2019-10 risk reports

TRANSCRIPT

Risk AnalysisWyoming State Treasurer’s Office

Total Return FocusedTarget Allocation Risk Summary

May 1, 2008 to June 30, 2019

Analysis provided by PerTrac RiskPlus powered by FinAnalytica. All values are annual.

Factor Contribution to Risk Portfolio Historical Stress Tests

Percent Contribution to Risk and ETLTotal Portfolio Summary

*Calculated with a 99% Confidence Interval.**Similar to the Sharpe Ratio which is a standard deviation-based performance measure, but STARR (stable tail-adjusted return ratio) uses the ETL in the denominator as a risk measure. STARR can be seen as a more effective indicator of risk-adjusted performance because it penalizes only for downside risk, while the standard deviation does not distinguish between upside and downside risk.

Volatility 6.2%

Value at Risk (VaR)* 12.9%

Expected Tail Loss (ETL)* 16.6%

Expected Tail Return (ETR)* 13.0%

Rachev Ratio (ETR/ETL)* 0.8

STARR Performance (Excess Return/ETL)** 0.1

7%

-1%

72%

2%

14%

0%

2%

3%

0%

-20% 0% 20% 40% 60% 80% 100%

Specific Risk

Commodity Risk

Equity Risk

FX Risk

Fixed Income Risk

Style Risk

Size Risk

Interest Rate Risk

Volatility

1.9%

-1.8%

7.3%

-7.3%

2.8%

-4.0%

7.0%

-6.5%

-17.2%-25%-20%-15%-10%

-5%0%5%

10%15%20%25%

25%

7%

37%

10%

8%

0%

0%

4%

0%

2%

6%

24%

8%

38%

11%

4%

0%

0%

4%

2%

3%

6%

11%

3%

14%

6%

8%

6%

5%

8%

29%

6%

5%

0% 10% 20% 30% 40% 50%

US EquitySmall Cap US…

International EquityMLPs

Private EquityCore Real Estate

Non-Core Real…Diversified…

Int. Duration…Bank Loans

Emerging Market…

Percent Contribution to ETL Percent Contribution to Risk Target Allocation

Page 2

Income FocusedTarget Allocation Risk Summary

May 1, 2008 to June 30, 2019

Analysis provided by PerTrac RiskPlus powered by FinAnalytica. All values are annual.

Factor Contribution to Risk Portfolio Historical Stress Tests

Percent Contribution to Risk and ETLTotal Portfolio Summary

*Calculated with a 99% Confidence Interval.**Similar to the Sharpe Ratio which is a standard deviation-based performance measure, but STARR (stable tail-adjusted return ratio) uses the ETL in the denominator as a risk measure. STARR can be seen as a more effective indicator of risk-adjusted performance because it penalizes only for downside risk, while the standard deviation does not distinguish between upside and downside risk.

Volatility 5.3%

Value at Risk (VaR)* 9.8%

Expected Tail Loss (ETL)* 12.6%

Expected Tail Return (ETR)* 11.3%

Rachev Ratio (ETR/ETL)* 0.9

STARR Performance (Excess Return/ETL)** 0.1

7%

-1%

76%

4%

11%

0%

1%

2%

0%

-20% 0% 20% 40% 60% 80% 100%

Specific Risk

Commodity Risk

Equity Risk

FX Risk

Fixed Income Risk

Style Risk

Size Risk

Interest Rate Risk

Volatility

22%

6%

33%

17%

4%

2%

0%

2%

6%

10%

20%

6%

31%

18%

4%

0%

0%

4%

7%

10%

8%

2%

10%

7%

3%

11%

3%

37%

12%

7%

0% 10% 20% 30% 40% 50%

US EquitySmall Cap US…

International EquityMLPs

Preferred StockCore Real Estate

Non-Core Real…Int. Duration…Bank Loans

Emerging Market…

Percent Contribution to ETL Percent Contribution to Risk Target Allocation

1.6%

-1.5%

5.7%

-5.7%

1.9%

-2.3%

5.6%

-4.9%

-15.6%-25%-20%-15%-10%

-5%0%5%

10%15%20%

Page 3

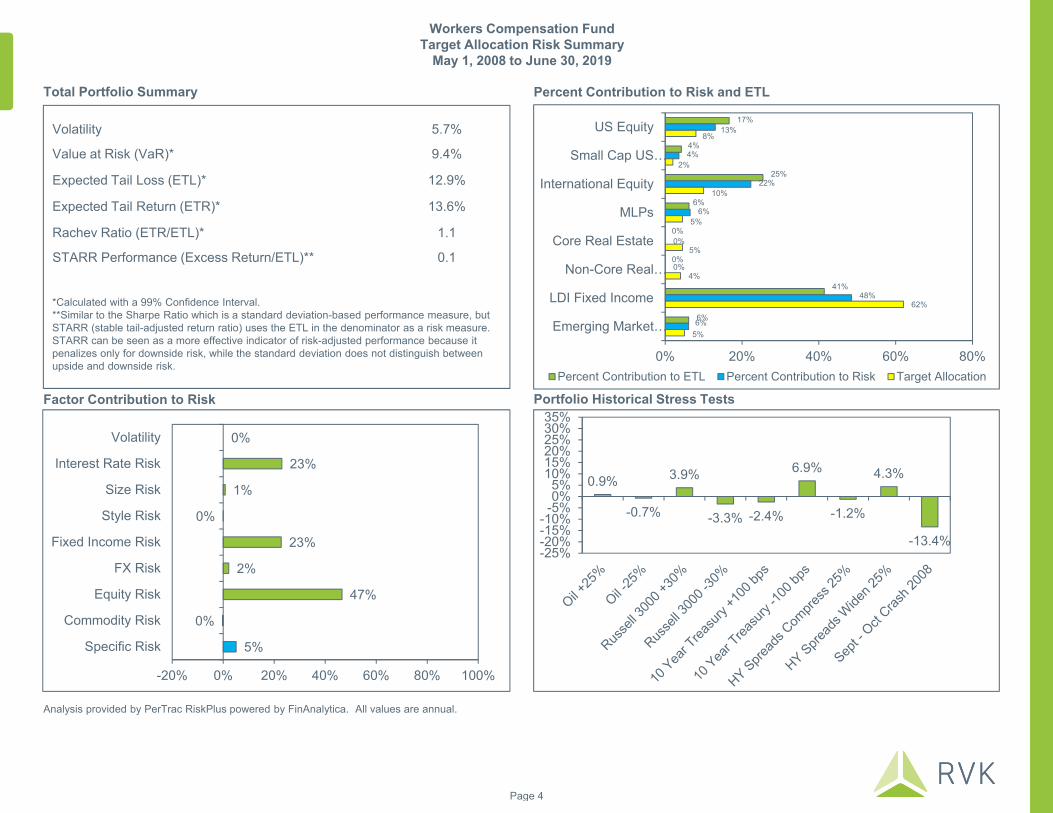

Workers Compensation FundTarget Allocation Risk Summary

May 1, 2008 to June 30, 2019

Analysis provided by PerTrac RiskPlus powered by FinAnalytica. All values are annual.

Factor Contribution to Risk Portfolio Historical Stress Tests

Percent Contribution to Risk and ETLTotal Portfolio Summary

*Calculated with a 99% Confidence Interval.**Similar to the Sharpe Ratio which is a standard deviation-based performance measure, but STARR (stable tail-adjusted return ratio) uses the ETL in the denominator as a risk measure. STARR can be seen as a more effective indicator of risk-adjusted performance because it penalizes only for downside risk, while the standard deviation does not distinguish between upside and downside risk.

Volatility 5.7%

Value at Risk (VaR)* 9.4%

Expected Tail Loss (ETL)* 12.9%

Expected Tail Return (ETR)* 13.6%

Rachev Ratio (ETR/ETL)* 1.1

STARR Performance (Excess Return/ETL)** 0.1

5%

0%

47%

2%

23%

0%

1%

23%

0%

-20% 0% 20% 40% 60% 80% 100%

Specific Risk

Commodity Risk

Equity Risk

FX Risk

Fixed Income Risk

Style Risk

Size Risk

Interest Rate Risk

Volatility

17%

4%

25%

6%

0%

0%

41%

6%

13%

4%

22%

6%

0%

0%

48%

6%

8%

2%

10%

5%

5%

4%

62%

5%

0% 20% 40% 60% 80%

US Equity

Small Cap US…

International Equity

MLPs

Core Real Estate

Non-Core Real…

LDI Fixed Income

Emerging Market…

Percent Contribution to ETL Percent Contribution to Risk Target Allocation

0.9%

-0.7%

3.9%

-3.3% -2.4%

6.9%

-1.2%

4.3%

-13.4%-25%-20%-15%-10%-5%0%5%

10%15%20%25%30%35%

Page 4

Pool ATarget Allocation Risk Summary

May 1, 2008 to June 30, 2019

Analysis provided by PerTrac RiskPlus powered by FinAnalytica. All values are annual.

Factor Contribution to Risk Portfolio Historical Stress Tests

Percent Contribution to Risk and ETLTotal Portfolio Summary

*Calculated with a 99% Confidence Interval.**Similar to the Sharpe Ratio which is a standard deviation-based performance measure, but STARR (stable tail-adjusted return ratio) uses the ETL in the denominator as a risk measure. STARR can be seen as a more effective indicator of risk-adjusted performance because it penalizes only for downside risk, while the standard deviation does not distinguish between upside and downside risk.

Volatility 4.2%

Value at Risk (VaR)* 6.6%

Expected Tail Loss (ETL)* 8.9%

Expected Tail Return (ETR)* 8.6%

Rachev Ratio (ETR/ETL)* 1.0

STARR Performance (Excess Return/ETL)** 0.1

7%

-1%

69%

0%

21%

0%

1%

2%

0%

-20% 0% 20% 40% 60% 80% 100%

Specific Risk

Commodity Risk

Equity Risk

FX Risk

Fixed Income Risk

Style Risk

Size Risk

Interest Rate Risk

Volatility

26%

4%

30%

15%

12%

0%

8%

6%

0%

22%

3%

28%

16%

13%

0%

11%

7%

0%

8%

1%

8%

5%

7%

8%

49%

10%

5%

-10% 0% 10% 20% 30% 40% 50%

US Equity

Small Cap US Equity

International Equity

MLPs

Preferred Stock

Non-Core Real Estate

Int. Duration Fixed Income

Bank Loans

Cash Equiv.

Percent Contribution to ETL Percent Contribution to Risk Target Allocation

1.0%

-1.0%

4.2%

-4.2%

0.6%

-0.2%

3.7%

-3.0%

-12.3%

-25%-20%-15%-10%-5%0%5%

10%15%20%

Page 5

LSRATarget Allocation Risk Summary

May 1, 2008 to June 30, 2019

Analysis provided by PerTrac RiskPlus powered by FinAnalytica. All values are annual.

Factor Contribution to Risk Portfolio Historical Stress Tests

Percent Contribution to Risk and ETLTotal Portfolio Summary

*Calculated with a 99% Confidence Interval.**Similar to the Sharpe Ratio which is a standard deviation-based performance measure, but STARR (stable tail-adjusted return ratio) uses the ETL in the denominator as a risk measure. STARR can be seen as a more effective indicator of risk-adjusted performance because it penalizes only for downside risk, while the standard deviation does not distinguish between upside and downside risk.

Volatility 4.1%

Value at Risk (VaR)* 7.5%

Expected Tail Loss (ETL)* 9.8%

Expected Tail Return (ETR)* 8.6%

Rachev Ratio (ETR/ETL)* 0.9

STARR Performance (Excess Return/ETL)** 0.1

27%

8%

40%

12%

6%

5%

1%

2%

24%

8%

38%

13%

5%

7%

2%

3%

7%

2%

9%

4%

6%

33%

33%

4%

0% 10% 20% 30% 40% 50%

US Equity

Small Cap US Equity

International Equity

MLPs

Diversified Hedge Funds

Int. Duration Fixed Income

Low Duration Fixed Income

Bank Loans

Percent Contribution to ETL Percent Contribution to Risk Target Allocation

2%

-1%

79%

1%

14%

1%

2%

2%

1%

-20% 0% 20% 40% 60% 80% 100%

Specific Risk

Commodity Risk

Equity Risk

FX Risk

Fixed Income Risk

Style Risk

Size Risk

Interest Rate Risk

Volatility

1.2%

-1.2%

4.7%

-4.7%

1.0%

-1.1%

3.9%

-3.4%

-11.3%

-25%-20%-15%-10%-5%0%5%

10%15%20%

Page 6

Stress Test Summary

Fund Permanent Mineral Trust

Permanent Land Fund

University Permanent Land Fund

Hathaway Scholarship

Common School

Permanent Land Fund

Higher Education

Workers Comp.Fund

Pool A LSRA

Fund Value as of 6/30/2019 ($M) $7,972.0 $194.7 $26.2 $591.9 $4,078.5 $120.3 $2,234.3 $243.3 $1,554.8

Stress Test

Returns (%)

Oil +25% 1.9% 1.9% 1.9% 1.9% 1.6% 1.6% 0.9% 1.0% 1.2%

Oil -25% -1.8% -1.8% -1.8% -1.8% -1.5% -1.5% -0.7% -1.0% -1.2%

Russell 3000 +30% 7.3% 7.3% 7.3% 7.3% 5.7% 5.7% 3.9% 4.2% 4.7%

Russell 3000 -30% -7.3% -7.3% -7.3% -7.3% -5.7% -5.7% -3.3% -4.2% -4.7%

10 Year Treasury +100 bps 2.8% 2.8% 2.8% 2.8% 1.8% 1.8% -2.4% 0.6% 1.0%

10 Year Treasury -100 bps -4.0% -4.0% -4.0% -4.0% -2.3% -2.3% 6.9% -0.2% -1.1%

HY Spreads Compress 25% 7.0% 7.0% 7.0% 7.0% 5.6% 5.6% -1.2% 3.7% 3.9%

HY Spreads Widen 25% -6.5% -6.5% -6.5% -6.5% -4.9% -4.9% 4.3% -3.0% -3.4%

Sept - Oct Crash 2008 -17.2% -17.2% -17.2% -17.2% -15.6% -15.6% -13.4% -12.3% -11.3%

Stress Test

Returns($M)

Oil +25% $154.3 $3.8 $0.5 $11.5 $64.5 $1.9 $19.4 $2.5 $18.0

Oil -25% -$144.7 -$3.5 -$0.5 -$10.7 -$60.1 -$1.8 -$15.5 -$2.5 -$18.2

Russell 3000 +30% $585.1 $14.3 $1.9 $43.4 $232.9 $6.9 $86.5 $10.3 $73.1

Russell 3000 -30% -$578.8 -$14.1 -$1.9 -$43.0 -$231.7 -$6.8 -$74.0 -$10.2 -$73.2

10 Year Treasury +100 bps $225.6 $5.5 $0.7 $16.7 $74.6 $2.2 -$54.5 $1.4 $16.2

10 Year Treasury -100 bps -$316.5 -$7.7 -$1.0 -$23.5 -$95.4 -$2.8 $154.6 -$0.6 -$17.4

HY Spreads Compress 25% $555.6 $13.6 $1.8 $41.3 $227.2 $6.7 -$27.3 $8.9 $61.1

HY Spreads Widen 25% -$516.6 -$12.6 -$1.7 -$38.4 -$198.2 -$5.8 $97.0 -$7.4 -$53.3

Sept - Oct Crash 2008 -$1,372.2 -$33.5 -$4.5 -$101.9 -$634.5 -$18.7 -$298.7 -$29.8 -$175.9

Page 7