2014 health care reform overview 11-29-12 - unitedhealthcare

TRANSCRIPT

Cover

area with cropped

image.

Do not overlap

blue bar.

Completely cover

gray area.

UnitedHealthcare and Health Reform

On the Horizon: 2014

Health Care Landscape Reform Timeline

Though several key compliance provisions are behind us, the most material

marketplace changes won’t come until 2014 – Adjusted Community Rating, Guaranteed

Issue, Industry Fees, Essential Health Benefits, Medicaid Expansion and Exchanges

Compliance Compliance, Growth and Transparency

2

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

3

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

July/August September Q4 2012 Q1 2013

• Supreme Court

decision (late June)

• MLR rebates

delivered 8/1

• Expansion of

Women’s

Preventive Care

• MLR process

begins for 2013 –

survey to

determine ATNE

• Summary of

Benefits and

Coverage

document for new

and open

enrollments after

9/23

• PCORI fee for

plans ending

10/1/12 (pay by

July 2013)

• Guidelines for

Essential Health

Benefits and

state benchmark

plan decisions

• New product

portfolio and rate

filings begin

Advocacy on impact of 2014 ACA requirements & market changes

• FSA limits $2500

• Employer

Required W-2

filing

• Broker meetings

and updates on

new product

portfolio – ACR

and market

changes for small

group

• Exchange

notification

Health Care Reform Landscape 2012 Focus

4

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Highlights

• 30 million newly insured

individuals

• Perhaps 80 million

switching coverage source

• 20+ million purchasing

through Exchanges

• Number covered by

Medicaid increases by 15+

million

• Average subsidy of $5,000-

$6,000 per subsidized

enrollee

• Medicaid primary care

reimbursement increased to

Medicare rates (2013 and

2014)

Estimates above based on public sources

including CBO and Lewin Group publications

Guaranteed

Issue

Taxes, Fees &

Assessments

Employer

Mandate /

Penalty

Medicaid

Coverage

Expansion

Premium

Subsidies

Cost-Sharing

Subsidies

Adjusted

Community

Rating

Expanded

Benefits /

Mandates

Cost-Sharing

Limits

Risk

Adjustment &

Reinsurance

CO-OPS &

Multi-State

Plans

Individual

and SHOP

Exchanges

2014 PPACA Insurance Market Provisions

Though several key compliance requirements are behind us, the

most material marketplace changes won’t come until 2014

Health Care Reform Landscape What Happens in 2014?

Health Care Reform Landscape What Happens in 2014?

5

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

On the Horizon

• Expanded Benefits – State-defined Essential Health Benefits (EHB) to include ten mandated

categories, including pediatric dental/vision; No lifetime limits; No annual dollar limits on EHB; Actuarial

value thresholds.

• State definitions of EHB will vary and may require product adjustments. Employers will need to

adjust plan design and offerings based on rules going into effect.

• Rating Changes – Community rating; Guaranteed issue of coverage; No medical underwriting; Ban

on pre-existing condition exclusions (for all ages).

• Health insurance in the individual and small group market will only be able to vary premiums by

family size, geography, tobacco use and age. Other rating factors currently used, such as gender

industry, group size, health status and medical history will be prohibited.

• Taxes and Fees – Assessments to insurers and employers to pay for subsidies and risk adjustments

(e.g., Patient-Centered Outcomes Research Institute Fee, Insurer Fee, Reinsurance Fee)

The Resulting Landscape

• A number of fees and taxes, and benefit requirements that will affect the cost of health care for

employers during the next several years.

• While the exact cost may differ for each employer based on location and plan design offered, on

average employers are expected to see a substantial increase in costs.

6

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Eff.

Date

Provision Description Small Group1 Large Group Individual Applies

to GF?2

FI ASO FI ASO

8-1

2

Women’s

Preventive

Expand to include additional screening, prenatal office

visits, breastfeeding support and some contraceptives. Yes Yes Yes Yes Yes

1-1

3

FSA Limits Employee contributions limited $2,500 per year, with

increases allowed in future years to adjust for inflation. Yes Yes Yes Yes n/a Yes

1-1

4

Essential Health

Benefits (EHB)

Health Plans must provide EHB for individual and small

group. Ten mandated benefit categories (to include

pediatric dental and vision). Subject to state variation. Yes No No No Yes

Annual/Lifetime

Limits

Must be removed for all services defined as essential

health benefits Yes Yes Yes Yes Yes3 Yes3

Deductible

Limits

Plan design deductibles may not exceed a $2,000 (self-

only) or $4,000 (other than self-only) limitation Yes No No No No

OOP Max Must comply with OOP limits for HSA qualified plans Yes Yes Yes Yes Yes

Clinical Trials Must cover routine costs associated with clinical trials Yes Yes Yes Yes Yes

Actuarial Value Plans must be Bronze (60%), Silver(70%), Gold (80%) or

Platinum (90%) Metallic Levels Yes No No No Yes

Waiting Periods Maximum 90 day waiting period Yes Yes Yes Yes No Yes

Pre-Ex

Conditions

Pre-existing condition exclusions must be removed for all

members, not just those under age 19. Yes Yes Yes Yes Yes Yes

Community

Rating

Rate factors limited to family structure, benefit plan design, geography, tobacco use and age. Prohibited: gender, group size, health status, medical history

Yes No No No Yes

Expanded Benefits & Rating Changes General Overview

1 Prior to 2016, states may define SG as 1-50 2 All provisions listed apply to nongrandfathered plans 3 Removal of annual limits does not apply to grandfathered Individual plans

7

Confidential Property of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Plans in individual and small group markets must provide Essential Health Benefits Package – four components of the package:

1. Essential Health Benefits – 10 required coverage categories • Pediatric dental and “habilitative services” are “new”, not typically covered by UHC

• HHS has delegated EHB definition via “benchmark plans” to states (by Q4 2012)

• Practical impact State mandates will be required by EHB

2. Out-of-Pocket Maximum new accumulation rules and ceiling • OOPM ceiling at HSA level: likely $6,400/12800 in 2014 (indexed to inflation)

• All cost-sharing (for essential health benefits) must accumulate to OOPM

• Applies broadly all plans, all group sizes, all funding approaches

• Does not apply to out-of-network benefits

3. Small group deductible ceiling $2,000 single/$4,000 family • Indexed to inflation

• Exception for Bronze plans if you cannot “reasonably” design one with a $2000 deductible

• Does not apply in individual market

• Does not apply to out-of-network benefits

4. Limited to “Metallic” coverage levels (Bronze, Silver, Gold, Platinum) • Defined by actuarial value (plus/minus 2%): Bronze/60%, Silver/70%, Gold/80%, Platinum/90%

• Federal requirement to offer one Silver, one Gold plan on Exchanges

• Metallic level requirement applies BOTH on and off-exchange

*Grandfathered plans exempt from above requirements

Confidential Property of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

7

Expanded Benefits Reform Provisions Impacting Product & Plan Design

Individuals and employers will be required to have/provide “minimal essential coverage” • Minimum actuarial value of 60%

PPACA plan design rules pricing impact dependent on starting plan design & customer reaction

Small group pricing impact estimate: 4-11% pricing increase (in extreme situations, could be >20%)

Large group estimate: 3-6%

These changes are independent of other price impacts from PPACA (e.g. taxes/fees, community rating, etc.)

Confidential Property of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

8

Impact Assessment Estimated Pricing Impacts from ACA-driven Plan Design Changes

Plan A Plan B Plan C Plan D Plan E

Description

Mainstream copay

plan

Richer copay plan

(if conform to Silver)

Richer copay plan

(if conform to Gold)

High deductible

copay plan

Very high deductible

HSA plan

Deductible $1,500 $500 $500 $2,500 $5,000

Coinsurance 80% 80% 80% 90% 100%

Approx. Actuarial Value 70% 75% 75% 70% 60%

Essential Health Benefits 1-5% 1-5% 1-5% 1-5% 1-5%

Conform to Metallic Level n/a 3-7% 3-7% n/a n/a

Flat-dollar copays to OOPM 3-6% 3-6% 3-6% 3-6% n/a

Lower Deductible to Ceiling n/a n/a n/a 1-2% 11-17%

Changes to Compensate for Deductible n/a n/a n/a 1-2% 11-17%

Deductible $1,500 $1,500 $500 $2,000 $2,000

Coinsurance 80% 80% 90% 85% 50%

Approx. Actuarial Value 70% 70% 80% 70% 60%

Direct Pricing Impact 5-13% 12-22%

Impact if Compensating for Deductible Ceiling 4-11% 1-5% 4-11% 1-4% 7-18% Total

Starting

Plan Details

PPACA-

Driven

Product

Changes

Revised

Plan Details

9

Description Effective

Date

Timing /

Duration

Payment

Cycle

Segment

Impact Basis of Assessment

PCORI Fee

• Help fund Patient-Centered Outcomes Research Institute

• Will assist patients, clinicians, purchasers and policy-makers

in making informed health decisions by advancing the quality

and relevance of evidence-based medicine through the

synthesis and dissemination of comparative clinical

effectiveness research findings.

• Proposed rule

10/1/12

Begins

2012

Phases out

2019

July 31

(calendar year

following end

of plan year)

FI and ASO

(ASO paid and

remitted by

customer)

Groups and

Individuals

$1 pmpy in Year 1

$2 pmpy in Year 2

Insurer Fee

• Annual fee on health insurance sector, allocated by market

share, to fund health insurance exchange subsidies.

• Fees assessed on net written health insurance premiums,

with certain exclusions.

• No federal guidance received to date

1/1/14 Permanent

No later than

September 30

of calendar

year

FI Only

Groups and

Individuals

Industry wide targets

$8B – 2014

$11.3B – 2015

$11.3B – 2016

$13.9B – 2017

$14.3B – 2018

~ 2.3% of premium

Reinsurance

Fee

• Transitional fees to stabilize individual market; assessed on

a per capita basis for both fully insured and ASO members.

• Fee funds reinsurance for high claimants in non-

grandfathered individual market plans, on and off Exchange.

• Final Rule from CCIIO; awaiting federal and state notices of

payment rules (fall 2012)

1/1/14 3 Years

(2014-2016)

FI: State

determined;

ASO: Federal,

Quarterly

basis

beginning

1/1/14

FI and ASO

(ASO funded

by customer,

TPA remit on

behalf of ASO

groups)

Groups and

Individuals

Industry wide federal

targets, to which states

may add:

$12B – 2014

$8B – 2015

$5B – 2016

~ $6 pmpm

Excise Tax

on High Cost

Coverage

(Cadillac Tax)

• Imposes an excise tax on insurers and employers who offer

rich benefit coverage.

• No federal guidance to date.

1/1/18 Permanent TBD

FI and ASO

Groups

40% of value of

employer-sponsored

coverage exceeding

$10,200

individual/$27,500

family; indexed by cost

of living in subsequent

years

* Projections based on analysis of study by Oliver Wyman & AHIP 2012

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Taxes and Fees General Overview

10

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Individual Market Premium Increase Small Group Market Premium Increase

Avg Rate

Increase

15%

Taxes / Fees

3.8%

Product

5%

Pre-Reform Post-Reform

15%

25% - 50%

Healthiest

Groups

25%

Avg Rate

Increase

12%

Taxes / Fees

3.8%**

Rating Rules

/ Product

100%+*

Pre-Reform Post-Reform

12%

116%

Reform Compliance Drives

Significant Price Increase

Community Rating Causes Material

Price Disruption For Healthiest Groups

• Consumers (both group and individual buyers) will face substantial price increases,

further pressuring the system.

• New pricing rules and new product design mandates will have a significant impact

on the price consumers pay for insurance in 2014 and beyond.

* Individual rates expected to increase 100% to up to 200% due to product and rating changes.

** May be partially offset by reinsurance payments, net impact not yet known.

Reform Premium Impact Assessment Individual, Small and Large Fully Insured Market

Product

3 to 6%

Pre-Reform Post-Reform

15%

20% to 25%

Avg Rate

Increase

15%

Taxes / Fees

3.8%

Avg Rate

Increase

15%

Avg Rate

Increase

15%

Avg Rate

Increase

15%

Large Group Premium Increase

Incremental Increase to rates beginning in

2013 to cover taxes, fees, and benefit Δs

11

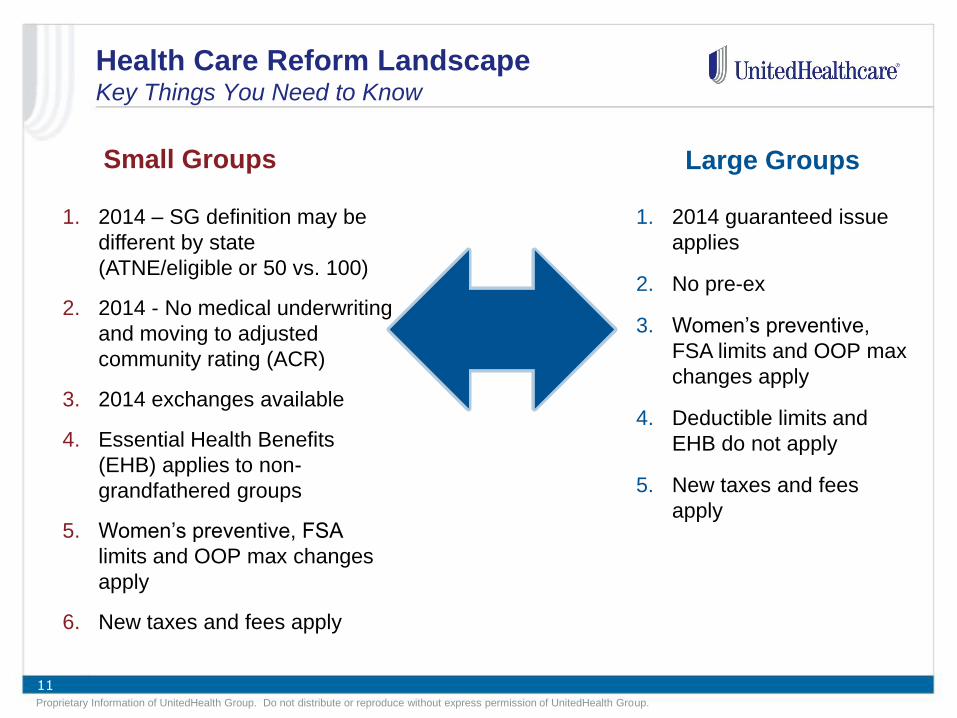

Health Care Reform Landscape Key Things You Need to Know

Small Groups

1. 2014 – SG definition may be

different by state

(ATNE/eligible or 50 vs. 100)

2. 2014 - No medical underwriting

and moving to adjusted

community rating (ACR)

3. 2014 exchanges available

4. Essential Health Benefits

(EHB) applies to non-

grandfathered groups

5. Women’s preventive, FSA

limits and OOP max changes

apply

6. New taxes and fees apply

Large Groups

1. 2014 guaranteed issue

applies

2. No pre-ex

3. Women’s preventive,

FSA limits and OOP max

changes apply

4. Deductible limits and

EHB do not apply

5. New taxes and fees

apply

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Responsible

health

consumers

Integrated

clinical

services

Powerful

information

Focus on

service

Network

access

Innovative

solutions

We give

individuals

personal

information and

support to help

identify and

respond sooner

to health risks

and opportunities.

Integrating more

clinical data

sources and

evidence based

medicine

standards helps

us to identify risks

earlier and better

control costs.

We provide

insights

vital to improve

decision making

and health

results.

Continuous

process

improvements

drive a better

consumer

experience and

greater

satisfaction.

Our large

network

better access and

lower, more

predictable costs

on a local and

national level.

Creative

products

and technologies

that change

behavior and

support higher

quality outcomes.

UnitedHealthcare Engaged and Positioned for the Future

12

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

12

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

Better

information.

Better

health.

Better

decisions.

13

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

United for Reform Resource Center

• Health Reform Provisions and Health Reform Videos

− Summary, Links, FAQs, Video, Employer Guide

www.uhc.com/reform

14

Proprietary Information of UnitedHealth Group. Do not distribute or reproduce without express permission of UnitedHealth Group.

• Adult child coverage until

age 26

• Annual dollar limits

restricted

• Early retiree reinsurance

program (ERRP)

• ER coverage as

in-network, no

prior authorization G

• Initial appeals review

standards G

• Lifetime dollar limits

prohibited

• Medicare Part D rebate

for beneficiaries in the

gap

• No pre-existing conditions

for kids until age 19

• Online consumer

information at

healthcare.gov

• Pediatricians as PCPs,

direct access to

OB/GYNs G

• Preventive services with

no cost sharing G

• Rescissions prohibited

except for fraud or non-

payment

• Small business tax credit

• Temporary high risk pool

• Annual fee on pharmaceutical manufacturers begins

• Annual rate review process

• Appeals ombudsmen and process documentation G

• Auto-enrollment for groups with 200+ FTEs (implementation delayed until regulations released)

• Discounts in Medicare Part D “donut hole”

• HSAs/HRAs/FSAs: limitations for OTC medications

• Increase penalty for non-qualified HSA withdrawals

• Minimum medical loss ratio (MLR): 85% for large group; 80% for small group and individual

• Non-discrimination rules apply to insured plans (implementation delayed until regulations are released) G

• Small business wellness grants

• Administrative

simplification begins

• Annual fee on medical

device sales begins

• Deduction for

expenses allocable to

the Part D subsidy for

“qualified prescription

drug plans” eliminated

• Employee notification

of access to

Exchanges

• FSA contributions

limited to $2,500

• High earner tax begins

• Patient-centered

Outcomes Research

Institute (PCORI) fee

increases to $2 per

member/year

• W-2 reporting on the

value of employer-

sponsored health

benefits

• Annual insurer industry fee through 2018

• Coverage for all adult children until age 26 including those that have employer coverage (formerly not covered for grandfathered plans)

• Deductible caps cannot exceed $2K for individual and $4K for family G

• Guarantee issue and renewal rules G

• Health Benefit Exchanges

• ICD-10 code adoption

• Individual & employer mandates

• Mandatory coverage for clinical trials G

• No annual limits

• No pre-existing condition exclusions

• OOP limits must comply with OOP limits for HSA qualified plans G

• Rating restrictions G

• Standardized essential health benefits

• Tax credits and subsidies for individuals and small employers

• Waiting period limits

• 60-day advance notice

of material modifications

• Accountable Care

Organization

requirements

• Appeals provision fully

implemented G

• First medical loss ratio

rebates to be paid by

August

• New women’s

preventive services with

no cost sharingG

• Patient-centered

Outcomes Research

Institute (PCORI) fee

($1 per member/year)

• Quality bonus begins for

Medicare Advantage

plans

• Quality of Care

Reporting Requirements

• Summary of Benefits

and Coverage (SBC)

and the Uniform

Glossary

• High-value plan

excise tax begins

(2018)

• Medicare Part D

“donut hole” closed

by 2020

• States can open

Exchanges to CHIP

eligibles (2015) and

all employers (2017)

2010 2011 2014 2012 2013 2015 & beyond

G Grandfatherable provision

Rev. 9/12

Note: some provisions apply only to fully insured business (e.g., MLR and guarantee issue)

Health Care Reform Timeline