©2014, college for financial planning, all rights reserved. session 11 taxation of life insurance,...

TRANSCRIPT

©2014, College for Financial Planning, all rights reserved.

Session 11Taxation of Life Insurance, Disability Insurance, and Annuities

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMIncome Tax Planning

Session Details

Module 6

Chapter(s)

1 and 2

LOs 6-1 Identify characteristics of a form of cash value life insurance policy.

6-2 Analyze a situation to identify an income tax implication of an insurance policy.

6-3 Identify characteristics of a form of annuity contract.

6-4 Analyze a situation to identify an income tax implication of a commercial annuity.

11-2

Payouts from Life Insurance

11-3

Payouts from Life Insurance

11-4

Modified Endowment Contract

MEC Rules• Life insurance contracto meets state law definitiono meets IRC definitiono issued on or after June 21, 1988o fails to meet the 7-pay test

• Distributions treated on LIFO basiso withdrawalso loanso dividends received as cash or used to pay a

loan• 10% penalty tax on taxable portion

11-5

Disability Insurance Benefits

• If employer paid—benefits fully taxable

• If employee paid—benefits fully excluded

• If employer & employee paid—benefits partially taxable

• If taxable—benefits subject to FICA and FUTA for first 6 months

11-6

Annuity Contracts

• Fixed Annuity: Fixed annuity payment guaranteed upon payment of level or flexible premiums

• Variable Annuity: Amount of annuity payment varies according to investment performance of underlying assets

• Deferred Annuity: Annuitant pays now for future fixed or variable payments

• Accumulation of Earnings: Grows on a tax-deferred basis

11-7

Commercial Annuities

Nonperiodic distributions• Post-August 13, 1982, Contract: Fully taxable

interest to the extent that cash surrender value of contract exceeds the investment (LIFO)

• Pre-August 14, 1982, Contract: Nontaxable premium dollars treated as first distributed (FIFO)

Distribution prior to age 59½• Inclusion of taxable amount as ordinary income

• 10% premature withdrawal penalty on taxable portion of withdrawal

11-8

Annuitized Distributions• Fixed Annuity—Exclusion ratio

• Variable Annuity—Amount excluded

11-9

Investment in contract

Total expected return

Investment

Number of payments

If annuity start date before 1987, exclusion applies to ALL payments received.

• Partial annuitization allowed—after 2010

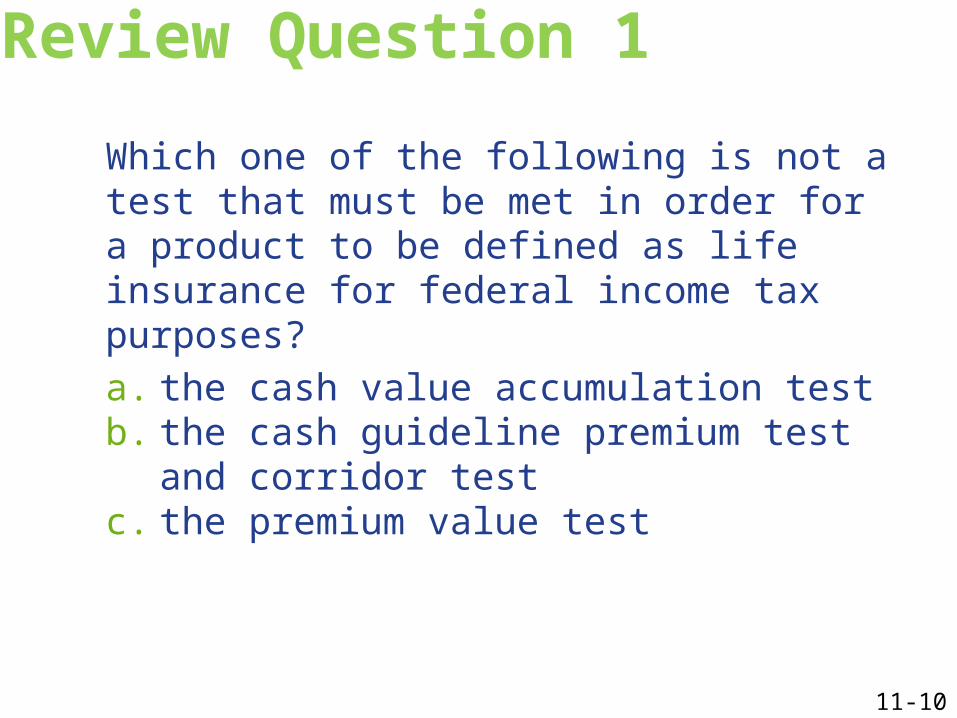

Review Question 1

Which one of the following is not a test that must be met in order for a product to be defined as life insurance for federal income tax purposes?a. the cash value accumulation testb. the cash guideline premium test and

corridor testc. the premium value test

11-10

Review Question 2

Which one of the following does not correctly state a characteristic of a commercial annuity?a. With an annuity, there is a maximum annual

contribution per year, which is adjusted yearly for inflation.

b. An annuity is a contract in which investments are made in exchange for a promise of regular frequent payments for the rest of a taxpayer’s life or a fixed period of time.

c. Annuity contracts may vary regarding the payment time period and the frequency of the payments.

d. An annuity payment is generally part return of capital and part interest payment.

11-11

Review Question 3

Which one of the following statements is true regarding non-periodic distributions from an annuity contract prior to the annuity start date, issued after August 13, 1982?

a. A non-periodic distribution is first considered a tax-free return of principal and then a taxable interest payment.

b. A non-periodic distribution is prorated equally between a tax-free return of principal and a taxable interest payment.

c. A non-periodic distribution is taxed under the exclusion ratio rules.

d. A non-periodic distribution is taxed first as a taxable interest payment until the interest payments are completely exhausted and then as a tax-free return of principal.

11-12

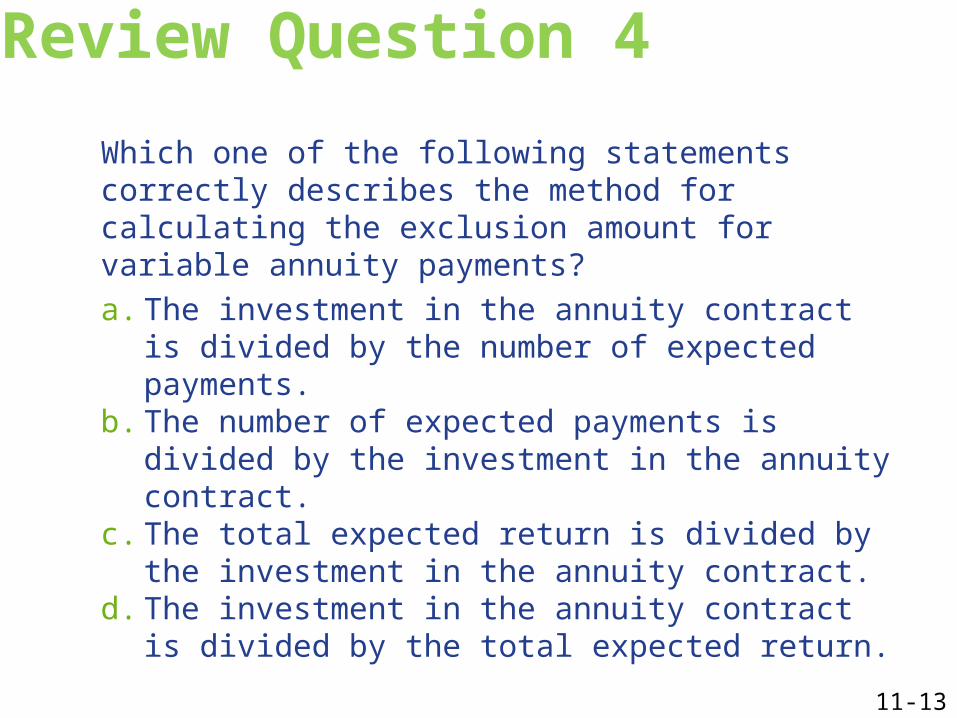

Review Question 4

Which one of the following statements correctly describes the method for calculating the exclusion amount for variable annuity payments?a. The investment in the annuity contract is

divided by the number of expected payments.

b. The number of expected payments is divided by the investment in the annuity contract.

c. The total expected return is divided by the investment in the annuity contract.

d. The investment in the annuity contract is divided by the total expected return.

11-13

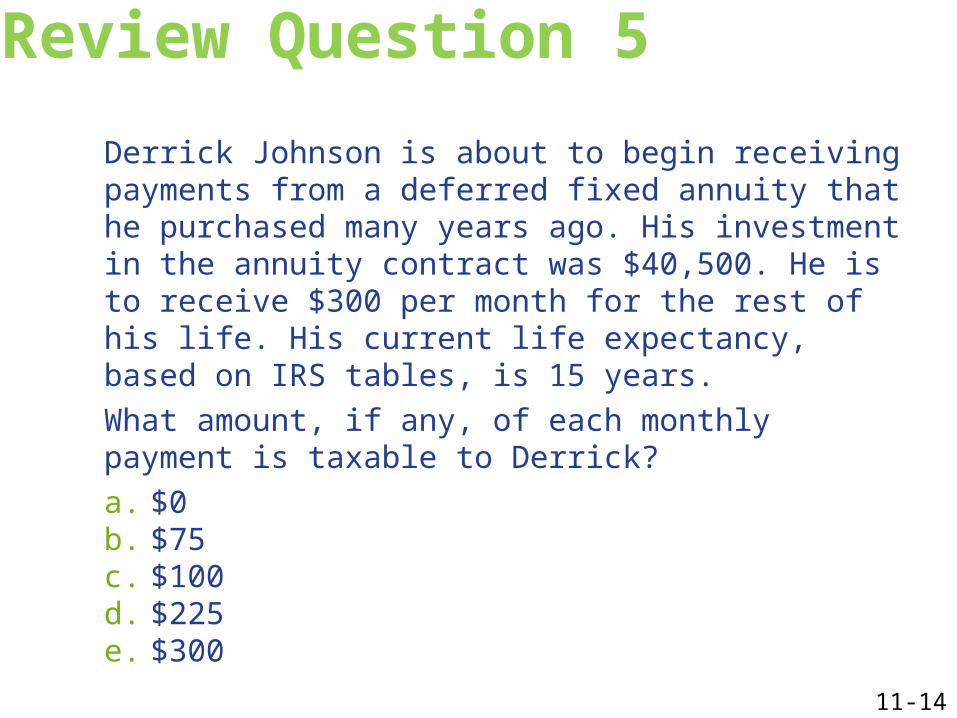

Review Question 5

Derrick Johnson is about to begin receiving payments from a deferred fixed annuity that he purchased many years ago. His investment in the annuity contract was $40,500. He is to receive $300 per month for the rest of his life. His current life expectancy, based on IRS tables, is 15 years.What amount, if any, of each monthly payment is taxable to Derrick?a. $0b. $75c. $100d. $225e. $300

11-14

©2014, College for Financial Planning, all rights reserved.

Session 11End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMIncome Tax Planning