2013 annual report - akita-drillingusa.com · as a company founded to break through traditional...

TRANSCRIPT

2013 ANNUAL REPORT

GREATER DEPTHS. NEW HEIGHTS.

ABOUT XTREMEXtreme rilling an Coil Services Cor . esigns, uil s an o erates a eet o

high-s eci cation rilling rigs an coile tu ing well service units. ur eet is

equipped with numerous patented and proprietary technologies developed to

improve sa ety, per ormance and mo ility. We currently operate our X R drilling

rigs and XSR coiled tubing units under contracts with oil and natural gas explora-

tion and production companies and integrated oil eld service providers in orth

America and Asia.

A YEAR OF NEW BENCHMARKS

REVENUE (in millions) OPERATING DAYS EBITDA (in millions)

2009 2009 20092010 2010 2010

$229.8

8,068

$73.7

$174.5

6,550$35.0$104.0

4,602

$21.9

$85.6

3,247$22.1

$99.4

3,899 $26.0

2011 2011 20112012 2012 20122013 2013 2013

As a company founded to break through traditional barriers in our industry, Xtreme Drilling and Coil Services has been setting records almost since inception. However, nothing in our history quite compares to 2013.

It was an exceptional year on many fronts, as we established

new industry benchmarks with our eld performance and

surged past previous high-water marks for the company,

both operationally and nancially.

Our primary goal for 2013 was optimizing our operations

and maximizing ef ciency to capitalize on the aggressive

eet expansion we undertook previously. We are proud to

report we accomplished that mission, as last year was our

busiest and most productive ever for both the XDR and

XSR divisions of our company. Our operating days topped

8,000 for the rst time ever, pushing our revenue to a

record $229,823,000 even as we maintained the same rig

count. Other key nancial metrics hit historic levels as well,

including pro t margins and EBITDA.

Xtreme also made great strides in strengthening the balance

sheet, using our growing free cash ows to substantially

reduce leverage incurred during our $200+ million capital

expansion program. We are pleased that the marketplace

recognized this progress, as our share price increased by

118 in 2013.

Also of note, our business came full circle in an important

sense in 2013. Xtreme s history is deeply rooted in driving

innovation in coiled tubing drilling technology, and we have

numerous patents to show for it. However, in recent years

we shifted our focus almost entirely to traditional jointed

pipe drilling in response to the rapid proliferation of horizontal

wells in orth American resource plays. ow we are excited

to be putting that breakthrough coiled tubing technology to

work again this time, for ultra-deep completions in those

same long-lateral wells.

Commencing operations with XSR Unit #116 in the Eagle Ford

It was a landmark year for both our XDR drilling division and XSR coiled tubing division.

XDR/XSRBUSINESS DIVISIONS After growing our XDR drilling eet dramatically in prior years,

we maximized utilization levels on an unprecedented scale in

2013. At year-end, all 21 of these Tier 1 rigs were working

mostly on long-term contracts. Total operating days for the

XDR division reached an all-time high of 6,834.

Geographically, we continued to focus on two of North

America s most proli c shale oil plays. Our largest presence

is in the Niobrara Shale in Colorado and Wyoming, where

12 XDR rigs were working at year-end. There, our high-

speci cation rigs continued to set the performance standard

with superior mobility that accelerates drilling and reduces

move times between well pads. We also further grew our

presence in the Bakken Shale in North Dakota, where we had

six rigs working at year-end. The other three XDR rigs were

working in Canada.

“Our leading-edge technology and outstanding service quality

truly set us apart in the XDR division s core operating areas

of Colorado and North Dakota,” Chief Executive Of cer Tom

Wood noted. “The market remains strong for Xtreme s drilling

services in the Bakken and Niobrara, as our operational

ef ciency and best-in-class mobilization times continue to

drive down costs for our customers.”

Eagle Ford 4 XSR COILED TUBING UNITS

XDR RIGS ACTIVE

100% At Year-End

XDR ALL-TIME HIGH UTILIZATION

6,834 Operating Days

Niobrara Shale 12 XDR DRILLING RIGS

Bakken Shale 6 XDR DRILLING RIGS

Canada 3 XDR DRILLING RIGS

The XDR division s high utilization levels are expected to

continue into the future, as our large backlog of contracted

work grew to approximately 6,000 days last year. We are also

expanding into new international markets which may offer

greater opportunity for our smaller rigs.

For our XSR coiled tubing division, last year was full of

accomplishment. After launching our extended-reach

completion services in 2012, we have rapidly established

ourselves as a market leader in the Eagle Ford Shale in South

Texas. We are also the longest-reach provider in this basin,

which has the largest production of oil and natural gas liquids

among U.S. resource plays. In fact, we set an Eagle Ford

record in 2013 by reaching a total measured depth of

20,344 feet with coiled tubing including a lateral length

over 10,000 feet. These distinctions allowed us to increase

both our service rates and utilization levels, as total operating

days for the XSR division reached a new high of 1,234.

In addition to superior reach, Xtreme has established a

reputation for outstanding performance with our proprietary

large-diameter coil. XSR units are substantially accelerating

plug millouts and reducing stuck-in-hole incidents and

ran 16.8 million feet of coiled tubing in 2013 without ever

leaving pipe downhole. We are especially proud of that last

accomplishment as it highlights the unmatched reliability

of our coiled tubing services. With that stellar track record,

Xtreme is not only completing ultra-deep wells, but also

gaining traction in the 14,000-16,000 foot market as operators

seek to mitigate risk.

Xtreme is achieving these successes by leveraging

innovations we originally developed for coiled tubing drilling.

For example, our XSR units utilize electric injectors and

PLC-based controls for greater power and precision, and

2-5 8” coiled tubing for extended lateral reach. Recognizing

the advantages, the market is increasingly favoring these

technologies over traditional features such as hydraulic

power and smaller-diameter coil. We believe this clearly

differentiates Xtreme in the marketplace and offers our

customers a value proposition no other company can match.

Additionally, two XSR units continue to perform re-entry

drilling in Saudi Arabia, where we signed new three-year

contracts with the operators we have worked with there

since 2010. This project has been a tremendous technical and

nancial success for the company.

XSR EAGLE FORD RECORD

20,344 ftTotal Measured Depth

XSR ALL-TIME HIGH UTILIZATION

1,234Operating Days

After keeping the rig count unchanged and concentrating on our core markets last year, Xtreme’s focus will return to

and geographical footprint.

Our burgeoning XSR division will add new coiled tubing units

as it pursues expansion into West Texas. We anticipate

funding this initiative entirely with free cash, given the

strength of our operating revenues.

“As our reputation for excellence in coiled tubing services

continued to build in 2013, customer demand in the Eagle Ford

began to consistently outstrip our capacity,” Chief Executive

Of cer Tom Wood commented. “Xtreme is moving quickly to

meet that demand and pursue expansion into other

markets by making new-build XSR units the focus of our

2014 capital investment program.”

Also in 2014, the XDR division will explore opportunities to

move smaller drilling rigs into new international markets as

the push toward deeper wells and larger equipment continues

in the U.S. These efforts were already yielding results early in

the year, when we signed a multi-year contract to relocate

two XDR 300 rigs to India.

Finally, even with all that we accomplished last year, we see

opportunities to further optimize our operations and drive

pro t margins. These efforts will continue in 2014, as we seek

to maximize our return on previous capital investments while

building on the unprecedented successes of the past year.

North AmericaIndia

Saudi Arabia

INTERNATIONAL PRESENCE

(Note: India operations expected to commence in Q3 2014)

Coiled tubing re-entry drilling in Saudi Arabia

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Management for Xtreme Drilling and Coil Services Corp. (“Xtreme” or the “Company”), formerly known as Xtreme Coil Drilling Corp., based this Management’s Discussion and Analysis (“MD&A”) on operating and financial results for the three and twelve months ended December 31, 2013, and provides comparative information for the three and twelve months ended December 31, 2012. Management recommends reading this discussion and analysis of Xtreme’s financial condition and results of operations in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2013 and related notes (the “Audited Financial Statement”). Xtreme’s common shares trade on the Toronto Stock Exchange under the symbol “XDC”. The Company prepares its consolidated financial statements and comparative information in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). Unless otherwise stated, all amounts are expressed in Canadian dollars (“CAD”). Management’s discussion and analysis is based on information available as of March 11, 2014. Forward-Looking Information This MD&A, or documents incorporated herein, contains forward-looking information (“FLI”). FLI is typically contained in statements with words such as “anticipate”, “believe”, “estimate”, “expect”, “plan”, “schedule”, “intend”, “propose” or similar words suggesting future outcomes or an outlook. More particularly, this MD&A contains FLI that may relate to contracting, marketing, financing, construction, modifications, deployment, operation, and utilization of drilling and service rigs in the Company’s current and future fleet. Although Xtreme believes expectations reflected in such FLI are reasonable, readers should not place undue reliance on them because Xtreme can give no assurance they will prove to be correct. There are many factors that could cause FLI not to be correct, including risks and uncertainties inherent in the Company's business. FLI is based on certain factors and assumptions including, but not limited to: the assessment of current and projected future drilling, well servicing and related operations; ongoing and future strategic business alliances, negotiations and opportunities to enter new, extend or complete existing contracts; the availability and cost of financing; currency exchange rates; timing and magnitude of capital expenditures; expenses and other variables affecting rig operation, modification and construction; the ability and commitment of vendors to provide rig component equipment, services and supplies, including labor, in a cost-effective and timely manner; the issuance of applied-for patents; changes in tax structures and rates; and, government regulations. Although Xtreme considers the assumptions used to prepare this MD&A reasonable, based on information available to management as of March 11, 2014, ultimately the assumptions may prove to be incorrect. FLI is also subject to certain factors, including risks and uncertainties, which could cause actual results to differ materially from management's current expectations. These factors include, but are not limited to: the cyclical nature of drilling and well servicing market demand, currency exchange rates and commodity prices; access to credit and to equity markets; the availability and retention of qualified personnel; vendor-provided equipment components and services; and, competition for customers. Management’s assumptions considered the following: compliance with the terms of the Company’s current credit facility; ongoing access to key services, supplies and components required to continue operating and maintaining equipment, including fuel; continued successful performance of drilling, well servicing and related equipment; expectations regarding gross margin; recruitment and retention of qualified personnel; continuation or extension of existing long-term, multi-well contracts or other contracts; revenue expectations related to shorter-term drilling and well servicing opportunities; willingness and ability of customers to remit amounts owing to Xtreme in accordance with normal industry practices; and, management of accounts receivable in direct relation to revenue generation.

5

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

In preparing this MD&A, management considered the following risk factors: fluctuations in crude oil and natural gas prices, as well as supply and demand; fluctuation in currency exchange and interest rates; financial stability of Xtreme’s customers; current and future applications for Xtreme's proprietary technology; related services provided by, and competition from, other drilling and well servicing contractors; regulatory and economic conditions in regions where Xtreme operates; environmental constraints; changes to government legislation; international trade barriers or restrictions; and, where appropriate, global economic, political and military events. FLI contained in this MD&A about prospective results of operations, financial position or cash provided by operating activities is based on assumptions about future events, including economic conditions and proposed courses of action, and on management’s assessment of relevant information currently available. Readers are cautioned such financial outlook information contained in this MD&A is not appropriate for purposes other than for which it is disclosed here. Readers should not place undue importance on FLI and should not rely on this information as of any other date. Except as required pursuant to applicable securities laws, Xtreme disclaims any intention, and assumes no obligation, to update publicly or revise FLI to reflect actual results, whether as a result of new information, future events, changes in assumptions, changes in factors affecting such FLI or otherwise. Description of the Business Xtreme designs, builds, and operates a fleet of high-specification drilling rigs and coiled tubing well service units featuring leading-edge proprietary technology including alternating current (“AC”) high capacity coil injectors, deep re-entry drilling capability, modular transportation systems and continuous integration of in-house advances in methodologies. Currently Xtreme operates two service lines: drilling services (“XDR”) and coil services (“XSR”) under contracts with oil and natural gas exploration and production companies and integrated oilfield service providers in Canada, the United States of America (“United States” or “US”) and the Kingdom of Saudi Arabia (“Saudi Arabia”). Xtreme continues to evaluate opportunities for additional projects within, and beyond, these core regions of operation. Drilling Services In the United States, Xtreme contracts to drill primarily in the resource plays of the Williston Basin and the Greater Denver-Julesburg Basin. Xtreme’s XDR 300, 400 and 500 rigs are designed for these deeper geological zones. In Canada, the XDR 200 rigs are working primarily in Canada’s unconventional plays. Xtreme recently entered into a letter agreement for two XDR 300 drilling rigs on a multi-year drilling contract in an international market. This agreement provides a long-term solution for these two 300 series rigs as they are optimal for the contracted market. The operation is expected to begin in the third quarter of 2014. At December 31, 2013, the Company had all 21 drilling rigs working. Coil Services Xtreme offers some of the deepest-reach coiled tubing service units in the world. The Company continues to respond to the rapid growth of drilling activity in North American resource plays, customizing units for operations in deeper shale formations. Xtreme deployed the first of the new extended-reach units in early 2012 to the Eagle Ford Shale in South Texas. In Saudi Arabia, Xtreme has two coiled tubing units deployed on a deep horizontal re-entry drilling project in the Middle East, which are critical to overall reserves recovery. The target re-entry wells are deep and technically challenging, have multi-lateral well profiles and require under-balanced drilling.

6

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

At December 31, 2013, the Company had five of the seven coil services rigs working. Fleet The following table summarizes the Company’s fleet as of March 11, 2014.

Model Drilling Rigs Coil Service Units

XSR 200 4

XSR 200 Plus 3

XDR 200 4

XDR 300 4

XDR 400 2

XDR 500 11

21 7

Utilization rates are a key statistic for the drilling industry since they measure revenue volume and influence pricing. During 2013, Xtreme achieved 8,063 operating days, which corresponded to an average utilization rate of 85 percent. The drilling and coil services units had utilization of 89 percent and 69 percent, respectively. It should be noted that Xtreme calculates utilization rates based upon drilling rigs and coil service units available for service. Standby revenue is taken into account in Xtreme’s utilization statistic.

During the fourth quarter of 2013, the Company adjusted the methodology for calculating utilization in the US coil services division. Available operating days is now defined as 22 days per month for each unit as opposed to total calendar days as calculated in the past. This was based on the fact that on average the coil service units in the US spends 5 to 6 days mobilizing between wells and 2 to 3 days on preventive maintenance during the month. Utilization for prior periods presented has been restated to conform to the current presentation.

From time to time, the Company enters into drilling contracts for extended terms. At December 31, 2013, Xtreme had 13 XDR rigs with multi-year contracts that extend into 2014 or beyond. Of these contracts, six are anticipated to expire in 2014 and seven in 2015.

Patents At March 11, 2014, Xtreme held 36 patents related to technologies for drilling with coiled tubing and conventional drill pipe as well as for certain rig and equipment transportation methods. These patents have been issued in the United States, Canada, Eurasia, Mexico, Indonesia, Australia, and Russia. Xtreme has more than 34 patent-related applications in progress in the United States, Canada and other worldwide jurisdictions.

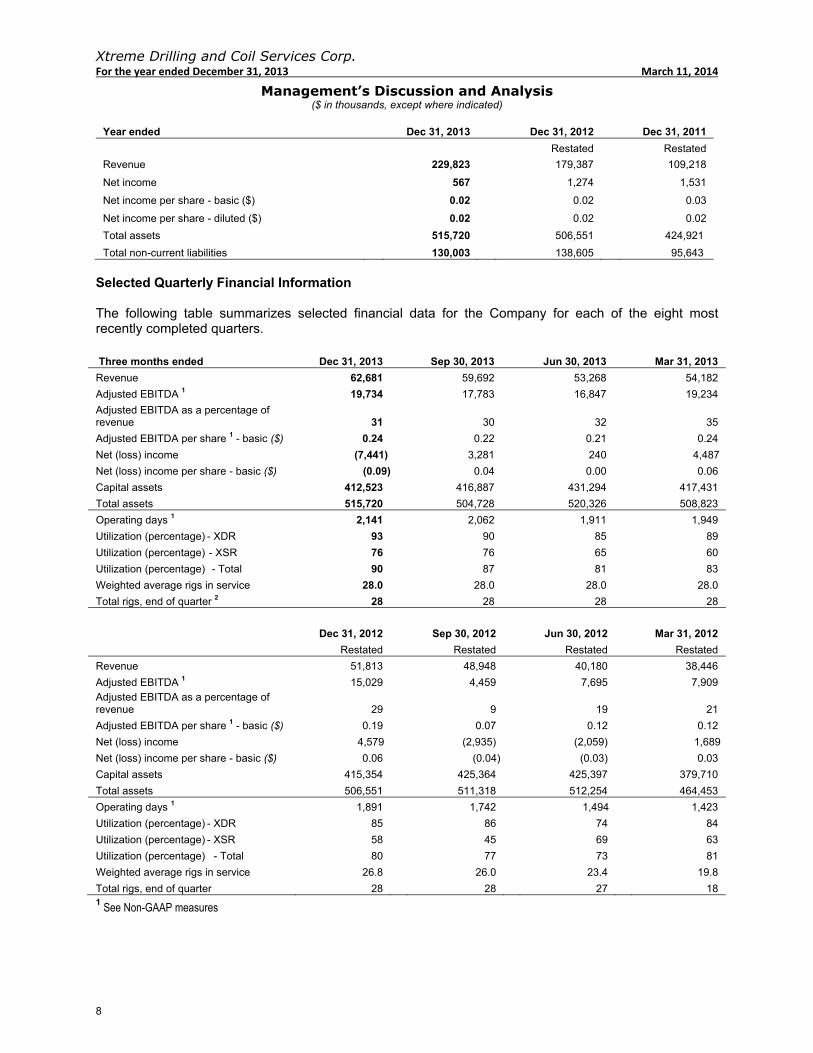

Selected Annual Information The following table summarizes selected financial data for the Company for each of the three most recently completed financial years. The information set forth below should be read in conjunction with the consolidated Annual Financial Statements.

7

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Year ended Dec 31, 2013 Dec 31, 2012 Dec 31, 2011

Restated Restated

Revenue 229,823 179,387 109,218

Net income 567 1,274 1,531

Net income per share - basic ($) 0.02 0.02 0.03

Net income per share - diluted ($) 0.02 0.02 0.02

Total assets 515,720 506,551 424,921

Total non-current liabilities 130,003 138,605 95,643

Selected Quarterly Financial Information The following table summarizes selected financial data for the Company for each of the eight most recently completed quarters. Three months ended Dec 31, 2013 Sep 30, 2013 Jun 30, 2013 Mar 31, 2013

Revenue 62,681 59,692 53,268 54,182

Adjusted EBITDA 1 19,734 17,783 16,847 19,234

Adjusted EBITDA as a percentage of revenue 31 30 32 35

Adjusted EBITDA per share 1 - basic ($) 0.24 0.22 0.21 0.24

Net (loss) income (7,441) 3,281 240 4,487

Net (loss) income per share - basic ($) (0.09) 0.04 0.00 0.06

Capital assets 412,523 416,887 431,294 417,431

Total assets 515,720 504,728 520,326 508,823

Operating days 1 2,141 2,062 1,911 1,949

Utilization (percentage) - XDR 93 90 85 89

Utilization (percentage) - XSR 76 76 65 60

Utilization (percentage) - Total 90 87 81 83

Weighted average rigs in service 28.0 28.0 28.0 28.0

Total rigs, end of quarter 2 28 28 28 28

Dec 31, 2012 Sep 30, 2012 Jun 30, 2012 Mar 31, 2012

Restated Restated Restated Restated

Revenue 51,813 48,948 40,180 38,446

Adjusted EBITDA 1 15,029 4,459 7,695 7,909 Adjusted EBITDA as a percentage of revenue 29 9 19 21

Adjusted EBITDA per share 1 - basic ($) 0.19 0.07 0.12 0.12

Net (loss) income 4,579 (2,935) (2,059) 1,689

Net (loss) income per share - basic ($) 0.06 (0.04) (0.03) 0.03

Capital assets 415,354 425,364 425,397 379,710

Total assets 506,551 511,318 512,254 464,453

Operating days 1 1,891 1,742 1,494 1,423

Utilization (percentage) - XDR 85 86 74 84

Utilization (percentage) - XSR 58 45 69 63

Utilization (percentage) - Total 80 77 73 81

Weighted average rigs in service 26.8 26.0 23.4 19.8

Total rigs, end of quarter 28 28 27 18 1 See Non-GAAP measures

8

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Quarter by Quarter Analysis

2012 Analysis

In the first quarter of 2012, the core drilling services segment continued to perform well. The US drilling segment delivered two new-build XDR 500 rigs and three rigs previously idle in the US began working in Canada. In the US, the coil services segment rolled out at a slower than desired pace due to pump delays and personnel shortages. The Saudi Arabia coil services segment continued strong performance of the two units.

In the second quarter the Company continued to focus on the deployment of the new build XDR drilling rigs as well as building the XSR coil service segment. In the US, operating days increased over the first quarter, a result of the deployment of the new-build XDR drilling rigs. Canada drilling services segment had a slow post break up start based on very wet weather in Alberta. The US XSR business was still challenging due to the softness in the market coupled with a slower roll out than anticipated. While the operating days doubled in the second quarter, the Company was not profitable in this segment based on higher than anticipated coil expenses in the period. The Saudi Arabian coil services segment continued to be the Company strongest operating segment.

In the third quarter, Xtreme recognized significant revenue growth with all but one of the new-build XDR 500 rigs completed and in operation. Revenue and Adjusted EBITDA was from the previous period. Both of these represent the highest quarterly results the Company had achieved to date. Canada drilling services segment continued to be slow as a result of a decrease in horizontal well permits. The US coil services segment was scaled back to one operating unit in the third quarter, which negatively impacted financial results. In Saudi Arabia, the coil services segment operating days decreased slightly, but operations continued to excess expectations.

In the fourth quarter of 2012, the Company mobilized the final XDR 500 drilling rig in the United States. The Company had 19 or 21 drilling rigs working in the United States and three drilling rigs working in Canada. The US coil services segment had two of five units working and the Saudi Arabia coil services segment continued strong performance on the two units working.

2013 Analysis

In the first quarter of 2013, Xtreme’s drilling services segment continued to be the largest revenue segment in the Company, mostly attributable to the US drilling operations. The Canadian operations were slowed as a result of fewer horizontal well permits issued. The US coil services segment began to hit a stride on the latter half of the first quarter and the Saudi Arabian coil services segment continued strong performance as a result of strong utilization.

In the second quarter of 2013, the Company continued to focus on improving financial and operating performance. Utilization in the US XDR drilling segment remained strong with only one idle rig. In Canada the three XDR rigs that operated in the second quarter had a significantly higher utilization than industry average; however margins remain under pressure based on lower day rates. The US XSR business had a significant increase in utilization and operating margin during the second quarter. The Saudi XSR business maintained strong utilization and margins during the second quarter.

In the third quarter, the US drilling services segment was negatively impacted by substantial rain and flooding in Colorado. The Company had nine XDR rigs operating in Colorado for September. During the quarter, repair and maintenance expenses were up per operating day due to the associated equipment failures, additional maintenance on a previously stacked rig and modifications to a XDR 300 rig that

9

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

switched customers. These expenses along with increased inventory consumption decreased operating margin in the US as compared to the second quarter. The Canadian drilling services segment had higher utilization due to increased operating days. The coil services segment had another strong quarter based on improvement of performance and pricing. In the US coil services segment’s operating margin increased due to additional operating days.

At the end of the fourth quarter of 2013, the US drilling services segment had all rigs working, resulting in the Company highest revenue and operating days to date. Operating days and utilization was down slightly in Canada. The US coil services segment utilization increased slightly over the third quarter. Additionally, two XSR units continued to have strong performance in Saudi Arabia.

Year over Year Analysis

An assessment or comparison of Xtreme’s quarterly results, at any given time, requires consideration of seasonality. From a seasonality perspective, Xtreme operates rigs in Canada; therefore, operations are impacted by weather and seasonal factors. The winter season, which incorporates the first quarter, is generally a busy period in Canada as oil and gas companies take advantage of frozen conditions to move drilling rigs into regions which might otherwise be inaccessible to heavy equipment due to swampy conditions. The second quarter normally encompasses a slow period referred to as spring break-up. During this period, melting conditions result in temporary municipal road bans that effectively prohibit the movement of drilling rigs. The third and fourth quarters in Canada are usually representative of average activity levels. See also “Seasonality of Operations” below for a discussion of how the Company’s operations in areas of the United States and in Saudi Arabia are impacted by weather and seasonal factors. Operating days increased four percent sequentially to 2,141 and 23 percent year-over-year. Revenue increased five percent sequentially to $62,681 and 21 percent year-over-year. The Company recorded a net loss for the fourth quarter of $7,441 compared to a net income of $3,281 for the sequential period. The decrease in income from the third quarter is primarily driven by the impact of accelerated depreciation, a result of changes in estimated useful lives of certain assets, the write-off of certain property and equipment, the write-off of unamortized deferred loan fees, a result of extinguishment of the previous credit facility, and the unfavorable impact of the foreign exchange loss of $3,025, a result of translating the Company’s USD denominated debt to CAD as of the end of the fourth quarter. The month end exchange rate used to translate the USD-denominated assets and liabilities to CAD was 1.0636 at December 31, 2013 (1.1105 at March 11, 2014).

Adjusted EBITDA for the fourth quarter of $19,734 increased 11 percent sequentially and 31 percent year-over-year. Adjusted EBITDA was $0.24 per share, a $0.02 per share increase sequentially and a $0.05 per share increase from the prior year period. Capital assets of $412,523 decreased one percent year-over-year. Capital and total assets decreased due primarily to the sale of an XSR rig package during the first quarter of 2013, lower capital expenditures, and an increase in depreciation expense due to a change in methodology and change in useful lives. During the fourth quarter of 2013, the Company had capital additions of approximately $3,900, compared to approximately $6,600 in the third quarter and approximately $9,200 in the prior year quarter.

10

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Results of Operations - Year ended December 31, 2013 compared to December 31, 2012 Revenue, Operating Expenses and Gross Margin

2013 2012 Change % Change

Restated

Revenue 229,823 179,387 50,436 28

Operating expenses 144,873 127,835 17,038 13

Gross margin 84,950 51,552 33,398 65

Operating days 8,063 6,550 1,513 23

Revenue per operating day 28.5 27.4 1.1 4

Operating expenses per operating day 18.0 19.5 (1.5) (8)

Gross margin per operating day 10.5 7.9 2.6 33

Rig utilization (percentage) – XDR 89 83 6 7

Rig utilization (percentage) – XSR 69 58 11 19

Rig utilization (percentage) - Total 85 78 7 9

Revenue increased to $229,823 for the year ended December 31, 2013, from $179,387 for the year ended December 31, 2012. Stronger market conditions and the improvement in performance of coil servicing operations in the United States resulted in the Company achieving 8,063 operating days in 2013 compared to 6,550 in 2012. The stronger market and service offerings for the coil services in the United States had a positive impact on day rates, as the average revenue per operating day increased from $27.4 to $28.5. Revenue improvements were broadly based, as drilling revenue increased as a result of increased demand for the Company’s rigs, more operating days and better utilization in both drilling and coil services in 2013. Drilling services revenue for the year ended December 31, 2013, was $173,147 compared to $141,440 for the year ended December 31, 2012. Coil services revenue for the year ended December 31, 2013, was $56,676 compared to $37,947 for the year ended December 31, 2012. Rig utilization for drilling services was 89 percent for the year ended December 31, 2013, compared to 83 percent for the year ended December 31, 2012. Rig utilization for coil services was 69 percent for the year ended December 31, 2013, compared to 58 percent for the year ended December 31, 2012. Operating expenses increased to $144,873 for the year ended December 31, 2013, from $127,835 for the year ended December 31, 2012. This increase in total operating expenses was the result of increased activity, offset by a decrease in field-level expenses, a result of cost control measure implemented in late 2012. Operating expenses are tied to activity levels and were $18.0 per operating day, for the year ended December 31, 2013, compared to $19.5 per operating day, for the year ended December 31, 2012. Operating expenses for drilling services were $108,752 in 2013 compared to $95,922 in 2012. Operating expenses for coil services for 2013 were $36,121 compared to $31,913 for 2012. Gross margin was $84,950 for the year ended December 31, 2013, up from $51,552 for the year ended December 31, 2012. The improvement in gross margin was a combined result of higher rig utilization, higher day rates, and a decrease in operating costs at the field level, a result of cost control measures implemented in late 2012. The gross margin per operating day increased from $7.9 for the year ended December 31, 2012, to $10.5 for the year ended December 31, 2013.

11

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

General and Administrative (“G&A”) Expenses

2013 2012 % Change

G&A expenses 11,280 10,226 10

G&A expenses were $11,280 in 2013 compared to $10,226 in 2012. The Company recovered legal costs of approximately $510 and $1,600 in 2013 and 2012, respectively, a result of the settlement of litigation. Exclusive of the recovery of these legal costs, G&A would be $11,790 and $11,826 for the years ended December 31, 2013 and 2012, respectively. The decrease from 2012 is primarily due to a decrease in legal fees. G&A expenses represented five percent of total revenue in 2013 compared to six percent in 2012.

Impairment of Accounts Receivable

2013 2012 % Change

Impairment of accounts receivable 72 6,235 (99)

Impairment of accounts receivable was $72 for 2013, a decrease from $6,235 in 2012. In September 2013, the Company recovered approximately $2,690 relating to previously billed amounts plus legal fees of approximately $510. The carrying amount of trade accounts receivable was approximately $2,760, resulting in an additional write-off of approximately $70 for uncollected amounts. In 2012, the Company won a judgement against a former customer for certain billed amounts, but recognized an impairment loss of $1,500 related to the write-off of uncollected amounts. In 2012, the Company also entered into a confidential legal settlement with another former customer and recovered certain previously billed amounts, but recognized an impairment loss of $4,735. Change in Fair Value of Non-controlling Interest Liability

2013 2012 % Change

Change in fair value of non-controlling interest liability 1,481 (829) n/a

Change in fair value of non-controlling interest liability was $1,481 in 2013 compared to ($829) in 2012. The change in fair value of non-controlling interest liability relates to the increase in the fair value of the put option held by the minority interest partner.

Depreciation and Amortization 2013 2012 % Change

Depreciation and amortization 51,495 27,569 87

As of January 1, 2013, the Company changed its estimate of depreciable lives of rig components and related equipment from units-of-production to straight-line, resulting in an increase of depreciation expense of approximately $4,600. Exclusive of the increase due to the change in estimate, the increase in depreciation and amortization from $27,569 to $51,495 is mostly attributable to approximately $9,500 in depreciation of capital spares not previously depreciated under units-of-production and the write-off of certain equipment as a result of a physical asset verification for approximately $3,900. Effective October 1, 2013, the Company accelerated depreciation on capital spares and certain other rig equipment for approximately $3,500 for capital spares which are not expected to be fully recoverable.

12

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Stock-Based Compensation

2013 2012 % Change

Stock-based compensation 1,321 1,245 6

Stock-based compensation was $1,321 for 2013, an increase from $1,245 in 2012. The increase is due primarily to the impact of restricted stock units issued during the year, offset by fewer awards of options to purchase future shares were granted. Foreign Exchange

2013 2012 % Change

Foreign exchange loss (gain) 6,494 (1,790) n/a

Foreign exchange gains and losses result directly from the fluctuation in values of the USD relative to the CAD on the assets and liabilities denominated in USD. Operations in the United States and Saudi Arabia are denominated primarily in USD. For 2013 the Company recorded a foreign exchange loss of $6,494 compared to a foreign exchange gain of $1,790 for 2012. The foreign exchange loss was due primarily to the realized loss on translation of the USD-denominated debt as a result of the higher value of the USD relative to the CAD. Interest Expense

2013 2012 % Change

Interest expense 7,866 7,919 1

Interest expense for 2013, was $7,866 compared to $7,919 for 2012. Included in interest expense in 2013 is $1,199 of deferred loan fees written-off due to repayment of borrowings under the prior financing arrangements. Exclusive of the deferred loan fees interest expense for 2013 would have been $6,677. The decrease from 2012 is a result of lower interest rates during the period. Exclusive of the write-off, the effective interest rate for 2013 was 5.1 percent, compared to 7.4 percent for 2012.

Income (loss) Before Tax

2013 2012 % Change

Income (loss) before tax 4,920 (3,126) n/a

Income before tax for 2013 was $4,920, an increase from loss before tax of $3,126 recorded in 2012. The increase is due primarily to the increase in revenue and gross margin, offset by the increase in depreciation expense, the unfavorable impact of the foreign exchange loss reflected in the year ended December 31, 2013, and the write-off of deferred loan fees.

Income Tax 2013 2012 % Change

Income tax expense (benefit) 4,353 (4,400) n/a

Income tax expense for 2013, was $4,353 compared to income tax benefit of $4,400 recorded in the prior year period. The increase from the prior year is due to increase in pre-tax income.

Net Income 2013 2012 % Change

Net income 567 1,274 (55)

Net income for 2013 was $567, a decrease from net income $1,274 recorded in 2012. The decrease in the respective periods is due primarily to the increase in depreciation expense, the unfavorable impact of

13

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

the foreign exchange loss, the write-off of deferred loan fees, and the increase in income tax expense, offset by the increase in revenue and gross margins. Results of Operations – Three months ended December 31, 2013 compared to December 31, 2012 Revenue, Operating Expenses and Gross Margin

Three months ended

Dec 31, 2013 Dec 31, 2012 Change % Change

Restated

Revenue 62,681 51,813 10,868 21

Operating expenses 39,631 34,467 5,164 15

Gross margin 23,050 17,346 5,704 33

Operating days 2,141 1,891 250 13

Revenue per operating day 29.3 27.4 1.9 7

Operating expenses per operating day 18.5 18.2 0.3 2

Gross margin per operating day 10.8 9.2 1.6 17

Rig utilization (percentage) – XDR 93 85 8 9

Rig utilization (percentage) – XSR 76 58 18 31

Rig utilization (percentage) - Total 90 80 10 13

Revenue increased to $62,681 for the three months ended December 31, 2013, from $51,813 for the three months ended December 31, 2012. The expansion of the drilling rig fleet, coupled with stronger market conditions, and the the improvement in performance of coil servicing operations in the United States resulted in the Company achieving 2,141 operating days compared to 1,891 in 2012. The stronger market and service offerings for the coil services in the United States had a positive impact on day rates, as the average revenue per operating day increased from $27.4 to $29.3. Revenue improvements were broadly based, as drilling revenue increased as a result of increased demand for the Company’s rigs, more operating days and better utilization in both drilling and coil services in 2013. Drilling services revenue for the three months ended December 31, 2013 was $45,286 compared to $40,701 for the three months ended December 31, 2012. Coil services revenue for the three months ended December 31, 2013, was $17,395 compared to $11,112 for the three months ended December 31, 2012. Rig utilization for drilling services was 93 percent for the three months ended December 31, 2013, compared to 85 percent for the three months ended December 31, 2012. Rig utilization for coil services was 76 percent for the three months ended December 31, 2013, compared to 58 percent for the three months ended December 31, 2012. Operating expenses increased to $39,631 for the three months ended December 31, 2013, from $34,467 for the three months ended December 31, 2012. Operating expenses are tied to activity levels and were $18.5 per operating day, for the three months ended December 31, 2013 and 2012. The increase in total operating expenses was the result of increased activity coupled with an increase in repair and maintenance costs. Operating expenses for drilling services were $29,660 for the three months ended December 31, 2013, compared to $26,583 for the three months ended December 31, 2012. Operating expenses for coil services for 2013 were $9,970 for the three months ended December 31, 2013 compared to $7,884 for the three months ended December 31, 2012. Gross margin was $23,807 for the three months ended December 31, 2013, up from $17,346 for the three months ended December 31, 2012. The improvement in gross margin was a combined result of higher rig utilization, higher day rates, and a decrease in operating costs at the field level, a result of cost

14

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

control measures implemented in late 2012. The gross margin per operating day increased from $9.2 for the three months ended December 31, 2012, to $11.1 for the three months ended December 31, 2013. General and Administrative (“G&A”) Expenses

Dec 31, 2013 Dec 31, 2012 % Change

G&A expenses 3,316 2,316 43

G&A expenses increased to $3, 316 in the fourth quarter of 2013 from $2,316 in the fourth quarter of 2012, due primarily to an increase in professional fees. G&A expenses represented five percent of total revenue in the fourth quarter of 2013 and 2012, respectively.

Change in Fair Value of Non-controlling Interest Liability

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Change in fair value of non-controlling interest liability 2,375 1,022 n/a

Change in fair value of non-controlling interest liability was $2,375 in the fourth quarter of 2013 compared to $1,022 in the fourth quarter of 2012. The change in fair value of non-controlling interest liability relates to the increase in the fair value of the put option held by the minority interest partner.

Depreciation and Amortization

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Depreciation and amortization 20,886 10,127 n/a

As of January 1, 2013, the Company changed its estimate of depreciable lives of rig components and related equipment from units-of-production to straight-line, resulting in an increase of depreciation expense of approximately $1,100. Exclusive of the increase due to the change in estimate, the increase in depreciation and amortization from $10,127 to $20,886 is mostly attributable to approximately $9,500 in depreciation of capital spares not previously depreciated under units-of-production and the write-off of certain equipment as a result of a physical asset verification of approximately $3,900. Effective October 1, 2013, the Company accelerated depreciation on capital spares for approximately $3,500 for capital spares which are not expected to be fully recoverable.

Stock-Based Compensation

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Stock-based compensation 355 73 n/a

Stock-based compensation was $355 for the fourth quarter of 2013, an increase from $73 in the fourth quarter of 2012. The increase is due primarily to the awards of restricted stock units during the period.

15

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Foreign Exchange

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Foreign exchange loss 3,025 937 n/a

Foreign exchange gains and losses result directly from the fluctuation in values of the USD relative to the CAD on the assets and liabilities denominated in USD. Operations in the United States and Saudi Arabia are denominated primarily in USD. For the fourth quarter of 2013 the Company recorded a foreign exchange loss of $3,025 compared to a foreign exchange loss of $937 for the fourth quarter of 2012. The foreign exchange loss was due primarily to the realized loss on translation of the USD-denominated debt as a result of the higher value of the USD relative to the CAD. Interest Expense

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Interest expense 2,588 2,408 7

Interest expense for the fourth quarter of 2013, was $2,588 compared to $2,408 for the fourth quarter of 2012. Included in interest expense in 2013 is $1,199 of deferred loan fees written-off due to repayment of borrowings under the prior financing arrangements. Exclusive of the deferred loan fees interest expense for 2013 would have been $1,389. The decrease from 2012 is a result of lower interest rates during the period. Exclusive of the write-off, the effective interest rate for 2013 was 4.5 percent, compared to 7.1 percent for 2012.

Impairment on Assets Held for Sale

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Impairment on assets held for sale – 3,133 n/a

Impairment on assets held for sale for the fourth quarter of 2012 of $3,133 was a result of a difference between the sales price of certain assets sold to an independent third party, less selling costs, and the net book value of the assets of $12,441.

Loss Before Tax

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Loss before tax 9,431 2,829 n/a

Loss before tax for the fourth quarter of 2013, was $9,431 reflecting an increase from loss before tax of $2,829 recorded in the fourth quarter of 2012. The increase is the increase in depreciation expense, the unfavorable impact of the foreign exchange loss, and the write-off of deferred loan fees, offset by an increase in revenue and gross margin, for three months ended December 31, 2013. Income Tax

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Income tax benefit 1,990 6,656 n/a

16

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Income tax benefit for the fourth quarter of 2013, was $1,990 compared to an income tax benefit of $6,656 recorded in the fourth quarter of 2012. Net (Loss) Income

Three months ended

Dec 31, 2013 Dec 31, 2012 % Change

Net (loss) income (7,441) 4,579 n/a

Net loss for the fourth quarter of 2013 was $7,441 reflecting a decrease from net income of $4,579 recorded in the fourth quarter of 2012. The change for the respective periods is due primarily to the increase in depreciation expense, the unfavorable impact of the foreign exchange loss, and the write-off of deferred loan fees, offset by the increase in revenue and gross margins. Financial Condition, Liquidity and Capital Resources ($ millions) Dec 31, 2013 Dec 31, 2012 % Change

Total debt (including amounts outstanding under the operating line) 129.1 147.8 (13)

Less: cash and cash equivalents 12.2 5.9 107

Net debt 1 116.9 141.9 (18) 1 See Non-GAAP measures

Net debt as of December 31, 2013, was $116.9 million, reflecting a decrease of $25.0 million from net debt of $141.9 million as of December 31, 2012, primarily due to a decrease in total debt of approximately $18.7 million and an increase in cash of approximately $6.3 million. For 2013, the Company generated approximately $61.9 million in cash from operations, utilized primarily to pay long-term debt ($30.6 million), pay down amounts outstanding under the operating line of credit ($7.8 million), and for capital expenditures made during the period ($23.1 million) Bank Indebtedness On December 27, 2013, the Company reached an agreement with a syndicate of financial institutions led by Wells Fargo to enter into a new senior credit facility for $150,000 (“the Credit Agreement”). The Credit Agreement consists of a revolving credit facility of $140,000, denominated in USD, and a $10,000 revolving credit facility, available in CAD and/or USD. The Credit Agreement has a term of three years with the ability to increase the facility to $175,000. The Credit Agreement is secured by property and equipment and inventory held in Canada and the United States, as well as cash and trade receivables in Canada and the United States of approximately $5,333 and $52,824, respectively, at December 31, 2013. At December 31, 2013, the Company had borrowed $120,000 USD and $2,000 CAD under the Credit Agreement and does not have any of the amounts due under the Credit Agreement as current. As of December 31, 2013, the Company was in compliance with the debt covenants under the Credit Agreement as follows:

• Leverage Ratio - 1.77 to 1.00 (not above 3.00 to 1.00 required)

• Interest Coverage Ratio – 6.43 to 1.00 (not below 3.00 to 1.00 required)

During the three and twelve months ended December 31, 2013, the Company recognized interest expense of $1,389 and $6,667, respectively, on its outstanding borrowings during the respective periods. The effective annual interest on borrowings was approximately 4.5 percent and 5.1 percent for the three and twelve months ended December 31, 2013, respectively (approximately 7.4 percent for the year ended December 31, 2012).

17

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Prior to the execution of the Credit Agreement, the Company’s borrowings consisted of a $150,000 credit facility with a syndicate of institutions, consisting of $15,000 as a revolving operating loan facility denominated in Canadian dollars and $135,000 as an extendible loan facility denominated in USD. In December 2013, the Company repaid these borrowings and related interest with proceeds from The Credit Agreement. Unamortized debt issuance costs related to these borrowings of $1,199 were expensed and included in interest expense for the year ended December 31, 2013.

As of December 31, 2013, the Company had no borrowings under the operating loan facility ($7,834 at December 31, 2012 under the previous facility).

Other Financing

On November 20, 2009, Xtreme entered into an agreement with a major diversified oilfield services company (“the Diversified Services Company”), in which the Diversified Services Company agreed to fund up to USD$5,700 in customization costs for an XSR 200 drilling rig and to pay for certain significant mobilization and start-up costs to deploy the rig to Saudi Arabia upon project award. Under the terms of the agreement, the repayment of the loan is USD$2 per day for each day the rig is earning day-rate revenue.

The loan for customization costs was assumed in connection with the sale of the first rig to the subsidiary Xtreme Equipment Group S.A. As a result of fully consolidating the related accounts for certain subsidiaries, as of December 31, 2013, the Company had $669 outstanding as advanced from the Diversified Services Company (December 31, 2012 - $4,201), which is included in the current portion of long-term debt (December 31, 2012 - $4,201). The loan was paid off January 2014.

Liquidity Risks

See “Business Risks and Uncertainties” below for a discussion of the Company’s liquidity risks.

Capital Expenditures and Commitments Three months ended Twelve months ended

($ millions) Dec 31, 2013 Dec 31, 2012 % Change Dec 31, 2013 Dec 31, 2012 % Change

Capital expenditures 3.9 9.5 (59 ) 23.1 112.4 (79)

Capital expenditures for the three and twelve months ended December 31, 2013, were $3.9 million and $23.1 million, respectively, a decrease from capital expenditures of $9.5 million and $112.4 million during the three and twelve months ended December 31, 2012, respectively. In December 2012, the Company concluded its capital expansion program. Capital expenditures in 2013 were primarily related to maintenance capital expenditures, facilities and purchase of spare equipment.

($ millions) Dec 31, 2013 Dec 31, 2012 % Change

Commitments 2.7 3.2 (16)

Commitments as of December 31, 2013, were $2.7 million, a decrease from commitments of $3.2 million as of December 31, 2012. In December 2012, the last drilling rig that was part of the capital expansion program was completed. All commitments are expected to be paid within the next twelve months.

18

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Contractual Obligations The table below illustrates various contractual obligations which the Company expects to repay, including any interest payments required.

Less than 1 1 – 3 4 –5 After 5

Contractual obligations Total Year Years Years Years

Accounts payable and accrued liabilities 28,051 28,051 – – _

Long-term debt 130,358 669 129,689 – _

Commitments 2,710 2,710 – – _

Operating leases 3,158 979 1,283 896 _

Total contractual obligations 164,277 32,409 130,972 896 _

Segmented Information The Company determines its operating segments based on internal information regularly reviewed by management to allocate resources and assess performance. The Company operates in three geographic areas within two operating segments, which are Drilling Services and Coil Services. Such services are provided in Canada, the United States and internationally. Beginning in the first quarter of 2012, the Company revised the presentation format of its segment disclosure to better align with the Company’s service offerings and management structure. As a result of this change in presentation, the Company reports revenue and expenses and assets based on the Drilling Services, Coil Services, and Corporate and Other segments. This change reflects the Company’s evolution into new market offerings and management’s focus on allocating resources and measuring performance. This change in segment reporting had no impact on the Company’s consolidated statement of financial position, statement of income or cash flows for any periods.

• Drilling represents assets, revenues and expenses associated with the fleet of high specification drilling rigs contracted with oil and natural gas exploration and production companies and integrated oilfield service providers. These drilling rigs are designed for deeper geological zones.

• Coil Services represents the assets, revenues and expenses associated with Xtreme’s coiled

tubing well service units, targeting primarily post fracture treatment cleanouts, re-entry, and horizontal drilling. The change in the fair value of non-controlling interest liability is allocated to coil services.

• Corporate and Other represents the general and administrative costs of the Company,

depreciation and amortization expense, interest expense, realized and unrealized foreign exchange gains and losses and employee incentive compensation charges. The Company views its corporate segment as a support function that provides assistance to more than one segment.

The tables below segment the Company’s revenue, operating earnings (loss) and assets by service line and geographic area.

19

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Drilling

Services Coil Services Corporate and

Other Total

For the year ended December 31, 2013

Revenue 173,147 56,676 – 229,823

Income (loss) before tax 64,395 20,555 (80,030) 4,920

Total assets 367,686 104,350 43,684 515,720

Total liabilities 12,457 24,997 134,032 171,486

Intangible assets – – 3,917 3,917

Capital additions 17,281 5,456 322 23,059

Drilling

Services Coil Services Corporate and

Other Total

For the year ended December 31, 2012

Revenue 141,440 37,947 – 179,387

Income (loss) before tax 45,518 6,033 (54,677) (3,126)

Total assets 343,874 125,297 37,380 506,551

Total liabilities 11,082 21,504 155,958 188,544

Intangible assets – – 4,220 4,220

Capital additions 89,093 23,234 30 112,357

Canada United States Other

International Total

For the year ended December 31, 2013

Revenue 14,860 185,064 29,899 229,823

Total assets 64,138 403,812 47,770 515,720

Canada United States Other

International Total

For the year ended December 31, 2012

Revenue 12,527 140,675 26,185 179,387

Total assets 58,765 394,280 53,506 506,551 Outstanding Shares Data

Dec 31, 2013 Dec 31, 2012

Balance, beginning of period 80,790,315 65,666,266

Shares issued during the period – 15,001,750

Employee options exercised 371,665 122,299

Restricted stock units exercised 103,752 –

Balance, end of period 81,265,732 80,790,315

At December 31, 2013, the Company had outstanding options to purchase 3,161,335 common shares (December 31, 2012 – 3,464,000) at a weighted average exercise price of $2.98 per share (December 31, 2012 – $3.13). The Company’s shareholders approved an Incentive and Retention Plan on April 18, 2012 designed to provide the Company’s directors, officers and key employees and consultants with an opportunity to

20

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

receive cash and/or equity-based incentives associated with common shares of the Company and to benefit from the appreciation of the common shares. Under the incentive plan, restricted stock units granted to eligible individuals vest annually. Vested restricted stock units may be settled in cash or equity, at the discretion of the Company, at a value determined by the fair market value of the common shares at the vesting date. The fair value of the services received in exchange for the grant of the options is recognized as an expense. The total amount to be expensed is determined by reference to the fair value of the shares granted including any market performance conditions, excluding the impact of any service and non-market performance vesting conditions, and including the impact of any non-vesting conditions. Non-market performance and service conditions are included in assumptions about the number of shares that are expected to vest. The total expense is recognized over the vesting period, which is the period over which all of the specified vesting conditions are to be satisfied. The following table summarizes the restricted stock unit awards outstanding at December 31, 2013 and 2012:

Dec 31, 2013 Dec 31, 2012

Restricted stock units granted 1,015,992 311,244

As of March 11, 2014, the Company’s share capital was $328,416 and 81,567,398 common shares were issued and outstanding. Also as of March 11, 2014, the Company had 1,514,288 issued and outstanding restricted stock units and outstanding options entitling the holders to purchase 2,991,003 common shares. Disclosure Controls and Procedures and Internal Controls over Financial Reporting

Disclosure controls and procedures (“DC&P”) means controls and other procedures of an issuer that are designed to provide reasonable assurance that information required to be disclosed by the issuer in its annual filings, interim filings or other reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time periods specified in the securities legislation and include controls and procedures designed to ensure that information required to be disclosed by an issuer in its annual filings, interim filings or other reports filed or submitted under securities legislation is accumulated and communicated to the issuer’s management, including its certifying officers, as appropriate to allow timely decisions regarding required disclosure; Internal controls over financial reporting (“ICFR”) means a process designed by, or under the supervision of, an issuer’s certifying officers, and effected by the issuer’s board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with the issuer’s GAAP and includes those policies and procedures that:

(a) pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the issuer;

(b) are designed to provide reasonable assurance that transactions are recorded as necessary to

permit preparation of financial statements in accordance with the issuer’s GAAP, and that receipts and expenditures of the issuer are being made only in accordance with authorizations of management and directors of the issuer; and

(c) are designed to provide reasonable assurance regarding prevention or timely detection of

unauthorized acquisition, use or disposition of the issuer’s assets that could have a material effect on the annual financial statements or interim financial statements.

The Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”) have designated or caused to be designated under their supervision, DC&P to provide reasonable assurance that (i) material information

21

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

relating to the Company, including its consolidated subsidiaries, is made known to the CEO and CFO by others within those entities, particularly during the period in which the interim filings of the Company are prepared; and (ii) information required to be disclosed by the Company in its annual filings, interim filings or other reports filed or submitted by it under securities legislation is recorded, processed, summarized and reported within the time period specified in securities legislation. The CEO and CFO do not expect that DC&P will prevent or detect all errors, misstatements and fraud but are designed to provide reasonable assurance of achieving their objectives. A control system, no matter how well designed or operated, can only provide reasonable, not absolute, assurance that the objectives of the control system are met. In addition to the DC&P, the CEO and CFO have designed ICFR or caused them to be designed under their supervision to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with International Financial Reporting Standards. The Company’s ICFR may not prevent or detect all errors, misstatements and fraud. The design of internal controls must take into account cost-benefit constraints. A control system, no matter how well designed or operated, can only provide reasonable, not absolute, assurance that objectives of the control system are met. While the Company is continually enhancing its ICFR, no material changes were made during the year ended December 31, 2013, that would materially affect, or are reasonably likely to materially affect, the Company’s ICFR. Management concluded that the Company’s DC&P and ICFR were effective as of December 31, 2013. Non-GAAP Measures Certain supplementary measures in this MD&A do not have any standardized meaning as prescribed under IFRS and, therefore, are considered non-GAAP measures. These measures have been described and presented to provide shareholders and potential investors with additional information regarding the Company’s financial results, liquidity and ability to generate funds to finance its operations. These measures may not be comparable to similar measures presented by other entities, and are further explained as follows. For the three and twelve months ended December 31, 2012, operating days, rig utilization (percentage), weighted average rigs in service and completed rigs, includes 100 percent of the statistical rig data for the two rigs operating in Saudi Arabia which, for financial reporting purposes, is proportionally consolidated. Operating Days Operating days represent the total of all drilling, moving, standby and other revenue days for each drilling rig in the fleet during the period. Management uses operating days to measure rig utilization which quantifies the revenue-generating activity of the fleet of drilling rigs.

Rig Utilization Xtreme calculates rig utilization as total operating days for all rigs divided by total days in service for all rigs. During the fourth quarter of 2013, the Company adjusted the methodology for calculating utilization in the US coil services division. Available operating days is now defined as 22 days per month for each unit as opposed to total calendar days as calculated in the past. This was based on the fact that on average the coil service units in the US spends 5 to 6 days mobilizing between wells and 2 to 3 days on preventive maintenance during the month. Utilization for prior periods presented has been restated to conform to the current presentation. Gross Margin Gross margin represents revenue less operating expenses. Management believes gross margin is a useful supplemental measure of the financial performance of Xtreme’s principal business activities before

22

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

considering how activities are financed or taxed, as well as other expenses not closely associated with activity levels. The following is the calculation of gross margin.

2013 2012

Revenue 229,823 179,387

Less: Operating expenses 144,873 127,835

Gross margin 84,950 51,552

EBITDA

EBITDA is a measure of the Company’s operating profitability. EBITDA provides an indication of the results generated by the Company’s principal business activities prior to how these activities are financed, assets are depreciated and amortized, or how results are taxed in various jurisdictions. EBITDA is defined as net income (loss) before interest, income taxes, and depreciation and amortization.

2013 2012

Net income 567 1,274

Tax expense (benefit) 4,353 (4,400)

Interest expense 7,866 7,919

Amortization of intangibles 303 303

Depreciation of property and equipment 51,192 27,266

EBITDA 64,281 32,362

Adjusted EBITDA

Adjusted EBITDA is used by management and investors to analyze EBITDA (as defined above) prior to the effect of foreign exchange and share-based payment expense and is not intended to represent net earnings as calculated in accordance with IFRS. Adjusted EBITDA is calculated as follows:

2013 2012

EBITDA 64,281 32,362

Adjustments for non-cash items 9,317 (404)

Adjusted EBITDA 73,598 31,958

Adjusted EBITDA per share ($) 0.91 0.46

Net (loss) income per share ($) (0.09) 0.02

Adjusted EBITDA attributable to:

Owners of the parent 72,704 30,107

Non-controlling interest 894 1,851

73,598 31,958

Adjustment for non-cash items include share-based payment expenses, foreign exchange gains and losses, and non-recurring losses on damage to property and equipment. It is management’s view that these items referred to above are not normal operating costs and / or are non-cash operating expenses that should be added back to earnings as they are not reflective of sustainable, ongoing operations.

23

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

The adjustments for non-cash items are as follows:

2013 2012

Stock-based compensation 1,321 1,245

(Gain) loss on sale of equipment (132) 257

Foreign exchange (gain) loss 6,494 (1,790)

Change in fair value of non-controlling interest liability 1,481 (829)

Loss on damage of property and equipment – 538

Other expense 153 175

9,317 (404)

The Company believes Adjusted EBITDA and Adjusted EBITDA per share are important measures of operating performance because it allows management, investors and others to evaluate and compare core operating results, including the return on capital and operating efficiencies, from period to period by removing the impact of the capital structure (interest expense from outstanding debt), asset base (depreciation and amortization), tax consequences, other non-operating items and share-based compensation. Furthermore, the Company uses Adjusted EBITDA for business planning purposes and to evaluate and price potential acquisitions. In addition to its use by management, the Company also believes Adjusted EBITDA is a measure widely used by securities analysts, investors and others to evaluate the financial performance of the Company and other companies in the drilling services industry. Other companies may calculate Adjusted EBITDA differently, and therefore the Adjusted EBITDA presented by the Company may not be comparable to similarly titled measures of other companies.

Net Debt

Net debt is a measurement used by management and the investment community which is composed of total debt, including amounts outstanding under the operating line, less cash and cash equivalents. Critical accounting estimates and judgments The preparation of financial statements requires management to use judgment in applying its accounting policies and estimates and assumptions about the future. Estimates and other judgments are continuously evaluated and are based on management’s experience and other factors, including expectations about future events that are believed to be reasonable under the circumstances. Critical accounting judgments Significant judgments are used in the application of accounting policies related to the following material amounts recognized in the consolidated financial statements: Consolidation

See “New and amended standards adopted by the Company” below for a discussion of the Company’s decision to consolidate Xtreme Equipment Group S.A. and Xtreme Coil Drilling Saudi Arabia Ltd. at January 1, 2013.

Assessment of Impairment Indicators For its long lived assets with determinable useful lives, Xtreme assesses for impairment at least annually as well as when circumstances suggest that the carrying amount exceed the recoverable amount, as well as the internal and external factors to determine if an impairment test is warranted.

24

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

Cash Generating Units Assets are grouped into cash generating units for the purpose of impairment testing. A CGU is defined as the lower grouping of integrated assets that generate identifiable cash inflows that are largely independent of cash inflows of other assets or groups of assets. The allocation of assets into CGUs requires significant judgment and interpretation with respect to interchangeability of rig characteristics and technology, geographic proximity, and other economic factors, including price and contract risk, operational risk, development costs and tax regimes. Critical accounting estimates Xtreme uses significant estimates in the determination of a number of account balances. These estimates have a significant risk of causing a material adjustment to the carrying amounts of the underlying assets and liabilities within the next fiscal year. Material accounts subject to significant estimates are as follows: Allowance for Doubtful Accounts

The Company performs ongoing customer credit evaluations and grants credit based on a review of historical collection experience, current aging status, financial condition of the customer and anticipated industry conditions. Customer payments are regularly monitored and a provision for doubtful accounts is established based on specific situations and overall industry conditions. Impairment of Long-lived Assets

The Company evaluates its property and equipment for impairment annually and whenever events or changes in circumstances indicate the carrying amount may not be recoverable. If there is any indication of impairment, the recoverable amount of the asset is estimated to determine the impairment loss, if any. To calculate the recoverable amount, estimates are made regarding the following factors: future demand for the Company's services by oil and gas exploration and production companies, foreign currency exchange rates and interest rates, changes in the cost and availability of financing, replacement costs of drilling equipment, future repair and maintenance costs, and the Company's future operating and financial results. In assessing fair value less costs to disposal, the estimated future cash flows are discounted to their present value using a discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted. As a result, any impairment losses are a result of management’s best estimates of expected revenues, expenses and cash flows at a specific point in time. These estimates are subject to measurement uncertainty as they are dependent on factors outside management’s control. Depreciation

Depreciation of the Company’s property and equipment incorporates estimates of useful lives and residual values. These estimates may change as more experience is obtained or as general market conditions change, thereby impacting the value of the Company’s property and equipment. During the first quarter of 2013, the Company performed a review of the depreciable lives of the rig components and related equipment. The Company’s rig components and related equipment were being depreciated on the units-of-production (“UOP”) method over a period of 3,650 to 9,125 operating days. Some rig components and equipment was also being depreciated on a straight line basis over a period of 3 to 10 years. Based on the review of the rig components and related equipment and their performance, it was determined that the estimated useful lives should be modified to better reflect the current operations and expected usage and future economic benefits. As a result of the review, management determined the following:

25

Xtreme Drilling and Coil Services Corp. For the year ended December 31, 2013 March 11, 2014

Management’s Discussion and Analysis ($ in thousands, except where indicated)

• For rigs operating in the US and Saudi Arabia, rig components and related equipment previously depreciated under UOP would be depreciated on a straight-line basis over a period of 10 to 15 years;

• For rigs operating in Canada, rig components and related equipment previously depreciated under UOP would be depreciated on a straight-line basis over a period of 13 to 20 years. The reason for the extended life versus the US and Saudi rigs is that Canadian rigs operate 9 to 10 months of the year due to break-up whereas the US and Saudi rigs work or are capable of working for the full year;

• Some rig components and related equipment previously depreciated under UOP were converted to straight line as their usage over time has no relation to production;

• The lives of assets previously depreciated under the straight-line method appeared reasonable and no changes were deemed necessary;

• The salvage value estimate of 20 percent continues to appear reasonable and no changes were made.

Management reviewed the remaining assets, such as drill pipe, vehicles, office and leasehold improvements, etc. and determined that no changes were required at this time. These assets are depreciated on a straight-line basis over a period of 3 to 10 years. Additionally, starting October 1, 2013, a second change in estimate on useful lives for certain property, plant and equipment and capital spares assets took place during the year. Essentially this arose after the completion of the physical asset verification undertaken by the Company.

Fair Value of Financial Instruments

The Company’s financial instruments included in the consolidated statements of financial position are comprised of cash and cash equivalents, accounts receivable, current liabilities, bank indebtedness and long-term debt. The fair values of financial instruments included in the consolidated statement of financial positions approximate their carrying amounts due to the short-term maturity of those instruments. Long-term debt is carried at amortized cost using the effective interest method of amortization. Income Taxes