2012 americas school of mines€¦ · 2012 americas school of mines license to operate – social...

TRANSCRIPT

2012 Americas School ofMines

www.pwc.com

License to operate – socialimpact and return on investment

Speakers:Speakers:

Rob Campbell-Watt, Director, PwC US

Patricia Awad, Manager, PwC Chile

Natalie Siegel, Director, PwC Australia

Agenda

Four topics covered:

1. Social license to operate

2. Conflict minerals update

3. Social impact assessment

PwC 2

4. Indigenous community investment: outcomes not inputs

Topic one

Social license to operate

PwC 3

Introduction to concept of license to operate

• Success of mining operations is dependent on a license to operate

• What is a “social license to operate” and its significance?

• ICMM: Ties social license to operate to Sustainable developmentprinciples, includes social and economic development

• World Bank: “acquiring free, prior and informed consent fromindigenous peoples, and local communities through mutual

PwC

indigenous peoples, and local communities through mutualagreements”

• US context – why is this important?

• Good vs bad operators

• Industry dealing with reserve access constraints, lost opportunity

• NMA and other representatives looking at leading practice

4

US context – Unlock future potential of US mining

Nonfuel Mineral assessment: National Coal Resource Assessment:

PwC 5

National Coal Resource Assessment 5 highest productionregions:(1) Northern and Central Appalachian Basin(2) Gulf Coast(3) Illinois Basin(4) Colorado plateu(5) Northern Rocky Mountains and Great plains

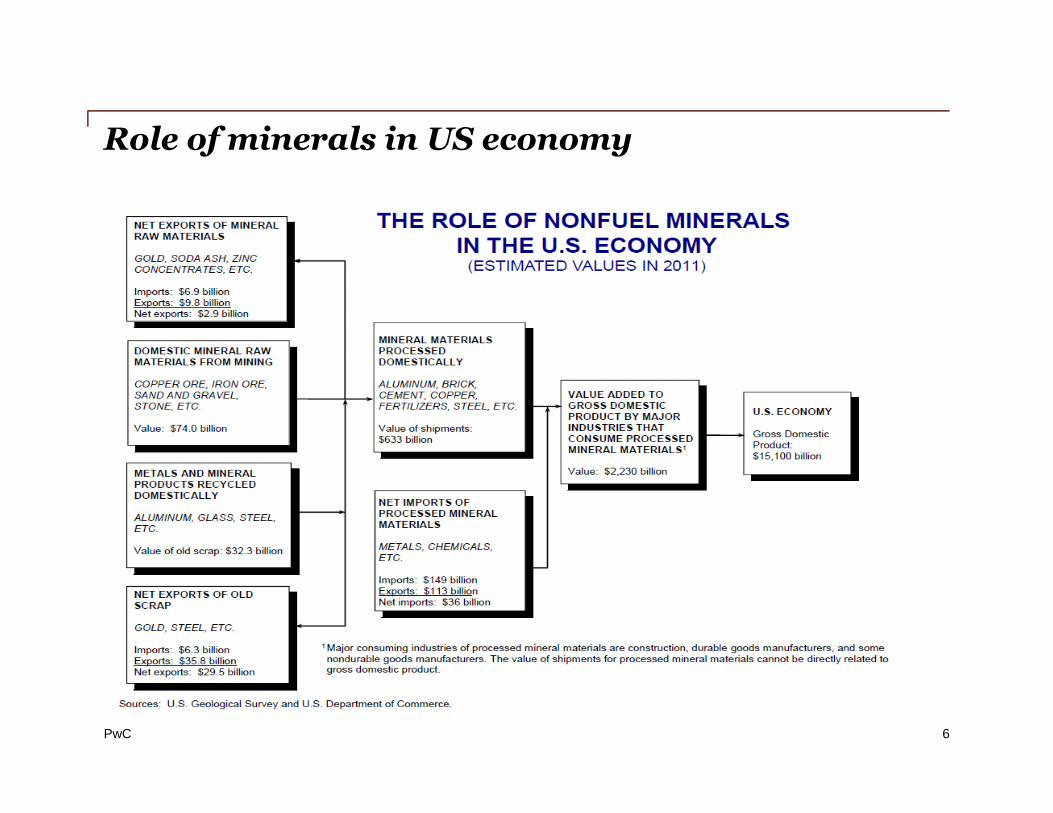

Role of minerals in US economy

PwC 6

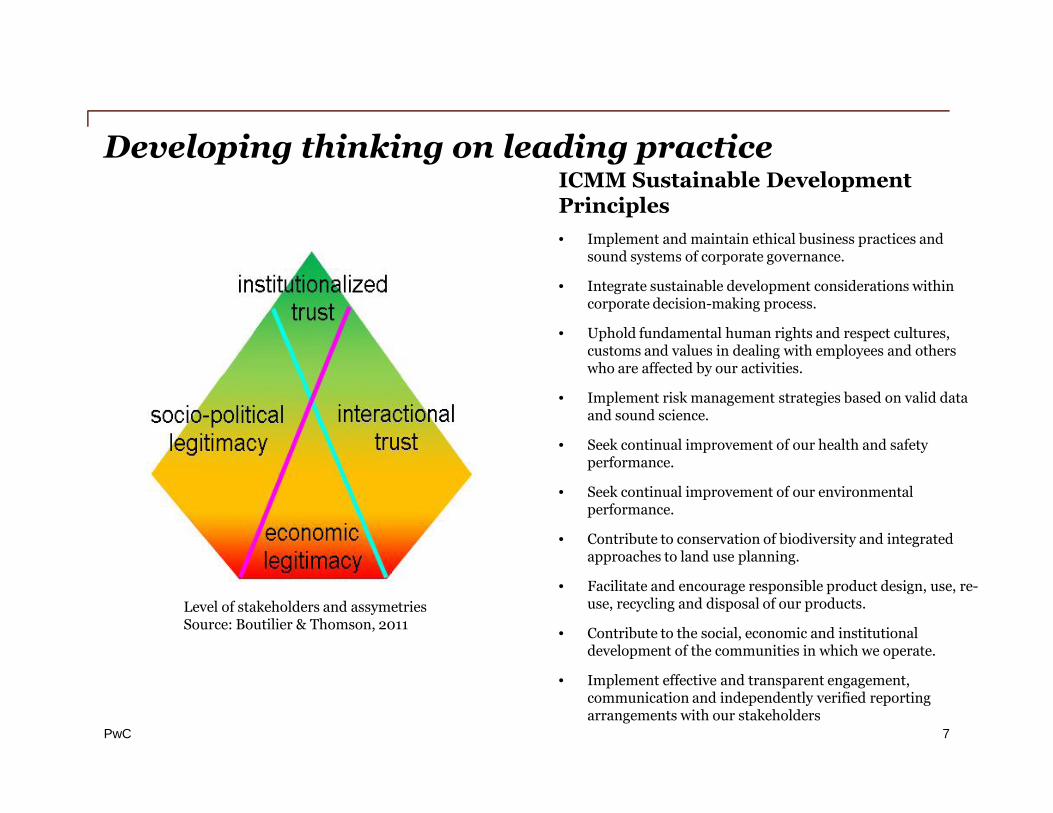

Developing thinking on leading practiceICMM Sustainable DevelopmentPrinciples

• Implement and maintain ethical business practices andsound systems of corporate governance.

• Integrate sustainable development considerations withincorporate decision-making process.

• Uphold fundamental human rights and respect cultures,customs and values in dealing with employees and otherswho are affected by our activities.

• Implement risk management strategies based on valid data

PwC

Level of stakeholders and assymetriesSource: Boutilier & Thomson, 2011

and sound science.

• Seek continual improvement of our health and safetyperformance.

• Seek continual improvement of our environmentalperformance.

• Contribute to conservation of biodiversity and integratedapproaches to land use planning.

• Facilitate and encourage responsible product design, use, re-use, recycling and disposal of our products.

• Contribute to the social, economic and institutionaldevelopment of the communities in which we operate.

• Implement effective and transparent engagement,communication and independently verified reportingarrangements with our stakeholders

7

Stakeholders and their material issues

PwC 8

Example methodology for displaying economicbenefits & social return of mining operations

PwC 9

Topic 2

Developments associated with ConflictMinerals (regulatory and social license)

PwC 10

What are “Conflict Minerals”?

Columbite(Tantalum)

Tungsten

PwC 11

Cassiterite(Tin)

Gold

Update as of May 2012

Requirements of S1502 of the Dodd-Frank Act

Examine products todetermine whether and towhat extent Section 1502

applies

Develop and conduct dueComply with disclosure

PwC 12

Develop and conduct duediligence protocol

Acquire private sectoraudit

Comply with disclosurerequirements

Update as of May 2012

The SEC continues to grapple with thecomplexity of conflict minerals

Dec. 2011SEC missesextended deadlinefor final SEC rules

Summer 2011

Dec. 2010OECD releasesDue Diligencefor

July 2011House Committee on FinancialServices submits letter to SECurging to adopt “transitionalimplementation”

March 2012SEC Chairman Shapiroindicates at a HouseSubcommittee meetingthat rules will not bereleased till mid-year

March 2012Maryland legislatureapproves HB 425regarding conflict

PwC 13

Jul. 21,2010Dodd-FrankAct signedinto law

May 2011EICC / GeSIannounce firstconflict – freesmelters

20112010

Oct. 2011SEC reopensComment Periodand hosts a publicConflict MineralsRoundtable.

2012

Summer 2011Common reportingtools released byEICC and GeSi

Oct. 2011California passesconflict mineralslaw regarding stateprocurement

forResponsibleSupply Chainsguidelines

Feb. 2012Senator Leahyand otherssend letter toSEC regardingstricterliability anduse of reliablecost studies

regarding conflictminerals

April 2012Hearing heldwith SEC todiscuss costbenefitanalysis ofrules makingmore broadly

SEC comments have provided hints about thepotential direction of the final rules

The SEC has indicated that thefinal rules may:

• Include transition period forcompanies to reportindeterminate origin so that

In addition, the SEC has beenunder further pressure to:

• Incorporate rigorous cost-benefitanalysis for measures proposed

PwC

indeterminate origin so thatdue diligence and upstreamcertifications mechanisms canmature

• Likely not include a deminimis exception

• Adhere to stricter liabilitydefinitions by requiring theconflict minerals report to befiled rather than furnished

14

Despite the delay, industry initiatives continue toproceed

• Traceability and certificationmechanisms continue to beimplemented across the DRCcountries

• First gold and tin audits completed

Artisanal or CommercialMine

Wit

hin

DR

CA

djo

inin

gC

ou

ntr

ies

Comptoirs

Négociant

Up

stream

PwC

• The number of Conflict – freetantalum smelters grows to 10

• AIAG and EICC continue to refinequestionnaire tools

• OECD 3T pilot groups to issueinterim findings report in Spring2012

• OECD Gold pilot group tocommence in 2012

15

Smelter/Refiner

Component Manufacturer

Product Manufacturer

Original EquipmentManufacturer (OEM)

Ad

join

ing

Co

un

trie

sG

lob

al

Ma

rk

ets

Traders

Risk

Up

stream

Do

wn

stream

Progress is increasing at the upstream levels

• On the ground initiatives are slowly expanding

• Preliminary reports from the OECD’s upstream pilot group indicate

• Awareness of due diligence expectations is increasing

PwC

• Majority of “comptoirs” report that they have adopted a policy

There is slow convergence of on-the ground initiatives

• Smelter have been slow to join the conflict – free smelter program

• Some downstream companies have become aggressive aboutvertically integrating up the supply chain to the mines

16

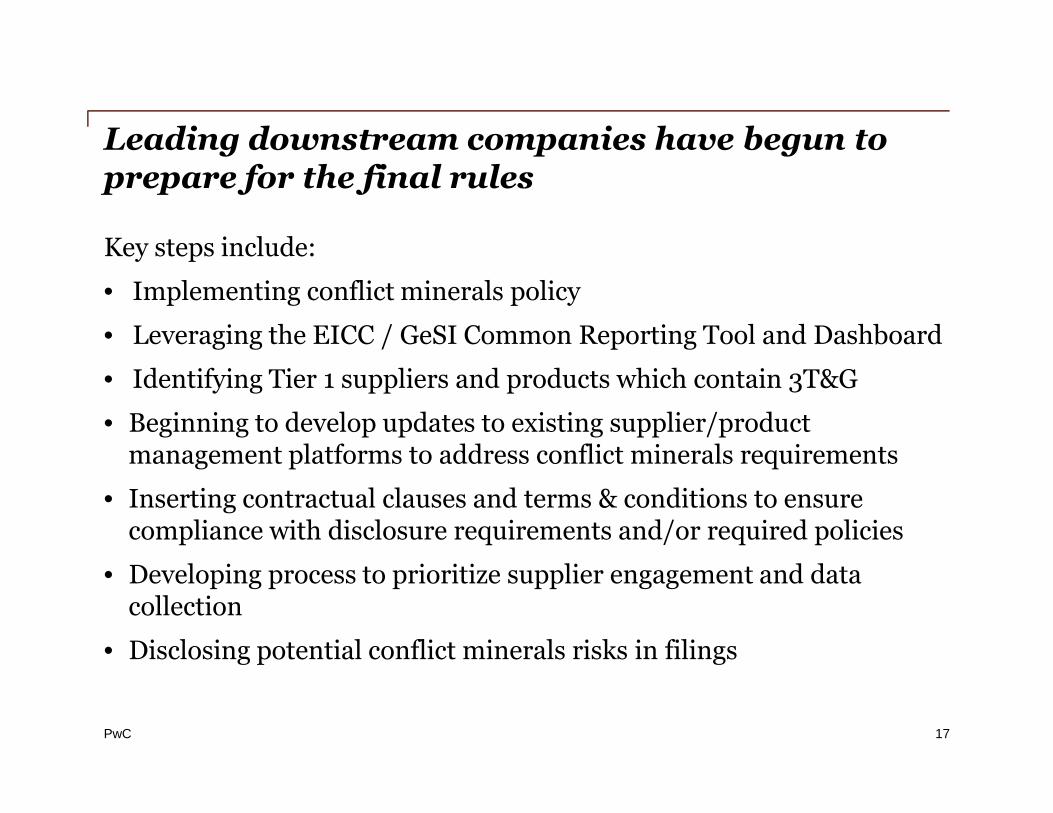

Leading downstream companies have begun toprepare for the final rules

Key steps include:

• Implementing conflict minerals policy

• Leveraging the EICC / GeSI Common Reporting Tool and Dashboard

• Identifying Tier 1 suppliers and products which contain 3T&G

PwC

• Beginning to develop updates to existing supplier/productmanagement platforms to address conflict minerals requirements

• Inserting contractual clauses and terms & conditions to ensurecompliance with disclosure requirements and/or required policies

• Developing process to prioritize supplier engagement and datacollection

• Disclosing potential conflict minerals risks in filings

17

Topic 3

Social Impact Assessment and Chileanexperience

How do we say no?

PwC

How do we say no?

Assessing the social impacts of miningprojects and developing a communitystrategy

18

What the companies are saying

“We spend lots of money on CI, but relations with communitiesdon’t improve (and sometimes even deteriorate)”

“Our CI program has become a source of conflict among communities”

“Local stakeholders have become dependent on us”

“There are endless requests from communities— how do we say no?”

PwC

“There are endless requests from communities— how do we say no?”

“We get pulled in a hundred different directions”

“We’ve ended up having to take over the government’s role”

“We are doing all these good things for the community, but no one givesus any credit”

“In the end, we have little to show for all the resources we’ve spent”

From: IFC, Community Investment – A Good Practice Guide for Companies doing Business in Emerging Markets

19

A simple definition of SIA

The process of assessing or estimating, in advance , the socialconsequences that are likely to follow from specific projectdevelopments.

PwC

From: Social Impact Assessment in the Mining Industry: Current Situation and Future Directions Susan A. Joyce GolderAssociates Ltd., Canada & Magnus MacFarlane Warwick Business School, UK.

20

Let’s take a look at the facts…

Mining activity hasimpacts

(+) (-)

Mining companiesspend money

Chile > US$20 Million - 2010

PwC 21

Yet…risk and conflict prevails

What goes wrong?

What goes wrong?

There is a gapbetween the realimpacts and CIpractices or strategy

Who’s in charge?When?

SIA as an ongoingprocess, throughoutthe life cycle of themine?

PwC

Underestimatingthe risks of the “openchequebook” – thewrong kind ofempowerment

22

Exploration Construction Operation Closure

• SocialBaseline

• Assessingthe expectedimpacts and

•Monitoring

• Ongoingstakeholderengagement

•Monitoring

• Ongoingstakeholderengagement

•Monitoring

• Ongoingstakeholderengagement

•Sustainability

PwC 23

impacts andrisks

• MitigationmeasuresCI plan

• Re-focusingCI efforts

•New socialbaseline forprogrammes

• Re-focusingCI efforts

•Sustainabilityofcommunitiesafter closure

Assessing thecumulativeimpacts of amine expansion+ 6 other

PwC

+ 6 otherdevelopments:a practicalexample

24

•Quality of life•Economic development•Employment•Landscape•Transportation•Health•Tourism•Housing•Water

SIA is a dynamic, ongoing process of integrating knowledge

on potential and real social impacts into decision making

and management practices.

PwC

From: Social Impact Assessment in the Mining Industry: Current Situation and Future Directions Susan A.

Joyce Golder Associates Ltd., Canada & Magnus MacFarlane Warwick Business School, UK.

25

Topic 4

Bang for your Buck:

Changing how we do business inIndigenous/Local communities so we get

PwC

Changing how we do business inIndigenous/Local communities so we get‘value for money’ – and so do they.

26

Why would you invest in the local community?

Is it just to tick a box? Is it just to be nice?

• When you are mandated

PwC

• There are big commercial advantages in doing so

27

If you are already spending on the community,what are you getting for it?

If you are about to start spending, how will youdesign your investment so you get something for it

and the community does to?

PwC

and the community does to?

Some Local examples

28

Lessons: Australian Indigenous EmploymentPrograms

PwC 29

So what does this mean?

Key lessons for going forward with local community activityand investment design:

• What is the value to your business of this activity; Does it have adollar value? What are the risks of doing it poorly

PwC

• Determine community need using an evidence base. This meansreally understanding the local community and its context

• This means research plus proper (not tokenistic) consultation

• Can we just pass it off by saying ‘this stuff is the government’sresponsibility’? What is the real risk to our business in saying that?

30

Thank you

© 2012 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United Statesmember firm, and may sometimes refer to the PwC network. Each member firm is a separatelegal entity. Please see www.pwc. com/structure for further details.