2017 10 03 - pfi - portfolio acquisition and equity ... · pdf fileto support the acquisition...

TRANSCRIPT

� Property for Industry (PFI) is an NZX listed property vehicle focused on industrial property

� PFI’s strategy is to invest in quality industrial property in prime locations in order to deliver attractive

returns with a low level of volatility

� PFI has:

• A $1.1bn property portfolio with an 85% weighting to Auckland

• An experienced and internalised management team supported by a strong governance framework

• A proven track record with a history of stable earnings and sound risk management

• Robust portfolio metrics with a WALT of 4.8 years and occupancy of 99.5%

• A strong balance sheet with an LVR of 34.2% and an ICR of 3.6 times

• Delivered an average annual return to shareholders since inception of ~9.6% and over the past 10 years

has outperformed the NZX50 and the NZX Property Index

PFI OVERVIEW

4PROPERTY FOR INDUSTRY EXECUTIVE SUMMARY

Fletcher Building Products, 30-32 Bowden RoadNote: all statistics as at 30 June 2017 and prior to the Acquisition and Offer

� PFI has secured a portfolio of eight industrial properties and one head office for an acquisition price of

$69.5m (the Acquisition)

• The portfolio includes seven properties leased to the Transport Investments Limited Group (TIL), one of

New Zealand’s largest private domestic freight and logistics businesses

• The two additional properties are leased to NZ Post, Aviagen and Rockgas

� The portfolio is comprised of quality properties with attractive lease terms

• The acquisition portfolio has a WALT of 13.9 years which will increase PFI’s overall portfolio WALT by 0.6

years1

• All TIL properties benefit from fixed rent reviews of 4.55% every two years, providing future rental growth

• The acquisition portfolio also provides for significant medium to long-term development potential with low

site coverage of ~25% across the nine acquisition sites

PORTFOLIO ACQUISITION

5PROPERTY FOR INDUSTRY EXECUTIVE SUMMARY

1. Pro forma as at 30 June 2017, under the assumption that the portfolio was acquired on 30 June 2017

� To support the Acquisition and ongoing activity in its portfolio, PFI is seeking to raise approximately

$70m of new equity via a fully underwritten pro rata rights issue (the Offer)

• 1 for 10 rights issue, at an Issue Price of $1.54 fully underwritten by Forsyth Barr Group Limited

• PFI Board and senior executives have committed to take up all Rights in respect of their beneficial

shareholdings under the Offer

� Post the Acquisition and the Offer:

• PFI’s LVR will decrease from 34.2% to 32.3%1

• The PFI Board confirms the previously provided guidance for distributable profit of between 7.70 and 7.90

cents per share and a cash dividend of 7.45 cents per share for FY17 is unchanged

EQUITY RAISING

6PROPERTY FOR INDUSTRY EXECUTIVE SUMMARY

1. Based on PFI’s Consolidated Statement of Financial Position as at 30 June 2017. Calculated as the value of borrowings (adjusted for the value of the Acquisition, the proceeds of the Offer and transaction costs) divided by the value of investment properties (adjusted for the value of the Acquisition).

EXISTING PORTFOLIO SNAPSHOT

8

� PFI’s existing property portfolio:

• is diversified across 83 properties and 144

tenants

• has 99.5% occupancy and a WALT of 4.78

years

• has an 85.3% weighting towards Auckland

and an 85.4% weighting towards industrial

property

� PFI has consistently delivered robust portfolio

metrics with average occupancy of 98.6% and an

average WALT of 4.8 years since 2008

PROPERTY FOR INDUSTRY PFI OVERVIEW

Note: all statistics as at 30 June 2017 and prior to the Acquisition

9

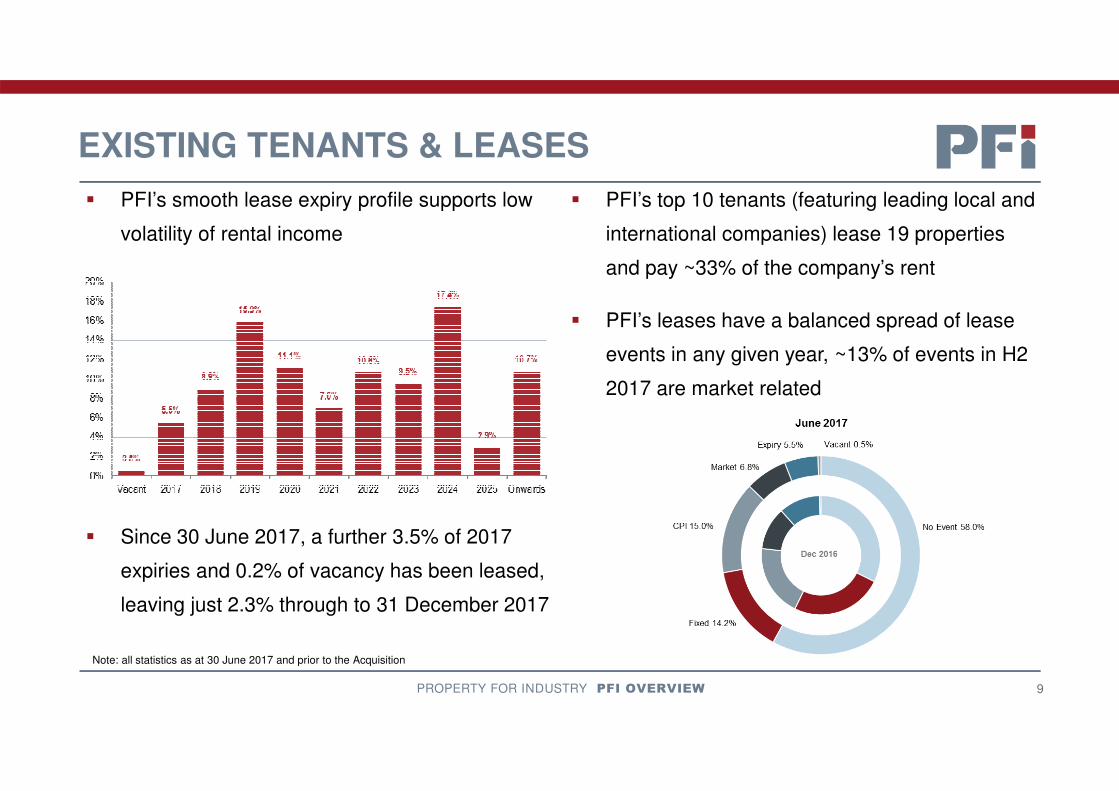

EXISTING TENANTS & LEASES

� PFI’s smooth lease expiry profile supports low

volatility of rental income

PROPERTY FOR INDUSTRY PFI OVERVIEW

� PFI’s top 10 tenants (featuring leading local and

international companies) lease 19 properties

and pay ~33% of the company’s rent

� PFI’s leases have a balanced spread of lease

events in any given year, ~13% of events in H2

2017 are market related

� Since 30 June 2017, a further 3.5% of 2017

expiries and 0.2% of vacancy has been leased,

leaving just 2.3% through to 31 December 2017

Note: all statistics as at 30 June 2017 and prior to the Acquisition

MARKET UPDATE

10

� CBRE’s August 2017 report showed high levels of occupier demand for industrial property, with

Auckland industrial vacancy of just 1.6% or 196,900 sqm

� Colliers International July 2017 “Commercial Property Investor Confidence Survey” showed high

levels of investor confidence in industrial property, with all three main centres experiencing net

positive confidence and an increase in confidence from the prior survey

PROPERTY FOR INDUSTRY PFI OVERVIEW

� ANZ’s “Truckometer” (see graph on right) illustrates a

strong correlation between Prime Industrial Yields and

the Heavy Traffic Index, and the Truckometer “direction

of travel” suggests yields could tighten further

� A mix of strong economic growth, favourable occupier

supply and demand dynamics and high levels of

investor market confidence has seen industrial property

yields falling a further ~30 basis points (0.3%) in the first

six months of 2017 (CBRE, July 2017)

1H17 RESULTS SUMMARY

11PROPERTY FOR INDUSTRY PFI OVERVIEW

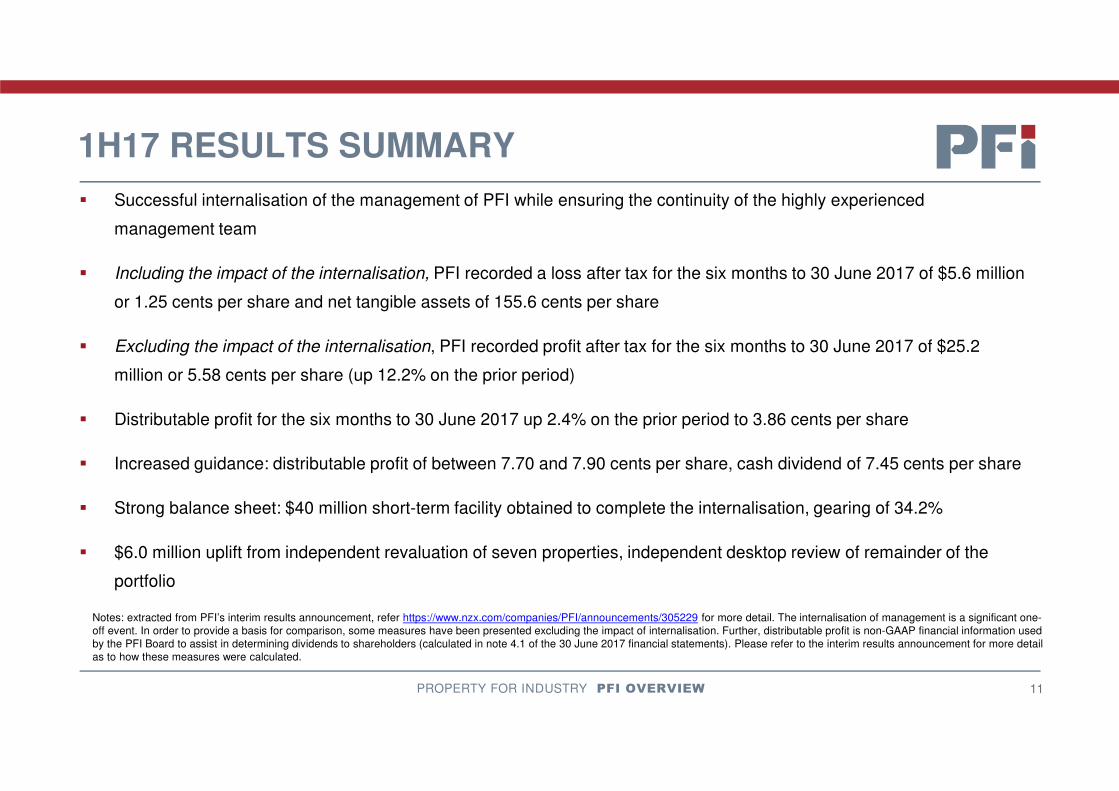

� Successful internalisation of the management of PFI while ensuring the continuity of the highly experienced

management team

� Including the impact of the internalisation, PFI recorded a loss after tax for the six months to 30 June 2017 of $5.6 million

or 1.25 cents per share and net tangible assets of 155.6 cents per share

� Excluding the impact of the internalisation, PFI recorded profit after tax for the six months to 30 June 2017 of $25.2

million or 5.58 cents per share (up 12.2% on the prior period)

� Distributable profit for the six months to 30 June 2017 up 2.4% on the prior period to 3.86 cents per share

� Increased guidance: distributable profit of between 7.70 and 7.90 cents per share, cash dividend of 7.45 cents per share

� Strong balance sheet: $40 million short-term facility obtained to complete the internalisation, gearing of 34.2%

� $6.0 million uplift from independent revaluation of seven properties, independent desktop review of remainder of the

portfolio

Notes: extracted from PFI’s interim results announcement, refer https://www.nzx.com/companies/PFI/announcements/305229 for more detail. The internalisation of management is a significant one-off event. In order to provide a basis for comparison, some measures have been presented excluding the impact of internalisation. Further, distributable profit is non-GAAP financial information used by the PFI Board to assist in determining dividends to shareholders (calculated in note 4.1 of the 30 June 2017 financial statements). Please refer to the interim results announcement for more detail as to how these measures were calculated.

13PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

ACQUISITION OVERVIEW

� PFI has secured a portfolio of nine quality properties

for an acquisition price of $69.5m

� Includes seven properties leased to the Transport

Investments Limited Group, one of New Zealand’s

largest private domestic freight and logistics

businesses

� The two additional properties are leased to NZ Post,

Aviagen and Rockgas

� The portfolio has a WALT of 13.9 years and the

acquisition price reflects a passing yield of 7.22%

� Settlement of the Acquisition is scheduled to occur on

31 October 2017

Purchase price by location

STRATEGIC RATIONALE

14PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

� The Acquisition portfolio comprises eight quality industrial properties and TIL’s head office located in Auckland,

New Plymouth, Napier, Nelson, Blenheim and Christchurch

� The Acquisition portfolio:

� Establishes PFI’s presence in additional centres across New Zealand, whilst maintaining a high

weighting towards the attractive Auckland property market

� Will improve a number of PFI’s portfolio metrics, including an extension of PFI’s WALT by 0.6 years1

� Has been purchased with attractive lease terms, with all TIL properties benefiting from fixed rent

reviews of 4.55% every two years, providing future rental growth

� Has low site coverage of ~25% across the nine acquisition sites providing for significant medium to

long-term development potential

� Establishes a strategic partnership with a quality nationwide tenant

1. Pro forma as at 30 June 2017, under the assumption that the portfolio was acquired on 30 June 2017

15

OVERVIEW OF TIL

� One of New Zealand’s largest privately owned domestic freight and

logistics businesses, TIL:

• Is the parent company for a number of well known New

Zealand transport and logistics brands including Hooker Pacific,

TNL, Roadstar, Pacific Fuel Haul and MOVE Logistics

• Has a comprehensive nationwide freight platform, including a

significant regional presence, operating from approximately 50

branches with over 1,600 employees

• Owns and operates a fleet of approximately 800 trucks,

including one of the largest privately owned tanker fleets in New

Zealand

• Provides freight, warehousing and logistics, heavy haulage and

specialised equipment services

• Has a history of successful strategic acquisitions

PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

16

PORTFOLIO SUMMARY

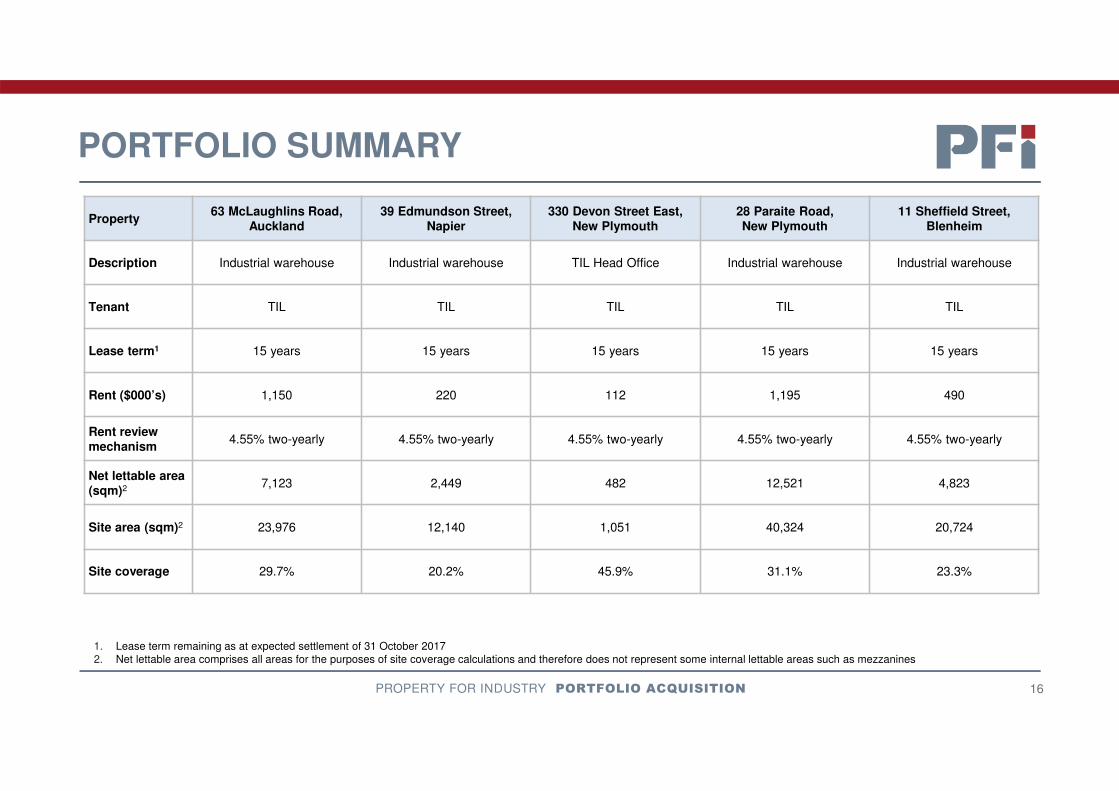

Property63 McLaughlins Road,

Auckland39 Edmundson Street,

Napier330 Devon Street East,

New Plymouth28 Paraite Road,New Plymouth

11 Sheffield Street, Blenheim

Description Industrial warehouse Industrial warehouse TIL Head Office Industrial warehouse Industrial warehouse

Tenant TIL TIL TIL TIL TIL

Lease term1 15 years 15 years 15 years 15 years 15 years

Rent ($000’s) 1,150 220 112 1,195 490

Rent review mechanism

4.55% two-yearly 4.55% two-yearly 4.55% two-yearly 4.55% two-yearly 4.55% two-yearly

Net lettable area (sqm)2 7,123 2,449 482 12,521 4,823

Site area (sqm)2 23,976 12,140 1,051 40,324 20,724

Site coverage 29.7% 20.2% 45.9% 31.1% 23.3%

PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

1. Lease term remaining as at expected settlement of 31 October 20172. Net lettable area comprises all areas for the purposes of site coverage calculations and therefore does not represent some internal lettable areas such as mezzanines

17

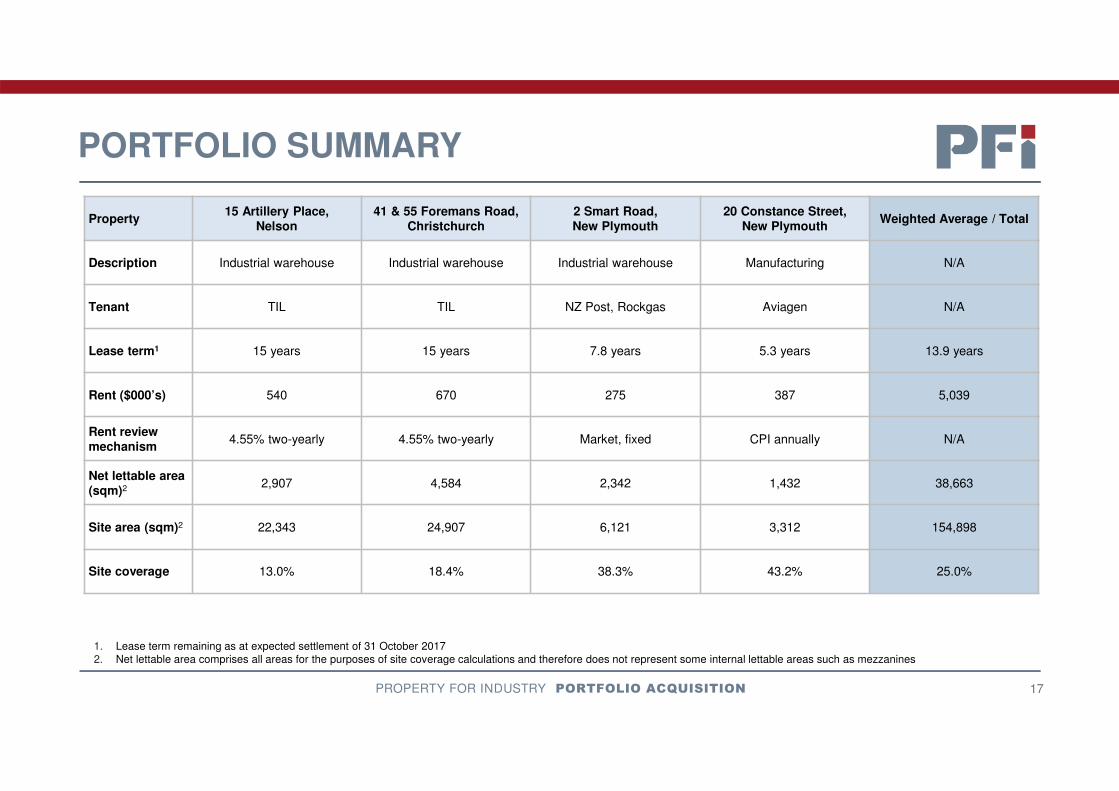

PORTFOLIO SUMMARY

Property15 Artillery Place,

Nelson41 & 55 Foremans Road,

Christchurch2 Smart Road,New Plymouth

20 Constance Street,New Plymouth

Weighted Average / Total

Description Industrial warehouse Industrial warehouse Industrial warehouse Manufacturing N/A

Tenant TIL TIL NZ Post, Rockgas Aviagen N/A

Lease term1 15 years 15 years 7.8 years 5.3 years 13.9 years

Rent ($000’s) 540 670 275 387 5,039

Rent review mechanism

4.55% two-yearly 4.55% two-yearly Market, fixed CPI annually N/A

Net lettable area (sqm)2 2,907 4,584 2,342 1,432 38,663

Site area (sqm)2 22,343 24,907 6,121 3,312 154,898

Site coverage 13.0% 18.4% 38.3% 43.2% 25.0%

PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

1. Lease term remaining as at expected settlement of 31 October 20172. Net lettable area comprises all areas for the purposes of site coverage calculations and therefore does not represent some internal lettable areas such as mezzanines

IMPACT OF THE ACQUISITION

18PROPERTY FOR INDUSTRY PORTFOLIO ACQUISITION

Pre Acquisition1 Acquisition2 Post Acquisition3

Investment properties ($m) 1,096.0 69.8 1,165.8

Number of properties 83 9 92

Number of tenants 144 4 148

Contract rent ($m) 73.2 5.0 78.2

Occupancy 99.5% 100.0% 99.6%

WALT 4.8 years 13.9 years 5.4 years

Industrial property 85.4% 97.9% 86.2%

Auckland property 85.3% 30.0% 81.8%

Passing yield 6.69% 7.22% 6.72%

� The Acquisition will improve a range of PFI’s portfolio metrics:

1. As at 30 June 20172. As at expected settlement of 31 October 20173. Pro forma as at 30 June 2017, under the assumption that the portfolio was acquired on 30 June 2017

EQUITY RAISING OVERVIEW

20PROPERTY FOR INDUSTRY EQUITY RAISING

PFI to raise approximately $70m through a pro rata renounceable rights issue

• 1 for 10 pro rata renounceable rights issue, fully underwritten at an Issue Price of $1.54 per New Share

• Traditional rights issue, with Rights trading, provides all Eligible Shareholders with the opportunity to participate

• PFI Board and senior executives have committed to take up all Rights in respect of their beneficial shareholdings under the

Offer

• The Offer is fully underwritten by Forsyth Barr Group Limited

Purpose of the Offer

• PFI will initially fund the Acquisition via an extension of banking facilities with the proceeds of the proposed Offer being used to

repay debt and reduce gearing

• PFI expects that the post Offer gearing position provides appropriate funding for committed development projects and further

portfolio activity

Impact of the Acquisition and Offer

• Post the Acquisition and the Offer:

• PFI will have pro forma June 2017 gearing of 32.3%1

• PFI continues to provide guidance for distributable profit of between 7.70 and 7.90 cents per share and a cash dividend

of 7.45 cents per share for FY17

1. Based on PFI’s Consolidated Statement of Financial Position as at 30 June 2017. Calculated as the value of borrowings (adjusted for the value of the Acquisition, the proceeds of the Offer and transaction costs) divided by the value of investment properties (adjusted for the value of the Acquisition).

EQUITY RAISING TERMS

21

1. TERP is the theoretical ex-rights price of $1.658 which is equal to the average price of 1 New Share at the Issue Price of $1.54 and 10 Existing Shares at $1.67 being the closing price as at 3 October 2017

Entitlement ratio 1 New Share for every 10 Existing Shares held at 5.00pm on 12 October 2017

Offer size Approximately $70m

Maximum New Shares to be issued

45,338,605

Issue Price $1.54

Offer discount 7.1% to TERP1

RankingNew Shares issued on completion of the Offer will rank equally with Existing Shares and will be quoted on the NZX Main Board

EligibilityAvailable to persons recorded on PFI’s share register on the Record Date, with a registered address in New Zealand or Australia (Eligible Shareholders)

Options for Eligible Shareholders

Each Eligible Shareholder may choose to take up all or some of your Rights, sell all or some of your Rights on market, take up some of your Rights and sell all or some of your balance on market or do nothing with all or some of your Rights. If you do nothing, your Rights will lapse and you will not be able to subscribe for any New Shares or realise any other value for your Rights

The PFI Board encourages you to either take up your Rights in full or sell your Rights on market

PROPERTY FOR INDUSTRY EQUITY RAISING

TIMETABLE1

22

Announcement of the Offer 4 October 2017

Rights trading commences on the NZX Main Board 11 October 2017

Record Date for determining Entitlements 5.00 pm, 12 October 2017

Offer Document, Entitlement and Acceptance Forms sent to Eligible Shareholders 13 October 2017

Rights trading ends on the NZX Main Board 5.00 pm, 26 October 2017

Closing Date for the Offer (last day for receipt of the completed Entitlement and

Acceptance Form with payment)1 November 2017

Allotment of New Shares under the Offer (Issue Date) 7 November 2017

Expected date for quotation of New Shares issued under the Offer 7 November 2017

Mailing of holding statements By 13 November 2017

1. These dates are subject to change and are indicative only. PFI reserves the right to amend this timetable (including by extending the Closing Date of the Offer) subject to applicable laws and the Listing Rules

PROPERTY FOR INDUSTRY EQUITY RAISING

DISCLAIMER

24

IMPORTANT NOTICE

The information included in this presentation is provided by Property For Industry Limited (PFI) as at 4 October 2017 and is provided in relation to a pro rata renounceable Rights Offer of New Shares in PFI to be made to Eligible Shareholders under clause 19 of Schedule 1 of the Financial Markets Conduct Act 2013 (New Shares).

PFI does not guarantee the repayment of capital or the performance referred to in this presentation.

Information

This presentation contains summary information about PFI and its activities which is current as at the date of this presentation. The information in this presentation is of a general nature and does not purport to be complete nor does it contain all the information which a prospective investor may require in evaluating a possible investment in PFI or that would be required in a product disclosure statement under the Financial Markets Conduct Act 2013. Any historical information in this presentation is, or is based upon, information that has been released to NZX Limited (NZX). This presentation should be read in conjunction with PFI’s periodic and continuous disclosure announcements, which are available at www.nzx.com.

This presentation is for information purposes only and is not an invitation or offer of securities or financial products for subscription, purchase or sale in any jurisdiction. Any decision to acquire New Shares should be made on the basis of the separate offer document to be lodged with NZX (the Offer Document). Any Eligible Shareholder who wishes to participate in the Offer should review the Offer Document and apply in accordance with the instructions set out in the Offer Document and the Entitlement and Acceptance Form accompanying the Offer Document. The Offer is only made to Eligible Shareholders, being Shareholders with a registered address in New Zealand or Australia (who are not in the United States and that are not acting for the account or benefit of a person in the United States). This presentation and the Offer Document do not constitute an offer, advertisement or invitation in any place in which, or to any person to whom, it would not be lawful to make such an offer, advertisement or invitation.

NZX

The New Shares have been accepted for quotation by NZX and will be quoted on the NZX Main Board after the completion of the allotment process. The NZX Main Board is a licensed market under the Financial Markets Conduct Act 2013. NZX accepts no responsibility for any statement in this presentation.

Australia

This document and the offer of New Shares are being made available in Australia in reliance on the Australian Securities and Investments Commission Corporations (Foreign Rights Issues) Instrument 2015/356.

PROPERTY FOR INDUSTRY DISCLAIMER

This document is not a prospectus, product disclosure statement or any other formal “disclosure document” for the purposes of the Australian Corporations Act 2001 ("Australian Corporations Act") and is not required to, and does not, contain all the information which would be required in a "disclosure document" under the Australian Corporations Act. This document has not been, and will not be, lodged or registered with the Australian Securities and Investments Commission or the Australian Securities Exchange and the issuer is not subject to the continuous disclosure requirements that apply in Australia.

Prospective investors should not construe anything in this document as legal, business or tax advice nor as financial product advice for the purposes of Chapter 7 of the Australian Corporations Act.

Past Performance

Past performance is not a reliable indicator of future performance.

Future Performance

The presentation includes a number of forward looking statements. Forward looking statements, by their nature, involve inherent risks and uncertainties. Many of those risks and uncertainties are matters which are beyond PFI’s control and could cause actual results to differ from those predicted. Variations could either be materially positive or materially negative. Except as required by law or regulation, PFI undertakes no obligation to provide any additional or updated information whether as a result of new information, future events or results or otherwise.

Not Financial Advice

This presentation has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this presentation, and seek professional advice, having regard to the investor’s objectives, financial situation and needs.

Disclaimer

None of Forsyth Barr Limited (the Lead Manager), Forsyth Barr Group Limited (the Underwriter), PFI’s advisers nor any of their respective affiliates, related bodies corporate, directors, officers, partners, employees and agents (the Associated Persons), have authorised or cause the issue or provision of this presentation and, except to the extent set out in this presentation, none of them makes or purports to make any statement in this presentation and there is no statement which is based on any statement by any of them. To the maximum extent permitted by law, PFI, the Lead Manager, the Underwriter and the Associated Persons exclude and disclaim all liability for any expenses, losses, damages or costs incurred in respect of the Offer and any decision to acquire New Shares. The Lead Manager, the Underwriter and the Associated Persons make no representation or warranty as to the information in this presentation and make no recommendation as to whether any person should participate in the Offer.

Note

All capitalised terms used in this presentation have the meanings given in the Glossary of PFI’s Offer Document dated 4 October 2017.