2011.09.07 goldman sachs 8th annual european medtech … relations... · goldman sachs 8th annual...

TRANSCRIPT

Goldman Sachs 8th Annual European Medtech and Healthcare Services ConferenceLars RasmussenPresident & CEO

Goldman Sachs conference7 September 2011

Page 1

Forward-looking statements

The forward-looking statements contained in this presentation includingThe forward looking statements contained in this presentation, including forecasts of sales and earnings performance, are not guarantees of future results and are subject to risks, uncertainties and assumptions that are difficult to predict. The forward-looking statements are based on Coloplast’s p g pcurrent expectations, estimates and assumptions and based on the information available to Coloplast at this time.

Heavy fluctuations in the exchange rates of important currencies, significant changes in the healthcare sector or major changes in the world economy may impact Coloplast's possibilities of achieving the long-term objectives set as well as for fulfilling expectations and may affect the company’s financial outcomes.

Goldman Sachs conference7 September 2011

Page 2

Agenda

Leading in intimate healthcare

Stable intimate healthcare trends

Our ambition

Goldman Sachs conference7 September 2011

Page 3

Coloplast is a leading medtech company specialising inColoplast is a leading medtech company specialising in intimate healthcare needs...

50 years of innovation and growth:50 years of innovation and growth:

Global no. 1 in Ostomy Care

Global no. 1 in Urology & Continence Care

Global no. 4 in Advanced Wound & Skin Care

Headquartered in Denmark

Production in Denmark, Hungary, China, US , g y, ,and France

~7,000 employees globally Sales (DKK mill)

3,600

9,537

CAGR+23%

1957 19901970 20101980

Goldman Sachs conference7 September 2011

Page 4

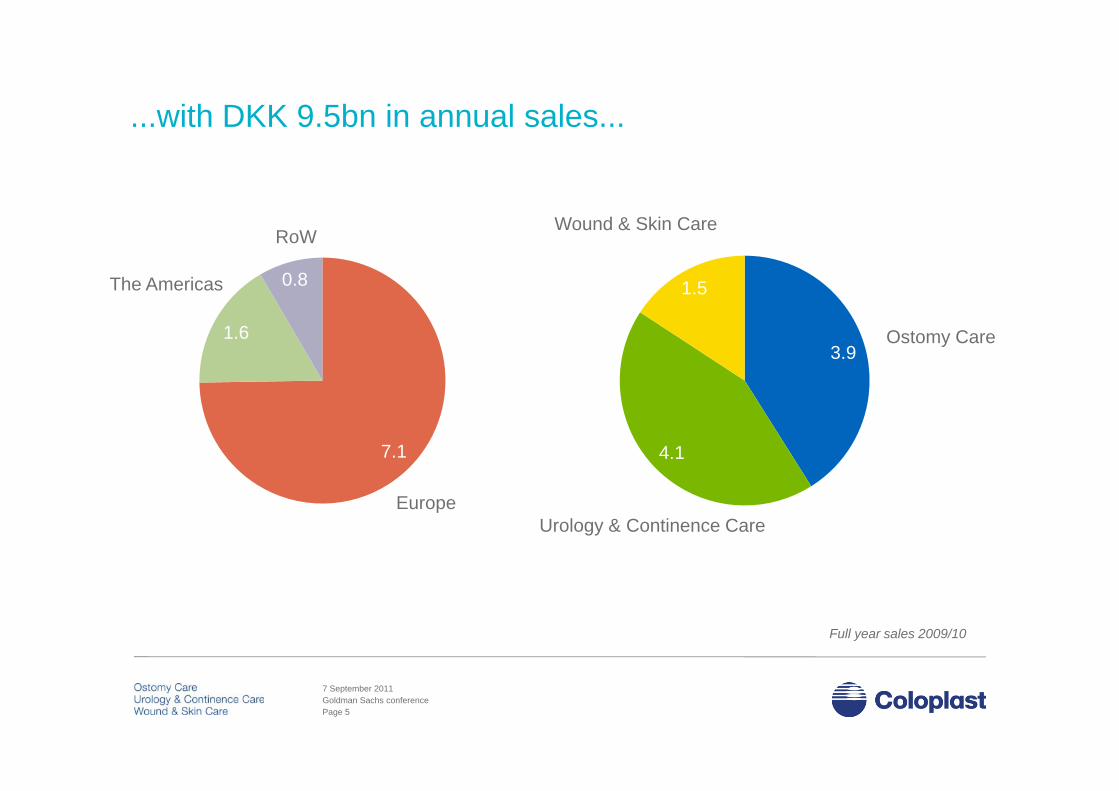

...with DKK 9.5bn in annual sales......with DKK 9.5bn in annual sales...

0.8 1.5The Americas

RoWWound & Skin Care

1.63.9

Ostomy Care

7.1 4.1

EuropeUrology & Continence Care

Full year sales 2009/10

Goldman Sachs conference7 September 2011

Page 5

Key messages for 3 quarters (1 October 2010 – 30 June 2011)Key messages for 3 quarters (1 October 2010 30 June 2011)

• 6% organic sales growth in line with guidance. 7 020

7,601

Sales

+8%

Reported growth was 8%

• Continued gross margin improvement from 61% to 64% from higher efficiency in production

7,020

9M 2009/10 9M 2010/11

to 64% from higher efficiency in production

• Very satisfactory EBIT margin of 24%

• Full year guidance for 2010/11:1,425 1,839

Operating profit

+29%

• Full year guidance for 2010/11:

• Organic growth rate around 6% (~7% in DKK)

9M 2009/10 9M 2010/11

• EBIT margin in fixed currencies and DKK of 24% - 25% 20% 24%

Operating margin

9M 2009/10 9M 2010/11

Goldman Sachs conference7 September 2011

Page 6

Stable intimate healthcare trends

Growing elderly population increasescustomer base for Coloplast productsDemographics

Expanding healthcare coverage for populations in emerging marketsincreases addressable market

Emerging markets

Surgical and medical trends are towardsearlier detection and cure, eventually

d i dd bl k t fSurgical and

di l t d reducing addressable market for Coloplast treatment products

Economic restraints push for

medical trends

preimbursement reforms, introduction of tenders, and lower treatment cost

Healthcare reforms

Goldman Sachs conference7 September 2011

Page 7

Three main organic levers will enable us to deliver onThree main organic levers will enable us to deliver on our ambition

We want to...

Organic growth

...and this is our ambition

...serve our customers better than anyone else

provide end user products and services better than

1

2

• Outgrow the market

• Deliver margins in …provide end-user products and services better than anyone else

run our business better than anyone else

2

3

gline with the best performing medical device …run our business better than anyone elsecompanies

Goldman Sachs conference7 September 2011

Page 8

1We continue to investWe continue to investin professionalizing our sales force

The local launch execution initiative focuses on the full launch phase in a local setting

The sales leadership initiative focuses on strengthening the skills of our 1st line sales

managers

S d di d hPre-launch

• Standardized approach to launch in the local markets

• Comprehensive approach to map the key market

Training

Launch

p ydynamics pre-launch

• Maximum focus in local organization during launch

Recruiting KPIsSales rep.

Post-launch

• KPIs and follow-up post-launch

• Clear responsibilities and il t th h t

Incentive schemes

milestones throughout

Goldman Sachs conference7 September 2011

Page 9

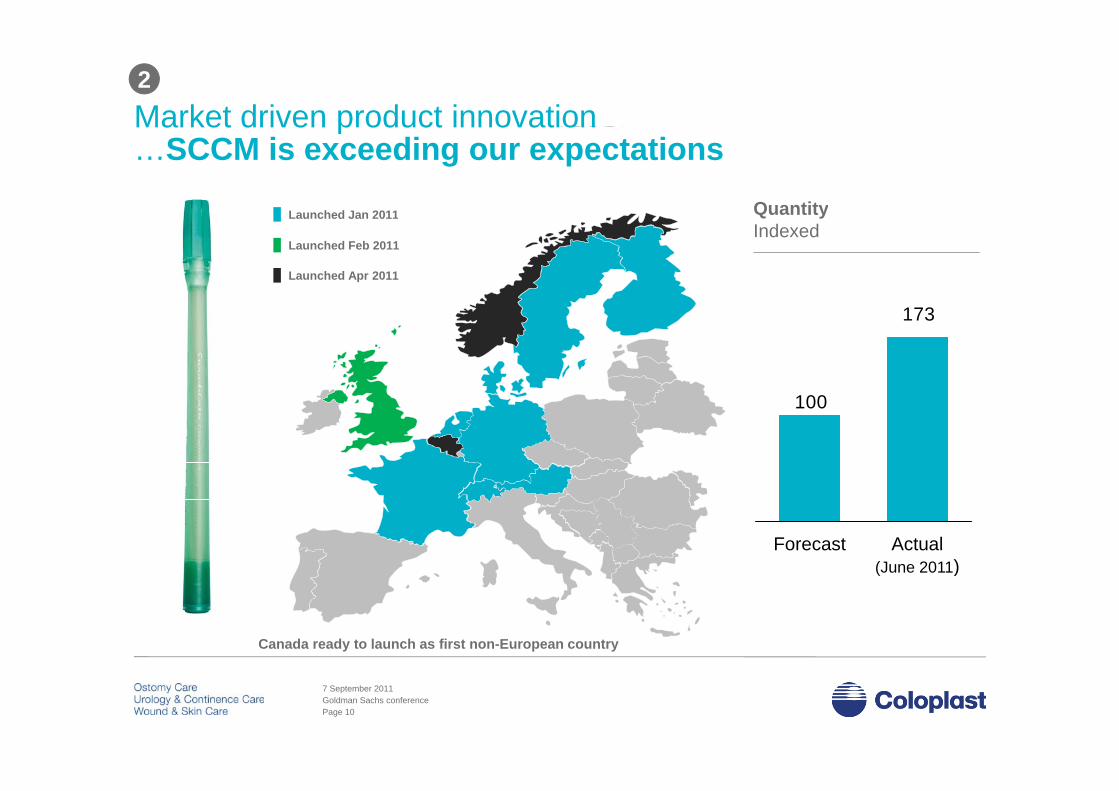

Market driven product innovation2

Launched Jan 2011

Market driven product innovation…SCCM is exceeding our expectations

QuantityLaunched Jan 2011

Launched Feb 2011

Launched Apr 2011

Q yIndexed

173

100100

Actual(June 2011)

Forecast

Canada ready to launch as first non-European country

( )

Goldman Sachs conference7 September 2011

Page 10

Market driven product innovation2

Launched Mar 2011

Market driven product innovation…SenSura® Mio

QuantityLaunched Mar 2011

Launched Apr 2011

Q yIndexed

161

100100

Actual(June 2011)

Forecast( )

Goldman Sachs conference7 September 2011

Page 11

We continue to build relationships2We continue to build relationships with our end-users, customers and KOL’s

Goldman Sachs conference7 September 2011

Page 12

We continue the journey3We continue the journeyby creating a more simple and efficient organisation

Lean & agile

Chronic Care Country Model

Lean & agile HQ

Optimizing HQ functions

Country Model

Transforming Global

functions

Global Operations

2008 2009 2010 2011

Goldman Sachs conference7 September 2011

Page 13

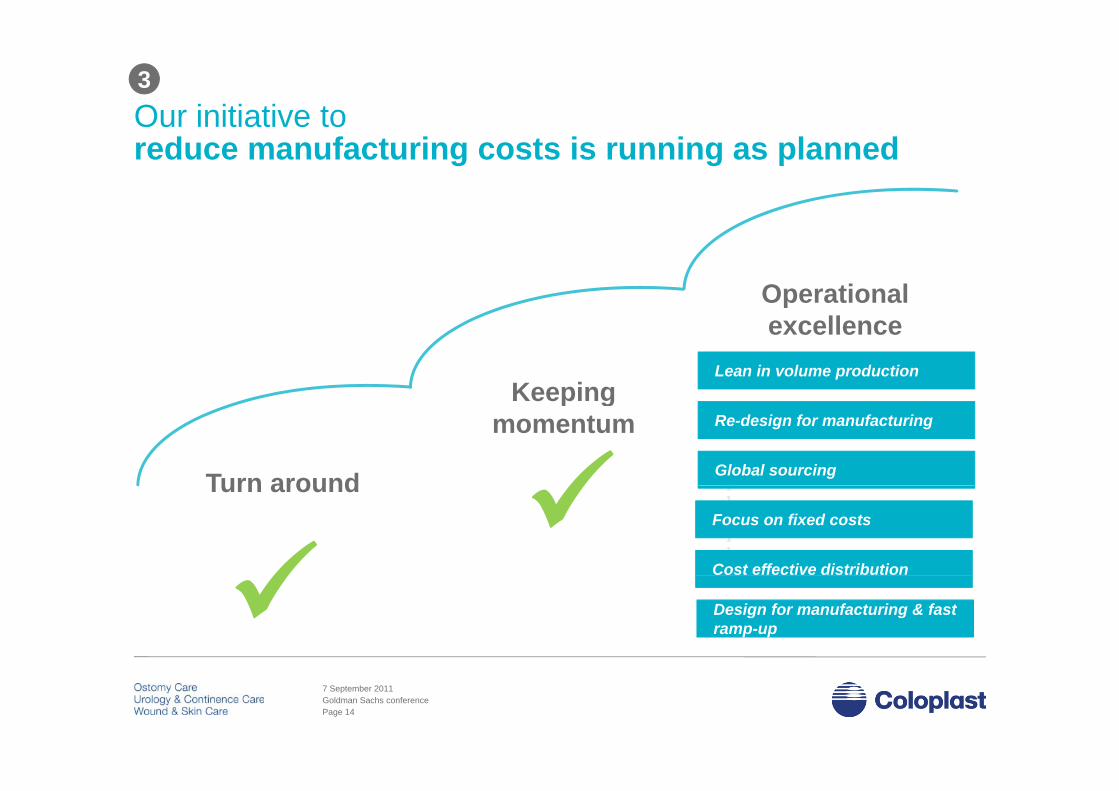

Our initiative to3Our initiative toreduce manufacturing costs is running as planned

Operational

Keeping

pexcellence

Lean in volume production

Turn around

Keeping momentum

1

Re-design for manufacturing

Global sourcingTurn around

1

11111

Focus on fixed costs

Cost effective distribution Design for manufacturing & fast ramp-up

Goldman Sachs conference7 September 2011

Page 14

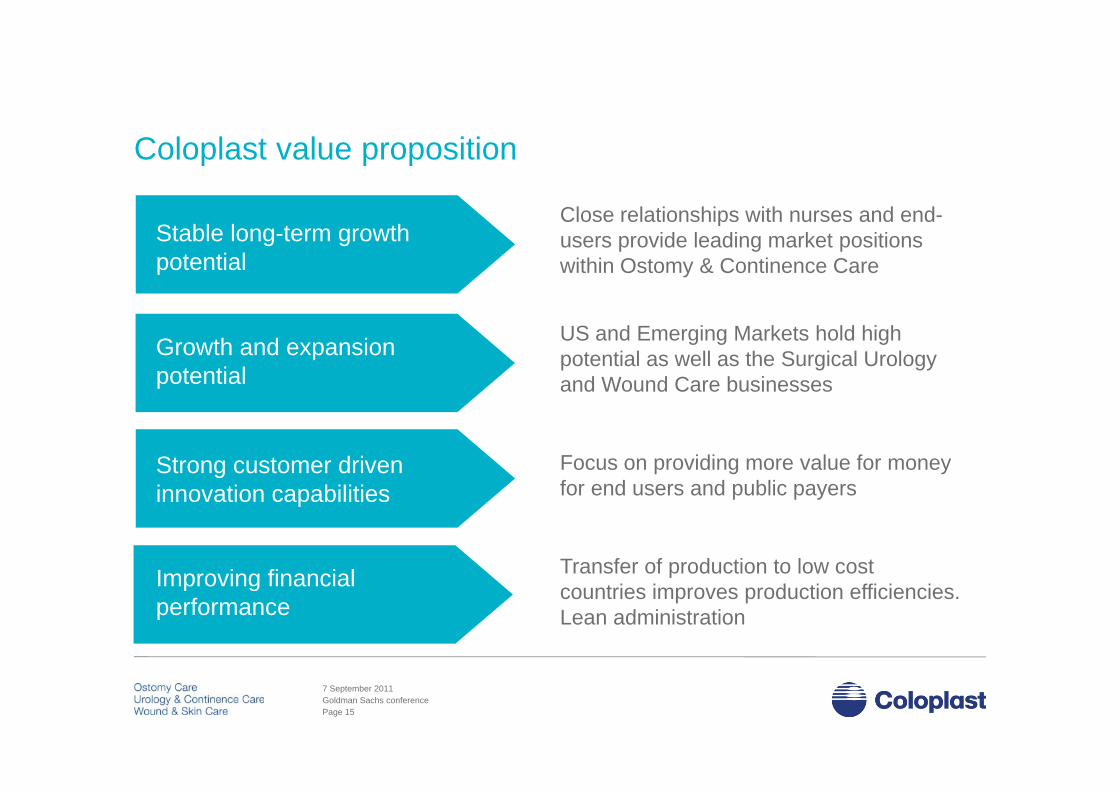

Coloplast value proposition

Close relationships with nurses and end-Close relationships with nurses and end-users provide leading market positions within Ostomy & Continence Care

Stable long-term growthpotential

US and Emerging Markets hold highpotential as well as the Surgical Urologyand Wound Care businesses

Growth and expansionpotential

Strong customer driven i ti biliti

Focus on providing more value for moneyfor end users and public payers

Improving financial Transfer of production to low cost

innovation capabilities for end users and public payers

Improving financialperformance

pcountries improves production efficiencies. Lean administration

Goldman Sachs conference7 September 2011

Page 15

?? ??

? ??? ?? ??

??

??

???

? ? ?? ? ?? ? ?Goldman Sachs conference7 September 2011

Page 16