2012 economic opportunity for all campaign. tax policies create wealth, but who benefits? ...

TRANSCRIPT

2012 Economic Opportunity for All Campaign

Tax Policies Create Wealth, But Who Benefits?

Unfortunately, current asset-building policy primarily rewards those who are already wealthy.

Progressive tax policy should help people with lower incomes keep more of what they earn and provide incentives to earn more so as to help them lift and keep themselves out of poverty.

Key tax credits like the Earned Income Tax Credit and Child Tax Credit, as well as asset building policies like the Saver’s Bonus lift and keep people out of poverty, encourage work, and promote personal responsibility.

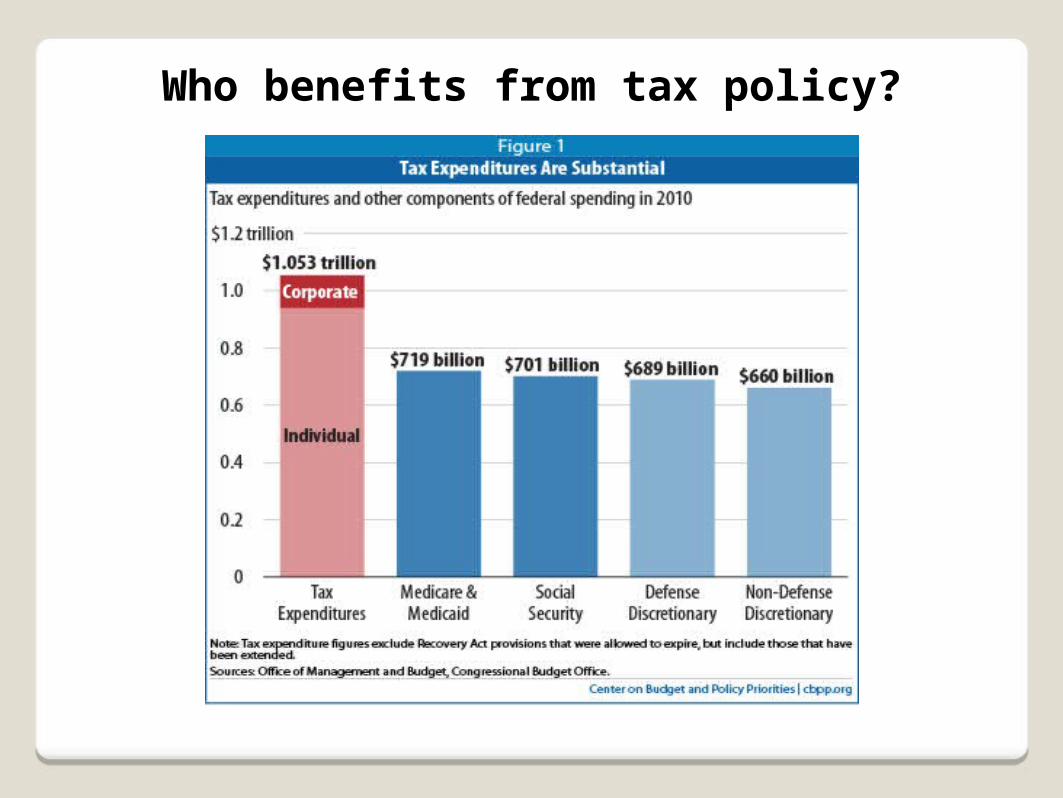

Who Benefits from Tax Policies?

Highest-income Americans have

seen their tax rates fall steadily

even as their incomes have

skyrocketed.

Who Benefits from Tax Policies?

• The US spent $400 billion in 2009 to help families build assets through tax benefits for mortgage interest, property tax, and capital gains. Most of those funds went toward tax breaks.

• More than half of these breaks went to the wealthiest five percent of taxpayers, who averaged a net benefit of $95,000 each. The bottom 60% of taxpayers averaged just $5 each.

Tax cuts & the Debt

Tax cuts & wars account for

nearly half of public debt by

2019

RESULTS will work to make the 2009 improvements to the Earned Income Tax Credit and Child Tax Credit permanent

These improvements will expire in December 2012

RESULTS will work to promote policies that help low-income individuals and families build savings and assets, primarily through building support for the Savers Bonus

We want to ensure that the Saver’s Bonus is included in future tax reform legislation in the next few years

RESULTS will also take advantage of opportunities to expand other asset development policies, e.g. Individual Development Accounts and Children’s Savings Accounts

2012 Economic Opportunity Campaign Goals

Earned Income Tax Credit

Designed to “make work pay” by providing an income tax refund for workers in low-wage jobs

“Refundable” credit: eligible taxpayer gets refund even if he/she owes no income tax Fully refundable: ($ EITC)-($taxes owed)

= $ refundEligibility is based on income, amount of

refund based on income family size

Earned Income Tax Credit

EITC Works!

The EITC is the largest poverty reduction program in the U.S. In 2010, the EITC lifted 5.4 million people out of poverty

The EITC lifts more children out of poverty than any other program - an estimated 3 million children in 2010

EITC recipients, over the course of a study from 1989 through 2006, in sum, paid more in taxes than they received in benefits.

Over 60% of EITC filers claim the credit for only 1-2 years at a time

Child Tax Credit

Tax credit designed to offset expenses of raising a child

Allows for maximum tax credit of $1,000 per child

Must earn between $3,000 and $75,000 to claim full credit ($110K for married couples)

Unlike EITC, taxpayer does not simply get the difference between the credit and taxes owed (partially refundable credit) Household must earn $9,667 to receive full $1,000 as a tax

refund

CTC is largest tax provision benefitting families with children Center on Budget and Policy Priorities estimates the CTC

lifted 2.3 million people out of poverty in 2009, 1.3 million of them children

ARRA Improvements to EITC and CTC

Income eligibility threshold for the CTC lowered to $3,000 so more low-income families could claim it (previously had to earn more than $12,000 to claim the CTC)

Married couples can now earn more without losing their EITC

Families with 3 or more children get a larger EITC (previously received same credit at 2 children families)

ARRA Improvements Making a Difference

CBPP estimates that the ARRA EITC and CTC improvements alone lifted 1.6 million people out of poverty in 2010

However, if allowed to expire in 2012, millions of Americans will be at risk of falling into poverty

President Obama has called for making the ARRA improvements to the EITC and CTC permanent

RESULTS urges Congress to protect low-income working families by making the EITC and CTC changes

permanent.

Volunteer Income Tax Assistance Program(VITA)

Program overseen by the IRA designed to provide free income tax preparation services to low-income taxpayers (less than $50,000 per year).

Purpose is to help low-income individuals and families get free tax-filing assistance without having to pay a professional preparer. IRS estimates at 20 percent of households eligible for the EITC do not claim it.

Local VITA programs around the country are usually administered by local non-profits (United Way, AARP, universities). VITA volunteers get trained on tax law and prepare the returns using online IRS software.

VITA programs help countless families around the country file their taxes and get their refunds. Despite its success, Congress only appropriated $12 million for the program in 2011, which is not enough to meet the demand for services.

Sen. Sherrod Brown (D-OH) and Rep. Mike Honda (D-CA-15) have introduced the VITA Act of 2011 in both the House and Senate (S.816 and H.R.2151). This bill would authorize $30 million annually toward VITA services and remove program spending restrictions to allow more funds to be spent on operations, outreach, and asset development services.

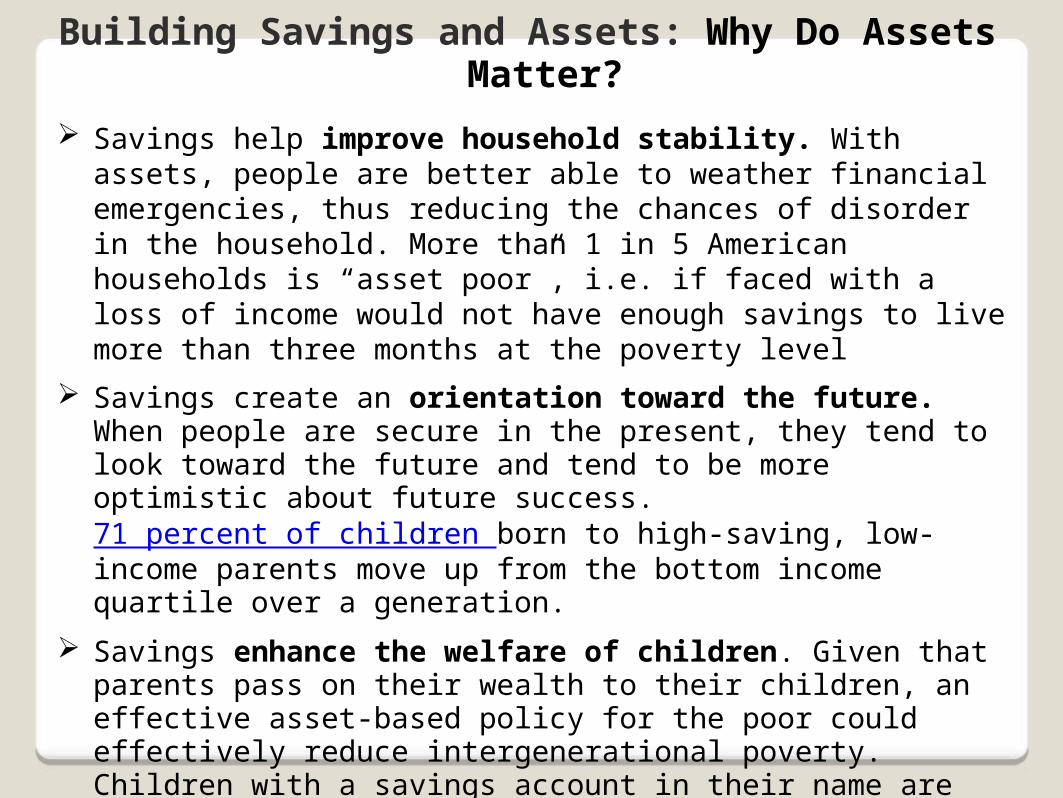

Building Savings and Assets: Why Do Assets Matter?

Savings help improve household stability. With assets, people are better able to weather financial emergencies, thus reducing the chances of disorder in the household. More than 1 in 5 American households is “asset poor”, i.e. if faced with a loss of income would not have enough savings to live more than three months at the poverty level

Savings create an orientation toward the future. When people are secure in the present, they tend to look toward the future and tend to be more optimistic about future success. 71 percent of children born to high-saving, low-income parents move up from the bottom income quartile over a generation.

Savings enhance the welfare of children. Given that parents pass on their wealth to their children, an effective asset-based policy for the poor could effectively reduce intergenerational poverty. Children with a savings account in their name are six times more likely to attend college than those without an account.

The Saver’s Bonus

How the Saver’s Bonus works:o Taxpayer agrees to deposit all or part of tax refund into an eligible savings

product (e.g. IRA, 401k, education account, Treasury bond)o If the taxpayer does not have an account, he/she can sign up for one on their

tax returno As an incentive, low-income taxpayers would receive a dollar-for-dollar match

for their deposits, up to $500 per year

o Only low-income households can participate

Intended to use the convenience and timing of tax season to promote savings Many low-income taxpayers receive their largest

checks of the year at tax time (refunds from EITC, CTC, etc.)

Use this opportunity to help people create a savings account right on the tax return

Studies show that when people have the opportunity and incentive to save, they will

The Saver’s Bonus in Action

Started in New York City as $aveNYC in 2008. Participants agreed to deposit at least $200 into a designated savings account. After one year, if they maintained their initial deposit, they received a 50 percent matching deposit up to $500.

Among the 2,200 people who opened an account under $aveNYC, eighty percent maintained their deposits for a year and received the match.

Seventy percent of $aveNYC participants who received the match rolled over their account or participated in the following year’s program.

The average $aveNYC participant saved $561 and over half contributed the maximum amount eligible for the match.

When asked, the top reasons participants gave for opening an account were the ease of opening an account (67 percent) and the match on deposits (64 percent).

$aveNYC became $aveUSA in 2011 and expanded to Tulsa, Newark, and San Antonio. As of February 2012, $aveUSA had opened over 1,600 savings accounts and participants had saved nearly $1 million.

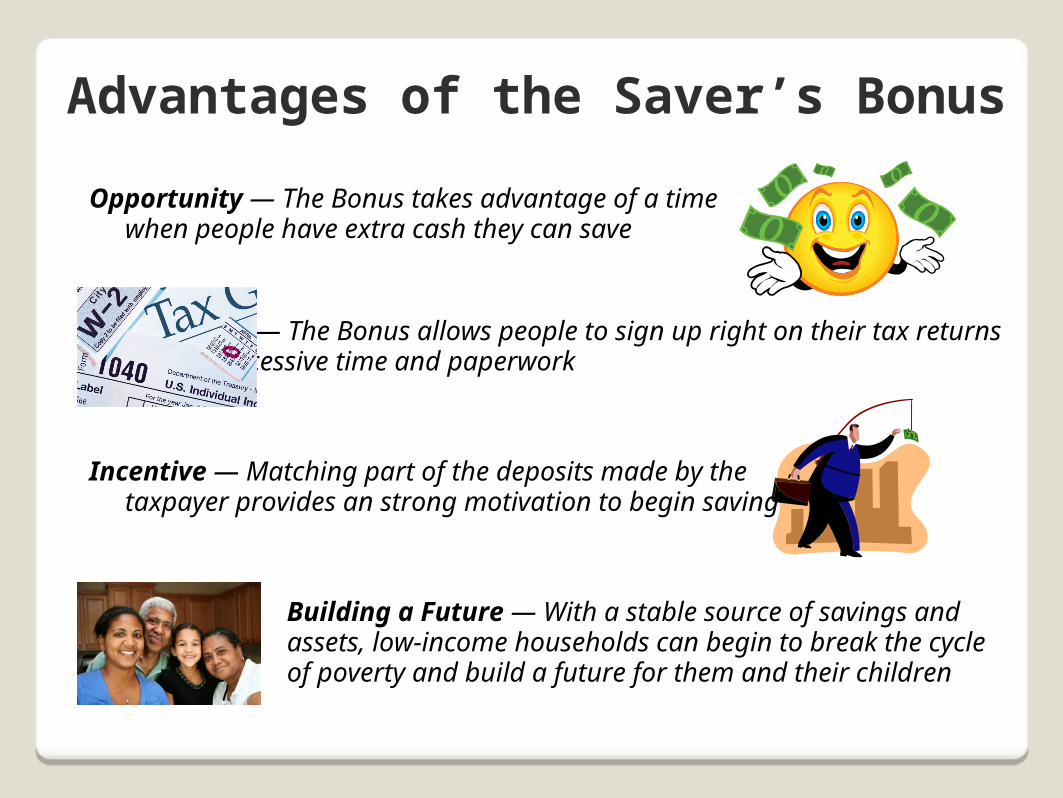

Advantages of the Saver’s Bonus

Opportunity — The Bonus takes advantage of a time when people have extra cash they can save

Convenience — The Bonus allows people to sign up right on their tax returns without excessive time and paperwork

Incentive — Matching part of the deposits made by the taxpayer provides an strong motivation to begin saving

Building a Future — With a stable source of savings and assets, low-income households can begin to break the cycle of poverty and build a future for them and their children

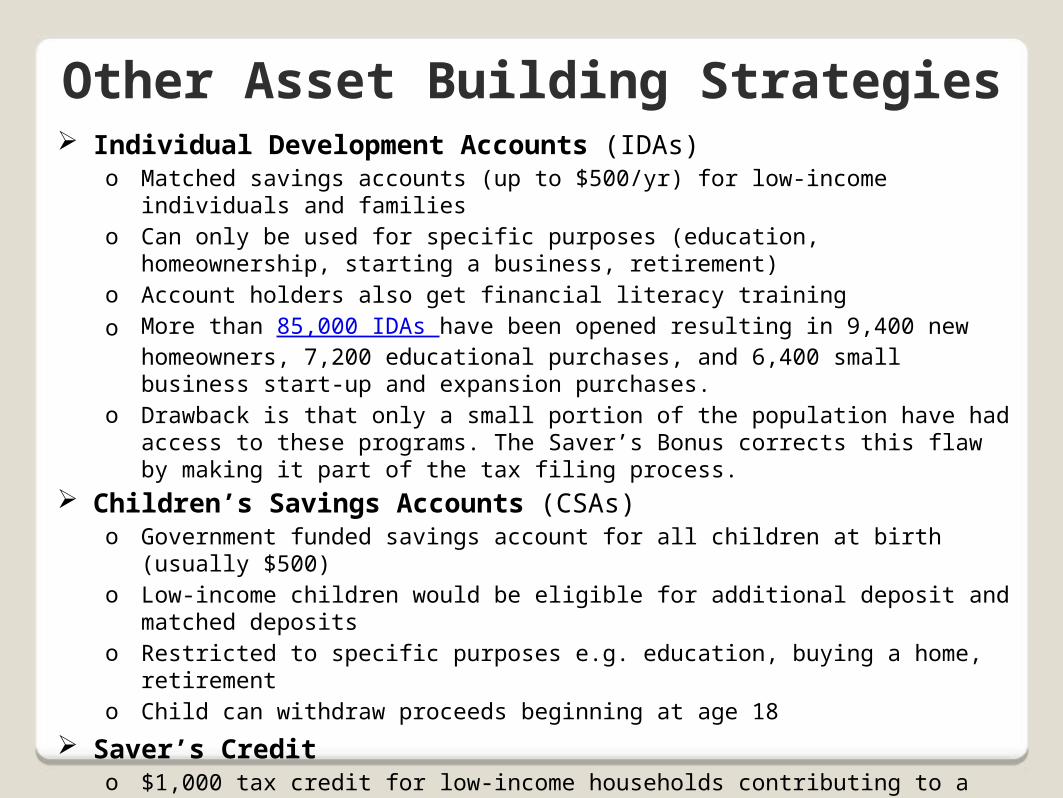

Other Asset Building Strategies Individual Development Accounts (IDAs)

o Matched savings accounts (up to $500/yr) for low-income individuals and familieso Can only be used for specific purposes (education, homeownership, starting a

business, retirement)o Account holders also get financial literacy trainingo More than 85,000 IDAs have been opened resulting in 9,400 new homeowners, 7,200

educational purchases, and 6,400 small business start-up and expansion purchases.o Drawback is that only a small portion of the population have had access to these

programs. The Saver’s Bonus corrects this flaw by making it part of the tax filing process.

Children’s Savings Accounts (CSAs)o Government funded savings account for all children at birth (usually $500)o Low-income children would be eligible for additional deposit and matched depositso Restricted to specific purposes e.g. education, buying a home, retiremento Child can withdraw proceeds beginning at age 18

Saver’s Credito $1,000 tax credit for low-income households contributing to a retirement accounto Currently a non-refundable credit, which means that low-income households that owe

little or no taxes (typically families earning under $40,000) receive no benefit

Engage: One of the most effective ways to break the cycle of poverty is by helping low-income households build up savings and assets.

Problem: Unfortunately, current asset-building policy primarily rewards those who are already wealthy. Of the largest asset-building policies in the U.S. (tax benefits for mortgage interest, property tax, and capital gains), 45 percent of the benefits go to the top 1 percent households; those in the bottom 60 percent receive only 3 percent of the benefits.

EPIC Laser Talk: The Saver’s Bonus

Inform/Illustrate:

In contrast, the Saver’s Bonus uses the convenience of tax time to help low-income Americans start saving. Low-income families would check a box on their tax return asking the IRS to deposit all or part of their tax refund into an eligible savings account. To encourage participation, part of their deposit would be matched up to $500 per year. It’s that simple… and it works. A pilot project called $aveUSA, which is modeled on the Saver’s Bonus, helped open over 1,600 accounts and helped participants save nearly $1 million in only its first year.

EPIC Laser Talk: The Saver’s Bonus

Call to Action (House): Will you speak to House Ways and Means Committee

Chairman Dave Camp (R-MI-4) and Ranking Member Sander Levin (D-MI-12) and urge them to support low-income asset building policies like the Saver’s Bonus in any upcoming tax legislation?

Call to Action (Senate): Will you speak to Senate Finance Committee Chairman

Max Baucus (D-MT) and Ranking Member Orrin Hatch (R-UT) and urge them to support low-income asset building policies like the Saver’s Bonus in any upcoming tax legislation?

EPIC Laser Talk: The Saver’s Bonus

Engage: The Earned Income Tax Credit and Child Tax Credit) are a financial lifeline for people working in low-wage jobs. In 2010, these credits lifted 9.3 million Americans out of poverty, many of them children.

Problem: Unfortunately, recent improvements to the EITC and CTC will expire at the end of this year, putting millions of children and families at risk of falling into poverty.

EPIC Laser Talk: EITC and CTC

Inform/Illustrate:

In 2009, Congress increased the EITC for larger families and married couples while also expanding the CTC so that lower-income working parents could claim it. These changes alone lifted 1.6 million out of poverty in 2010. And these credits don’t just benefit those who get them. Recipients of the EITC and CTC tend to spend these credits quickly and locally, which helps the local economy. Economists estimate that the EITC generates $1.50 to $2.00 in economic activity for every one dollar spent.

EPIC Laser Talk: EITC and CTC

Call to Action (House): We need to protect working families. Will you please

speak to House Ways and Means Committee Chairman Dave Camp (R-MI) and Ranking Member Sander Levin (D-MI) and urge them to make the 2009 EITC and CTC improvements permanent?

Call to Action (Senate): We need to protect working families. Will you please

speak to Senate Finance Committee Chairman Max Baucus (D-MT) and Ranking Member Orrin Hatch (R-UT) and urge them to make the 2009 EITC and CTC improvements permanent?

EPIC Laser Talk: EITC and CTC

Economic Opportunity ResourcesRESULTS

www.results.org

New America Foundation’s Asset Building Projectwww.assetbuilding.org

Corporation for Enterprise Developmentwww.cfed.org

Center on Budget and Policy Prioritieswww.cbpp.org

National Community Tax Coalitionwww.tax-coalition.org

Center for Tax Justicewww.ctj.org

Coalition on Human Needswww.chn.org

Half In Ten: Campaign to Cut Poverty in Half www.halfinten.org

RESULTS/RESULTS Educational Fund 750 First St NE, Ste 1040

Washington DC 20002

RESULTS Economic Opportunity Campaign Contacts:

Meredith Dodson, [email protected], (202) 782-7100, x116Jos Linn, [email protected], (515) 288-3622

www.results.org