2018 clarivate/cortellis year in review · 2018 clarivate/cortellis year in review analysis...

TRANSCRIPT

2018 Clarivate/Cortellis Year in Review

Analysis premiered during the JP Morgan WeekSan Francisco, California7-10 January 2019

2

Presenters

Jamie Munro leads the Portfolio & Licensing practice at Clarivate Analytics including heading up CMRInternational, the R&D benchmarking service. Dr Munro has significant life science experience including over 15years large pharma experience as well as a PhD in Finance.

Helen Dowden is a strategic intelligence professional with more than 20 years pharmaceutical industry experience. She has a PhD in pharmacology, and is currently working as a Consultant within Clarivate’s Life Sciences Professional Services team. Helen has expertise in oncology deals analysis.

3

Contributors

Laura Vitez has over 25 years of experience in the life sciences industry. She has held lead or advisory roles at multiple small biotechs, a mid-sized pharma company, and two consulting firms, bringing in over $2B deal dollars. She holds an MS in biochemistry and a BA in mathematics and chemistry.

Lisa Christadore has 5+ years consulting with pharmaceutical clients across R&D, clinical, competitive intelligence, and BD. She has interviewed over 100 physicians, scientists, and investors and works closely with Clarivate’s Deals Intelligence team. She is a medical writer, deals enthusiast, and holds a PhD in Biochemistry with a focus on drug discovery.

Isabel Rodriguez has over 15 years of experience in the pharmaceutical business from early discovery research to the clinical practice, and works with clients on a range of assignments including the analysis of disease landscape, competitive intelligence, business development and licensing, disease target evaluation, technology assessment and intellectual property trends. Isabelholds a Doctorate in Pharmacy from the University of Barcelona.

Paul D’Souza has over 11 years as a pharmaceutical industry analyst, maintaining and analysing content on various competitive intelligence databases, including Clarivate Analytics’ Cortellis Deals Intelligence module, to support decision making across the pharmaceutical sector. He currently analyses quarterly trends in pharmaceutical mergers & acquisitions and licensing activity and holds an MBA and a BSc in Pharmacology & Physiology.

Karen Pihl-Carey is an analyst and writer for BioWorld who has tracked the biopharma industry since 1999. She manages databases of deals, financings, FDA approvals and clinical data that provide historical background and indicate industry trends.

4

Contents

Introductions 2

Recap of 2017 implications 7

Dealmaking 2018 Year-in-Review 8

Overview 9

Mergers and Acquisitions (M&A) 11

Licensing, Joint Ventures, and Research Collaborations 16

IPOs and VC 25

Top Pharma Dealmaking Activity 29

Biopharma Industry 2018 Year-in-Review 33

Oncology: Still the biggest driver of deal activity 34

Approvals and Other Drivers of ROI 45

Summary 62

5

Clarivate Analytics Life Sciences

Clarivate Analytics is the global leader in providing trusted insights and analytics to accelerate the pace of innovation.

Building on a heritage going back more than a century and a half, we have built some of the most trusted brands across the innovation lifecycle, including Web of Science, Cortellis, Derwent, Techstreet, CompuMark, and MarkMonitor.

Today, Clarivate Analytics is a new and independent company on a bold entrepreneurial mission to help our clients radically reduce the time from new ideas to life-changing innovations.

Cortellis Competitive IntelligenceLeading pipeline database for depth and breadth of content

Cortellis Deals IntelligenceRapid insights into critical deal making trends

Cortellis Regulatory IntelligenceMost comprehensive regulatory content and analysis

Cortellis Clinical Trials IntelligenceBroadest source of clinical trials intelligence

MetaCoreProprietary toolbox for discovery of biological pathways

Integrity & Drug Research AdvisorUnique provider of multifaceted drug research content

BioWorld NewsDaily actionable intelligence and incisve analysis

This report contains general information only and is based on the experiences and research of Clarivate Analytics practitioners. Clarivate Analytics is not, by means of this report, rendering business, financial, investment, or other professional advice or services. This report is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Clarivate Analytics, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this report.

Disclaimer

7

o Industry continues to innovate & will need to continue

Targeted therapies addressing unmet need

Oncology to remain a focal point

Challenges for NS, anti-infectives

o Challenges remain

Value generation

o Levers

Revenues – price challenges

Costs – hurdles

Pick winners – long term, beyond the tenure of many CEOs

Business development

• M&A – tax / repatriation

• Licensing to fill gaps and deliver strategy

• Regional opportunities / China

Let’s take a look at what we said last year…

Dealmaking 2018

Year-in-Review

9

M&A11%

Licenses41%

Asset Purchases

5%

Funding18%

Commercial14%

Other10%

Service1%

M&A64%

Licenses26%

Asset Purchases

5%

Overview of all life sciences deals captured by Cortellis in 2018 by percentage

4014Total transactions

announced in 2018

$428 BTotal deal dollars

announced in 2018

• Unless otherwise noted, all dollars throughout presentation are USD and are nominal figures (not corrected for inflation).• Transaction types: M&A = 50-100% acquisitions, mergers, reverse mergers; Licenses = licenses, joint ventures, research

collaborations; Asset Purchases = products and business unit acquisitions; Funding = acquisitions of < 50% equity, grants, loans, other funding types; Commercial = distribution, supply, co-promotion agreements; Service = contract services; Other = royalty buyouts, spin-outs, settlements.

Funding 15%; Commercial 2%; Service 0.2%; Other 1.2%

10

M&A, 482 M&A, 449

Licenses, 1811

Licenses, 1658

Asset Purch, 210 Asset Purch,

184

Funding, 941

Funding, 734

Commercial, 563

Commercial, 560

Service, 465

Service, 376

Other, 50

Other, 53

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2017 2018

Volume

M&A, $256M&A, $276

Licenses, $88

Licenses, $111

Asset Purch, $33

Asset Purch, $22

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2017 2018

Announced $ billion

All life sciences deals in 2018 vs. 2017 by number and total deal size $ billion

4014

4522 $428 B$392 B

** Funding $6.0 (2017), $14.9 (2018); Commercial $24.0, $2.0; Service <$0.1, $0.2; Other (royalty buy-out, spin-out, settlement) $4.4, $1.2.

**

**

2018 Dealmaking

Year-in-Review

Mergers and Acquisitions (M&A)

12

Ten years of life sciences M&A transactions (adjusted $)

*Dollars are adjusted for inflation. Chart Includes all announced M&As plus four mega Asset Purchase transactions: Nestle/Pfizer Nutrition (2012), Novartis/GlaxoSmithKline Oncology (2014), Bayer/Merck Consumer Care (2014), Teva/Allergan Generics (2015).

254293 277 261

351

443

489

561

482449

$125 $122

$157

$94

$124

$347

$276

$239

$262

$276

$0

$50

$100

$150

$200

$250

$300

$350

$400

0

100

200

300

400

500

600

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Agg

rega

te a

nn

ou

nce

d $

bill

ion

No. transactions

Aggregate M&A $ billion*

13

Top twenty M&As of 2018 by total size

14

0

10

20

30

40

50

60

No

. M&

A t

ran

sact

ion

s

Volume breakdown by Rx Area 2018 vs. 2017

2017

2018

2017 vs. 2018 M&As by known therapeutic focus

Analysis covers M&A transactions with an identifiable core therapeutic focus.

Not shown:

TAs for which there

were ≤5 M&As

announced in 2018:

• Immune

• Toxicity

• Inflammatory

15

Ten years of life sciences megamergers (nominal $)

$68.0

$49.6

$20.1 $19.7

$13.7

$29.1

$11.2 $11.9 $13.6

$25.0

$16.0 $13.4 $14.2

$42.9

$17.0

$12.2

$66.0

$17.0

$11.1

$20.8

$40.5

$32.0

$10.4

$23.6

$66.0

$14.3

$30.2

$16.6

$24.2

$11.9

$69.0

$11.6

$67.0

$13.0

$62.3

$0

$10

$20

$30

$40

$50

$60

$70

$80

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

$ b

illio

n

Year

Announced M&A deals > $10 billionYear Partner/Prinicpal

2009Pfizer/Wyeth

Merck/Schering-Plough

2010 Sanofi/Genzyme

2011

J&J/Synthes

Takeda/Nycomed

Express Scripts/Medco

Gilead/Pharmasset

2012 Nestle/Pfizer Nutrition

2013 Thermo Fisher/Life Tech

2014

Allergan (fka Actavis)/Forest

Novartis/GSK oncology products

Zimmer/Biomet

Bayer/Merck Consumer Care

Medtronic/Covidien

Merck/Sigma-Aldrich

BD/Carefusion

Actavis/Allergan

2015

Pfizer/Hospira

Valeant/Salix

AbbVie/Pharmacyclics

Teva/Allergan Generics

Shire/Baxalta

2016

AbbVie/Stemcentrx

Abbott/St Jude

Bayer/Monsanto

Pfizer/Medivation

2017

J&J/Actelion

Reckitt Benckiser/Mead Johnson

BD/C R Bard

Gilead/Kite

CVS/Aetna

2018

Sanofi/Bioverativ

Cigna/Express Scripts

GSK/Novartis consumer HC

Takeda/ShireDollars are the announced nominal values, not adjusted for inflation.

2018 Dealmaking

Year-in-Review

Licenses, Joint Ventures, and Research Collaborations

17

$25.27$25.72

$11.59

$22.32

$18.16$16.47

$25.31

$31.66

$20.62

$26.24$24.31

$25.58

$20.33

$13.39

$27.80$28.55

$32.32

$17.02

$22.03

$40.04

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

0

100

200

300

400

500

600

Agg

rega

te a

nn

ou

nce

d d

eal

do

llars

($

B)*

No

. an

no

un

ced

tra

nsa

ctio

ns

No. announced transactions Aggregate announced $B (adjusted)

Five years of licensing and collaborations by quarter (adjusted $)

*Dollars are adjusted for inflation. Chart includes all announced License, Joint Venture, and Research-Only collaborations.

2014 2015 2016 2017 2018

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

18

Ten years of average and median total license size (adjusted $)

* Dollars are adjusted for inflation.. Chart includes all announced License, Joint Venture, and Research-Only collaborations.

$231

$251

$196$204

$225

$330

$281

$330

$293

$371

$63

$40 $36 $31 $33

$51

$80$87

$67

$101

$0

$50

$100

$150

$200

$250

$300

$350

$400

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

$ m

illio

n*

No

. an

no

un

ced

tra

nsa

ctio

ns

No. announced transactions Average (Inflation-adjusted) $M Median (Inflation-adjusted) $M

19

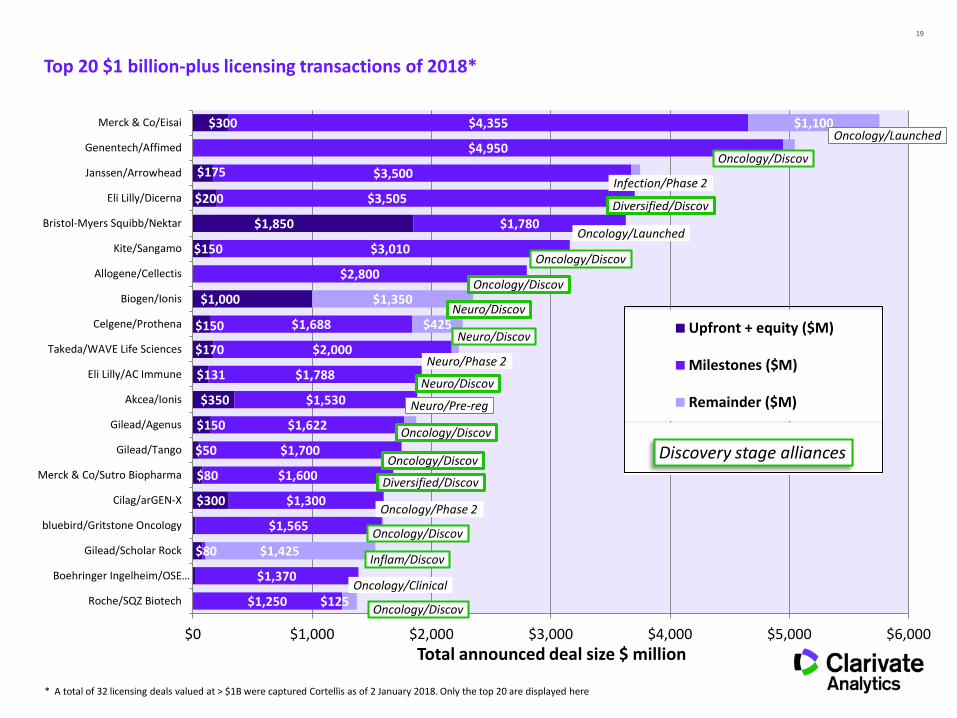

Top 20 $1 billion-plus licensing transactions of 2018*

$80

$300

$80

$50

$150

$350

$131

$170

$150

$1,000

$150

$1,850

$200

$175

$300

$1,250

$1,370

$1,565

$1,300

$1,600

$1,700

$1,622

$1,530

$1,788

$2,000

$1,688

$2,800

$3,010

$1,780

$3,505

$3,500

$4,950

$4,355

$125

$1,425

$425

$1,350

$1,100

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000

Roche/SQZ Biotech

Boehringer Ingelheim/OSE…

Gilead/Scholar Rock

bluebird/Gritstone Oncology

Cilag/arGEN-X

Merck & Co/Sutro Biopharma

Gilead/Tango

Gilead/Agenus

Akcea/Ionis

Eli Lilly/AC Immune

Takeda/WAVE Life Sciences

Celgene/Prothena

Biogen/Ionis

Allogene/Cellectis

Kite/Sangamo

Bristol-Myers Squibb/Nektar

Eli Lilly/Dicerna

Janssen/Arrowhead

Genentech/Affimed

Merck & Co/Eisai

Upfront + equity ($M)

Milestones ($M)

Remainder ($M)

Oncology/Launched

Oncology/Discov

Infection/Phase 2

Oncology/Launched

Neuro/Discov

Oncology/Discov

Diversified/Discov

Neuro/Phase 2

Neuro/Discov

Neuro/Pre-reg

Oncology/Discov

Oncology/Phase 2

Oncology/Discov

Inflam/Discov

Oncology/Clinical

Oncology/Discov

Discovery stage alliances

Total announced deal size $ million

Diversified/Discov

Oncology/Discov

Neuro/Discov

Oncology/Discov

* A total of 32 licensing deals valued at > $1B were captured Cortellis as of 2 January 2018. Only the top 20 are displayed here

20

$0

$10

$20

$30

$40

$50

$60

25th Percentile Median 75th Percentile Average

$ m

illio

n*

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ten-year trend in upfront cash license payments (adjusted $)

* Dollars are adjusted for inflation. Chart includes all announced License, Joint Venture, and Research-Only collaborations that reported an upfront cash payment. (2017 data exclude Merck/AstraZeneca and Biogen/Forward)

2018 upfront cash

25th percentile $3 M

Median $10 M

75th percentile $40 M

Average $38 M

21

Top 20 upfront cash payments in 2018 licensing transactions

Rank Licensee Licensor Upfront $M Stage Rx Area

1 Bristol-Myers Squibb Nektar $1,000 Approved Oncology

2 United Therapeutics Arena $800 Phase 3 Cardiovascular

3 Biogen Ionis $375 Discovery Neurology

4 Merck & Co. Eisai $300 Approved Oncology

5 Cilag (J&J) arGEN-X $300 Phase 2 Oncology

6 Janssen Arrowhead $175 Phase 2 Infection

7 Kite Pharma Sangamo $150 Discovery Oncology

8 Akcea Therapeutics Ionis $150 Pre-registration Neurology

9 Sanofi Denali $125 Phase 1 Neurology & Autoimm/Inflam

10 Gilead Agenus $120 Discovery Oncology

11 EUSA Janssen $115 Approved Immune

11 Takeda WAVE Life Sciences $110 Phase 2 Neurology

11 Novartis Spark Therapeutics $105 Registered Ophthalmologic

14 Eli Lilly Dicerna $100 Discovery Cardiovascular & Neurology

15 Celgene Prothena $100 Discovery Neurology

16 Janssen Theravance $100 Phase 1 Gastrointestinal

17 AbbVie Morphic Therapeutics $100 Discovery Autoimm/Inflam

18 Shionogi SAGE Therapeutics $90 Phase 2 Neurology

19 Eli Lilly AC Immune $81 Discovery Neurology

20 Roche Ionis $75 Phase 2 Ophthalmologic

22

2018 licenses by therapeutic area

Cancer, 515

Neurology/Psychiatric, 183

Infection, 129

Diversified, 91

Endocrine/Metabolic, 63

Gastrointestinal, 63

Dermatologic, 39

Cardiovascular, 37

Other/Miscellaneous, 34

Ocular, 34

Immune, 33

Genitourinary/Sexual Function, 30Inflammatory, 25Musculoskeletal, 23

Hematologic, 17 Respiratory, 17 Toxicity/Intoxication, 13

Chart includes all announced License, Joint Venture, and Research-Only collaborations where a Therapy Area is defined

23

Deal-making by Chinese companies dwarfed by US but showing robust growth

Country refers to company HQ location. Includes all announced License, Joint Venture, and Research-Only collaborations.

-10

10

30

50

70

90

China

China Principal (sell) China Partner (Buy)

China/China

-10

10

30

50

70

90

Japan

Japan Principal (Sell) Japan Partner (Buy)

Japan/Japan

-10

10

30

50

70

90

South Korea

S Korea Principal (Sell) S Korea Partner (Buy)

S Korea/S Korea

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USA

USA/USA Inter-country

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USA

USA Principal (Sell) USA partner (Buy)

24

Notable China inter-regional buy-side deals in 2018 – aimed at access to innovative meds in China

Sellside Buyside DateTotal

(Upfront)Asset/Technology

Phase of lead asset

Zymeworks(Canada)

BeiGene 05/2018 $722 ($20)Rights to Azymetric and EFECT platforms to develop and commercialize up to

three other bispecific antibodies worldwideDiscovery

AstraZeneca(UK)

Luye Pharma Group

01/2018 $546 ($260)Sale and license of rights to Seroquel and Seroquel XR in UK, China and other

international marketsLaunched

Zymeworks(Canada)

BeiGene 02/2018 $430 ($40)Develop and commercialize ZW-25 and ZW-49 HER2-targeted bispecific

antibodies in Asia (excl. Japan), Australia & New ZealandPhase I

Agios(US)

C-Stone Pharmaceuticals

06/2018 $424 ($12)Develop and commercialize ivosidenib (Tibsovo, AG-120) for AML and

cholangiocarcinoma in China, Hong Kong, Macau and TaiwanPre-

registration

Incyte (US)

Innovent Biologics 12/2018 $392 ($40)Develop and commercialize pemigatinib, itacitinib and parsaclisib in

hematology and in China, Hong Kong, Macau and TaiwanPhase III

Blueprint(US)

C-Stone Pharmaceuticals

06/2018 $386 ($40)Develop and commercialize avapritinib , BLU-554 and BLU-667 for cancers in

China, Hong Kong, Macau and TaiwanPhase III

Revance(US)

Shanghai FosunPharmaceutical

12/2018 $260 ($30)Develop and commercialize DaxibotulinumtoxinA (RT-002) against aesthetic and

neuroscience conditions in China, Hong Kong and MacauPhase III

Puma (US)

CANbridge 01/2018 $255 ($30)Develop and commercialize Nerlynx (neratinib oral) against cancer in China,

Taiwan, Hong Kong and MacauLaunched

Verastem(US)

CSPC Pharmaceutical 09/2018 $175 ($15)Develop and commercialize products containing duvelisib in China, Hong Kong,

Macau and Taiwan for all oncology indicationsLaunched

MacroGenics(US)

Zai Lab 11/2018 $165 ($25)Develop and commercialize three I-O programs margetuximab , MGD-019 and

MGD-013 in China, Hong Kong, Macau and TaiwanPhase III

Karyopharm(US)

Antengene 05/2018 $162 ($12)Develop and commercialize selinexor, eltanexor and KPT-9274 for oncology, and

verdinexor for non-oncology in various Asian countriesPhase III

Adocia(France)

Tonghua Dongbao 04/2018 $135 ($50)Develop, manufacture and commercialize BioChaperone Combo and Lispro for

diabetes in China and other designated countriesPhase II

Mirati(US)

BeiGene 01/2018 $133 ($10)Develop, manufacture and commercialize sitravatinib in Australia, New Zealand

and Asia excl. JapanPhase II

VBI Vaccines(US)

Brii Biosciences 12/2018 $128.5 ($4)Develop recombinant, protein-based immuno-therapeutic, VBI-2601 against

chronic HBV in China, Hong Kong, Taiwan and MacauDiscovery

Tocagen(US)

ApolloBio 04/2018 $127 ($16)Develop and commercialize Toca-511 against high-grade glioma (HGG) in

China, Hong Kong, Macau and TaiwanPhase III

2018 Dealmaking

Year-in-Review

IPOs and VC

26

Biopharma IPOs – significant uptick in last 5 years

Source: BioWorld (data current as of end of November 2018)

$0.00

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

$6,000.00

$7,000.00

$8,000.00

$9,000.00

0

10

20

30

40

50

60

70

80

90

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Number of financings Year total ($M)

27

Biopharma VC investment also shows strong growth

Source: BioWorld (data current as of end of November 2018)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Number of financings Year total ($M)

28

China begins to emerge as a centre for VC investment in recent years

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Tota

l rai

sed

($

M)

No

. fin

anci

ngs

China # USA # Europe # China $ (M) USA $ (M) Europe $ (M)

Source: BioWorld (data current as of end of November 2018)

2017 Dealmaking

Year-in-Review

Top Pharma Dealmakers

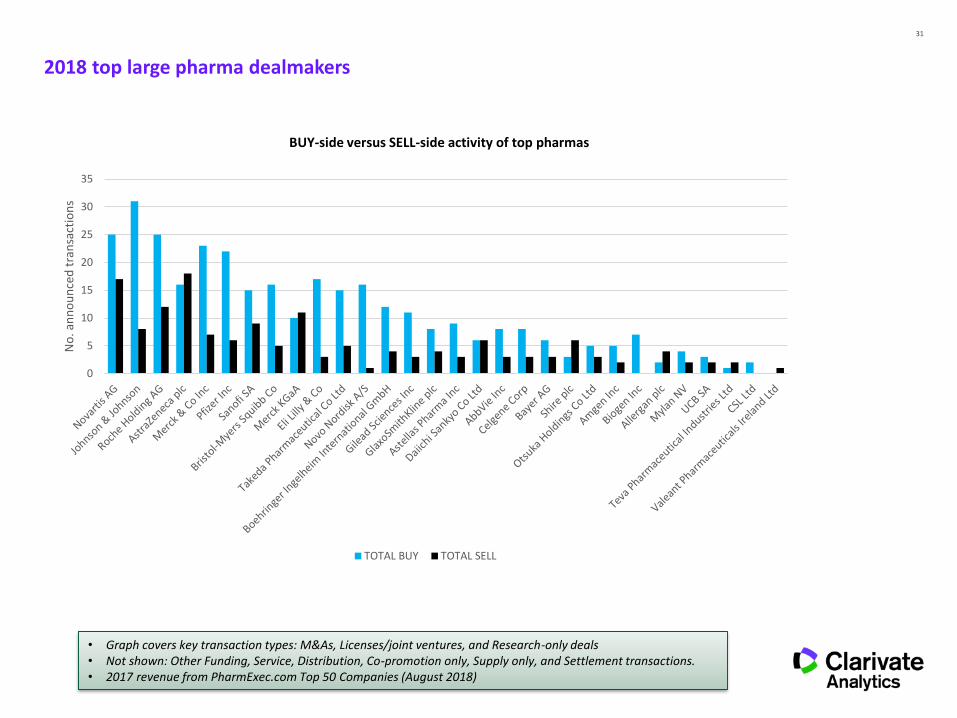

30

2018 top large pharma dealmakers

• Graph covers key transaction types: M&As, Licenses/joint ventures, and Research-only deals• Not shown: Other Funding, Service, Distribution, Co-promotion only, Supply only, and Settlement transactions.• 2017 revenue from PharmExec.com Top 50 Companies (August 2018)

Deal-making volume in 2018 vs. 2017 revenues and R&D spend for the top 30 pharma companies

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

0

5

10

15

20

25

30

35

40

Pfi

zer

Inc

No

vart

is A

G

Ro

che

Ho

ldin

g A

G

Mer

ck &

Co

Inc

Joh

nso

n &

Jo

hn

son

San

ofi

SA

Gla

xoSm

ith

Klin

e p

lc

Ab

bV

ie In

c

Gile

ad S

cien

ces

Inc

Am

gen

Inc

Ast

raZe

nec

a p

lc

Bri

sto

l-M

yers

Sq

uib

b C

o

Eli L

illy

& C

o

Teva

Ph

arm

ace

uti

cal I

nd

ust

rie

s Lt

d

Bay

er A

G

No

vo N

ord

isk

A/S

Alle

rgan

plc

Shir

e p

lc

Bo

eh

rin

ger

Inge

lhe

im In

tern

atio

nal

…

Take

da

Ph

arm

aceu

tica

l Co

Ltd

Cel

gen

e C

orp

Myl

an N

V

Ast

ella

s P

har

ma

Inc

Bio

gen

Inc

CSL

Ltd

Dai

ich

i San

kyo

Co

Ltd

Mer

ck K

GaA

Ots

uka

Ho

ldin

gs C

o L

td

Val

ean

t P

har

mac

eu

tica

ls Ir

elan

d L

td

UC

B S

A

$ m

illio

n

No

. an

no

un

ced

tra

nsa

ctio

ns

TOTAL LicJVRsch TOTAL M&A TOTAL OTHER 2017 Revenue ($M) 2017 R&D spend ($M)

31

2018 top large pharma dealmakers

• Graph covers key transaction types: M&As, Licenses/joint ventures, and Research-only deals• Not shown: Other Funding, Service, Distribution, Co-promotion only, Supply only, and Settlement transactions.• 2017 revenue from PharmExec.com Top 50 Companies (August 2018)

BUY-side versus SELL-side activity of top pharmas

0

5

10

15

20

25

30

35

No

. an

no

un

ced

tra

nsa

ctio

ns

TOTAL BUY TOTAL SELL

32

2018 therapy area focus for top large pharma dealmakers

• Covers announced total deal size for key transactions types, M&As, Licenses/joint ventures, Research-only deals, and Other (Asset Purchases, Equity Stakes, Spin-outs), with identifiable therapeutic focus areas.

• Not shown: Toxicity, Unknown and Not Applicable therapy areas. • Diversified total does not include Takeda/Shire acquisition (Total for Diversified is $92,934 with deal included).• Companies are the Top 30 in terms of 2017 revenue (derived from PharmExec.com Top 50 Companies, August 2018)

Biopharma Industry 2018 Year-in-Review

2018 Biopharma Industry

Year-in-Review

Oncology

35

Oncology represents the greatest activity in deal making

Number of buy-side transactions by therapy area for top pharma dealmakers

• Covers key transactions types, M&As, Licenses/joint ventures, Research-only deals, and Other (Asset Purchases, Equity Stakes, Spin-outs), with identifiable therapeutic focus areas.

• Covers all technologies.• Not shown: Other, Genitourinary, Musculoskeletal, Toxicity, Unknown and Not Applicable therapy area deals. • Companies are the top 30 pharmas as ranked by 2017 revenues.

J&J

Me

rck

No

vart

is A

G

Ro

che

Eli L

illy

& C

o

Take

da

San

ofi

AZ

No

vo N

ord

isk

Pfi

zer

BI

Ab

bV

ie

Gil

ead

Ast

ell

as

Bio

gen

Me

rck

KG

aA

Ce

lge

ne

Dai

ich

i San

kyo

GSK

Am

gen

Bay

er

BM

S

Myl

an

Ots

uka

All

erg

an

CSL

Shir

e

UC

B

Teva

TOTA

L

Oncology 9 17 8 12 2 3 3 9 6 4 5 5 3 7 1 6 1 2 1 1 3 108

Neuroscience 6 1 3 3 3 3 1 1 1 2 1 7 3 2 1 2 40

Immuno/Inflam 2 1 4 1 1 1 1 2 1 1 1 1 1 1 1 1 1 1 23

Endo/Met 2 3 1 8 1 1 16

Infection 1 1 1 2 5 1 1 2 1 1 16

Diversified 1 3 1 2 3 1 1 1 13

GI 2 1 4 1 1 9

Dermatology 3 1 1 5

Hematology 1 2 1 1 5

Ophthalm 3 1 1 5

Respiratory 1 1 1 1 1 5

Cardiology 1 2 1 4

Total 27 20 20 18 14 14 13 12 12 12 9 8 8 7 7 7 6 6 6 3 3 3 3 3 2 2 2 2 0 222

36

Clarivate’s data and methodologies for oncology transactions

All announced business transactions were extracted from Cortellis for Deals Intelligence database between January 2014 and end of 2018 in the following categories:

• M&As - 183

• Licenses, Joint Ventures and Research Collaborations – 2,483

Unless otherwise noted the analysis focuses only on deals aimed at therapeutics:

• Included: Small molecules (MTT), Biologics (mAbs, siRNA, peptides, etc), Cell therapies, Vaccines, Gene therapies.

• Excluded: Medical devices, Diagnostics , Biomarkers, Discovery Technology, Software, Generics, OTC products.

37

Small molecule, 705

Antibodies, 491

DNA/RNA/Oligonucleotide/Gene & Cell

therapy/Oncolytic virus/Other cancer

vaccines, 401

Proteins/peptides, 68 Other , 14

$331 billion aggregate deal dollars in oncology announced since 2014; 64% of the deals are focused on therapeutic assets

• Source: Cortellis Deals Intelligence.• Covers key transactions types with an identifiable technologies; all included.

GSK Novartis asset purchase not included

Therapeutic, 1703

Biomarkers/Diagnostics/Imaging, 495

Genomics/Other Drug Discovery

Technologies, 235

Devices, 80

Instruments/Software/Service, 79

Generic/Biosimilar/OTC, …

Formulation, 36Other, 11

Breakdown of Therapeutic asset deals

Oligonucleotides/Gene & cell therapy/Cancer vaccines, 401

38

In 2018, both large and small pharma are active participants oncology licensing

In-licensing activity for big pharma (95 total deals; $31.8 billion total value)

Licensee/Licensor Total/Upfront Notable Assets Phase Indication

Merck & Co./Eisai $5.8 B/$300 M pembrolizumab, lenvatinib Launched Broad cancer focus

Roche/Affimed $5.0 B/unspecified NK cell engager-based immunotherapies Discovery Broad cancer focus

Bristol-Myers Squibb/Nektar $3.6 B/$1000 M Nivolumab, ipilimumab, NKT-214 Launched Broad cancer focus

Gilead/Sangamo Therapeutics $3.2 B/$150 M Cell therapies using zinc finger tech. Discovery Broad cancer focus

Gilead/Agenus $1.9 B/$120 M I-O therapies incl. AGEN-1423 Discovery Broad cancer focus

Gilead/Tango Therapeutics $1.8 B/$50 M I-O therapies Discovery Broad cancer focus

Cilag (J&J)/arGEN-X $1.6 B/$300 M cusatuzumab Ph II AML, MDS

Boehringer Ingelheim/OSE $1.4 B/$18 M OSE-172 Clinical Solid tumors

Roche/SQZ Biotech $1.4 B/$125 M Antigen-presenting cell-based therapies Discovery Broad cancer focus

Janssen/Yuhan $1.3 B/$50 M lazertinib Ph II NSCLC

Notable activity for smaller biotechnology (246 total deals; $17.6 billion total value )

Licensee/Licensor Total/Upfront Notable assets Phase Indication

Allogene/Cellectis $2.8 B/unspecified UCAR-T cell therapies Discovery Broad cancer focus

Bluebird/Gritstone $1.6 B/$20 M Cell therapies using EDGE tech. Discovery Broad cancer focus

Oncologie/Mologen $1.3 B/$4 M lefitolimod Registered Broad cancer focus

ONO/Fate Therapeutics $1.3 B/$10 M CART-cell therapies Discovery Broad cancer focus

Seattle Genetics/Pieris $1.2 B/$30 M Bispecific antibody-anticalin fusion proteins Discovery Broad cancer focus

LG Chem/Cue Biopharma $1.1 B/$5 M CUE-101 Discovery Broad cancer focus

AML = acute myeloid leukemia; MDS = myelodysplastic syndromes; NSCLC = non-small cell lung cancer

Includes therapeutic-focused deals with oncology as a major focus

39

Early-phase small molecules make up largest percentage of oncology deals and significant portion of total value

Includes M&A, Licensing, Joint venture, Research only and significant Asset Purchase deals (2014-2018).Excluded: Medical devices, Diagnostics , Biomarkers, Discovery Technology, Software, Generics, OTC products. Excluded: Deals where stage of asset at signing is “Launched” or unknown.

No. oncology deals Total announced value ($M)

Discovery Phase 1 Phase 2 Phase 3 Pre-reg/Reg

818

139

228

12041

$124,386

$18,417

$45,115

$12,366

$15,858

40

Increase in oncology licensing at large pharma companies is driven in part by greater overall deal activity

Upfront payment trends ($M) Total deal size trends

2014 2015 2016 2017 2018

Number of deals 36 45 36 22 25

Includes Licensing, Joint venture, Research only deals where deal terms disclosed..Excluded: Medical devices, Diagnostics , Biomarkers, Discovery Technology, Software, Generics, OTC products.

$0

$100

$200

$300

$400

$500

$600

$700

$800

2014 2015 2016 2017 2018

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Med

ian

Dea

l Val

ue

ran

ge (

$M

)

Tota

l an

d M

ax D

eal V

alu

e ra

nge

($

M)

Max Deal Value ($M) Total Deal Value ($M) Median Deal Value ($M)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2014 2015 2016 2017 2018

$0

$10

$20

$30

$40

$50

$60

Tota

l an

d M

ax U

pfr

on

t ra

nge

($

M)

Med

ian

Up

fro

nt

ran

ge (

$M

)

Max Upfront ($M) Total Upfront ($M) Median Upfront ($M)

41

$2.8 billion paid upfront; $26 billion downstream for top 10 oncology licensing deals by size in 2018

Source: Cortellis. press releases

Licensee Licensor DateTechnology/

Mechanism of actionTotal$M

Upfront1

$MDownstream fees and terms

Merck & Co. Eisai 03/2018 PD-1/lenvatinib I-O combination 5,755 300

$650 millionOption rights through 2020

$450 millionReimbursement for R&D expenses

$385 million Regulatory and sales milestones

$3,970 millionSales milestones associated with Lenvima

Roche Affimed 08/2018NK cell engager-based immunotherapeutics

5,046 ND

$250 millionDevelopment milestones

$1,100 millionOn receipt of regulatory approvals

$3,600 millionSales milestones Tiered royalties

Bristol-Myers Squibb

NektarTherapeutics

02/2018 PD-1/NKT-214 I-O combination 3,6301,000

(plus 850 equity)

$1,430 million Development and regulatory milestones

$350 millionSales milestones

Kite Pharma (Gilead)

SangamoTherapeutics

02/2018Engineered cell therapies using zinc finger nuclease technology platform

3,160 150

$1,260 millionResearch, development and first commercial sale milestones

$1,750 millionSales-based milestones if annual worldwide net sales reach.$455 million

Allogene Cellectis 04/2018Allogeneic UCAR-T cell therapy

programs 2,800 ND

$185 million per target for 15 targets Tiered royalties in the high single digits on net sales of any products

commercialized by Allogene

Gilead Agenus 12/2018 I-O therapies incl. AGEN-1423 1,872120

(plus 30 equity)

$553 millionDevelopment and commercial milestones

High single digit to mid-teen percent royalties on AGEN-1423$50 million

Option exercise fee for each option after exercising$520 million

Additional dvlpt and commercial milestones for each option programHigh single digit to mid-teen percent royalty payments for each option

GileadTango

Therapeutics10/2018 I-O therapies 1,750 50

$1,700 millionPreclinical fees and development, regulatory and commercial milestones

Low double-digit tiered royalties on net sales across all programs

Cilag (J&J) arGEN-X 12/2018Anti-CD70 antibodies incl.

cusatuzumab1,600

300(plus 200 equity

under separate deal)

$1,300 millionDevelopment, regulatory and sales milestones

BluebirdGritstone Oncology

08/2018 Cell therapies using EDGE tech. 1,59520

(plus 10 equity)

$129 million per therapy product & $27.5 million per target product Development, regulatory, and commercial milestones

Low single-digit tiered royalty payments upon on annual net sales

Boehringer Ingelheim

OSE Immunothera

peutics04/2018

Myeloid checkpoint inhibitor antibody, OSE-172

1,389 18

$18 millionOn initiation of a phase I clinical study

$1,350 millionDevelopment, commercialization and sales milestones

Royalties on worldwide net sales

42

Top 10 oncology M&A deals in 2018 total $21.7 billion and include new technologies

Sellside Buyside DateStage Financials

$MAsset/

TechnologyD I II III PR/R L

Juno Therapeutics

Celgene 01/2018 $9,000 Cell therapy

TESARO GlaxoSmithKline 12/2018 $5,100Small

molecule

ARMO Biosciences Eli Lilly 05/2018 $1,600 MAb

BeneVir Biopharm Janssen 02/2018$1,040 ($140 UF, $900 milestones)

Recombinant virus

Tusk Therapeutics Roche 09/2018$781 ($83 UF,

$697 milestones)Antibody

Cascadian Therapeutics

Seattle Genetics 01/2018 $614Small

molecule

AurKa Pharma Eli Lilly 05/2018$575 ($110 UF,

$475 milestones)Small

molecule

Denali Therapeutics F-Star Gamma 05/2018$465 ($18 UF,

$447 milestones) MAb

Viralytics Merck & Co. 02/2018 $394IntratumoralI-O therapy

ViraTherapeuticsBoehringer Ingelheim

09/2019 $210Recombinant

virus

1 Only M&A deals for therapeutics were considered, and where “Cancer” is the primary focus

43

Percentage of oncology licensing deals from 2014-2018 by region

~1% (North America → Aus/NZ)~1% (Aus/NZ → North America)

<1% (North America → Central/South America)<1% (Central/South America → North America)

~41% (North America → North America)

~11% (Europe → Europe)

~5% (Asia → North America)~7% (North America → Asia)

~8% (Asia → Asia)

~1% (Asia → Europe)~3% (Europe → Asia)

~1% (Europe → Aus/NZ )<1% (Aus/NZ → Europe)

~10% (Europe → North America)~10% (North America → Europe

<1% (Asia → Aus/NZ)<1% (Aus/NZ → Asia)

~1% (Aus/NZ → Aus/NZ)

~1% (North America → Israel/M. East)<1% (Israel/M.East→ North America)

<1% (Europe → Israel/M. East)<1% (Israel/M.East→ Europe)

44

Summary of findings

• Oncology represents the largest number of deals

• High value deals driven by immuno-oncology

• Median deal value rose in 2018 but upfronts static

• Discovery-stage deals capable of commanding high value

• Oncolytic virus technology make a prominent showing in M&A activity

• Opportunity remains for inter-regional deal-making

2018 Biopharma Industry

Year-in-Review

Approvals and Other Drivers of ROI

Analysis suggests large pharma ROI has continues to fall

47

But an orphan NME approval is not the end of the story…

0

200

400

600

800

1000

1200

Nu

mb

er

of

elig

ible

US

pat

ien

ts

(10

00

s)

Incremental growth in eligible patients for treatment with Keytruda (2014-2017)*

First FDA approval (orphan indication) for advanced melanoma refractory to ipilimumaband BRAF inhibitors and with V600 BRAF mutation

Advanced PD-L1+ NSCLC that has progressed after other treatments

Recurrent/metastatic head and neck squamous cell carcinoma (PD-L1 independent) that has progressed after platinum-containing chemotherapy

Additional indications

Source: IPD, NCI Cancer Stat Facts, and various publications* Patient number estimates are based on the prevalence of the cancer in the US. Assumptions have been made with regard to theproportion of patients eligible for Keytruda therapy (stage of disease, line of therapy, etc,)

48

o Stott suggests that the industry that is entering a vicious cycle of negative growth and terminal

decline as its fundamental business model has run out of steam by the Law of Diminishing

Returns

Pharma's broken business model – An industry on the brink of terminal decline by Stott

49

o There is a limited

correlation

between R&D

productivity and

Company

Performance

Biopharma R&D Productivity and Growth 2017: Big Pharma closes the gap (Catenion)

Enterprise Value Jan 2010 – Dec 2018

51

0

5

10

15

20

25

30

35

0 1000 2000 3000 4000 5000 6000 7000Sale

s fr

om

pro

du

cts

app

rove

d in

last

fiv

e ye

ars

as %

to

tal

ph

arm

a sa

les

Sales from products approved 2013-2017 ($M)

Sales from products approved in last five years (2013-2017)

Large pharma revenues have been driven by older products

Established products are driving sales

Sources: Clarivate Analytics 2018Approvals data from Cortellis Regulatory Intelligence and FDAProduct and company sales data from company Annual Reports/20-F or 10-K filingsPatent expiry data from company reports (as above) and NewportExchange rates from www.x-rates.com

0%

10%

20%

30%

40%

50%

60%

70%

80%

Off-patent sales as % total sales (2017)

52

The cost per from US$2 billion in 2014 to US$3 billion mark in 2016 and 2017

1903

2601

3239 3252

0

500

1000

1500

2000

2500

3000

3500

2014 2015 2016 2017

Co

st

in U

S$

mil

lio

n

Year

2014 2015 2016 2017

Approvals limited to lead projects. Adjusted to account for co-developments between companies. Limited to 2018

participants and includes companies that have provided expenditure for each year and have at least 0.5 approvals

Source: 2018 CMR R&D and Investment Metrics programmes

o While the cost per NME approval has increased by 50% between 2014 and 2017 the median peak

sales value per FDA approval has remained fairly constant at $1.0 billion during the same period.

53

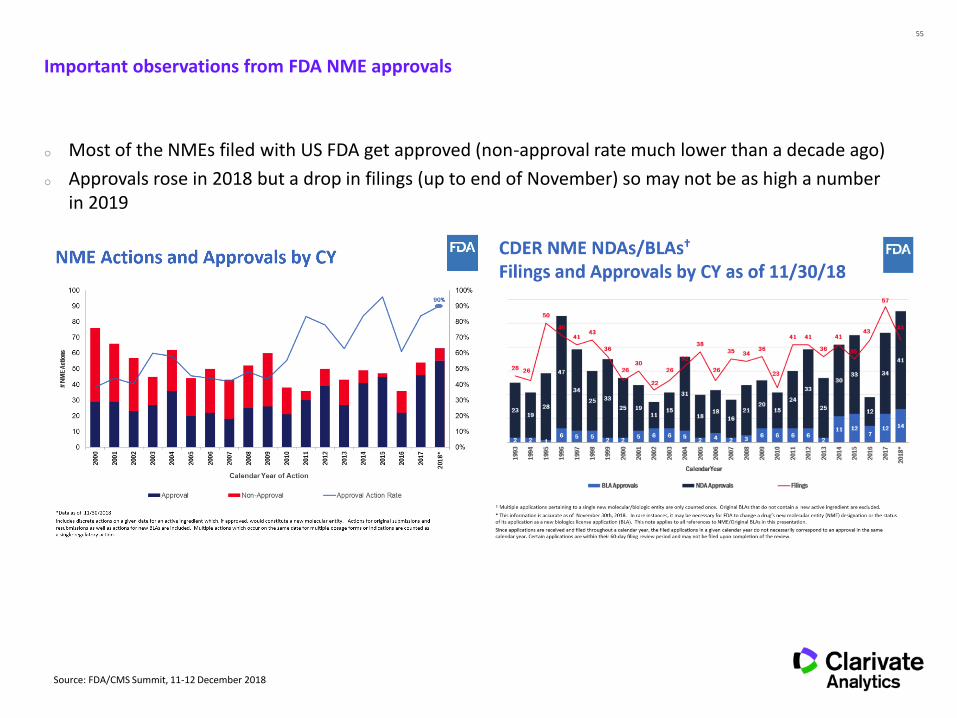

Source: FDA

Record-breaking year for FDA NME approvals: orphan drugs exceed >50% for first time

No. US FDA CDER NME approvals 2010-2018

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

2010 2011 2012 2013 2014 2015 2016 2017 2018*

% a

pp

rova

ls d

irec

ted

at

orp

han

ind

icat

ion

s

No

. FD

A C

DER

NM

E ap

pro

vals

SM Biologic % orphan approvals

54

Only 19% of 2018 NME approvals forecast to generate sales >$1Bn by end of 2023

Approvals with forecast sales >$1B

Major pharma, 7

Other pharma, 4

Approvals with forecast sales <$1B, 48

55

o Most of the NMEs filed with US FDA get approved (non-approval rate much lower than a decade ago)

o Approvals rose in 2018 but a drop in filings (up to end of November) so may not be as high a number in 2019

Important observations from FDA NME approvals

Source: FDA/CMS Summit, 11-12 December 2018

56

Oncology no longer main driver of approvals and most approved for orphan indications

Source: FDA, Clarivate Analytics analysis

2018

Other orphan approvals, 20

Oncology orphan approvals, 14

Oncology non-orphan approvals,

4

Other non-orphan approvals, 21

57

Trends in 2018 approvals

New drugs continue to address fewer patients

US FDA CDER NME approvals Patients covered by approved indications (M)1

Source: FDA, IPD, Clarivate Analytics analysis1 Epidemiology data from IPD and published scientific literature. Patient numbers are for US only

21

59

2010 2018

190

168

2010 2018

*

* Two of the drugs approved drugs in 2018 have been assigned as “zero” patients:

TPOXX (tecovirimat) for the treatment of smallpox when used as a bioweaponMOXIDECTIN (moxidectin) for onchocerciasis (river blindness) due to Onchocerca volvulus. There are no cases in the US, but the WHO estimates 18 M patients worldwide

58

Pricing remains a source of contention

Source: Novartis Investor Day, 5 November 2018, Slide 48

59

Percent of US NME approvals sponsored by top pharma companies has been falling year on year

Note: Acquisitions or licensing deals bringing in assets from a non Top 20 pharma that occurred within one year of eventual approval not counted for the Top 20 Pharma (usually not listed as sponsor in these cases anyway). Co-development of a molecule with a non Top 20 pharma company counted as half an approval

Source: FDA, Clarivate Analytics analysis

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014 2015 2016 2017 2018*

Top 20 pharma sponsors

60

Deal-making still accounting for more than 50% of NME approvals

All NME approvals Oncology NME approvals

US FDA CDER NME approvals resulting from licensing/acquisition (2010-2018)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018*

61The funding challenge (illustrative)

2018 Biopharma Industry

Year-in-Review

Summary

63

o Industry continues to concentrate BD on areas of unmet medical need, e.g. oncology, rare diseases

o With differences between biopharma and VC in terms of investing at risk, i.e. neuroscience

o China deal-making continues to grow

o Some of the doom-and-gloom papers suffer from methodological issues

o Companies are creating value although it is driven commercially and questions remain about ROI

o Rare disease/niche remains an attractive strategy which will continue to keep the spotlight on drug pricing

o Greater funding challenges remain which will require further innovation and bold leadership

Summary

Q&A

65

Contact us

Jamie Munro, PhDGlobal Practice Leader, Portfolio & LicensingMobile +44 782 447 4864 ; Office +44 207 433 4910Friars House, Southwark, London, UK

Helen Dowden, PhDConsultant, Portfolio & LicensingMobile +44 (0)7553 855 669

Powering life sciences innovation with trusted content, analytics & technology.

clarivate.com/contact-us