©2015, college for financial planning, all rights reserved. session 9 iras–traditional deductions...

TRANSCRIPT

©2015, College for Financial Planning, all rights reserved.

Session 9IRAs–Traditional Deductions and Roth Contributions

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits

Session Details

Module 5

Chapter(s)

1, 3

LOs 5-2 Describe the basic characteristics of traditional IRAs, and analyze a situation to calculate the amount of an IRA contribution that is deductible.

5-4 Describe the basic characteristics of Roth IRAs, and analyze a situation to calculate the eligible contribution amount.

9-2

IRA Statutory Requirements

• Eligibility: Compensation (earned income, alimony) and must be under age 70½ (no age limit on Roth IRAs)

• Contribution limit: 100% of earned income up to $5,500 (spousal IRAs allowed), $1,000 age 50 catch-up

• Contribution deadline: April 15—no extensions

• Taxation: Earnings are tax-deferred

• Minimum: If an amount greater than $0, but less than $200 is deductible, then a $200 minimum deductible contribution is allowed

9-3

IRA Statutory Requirements

• Fully vested • No life insurance or collectibles• No loans• RMDs starting at age 70½

(not for Roth IRAs)• 6% penalty tax on excess

contributions

9-4

IRA Deductibility Active Participant Status

An employee is an active participant in a defined contribution plan if, during the taxable year, the employee received any annual additions to his/her account.

An employee is an active participant in a defined benefit plan if the employee is eligible to participate in the plan and has not opted out. (Note that investment earnings do not affect active participant status.)

or orEmployer

ContributionEmployee Contribution

(either voluntary or mandatory)Forfeiture

To one of the following plans:• All qualified plans• Tax-sheltered annuity (TSA) under §403(b)• Simplified employee pension (SEP) & SIMPLE plans• Government pension plan

9-5

Traditional IRA Deduction Phaseout Amounts (2015)

Single Taxpayer

Not an Active Participant

Active Participant

No Phaseout

$61,000-$71,000

Married Taxpayers Filing JointlyNeither is an

Active Participant

One Active Participant

Both Active Participants

No Phaseout

Active participant:

$98,000-$118,000

$98,000-$118,000

Other Spouse:

$183,000-$193,000

9-6

Calculation of Deductible IRA Contribution

1.Determine the deductible percentage

2.Multiply by the maximum contribution amount

3.The result is the maximum dollar amount that can be deducted (rounded up to the next $10)

Example: Single, Modified AGI $66,000

$71,000 $66,000.5 $5,500 $2,750

$10,000

9-7

Calculation of Deductible IRA Contribution (1)

1.Determine the deductible percentage

2.Multiply by the maximum contribution amount

3.The result is the maximum dollar amount that can be deducted (rounded up to the next $10)

Example: Married/Joint active participant, Modified AGI of $98,316

$118,000 $98,316.9842 $5,500 $5,413.10

$20,000

$5,413.10 rounded up to nearest $10 $5,420.00

9-8

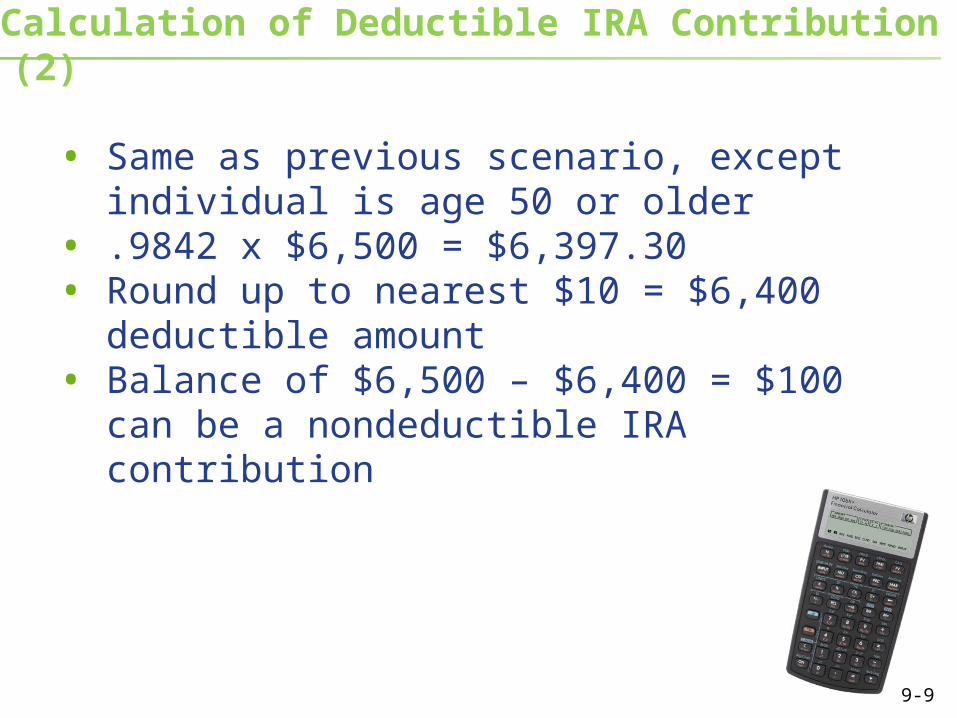

Calculation of Deductible IRA Contribution (2)

• Same as previous scenario, except individual is age 50 or older

• .9842 x $6,500 = $6,397.30• Round up to nearest $10 = $6,400

deductible amount • Balance of $6,500 – $6,400 = $100

can be a nondeductible IRA contribution

9-9

Roth IRA Contribution 2015 Phaseouts

Filing Status Phaseout*

Single $116,000–$131,000

Married, filing jointly $183,000–$193,000* Without regard to “active participant” status

9-10

Question 1

Allen Baker, a single 40-year-old taxpayer with an AGI of $69,800, is covered by his employer’s profit sharing/401(k) plan. During the plan year, no employer contribution was made and Allen did not make any salary reduction contributions to the 401(k) portion of the plan. Allen’s account balance increased by $120; this was attributable to investment earnings of $80 and forfeitures of $40. If he contributes $5,500 to his IRA, what is the amount of his allowable IRA deduction?a. $0b. $200c. $660d. $5,500 9-11

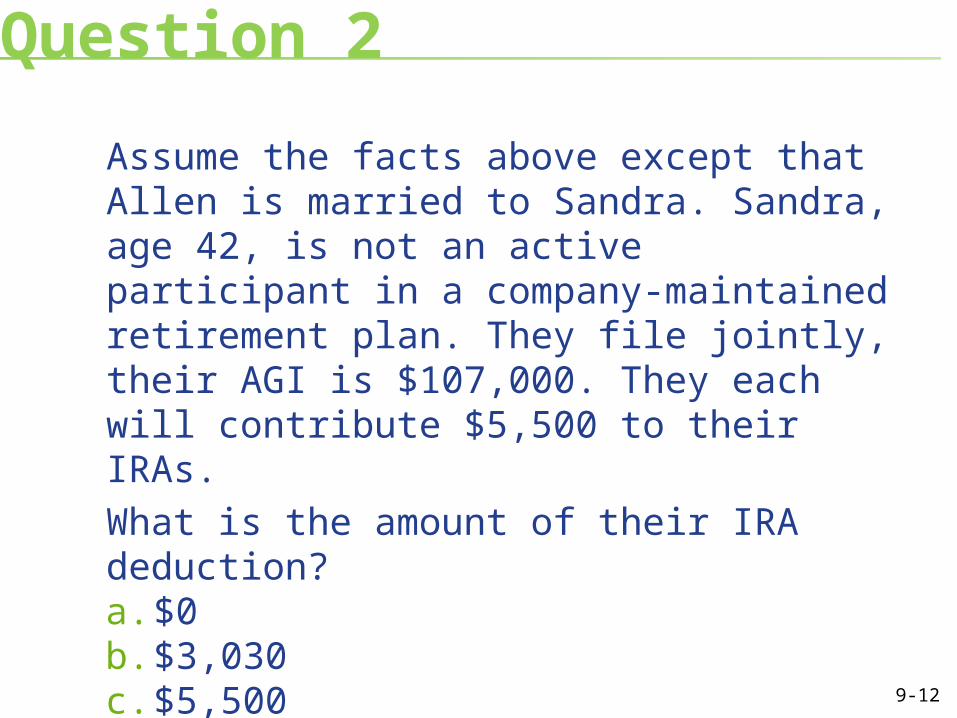

Question 2

Assume the facts above except that Allen is married to Sandra. Sandra, age 42, is not an active participant in a company-maintained retirement plan. They file jointly, their AGI is $107,000. They each will contribute $5,500 to their IRAs.What is the amount of their IRA deduction?a. $0b. $3,030c. $5,500d. $8,530e. $11,000 9-12

Question 3

Ken and Barbie file jointly. Both work, and their combined AGI is $106,000. This year, Ken’s profit sharing account earned over $5,000, but the company made no contributions and there were no forfeitures. Barbie declined to participate in her company’s defined benefit plan in July because she wants to contribute to and manage her own retirement money. (Her benefit at age 65 under the plan was $240 per month.)

How much of their $11,000 contribution can they deduct?a. $0b. $5,500c. $8,800d. $11,000

9-13

Question 4

Lucy received a $1,200 profit sharing contribution this year. Lucy and George are married, filing jointly. George is an artist who had no earnings this year. Their combined AGI for this year is $109,000. How much of their $11,000 IRA contribution can they deduct?a. $0b. $5,500c. $7,980d. $11,000

9-14

Question 5

Sally and Joe are married, filing jointly. Their combined AGI is $146,000. They are both active participants in their employers’ plans. After making the maximum qualified plan contributions, they wish to make contributions to their Roth IRAs. How much can they contribute to their Roth IRAs?a. $0b. $1,000c. $5,500d. $11,000 9-15

Question 6

Jerry’s AGI totals $121,000 this year. He is single. What is the maximum amount he can contribute to his Roth IRA this year?a. $0b. $1,000c. $3,670d. $5,500

9-16

©2015, College for Financial Planning, all rights reserved.

Session 9End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits