20150410.c&w.rtailin poland ekli

TRANSCRIPT

12-15 NİSAN2015VARŞOVA-KRAKOV

RETAIL IN POLAND

APRIL 2015

1

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

CONTENT

MACRO-ECONOMIC REVIEW

RETAIL MARKET STRUCTURE

KEY SHOPPING CENTRES

HIGH STREETS

PRIME RENTS

RETAIL MARKET TRENDS

POLAND MARKET ENTRY GUIDE

MACRO-ECONOMIC REVIEWECONOMY AND POLITICAL BACKGROUND

DEMOGRAPHIC OVERVIEW

SPENDING

3

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

ECONOMY & POLITICAL BACKGROUND

Poland• Located in central Europe, provides a strategic link between western and eastern Europe

plus connection to Scandinavia and other Baltic states via the Baltic sea to the north

• The largest of central European countries (38.5 million inhabitants)

• The only EU nation to escape recession in 2009

• Key target for international retail companies because of its investment-friendly businessclimate and growth prospects

• Reputation of a star performer in economic terms within the EU

• Youthful age profile of the consumer market (some 35% of the population is aged under30 years old)

• A number of sectors are dominated by foreign retailers, notably food, DIY and furniture

• While the retail market is well developed, it remains fragmented overall, with a largenumber of shops

4

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

ECONOMY & POLITICAL BACKGROUND

Source: Oxford Economics Ltd., Consensus Economics Inc, World Bank and Credit Suisse

• Population: 38.5 million• GDP US$: 535.3 bilion• Public sector balance: -4.0% of GDP • Public sector debt: 55.7% of GDP• Current account balance: -1.3% of GDP• Parliament: Coalition of the Civic Platform

Party and the smaller Polish People's Party

• President: Bronisław Komorowski• Prime Minister: Ewa Kopacz• Election dates: Mid-2015 (Presidential)

Late 2015 (Parliamentary)

5

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

ECONOMIC INDICATORS* 2011 2012 2013 2014 2015F

GDP growth 4.5 2.1 1.6 3.2 3.4

Consumer spending 2.7 1.1 0.8 2.5 3.1

Industrial production 7.1 1.4 2.4 4.2 5.3

Investment 8.2 -1.7 -0.1 8.2 5.1Unemployment rate (%) 12.4 12.8 13.5 12.5 11.9

Inflation 4.2 3.7 1.2 0.3 1.5

PLZ/€ (average) 4.12 4.19 4.20 4.18 4.13

PLZ/US$ (average) 2.96 3.26 3.16 3.14 3.34Interest rates: 3-month (%) 4.3 4.7 2.8 2.4 2.3Interest rates 10-year (%) 6.0 5.0 4.0 3.6 3.2

NOTE: *annual % growth rate unless otherwise indicated. E estimate F forecastSource: Oxford Economics Ltd. and Consensus Economics Inc

ECONOMY & POLITICAL BACKGROUND

6

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

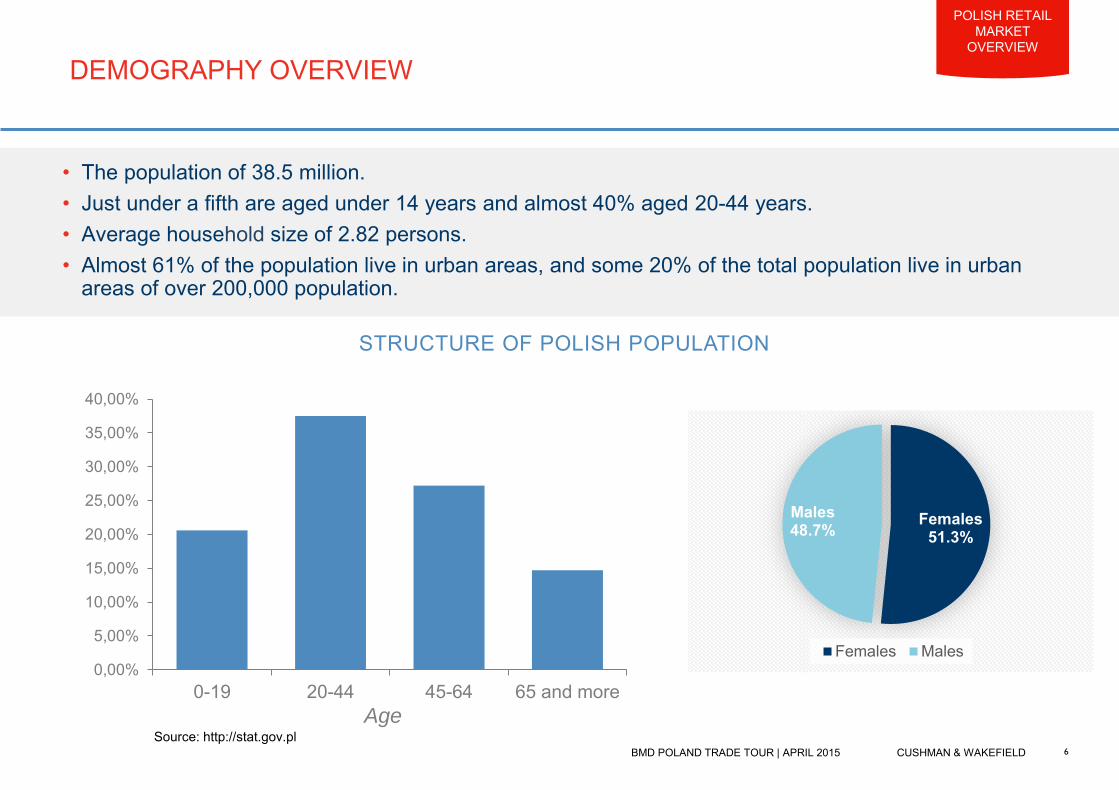

STRUCTURE OF POLISH POPULATION

DEMOGRAPHY OVERVIEW

• The population of 38.5 million.• Just under a fifth are aged under 14 years and almost 40% aged 20-44 years.• Average household size of 2.82 persons.• Almost 61% of the population live in urban areas, and some 20% of the total population live in urban

areas of over 200,000 population.

Source: http://stat.gov.pl

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

0-19 20-44 45-64 65 and more

Females51.3%

Males 48.7%

Females Males

Age

7

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

SPENDING

Source: http://stat.gov.pl

AVERAGE MONTHLY EXPENDITURE PER CAPITA IN HOUSEHOLDS COMPARED WITH THE NATIONAL AVERAGE (POLAND=100)

130.1%

110.4%

101.5%

99.8%

96.9%

96.7%

96.7%

95.3%

94.5%

92.9%

92.3%

90%

88.8%

85.4%

85.1%

76.8%

dolnośląskie

kujawsko-pomorskie

lubelskie

lubuskie

łódzkie

małopolskie

mazowieckie

opolskie

podkarpackie

podlaskie

pomorskie

śląskieświętokrzyskie

warmińsko-mazurskie

wielkopolskie

zachodniopomorskieVoivodships with average monthlyexpenditure exceeding 110.0% of the national average.

Voivodships with average monthlyexpenditure between 100.0% and 109.9% of the national average.

Voivodships with average monthlyexpenditure between 90.0 and 99.9% of the national average.

Voivodships with average monthlyexpenditure less than 90.0% of the national average.

8

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

DISTRIBUTION OF ANNUAL HOUSEHOLDSPEND BY CATEGORY

1% 2% 3% 3%4%5%

5%

5%

5%

6%7%

10%

21%

25%

Education Pocket moneyAlcoholic beverages and tobacco Restaurants & HotelsOther Expenditures Furnishings, household equipmentClothing & footwear CommunicationHealth Misc. Goods & ServicesRecreation & culture TransportHousing Food & Non-alcoholic beverages

SPENDING

SPENDING PATTERNS

The largest spendingcategories are:

• food & non-alcoholic beverages (24.9%)

• housing and utilities (20.8%),

• transport (9.6%)

Source: http://stat.gov.pl

RETAIL MARKET STRUCTURE

10

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

RETAIL MARKET STRUCTURE

LARGEST POLISH AGGLOMERATIONS

NAME POPULATIONPURCHASING POWER IN EUR PER PERSON

WarsawAgglomeration 2,521,182 9,708

Katowice Conurbation 2,187,122 6,326

Kraków Agglomeration 1,025,039 6,715

Trójmiasto Agglomeration 1,022,059 7,096

Łódź Agglomeration 992,373 6,478

PoznańAgglomeration 815,836 7,074

Wrocław Agglomeration 778,838 7,608

SzczecinAgglomeration 556,737 6,887

POLAND TOTAL 38,495,659 6,170

• The retail market is fragmented, witha large percentage of independentretailers operating around the country,particularly in small towns and rural areas.

• However, the market is undergoingconsolidation, with the major internationalhypermarket/supermarket operators nowexpanding into smaller towns and cities.

• Shopping centres account for the largestshare of existing retail stock.

• A number of sectors are dominated byforeign retailers, notably food, DIY andfurniture.

• The consumer market is attractivebecause of its young age profile.

• Top retail destinations in Poland continueto be found in eight main cities: Warsaw,Kraków, Łódź, Wrocław, Poznań,Katowice, Tricity and Szczecin (26% of thePolish population live in eight biggestPolish conurbations).

• Warsaw is the first port of call, followed byother major cities.

KEY SHOPPING CENTRES

12

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

KEY 15 SHOPPING CENTRES IN POLAND

WARSZAWA

ArkadiaZłote TarasyGaleria Mokotów

KRAKÓW

Galeria Krakowska Bonarka

KATOWICE

Galeria KatowickaSilesia City Center

WROCŁAW

Magnolia ParkGaleria Dominikańska

POZNAŃ

Stary Browar

Galeria BałtyckaRiviera

TRÓJMIASTO

SZCZECIN

Galeria Kaskada

ŁÓDŹGaleria ŁódzkaManufaktura

NAME GLA FOOTFALL(mln per annum)

Arkadia 103,000 19.9Złote Tarasy 63,500 18.5Galeria Mokotów 67,500 12.5

Galeria Krakowska 57,700 36.5

Bonarka City Center 91,000 12.0

Galeria Katowicka 48,000 13.0

Silesia City Center 84,000 14.4

Stary Browar 47,500 10.8Magnolia Park 100,000 10.0Galeria Dominikańska 24,300 12.0

Galeria Bałtycka 46,400 10.6Riviera 70,500 7.2Manufaktura 110,000 15.0Galeria Łódzka 45,000 8.0Galeria Kaskada 43,000 9.1

13

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

KEY SHOPPING CENTRES: ARKADIA, WARSAW

Developer: ERE GroupOwner: Unibail RodamcoOpening Date: 2004Address: Al. Jana Pawła II 82GLA: 103,000 sq mNumber of stores: 254Number of retail levels: 2Parking: 4,300 free; 300 paidOccupancy: 100%Anchor tenants: Carrefour, Leroy Merlin, C&A, Saturn Cinema City, H&M, Marks & Spencer,Royal Collection.Number of visitors: 19.9 million per year

0.4%

0.4% 1.6%1.6%2.0% 2.4%

2.4%

3.6%3.6%

4.0%

7.1%

9.1%

9.5%10.7%

11.5%

30.1%

DIY Hyper/supermarket Entertainment & Leisure

Sport equipment Multimedia Electronic equipment

Home Accessories Children & Maternity Other

Food speciality Health & Beauty Accessories & Jewellery

Services Leather, Bags & Shoes Food court, restaurants

Fashion - mixed

TENANTS CATEGORY SPLIT IN ARKADIA

14

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

0.5% 2.0%

0.5% 2.0%2.0% 2.0%

1.0%4.0%

2.0%

8.1%

8.1%

6.1%

11.1%18.2%

32.4%

DIY Hyper/supermarket Entertainment & Leisure

Sport equipment Multimedia Electronic equipment

Home Accessories Children & Maternity Other

Food speciality Health & Beauty Accessories & Jewellery

Services Leather, Bags & Shoes Food court, restaurants

Fashion - mixed

KEY SHOPPING CENTRES: ZŁOTE TARASY, WARSAW

Developer: ING REIM/Unibail RodamcoOwner: Unibail Rodamco/CBRE GI/AxaOpening Date: 2007Address: Ul. Złota 59GLA: 63,500 sq mNumber of stores: 199Number of retail levels: 5Parking: 1,700 paidOccupancy: 100%Anchor tenants: Carrefour Express, Saturn, Intersport, Foot Locker, Marks & Spencer, Zara, H&M, MultikinoNumber of visitors: 18.5 per year

TENANTS CATEGORY SPLIT

15

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

0.4%

0.8%0.4% 1.5%

1.9% 3.4%2.7%

3.4%2.3%

6.5%

6.9%

6.9%

11.5%14.2%

37.2%

DIY Hyper/supermarket Entertainment & Leisure

Sport equipment Multimedia Electronic equipment

Home Accessories Children & Maternity Other

Food speciality Health & Beauty Accessories & Jewellery

Services Leather, Bags & Shoes Food court, restaurants

Fashion - mixed

KEY SHOPPING CENTRES: GALERIA MOKOTÓW, WARSAW

Developer: GTCOwner: Unibail RodamcoOpening Date: 2000Address: Ul. Wołoska 12 GLA: 67,500 sq mNumber of stores: 261Number of retail levels: 3Parking: 2,500Occupancy:100%Anchor tenants: Carrefour, Zara, KappAhl, Empik, Smyk, Euro RTV AGD, Peek & Cloppenburg, Go Sport, Cinema CityNumber of visitors: 12.5 milion per year

TENANTS CATEGORY SPLIT

16

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

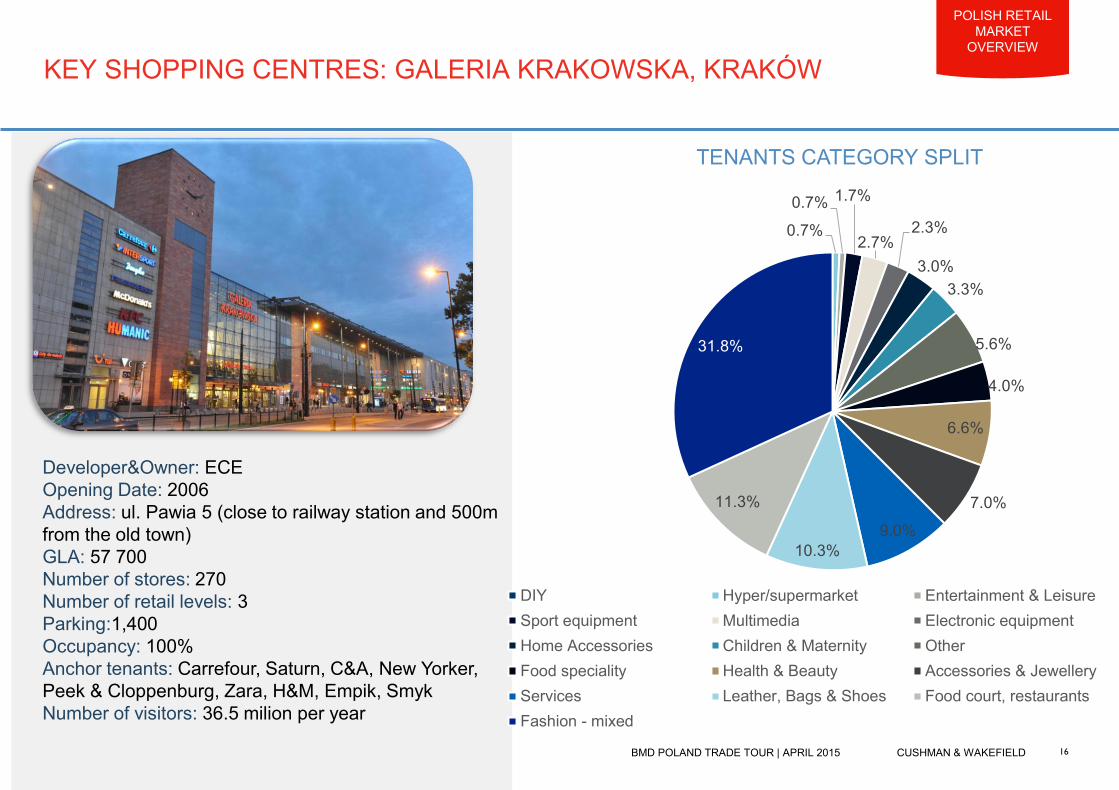

KEY SHOPPING CENTRES: GALERIA KRAKOWSKA, KRAKÓW

Developer&Owner: ECEOpening Date: 2006Address: ul. Pawia 5 (close to railway station and 500m from the old town)GLA: 57 700Number of stores: 270Number of retail levels: 3Parking:1,400Occupancy: 100%Anchor tenants: Carrefour, Saturn, C&A, New Yorker, Peek & Cloppenburg, Zara, H&M, Empik, SmykNumber of visitors: 36.5 milion per year

TENANTS CATEGORY SPLIT

0.7%

0.7% 1.7%

2.7%2.3%

3.0%3.3%

5.6%

4.0%

6.6%

7.0%

9.0%10.3%

11.3%

31.8%

DIY Hyper/supermarket Entertainment & LeisureSport equipment Multimedia Electronic equipmentHome Accessories Children & Maternity OtherFood speciality Health & Beauty Accessories & JewelleryServices Leather, Bags & Shoes Food court, restaurantsFashion - mixed

17

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

KEY SHOPPING CENTRES: BONARKA CITY CENTER, KRAKÓW

Developer: TriGranit&ImmoestOwner: Trigranit DevelopmentOpening Date: 2009Address: ul. Pawia 5 (close to railway station and 500 m from the old town)GLA: 91,000Number of stores: 251Number of retail levels: 2Parking: 3,200Occupancy: 96%Anchor tenants: Auchan hypermarket, Leroy Merlin, 20-screen Cinema City, TK Maxx, H&MNumber of visitors: 12

TENANTS CATEGORY SPLIT

0.4%

0.4% 1.3% 1.3%1.3%3.5%

4.4%3.1%2.7%

3.1%

8.4%

8.0%10.2%

10.2%

9.3%

32.0%

DIY Hyper/supermarket Entertainment & LeisureSport equipment Multimedia Electronic equipmentHome Accessories Children & Maternity OtherFood speciality Health & Beauty Accessories & JewelleryServices Leather, Bags & Shoes Food court, restaurantsFashion - mixed

18

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

HIGH STREETS

• High street stores’ total floorspacetypically equals that of a medium-sized shopping centre.

• Demand for high street space comes mainly from restaurants, cafes, fashion retailers, services and daily shopping stores.

• Due to low availability of units in top high street destinations, rents have remained at high levels of EUR 75-90/sq m/month.

• Tenants tend to be mainly local retailers and businesses, with occasional more renowned anchortenant.

• The best high streets are in Kraków and Warsaw.

Source: Cushman & Wakefield Valuation & Advisory, February 2015

0,05,010,015,020,025,030,035,040,045,0

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Warszawa Łódź Poznań Szczecin

EU

R/s

q m

/mon

th

Estimated supply GLA

Average rent (commercial units independently owned)

ESTIMATED SUPPLY AND AVERAGE RENTS IN HIGH STREETS

Sq.

m.

19

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

PRIME RENTS

Source: Cushman & Wakefield Valuation & Advisory, February 2015

0 50 100 150

Other cities

Łódź

Wrocław

Trójmiasto

Szczecin

Poznań

Kraków

Katowice

Warszawa

high streets shopping centres

EUR/sq m/month

• The highest rents are commandedin Warsaw’s prime shopping centres at EUR 100-140/sqm/month for a fashion store sized between 100 sq m and 150 sq m.

• Rents average EUR 35-45/sqm/month in the other seven conurbations and EUR 20-25/sqm/month in small and medium-sized cities.

PRIME RENTS IN SHOPPING CENTRES AND HIGH STREETS

20

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

46 SHOPSSIZE: 2,000 sq m

TOP FASHION RETAILERS IN POLAND

97 SHOPSSIZE: 500 sq m

147 SHOPSSIZE: 2,500 sq m

21 SHOPSSIZE: 1,400 sq m

99 SHOPSSIZE: 800 –1,200 sq m

27 SHOPSSIZE: 2,500 sq m

145 SHOPSSIZE: 500 sq m

51 SHOPSSIZE: 500 sq m

73 SHOPSSIZE: 500 sq m

33 SHOPSSIZE: 500 sq m

15 SHOPSSIZE: 500 sq m

150 SHOPSSIZE: 1,500 – 2,000 sq m

120 SHOPSSIZE: 500 sq m

145 SHOPSSIZE: 500 sq m

23 SHOPSSIZE: 500 sq m

80 SHOPSSIZE: 1,400 sq m

21

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

TOP HOME&DECOR RETAILERS

40 SHOPSSIZE: 200 SQ M

15 SHOPSSIZE: 300 SQ M

101 SHOPSSIZE: 500 SQ M

3 SHOPSSIZE: 500 SQ M

35 SHOPSSIZE: 200 SQ M

9 SHOPSSIZE: 300 SQ M

22

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

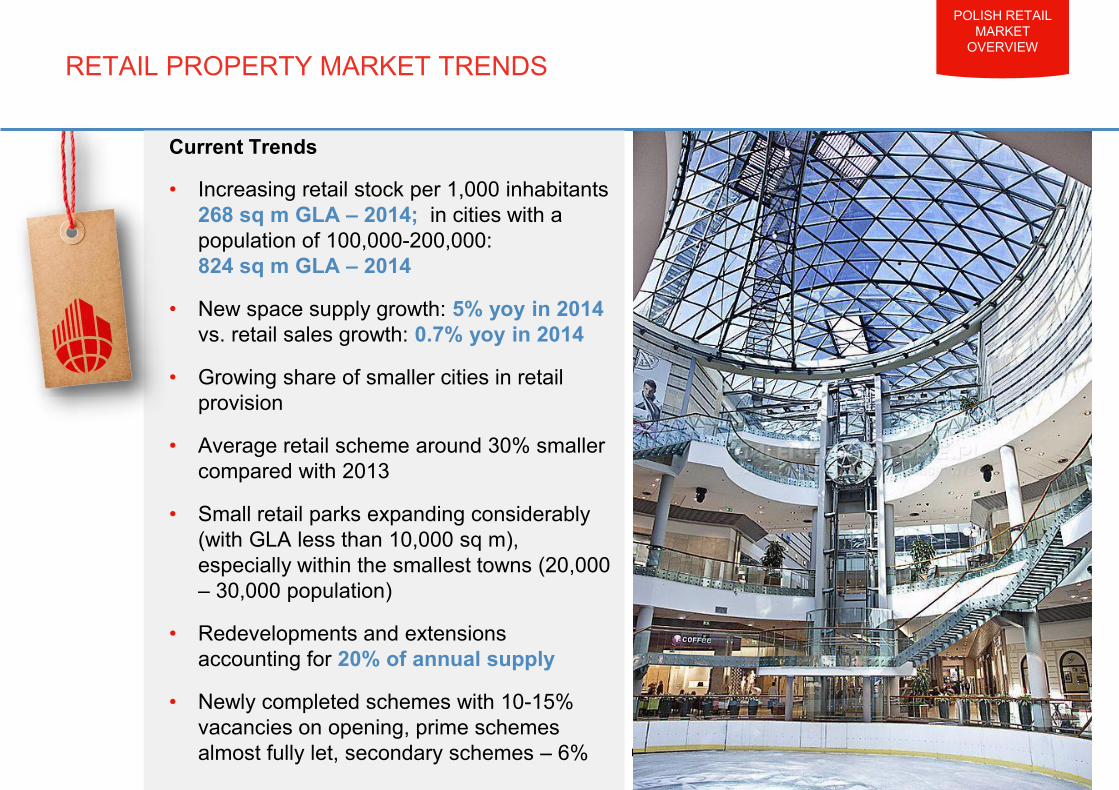

Current Trends

• Increasing retail stock per 1,000 inhabitants268 sq m GLA – 2014; in cities with a population of 100,000-200,000: 824 sq m GLA – 2014

• New space supply growth: 5% yoy in 2014vs. retail sales growth: 0.7% yoy in 2014

• Growing share of smaller cities in retailprovision

• Average retail scheme around 30% smaller compared with 2013

• Small retail parks expanding considerably(with GLA less than 10,000 sq m), especially within the smallest towns (20,000– 30,000 population)

• Redevelopments and extensionsaccounting for 20% of annual supply

• Newly completed schemes with 10-15% vacancies on opening, prime schemes almost fully let, secondary schemes – 6%

RETAIL PROPERTY MARKET TRENDS

23

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

POLAND MARKET ENTRY GUIDE

A business needs to be registered in the Register of Business Entities at the National Court Registry (KRS) or in the Register of Commercial Activity. An incorporated company, i.e. a limited company and a joint-stock company, may start its operationbefore registering.

There are five steps to commence business in Poland.

• Apply for entry in the register of trade (normally a small fee)• Classify business and receive a written confirmation of trade organisation • Apply for a REGON number at the Central Statistical Office (GUS) in Poland • Register at the Social Insurance Institution (ZUS)• Apply for a tax identification number (NIP) at the tax office

European Economic Area (EEA) nationals may set up a variety of types of business under the same rules as Polish entrepreneurs/companies.

Further Information: http://www.paiz.gov.pl/en

24

POLISH RETAIL MARKET

OVERVIEW

BMD POLAND TRADE TOUR | APRIL 2015 CUSHMAN & WAKEFIELD

ENTRY TO THE POLISH MARKET

Nationals from outside EEA have the right, unless international agreements state otherwise, to undertake and run business activity in the following forms:

• Limited partnership• Limited joint-stock partnership• Limited liability company • Joint-stock company

Business activity in Poland is governed by the Economic Freedom Act, which controls everything relating to setting up and running businesses in Poland.

The Act has helped to provide a more business friendly environment.

Also some regulations and support for businesses in Poland with the Commercial Companies Code of September 2000, which brought Poland in line with EU law and regulations.

Further Information: http://www.paiz.gov.pl/en

www.cushmanwakefield.pl

CONTACT DETAILS:

MAREK NOETZELPartner, Head of Retail DepartmentTel: +48 (0) 22 820 20 20Mob: +48 (0) 605 32 46 32Fax: +48 (0) 22 820 20 21

E-mail: [email protected]

NASZE PORTFOLIODZIAŁ POWIERZCHNI HANDLOWYCH

OUR PORTFOLIORETAIL SERVICES

CUSHMAN & WAKEFIELD 1

PORTFOLIO

• Zespół ds. nieruchomości handlowych świadczy usługi na rzecz inwestorów, najemców i wynajmujących nieruchomości handlowo-

rozrywkowe w kraju i za granicą.

• Oferujemy kompleksowe usługi dla handlowców zainteresowanych rozwojem działalności na całym świecie – od wejścia na nowy rynek i

strategię wyboru lokalizacji po pośrednictwo w innych krajach. Dzięki dogłębnej znajomości rynków nieruchomości handlowych oraz

globalnej perspektywie nasi pracownicy pomagają firmom osiągać cele biznesowe związane z centrami i parkami handlowymi, sklepami

przy głównych ulicach handlowych i centrami wyprzedażowymi.

• Our Retail Team provides services for retail and leisure occupiers, landlords and investors, and markets retail properties on a local and

global basis.

• We are a one-stop-shop for retailers looking to grow their business internationally, from new market entry and location strategy to

international agency. From shopping centres and retail parks, to high streets and factory outlets, our retail and leisure specialists

leverage their vast industry knowledge and global perspective to meet your goals.

NASZE USŁUGI / RETAIL AGENCY SERVICES

Marek Noetzel

Partner,

Head of Retail / Dyrektor Działu

Powierzchni Handlowych

CUSHMAN & WAKEFIELD 2

PORTFOLIO

PARTNER /

HEAD OF RETAIL

MAREK NOETZEL

SENIOR NEGOTIATOR

DARIA KOTARSKA

SENIOR NEGOTIATOR

ANNA HOFMAN

SENIOR NEGOTIATOR

JUSTYNA BARTOSZ

ASSOCIATE /

SENIOR NEGOTIATOR

MAGDALENA GNIAZDOWSKA

NEGOTIATOR

KATARZYNA JABŁOŃSKA-

MIEDZIK

ASSOCIATE /

SENIOR NEGOTIATOR

SZYMON ŁUKASIK

NOWE CENTRA HANDLOWE

NEW SHOPPING CENTRES

ISTNIEJĄCE CENTRA HANDLOWE

EXISTING SHOPPING CENTRES

REPREZENTACJA NAJEMCY

TENANT REPRESENTATION

PARKI HANDLOWE / SPRZEDAŻ DZIAŁEK

RETAIL PARKS / SITES DISPOSALS

NEGOTIATOR

AGNIESZKA ŁUKASZUK -

CZERNAJ

ASSOCIATE /

SENIOR NEGOTIATOR

TOMASZ GÓRSKI

NEGOTIATOR

TOMASZ LIPIŃSKI

CONSULTANCY

SENIOR CONSULTANT

MAGDALENA SADAL

TEAM ASSISTANT & MARKETING

ASSISTANT

MAŁGORZATA

GRZYWACZEWSKA

USŁUGI DZIAŁU POWIERZCHNI HANDLOWYCH

RETAIL AGENCY SERVICES

CUSHMAN & WAKEFIELD 3

PORTFOLIONOWE CENTRA

HANDLOWE

NEW SHOPPING

CENTERS

CUSHMAN & WAKEFIELD 4

PORTFOLIO

FORUM GDAŃSK, GDAŃSK

• Deweloper / Developer: Multi Development

• Otwarcie / Opening: Q1 2017

• GLA: 62,000 m2

• Miejsca parkingowe /

Parking places: 1 200

• Kontakt / Contact:

• Opis projektu:

Forum Radunia zlokalizowana w centrum Gdańska ma szansę

zostać jednym z głównych obiektów handlowo-rozrywkowych

w regionie.

• Project description:

Strategically located in the heart of Gdansk, near its historical

centre, Forum Radunia is set to become the prime retail and

leisure destination in the region.

• Główni najemcy / Anchor Tenants:

CUSHMAN & WAKEFIELD 5

PORTFOLIO

GALERIA KABATY, WARSZAWA

• Deweloper / Developer: Tesco

• Otwarcie / Opening: 2017

• GLA: 43,000 m2

• Miejsca parkingowe /

Parking places: 2,000

• Kontakt / Contact:

• Opis projektu:

Korzystne położenie w dzielnicy Ursynów, kreatywne

rozwiązania architektoniczne oraz funkcjonalny układ galerii to

charakterystyka Galerii Kabaty, która ma powstać w

południowej części Warszawy.

• Project description:

Favourable location in the Ursynów district, creative

architectural solutions and functional layout will help create a

new and exciting shopping environment in the southern part of

the city.

CUSHMAN & WAKEFIELD 6

PORTFOLIO

IKEA BIELANY, WROCŁAW

• Deweloper / Developer: Inter IKEA

• Otwarcie / Opening: November 2015

• GLA: 145,000 m2

• Miejsca parkingowe /

Parking places: 4,700

• Kontakt / Contact:

• Opis projektu:

Remont i rozbudowa Parku Handlowego Bielany spowoduje

powiększenie centrum do 145.000 m kw, co pozwali pomieścić

około 200 sklepów.

• Project description:

The refurbishment and extension of Park Handlowy Bielany will

almost double the size of the centre to 145,000 sq m, allowing

it to accommodate about 200 shops compared to some 80 at

the moment.

• Główni najemcy / Anchor Tenants:

CUSHMAN & WAKEFIELD 7

PORTFOLIO

FORUM BEMOWO, WARSZAWA

• Deweloper / Developer: Phoenix Development

• Otwarcie / Opening: 2016/2017

• GLA: 22,000 m2

• Miejsca parkingowe /

Parking places: 536

• Kontakt / Contact

• Opis projektu:

Forum Bemowo to centrum handlowe zlokalizowane na

warszawskim Bemowie z doskonałym dostępem do centrum

miasta.

• Project description:

Forum Bemowo is ideally located fronting the district’s main

arterial road with excellent access to public transport.

• Główni najemcy / Anchor tenants:

CUSHMAN & WAKEFIELD 8

PORTFOLIO

GALERIA NEPTUN, STAROGARD GDAŃSKI

• Deweloper / Developer: Galeria Neptun Sp. z o.o.

• Otwarcie / Opening: 25 April 2015

• GLA: 25,000 m2

• Miejsca parkingowe /

Parking places: 500

• Kontakt / Contact:

• Opis projektu:

Galeria Neptun będzie pierwszym nowoczesnym centrum

handlowym w Starogardzie Gdańskim. W obiekcie tym będzie

również kino.

• Project description:

Galeria Neptun will be the first modern retail scheme with a

multiplex offer in Starogard Gdański.

• Główni najemcy / Anchor tenants:

CUSHMAN & WAKEFIELD 9

PORTFOLIO

MARCREDO CENTER, ZAWIERCIE

• Developer / Developer: elbfonds Development

• Otwarcie / Opening: 2016

• GLA: 20,000 m2

• Miejsca parkingowe /

Parking places: 600

• Kontakt / Contact:

• Opis projektu:

Marcredo Center to centrum handlowe, które powstanie na

skrzyżowaniu ul. Wojaska Polskiego z obwdnicą Zawiercia.

• Project description:

Marcredo Center is located at the junction of Wojska

Polskiego with ring road of Zawiercie with very good visibility.

• Główni najemcy / Anchor tenants:

CUSHMAN & WAKEFIELD 10

PORTFOLIO

MARCREDO CENTER, KOŁOBREZG

• Deweloper / Developer: elbfonds Development

• Otwarcie / Opening: 2017

• GLA: 15,600 m2

• Miejsca parkingowe /

Parking places: 600

• Kontakt / Contact:

• Opis projektu:

Marcedo Center będzie pierwszym nowoczesnym obiektem

handlowym w Kołobrzegu.

• Project description:

Marcredo Center will be the first modern retail scheme in

Kołobrzeg.

CUSHMAN & WAKEFIELD 11

PORTFOLIO

EXISTING SHOPPING

CENTERS

ISTNIEJĄCE CENTRA

HANDLOWE

CUSHMAN & WAKEFIELD 12

PORTFOLIO

GALERIA KATOWICKA, KATOWICE

• Opis projektu:

Galeria Katowicka łączy w sobie funkcje galerii handlowej,

dworca kolejowego oraz autobusowego. Znajdziemy w niej

ponad 200 sklepów zlokalizowanych na 5 kondygnacjach, a

wśród nich restauracje, usługi, znane marki odzieżowe oraz

kino.

• Project description:

Neinver develops a complex which mixed functions of a railway

station, bus station, retail, business, service and culture use. In

front of the station building is a commercial zone – a five-level

complex mixing retail and service functions with an office part

on the west side and a separate office building near Młyńska St.

Over 200 shopping, service and food – court units located on

two floors, the best polish and international brands and cinema.

• Główni najemcy / Anchor tenants:

» Deweloper / Developer: Neinver Polska

» Otwarcie / Opening: 2013

» GLA: 53 000 m2

» Miejsce parkingowe /

Parking places: 1 100

» Kontakt / Contact:

CUSHMAN & WAKEFIELD 13

PORTFOLIO

ARKADY WROCŁAWSKIE, WROCŁAW

• Deweloper / Developer: LC Corp

• Otwarcie / Opening: 2007

• GLA: 30 000 m2

• Miejsca parkingowe /

Parking places: 1100

• Kontakt / Contact:

• Opis projektu:

Arkady Wrocławskie są nowoczesnym centrum handlowym

oraz biznesowym zlokalizowanym w centrum Wrocławia, w

odległości 15 minut pieszo od Rynku Starego Miasta i 5 minut

od dworca kolejowego Wrocław Główny. W galerii

funkcjonuje ponad 100 sklepów na 3 poziomach.

• Project description:

Arkady Wrocławskie is a modern shopping and business

centre, located in the hart of Wrocław, at the distance of 15

min. walk from the Old Town and 5 min. from central railway

station. 110 stores and service outlets located on 3 retail

floors.

• Główni najemcy / Anchor tenants:

CUSHMAN & WAKEFIELD 14

PORTFOLIO

• Opis projektu:

Sky Tower to pierwszy wrocławski drapacz chmur oraz nazwa

mieszczącej się w nim Galerii handlowej. W Galerii, oprócz

markowych sklepów i butików, znajdują się również

restauracje, kawiarnie oraz bary. Jest też część rozrywkowa z

salą bilardową i kręgielnią.

• Project description:

Sky Tower is the first skyscraper in Wrocław. Sky Tower is

also the name of shopping gallery where we can find designer

stores, boutiques restaurants, bars and entertainment part with

billiards room and bowling.

• Główni najemcy / Anchor tenants:

SKY TOWER, WROCŁAW

• Deweloper / Developer: LC Corp

• Otwarcie / Opening: 2012

• GLA: 25 000 m2

• Miejsca parkingowe /

Parking places: 1500

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 15

PORTFOLIO

GEMINI PARK, BIELSKO-BIAŁA

• Opis projektu:

Gemini Park Bielsko-Biała to nowoczesne i przestronne

centrum handlowe. Ponad 40 tysięcy metrów kwadratowych,

120 znanych i cenionych marek, a także komfortowy parking

wyróżniają Centrum na tle konkurencji. Gemini Park Bielsko-

Biała charakteryzuje się znakomitą lokalizacją i świetnymi

rozwiązaniami komunikacyjnymi.

• Project description:

Gemini Park is a family-oriented spacious shopping centre with

ample parking and convenient public transport links aimed at

creating attractive and enjoyable shopping experience.

• Główni najemcy / Anchor tenants:

• Deweloper / Developer: Gemini Holdings

• Otwarcie / Opening: 2009

• GLA: 42 000 m2

• Miejsca parkingowe /

Parking places: 1 100

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 16

PORTFOLIO

• Opis projektu:

Centrum Handlowe Plejada powstało w 2001 roku i od tamtej

pory nieustannie przechodzi kolejne fazy rozwoju, starając się

sprostać klientom o rozmaitych oczekiwaniach. W ofercie

znajdują się zarówno sklepy odzieżowe, jak i doskonale

wyposażone punkty usługowe. Na gości czekają przepełnione

zapachami restauracje i kawiarnie oraz praktyczne lokale

handlowe, proponujące produkty z wielu segmentów sprzedaży

(wyposażenie domu, multimedia, elektronika, sprzęt AGD/RTV

i inne). Znajduje się tu również hipermarket Carrefour,

gwarantujący udane, codzienne zakupy.

• Project description:

Plejada was established in 2001 and since then has constantly

experiencing further development phase , trying to meet the

expectations of various clients . We offer both fashion stores,

as well as well-equipped service points. Guests will find

restaurants and cafes as well as practical commercial premises,

offering products from many segments of sales ( home

furnishings, multimedia, electronics and others). There is also a

Carrefour hipermarket.

• Główni najemcy / Anchor tenants:

PLEJADA, SOSNOWIEC

• Deweloper / Developer: St. Martins

• Otwarcie / Opening: 2001

• GLA: 20 000 m2

• Miejsca parkingowe /

Parking places: 1300

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 17

PORTFOLIO

• Opis projektu:

Galeria Trzy Korony to miejsce doskonałe dla udanych zakupów

w gronie przyjaciół i rodziny. Wśród obecnych marek znajdują się

regionalni przedsiębiorcy oraz cenione, sieciowe marki

odzieżowe. Galeria znajduje się w bardzo korzystnym położeniu

w odległości ok. 10 minut pieszo od rynku starego miasta.

Znajduje się tu ponad 120 sklepów, restauracji i kawiarni, oraz

punktów usługowych, ponadto strefa fitness i kino.

• Project Description:

Gallery Trzy Korony is a place perfect for shopping with your

friends and family. You can find there some local brands, next to

well known top brands. Gallery is located only about 10 minutes

on foot from the city’s old market. There are over 120 shops,

restaurants, cafes and service points, what is more there is fitness

zone and cinema.

• Główni najemcy / Anchor tenants:

GALERIA TRZY KORONY, NOWY SĄCZ

• Deweloper / Developer: CD Lokum

• Otwarcie / Opening: 2013

• GLA: 35 495 m2

• Miejsca parkingowe /

Parking places: 765

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 18

PORTFOLIO

• Opis projektu:

Galeria Rondo Bochnia jest usytuowana w centrum Bochni.

Znajdują się tu liczne sklepy, butiki oraz punkty usługowe.

Zainteresowanych zakupem elektroniki, odtwarzaczy oraz

sprzętów gospodarstwa domowego zapraszamy do Galerii

Rondo. Znajduje się tu również supermarket spożywczy

TESCO. Galeria Rondo to również miejsce spotkań

z przyjaciółmi, gdzie można miło spędzić czas przy filiżance

dobrej kawy, lub wybrać się na pyszny lunch.

• Project description:

Gallery Rondo Bochnia is located in the center of Bochnia.

There are many shops, boutiques and service proints. Clients

who plan to buy electronics, audio players and household

appliances should visit Galeria Rondo. There is also a

supermarket Tesco. Gallery Rondo is also a place to meet

friends , where you can spend time with a good cup of coffee,

or enjoy a delicious lunch.

• Główni najemcy / Anchor tenants:

GALERIA RONDO, BOCHNIA

• Deweloper / Developer: CD Lokum

• Otwarcie / Opening: 2010

• GLA: 12 600 m2

• Miejsca parkingowe /

Parking places: 600

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 19

PORTFOLIO

• Opis projektu:

Galeria Dębicka stanowi główne centrum handlowe miasta

Dębica. Centrum posiada bardzo silny skład najemców,

dopasowany do potrzeb lokalnego rynku. Znajdują się tu butiki

odzieżowe znanych marek, sklepy kosmetyczne i obuwnicze.

Wśród oferty galerii nie brakuje restauracji, licznych punktów

usługowych, a także hipermarketu i salonu ze sprzętem RTV i

AGD. Duża różnorodność połączona z obecnością ulubionych

marek Polaków stanowi bardzo atrakcyjną ofertę dla klientów,

dla których na bieżąco przygotowywane są specjalne oferty

i promocje.

• Project description:

Dębicka Gallery is the main shopping center of Dębica. It has

very strong tenant mix, that matches needs of local market. In

the offer of Dębicka there are clothing boutiques of well-

known brands, health and beauty shops, as well as shoe shops.

There are also restaurants, many service points, a hypermarket

and RTV/AGD store. A big variety of shops combined with

presence of favorite brands makes it a very attractive offer. The

Center prepares many special offers and discounts for clients.

• Główni najemcy / Anchor tenants:

GALERIA DĘBICKA

• Deweloper / Developer: CD Lokum

• Otwarcie / Opening: 2007

• GLA: 12 500 m2

• Miejsca parkingowe /

Parking places: 595

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 20

PORTFOLIO

• Opis projektu:

marcredo Center Kutno zlokalizowane jest blisko centrum

miasta, z bardzo dobrym dojazdem zarówno samochodem, jak i

środkami komunikacji miejskiej. W centrum znajduje się

supermarket, DIY, najemcy z branży modowej i restauracje,

przyciągające mieszkańców Kutna i okolic.

• Project description:

marcredo Shopping Center is located near to the city center

with very good access by car and public transport. In the center

we will find supermarket, DIY, fashion anchors and restaurants,

that attract clients from Kutno and the surrounding area.

• Główni najemcy / Anchor tenants:

MARCREDO CENTER, KUTNO

• Deweloper / Developer: Elbfonds

• Otwarcie / Opening: 2014

• GLA: 16 700 m2

• Miejsca parkingowe /

Parking places: 500

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 21

PORTFOLIO

• Opis projektu:

marcredo Center Szczecin to park handlowy, zlokalizowany

w bardzo dobrym punkcie komunikacyjnym – tuż przy drodze

krajowej nr 10. Obiekt skupia wielkopowierzchniowe sklepy,

przyciągające klientów ze Szczecina i okolic.

• Project description:

Marcredo Center Szczecin is a retail park, located near to the

national road 10. The center consists of big-size stores, that

attract clients from Szczecin and the surrounding area.

• Główni najemcy / Anchor tenants:

MARCREDO CENTER, SZCZECIN

• Deweloper / Developer: Elbfonds

• Otwarcie / Opening: 2013

• GLA: 14 000 m2

• Miejsca parkingowe /

Parking places: 450

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 22

PORTFOLIO

HIGH STREETS

ULICE HANDLOWE

CUSHMAN & WAKEFIELD 23

PORTFOLIO

NOWY ŚWIAT / ŚWIĘTOKRZYSKA

• Developer / Developer: Świętokrzyska 3

• Otwarcie / Opening: 2014

• GLA: 4 000 – 5 200 m2

• Kontakt / Contact:

• Opis projektu:

Budynek znajdujący się na rogu ulic Nowy Świat i

Świętokrzyska w Warszawie.

• Project description:

The townhouse fronting both Świętokrzyska Street and Nowy

Świat Street. The building is currently undergoing a thorough

refurbishment.

• Najemcy / Tenants:

CUSHMAN & WAKEFIELD 24

PORTFOLIO

SILVER TOWER CENTER/ WROCŁAW

• Deweloper / Developer: Wisher Enterprise

• Otwarcie / Opening: 2015

• GLA: 2 000 m2

• Kontakt / Contact:

• Opis Projektu:

Silver Tower Center to budynek znajdujący się naprzeciw

dworca kolejowego Wrocław Główny, 10 minut od centrum

miasta. Obekt ten pełni funkcję biurową, handlową oraz

hotelową.

• Project description:

Silver Tower Center is located opposite the central railway

station, 10 min from the city centre. The building provides a

total of 14,600 sq m of office, retail and hotel accommodation.

• Najemcy / Tenants:

CUSHMAN & WAKEFIELD 25

PORTFOLIO

RETAIL PARKS

PARKI

HANDLOWE

RETAIL PARKS

CUSHMAN & WAKEFIELD 26

PORTFOLIO

RETAIL PARK RADZIONKÓW

• Deweloper / Developer: Budecon

• Otwarcie / Opening: 2015

• GLA: 4 600 m2

• Kontakt / Contact:

• Opis projektu:

Park handlowy zlokalizowany w Radzionkowie, u zbiegu ulic

Unii Europejskiej i Szymały.

• Project description:

Retail Park located in Radzionków, crossroad Unii Europejskiej

and Szymały street. Retail park with wide offer of clothes,

footwear-gallantry and electronic stuff in the immediate vicinity

of supermarket.

• Najemcy / Tenants:

CUSHMAN & WAKEFIELD 27

PORTFOLIO

RETAIL PARK ŚWIĘTOCHŁOWICE

• Developer / Developer: Budecon

• Otwarcie / Opening: 2015

• GLA: 2 000 m2

• Kontakt / Contact:

• Opis projektu:

Park handlowy z szerokim asortymentem odzieżowym,

obuwniczym oraz elektronicznym w bezpośrednim sąsiedztwie

sklepu spożywczego.

• Project description:

Retail park with wide offer of clothes, footwear-gallantry and

electronic stuff in the immediate vicinity of supermarket.

• Nejemcy / Tenants:

CUSHMAN & WAKEFIELD 28

RETAIL SERVICES

MULTISHOP JAROCIN

• Deweloper / Developer: Multishop Development

• Otwarcie / Opening: 2016

• GLA: 6 000 m2

• Miejsca parkingowe /

Parking places: 230

• Kontakt / Contact:

• Opis projektu:

Park handlowy Multishop powstaje w Jarocinie, w niedużej

odległości od centrum miasta i będzie doskonałym wyborem

dla osób chcących uniknąć zakupów w zatłoczonym

śródmieściu.

• Project description:

The site is a short distance from the city centre. Planned retail

park will be the best choice for those who enjoy a great

shopping experience but avoid the busy city center.

CUSHMAN & WAKEFIELD 29

RETAIL SERVICESREPREZENTACJA

NAJEMCY

TENANT

REPRESENTATION

CUSHMAN & WAKEFIELD 30

RETAIL SERVICES

Warszawa, Marszałkowska

• Fashion Anchor

• In 2008 we started the cooperation with TK Maxx. At

first it was limited to market study and initial guidance

but in 2009 C&W were appointed the expansion agent

for this international retailer

• We assisted in the opening of 20 up to date among

them the TK Maxx European flagship store at

Marszałkowska street in Warsaw

• Duży najemca modowy

• W 2008 nawiązaliśmy współpracę z właścicielem marki TK

Maxx. Najpierw przygotowaliśmy dla naszego klienta raport

rynkowy by następnie od 2009 zostać agentem

odpowiedzialnym za rozwój sklepów TK Maxx na terenie

Polski

• Za naszym pośrednictwem firma TJX Maxx otworzyła 20

sklepów TK Maxx, w tym ich flagowy sklep przy ul

Marszałkowskiej w Warszawie

Gdynia, CH RivieraWarszawa, Targówek Retail Park

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 31

RETAIL SERVICES

Warszawa, Arkadia

• Fashion & Sport Retailer

• In 2010 C&W started the cooperation with Foot

Locker. We started with the market study and initial

guidance but in 2011 C&W were appointed the

exclusive agent for this international retailer

• C&W assisted Foot Locker in opening 6 stores, among

them Warsaw Arkadia and Warsaw Złote Tarasy

• Najemca: moda i sport

• W 2010 nawiązaliśmy współpracę z firmą Foot Locker.

Najpierw przygotowaliśmy dla naszego klienta raport rynkowy

by następnie od 2011 zostać agentem odpowiedzialnym za

rozwój wszystkich sklepów Foot Locker na terenie Polski

• Za naszym pośrednictwem firma Foot Locker otworzyła 6

sklepów, w tym w dwóch warszawskich centrach handlowych

Arkadia i Złote Tarasy

Bonarka City Center, KrakówWrocław, Pasaż Grunwaldzki

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 32

RETAIL SERVICES

Warszawa, Atrium Targówek

• Men’s Fashion Retailer

• In 2012 C&W started the cooperation with Brice. We

started with the market study and initial guidance and

then C&W were appointed the exclusive agent for this

international retailer

• C&W assisted Brice in opening 2 stores in shopping

centers - Atrium Targówek in Warsaw, Galeria

Katowicka in Katowice

• Francuska sieć mody męskiej

• W 2012 nawiązaliśmy współpracę z firmą Brice. Najpierw

przygotowaliśmy dla naszego klienta raport rynkowy by

następnie zostać agentem odpowiedzialnym za rozwój sklepów

Brice na terenie Polski

• Za naszym pośrednictwem firma Brice otworzyła 2 sklepy, w

Atrium Targówek w Warszawie oraz w Galerii Katowickiej

• Kontakt / Contact:

CUSHMAN & WAKEFIELD 33

RETAIL SERVICES

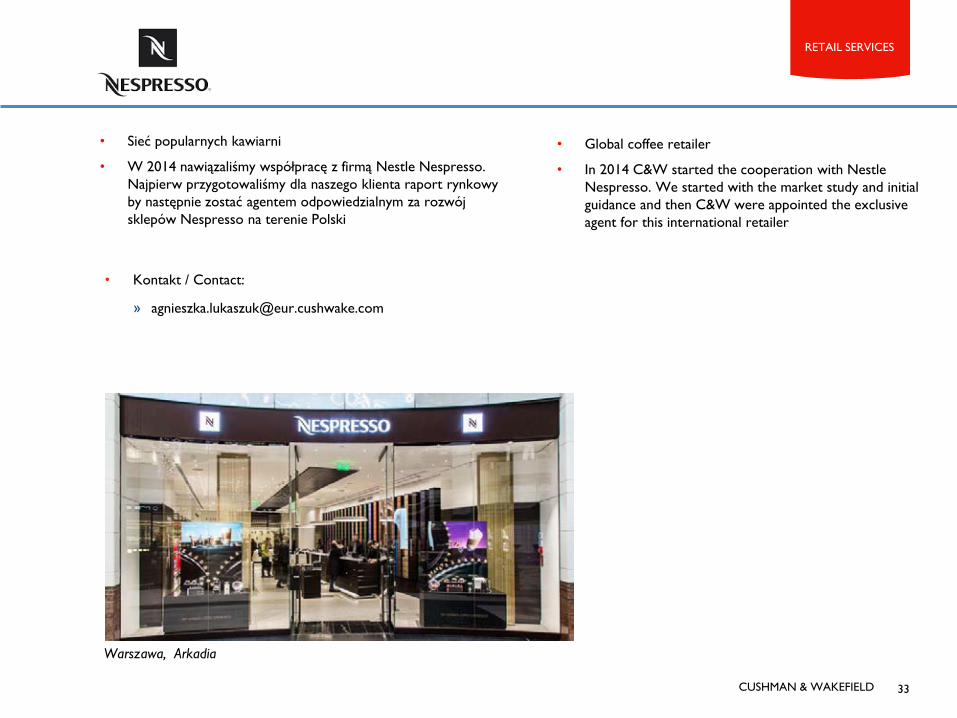

Warszawa, Arkadia

• Global coffee retailer

• In 2014 C&W started the cooperation with Nestle

Nespresso. We started with the market study and initial

guidance and then C&W were appointed the exclusive

agent for this international retailer

• Sieć popularnych kawiarni

• W 2014 nawiązaliśmy współpracę z firmą Nestle Nespresso.

Najpierw przygotowaliśmy dla naszego klienta raport rynkowy

by następnie zostać agentem odpowiedzialnym za rozwój

sklepów Nespresso na terenie Polski

• Kontakt / Contact:

www.cushmanwakefield.com

CUSHMAN & WAKEFIELD POLSKA SP. Z O.O.

Pl. Piłsudskiego 1

00-078 Warszawa

Tel. 22 820 20 20