2015 brp-special-report-mobile-technology 0219151

TRANSCRIPT

Gold Sponsors:

Mobile Technology – Transforming the Customer Experience

BRP SPECIAL REPORT A supplemental report based on the findings from the

2015 POS/Customer Engagement Benchmarking Survey

http://bit.ly/BRPSurvey

Mobile Technology – Transforming the Customer Experience | 2

increase in mobile POS

implementations in 2 years

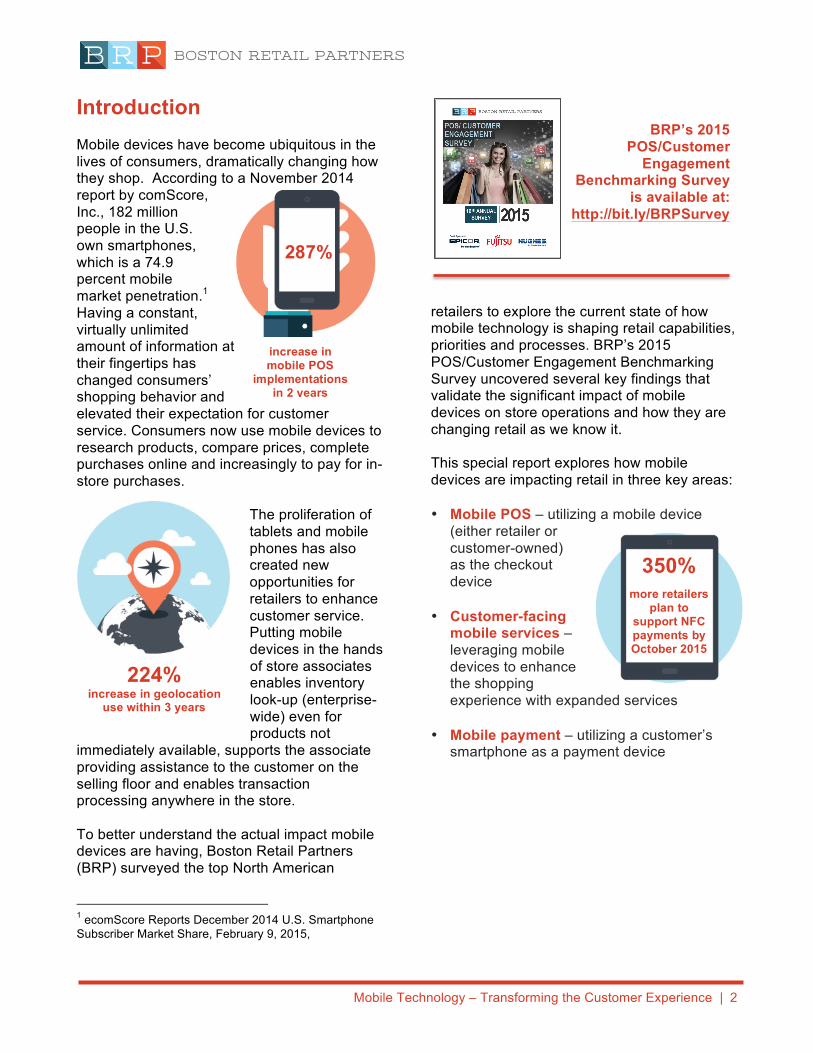

Introduction Mobile devices have become ubiquitous in the lives of consumers, dramatically changing how they shop. According to a November 2014 report by comScore, Inc., 182 million people in the U.S. own smartphones, which is a 74.9 percent mobile market penetration.1 Having a constant, virtually unlimited amount of information at their fingertips has changed consumers’ shopping behavior and elevated their expectation for customer service. Consumers now use mobile devices to research products, compare prices, complete purchases online and increasingly to pay for in-store purchases.

The proliferation of tablets and mobile phones has also created new opportunities for retailers to enhance customer service. Putting mobile devices in the hands of store associates enables inventory look-up (enterprise-wide) even for products not

immediately available, supports the associate providing assistance to the customer on the selling floor and enables transaction processing anywhere in the store. To better understand the actual impact mobile devices are having, Boston Retail Partners (BRP) surveyed the top North American

1 ecomScore Reports December 2014 U.S. Smartphone Subscriber Market Share, February 9, 2015,

retailers to explore the current state of how mobile technology is shaping retail capabilities, priorities and processes. BRP’s 2015 POS/Customer Engagement Benchmarking Survey uncovered several key findings that validate the significant impact of mobile devices on store operations and how they are changing retail as we know it. This special report explores how mobile devices are impacting retail in three key areas: • Mobile POS – utilizing a mobile device

(either retailer or customer-owned) as the checkout device

• Customer-facing mobile services – leveraging mobile devices to enhance the shopping experience with expanded services

• Mobile payment – utilizing a customer’s

smartphone as a payment device

224% increase in geolocation

use within 3 years

350%

more retailers plan to

support NFC payments by October 2015

287%

BRP’s 2015

POS/Customer Engagement

Benchmarking Survey is available at:

http://bit.ly/BRPSurvey

Mobile Technology – Transforming the Customer Experience | 3

Mobile POS Enables the Customer Mobile point of sale (POS) enables the store associate to complete a customer purchase on the sales floor at the moment a buying decision is made. Bringing the checkout process to the customer at the moment she makes her purchasing decision (and before she changes her mind) also benefits the retailer. With mobile POS devices, associates are no longer chained to the checkout desk so they can interact with the customer anywhere in the store. Associates can also use mobile POS devices to answer customer questions, locate non-stocked or special order products and provide product or store information. Retailers understand the value of mobile POS and are making it a key priority, as indicated by BRP’s 2015 POS/Customer Engagement Benchmarking Survey. When we asked some of the top North American retailers what their top priorities are for 2015, 24% reported mobile POS as one of their top three priorities (Exhibit 1). Respondants reported that 15%

have mobile POS already installed, 43% are planning to implement in two years and another 13% plan to implement at some point beyond two years. This indicates a 373% increase in the planned implementation of mobile POS (from 15% today to 71%) over the survey timeframe. The survey also reported 43% of retailers plan to allow customer-owned mobile devices as POS in the future, with 19% planning to make this leap in the next two years (Exhibit 2). There are different paths that retailers are taking to implement some form of mobile POS, as the application of mobile technology varies

5%

8%

13%

15%

18%

18%

21%

23%

26%

19%

13%

28%

49%

43%

41%

56%

10%

26%

26%

24%

16%

25%

18%

13%

18%

8%

18%

13%

5%

Customer-owned mobile device as POS

Cloud-based POS platform

A single commerce platform for store, mobile, and web (i.e, Unified Commerce)

Omni-channel integration

Mobile POS

Advanced CRM/loyalty

Mobile solutions for associates

Thin client solution

Store-level BI

Middleware Layer/SOA

Exhibit 2 Point of Sale Plans

Implemented Implement in < 2 years Implement in > 2 years

24%

34%

44%

44%

63%

Mobile point of sale

Customer-facing technology in the store

Real-time retail

Unified commerce platform

Payment security

Exhibit 1 Top Priorities

Mobile Technology – Transforming the Customer Experience | 4

greatly from retailer to retailer. In many cases, retailers are replacing some of their traditional “permanent” POS stations with mobile POS options through tablets or smartphones. Some are focusing on line-busting scenarios to reduce front-end traffic and improve customer throughput. Others seek to enhance the customer’s experience with personalized mobile client interactions. In these situations, mobile POS is definitely changing the way associates sell and the way customers shop. While retailers realize the importance of mobile POS and are working to install these capabilities, mobile POS was also reported as one of retailers’ biggest challenges, with 33% of survey respondents indicated that enabling mobile solutions was a top challenge for 2015. Some of the challenges noted by survey respondents planning to deploy mobile devices for POS are: • Choosing the right mobile technology in the

ever-changing landscape of vendors and considering the limited device support by some software vendors

• Process engineering to enable the use of a single device for multiple functions

• Updating back-end systems to support mobile point of sale capabilities

• Understanding the total cost of ownership including the impact of battery life and peripheral expenses

• Quantifying the benefits of capturing lost sales and increased customer satisfaction

While there are challenges to deploying mobile POS, it is becoming an imperative retail change that is being driving by customer expectations. Customer-facing Mobile Services meet Real-time Retail Customers have access to more information and tools than ever before and are accustomed to shopping online on a daily basis. Now they want that same digital experience in the store. Savvy retailers understand this and are leveraging customer-facing technology as part of the overall customer experience. Some areas where retailers are expanding their customer-facing mobile services include (Exhibit 3): • Geolocation – With geolocation

technology, customers shop with greater knowledge of their immediate

3%

5%

8%

16%

16%

19%

19%

24%

26%

3%

14%

24%

13%

22%

30%

22%

38%

29%

32%

54%

38%

48%

47%

46%

46%

41%

32%

37%

18%

Mobile wallet

Geolocating

Personalized recommendations

Mobile loyalty identification

Smartphone app

Prior purchase visibility

Shopping list/wish list

Product information (price, location, availability,

Mobile coupons, specials, promotions

Digital catalog

Exhibit 3 Customer-facing Mobile Services

Implemented and working well Implemented but needs improvement Implement within 3 years

Mobile Technology – Transforming the Customer Experience | 5

surroundings. Users can search within a given radius to find specific items, as well as connect directly with the retailer’s Website and online inventory. This technology can also be leveraged to improve the customer experience by offering real-time promotions and providing assistance locating a retailer’s store. Based on the POS/Customer Engagement Benchmarking Survey, 224% more retailers plan to use geolocating within three years.

• Personalized recommendations – Understanding the customer’s individual taste, shopping history, and even her friends’ opinions allows the retailer to offer her personalized promotions and shopping suggestions. This is the future of retail. 165% more retailers plan to offer personalized recommendations via customer-facing mobile technology within three years.

• Mobile loyalty identification –

Identification of a loyal customer via a mobile device is an easy way to identify when she walks in the store and offer her personalized services. 224% more retailers plan to implement mobile loyalty identification within three years.

Utilizing customer-facing technology is a natural outcome from the proliferation of mobile devices. As customers have become more comfortable and proficient with utilizing mobile technology and researching information on their own, retailers need to provide its associates the ability to access more information and services in the store to enhance the customer shopping experience and stimulate more sales. Mobile Payments are Hot! Mobile payment technology has returned to the news recently since Apple’s adoption of near field communications (NFC) technology into their proprietary Apple Pay app. With this addition to the latest iPhones, Apple has helped jump-start the mobile payment arena in the United States.

Mobile payments using NFC is a proven technology and has been widely accepted as a form of payment in parts of Asia for years. However, in the U.S. the mobile payment field is still quite muddy and there seem to be more questions than answers when it comes to identifying which mobile payment solutions will be the frontrunners in this growing arena. A recent study by Strategy Analytics’ predicts that NFC-enabled mobile handsets will account for $130B in worldwide payments by 2020.2 NFC technology and mobile payments appear to be here to stay and will continue to grow and influence the retail industry. However, one of the major inhibitors to adoption has been a very long change cycle in the payment area. Some progressive retailers have already invested in NFC technology when purchasing new payment terminals as part of their EMV upgrades. However, a large number have not and quite often the cost of upgrading an existing unit can be four times the cost of initially purchasing the units with the technology. Additionally, the time to implement and test changes such as NFC payments generally range between three to six months. Like most significant changes in retail, consumers will drive the shift to mobile payments. There are several mobile

2 Mobile Contactless Payments (2001-2020), Strategy Analytics, Publication Date: Dec 16 2014

3%

3%

5%

8%

13%

8%

8%

13%

15%

13%

30%

18%

5%

13%

13%

28%

35%

18%

31%

Bitcoin

CurrentC

Softcard

Google Wallet

Mobile payment in app

ApplePay

PayPal

Exhibit 4 Payment Types

Already accept

Plan to accept within 12 months Plan to accept within 1-3 years

Mobile Technology – Transforming the Customer Experience | 6

alternatives that will share a piece of the mobile payment space over the next few years, including PayPal, Google Wallet, Apple Pay and CurrentC. From these alternatives, there will be winners and losers, and perhaps new alternatives will emerge. While Apple Pay has the iconic name and many faithful followers, the number of retailers able to accept the NFC technology that drives Apple Pay has been limited by a scarcity of payment terminals that can accept contactless payment. According to our recent POS/Customer Engagement Benchmarking Survey, 10% of retailers support NFC payments today and an additional 35% of retailers plan to support NFC by October 2015 (which is a key deadline for EMV). This indicates a trend towards the implementation of payment terminals capable of accepting NFC payments. Survey respondents accept PayPal more than any other alternative payment type, with 13% already accepting it and more than 50% planning to accept it within three years (Exhibit 4). While only 8% of the respondents accept Apple Pay for payment today, an additional 48% plan to accept it within three years. There is the potential for Apple to do for mobile payments what it did for music with iTunes – make it a ubiquitous app. CurrentC, from the consortium of retailers known as

MCX, does not seem to have the same support, as only 21% plan to accept this payment type within three years. While the pros and cons of each of these payment types can be debated, many retailers are adopting a wait and see approach. There will be exponential growth in mobile payments in the U.S. over the next five years. Retailers are continuing to invest in the hardware required for mobile payments and the fact that consumers are faced with significant process changes with EMV that impact convenience and speed will both drive the advancement of mobile payments. There will likely still be more than one single mobile payment type. However, the few payment providers who master simplicity, convenience, security and simple integration for retailers will come out on top. Mobile Remains the Newest Frontier Mobile POS and customer engagement technology remain relatively immature from an adoption perspective, while traditional POS has had 40+ years to mature. The survey results make it clear that mobile technology and customer engagement are still early in

3%

5%

8%

16%

16%

19%

19%

24%

26%

3%

14%

24%

13%

22%

30%

22%

38%

29%

32%

54%

38%

48%

47%

46%

46%

41%

32%

37%

18%

Mobile wallet

Geolocating

Personalized recommendations

Mobile loyalty identification

Smartphone app

Prior purchase visibility

Shopping list/wish list

Product information (price, location, availability,

Mobile coupons, specials, promotions

Digital catalog

Exhibit 5 Customer-facing Mobile Services

Implemented and working well Implemented but needs improvement Implement within 3 years

Mobile Technology – Transforming the Customer Experience | 7

their evolution. This is evident in the results that show across categories the number of mobile services that have been implemented but still need improvement (Exhibit 5). There remain many areas where innovation and investment can improve the mobile arena. Conclusion There has been a huge technology shift in the past few years and mobile technologies in the hands of consumers and retail associates have been the driver. Mobile capabilities allow a retailer to break down the barrier between the online digital environment and the physical store. Mobile is driving retailers to upgrade and replace technology to keep ahead of their competitors’ customer experience offerings and to try to keep up with their very informed and technology-savvy customers. Some of the areas impacted include:

• Mobile devices as point of sale – utilizing

a mobile device as the checkout device

Nearly 300% more retailers plan to deploy mobile POS in the next two years

• Customer-facing mobile devices to offer personalized customer service – leveraging mobile devices to enhance the shopping experience

Approximately 200% more retailers plan to use geolocation within three years

• Mobile payments as alternative payment method – utilizing a customer’s smartphone as a payment device

350% more retailers plan to support NFC payments by October 2015

This area is clearly the new frontier that will transform retailers’ customer engagement model, operational budgets, in-store procedures and layouts. The one constant in the mobile space is that it continues to evolve rapidly and should be a significant part of a retailer’s strategy.

Mobile Technology – Transforming the Customer Experience | 8

About Boston Retail Partners

Boston Retail Partners (BRP) is an innovative and independent retail management consulting firm dedicated to providing superior service and enduring value to our clients. BRP combines its consultants' deep retail business knowledge and cross-functional capabilities to deliver superior design and implementation of strategy, technology, and process solutions. The firm's unique combination of industry focus, knowledge-based approach, and rapid, end-to-end solution deployment helps clients to achieve their business potential. BRP’s consulting services include:

Strategy Business Intelligence Business Process Optimization Point of Sale (POS) Mobile POS Store Systems and Operations CRM Unified Commerce Customer Experience & Engagement Order Management eCommerce Merchandise Management Supply Chain Information Technology Private Equity

For more information or assistance on any of the topics covered in this white paper, please contact:

To download the 2015 POS/Customer Engagement Benchmarking Survey please go to: www.bostonretailpartners.com/resources/2015-poscustomer-engagement-benchmarking-survey/ Boston Retail Partners Headquarters Independence Wharf, 470 Atlantic Ave., 4th Floor, Boston, MA 02210 www.bostonretailpartners.com

©2015 Boston Retail Partners. All rights reserved No part of this publication may be reproduced or transmitted in any form or for any purpose without the expressed permission of Boston Retail Partners. The information contained herein may be changed without prior notice.

Brian Brunk, Principal (405) 590-0542 [email protected] Ken Morris, Principal (617) 880-9355 [email protected] Walter Deacon, Principal (781) 337-2060 [email protected]

Perry Kramer, Vice President and Practice Lead (617) 899-7543 [email protected] Kathleen Fischer, Marketing Manager (330) 289-3342 [email protected] David Naumann, Director of Marketing (916) 673-7757 [email protected]