2011 federal tax update real estate & investment 1

TRANSCRIPT

2011 Federal Tax Update

Real Estate & Investment

1

© 2011 Vern Hoven Tax Seminars

3-1

2

New!

Real Estate Tax News

•Landlord’s 1099 reporting repealed▫Repeal retroactive to 1/1/11

•TIGTA tells IRS to audit more rentals▫53% of landlords misreport income▫$12b of unreported income▫IRS agrees to audit more rental activities

•Passive loss Form 8582 instructions to be revised

© 2011 Vern Hoven Tax Seminars

3-2

3

© 2011 Vern Hoven Tax Seminars

3-3

4

First Time Homebuyer Credit Update

•2008 Credit payback began in 2010•IRS sending reminder letters•Reminder: Allowed for purchases

through April, 2011 for▫Extended duty military▫Foreign service▫Intelligence community workers

© 2011 Vern Hoven Tax Seminars

3-4

5

The $250,000/$500,000 MFJ Exclusion Rule

3-5

6© 2011 Vern Hoven Tax Seminars

The Exclusion Rule!

•$250,000 (or $500,000 if married filing joint) of gain is excluded on sale (or exchange) of principal residence if:

1.Owned for two of last five years,2.Occupied for two of last five years, and3.No sale in last two years

3-5

7© 2011 Vern Hoven Tax Seminars

How to Exclude $500,000!

•Either spouse owns 2 out of 5 years•Both spouses use 2 out of 5 years•Neither spouse excluded gain in last 2 yrs•Must file “Married Filing Joint”

3-6

8

Is this Jessie?

© 2011 Vern Hoven Tax Seminars

Surviving Spouse May Qualify for $500,000 Exclusion•$500,000 exclusions applies if▫After 12/31/07▫Sale within 2 years of death of spouse▫Immediately prior to death

Either spouse owned 2 out of 5 years Both spouses used 2 out of 5 years Neither spouse excluded gain in last 2 yrs

3-6

9

Is this Jessie?

© 2011 Vern Hoven Tax Seminars

Recent Court Cases

•50% owner gets 100% of exclusion (Hsu)•Divided court says must live in house to

qualify for exclusion (Gates)

3-7

10

Is this Jessie?

© 2011 Vern Hoven Tax Seminars

No Exclusion for Prior Non-Qualified Use•Substantial limitation on vacation homes•Gain must be prorated, S/L for qualified

& non-qualified time•Non-qualified: time not principal

residence•Non-qualified time doesn’t include:▫After use as principal residence before sale ▫Temporary absence (up to two years)

3-8

11© 2011 Vern Hoven Tax Seminars

Example: Rent 2 yrs; Use 3 yrs

12

3-8

Sales Price $700,000

Purchase Price 400,000

Accumulated Dep. -20,000 $380,000

Gain $320,000

Dep. Recapture $20,000

Non-Qualified Use; 2/5 $120,000

Qualified Use: 3/5 $180,000

© 2011 Vern Hoven Tax Seminars

Example: Rent after Personal Use

13

3-8

Sales Price $600,000

Purchase Price 400,000

Accumulated Dep. -20,000 $380,000

Gain $220,000

Dep. Recapture $20,000

Non-Qual. Use: 2/12 N/A

Qualified Use: 10/12 $200,000

© 2011 Vern Hoven Tax Seminars

Example: Gain Before 2009

14

3-9

Sales Price $300,000

Purchase Price (7/1/05) 100,000

Accumulated Dep. -20,000 $80,000

Gain $220,000

Dep. Recapture $20,000

Pre-2009 Alloc. 3.5/8.5 $82,353

Qualified Use; 3/8.5 $70,588

Non-Qual. Use: 2/8.5 $47,059

© 2011 Vern Hoven Tax Seminars

Qualification for The “Reduced Exclusion” Rule•Homeowner Violates:▫2 Year Ownership Rule, or▫2 Year Use Rule, or▫Only Once in Last 2-year rule

•Because of:▫Change in Place of Employment▫Health, or▫IRS’s “Unforeseen Circumstances”

3-9

15© 2011 Vern Hoven Tax Seminars

Converting Residence to Rental

•Can you convert a personal residence to a rental property? Yes!•But watch out –•Basis is the lower of cost or FMV at date of

conversion•Losses resulting prior to rental are not

deductible

3-10

16© 2011 Vern Hoven Tax Seminars

3-10

17© 2011 Vern Hoven Tax Seminars

Foreclosures on the Rise

•Nevada, Arizona, California &Florida still leading the way▫(RealtyTrac.com)

•More than 1,000,000 foreclosures in 2010

3-

18© 2011 Vern Hoven Tax Seminars

COD Exceptions

1. Excluded by law, e.g., gifts & bequests2. Qualified student loan COD3. Cancelled debt would have been

deductible4. Qualified purchase price reduction

© 2011 Vern Hoven Tax Seminars

3-11

19

COD Exclusions

1. Qualified principal residence debt2. Bankruptcy COD3. Insolvency COD4. Qualified Farm COD5. Qualified real property business COD

© 2011 Vern Hoven Tax Seminars

3-11

20

Foreclosure Results in COD

•Reduction in debt taxable as ordinary income▫Form 1099-A (foreclosure sale), but not

needed if foreclosure and COD in same year▫Form 1099-C (loan reduced)

3-12

21© 2011 Vern Hoven Tax Seminars

Mortgage Modification

1. Foreclosures2. Deed in lieu3. Mortgage workout

3-12

22© 2011 Vern Hoven Tax Seminars

Foreclosure Results in COD

•Foreclosure▫Even a forced

sale is a taxable sale

3-12

23© 2011 Vern Hoven Tax Seminars

Nonrecourse vs. Recourse Debt

•Nonrecourse debt (not personally liable)•Recourse debt (personally liable)

3-12

24© 2011 Vern Hoven Tax Seminars

Foreclosure of Nonrecourse Debt

•Sales price = nonrecourse debt▫Result: No COD

•Home acquisition debt in 14 states often non-recourse (CA, MT)▫But, be careful! A refinance changes status

of debt

3-13

25© 2011 Vern Hoven Tax Seminars

Foreclosure of Nonrecourse Debt

$600,000Adjusted Basis

($50,000) LossForeclosure Gain (Loss)

$550,000Sales Proceeds (Debt)

26

3-13

© 2011 Vern Hoven Tax Seminars

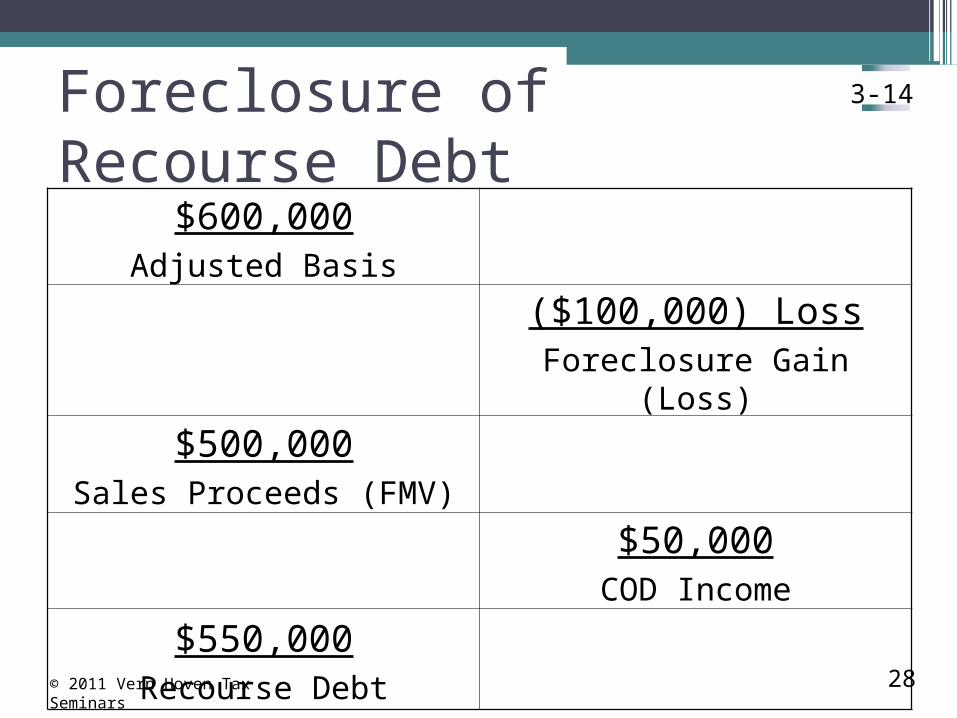

Foreclosure of Recourse Debt

• Recourse debt must be bifurcated1. Amount of cancellation of debt &2. Gain/loss on sale

• COD income results• Refi’s are often recourse debts

3-13

27© 2011 Vern Hoven Tax Seminars

Foreclosure of Recourse Debt

$600,000Adjusted Basis

($100,000) LossForeclosure Gain (Loss)

$500,000Sales Proceeds (FMV)

$50,000COD Income

$550,000Recourse Debt

28

3-14

© 2011 Vern Hoven Tax Seminars

Worksheet

•Calculates COD income for▫Foreclosures▫Repossessions

3-15

29© 2011 Vern Hoven Tax Seminars

Property Type Matters

•Business, investment or personal▫Business = ordinary loss on sale▫Investment = capital loss on sale▫Personal = non deductible loss on sale▫What did you do with the money?

3-15

30© 2011 Vern Hoven Tax Seminars

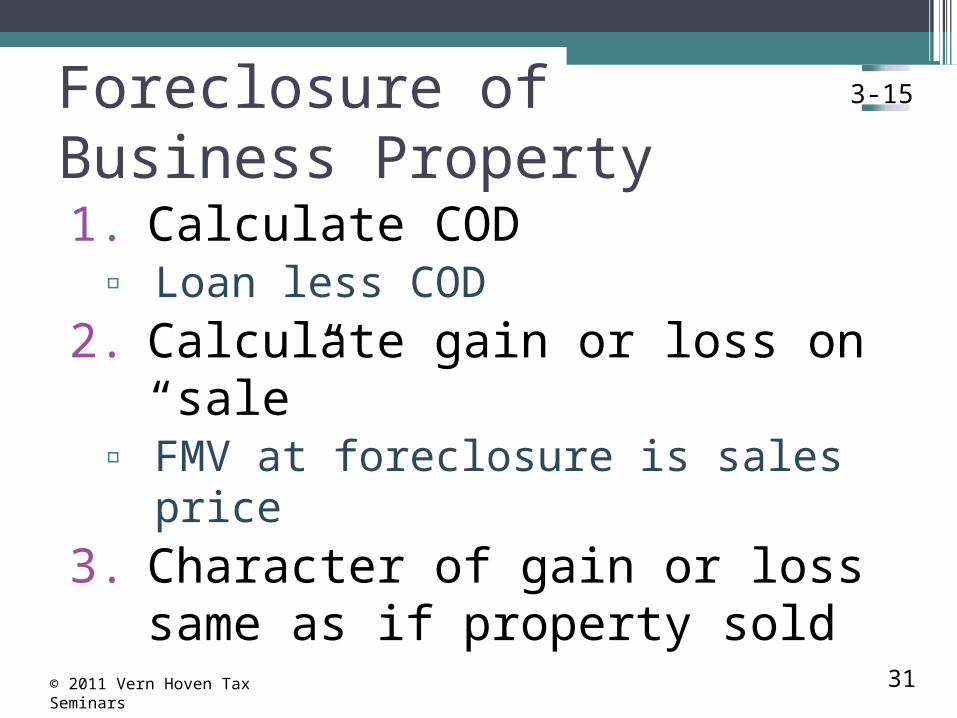

Foreclosure of Business Property

1. Calculate COD▫ Loan less COD

2. Calculate gain or loss on “sale”▫ FMV at foreclosure is sales price

3. Character of gain or loss same as if property sold

3-15

31© 2011 Vern Hoven Tax Seminars

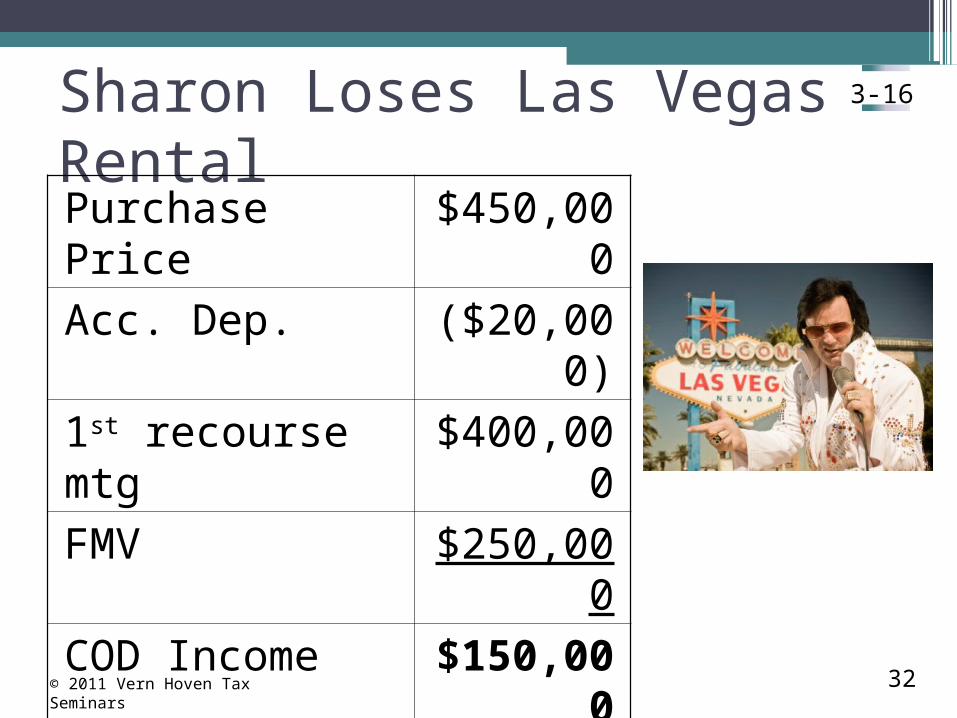

Sharon Loses Las Vegas RentalPurchase Price $450,000

Acc. Dep. ($20,000)

1st recourse mtg $400,000

FMV $250,000

COD Income $150,000

Sales Price $250,000

Adjusted Basis $430,000

Loss: Form 4797 $180,00032

3-16

© 2011 Vern Hoven Tax Seminars

Bill Loses Phoenix RentalPurchase Apartment Bldg $1,300,000

Down payment $250,000

Mortgage $1,050,000

Deferred gain $200,000

Depreciation taken $125,000

FMV at Foreclosure $1,000,000

COD at Foreclosure $50,000

Gain at “sale” $25,00033

3-16

© 2011 Vern Hoven Tax Seminars

Short Sale

•House sold, not enough to pay off bank•If “short pay” forgiven

by bank, COD results (Stevens)•Bank files Form

1099C

3-17

34© 2011 Vern Hoven Tax Seminars

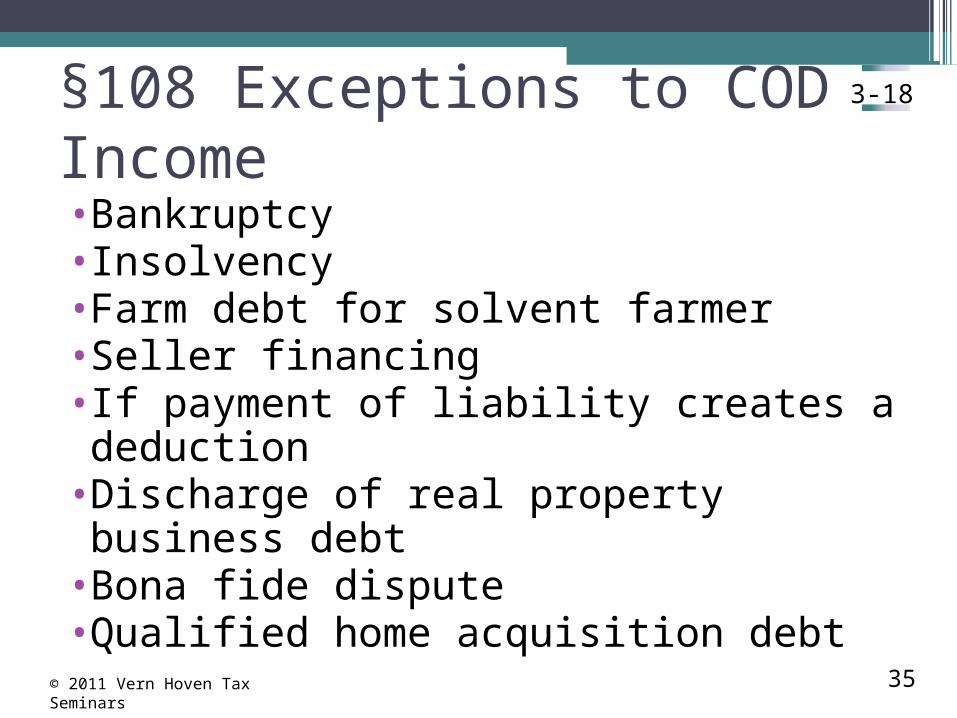

§108 Exceptions to COD Income

•Bankruptcy•Insolvency•Farm debt for solvent farmer•Seller financing•If payment of liability creates a deduction•Discharge of real property business debt•Bona fide dispute•Qualified home acquisition debt

3-18

35© 2011 Vern Hoven Tax Seminars

Bankruptcy

•Exclusion does not apply to a debtor in a bankruptcy case▫The bankruptcy exclusion rules apply ▫Taxpayer may choose insolvency exclusion

3-18

36© 2011 Vern Hoven Tax Seminars

Insolvency

•Taxpayer insolvent to extent liabilities exceed assets▫Includes house, pension, IRA, autos,

furniture, tools, etc.•How to calculate insolvency worksheet

•Pub. 4681

3-18

37© 2011 Vern Hoven Tax Seminars

Reduction of Tax Attributes

When COD non-taxable, reduce tax attributes in the following order1. NOLs2. General business credits3. AMT Credits4. Capital losses5. Basis reduction6. Passive activity losses7. Foreign tax credits

3-19

38© 2011 Vern Hoven Tax Seminars

Qualified Residence Debt Exception Under §108•Must meet two requirements

1. Qualified principal residence2. Qualified home acquisition debt

3-20

39© 2011 Vern Hoven Tax Seminars

Principal Residence

Requirement #1: Qualified Principal Residence ▫Same definition as §121 ▫Not available for vacation homes, rentals or

investment properties

3-20

40© 2011 Vern Hoven Tax Seminars

Qualified Acquisition Debt

Requirement#2: Original or refinanced debt used for

1. Acquisition, construction or improvement of principal residence

2. Secured by the principal residence3. Limited to recourse debt under $2 million4. Mortgage workout debt relief qualifies

3-20

41© 2011 Vern Hoven Tax Seminars

Only Portion is Acquisition Debt

•Ordering rules are required if acquisition debt less than total debt relief•Any forgiven home equity debt not used

for improvements cannot be excluded

3-20

42© 2011 Vern Hoven Tax Seminars

Mortgage Debt Forgiveness Facts/Checklist•Must be principal residence•Must be acquisition indebtedness•Homeowner not bankrupt•Homeowner not insolvent•Cancellation is not for personal services•See Interactive COD calculator on IRS

website

3-21

43© 2011 Vern Hoven Tax Seminars

Reduce Basis of Residence

•Basis of home is reduced by the amount of excluded income▫Turns ordinary income back into capital

gains

3-21

44© 2011 Vern Hoven Tax Seminars

© 2011 Vern Hoven Tax Seminars

3-22

45

§469 Passive Loss Overview

• Passive losses only deductible to the extent of passive income

• Excess losses carried forward• Current year passive income may be

offset by prior year passive losses• Losses are allowed if ▫ Complete disposition▫ To unrelated party▫ In taxable transaction

3-22

46© 2011 Vern Hoven Tax Seminars

What Activities Are Passive?

•Rentals, regardless of level of participation•Trade or business, if

no material participation

3-23

47© 2011 Vern Hoven Tax Seminars

IRS Issues 7 Rental Activity Tips

1. Income reported when received2. Advance rent reported when received3. Security deposits not taxable unless kept4. Property or services in lieu of rent

taxable5. Expenses paid by tenants are income6. Expenses pertaining to rental deductible7. All personal use must be pro rated

3-23

48© 2011 Vern Hoven Tax Seminars

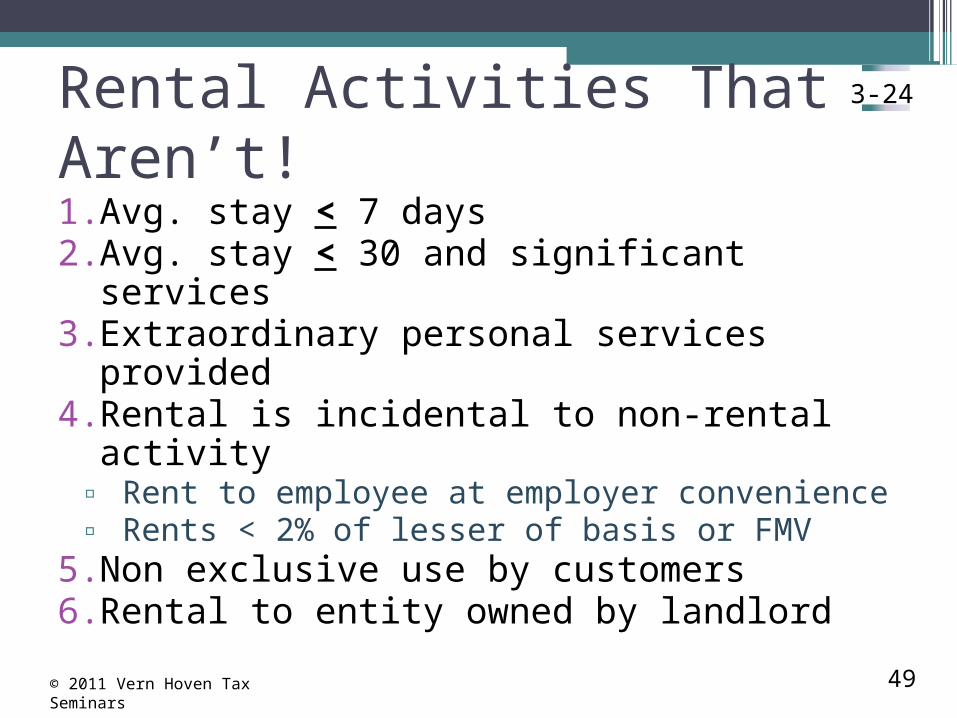

Rental Activities That Aren’t!

1. Avg. stay < 7 days2. Avg. stay < 30 and significant services3. Extraordinary personal services provided4. Rental is incidental to non-rental activity▫ Rent to employee at employer convenience▫ Rents < 2% of lesser of basis or FMV

5. Non exclusive use by customers6. Rental to entity owned by landlord

3-24

49© 2011 Vern Hoven Tax Seminars

Why Identify Activities?

1. Determine if a rental activity2. Determine if taxpayer materially

participates (Sidney Shaw)3. Determine whether or not complete

disposition has occurred 4. Apply pre enactment transitional rules

3-25

50© 2011 Vern Hoven Tax Seminars

Considerations When Grouping Activities1. Similarities & differences of businesses2. Common control of businesses3. Common ownership between businesses4. Geographical locations of each business5. Interdependencies between businesses6. Also, any other “reasonable method” to

determine “appropriate economic unit”▫ Consistency from year to year is required

3-26

51© 2011 Vern Hoven Tax Seminars

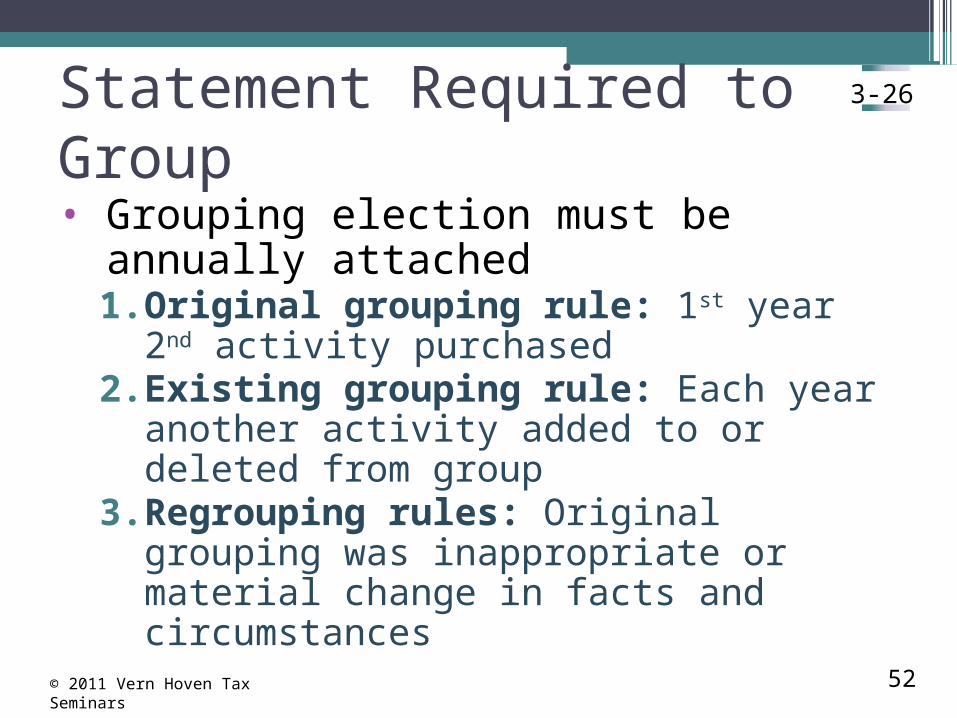

Statement Required to Group

• Grouping election must be annually attached 1. Original grouping rule: 1st year 2nd

activity purchased2. Existing grouping rule: Each year another

activity added to or deleted from group3. Regrouping rules: Original grouping was

inappropriate or material change in facts and circumstances

3-26

52© 2011 Vern Hoven Tax Seminars

Other Provisions of New Grouping Rules• Activities treated as separate if no

grouping election• Late election may be available if▫ Timely disclosure made by taxpayer▫ All relevant tax returns filed consistent with

desired activity groupings▫ Disclosure is made on tax return in year

omission is discoveredReasonable cause required if IRS discovers

3-28

53© 2011 Vern Hoven Tax Seminars

Passive Loss Cases

•Limited partner may MP▫500 hour or ▫5-of-the-last-10-years or any 3 year personal

service activity•LLC members not LPs per se (Newell,

Garnett, Gregg, Thompson,)▫IRS says “we quit” - AOD issued

3-29

54© 2011 Vern Hoven Tax Seminars

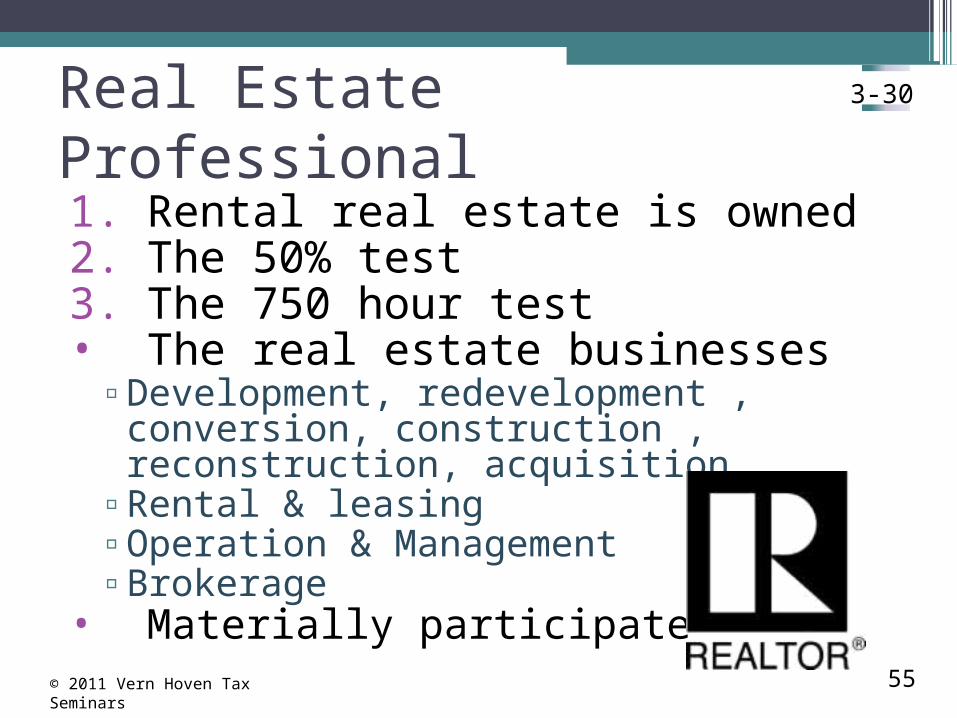

Real Estate Professional

1. Rental real estate is owned2. The 50% test3. The 750 hour test• The real estate businesses▫Development, redevelopment , conversion,

construction , reconstruction, acquisition▫Rental & leasing▫Operation & Management▫Brokerage

• Materially participate

3-30

55© 2011 Vern Hoven Tax Seminars

Time Test is Different

•50%/750 hour test▫Either spouse may be RE professional▫But spouses time may not be combined

(Goolsby)▫Must be >5% owner to count time (Bahas)▫On-call time doesn’t count (Moss)

•Material participation test

© 2011 Vern Hoven Tax Seminars

3-32

56

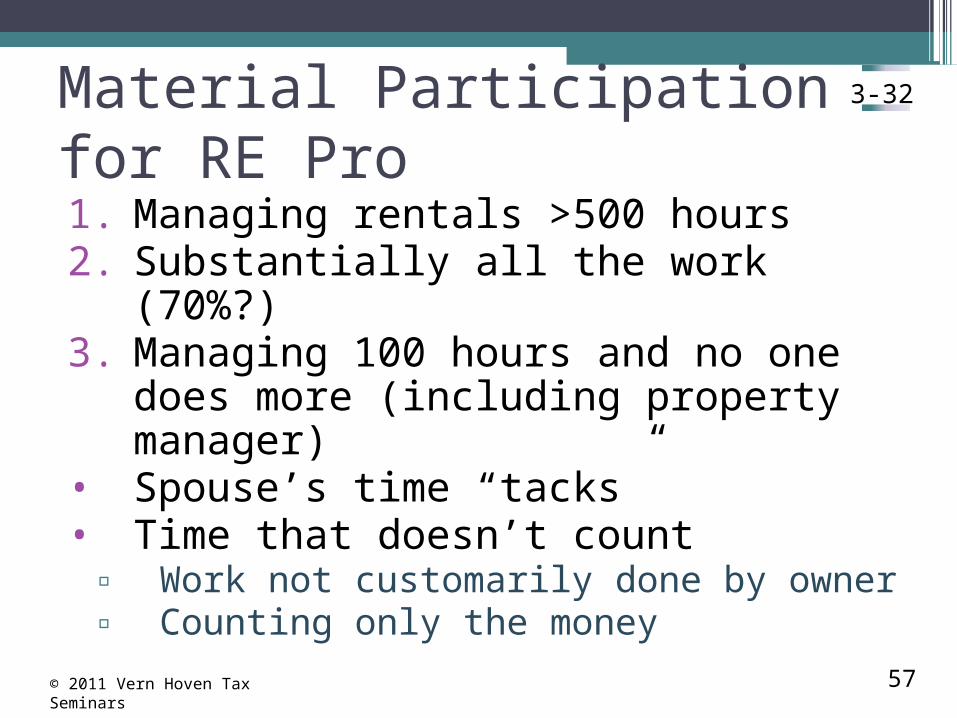

Material Participation for RE Pro

1. Managing rentals >500 hours2. Substantially all the work (70%?)3. Managing 100 hours and no one does

more (including property manager)• Spouse’s time “tacks”• Time that doesn’t count▫ Work not customarily done by owner▫ Counting only the money

© 2011 Vern Hoven Tax Seminars

3-32

57

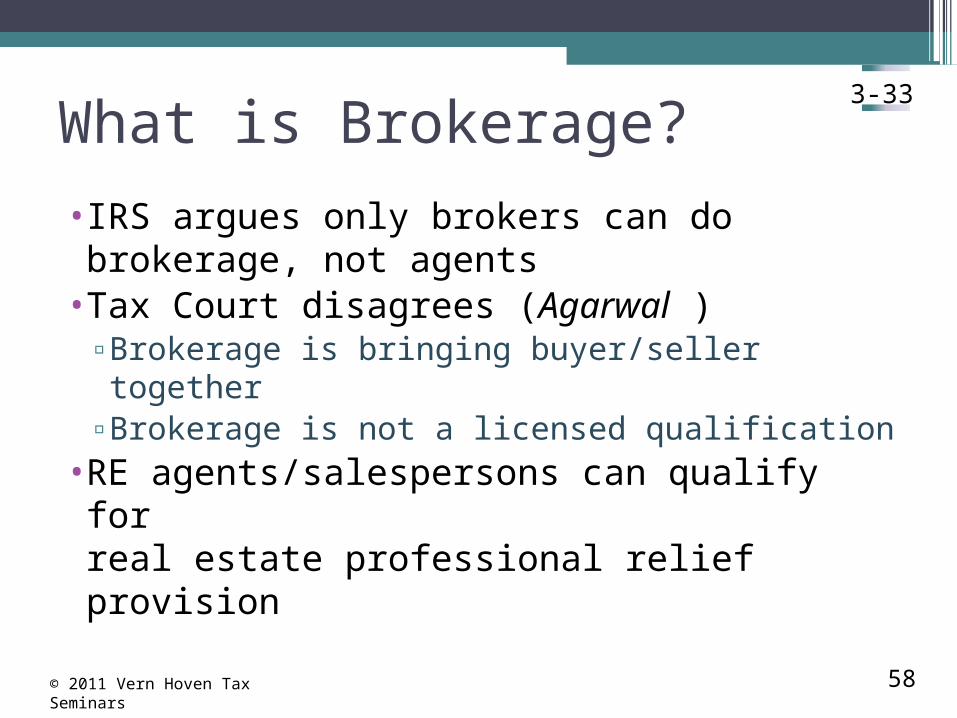

What is Brokerage?

•IRS argues only brokers can do brokerage, not agents•Tax Court disagrees (Agarwal )▫Brokerage is bringing buyer/seller together▫Brokerage is not a licensed qualification

•RE agents/salespersons can qualify for real estate professional relief provision

3-33

58© 2011 Vern Hoven Tax Seminars

Aggregation of Business and Rental by R.E. Professional•Each rental a separate activity •Unless election made to combine rentals▫(§469(c)(7)(A))

•File election in year rental purchased•Can be done late, with IRS permission

3-35

59© 2011 Vern Hoven Tax Seminars

Real Estate Professional Cases

•Bed and Breakfast not a real estate activity (Todd and Pamela Bailey)•Vacation rental not a real estate activity

(Bruce and Judy Bailey)•Real estate professional Donald Trask

forgot to make §469(c)(7)(A) election•Full time engineer misunderstands, and

then fails 50% test (Yusufu Anyika)•Denelda Goolsby made §469(c)(7)(A)

election but time records not credible

3-36

60© 2011 Vern Hoven Tax Seminars

Recharacterization Required•Certain property developed by TP and sold for a gain •Renting property to own business ▫Unless written binding contract before 2/19/88 (Farris)

•Significant participation passive activity net income•Qualified working interest in gas and oil•Rental from “raw land” (less than 30% depreciable)•Passive equity-financed lending activity• Intangible property leased by pass-through entity •Sale within 12 months of conversion to passive•Sale of “substantially appreciated” property • Income from a “dealers” investment property

© 2011 Vern Hoven Tax Seminars 61

3-46

No Recharacterization Active Passive

Passive Income $160,000

Less: Passive Deductions

-$200,000

Net Passive LOSS -$40,000

62© 2011 Vern Hoven Tax Seminars

3-46

No Recharacterization Active Passive

Passive Income $200,000

Less: Passive Deductions

-$160,000

Net Passive LOSS +$40,000

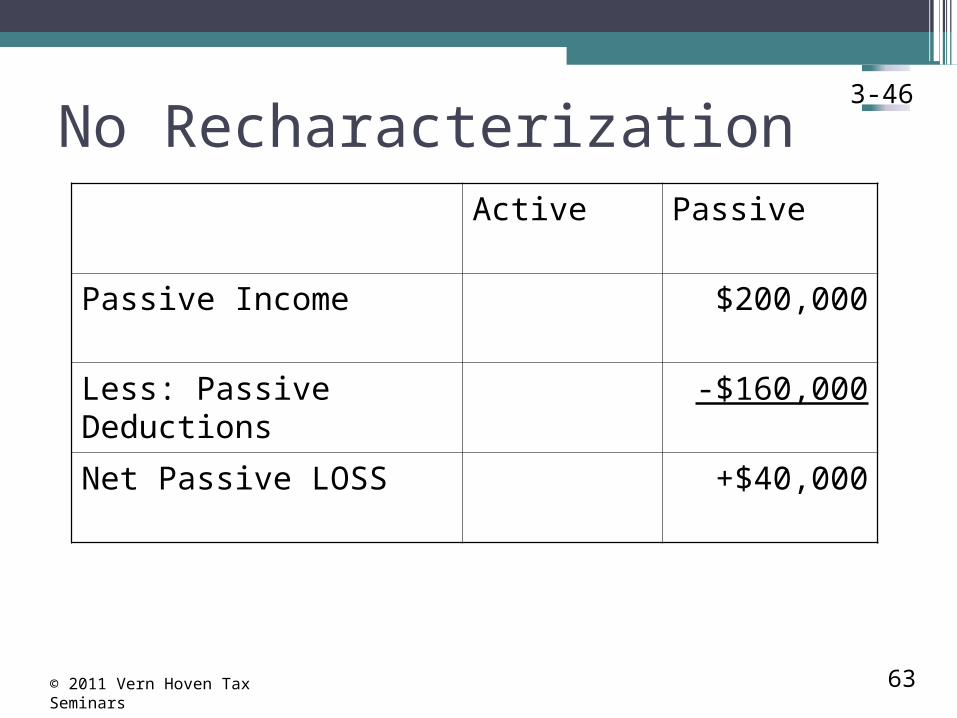

63© 2011 Vern Hoven Tax Seminars

3-46

No Recharacterization Active Passive

Passive Income $40,000 $160,000

Less: Passive Deductions

-$160,000

Net Passive LOSS -0-

64© 2011 Vern Hoven Tax Seminars

3-46

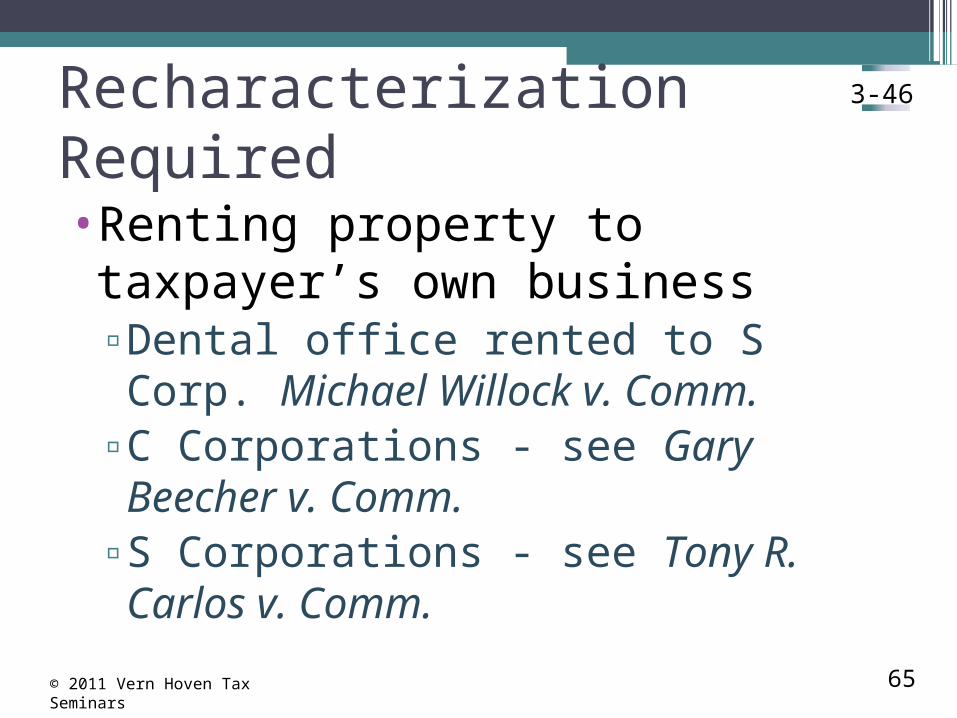

Recharacterization Required

•Renting property to taxpayer’s own business ▫Dental office rented to S Corp. Michael

Willock v. Comm.▫C Corporations - see Gary Beecher v.

Comm.▫S Corporations - see Tony R. Carlos v.

Comm.

© 2011 Vern Hoven Tax Seminars 65

3-46

Passive Loss Trigger Requirements

1. Dispose of entire interest2. Fully taxable transaction3. To unrelated party

© 2011 Vern Hoven Tax Seminars

3-47

66

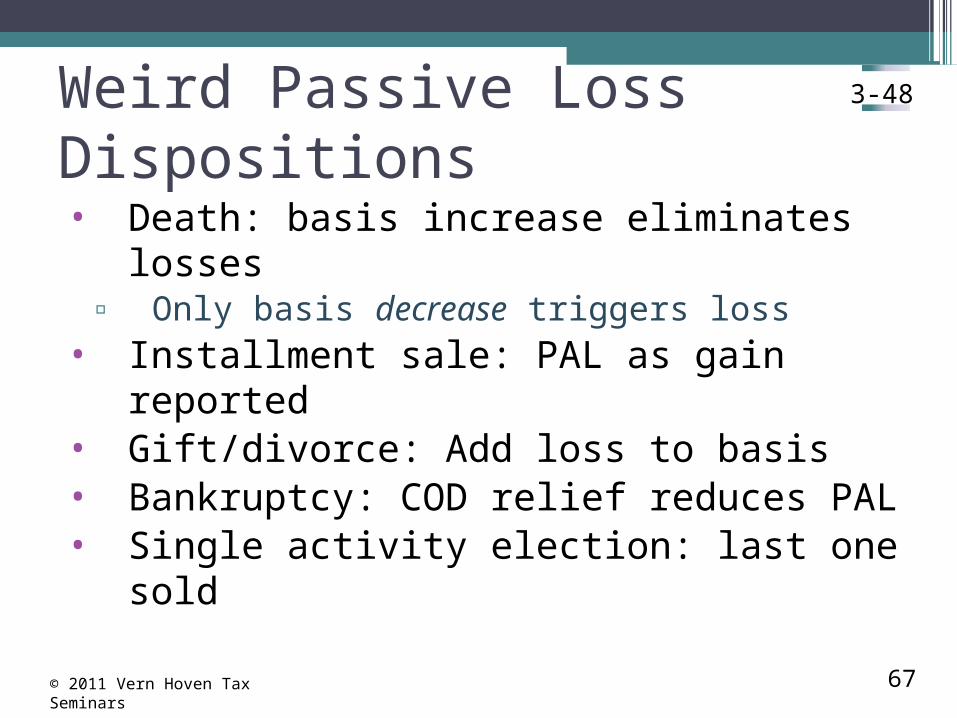

Weird Passive Loss Dispositions

• Death: basis increase eliminates losses▫ Only basis decrease triggers loss

• Installment sale: PAL as gain reported• Gift/divorce: Add loss to basis• Bankruptcy: COD relief reduces PAL• Single activity election: last one sold

© 2011 Vern Hoven Tax Seminars

3-48

67

© 2011 Vern Hoven Tax Seminars

3-49

68

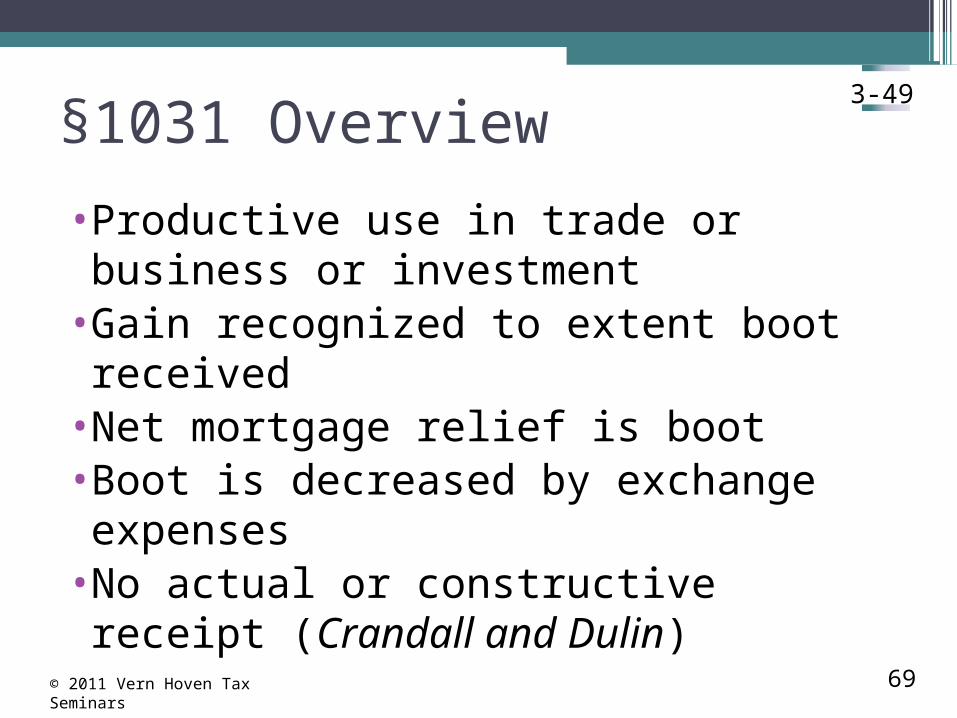

§1031 Overview

•Productive use in trade or business or investment•Gain recognized to extent boot received•Net mortgage relief is boot•Boot is decreased by exchange expenses•No actual or constructive receipt

(Crandall and Dulin)

3-49

69© 2011 Vern Hoven Tax Seminars

Qualified Use Requirements

•Productive use in trade or business or investment•Problem: Personal residence•Problem: Vacation homes •Problem: Property acquired for exchange

3-51

70© 2011 Vern Hoven Tax Seminars

Delayed Exchange Overview

•45 days to identify •180 days to complete exchange•Filing on time may reduce the 45/180

time limits

3-53

71© 2011 Vern Hoven Tax Seminars

Problems with Delayed Exchange•Miss 45/180 deadline? Gain recognized▫Even if cash already spent on new property

•Risks include▫Death of any party to exchange▫Divorce of buyer or seller ▫EPA or financing problems▫Qualified Intermediary steals money (It’s an

installment sale! Rev. Proc. 2010-14)

3-53

72© 2011 Vern Hoven Tax Seminars

Related Party Exchanges

•Original exchange not qualified for §1031 if either property disposed of within 2 years▫Using accommodator didn’t help (Ocmulgee)

•Exceptions▫Death, involuntary conversion or other non-

tax-avoidance purpose▫Diminish risk of loss

3-57

73© 2011 Vern Hoven Tax Seminars

Related Party Exchange Case

•OFI transfers shopping center (w/$6 million gain) to accommodator•OFI indentifies commercial property

owned by Treaty Fields (a related party)•Accommodator sells shopping center•Court says OFI-Treaty exchange occurs

first followed by Treaty selling w/2 years•Treaty’s sale triggers OFI’s $6M gain!

3-58

74© 2011 Vern Hoven Tax Seminars

Thank you!

75