2014 analyst day

TRANSCRIPT

1

2014 Analyst DayWaldorf Astoria - New York

June 5, 2014

Assisted Living Property – Chatham, NJ (92 units)Operated by Juniper Communities, LLC

2

This supplemental information contains forward‐looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, adopted pursuant to the Private Securities Litigation Reform Act of 1995. Statements that are not purely historical may be forward‐looking. You can identify some of the forward‐looking statements by their use of forward‐looking words, such as ‘‘believes,’’ ‘‘expects,’’ ‘‘may,’’ ‘‘will,’’ ‘‘should,’’ ‘‘seeks,’’ ‘‘approximately,’’ ‘‘intends,’’ ‘‘plans,’’ ‘‘estimates’’ or ‘‘anticipates,’’ or the negative of those words or similar words. Forward‐ looking statements involve inherent risks and uncertainties regarding events, conditions and financial trends that may affect our future plans of operation, business strategy, results of operations and financial position. A number of important factors could cause actual results to differ materially from those included within or contemplated by such forward‐looking statements, including, but not limited to, the status of the economy, the status of capital markets (including prevailing interest rates), and our access to capital; the income and returns available from investments in health care related real estate, the ability of our borrowers and lessees to meet their obligations to us, our reliance on a few major operators; competition faced by our borrowers and lessees within the health care industry, regulation of the health care industry by federal, state and localgovernments, (including as a result of the Patient Protection and Affordable Care Act of 2010 and the Health Care and Education Reconciliation Act of 2010), changes in Medicare and Medicaid reimbursement amounts (including due to federal and state budget constraints), compliance with and changes to regulations and payment policies within the health care industry, debt that we may incur and changes in financing terms, our ability to continue to qualify as a real estate investment trust, the relative illiquidity of our real estate investments, potential limitations on our remedies when mortgage loans default, and risks and liabilities in connection with properties owned through limited liability companies and partnerships. For a discussion of theseand other factors that could cause actual results to differ from those contemplated in the forward‐looking statements, please see the discussion under ‘‘Risk Factors’’ and other information contained in our Annual Report on Form 10‐K for the fiscal year ended December 31, 2013 and in our publicly available filings with the Securities and Exchange Commission. We do not undertake any responsibility to update or revise any of these factors or to announce publicly any revisions to forward‐looking statements, whether as a result of new information, future events or otherwise.

Safe Harbor

3

Welcome

Wendy Simpson

Chairman, Chief Executive Officer, and President

CEO and President since March 2007

Chief Financial Officer July 2000 – March 2007

Board Member since 1995

4

Investment StrategyClint Malin, EVP and Chief Investment Officer

Marketing StrategyMark Hemingway, VP of Marketing

Portfolio ManagementBrent Chappell, VP Investment & Portfolio Management

Financial OverviewPam Kessler, EVP, CFO and Secretary

Management Q&A SessionFireside Chat with Industry Experts

Lynne Katzmann, Founder, President and CEO of Juniper Communities, LLCRick Grimes, CEO of ALFA

Guest Speaker Q&A SessionCommunity Tour

Agenda

5

Portfolio Diversification Approach

Diversification

Property Type Geography Operator

MitigatesSingle‐Tenant Concentration

Mitigates Government

Reimbursement Exposure

MitigatesSingle‐State

Risk

6

57.3% 37.3%

4.0%1.4%

Skilled Nursing (SNF)101 PropertiesRevenue $66.2M

Assisted Living (ALF)106 Properties Revenue $43.1M

Other2 PropertiesRevenue $1.6M

Total Revenue $115.5M

Range of Care9 Properties

Revenue $4.6M

Diversification – Property Type

Pro Forma Trailing Twelve Months Ended March 31, 2014

7

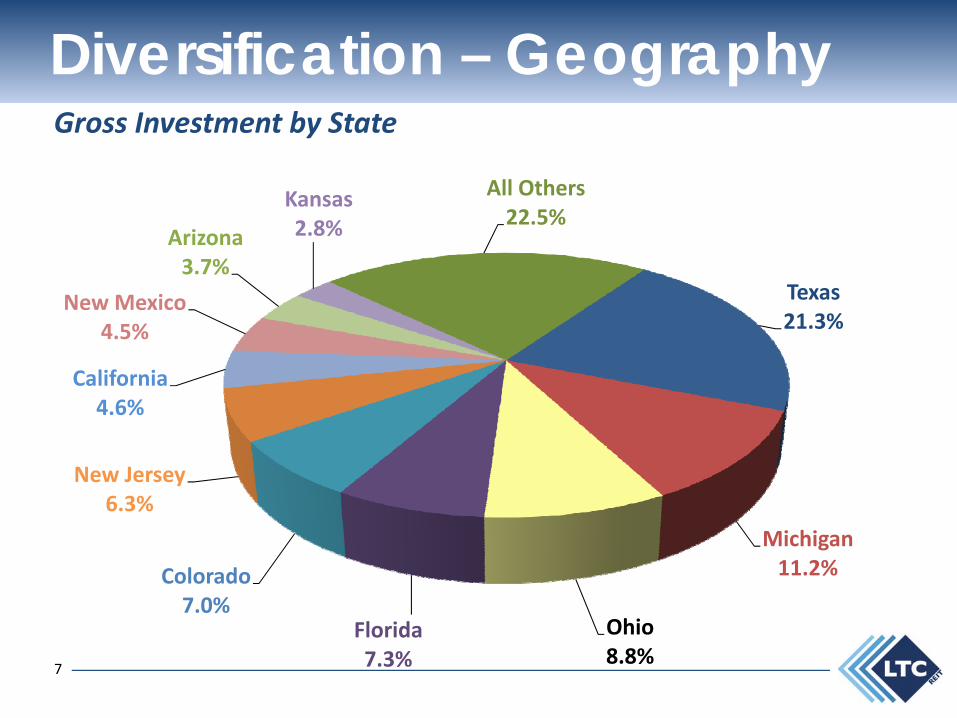

Texas21.3%

Michigan11.2%

Ohio8.8%

Florida7.3%

Colorado7.0%

New Jersey6.3%

California4.6%

New Mexico4.5%

Arizona3.7%

Kansas2.8%

All Others22.5%

Diversification – GeographyGross Investment by State

8

Prestige Healthcare12.3%

Senior Care Centers10.2%

Brookdale8.1%

Extendicare/ Enlivant7.9%

Juniper7.8%Preferred Care

7.5%

Carespring5.9%

Traditions Sr. Mgmt.5.6%

Fundamental4.0%

Skilled Healthcare3.6%

All Others27.1%

Diversification – OperatorGross Investment by Operator

9

$13

$94 $100

$245

$185

$0

$50

$100

$150

$200

$250

2009 2010 2011 2012 2013

Millions

Execution of Growth Strategy$637 Million in Investments Since 2008

10

Evolution

* Net of Asset Sales and Loan Payoffs

2008 TodayGross Investments* $581 Million $1.1 BillionAverage Portfolio Age ‐ SNF 25 years 17 yearsAverage Portfolio Age ‐ ALF 11 years 14 yearsTop 3 Tenants % of Annualized Revenue 47.2% 31.5%Debt + Preferred to Enterprise Value 30.2% 19.5%WACC 8.9% 6.0%

11

Expand Existing

Relationships

Build New Relationships

Consummate New Deals

Well Positioned for Growth

12

Investment Strategy

13

Clint Malin

Executive Vice President and Chief Investment Officer

Executive Vice President since June 2012

SVP and CIO since December 2010

VP and CIO May 2004 – December 2010

VP of Corporate Real Estate, Sun Healthcare Group

Investment Strategy

14

Sound Investment StrategyRegionally‐focused operators

Build on existing relationships

Marketing platform

Newer modernized properties

Off‐market transactions

Transaction size $10 ‐ $100 million

Diversity of property type (SNF, ALF, MC)

Strategic de novo development

15

Strong Lease-Up Results

79%

100%

57%

38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Amarillo, TX Littleton, CO Wichita, KS Slinger, WI

7/10/2013 7/9/2013 10/31/2013 2/14/2014

120‐beds SNF 60‐units MC 77‐units ALF/MC 106‐beds SNF

Development Lease‐Up

16

SNF45%

ALF/MC33%

MC22%

9.4%

7.8%8.4%

0%

2%

4%

6%

8%

10%

Development Expansion Renovation

WA Cash Yield

Development ActivityDevelopment, Expansion and Renovation

Commitments by Property TypeInvestment Commitment – $92.8M

Remaining Commitment

$56.3M61%

Funded to Date$36.5M39%

17

Re-Leasing Initiative

18

A Platform for Growth

Growth

Existing Relationships

Marketing Platform

Competitive Cost of Capital

Development Program

Proactive Portfolio Management

Proven Execution of Strategy

19

Marketing Strategy

20

Mark Hemingway

Vice President of Marketing since June 2013

VP Investment & Asset Management January 2011 –June 2013

Asset Management Consultant for LTC October 2002 – January 2011

VP Operations CLC Healthcare

Director of the Office of Long Term Care for the State of Arkansas

Marketing Strategy

21

Selling The Seven C’s of Success

Selling the

Seven C’s

CommitmentCustomer Success

ConsultativeApproach

CandorContact and Continuity

Communication

Competition

22

Candor

Customer Success

Consultative Approach

Commitment

Communication

Contact/Continuity

Competition

Selling The Seven C’s of SuccessSenior housing industryOperating partners

LTC’s long term success depends on customers/operating partners’ success

A trusted resourceRelationship focus

Transparent processPeople like doing business with people they know, like and trust

Frequent touch points with senior managementTenureRelationships that transcend business

SpeakingAdvertisingWeb – Rebranding initiative

AwarenessDifferentiation

23

Portfolio Management

24

Brent Chappell

VP, Investment and Portfolio Management

Joined LTC Properties –June 2013

VP, Portfolio Management, Nationwide Health Properties, Inc.March 2006 – February 2012

Director, Asset Management, Pacific Life Insurance Co.

Portfolio Manager, Catellus Development Corporation

Portfolio Management

25

Master Lease• Of our owned portfolio, 91% of the properties are subject to a master lease – with 91%

of our rent derived from these master leased properties (as of 3/31/14)

Triple‐Net (NNN) Structure• Taxes, insurance, assessments, maintenance and repair (including capital

expenditures), and all other operating costs are paid by lessee

Credit Enhancements• Guaranties• Security deposit – letter of credit• Escrow and reserve accounts• Minimum rent coverage / tangible net worth requirements

Property Inspections• Physical assessment of each facility once every two years

Financial Reporting• Facility level reporting required at least quarterly

Protective Lease TermsPortfolio of leased properties protectively structured

26

Same Property Portfolio Stats TTMOwned

PropertiesOccupancy Normalized

EBITDARM Coverage

NormalizedEBITDARCoverage

4Q13 3Q13 4Q13 3Q13 4Q13 3Q13

Assisted Living (1) 87.7% 87.4% 1.65 1.63 1.39 1.38

Skilled Nursing 79.7% 79.1% 2.28 2.34 1.68 1.73

Range of Care 86.7% 86.2% 1.85 1.80 1.39 1.34

(1) Excludes Extendicare/Enlivant

27

Coverage Relative to Select Peer Group

Note: As referenced for NHI, “EBITDARM Coverage ‐ Skilled” excludes NHC

1.90

2.17

1.71

2.28

1.90

1.661.70 1.70

1.00

1.20

1.40

1.60

1.80

2.00

2.20

EBITDARM Coverage ‐ Skilled

1.30 1.31 1.32

1.65

1.41

1.30 1.28

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

EBITDARM Coverage ‐ Seniors Housing

28

44.9%Pop: 19.8M ‐ 2.0M

18.2%Pop: 1.9M – 0.5M

17.2%Pop: 0.5M – 50K 15.6%

Pop: 218K– 13K

4.1%Pop: < 100K

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

MSAs 1‐31 MSAs 32‐100 MSAs > 100 Cities in Micro‐SA Cities not in an MSA or Micro‐SA

Over 60% in Top 100 MSAs

Gross Portfolio by MSAWeighted toward major metropolitan areas

29

Aggregate Government Reimbursement Exposure Less than 45%

Prepared for Reimbursement Uncertainty“Same Property Portfolio” Quality Mix

57% 16%

27%

Private Pay Medicare Medicaid

30

3.4%8.3%

2.5%8.9%

52.7%

1.0% 0.8% 0.1% 0.0%

12.0%

0%

10%

20%

30%

40%

50%

60%

2015‐2017 2018 2019 2020 Thereafter

Leases Loans

Investment Portfolio MaturitiesLease and Mortgage Loan Receivable Maturity(as a % of total gross owned investment and mortgage loans outstanding)

31

Financial Overview

32

Pam Kessler

Executive Vice President and CFO since December 2010

Senior Vice President and CFO March 2007 – December 2010

Vice President and Controller July 2000 – March 2007

The Ezralow Company (commercial real estate investment company)

Irvine Apartment Communities (multi‐family REIT)

Ernst & Young LLP

Financial Overview

33

Capital Structure Activities

WACC = 8.9% WACC = 6.0%

• $348 Million in Common Equity• $256 Million in Senior Unsecured Notes

$604 Million of New Capital Raised 2009‐2014

Redeemed Preferred Stock and Funded New Investments

Debt5%

Preferred Stock

Common Stock

2008

70%

25%

DebtPreferred Stock2%

Common Stock

Today

81%

17%

34

At 3/31/14 Capitalization

Debt

Bank borrowings – LIBOR +1.25% $41,000

Senior unsecured notes – weighted avg. rate 4.84% $251,633

Mortgage loans payable ‐‐

Bonds payable – weight avg. rate 3.27% $1,400

Total debt $294,033 17%

No. of Shares 5/30/14 Closing Price

Equity

Preferred stock – Series C $38,500 2%

Common stock 34,817,385 $39.74 $1,383,643 81%

Total equity $1,422,143 83%

Total Market Value $1,716,176 100%

Less: Cash and cash equivalents $(7,542)

Enterprise Value $1,708,634

Investment Grade Balance SheetNAIC‐2 Rated

35

Investment Grade Balance SheetNAIC‐2 Rated

LTC HC REIT AverageDebt to Enterprise Value 17.2% 30.3%Debt & Preferred to Enterprise Value 19.5% 31.2%Secured Debt to Total Debt 0.5% 20.1%Debt to Normalized TTM EBITDA 3.0x 5.7xNormalized TTM EBITDA/TTM Fixed Charges 6.7x 4.2x

36

$41.0M

$29.2M $26.7M$26.2M

$28.2M$25.7M

$32.2M $32.2M

$51.5M

$1.4M

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

2015 2016 2017 2018 2019 2020 2021 Thereafter

LOC Sr. Unsecured Bonds Payable

Debt Maturity

86% of debt is fixed long‐term with a weighted average interest rate of 4.8%14% of debt is short‐term floating rate debt under unsecured line of credit with pricing at LIBOR +125 at March 31, 2014

Millions

37

Investments Carry Attractive YieldsGAAP Yield Lease vs. WACC

10.4%10.8% 10.5%

9.1%9.6%

7.1% 7.1%6.6% 6.2% 6.3% 6.0%

0%

2%

4%

6%

8%

10%

12%

2009 2010 2011 2012 2013 Today

GAAP Lease Yield WACC

5‐Yr Average GAAP Lease Yield

9.9%

5‐Yr AverageWACC6.7%

38

• $199 million available under unsecured credit agreement • $30 million available under private shelf agreement

Additional $229 Million in Committed Debt Financing

Even Assuming full usage, leverage would remain modest

Ample Flexibility To Pursue Further Investments

Committed Financing to Fund Future Growth

39

$0.00

$0.22

$0.45

$0.68

$0.91

$1.13

$1.36

$1.59

$1.81

$2.04

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Since 2003, LTC has grown its annual dividend to $2.04 per share from $0.65.LTC currently pays a monthly dividend of $0.17 per share.

Safe and Growing Dividend

40

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

Target Payout 80%

Strong Dividend CoverageDiluted Normalized FAD Dividend Payout Ratio

41

Management Q&A

42

Fireside Chat

Lynne KatzmannFounder, President and CEO

Rick GrimesCEO

43

Juniper CommunitiesLynne KatzmannFounder, President and CEO

Founded: 1988

Communities: 18Assisted Living, Memory Care, Skilled Nursing

Annual Revenues: $65 million

Resident Capacity: 1,251

Geography: Colorado, Florida, New Jersey, Pennsylvania

LTC Relationship: Operator

44

Assisted Living Federation of America (ALFA)

Rick Grimes

CEO

Membership: Operators and managers of senior living communities; allied companies that serve with senior living operators

Mission: Members exemplify the principles of choice, dignity, and independence for seniors

Advocacy: Educates federal and state policymakers about the assisted living philosophy and advocates for public policy that advances quality of life for seniors

45

Guest Speakers Q&A