2012 paper f5 qanda sample download v1

TRANSCRIPT

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

©Tony Surridge Online Limited, 2012 1

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

ACCA Paper F5: PERFORMANCE MANAGEMENT

Diagnostic Tests - Questions and Answers

Published by Tony Surridge Online Limited in 2012

Copyright © Tony Surridge Online Limited

Part of the Tony Surridge +AddVance study materials range

Tony Surridge Online Limited [email protected]

www.tonysurridge.co.uk

Tony Surridge Online Limited is grateful to the Association of Chartered Certified Accountants (ACCA) and the Chartered Institute of Management Accountants (CIMA) for permission to reproduce past examination questions.

The suggested solutions in the exam answer bank have been prepared by Tony Surridge Online Ltd, unless otherwise stated.

This E-book is sold subject to the condition that no part of it shall be reproduced, transmitted, or freely distributed, in any form by any means, electronic, photocopying, recording or otherwise, without the prior permission in writing of

Tony Surridge Online Limited. This book is not to be used for commercial use. It is sold on the understanding that a private individual has bought it for individual personal use, and prohibits purchase by any company or organisation entity (limited or otherwise) or sole trader or partnership. Such entities must contact [email protected]

separately to purchase a multi-user license.

©Tony Surridge Online Limited, 2012 2

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

3 ©Tony Surridge Online Limited, 2012

“No snowflake in an avalanche ever feels responsible.” Voltaire

Thank you for helping to save our environment.

Studying ONLINE protects trees! LEARN ONLINE

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

+AddVance Study Material

Main Page Copyright statement Environmental notice For the ladies only Test your knowledge now! Formulae sheet

Syllabus Study Guide The structure of the syllabus A Specialist cost and management accounting techniques Intellectual levels B Decision-making techniques Learning hours C Budgeting Guide to exam structure D Standard costing and variance analysis Guide to examination assessment E Performance measurement and control Aim Main capabilities Relational diagram of main capabilities Rationale Detailed syllabus Approach to examining the syllabus

Diagnostic Test Topics 1: Activity Based Costing (ABC) 8: Make or Buy and Other Short-Term Decisions 2: Target Costing 9: Dealing with Risk and Uncertainty 3: Life-Cycle Costing (LCC) 10: Budgetary Systems and Types of Budgets 4: Backflush Accounting 11: Quantitative Analysis in Budgeting 5: Throughput Accounting 12: Standard Costing and Variance Analysis 6: Multi-limiting Factors and the Use of Linear Programming 13: Planning and Operational Variances 7: Pricing Decisions 14: The Scope of Performance Measurement For the Contents Pages: - Diagnostic Questions and Answers Click here - For Exam-status Questions and Answers Click here

ACCA Paper F5 Performance Management (PM) Practice Questions & Answers

“Where shall I begin, please your majesty?” he asked. “Begin at the beginning,” the king said gravely, “and go on till you come to the end: then stop.” Lewis Carroll Through the Looking-Glass

4 ©Tony Surridge Online Limited, 2012

Only Topic 12 is activated for this free sample

These two are activated for this free sample

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

THIS FORMULA SHEET IS PROVIDED IN THE

EXAM

5

Formulae Sheet Learning curve Y = axb Where Y = cumulative average time per unit to produce x units a = the time taken for the first unit of output x = the cumulative number of units b = the index of learning (log LR/log 2) LR = the learning rate as a decimal Regression analysis Demand curve

2bQ - a MR

0 Q when price a

quantityin changepricein change b

bQ - a P

=

==

=

=

( )( )2222

22

y)( - n)( - xnn

nxb -

ny a

)( - xnn b

bx a y

ΣΣΣΣ

ΣΣ−Σ=

ΣΣ=

ΣΣΣΣ−Σ

=

+=

yxyxxyr

xyxxy

5 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Diagnostic Test Standard Costing and

Variance Analysis Questions

ACCA Paper F5 Performance Management

6 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Question 1 C Company uses a standard costing system. The standard cost card for one of its products shows that the product should use 4 kg of material B per finished unit and that the standard price per kg is $4.50. C Company values its inventory of materials at standard prices. During April when the budgeted production level was 1,000 units, 1,040 units were made. The actual material quantity of material B used was 4,100 kg and material B inventories were reduced by 300 kg. The cost of the material B which was purchased was $14,400. The material price and usage variances for April were Price Usage $ $ A 2,700 F 450 A B 2,700 F 270 F C 4,050 F 270 F D 2,700 F 1,620 F (3 marks) Question 2 S Company has extracted the following details from the standard cost card of one of its products. Direct Labour 4.5 hours @ $6.40 per hour During March, S Company produced 2,300 units of the product and incurred direct wages costs of $64,150. The actual hours worked were 11,700. The direct labour rate and efficiency variances were Rate Efficiency $ $ A 2,090 F 7,402 A B 2,090 F 8,640 A C 10,730 F 7,402 A D 10,730 F 8,640 A (2 marks) Question 3 The following details relate to product T, which has a selling price of $44.00. $/unit Direct materials 15.00 Direct labour (3 hours) 12.00 Variable overhead 6.00 Fixed overhead 4.00 37.00 During April, the actual production of T was 800 units, which was 100 units fewer than budgeted. The budget shows an annual production target of 10,800, with fixed costs accruing at a constant rate throughout the year.

7 ©Tony Surridge Online Limited, 2012

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Actual overhead expenditure totaled $8,500 for April. The overhead variances for April were Volume Expenditure variance $ $ A 367 A 1,000 A B 500 A 400 A C 100 A 1,000 A D 100 A 400 A (2 marks) Question 4 Z Company uses a standard costing system and has the following labour cost standard in relation to one of its products. 4 hours skilled labour @ $6.00 per hour $24.00 During October, 3,350 of these products were made which was 150 units less than budgeted. The labour cost incurred was $79,893 and the number of direct labour hours worked was 13,450. The direct labour variances for the month were Rate Efficiency A $804 (F) $300 (A) B $804 (F) $300 (F) C $807 (F) $300 (A) D $840 (F) $3,300 (F) (2 marks) Question 5 J Company uses a standard costing system and has the following data relating to one of its products. $ $ Selling price 9.00 Variable costs 4.00 Fixed costs 3.00 7.00 Profit per unit 2.00 Its budgeted sales for October were 800 units, but actual sales were 850 units. The revenue earned from these sales was $7,480. If a profit reconciliation statement were to be drawn up using marginal costing principles, the sales variances would be Price Volume A $160 (A) $100 (F) B $160 (A) $250 (F) C $170 (A) $250 (F) D $170 (A) $100 (F) (2 marks)

8 ©Tony Surridge Online Limited, 2012

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Question 6 T Company uses a standard costing system, with its material inventory account being maintained at standard costs. The following details have been extracted from the standard cost card in respect of direct materials. 8 kg @ $0.80/kg = $6.40 per unit Budgeted production in April was 850 units. The following details relate to actual materials purchased and issued to production during April when actual production was 870 units. Materials purchased 8,200 kg costing $6,888 Materials issued to production 7,150 kg Which of the following correctly states the material price and usage variances to be reported? Price Usage A $286 (A) $152 (A) B $286 (A) $280 (A) C $286 (A) $294 (A) D $328 (A) $152 (A) (2 marks) Question 7 PG Company operates a standard costing system for its only product. The standard cost card is as follows. Direct materials (4 kg @ $2/kg) $ 8.00 Direct labour (4 hours @ $4/hour) $16.00 Variable overhead (4 hours @ $3/hour) $12.00 Fixed overhead (4 hours @ $5/hour) $20.00 Fixed overheads are absorbed on the basis of labour hours. Fixed overhead costs are budgeted at $120,000 per annum arising at a constant rate during the year. Activity in period 3 is budgeted to be 10% of total activity for the year. Actual production during period 3 was 500 units, with actual fixed overhead costs incurred being $9,800 and actual hours worked being 1,970. The fixed overhead expenditure variance for period 3 was A $2,200 (F) B $200 (F) C $50 (F) D $200 (A) (2 marks)

9 ©Tony Surridge Online Limited, 2012

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

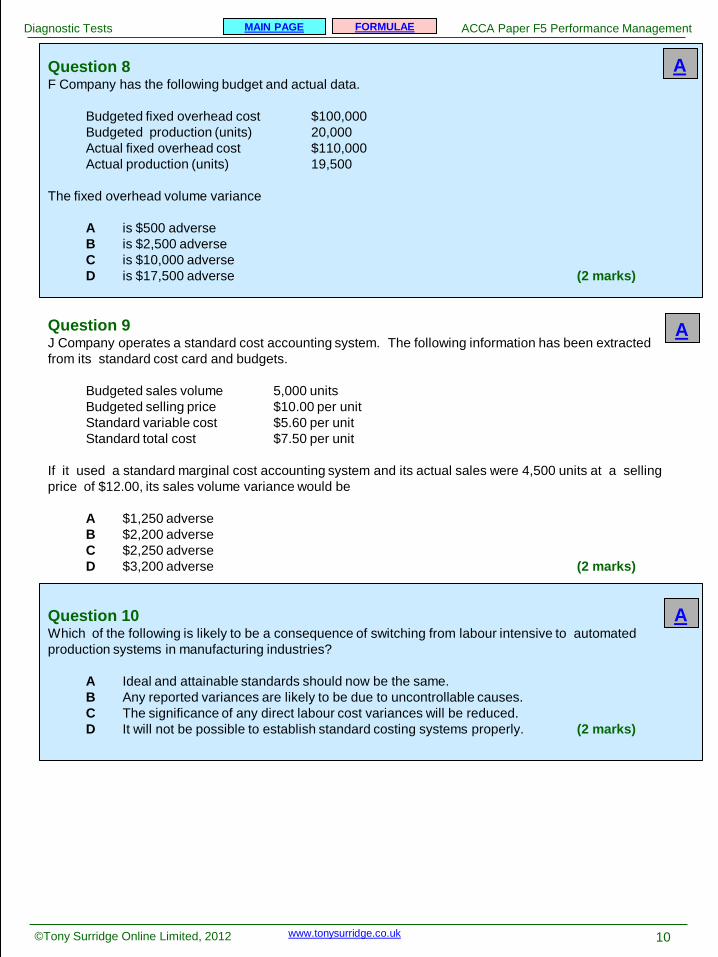

Question 8 F Company has the following budget and actual data. Budgeted fixed overhead cost $100,000 Budgeted production (units) 20,000 Actual fixed overhead cost $110,000 Actual production (units) 19,500 The fixed overhead volume variance A is $500 adverse B is $2,500 adverse C is $10,000 adverse D is $17,500 adverse (2 marks) Question 9 J Company operates a standard cost accounting system. The following information has been extracted from its standard cost card and budgets. Budgeted sales volume 5,000 units Budgeted selling price $10.00 per unit Standard variable cost $5.60 per unit Standard total cost $7.50 per unit If it used a standard marginal cost accounting system and its actual sales were 4,500 units at a selling price of $12.00, its sales volume variance would be A $1,250 adverse B $2,200 adverse C $2,250 adverse D $3,200 adverse (2 marks) Question 10 Which of the following is likely to be a consequence of switching from labour intensive to automated production systems in manufacturing industries? A Ideal and attainable standards should now be the same. B Any reported variances are likely to be due to uncontrollable causes. C The significance of any direct labour cost variances will be reduced. D It will not be possible to establish standard costing systems properly. (2 marks)

10 ©Tony Surridge Online Limited, 2012

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

The following data refers to Questions 11 - 13 Armenia Sling Company manufactures and sells a single product. Shown below is a summary of the budget for the year and actual results. Budget Actual $ $ $ $ Sales 500,000 600,000 Direct materials costs 200,000 300,000 Other costs (all fixed) 250,000 250,000 450,000 550,000 Profit 50,000 50,000 Fanny Bone, the company's owner, made two decisions on 1 January (1st day of the year). (1) She reduced the sales price of the product by 25% for all units sold in the year. (2) She switched to a different supplier for direct materials, purchasing a lower quality material but obtaining a 20% reduction on the budgeted price. There were no inventories of direct materials, work in progress or finished goods on either 1 January or 31 December. It is to be assumed that the original budget shown above was an accurate estimate of the likely results for the year before these two decisions were made. The original budget is to be taken as a basis for comparison with actual results, for budgetary control purposes. Question 11 Contribution is the difference between sales price and variable cost. What were the sales volume contribution variance and the sales price variance in the year, in $'000? Sales volume Sales price variance variance A $ 60 (F) $150 (A) B $150 (F) $200 (A) C $180 (F) $150 (A) D $180 (F) $200 (A) (3 marks) Question 12 What was the direct materials price variance in the year in $'000? A $20 (F) B $50 (F) C $60 (F) D $75 (F) (2 marks)

11 ©Tony Surridge Online Limited, 2012

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Question 13 The direct materials usage variance in the year (in $'000) was A $60 (A) B $55 (A) C $25 (A) D $20 (F) (3 marks) The following data refers to Questions 14 - 15 The budgeted sales of Product X in August were 2,400 units. Bruce Chinn Company, the company that manufactures Product X, uses a standard costing system, and the standard cost per unit of Product X is $21. The company recorded the following variances for the month. Sales price variance $ 300 (A) Sales volume profit variance $1,200 (F) During August 2,700 units of Product X were actually sold. Question 14 What was the budgeted profit for Product X in August? A $6,300 B $7,200 C $9,600 D $10,800 (2 marks) Question 15 What was the actual sales revenue for Product X in August? A $57,600 B $67,200 C $67,500 D $68,400 (2 marks) Question 16 A cleaning detergent, D5, is manufactured by mixing three materials. Standard cost details of the product are as follows: Cost per batch of 15 litres of D5: $ Material X 9 litres at $4.50 per litre 40.50 Material Y 4.5 litres at $1.50 per litre 6.75 Material Z 1.5 litres at $7.50 per litre 11.25 58.50

12 ©Tony Surridge Online Limited, 2012

This question is continued on the next screen

A

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

In October, the actual mix used was 300 litres of X, 112.5 litres of Y and 37.5 litres of Z. The output achieved was 420 litres of detergent D5. The material mix variance for each material was: Material X Material Y Material Z A $135 (F) $42.85 (A) $52.50 (A) B $130 (F) $42.85 (F) $56.25 (A) C $135 (A) $33.75 (F) $56.25 (F) D $130 (A) $33.75 (A) $52.50 (F) (2 marks) Question 17 Compare and contrast standard costing with the calculation of variances through budget flexing. (4 marks) Question 18 Describe briefly five purposes of a system of standard costing. (5 marks) Question 19 Explain three different levels of performance which may be incorporated into a system of standard costing. (3 marks) Question 20 Comment on whether standard costing applies in both manufacturing and service businesses and how it may be affected by modern initiatives of continuous improvement and cost reduction. (4 marks) Question 21 Discuss the problems associated with the use of traditional standard costing and variance analysis. (8 marks) Question 22 Comment on the meaning of the material mix variance and the yield variance. (3 marks) Question 23 "A high rate of inflation tends to make standard costing and variance analysis a waste of time" said the production manager to her managing director. You are required, as the management accountant, to draft a brief memorandum to the production manager in reply to her statement. (5 marks)

13 ©Tony Surridge Online Limited, 2012

A

A

A

A

A

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

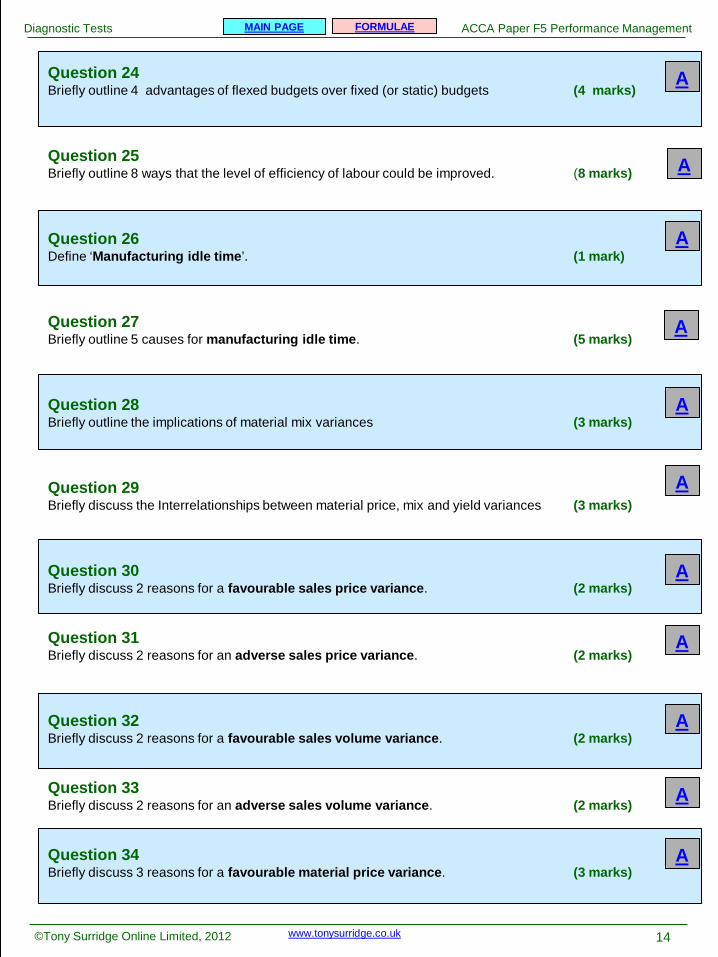

Question 24 Briefly outline 4 advantages of flexed budgets over fixed (or static) budgets (4 marks) Question 25 Briefly outline 8 ways that the level of efficiency of labour could be improved. (8 marks) Question 26 Define ‘Manufacturing idle time’. (1 mark) Question 27 Briefly outline 5 causes for manufacturing idle time. (5 marks) Question 28 Briefly outline the implications of material mix variances (3 marks) Question 29 Briefly discuss the Interrelationships between material price, mix and yield variances (3 marks) Question 30 Briefly discuss 2 reasons for a favourable sales price variance. (2 marks) Question 31 Briefly discuss 2 reasons for an adverse sales price variance. (2 marks) Question 32 Briefly discuss 2 reasons for a favourable sales volume variance. (2 marks) Question 33 Briefly discuss 2 reasons for an adverse sales volume variance. (2 marks) Question 34 Briefly discuss 3 reasons for a favourable material price variance. (3 marks)

14 ©Tony Surridge Online Limited, 2012

A

A

A

A

A

A

A

A

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

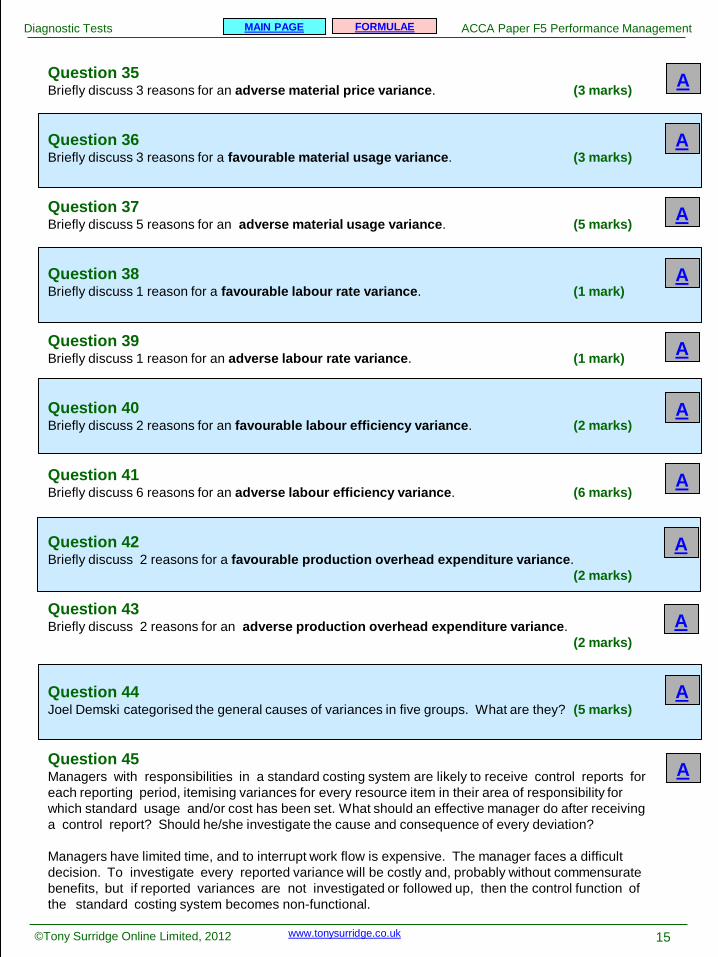

Question 35 Briefly discuss 3 reasons for an adverse material price variance. (3 marks) Question 36 Briefly discuss 3 reasons for a favourable material usage variance. (3 marks) Question 37 Briefly discuss 5 reasons for an adverse material usage variance. (5 marks) Question 38 Briefly discuss 1 reason for a favourable labour rate variance. (1 mark) Question 39 Briefly discuss 1 reason for an adverse labour rate variance. (1 mark) Question 40 Briefly discuss 2 reasons for an favourable labour efficiency variance. (2 marks) Question 41 Briefly discuss 6 reasons for an adverse labour efficiency variance. (6 marks) Question 42 Briefly discuss 2 reasons for a favourable production overhead expenditure variance. (2 marks) Question 43 Briefly discuss 2 reasons for an adverse production overhead expenditure variance. (2 marks) Question 44 Joel Demski categorised the general causes of variances in five groups. What are they? (5 marks) Question 45 Managers with responsibilities in a standard costing system are likely to receive control reports for each reporting period, itemising variances for every resource item in their area of responsibility for which standard usage and/or cost has been set. What should an effective manager do after receiving a control report? Should he/she investigate the cause and consequence of every deviation? Managers have limited time, and to interrupt work flow is expensive. The manager faces a difficult decision. To investigate every reported variance will be costly and, probably without commensurate benefits, but if reported variances are not investigated or followed up, then the control function of the standard costing system becomes non-functional.

15 ©Tony Surridge Online Limited, 2012

A

A

A

A

A

A

A

A

A

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Between the two extremes of investigating every variance that is reported and of investigating none of them, lies the optimal policy. However decision models specifying exactly which variances to investigate cannot deal with all aspects of the problem and in practice the decision becomes a subjective one, and is often left to the manager using discretion within the framework of general rules. Briefly outline five investigation decision-rule models that could be used to help resolve the problems identified above. (5 marks) Question 46 Briefly discuss the weakness of using the ‘monetary size of the variance investigation model’. (6 marks)

16 ©Tony Surridge Online Limited, 2012

END

A

A

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

END OF THE DIAGNOSTIC TEST FOR

STANDARD COSTING AND VARIANCE ANALYSIS

17 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Diagnostic Test Standard Costing and

Variance Analysis Answer Guides

ACCA Paper F5 Performance Management

18 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 1 B Price variance $ 3,800 kg should cost (x $4.50) 17,100 but did cost 14,400 Material price variance 2,700 (F) Note Units purchased = Units used + Closing inventory - Opening inventory = 4,100 - 300 = 3,800 kg Usage variance 1,040 units should use (x 4 kg) 4,160 kg but did use 4,100 kg Variance in kg 60 kg (F) x standard cost per kg $4.50 Material usage variance $270 (F) Answer to Question 2 D $ 11,700 hrs should cost (x $6.40) 74,880 but did cost 64,150 Labour rate variance 10,730 (F) 2,300 units should take (x 4.5 hrs) 10,350 hrs but did take 11,700 hrs Variance in hrs 1,350 hrs (A) x standard rate per hr x $6.40 Labour efficiency variance $8,640 (A) Answer to Question 3 D Overhead expenditure should have been $ ((800 x $6) + ((10,800 x $4)/12) 8,400 but was 8,500 Overhead expenditure variance 100 (A) $ Budgeted production at standard rate of absorption of fixed overheads ([10,800/12] x 4) 3,600 Actual production at standard rate (800 x 4) 3,200 Overhead volume variance 400 (A)

19 ©Tony Surridge Online Limited, 2012

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 4 C $ 13,450 hours should have cost (x $6) 80,700 but did cost 79,893 Direct labour rate variance 807 (F) 3,350 units should have taken (x 4 hrs) 13,400 hrs but did take 13,450 hrs Variance in hrs 50 hrs (A) x standard rate per hour x $6 Direct labour efficiency variance $ 300 (A) Answer to Question 5 C Actual sales 850 units Budgeted sales 800 units Variance in units 50 units (F) x standard contribution per unit ($(9 - 4)) x $5 Sales contribution volume variance $250 (F) $ Revenue for 850 units should have been (x $9) 7,650 but was 7,480 Selling price variance 170 (A) Answer to Question 6 D If material inventory is valued at standard cost, the price variance is based on actual purchases, i.e. the whole variance is eliminated as soon as the material is purchased. Price variance $ 8,200 kg should have cost (x $0.80) 6,560 but did cost 6,888 328 (A) Usage variance 870 units should have used (x 8 kg) 6,960 kg but did use 7,150 kg Usage variance in kg 190 kg (A) x standard cost per kg x $0.80 $ 152 (A) Answer to Question 7 B Assumption. There are twelve equal periods in one year. $ Budgeted fixed overhead cost per period ($120,000 ÷ 12) 10,000 Actual fixed overhead cost 9,800 Fixed overhead expenditure variance 200 (F)

20 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 8 B Standard fixed overhead cost per unit = $100,000/20,000 = $5 per unit $ Actual production at standard rate (19,500 x $5) 97,500 Budgeted production at standard rate (20,000 x $5) 100,000 Fixed overhead volume variance 2,500 (A) Answer to Question 9 B Since J Company uses a standard marginal costing system, the sales volume variance will be valued at the standard contribution of $4.40 per unit ($10.00 - $5.60). Budgeted sales volume 5,000 units Actual sales volume 4,500 units Sales volume variance in units 500 units (A) x standard contribution per unit x $4.40 Sales contribution volume variance in $ $2,200 (A) Answer to Question 10 C Standard costing systems can be established in an automated manufacturing system. Variances might identify controllable causes (such as inefficient maintenance) and automation does not mean that ideal and attainable standards are the same. However, direct labour costs will become a much smaller proportion of total costs, and so the significance of any direct labour cost variances will be much less than in non-automated systems or systems with a bigger labour element. Answer to Question 11 D Remove the price increase from the actual sales revenue: $600,000/0.75 = $800,000 (at budget prices). Actual sales (at same price level as budget) increased by $300,000 ($800,000 - $500,000.) The contribution in the budget is $500,000 - $200,000 = $300,000, or 60c per $1 of sales. Sales contribution volume variance = 60% of $300,000 (F) = $180,000 (F) Actual sales in the year = $600,000 Sales price actually charged = 75% of original budgeted sales price Actual sales at original budgeted price = $800,000 Sales price variance ($800,000 - $600,000) = $200,000 (A) Answer to Question 12 D Actual direct materials costs in the year = $300,000. This is 80% of the original budgeted price. Actual purchase quantities at original budget price = $300,000 ÷ 0.80 = $375,000. Material price variance = $375,000 - $300,000 = $75,000 (F)

21 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 13 B Actual production and sales = 160% of original budgeted quantity. ($800,000/$500,000) $ 160% of original budget quantity should use (x 1.6) ($200,000 x 1.6) 320,000 of materials at budget price but did use ($300,000/0.8) 375,000 of materials at budget price Usage variance 55,000 (A) Note $ $ Budgeted profit 50,000 Sales price variance 200,000 (A) Sales volume variance 180,000 (F) Materials price variance 75,000 (F) Materials usage variance 55,000 (A) Total variances 0 Actual profit (given in question) 50,000 Answer to Question 14 C Budgeted sales 2,400 units Actual sales 2,700 units Sales volume variance in units 300 units (F) x standard profit per unit X (unknown!) Sales volume variance in $ $1,200 (F) Thus, standard profit per unit (1,200 ÷ 300) $4 (thus, X = $4.) Budgeted profit in the month (2,400 units x $4) $9,600 Answer to Question 15 B $ Standard profit per unit 4 Standard cost per unit 21 Standard selling price per unit 25 $ 2,700 units should sell for (x 25) 67,500 Sales price variance 300 (A) 2,700 units did sell for 67,200

22 ©Tony Surridge Online Limited, 2012

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 16 C Workings: Weighted average standard price (WASP) per litre = $58.50/15 litres = $3.90. Actual usage Standard mix Mix variance Rate Mix variance litres litres litres $ $ Material X 300 (9/15) 270 30 (A) 4.50 135 (A) Material Y 112.5 (4.5/15) 135 22.5 (F) 1.50 33.75 (F) Material Z 37.5 (1.5/15) 45 7.5 (F) 7.50 56.25 (F) 450 450 45 (A) Answer to Question 17 The calculation of variances through budget flexing is achieved by adjusting the budget for the period to produce a realistic budget cost allowance for the actual level of activity achieved. The variance is the difference between the actual cost or revenue and the budgeted cost or revenue for the actual level of activity. The analysis of variances in a standard costing system is achieved by the comparison of the cost incurred with the standard cost that should have been incurred for the actual level of activity. There are therefore similarities between variance analysis with flexible budgets and standard costs. Both approaches compare the actual costs for a given level of activity with the expected costs for that volume of activity. However, there are differences between the two approaches. - With standard costing, variances are analysed in detail, reporting for example direct material price and direct material usage variances. With flexible budgeting, the reported cost variances are more likely to be total cost variances, e.g. total direct material cost variance. - All products or services are valued at standard cost in a standard costing system. With flexible budgeting there is not necessarily a standard costing system. Output is costed using normal costing methods. - With standard costing, all products or services have a standard selling price. With flexible budgeting, standard selling prices are unlikely to be used. Answer to Question 18 A standard costing system supports management in a number of ways. For example: (i) It can assist in the planning of budgets. Standards are the building blocks of periodic budgets. (ii) Standards are used for control purposes. They are used as performance indicators and the variances that are derived from the system reveal activities which are different from plans. This informs management of the need to take action to take advantage of any circumstances which have produced favourable variances or reduce or mitigate the effects of any adverse variances. (iii) If the prerequisites of a standard costing system are observed, the existence of appropriately set standards can act as targets and become a source of employee motivation.

23 ©Tony Surridge Online Limited, 2012

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

(iv) Standards are estimated costs which can be used to support decision making - such as pricing decisions. (v) Standard costs are often used for the valuation of inventory - raw materials, work-in-progress, finished goods. Answer to Question 19 Three different levels of performance are as follows: (a) Ideal standards An ideal standard is one which can be attained under the most favourable conditions possible (using maximum capacity) in the forthcoming period. The ideal standard will be revised period by period in the light of developments in technology, etc. Ideal standards will be used where management believe that they will provide the best type of standard needed for motivation and cost control. In some cases it will be reasonable to expect that no wastage of material will occur. However, in terms of labour efficiency, ideal standards, which would assume no inefficiency, no extra breaks, no loss of efficiency due to fatigue, may be no more than a pipe-dream. (b) Attainable standards A currently attainable standard will show the cost to be incurred under normal efficient operating conditions (the use of practical capacity). Allowances are made for normal wastage of materials, machine breakdowns, and loss of efficiency from fatigue. However although a currently attainable standard should be possible to achieve, it should also represent a high standard of performance. Standard costs determined in this way can be used for a variety of purposes, for example for budget preparation, for cost control by means of variance analysis, for product costing and for motivation. (c) Budget standard The budget standard is the standard set for the budget period and is normally based on the sales volume, and thus production volume, budgeted for the period concerned. Answer to Question 20 Relevant for mass production Standard costing is most suited to organisations whose activities consist of a series of common or repetitive operations. Typically, mass production systems are indicative of its main area of application. Use in service provision businesses It is possible to envisage the operation of standard costing and variance analysis systems within the service sector, though standards might not be set with the same degree of accuracy which apply in manufacturing due to the heterogeneous and intangible nature of services. For example, banks will have common processes for dealing with customer transactions, processing cheques etc, transport companies will have standard routes and vehicles, hotels and restaurants often use standard recipes for food preparation, and so on. Standards used in modern industry In modern industry, which includes both the manufacturing and service sectors, continuous improvement and cost reduction can be key issues which render standard costing difficult to apply. In order to remain competitive, it is essential that businesses address the cost levels of their various operations. But the continuous quest to reduce costs may mean that standards become transient and soon out of date. In such a situation, an alternative to the use of standard costing is to compare actual costs with those of a previous period, or to benchmark actual costs against industrial norms.

24 ©Tony Surridge Online Limited, 2012

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Managers must decide It is for management to judge the pros and cons of employing standard costing, and consequently whether such a system is appropriate for their needs. Answer to Question 21 Traditional standard costing systems are widely used though they present weaknesses. Examples are: E Emphasis on monetary values. The monetary values are used at the exclusion of important non-monetary measures and indicators. N No encouragement for managers to exceed the standard set. The cybernetic control system does not respond when standards are achieved. D Difficulty in setting accurate standards. Even the use of different policy levels of standard ('ideal', 'attainable' and 'budgeted') does not resolve the difficulties of setting accurate standards. B Batch related management reporting. The system is normally periodical (say monthly or four- weekly) and relates to batches. This long delay in reporting is unacceptable to operational managers working in modern factories. A Aggregated financial figures are often used. Reported figures are aggregates, and thus lose management value. What is the 'knowledge and understanding' difference between a reported variance of, say, $10,000 (A) and $12,000 (A)? S Surrogate financial figures are often used. The system places financial surrogate values on events which may cause inaccuracies, misunderstanding and subjectivity. Furthermore, the act of evaluating events in financial values tends to slow the reporting cycle. I Includes variances which might not be helpful for management. For example. conventional variances relating to material price, material usage, labour efficiency are not helpful in modern 'JIT' orientated factories. S Standards often include costs that are not relevant. Standard costs are often used for cost- based decisions. Standards do not relate to 'relevant costs' and may not be appropriate for short- run decisions. Tutorial comment: Remember our mnemonic 'END BASIS‘ Answer to Question 22 The material mix variance shows the increase (or reduction) in costs caused by the substitution of expensive materials for more cheaper (or cheaper materials for more expensive). It is not clear that a favourable mix variance represents an improvement for the firm. A short-term saving in costs may lead to a reduction in product quality with consequent quality costs. The standard is set with an appropriate mix. A deviation from this standard might represent a reduction in customer satisfaction (consider increasing the cheaper materials in a cake mix) with subsequent losses of sales in the future.

25 ©Tony Surridge Online Limited, 2012

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

An adverse yield variance represents an over-usage of materials in respect of the output actually achieved. A favourable yield variance represents a savings of normal loss. If a normal loss is not budgeted it is difficult to envisage a favourable yield variance, unless again, there has been a loss of quality. The mix and yield variance add to the total of the usage variances of the different materials incorporated in the mix, and in this respect are related. For example, a change in the mix could result in an increase in defective units (and thus an increase in the material usage). In the same way as for a usage variance, the usage variance could be due to a number of factors not related to the mix, such as machine malfunctioning, poor quality labour, and so on. Answer to Question 23 MEMORANDUM To: Production manager From: Management accountant 10th September Subject: Standard costing and variance analysis under inflationary conditions I have been requested by the managing director to respond to your comment on standard costing and variance analysis in time of inflation. Standard costs are made up of two elements: (i) a quantity of resource required per unit, and (ii) an estimated price per unit of the resource. When setting a value for the price element two possibilities exist: (i) to use a price prevailing at the start of the year; or (ii) to estimate an average price to be paid during the year ahead. Both methods cause difficulties. Method (i) will cause adverse (often uncontrollable) price variances as inflation causes prices to rise. Method (ii) would (in theory) cause favourable variances in the early periods of a year and adverse variances in the later periods of a year which will (if the estimated price is accurate) total to a nil variance for the year. Either of these techniques will allow an analysis of the trends of costs to be recognised. A further alternative is to revise the price element of the standard cost each accounting period, but this makes trend analysis very difficult. Variances arising from the use of Method (i), which involves retaining the standard price (unchanged) for the year can be improved and made more meaningful by the use of planning and operational variances. Using this approach the inflationary element might be treated as a planning variance, which is uncontrollable as far as operational management are concerned, with operational variances, the controllable element of the activity, highlighted for management attention. Thus the two price related variances may be of use under inflationary conditions.

26 ©Tony Surridge Online Limited, 2012

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 24 The main advantages of flexed budgets over fixed (or static) budgets are: (i) They are prepared for a range of activity instead of a single level. (ii) They supply a dynamic basis for comparison because they are automatically geared to changes in volume. (iii) They aid in the planning of budgets based on estimated capacity levels. (iv) They make variable costs and fixed costs transparent for management attention. Answer to Question 25 An improvement in the level of efficiency of labour can be achieved in different ways: S Satisfaction (job satisfaction) for workers. This relates to ‘Motivation Theory’. E Effective recruitment and selection of staff. Use of good interviewing techniques and psychographic testing, etc. E Employees being fully supported by managers, particularly workers new to the job. W Working conditions. E Efficient and effective work systems (routing, machine loading and logistical planning, etc.). Q Quality of plant and machinery, and its maintenance. U Use of ‘payments by results’ payment schemes. I Increase in the level of training. C Constructive teambuilding and teamwork. K Knocking down of demarcation ‘walls’ dividing workers, managers and departments. Tutorial comment: Remember our mnemonic ‘SEE WE QUICK‘ Answer to Question 26 Manufacturing idle time can be defined as: ‘time when an employee is unable to work because of some factor beyond his or her control. Usually the worker receives payment during idle time’. Answer to Question 27 The main causes for manufacturing idle time are: S Short orders. The budgeted sales order capacity is less than the attainable manufacturing capacity. P Production mix which is impossible to route through the factory without causing bottlenecks, or else bottlenecks caused by the differing capacities of equipment which are manufacturing the same product. A Absenteeism of staff, for whatever reason, can cause idle time for other employees. S Stock-outs when substitution material (if technically suitable) is also not available. M Machine malfunctions, also machine maintenance and ‘setting-up’ machines between batch runs. Tutorial comment: Remember our mnemonic ‘SPASM‘

27 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 28 A favourable mix variance would result from substituting cheaper materials for more expensive materials but this may not always be in a firm's best interests as the quality of the product may suffer or output may be reduced. An adverse mix variance would have the opposite effect of substituting expensive materials in the place of cheaper materials. There are two main reasons why this may occur: (i) a stock-out of the cheaper material occurs and it is economical to use expensive materials and maintain throughput; or (ii) there is a fault in the process, probably in the mixing machinery (most mixing is done by machine, like petrol and air is mixed in a car engine). Answer to Question 29 Generally, the use of a less expensive mix of material input will mean the production of fewer output than standard. This may be because of an increase in rejects due to imperfections in the lower quality inputs, or other similar factors. The overall result may be: - favourable material price variance - because less expensive materials are purchased - favourable mix variance - because some of these less expensive materials have been substituted for more expensive materials - adverse yield variance because the inferior materials have resulted in more defects and waste. Answer to Question 30 Possible causes of a favourable sales price variance are: Increase of sales price to take advantage of market price elasticity. A reduction in discounts planned. (Discounts effectively reduce the sales price.) Answer to Question 31 Possible causes of a averse sales price variance are: Reduction of sale price to take advantage of market price elasticity. The unplanned discounts given to customers.

Answer to Question 32 Possible causes of a favourable sales volume variance are: A reduction in the sales price has resulted in an increase in sales volume (demand). An increase in the firm’s share of market due to marketing activities such as advertising, product positioning, etc. Answer to Question 33 Possible causes of a averse sales volume variance are: An increase in the sales price has resulted in a fall in sales volume (demand). Loss of share of market due to ineffective marketing activities and offensive actions of competitors.

28 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 34 Possible causes of a favourable material price variance are: Unforeseen discounts received. Greater effectiveness in purchasing. Change in material prices. Answer to Question 35 Possible causes of a averse material price variance are: Price increases. Ineffective purchasing. Change in supplier’s discount policy. Answer to Question 36 Possible causes of a favourable material usage variance are: Material used of higher quality than standard. More effective use made of material. Errors in allocating materials to jobs (mix of materials). Answer to Question 37 Possible causes of a averse material usage variance are: Defective material Excessive waste. Theft. Stricter quality control (more rejects) Errors in allocating material to jobs. (mix of materials). Answer to Question 38 The main possible cause of a favourable labour rate variance is the use of apprentices or other workers at a rate of pay lower than standard. Answer to Question 39 The main possible cause of a averse labour rate variance results from unplanned wage rate increases. Answer to Question 40 Possible causes of a favourable labour efficiency variance are: Output produced more quickly than expected, i.e. actual output in excess of standard output set for the same number of hours because of staff motivation, effective supervision, better quality of equipment or materials, etc. Errors in allocating time to jobs.

29 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Answer to Question 41 Possible causes of a averse labour efficiency variance are: Idle time in excess of standard allowed. Machine breakdown(s). Non-availability of materials (stock outs). Absence or injury of workers. Output lower than standard because of deliberate labour ‘go slow’, lack of training, or sub-quality material used. Errors in allocating time to jobs. Answer to Question 42 Possible causes of a favourable production overhead expenditure variance are: Savings in costs incurred. More economical use of services. Answer to Question 43 Possible causes of a averse production overhead expenditure variance are: Increase in cost of services used. Change in type of services used.

Answer to Question 44 Joel Demski categorised the causes of variances in five groups: (i) Implementation deviation caused by a human or mechanical failure to achieve attainable standard, e.g. an over-usage of material due to ineffective supervision in the factory. (ii) Prediction deviation caused from errors in specifying the standard costs or other parameter values in a decision model, e.g. in determining the labour cost standard affected by a learning rate, ex ante predictions must be made, inter alia, of the future level of activity and the extent of learning. If the predictions are incorrect the labour standard will be wrong and variances will occur. (iii) Measurement deviation caused as a result of error in measuring the actual outcome, e.g. an adverse material variance reported in one process with a favourable usage variance for the same material in another process, caused by incorrect postings by the storekeeper. (iv) Model deviation which results from an error in the formulation of a decision model, e.g. in formulating a model to determine the rate of pay of workers involved in a group incentive bonus scheme, the treatment of allowances (such as contingency, relaxation and process allowances) incorporated in the basic standard hour may be incorrectly specified or dealt with. (v) Random deviations due to chance fluctuations of a cost or other parameter for which no cause can be identified, e.g. a small adverse labour efficiency variance for a period in which climatic temperature was particularly warm, a factor which may, or may not, have caused the variance. By definition a random variance per se calls for no control action affecting the current process.

30 ©Tony Surridge Online Limited, 2012

Q

Q

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

©Tony Surridge Online Limited, 2012 31

Answer to Question 45 The investigation decision-rule models that can be identified are: (i) Monetary significance of the variance model A variance is investigated if it exceeds a certain monetary size - say $500. (ii) Fixed percentage significance of standard model Another simple rule is to choose a fixed percentage, say 10 per cent and investigate all variances that exceed the standard by this amount. Using, for example, a material 'NN' used in a manufacturing process with a standard usage of 2.1 kilograms per standard hour. With a 10 per cent significance the upper and lower control limits are 2.31 (2.1. x 1.1) and 1.89 (2.1 x 0.9) kilograms respectively. If the average usage of material for a control period was reported as 2.25 kilograms it would not be highlighted for attention. The model is easy to implement, once the manager on the basis of the historical results, or comparisons with other work aided by experience and judgement, specifies the appropriate percentage to use. (iii) Statistical significance model The model requires that a measure of expected dispersion be specified for each account item. Using for example, a material ‘NN’ with a standard usage of 2.1 kilograms per standard hour, obtained from records of the average usage of the material in the process over the previous fifteen months and when production levels were approximately equal in each of the months sampled so that each observation can be weighed equally, and the data used to calculate a standard deviation, of say 0.056 kilos. The data could be used to set control limits based on: - say a confidence level of 95% (which is 1.96 standard deviation from the average) - the assumption of normally distributed deviations (say, +/- 0.11 kilos). If the variance is over 2.21 kgm (2.1 + 0.11) or under 1.99 (2.1 - 0.11) the manager could accept that the deviation is unusual, because probability of it occurring is less than 0.05 (5 chances in 100). (iv) Decision with costs and benefits of investigation model A simple decision theory model, based on cost-benefit analysis, using prior-period result analysis (i.e. probabilities of events based on previous periods). (v) The use of rule of thumb policy Managers take subjective judgement based on the situation, their experience, intuition and needs. Usually this means that the bigger the variance the more chance there is that it will be investigated. Hunch plays a part in the decision process. However, in practice, the size of a variance and its significance may not correlate. Such an informal approach to the investigation of variances would probably lead to unproductive investigative work. Answer to Question 46 The weaknesses of the monetary size of the variance include the following:

This answer is continued on the next screen

Q

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

©Tony Surridge Online Limited, 2012 32

(i) the choice of the monetary size, $500, $1,000, $1,500, or whatever, is likely to be subjective; (ii) it ignores the cost of investigating a variance; (iii) it does not consider type and probable cause of the variance; (iv) it does not reflect that some accounts are more important than others, in terms of interrelationships, trade off, etc.; (v) it will not signal when an important account that historically has been controlled very closely, suddenly departs from its historical pattern but with a variance that is still within the present monetary values; (vi) it will trigger investigation into accounts where sizable fluctuation is normally experienced from period to period. The model can be improved by the use of cost-benefit analysis based on statistical probabilities. With this approach probabilities (based on historical analysis of variances) that a variance of a certain size is likely to be controllable are measured. The net benefits from control action, the costs of investigation and the costs of control are incorporated in the decision-rule model.

END

Q

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

©Tony Surridge Online Limited, 2012

33

Score sheet: Diagnostic Test: Standard Costing and Variance Analysis

Question number

Marks available

Score

1 3

2 2

3 2

4 2

5 2

6 2

7 2

8 2

9 2

10 2

11 3

12 2

13 3

14 2

15 2

16 2

17 4

18 5

19 3

20 4

21 8

22 3

23 5

24 4

Total score c/fwd

Question number

Marks available

Score

Total score b/fwd

25 8

26 1

27 5

28 3

29 3

30 2

31 2

32 2

33 2

34 3

35 3

36 3

37 5

38 1

39 1

40 2

41 6

42 2

43 2

44 5

45 5

46 6

Total score 143

Percentage (%)

111 – 143 marks 73 – 110 marks 0 – 72 marks

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

The managers of Albion Company are reviewing the operations of the company with a view to making operational decisions for the next month. Details of some of the products manufactured by the company are given below. Product AR2 GL3 HT4 XY5 Selling price ($/unit) 21·00 28·50 27·30 Material R2 (kg/unit) 2·0 3·0 3·0 Material R3 (kg/unit) 2·0 2·2 1·6 3·0 Direct labour (hours/unit) 0·6 1·2 1·5 1·7 Variable production overheads ($/unit) 1·10 1·30 1·10 1·40 Fixed production overheads ($/unit) 1·50 1·60 1·70 1·40 Expected demand for next month (units) 950 1,000 900 Products AR2, GL3 and HT4 are sold to customers of Albion Company, while Product XY5 is a component that is used in the manufacture of other products. Albion Company manufactures a wide range of products in addition to those detailed above. Material R2, which is not used in any other of Albion’s products, is expected to be in short supply in the next month because of industrial action at a major producer of the material. Albion Company has just received a delivery of 5,500 kg of Material R2 and this is expected to be the amount held in inventory at the start of the next month. The company does not expect to be able to obtain further supplies of Material R2 unless it pays a premium price. The normal market price is $2·50 per kg. Material R3 is available at a price of $2·00 per kg and Albion Company does not expect any problems in securing supplies of this material. Direct labour is paid at a rate of $4·00 per hour. Folam Company has recently approached Albion Company with an offer to supply a substitute for Product XY5 at a price of $10·20 per unit. Albion Company would need to pay an annual fee of $50,000 for the right to use this patented substitute. Required: (a) Determine the optimum production schedule for Products AR2, GL3 and HT4 for the next month, on the assumption that additional supplies of Material R2 are not purchased. (7 marks) (b) If Albion Company decides to purchase further supplies of Material R2 to meet demand for Products AR2, GL3 and HT4, what should be the maximum price per kg that the company is prepared to pay? (3 marks) (c) Discuss whether Albion Company should manufacture Product XY5 or buy the substitute offered by Folam Company. Your answer must be supported by appropriate calculations. (5 marks) (d) Discuss the limitations of marginal costing (variable costing) as a basis for making short-term decision. (5 marks) (20 marks)

Albion Company: Question - 1 of 1 (A question covering the optimum production schedule and make or buy)

34

A

A

A

A

©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

(a) The optimum production schedule is found using limiting factor analysis. AR2 GL3 HT4 Material R2 ($/unit) 2·5 x 2 = 5·00 2·5 x 3 = 7·50 2·5 x 3 = 7·50 Material R3 ($/unit) 2 x 2 = 4·00 2 x 2·2 = 4·40 2 x 1·6 = 3·20 Labour ($/unit) 4 x 0·6 = 2·40 4 x 1·2 = 4·80 4 x 1·5 = 6·00 Variable o/h ($/unit) 1·10 1·30 1·10 Variable costs ($/unit) 12·50 18·00 17·80 Selling price ($/unit) 21·00 28·50 27·30 Contribution ($/unit) 8·50 10·50 9·50 Material R2 (kg/unit) 2 3 3 Contribution ($/kg of R2) 8·5/2 = 4·25 10·5/3 = 3·50 9·5/3 = 3·17 Ranking 1 2 3 Product Demand (units) R2 used (kg) Production (units) Contribution ($) AR2 950 1,900 950 8,075 GL3 1,000 3,000 1,000 10,500 HT4 900 600 200 1,900 5,500 20,475 The optimum production schedule is 950 units of Product AR2, 1,000 units of GL3 and 200 units of HT4, giving a total contribution of $20,475. The fixed production overheads are ignored in this analysis because they are assumed not to vary with changes in the level of production. (b) Further supplies of Material R2 will be used to produce additional units of Product HT4. The contribution per kg of Material R2 of Product HT4 is $3·17 and so if Albion pays 3·17 + 2·50 = $5·67 per kg for Material R2, the additional units of Product HT4 produced will make a zero contribution towards fixed costs. $5·67 is therefore the maximum price. (c) The variable cost of Product XY5: $/unit Material R3: 3 x 2 = 6·00 Labour: 1·7 x 4 = 6·80 Variable overhead: 1·40 14·20 The substitute offered by Folam gives a saving of $4 per unit. However, Albion Company would also pay an annual fee of $50,000 for the right to use the substitute. The company would need to manufacture more than 50,000/4 = 12,500 units per year of Product XY5, or 1,042 units per month, in order for the offered substitute to be financially acceptable. If it needed less than 12,500 units of Product XY5 per year, it would be cheaper to manufacture the product in house. This evaluation is from a short- term perspective: in the longer term, buying in may lead to fixed cost savings and lower investment, increasing the benefits of buying in and lowering the break-even point. Albion Company would also need to assure itself that the quality of the substitute was acceptable and that this quality could be maintained: the lower price offered by Folam might be associated with poorer quality than that deemed necessary by Albion Company. Orders for the substitute product would also need to be delivered promptly in order to avoid production hold-ups.

Albion Company: Answer - 1 of 2 (A question covering the optimum production schedule and make or buy)

35

Q

Q

©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Albion Company could also become dependent on Folam Company for supplies of the substitute product and might be vulnerable to future price increases by the supplier. Such price increases might reduce or even eliminate the cost saving of buying in. (d) Marginal costing (variable costing) treats fixed costs as a period cost, on the assumption that fixed costs do not change in the short term. The difference between selling price and variable costs is the variable contribution made by units sold towards meeting fixed costs and generating profit. Marginal costing has traditionally been used for short-term decisions such as whether to cease production of a product, whether to make a product or buy it from a supplier, and how to allocate scarce resources in order to maximise contribution. A major limitation with using marginal costing as the basis for making short-term decisions is the assumption that fixed costs are irrelevant to short-term decisions. In the longer term, fixed costs will change: for example, rent is usually regarded as a fixed cost and in the longer term rent might be expected to increase due to inflation. However, a change in fixed costs may be the result of a short-term decision: for example, if a product is discontinued and as a result the work of the marketing department decreases, in the longer term marketing costs would be expected to decrease. This points to the danger of relying on a simplistic analysis of costs into fixed costs and variable costs, and of assuming that only variable costs are relevant for decision-making purposes. It is possible for a fixed cost to be a relevant cost. It is also possible for a variable cost to be irrelevant, for example in the case where a variable cost is common to two decision alternatives. If fuel costs are incurred whether a machine is leased or bought, for example, these costs are not relevant to the decision on whether to lease or buy. Reliance on marginal costing as a basis for making short-term decisions may therefore lead to sub- optimal decisions overall for a company, as the analysis may fail to consider all relevant costs. A relevant cost is an incremental or differential cost at the whole company level. If a cost changes or is incurred, now or in the future, as a result of a decision, it is a relevant cost and should be considered when making a decision. When making short-term decisions, therefore, it is essential to adopt a whole company perspective in determining relevant costs. When making short-term decisions, a detailed analysis of cost behaviour is therefore needed in order to determine not only variable costs and fixed costs, but relevant costs as well.

Albion Company: Answer - 2 of 2 (A question covering the optimum production schedule and make or buy)

That's one small step for a man, one giant leap for mankind.

Neil Armstrong

Neil Alden Armstrong (born August 5, 1930) is an American former astronaut, test pilot, aerospace engineer, university professor, United States Naval

Aviator, and the first person to set foot upon the Moon.

Neil Armstrong USAF / NASA Astronaut

36

Q

Q ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

+AddVance ACCA F5 Diagnostic Tests

Diagnostic Questions and Answers Contents 1 of 1

Tutorial Syllabus classification Screen

Questions Answers

Tutorial 1 Activity Based Costing (ABC) 19 25

Tutorial 2 Target Costing 36 40

Tutorial 3 Life-Cycle Costing (LCC) 84 51

Tutorial 4 Throughput Accounting (TA) 57 66

Tutorial 5 Environmental Accounting 77 81

Tutorial 6 Cost behaviour and break-even analysis 88 104

Tutorial 7 Multi-limiting factors and the use of linear programming 124 130

Tutorial 8 Pricing Decisions 136 143

Tutorial 9 Make-or-Buy and other short-term decisions 157 168

Tutorial 10 Dealing with risk and uncertainty 186 197

Tutorial 11 Budgetary systems and types of budgets 218 227

Tutorial 12 Quantitative analysis in budgeting 261 271

Tutorial 13 Standard costing and variance analysis (This test is activated for this free sample) 291 304

Tutorial 14 Planning and operational variances 324 328

Tutorial 15 The scope of performance measurement 334 344

Trust in Allah, but tie your camel first. Arabic proverb

37 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Title Page Question Jola Publishing Company

A question covering traditional overhead and ABC 362

Answer Jola Publishing Company 364 Question Triple Company

A question covering Activity Based Costing (ABC) 367

Answer Triple Company 368 Question Big Cheese Chairs

A question covering target costing and cost gap 371

Answer Big Cheese Chairs 372 Question Yam Company

A question covering throughput costing 375

Answer Yam Company 376 Question Albion Company

A question covering the optimum production schedule and make or buy 379

Answer Albion Company 380 Question Sniff Company

A question covering further processing and break-even 382

Answer Sniff Company 384 Question Stay Clean

A question covering stay open decision, pricing strategies and outsourcing 388

Answer Stay Clean 390 Question Shortflower Company

A question covering relevant costing and closure decisions 394

Answer Shortflower Company 395 Question Higgins Company

A question covering linear programming 397

Answer Higgins Company 398 Question Bits and Pieces

A question covering incremental revenue 403

Answer Bits and Pieces 404 Question Shifter’s Haulage Company

A question covering maximax, maximin and probability 407

Answer Shifter’s Haulage Company 408 Question McIntyre Resort

A question covering a profit maximising fee, decision re variable cost v fixed cost

411

Answer McIntyre Resort 413 Question Leysel Company

A question covering flexible budgeting and a fixed overhead variance) 418

Answer Leysel Company 419 Question Northlands

A question covering budgeting in public sector organisation 422

Answer Northlands 423

38

1 OF 2 Please click to the next screen

Exam status Questions and Answers Contents 1 of 2 Click to page 361

38 ©Tony Surridge Online Limited, 2012

Only Albion Company is activated for this free sample

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

Title Page Question Electrical goods manufacturing

A question covering production budgets and times series analysis 425

Answer Electrical goods manufacturing 426 Question The Western

A question covering cost estimation, incremental budgets 429

Answer The Western 430 Question BFG Company

A question covering financial performance appraisal 432

Answer BFG Company 433 Question Domestic Electrical Appliances

A question covering the correlation, regression and forecasting 436

Answer Domestic Electrical Appliances 437 Question Crumbly Cake

A question covering material variances, performance appraisal and bonus 440

Answer Crumbly Cake 442 Question Simply Soup Company

A question covering material price, mix and yield variances 445

Answer Simply Soup Company 447 Question Secure Net

A question covering material price/usage and planning/operating variances 450

Answer Secure Net 451 Question Spike Company

A question covering budget revision and sales variances 455

Answer Spike Company 457 Question Chaff Company

A question covering performance appraisal and variances 461

Answer Chaff Company 463 Question Oliver Hairdresser

A question covering financial performance appraisal 468

Answer Oliver Hairdresser 470 Question Pace Company

A question covering performance appraisal and bonus 473

Answer Pace Company 474 Question Preston Financial Services

A question covering financial performance appraisal 478

Answer Preston Financial Services 480 Question Thatcher International Park

A question covering performance appraisal 482

Answer Thatcher International Park 483 Question Z Company

A question covering value for financial performance appraisal 486

Answer Z Company 487

39

2 OF 2

Exam status Questions and Answers Contents 2 of 2 Click to page 361

39 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

We hope you enjoyed our free sample, and found it useful. For the FULL WORKING version, buy it NOW, online at...

40 ©Tony Surridge Online Limited, 2012

www.tonysurridge.co.uk

Diagnostic Tests ACCA Paper F5 Performance Management MAIN PAGE FORMULAE

41 ©Tony Surridge Online Limited, 2012

Sorry... But that link will not work in this free sample copy.

To buy the full version, complete with all links, and even more Diagnostic Tests and exam- status Questions and Answers covering 14 topics for your ACCA F5 studies, please go to

www.TonySurridge.co.uk

“Dedicated to the Accountancy and Finance Profession”