47 48 Interest shall accrue at a rate of two percent per month if the underpayment rate 49 established under Section 6621(a)(2) of the Internal Revenue Code is greater than twenty 50 one percent and equal to or less than twenty four percent 51

52 [SECTIONS R1230.200 THROUGH R1230.400 REMAIN UNCHANGED53

IFTA Full Track Preliminary Ballot Proposal #02-2012

February 1, 2012 Page 3 of 3

NO REVISIONS FOLLOWING THE FIRST COMMENT PERIOD

FTPBP #2-2012 First Comment Period Ending May 16, 2012

FTPBP #2-2012 First Comment Period Ending May 16, 2012 Page 1 of 4

SUMMARY

41 Comments Support: 4 Oppose: 17 Undecided: 20

ALABAMA

Oppose

ALBERTA

Undecided

The ballot does not affect a Canadian jurisdiction.

ARIZONA

Oppose

Audit Committee

Undecided

The AC has no comment on this ballot.

BRITISH COLUMBIA

Undecided

CALIFORNIA

Oppose

CONNECTICUT

Oppose

We Oppose this ballot. This is consistent with our belief that there are still unanswered constitutional questions associated with IFTA imposing an interest rate.

IDAHO

Support

ILLINOIS

Undecided

IOWA

Oppose

FTPBP #2-2012 First Comment Period Ending May 16, 2012

FTPBP #2-2012 First Comment Period Ending May 16, 2012 Page 2 of 4

KANSAS

Undecided

Kansas is Undecided; We agree these formulas would make it easier on most carriers to calculate the interest.

MAINE

Oppose

MANITOBA

Undecided

Same comment as Nova Scotia.

MARYLAND

Undecided

MASSACHUSETTS

Oppose

MICHIGAN

Undecided

Still evaluating proposal

MINNESOTA

Oppose

Minnesota stand remains as with the prior interest ballot proposal. We question the legal authority of IFTA imposing an interest rate, interest rates are set by the governing body not the administrative body. In addition the new language is complex and confusing.

MISSOURI

Undecided

Missouri is interested in ABM discussions.

MONTANA

Undecided

Uncertain what variations of the IRS rates will do when assessing audits.

NEBRASKA

Support

If there were a "neutral" category when commenting on ballots - Nebraska's position would be neutral. Although we agree there may be some minor changes in the interest rate from year to year - who cares. Jurisdicictions will have to be able to handle interest rate changes in their IFTA systems whether that rate changes annually or every few years. It is true that this ballot would likely result in less changes -

FTPBP #2-2012 First Comment Period Ending May 16, 2012

FTPBP #2-2012 First Comment Period Ending May 16, 2012 Page 3 of 4

NEVADA

Support

NEW BRUNSWICK

Undecided

NEW HAMPSHIRE

Oppose

NEW JERSEY

Support

NEW MEXICO

Oppose

NEW YORK

Oppose

New York feels this ballot needs to be amended for clarification and simplification.

NORTH CAROLINA

Oppose

NORTH DAKOTA

Undecided

NOVA SCOTIA

Undecided

This ballot does not apply to Canadian jurisdictions as we are covered under R1230.200.

OHIO

Oppose

ONTARIO

Undecided

As a Canadian jurisdiction, Ontario is not subject to the same interest provisions. However, we have concerns whether the complexity of the language helps to simplify the requirement. We are not quite sure how this will be of benefit to the U.S. jurisdictions.

PENNSYLVANIA

Undecided

PRINCE EDWARD ISLAND

Undecided

Agree with Nova Scotia's comment.

FTPBP #2-2012 First Comment Period Ending May 16, 2012

FTPBP #2-2012 First Comment Period Ending May 16, 2012 Page 4 of 4

QUEBEC

Undecided

Same comment as Nova Scotia.

SASKATCHEWAN

Undecided

SK has no position on this issue

TEXAS

Oppose

UTAH

Oppose

VERMONT

Oppose

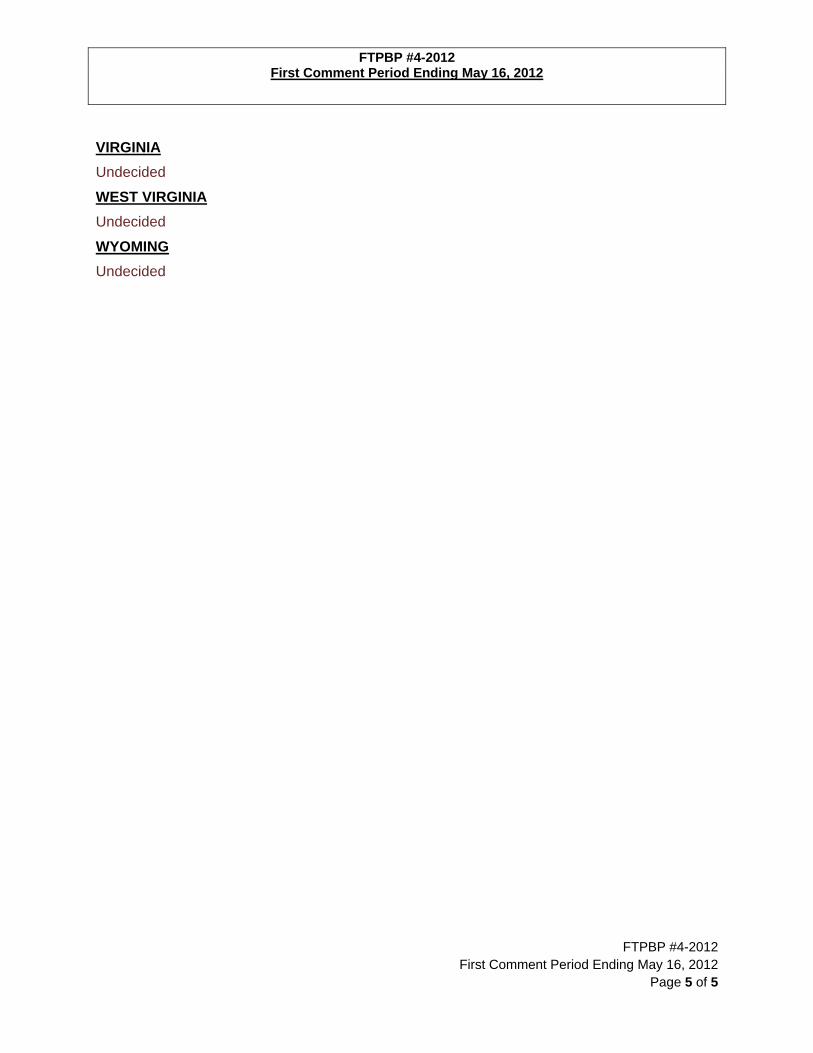

VIRGINIA

Undecided

WEST VIRGINIA

Oppose

WYOMING

Undecided

FOR DISCUSSION AT THE ANNUAL IFTA BUSINESS MEETING

IFTA Full Track Preliminary Ballot Proposal #03-2012

February 1, 2012 Page 1 of 2

IFTA FULL TRACK PRELIMINARY BALLOT PROPOSAL

#03-2012 Sponsor IFTA, Inc. Board of Trustees Date Submitted February 1, 2012 Proposed Effective Date Upon Passage Manual Sections to be Amended (January 1996 Version, Eff. July 1, 1998, as revised) IFTA Articles of Agreement R1800 Administration R1810 International Fuel Tax Association, Inc. Subject Establishing the Information Technology Advisory Committee (ITAC) as a Standing Committee History/Digest The ITAC was established as a special committee in 2006 by the International Fuel Tax Association, Inc. (IFTA, Inc.) Board of Trustees (Board). The ITAC was to review information technology solutions proposed by IFTA, Inc. information technology (IT) staff to determine if they meet the needs of the IFTA user community. The purpose of the ITAC is to identify user needs and recommend IT proposals to the Board. The ITAC works to enhance information technology capabilities of the IFTA, Inc. and its stakeholders involved in the administration of the IFTA. Additionally, the ITAC is responsible for serving as a technical source for membership, maintaining a committee member rotation chart, recruiting members and maintaining a list of potential committee members, and making recommendations to the Board to fill committee vacancies. Intent The intent of this ballot is to create the Information Technology Advisory Committee as a standing committee of the International Fuel Tax Agreement.

IFTA Full Track Preliminary Ballot Proposal #03-2012

February 1, 2012 Page 2 of 2

Interlining Indicates Deletion; Underlining Indicates Addition 1 ARTICLES OF AGREEMENT 2 3 R1800 ADMINISTRATION 4 5 *R1810 INTERNATIONAL FUEL TAX ASSOCIATION, INC. 6 7 [SECTION .100 REMAINS UNCHANGED] 8 9 [SECTIONS .200.010 THROUGH .070 REMAIN UNCHANGED] 10 11

.080 Information Technology Advisory Committee 12 13

There is established an Information Technology Advisory Committee to provide technical 14 guidance as well as recommendations to identify user needs and IT proposals. 15 16 17

[SECTIONS .300, .400 AND .500 REMAIN UNCHANGED] 18 19 20

NO REVISIONS FOLLOWING THE FIRST COMMENT PERIOD

FTPBP #3-2012 First Comment Period Ending May 16, 2012

FTPBP #3-2012 First Comment Period Ending May 16, 2012 Page 1 of 4

SUMMARY

42 Comments Support: 40 Oppose: 2 Undecided: 0

ALABAMA

Support

ALBERTA

Support

ARIZONA

Support

Audit Committee

Support

The AC is in Support of this ballot.

BRITISH COLUMBIA

Support

CALIFORNIA

Support

COLORADO

Support

CONNECTICUT

Oppose

We would prefer to see ITAC as a Special Committee with the Clearinghouse Advisory Committee becoming a subcommittee of ITAC.

IDAHO

Support

ILLINOIS

Oppose

IOWA

Support

FTPBP #3-2012 First Comment Period Ending May 16, 2012

FTPBP #3-2012 First Comment Period Ending May 16, 2012 Page 2 of 4

KANSAS

Support

Kansas Supports this ballot; ITAC will continue to have projects etc. to do with the growing technology changes happening every day to help keep IFTA working toward the future and changes that will need to be made to the agreement etc.

MAINE

Support

The ITAC is a valuable resource. It is logical to make this committee a standing committee.

MANITOBA

Support

MARYLAND

Support

MASSACHUSETTS

Support

MICHIGAN

Support

MINNESOTA

Support

Establishing the Information Technology Advisory Committee as a standing committee makes sense and consistent with the other standing committees.

MISSOURI

Support

MONTANA

Support

NEBRASKA

Support

NEVADA

Support

NEW BRUNSWICK

Support

NEW HAMPSHIRE

Support

FTPBP #3-2012 First Comment Period Ending May 16, 2012

FTPBP #3-2012 First Comment Period Ending May 16, 2012 Page 3 of 4

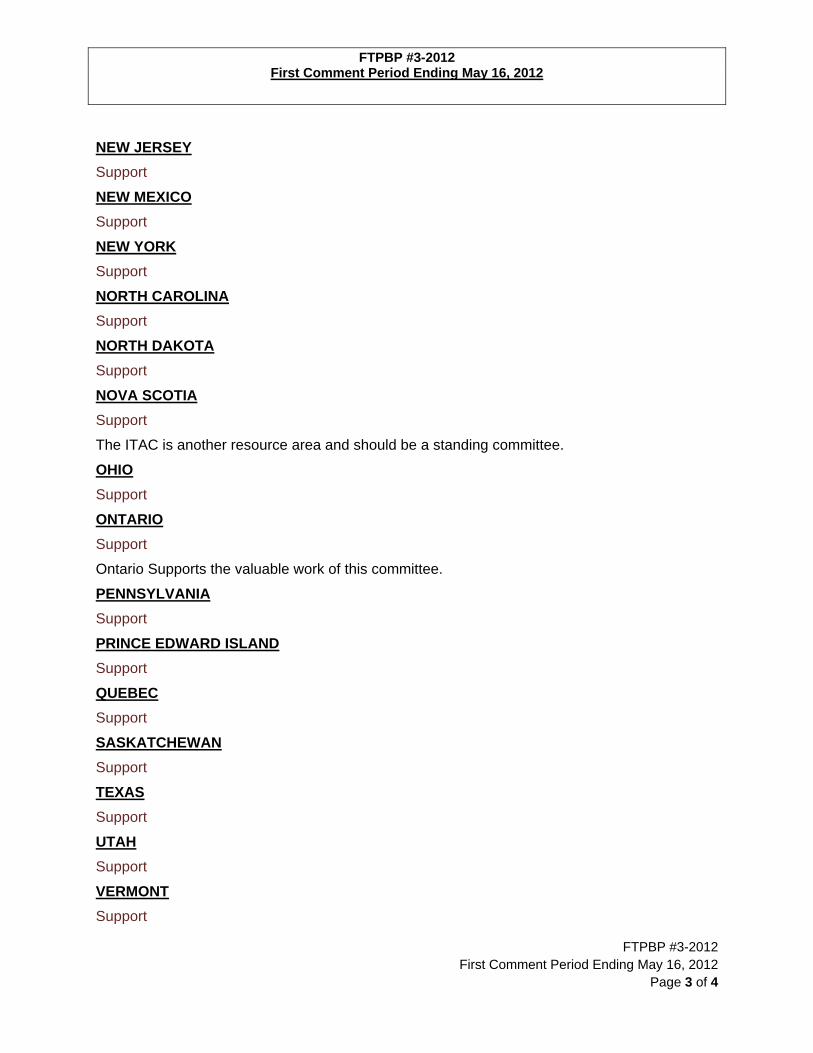

NEW JERSEY

Support

NEW MEXICO

Support

NEW YORK

Support

NORTH CAROLINA

Support

NORTH DAKOTA

Support

NOVA SCOTIA

Support

The ITAC is another resource area and should be a standing committee.

OHIO

Support

ONTARIO

Support

Ontario Supports the valuable work of this committee.

PENNSYLVANIA

Support

PRINCE EDWARD ISLAND

Support

QUEBEC

Support

SASKATCHEWAN

Support

TEXAS

Support

UTAH

Support

VERMONT

Support

FTPBP #3-2012 First Comment Period Ending May 16, 2012

FTPBP #3-2012 First Comment Period Ending May 16, 2012 Page 4 of 4

VIRGINIA

Support

WEST VIRGINIA

Support

WYOMING

Support

FOR DISCUSSION AT THE ANNUAL IFTA BUSINESS MEETING

IFTA Full Track Preliminary Ballot Proposal #4-2012

February 24, 2012 Page 1 of 3

IFTA FULL TRACK PRELIMINARY BALLOT PROPOSAL

#4-2012 Sponsor Jurisdiction of Alabama Date Submitted February 14, 2012 Proposed Effective Date January 1, 2013 Manual Sections to be Amended (September 2011 Version, Effective July 1, 1998, as revised) Articles of Agreement R245 - Qualified Motor Vehicle Subject Qualified Motor Vehicle Definition History/Digest Section R245 of the IFTA Articles of Agreement defines a Qualified Motor Vehicle as a motor vehicle used, designed, or maintained for transportation of persons or property and:

Having two axles and a gross vehicle weight or registered gross vehicle weight exceeding 26,000 pounds or 11,797 kilograms; or

Having three or more axles regardless of weight; or Is used in combination, when the weight of such combination exceeds 26,000 pounds or 11,797