2018 key sap investment updates · 2018-06-13 · (sap guidance also allows nav when permitted in a...

TRANSCRIPT

© 2018 National Association of Insurance Commissioners

2018 Key SAP Investment Updates

Julie Gann, Senior Manager II – Accounting and Reporting

Fatima Sediqzad, SCA Valuation and Accounting Policy Advisor

Robin Marcotte, Senior Manager II – Accounting

Jake Stultz, Senior Accounting and Reinsurance Policy Advisor

© 2018 National Association of Insurance Commissioners

Learning Objectives

1. Describe new and revised SAP Investment guidance.

2. Identify hot topics involving investments currently

being considered by the Statutory Accounting

Principles (E) Working Group.

3. Recognize how investment changes may impact

accounting and reporting, and the impact to RBC.

2

2

© 2018 National Association of Insurance Commissioners

Julie Gann

Senior Manager II – Accounting & Reporting

– Supports Statutory Accounting Principles (E) Working Group

– Provides technical & advisory services in SAP, GAAP & IFRS

Joined NAIC in February 2001. Prior Positions Include:

– NAIC Financial Examination Manager

– NAIC International Insurance Accountant

– Public accountant and insurance examiner consultant

CPA, FLMI, ARA and AIRC

Member of AICPA & MSCPA

3

3

© 2018 National Association of Insurance Commissioners

Fatima Sediqzad

SCA Valuation and Statutory Accounting Policy Advisor

– Supports Statutory Accounting Principles Working Group

– Reviews subsidiary, controlled and affiliated entity filings

– Provides technical & advisory services in SCA’s, SAP and

GAAP

Joined the NAIC in January 2016

Prior to joining the NAIC – employed in public accounting and a

private financial services firm

CPA

Member of AICPA

4

4

© 2018 National Association of Insurance Commissioners

Robin Marcotte

Senior Manager II – Accounting

– Supports Accounting Practices and Procedures Task Force

– Supports Statutory Accounting Principles Working Group

– Supports Risk Limiting Contracts Working Group

– Provides technical & advisory services in SAP, GAAP & IFRS

Joined the NAIC in August 2000

– Prior to joining the NAIC employed at a Dept. of Insurance

CPA, CFE, Associate in Reinsurance, CISA

Member of AICPA, MSCPA, and SOFE

5

5

© 2018 National Association of Insurance Commissioners

Jake Stultz

Senior Accounting Policy Advisor

– Supports Statutory Accounting Principles Working Group

– Supports Reinsurance Task Force

– Provides technical & advisory services in SAP, GAAP &

Reinsurance

Joined the NAIC in February 2017

Prior to joining the NAIC – employed in public accounting, real

estate and insurance

6

6

© 2018 National Association of Insurance Commissioners

Discussion Topics

Adopted Items

1. SSAP No. 26R – Systematic Value / Bank Loans

2. SSAP Nos. 1 and 32 – VOSTF and Blanks Symbol Changes

3. SSAP No. 41R – Surplus Notes

4. SSAP No. 68 – Goodwill Disclosures

5. SSAP No. 86 – Derivative Revisions

6. SSAP Nos. 92 and 102 – Fair Value Level 3 Disclosure

7. SSAP No. 97 – SCA Filings / Goodwill and SCA Loss Tracking

8. SSAP No. 100R – Use of Net Asset Value

9. SSAP No. 103R – Wash Sales

7

© 2018 National Association of Insurance Commissioners

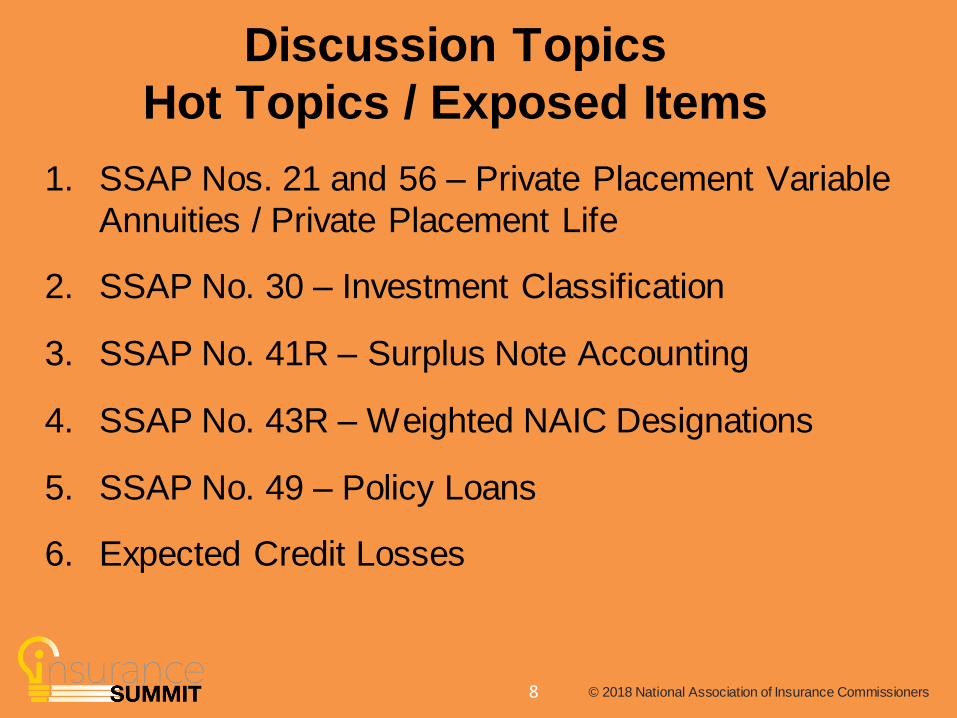

Discussion Topics

Hot Topics / Exposed Items

1. SSAP Nos. 21 and 56 – Private Placement Variable

Annuities / Private Placement Life

2. SSAP No. 30 – Investment Classification

3. SSAP No. 41R – Surplus Note Accounting

4. SSAP No. 43R – Weighted NAIC Designations

5. SSAP No. 49 – Policy Loans

6. Expected Credit Losses

8

© 2018 National Association of Insurance Commissioners

SSAP No. 26R: Bonds

Systematic Value / Bank Loans

Agenda Item 2013-36 / Substantive

– Substantive revisions to SSAP No. 26R impacting the

measurement method for SVO-Identified Bond ETFs.

– Effective Dec. 31, 2017

Key Change:

All SVO-Identified Bond ETFs required at fair value for year-end

2017 unless designated for systematic value.

Designated SVO-Identified items noted with code = *

No change to scope guidance involving SVO-Identified funds.

9

© 2018 National Association of Insurance Commissioners

SSAP No. 26R: Bonds

Measurement Methods

• Bonds, Excluding Mandatory Convertible Bonds:

– Amortized Cost or Lower of Amortized Cost / Fair Value

• Depends on NAIC designation and whether entity maintains AVR

• Mandatory Convertible Bonds:

– Lower of Amortized Cost / Fair Value • Not assigned NAIC designations

• SVO-Identified Funds:

– Fair Value Unless Designated at Systematic Value • Must meet NAIC designation requirements for SV

– SV is an irrevocable designation by CUSIP

– Must follow established SV approach

10

© 2018 National Association of Insurance Commissioners

SSAP No. 26R:

Bank Loans

Clarifies directly issued and acquired bank loans to

be in scope of SSAP No. 26R.

NAIC Staff Note:

Bank loan guidance is not intended to move investments

that are explicitly captured on a different reporting

schedule to Schedule D-1 as “bonds.”

• For example, mortgage loans are captured within SSAP

No. 37 and reported on Schedule B. Mortgage loans shall

not be reported as “bank loans” on Schedule D-1.

11

© 2018 National Association of Insurance Commissioners

SSAP Nos. 1 and 32:

VOSTF / BWG Changes

• Agenda Item 2018-05/ Nonsubstantive

Symbol Changes:

• New “PL” and “PLGI” for securities subject to private letter rating.

• Add “YE” symbol and “IF” as part of new SVO “carry-over”

procedures:

– YE = Annual Update – Existing SVO designation extended.

– IF = Initial filings – Insurer self-designates until SVO analysis.

• Modify “Z” – allowed as an indicator that a security is in transition

from one reporting status to another

• Eliminate use of “P” and “RP” and add specific line categories for

perpetual preferred and redeemable preferred stock

• Effective Annual 2018

12

12

© 2018 National Association of Insurance Commissioners

SSAP No. 41R: Surplus Notes

Agenda Item 2017-21 / Nonsubstantive

Clarifies that surplus notes cannot be “double-counted”

between the parent and SCA in any situation:

– Parent Issuer / SCA Holder

– SCA Issuer / Parent Holder

– Regardless of how acquired (Market / Directly)

Prior guidance only specifically addressed one scenario, but the

concept should apply universally.

13

© 2018 National Association of Insurance Commissioners

SSAP No. 68:

Additional Goodwill Disclosure Agenda Item 2017-18/ Nonsubstantive

• Captures additional goodwill information in Note 3.

• Disclosure components: (New items in blue)

– Acquisition Date

– Cost of Acquired Entity

– Original Amount of Admitted Goodwill

– Admitted Goodwill as of Reporting Date

– Amount of Goodwill Amortized during Reporting Period

– Admitted Goodwill as a % of SCA BACV, Gross of Admitted Goodwill

Reminders:

• Admitted Limitation / Impairment Assessment / Amortization

14

© 2018 National Association of Insurance Commissioners

14

© 2018 National Association of Insurance Commissioners

SSAP No. 86:

Derivative Financing Premiums

Agenda Item 2016-48 / Nonsubstantive

Expand disclosures / detail for derivatives with financing premiums

• Pay cost (premium) to acquire derivative throughout contract.

• Pay cost (premium) to acquire derivative at end of contract.

Identical Derivatives Reported Significantly Differently:

Traditional Financing

Cost Paid 5,000 Cost Deferred 6,000

Fair Value 5,000 Fair Value 0

Unrealized Loss (1,000) Unrealized Loss (1,000)

Fair Value 4,000 Fair Value (1,000)

Financing:

FV reflects

present value of

cash flows, so

amount owed nets

with derivative.

15

© 2018 National Association of Insurance Commissioners

SSAP No. 86:

Derivative Financing Premiums

Aggregate Disclosures – Required Year-End 2017

• Non-discounted total premium cost

• Premium due in each of the following 4 years, and thereafter.

• Fair Value of derivatives, excluding impact of financing premiums

Individual Disclosures – Required Year-End 2018

• Total cost

• Current year premium paid and amounts paid in prior years

• Future unpaid premium cost

• Fair value of derivative, excluding impact of financing premiums

• Unrealized gain / loss, excluding impact of financing premiums

16

© 2018 National Association of Insurance Commissioners

SSAP No. 86:

Variation Margin

Agenda Item 2017-04 / Nonsubstantive

Address questions on whether variation margin payments are

considered “settled” as opposed to “collateral.”

• Some Clearinghouses characterize as “legally settled”

• Although VM payments occur daily, derivative contract is still open.

• Settled = Realized Changes / Collateral = Unrealized Changes

Adopted Revisions:

• Amounts received as variation margin shall not be recognized as “settled” until the derivative contract has terminated and/or otherwise expired.

• Adopted with an effective date of Jan. 1, 2018 prospectively for entities that

previously considered VM payments to reflect settlement or gains/losses.

17

© 2018 National Association of Insurance Commissioners

SSAP No. 92 / 102:

Plan Asset FV Level 3 Disclosure

Agenda Item 2017-30 / Nonsubstantive

Removes the Fair Value – Level 3 Reconciliation Disclosures

• Reconciliation of beginning / ending balances, detailing:

– Actual return on plan assets

– Purchases / Sales / Settlements

– Transfers in / out of Level 3

Things to Remember:

• Plan Assets for Pensions / OPEB are not shown as insurer assets

• Fair Value of Plan assets used to determine funded status

Under Funded = Liability / Over Funded = Nonadmitted Asset

• Other FV disclosures (e.g., aggregate FV by level) are still required.

18

© 2018 National Association of Insurance Commissioners

SSAP No. 97:

SCA Filing Deadlines

Agenda Item 2017-08:

• Sub 1 – Required within 90 days after acquisition / formation

(Extended from prior 30-day requirement)

• Sub 2 – Required by August 31, or within 30 days after audit

report if audit report is routinely received after Aug. 31.

(Revised from the “by June” deadline)

• Late fees if filing late (except for audit report extension).

• File on time and with all information to avoid additional costs!

19

19

© 2018 National Association of Insurance Commissioners

SSAP No. 97:

Foreign Insurance SCAs Agenda Item 2017-20:

• 8.b.iv. Entities – Foreign Insurance SCAs

– Regardless if providing audited U.S. GAAP financials

or, audited foreign statutory financials, shall adjust to

the limited statutory basis of accounting in accordance

with paragraph 9.

• This was just a clarification in paragraph 8.b.iv for the U.S.

GAAP financials. Other guidance in the SSAP indicated that

the adjustment was applicable to both types of financials.

20

20

© 2018 National Association of Insurance Commissioners

SSAP No. 97:

SCA Loss Tracking

Agenda Item 2018-09 / Nonsubstantive

Clarifies current guidance and adds new disclosure

If share of losses exceeds carrying value: (No Concept Changes)

– Value is zero / discontinue use of equity method.

– Track losses / resume equity method once positive.

– Do not report negative SCA asset unless guarantee.

– If guarantee, reported negative equity and guarantee.

Guarantee is required under SSAP No. 5R

21

21

© 2018 National Association of Insurance Commissioners

SSAP No. 97:

SCA Loss Tracking

Agenda Item 2018-09 / Nonsubstantive

• Effective 2018 Disclosure

-- Only required if losses exceed carrying value --

• Current period share of net income / losses for SCA

• Accumulated share of net income / losses for SCA

• Investment in SCA (deficit or surplus)

• Guaranteed Obligation / Financial Support (Y / N)

• SCA Reported Value

22

22

© 2018 National Association of Insurance Commissioners

SSAP No. 100R: Fair Value

Use of Net Asset Value

Agenda Item 2017-24 / Substantive

• Substantive revisions allows net asset value (NAV) as a

practical expedient to fair value when certain conditions

exist. (Adopts GAAP – ASU 2009-12 & ASU 2015-07)

(SAP Guidance also allows NAV when permitted in a SSAP.)

Conditions:

1. Investment does not have readily determinable fair value, and

2. Investment is in an investment company or real estate fund for

which it is industry practice to measure investment assets at

fair value on a recurring basis and to issue financials

consistent with the principles of an investment company.

23

© 2018 National Association of Insurance Commissioners

SSAP No. 100R: Fair Value

Use of Net Asset Value

• Disclosure Impact

– NAV is not a “fair value” measurement. As such:

NAV shall not be included in the fair value hierarchy.

2018 Disclosure Revisions:

For 2017, NAV was included in FV Level 2 with separate

disclosure. This was just due to timing as the revisions were

adopted to allow for year-end 2017 application.

Asset Level 1 Level 2 Level 3 NAV Total

New Column

24

© 2018 National Association of Insurance Commissioners

SSAP No. 103R: Wash Sales

Disclosure Exclusions

Agenda Item 2017-23 / Nonsubstantive

• MMMF excluded from wash sale disclosure: Year-end 2017

Agenda Item 2017-31 / Nonsubstantive: Effective 2018

• Wash Sale Disclosure Excludes:

– All cash equivalents

– Short-term investments with credit assessments of NAIC 1-2

– Derivative transactions

• Disclosure is required in financials when the investment is sold.

Sell Dec. 15, 2017 / Purchased Jan. 15, 2018

Include in Dec. 31, 2017 Financials

25

© 2018 National Association of Insurance Commissioners

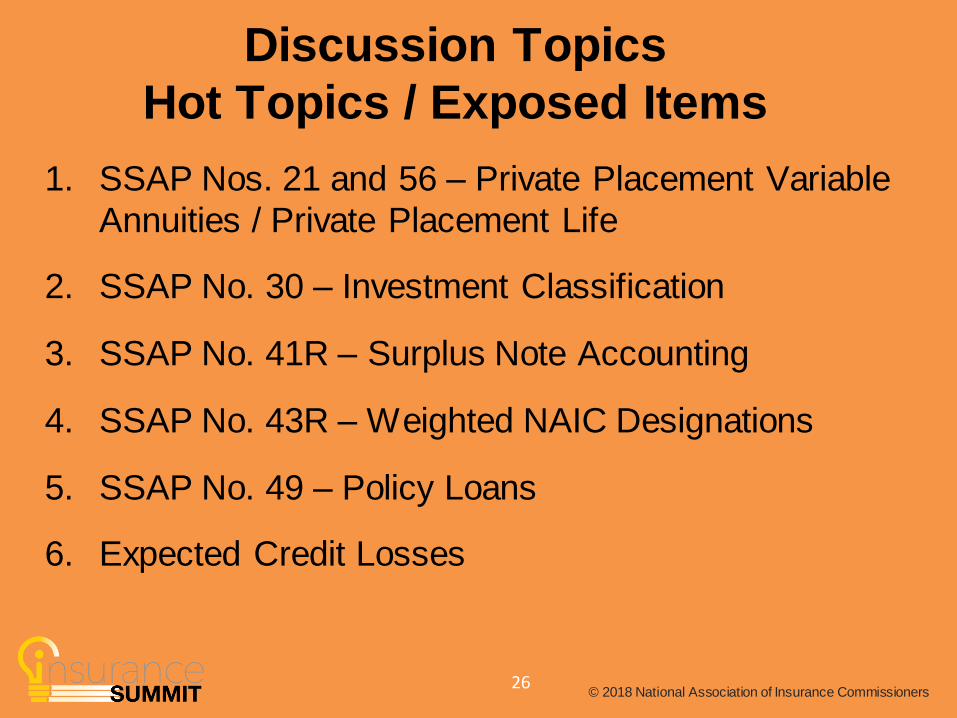

Discussion Topics

Hot Topics / Exposed Items

1. SSAP Nos. 21 and 56 – Private Placement Variable

Annuities / Private Placement Life

2. SSAP No. 30 – Investment Classification

3. SSAP No. 41R – Surplus Note Accounting

4. SSAP No. 43R – Weighted NAIC Designations

5. SSAP No. 49 – Policy Loans

6. Expected Credit Losses

26

© 2018 National Association of Insurance Commissioners

SSAP No. 21: Private Placement

Variable Annuities Background

• SSAP No. 21, paragraph 6 allows life insurance owned to be treated as an admitted asset as follows:

– Amount that could be realized on life insurance policies where the reporting entity is the owner and beneficiary or has otherwise obtained the rights to control the policy, is similar to a cash deposit that is realizable on demand.

– Permits amount that could be realized as an admitted asset, reported as an other-than invested asset. Considers cash surrender value and other contractual terms which limit or provide for additional realizable amounts.

No RBC on Other-Than Invested Asset Line

27

© 2018 National Association of Insurance Commissioners

© 2018 National Association of Insurance Commissioners

SSAP No. 21: Private Placement

Variable Annuities Agenda Item 2018-08 / Nonsubstantive

Issue Raised in Response to Inquiries:

• Private Placement = Not Registered with SEC (must qualify as

accredited investor / qualified purchaser)

• PPVA / PPLI – Either “Annuity” or “Life Insurance”

o PPVA typically an investment product with an “insurance dedicated fund”

offered by insurance carriers. (Tax advantages for holders.)

o May use alternative investment portfolios: Hedge funds, high-yield bonds, direct lending credit vehicles, etc.

o PPLI may also have these characteristics or be in more traditional form

(key person insurance/other protection-type features)

© 2018 National Association of Insurance Commissioners

28

© 2018 National Association of Insurance Commissioners

SSAP No. 21: Private Placement

Variable Annuities • Concern that SSAP No. 21 is used to avoid investment

reporting and RBC for investment-focused products.

Insurer Holders – 5-24-18 Exposed Guidance:

Admissible Amount that can be Realized on Life Insurance

– Incorporates IRC 7702 definition of “Life Insurance”

• Reg. as Life insurance, insurable interest;

• Significant transfer of mortality, Actuarial tests

– Admits if the reporting entity owner/ beneficiaries – not subject

to investment risk

• Net realizable value /CSV not subject to market risk

29 © 2018 National Association of Insurance Commissioners

© 2018 National Association of Insurance Commissioners

SSAP No. 56: Separate Account

Insurer Issuers

PPVA / PPLI – Insurance Company Issuers

• New 2018 Disclosure in the Separate Account GI:

– Identify Non-SEC registered products

30

© 2018 National Association of Insurance Commissioners

Product Identifier Separate Account Assets

Registered with SEC Not Registered with the SEC

Product Not Registered with SEC

PPVA PPLI Other

30

© 2018 National Association of Insurance Commissioners

SSAP No. 30: Investment Classification Project

Agenda Item 2017-32 / Substantive

– Improve common stock definition.

• Separate common stock from other items captured in scope.

– Include Closed-End Funds and Unit Investment Trusts

• Only allow SEC-Registered Funds

• Expands current reference of “mutual funds”

– Capture NAIC designations on Schedule D-2-2

• Would allow underlying nature of investment to drive RBC

• Specific for investments that can be reviewed by SVO.

© 2017 National Association of Insurance Commissioners

31

© 2018 National Association of Insurance Commissioners

SSAP No. 30: Investment Classification Project

Comments Considered

• Interested Parties – Supported proposed intent.

– NAIC staff to consider scope comments in issue paper.

Comments: GAAP equity definition and private stock warrants.

– Retain status-quo on SVO-Identified funds in SSAP No. 26R

• Vanguard – Mutual funds should be SSAP No. 26R Funds

– Mutual funds similar to SVO-Identified Bond ETFs.

– Allow reporting on Schedule D-1, under SSAP No. 26R and

Systematic value. 32

© 2017 National Association of Insurance Commissioners

32

© 2018 National Association of Insurance Commissioners

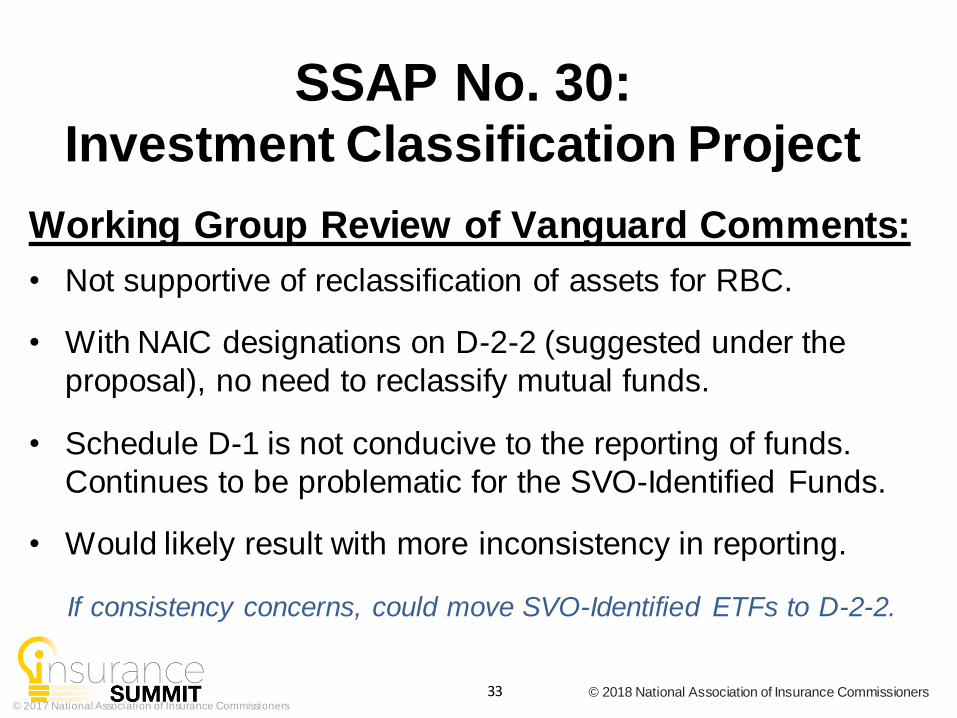

SSAP No. 30: Investment Classification Project

Working Group Review of Vanguard Comments:

• Not supportive of reclassification of assets for RBC.

• With NAIC designations on D-2-2 (suggested under the

proposal), no need to reclassify mutual funds.

• Schedule D-1 is not conducive to the reporting of funds.

Continues to be problematic for the SVO-Identified Funds.

• Would likely result with more inconsistency in reporting.

If consistency concerns, could move SVO-Identified ETFs to D-2-2.

33

© 2017 National Association of Insurance Commissioners

33

© 2018 National Association of Insurance Commissioners

SSAP No. 41R: Surplus Notes

Hot Topic

Agenda Item 2018-07 / Nonsubstantive

Issued debt instruments do not qualify as surplus notes if

linked to other products or transactions held by the insurer.

• Regulator approval for interest / principle payment on surplus

note determines whether insurer will receive amount due on a

held instrument.

• When cash flows due under a surplus note can be countered /

offset / netted with a cash flow due to on a held instrument.

Such notes are not subordinate to policyholders and other claimants.

Linked “assets” shall be nonadmitted as they are unavailable for

policyholders due to encumbrances or other third-party interests.

34

© 2018 National Association of Insurance Commissioners

SSAP No. 43R: Weighted Average Designations

Agenda Item 2018-03 / Nonsubstantive

• Eliminates “weighted average” NAIC designation reporting

for investments in lots. Requires either:

– Single-line reporting of entire investment at lowest NAIC

designation applicable to any lot.

– Multi-line reporting of investment by lot. (Allows different

NAIC designations by lot.)

• Consistent with existing reporting instructions.

– Required to report info at a lower level of detail if the

information would be inaccurate if reported in aggregate.

35

© 2017 National Association of Insurance Commissioners

35

© 2018 National Association of Insurance Commissioners

ASU 2016-13: Credit Losses

Agenda Item 2016-20 / Substantive

• Considers expected credit loss concept for SAP

– Existing SAP reflects an incurred loss methodology

• Key Items to Note in Considering ECL:

– Does not require any additional losses to be recognized than what is recognized under an incurred loss model.

– If there is no ECL, then nothing is recognized.

– ECL results in more timely recognition of credit losses.

– ECL can be adjusted to reflect updated estimates. 36

© 2017 National Association of Insurance Commissioners

© 2018 National Association of Insurance Commissioners

ASU 2016-13: Credit Losses

Current Status:

• Working Group directed NAIC to proceed with drafting an

issue paper with a proposal to replace the incurred loss

model with an expected credit loss concept.

– This direction identified that differences between U.S. GAAP

and SAP will necessitate modifications in the application of

the concept for statutory accounting.

– Development of the issue paper would allow state insurance

regulators and industry to complete an assessment of the

various components of the expected credit loss concept for

statutory accounting. 37

© 2017 National Association of Insurance Commissioners

37

© 2018 National Association of Insurance Commissioners

ASU 2016-13: Credit Losses

ECL – Amortized Cost Investments • GAAP: Valuation account deducted from amortized cost basis to

present the net amount expected to be collected.

– Completed on collective basis when similar risks

exist. Otherwise, completed as individual

assessments.

• SAP: General concept, mirror GAAP, with:

– Possible inclusion of Fair Value floor

– Exclusion for nonadmitted investments / receivables

– SAP specific guidance for reinsurance recoverables

– SAP guidance for acquired assets with credit

deterioration.

© 2017 National Association of Insurance Commissioners

38

© 2018 National Association of Insurance Commissioners

ASU 2016-13: Credit Losses

ECL – Fair Value (AFS through OCI) • GAAP: For impaired securities (FV is less than AC), assess

whether impairment is due to credit loss or other factors.

– Impairments from credit loss are recognized as ECL, limited to the

amount that fair value is less than amortized cost.

– Required at the individual security level.

Changes in FV non-credit = Other-

Comprehensive Income

Changes in FV credit-related = Expected Credit

Loss • SAP: General concept, mirror GAAP. Consider guidance if

investments move between FV and AC measurement.

39

© 2017 National Association of Insurance Commissioners

39

© 2018 National Association of Insurance Commissioners

Questions on Hot Topics / Exposed Items?

1. SSAP Nos. 21 and 56 – Private Placement Variable

Annuities / Private Placement Life

2. SSAP No. 30 – Investment Classification

3. SSAP No. 41R – Surplus Note Accounting

4. SSAP No. 43R – Weighted NAIC Designations

5. SSAP No. 49 – Policy Loans

6. Expected Credit Losses

40

© 2018 National Association of Insurance Commissioners

-- QUESTIONS --

2018 SAP UPDATES - INVESTMENTS

Julie Gann – [email protected] / Fatima Sediqzad – [email protected]

Robin Marcotte – [email protected] / Jake Stultz – [email protected]

41