2016- the iran upstream and downstream...

TRANSCRIPT

Horizon Development GroupYour gateway to Iran

Slide 1Date 18/05/2016

2016- The Iran Upstream and Downstream

Opportunity

What is needed? When is it needed? How to be

successful in providing what is required.

Horizon Development GroupYour gateway to Iran Slide 2Date 18/05/2016

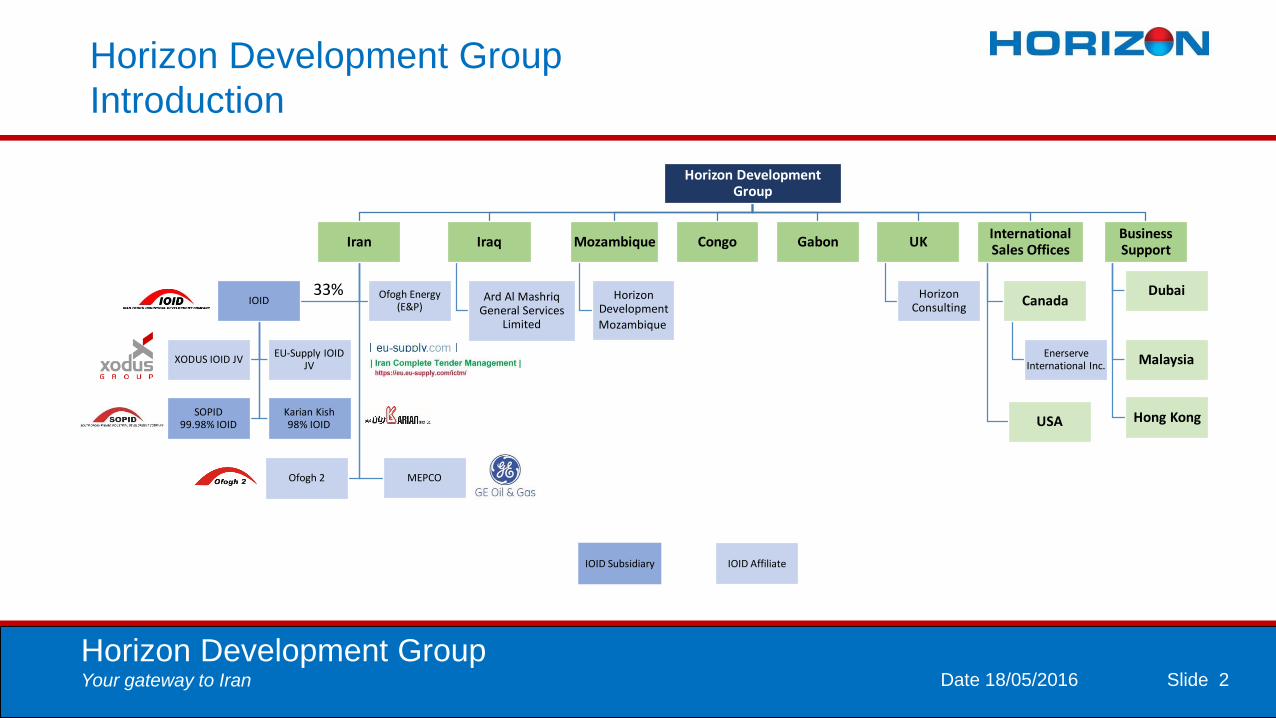

Horizon Development Group

Introduction

Horizon Development Group

Iran

IOID

XODUS IOID JVEU-Supply IOID

JV

SOPID 99.98% IOID

Karian Kish 98% IOID

Ofogh Energy (E&P)

MEPCOOfogh 2

Iraq

Ard Al MashriqGeneral Services

Limited

Mozambique

Horizon Development

Mozambique

Congo Gabon UK

Horizon Consulting

International Sales Offices

Canada

EnerserveInternational Inc.

USA

Business Support

Dubai

Malaysia

Hong Kong

33%

IOID AffiliateIOID Subsidiary

Horizon Development GroupYour gateway to Iran Slide 3Date 18/05/2016

Horizon Development Group

Iran Strategy

With the opening of the Iranian petroleum industry to foreign investment in 2016 our aims are to:

Grow our existing Iran service lines

Build new capabilities through joint venture partnerships with international equipment, goods and

service providers

Participate in field development and redevelopment projects in Iran as an equity investor with

reputable international oil companies on robust projects where we can

Improve the chance of project delivery to cost, quality and schedule targets through our understanding of Iran and how to build business momentum

Deliver on Iranian content targets and Iran’s technology transfer objectives

Horizon Development GroupYour gateway to Iran Slide 4Date 18/05/2016

What is needed

Iran’s 6th Five Year Plan

• Iran’s 6th five year plan

• Development of a resilient

economy

– 8% annual growth GDP

– Reform of state enterprises (60%

GDP) and banking sector

• Progress in science and

technology

• Promotion of cultural excellence

• Implications for the oil industry

• 3.7 MM bopd in 2014 rising to 4.6

MM bopd in 2020

– Oil exports to rise from 1.3 MM bopd

in 2015 to 2.4 MM bopd (implying a

decrease in Iranian oil consumption)

• 0.44 MM bcpd in 2014 rising to 1

MM bcpd in 2020 (Petrochem)

• Priority for shared fields

Horizon Development GroupYour gateway to Iran Slide 5Date 18/05/2016

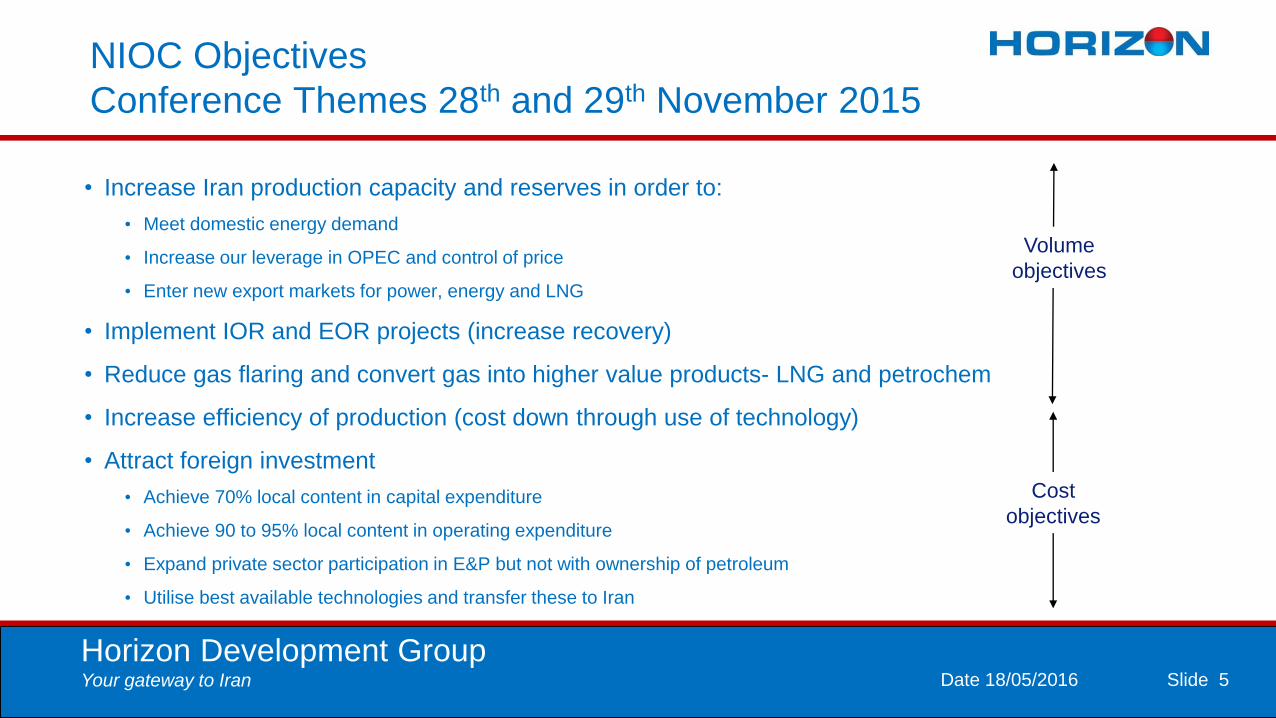

NIOC Objectives

Conference Themes 28th and 29th November 2015

• Increase Iran production capacity and reserves in order to:

• Meet domestic energy demand

• Increase our leverage in OPEC and control of price

• Enter new export markets for power, energy and LNG

• Implement IOR and EOR projects (increase recovery)

• Reduce gas flaring and convert gas into higher value products- LNG and petrochem

• Increase efficiency of production (cost down through use of technology)

• Attract foreign investment

• Achieve 70% local content in capital expenditure

• Achieve 90 to 95% local content in operating expenditure

• Expand private sector participation in E&P but not with ownership of petroleum

• Utilise best available technologies and transfer these to Iran

Volume

objectives

Cost

objectives

Horizon Development GroupYour gateway to Iran Slide 6Date 18/05/2016

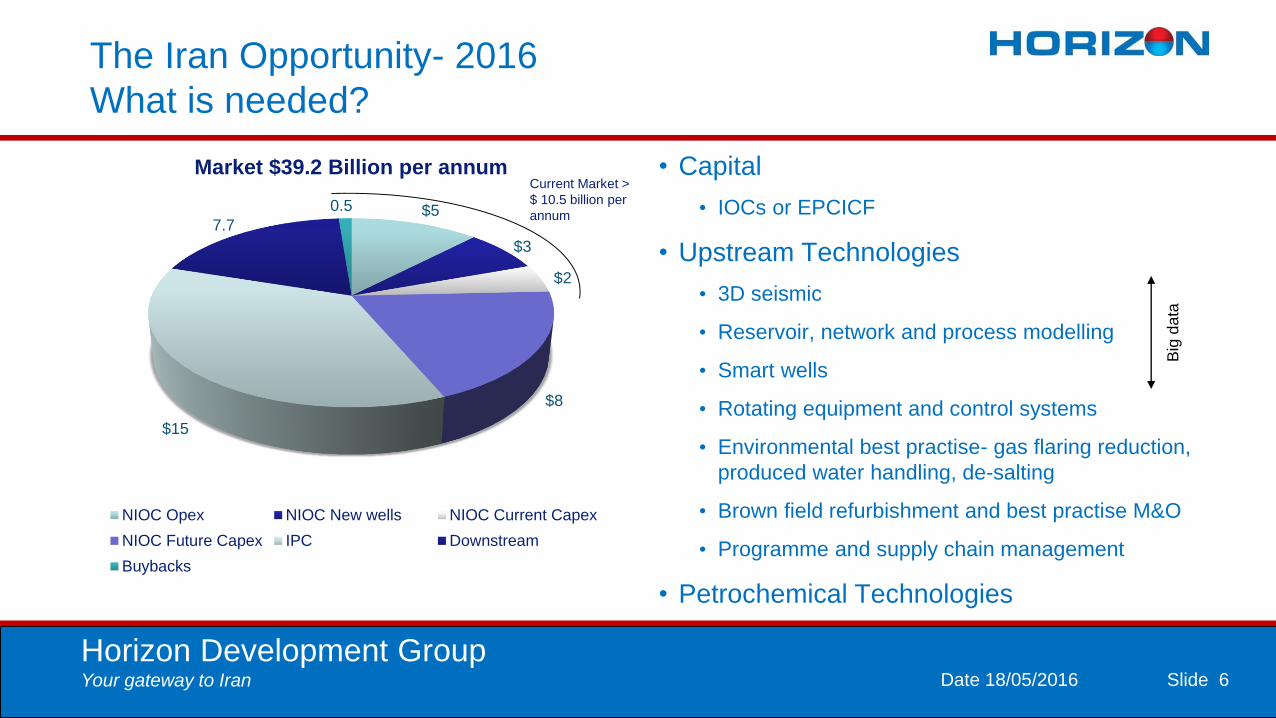

The Iran Opportunity- 2016

What is needed?

$5

$3

$2

$8

$15

7.7

0.5

Market $39.2 Billion per annum

NIOC Opex NIOC New wells NIOC Current Capex

NIOC Future Capex IPC Downstream

Buybacks

• Capital

• IOCs or EPCICF

• Upstream Technologies

• 3D seismic

• Reservoir, network and process modelling

• Smart wells

• Rotating equipment and control systems

• Environmental best practise- gas flaring reduction,

produced water handling, de-salting

• Brown field refurbishment and best practise M&O

• Programme and supply chain management

• Petrochemical Technologies

Current Market >

$ 10.5 billion per

annum

Big

da

ta

Horizon Development GroupYour gateway to Iran Slide 7Date 18/05/2016

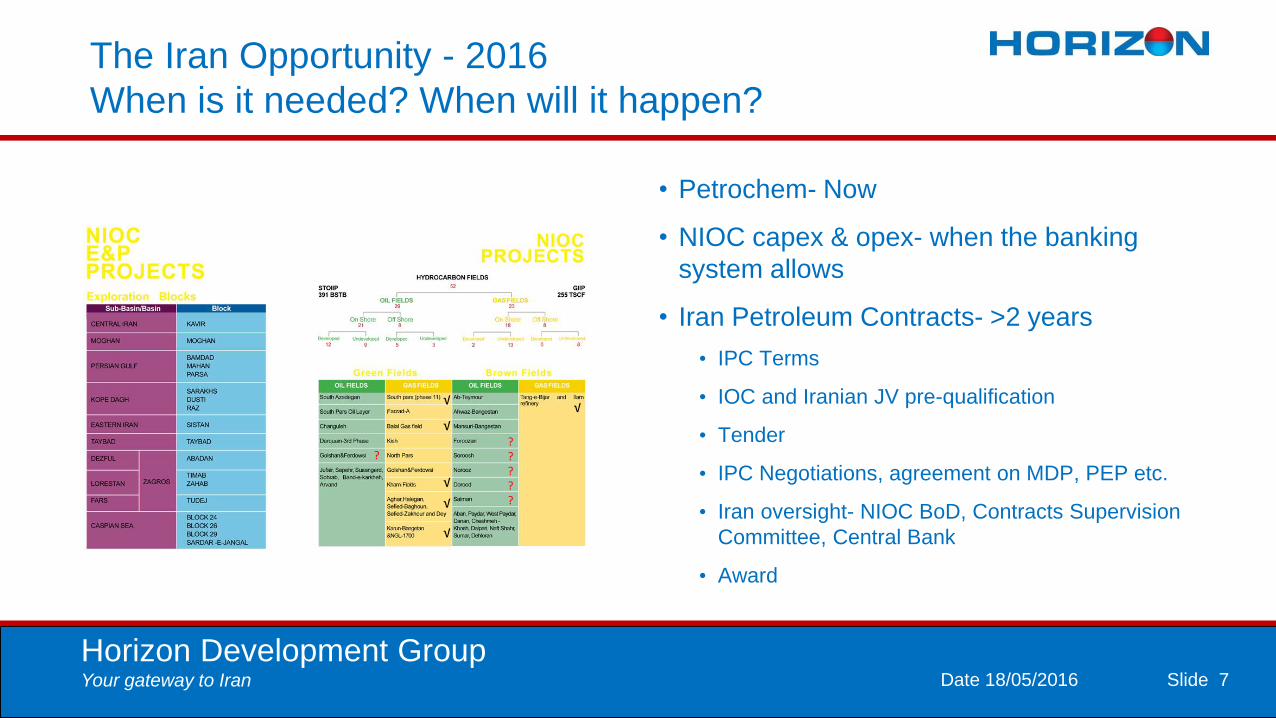

The Iran Opportunity - 2016

When is it needed? When will it happen?

• Petrochem- Now

• NIOC capex & opex- when the banking

system allows

• Iran Petroleum Contracts- >2 years

• IPC Terms

• IOC and Iranian JV pre-qualification

• Tender

• IPC Negotiations, agreement on MDP, PEP etc.

• Iran oversight- NIOC BoD, Contracts Supervision

Committee, Central Bank

• Award

√

√

√

√

√

√

??????

Horizon Development GroupYour gateway to Iran Slide 8Date 18/05/2016

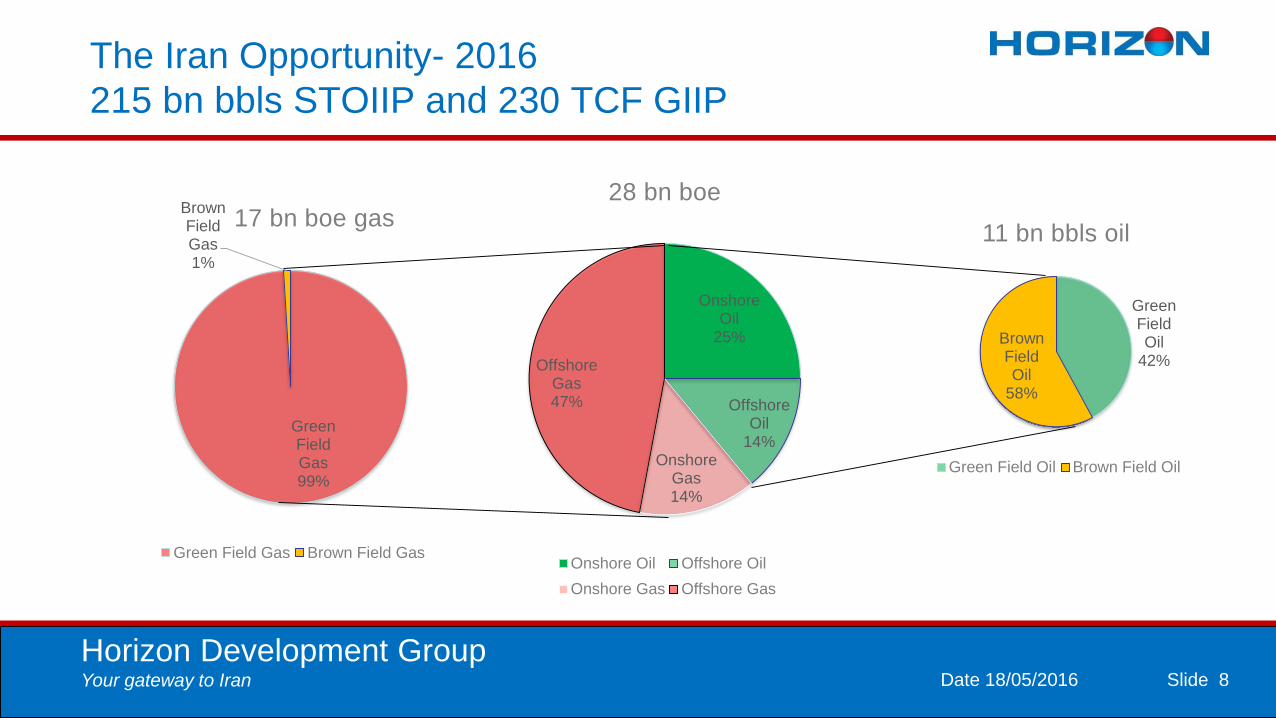

Onshore Oil

25%

Offshore Oil

14%Onshore

Gas14%

Offshore Gas47%

28 bn boe

Onshore Oil Offshore Oil

Onshore Gas Offshore Gas

The Iran Opportunity- 2016

215 bn bbls STOIIP and 230 TCF GIIP

Green Field Gas99%

Brown Field Gas1%

17 bn boe gas

Green Field Gas Brown Field Gas

Green Field Oil

42%

Brown Field Oil

58%

11 bn bbls oil

Green Field Oil Brown Field Oil

Horizon Development GroupYour gateway to Iran Slide 9Date 18/05/2016

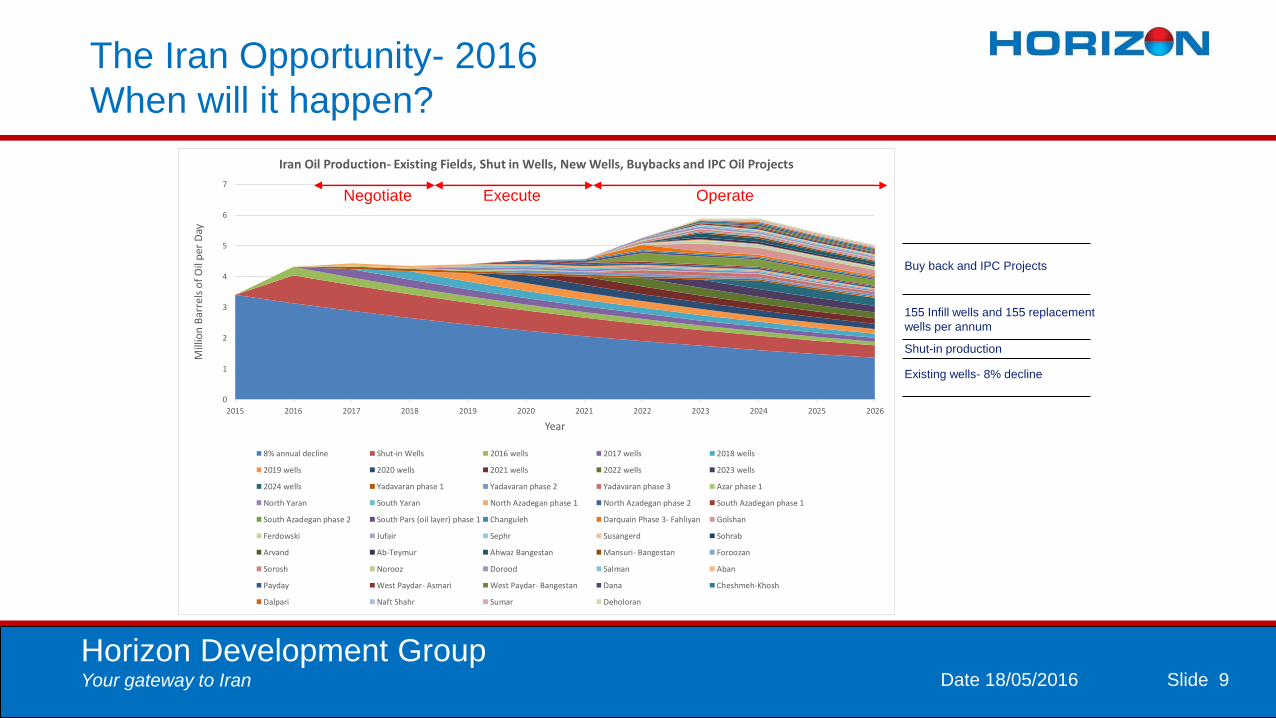

The Iran Opportunity- 2016

When will it happen?

0

1

2

3

4

5

6

7

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Mill

ion

Bar

rels

of

Oil

per

Day

Year

Iran Oil Production- Existing Fields, Shut in Wells, New Wells, Buybacks and IPC Oil Projects

8% annual decline Shut-in Wells 2016 wells 2017 wells 2018 wells

2019 wells 2020 wells 2021 wells 2022 wells 2023 wells

2024 wells Yadavaran phase 1 Yadavaran phase 2 Yadavaran phase 3 Azar phase 1

North Yaran South Yaran North Azadegan phase 1 North Azadegan phase 2 South Azadegan phase 1

South Azadegan phase 2 South Pars (oil layer) phase 1 Changuleh Darquain Phase 3- Fahliyan Golshan

Ferdowski Jufair Sephr Susangerd Sohrab

Arvand Ab-Teymur Ahwaz Bangestan Mansuri- Bangestan Foroozan

Sorosh Norooz Dorood Salman Aban

Payday West Paydar- Asmari West Paydar- Bangestan Dana Cheshmeh-Khosh

Dalpari Naft Shahr Sumar Deholoran

Existing wells- 8% decline

Buy back and IPC Projects

155 Infill wells and 155 replacement

wells per annum

Shut-in production

OperateExecuteNegotiate

Horizon Development GroupYour gateway to Iran Slide 10Date 18/05/2016

The Iran Opportunity-2016

How to be successful in providing what is required?

• Risks and Issues

• Banking System

• Sanctions

• Terms and NIOC capacity to negotiate

• ROI- South Pars 6-8 and Darquain Phase 2

were out of the money

• Getting your client to understand the

problem, the need and the solution

• Business momentum

• Vested interests

• Enablers to successful entry

• Capital

• Technology transfer

• Project and Supply Chain Management

• Environmental Issues

– Gas flaring and produced water disposal

• Local partner- >51% local content with a

PJSC & >95% during production operations

• Stakeholder Management

• Iran wants you!

Snap back Not and issueUN & EU

Compliance

UN, US & EU

Compliance

Exo

ge

no

us

Horizon Development GroupYour gateway to Iran Slide 11Date 18/05/2016

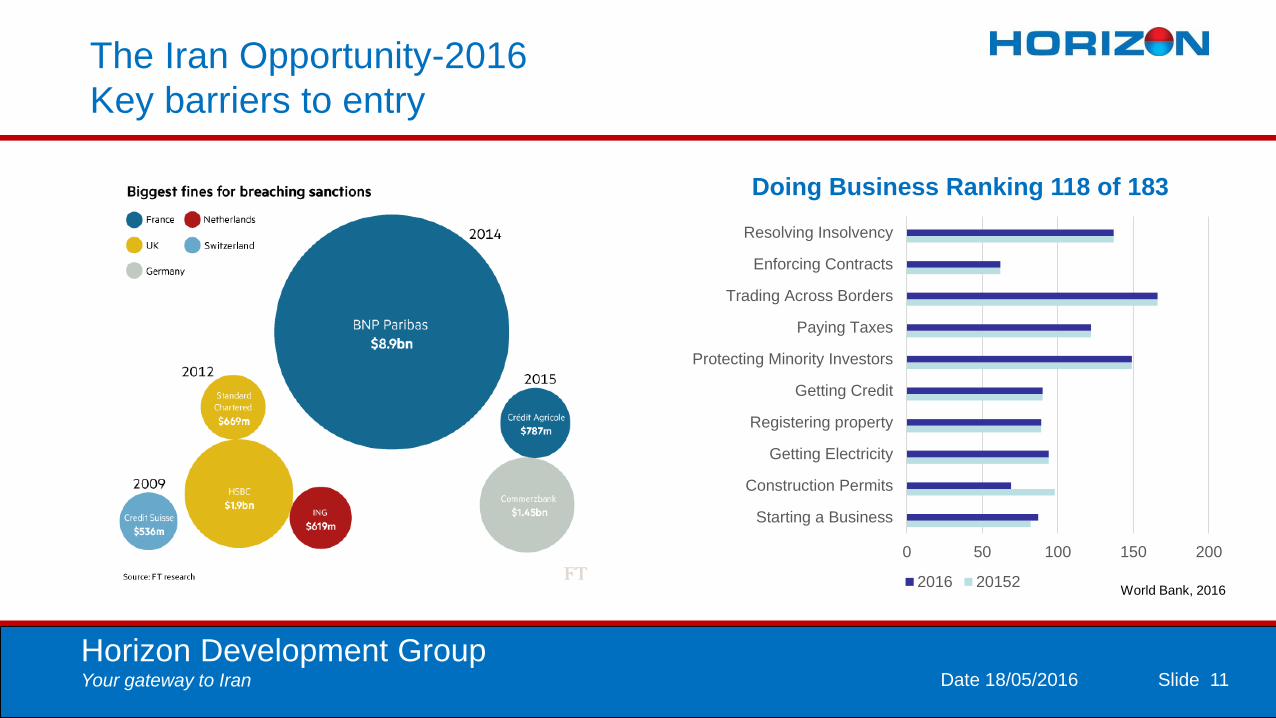

The Iran Opportunity-2016

Key barriers to entry

World Bank, 2016

0 50 100 150 200

Starting a Business

Construction Permits

Getting Electricity

Registering property

Getting Credit

Protecting Minority Investors

Paying Taxes

Trading Across Borders

Enforcing Contracts

Resolving Insolvency

Doing Business Ranking 118 of 183

2016 20152

Horizon Development GroupYour gateway to Iran Slide 12Date 18/05/2016

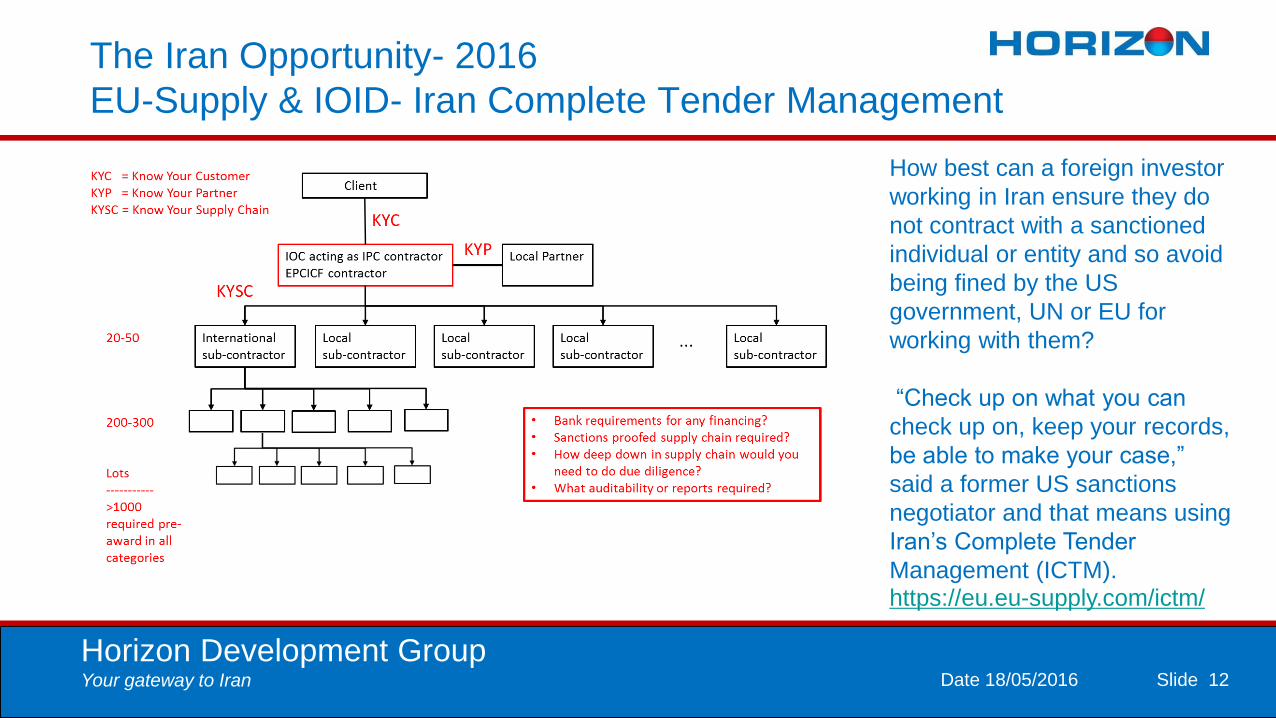

The Iran Opportunity- 2016

EU-Supply & IOID- Iran Complete Tender Management

How best can a foreign investor

working in Iran ensure they do

not contract with a sanctioned

individual or entity and so avoid

being fined by the US

government, UN or EU for

working with them?

“Check up on what you can

check up on, keep your records,

be able to make your case,”

said a former US sanctions

negotiator and that means using

Iran’s Complete Tender

Management (ICTM).https://eu.eu-supply.com/ictm/