2020 kitchen & bath market outlook - nkba

TRANSCRIPT

2020 Kitchen & BathMarket Outlook

— S e p t e m b e r U p d a t e —

About This ReportThe National Kitchen & Bath Association commissioned the highly regarded John Burns Real Estate Consulting company (JBREC) to produce this kitchen and bath industry report. In addition to quantifying the overall size of the kitchen and bath market, this analysis reviews current housing industry factors and consumer behaviors impacting 2020 industry growth.

JBREC’s analysis employed research from a wide variety of sources: (1) secondary research (e.g., U.S. Census American Housing Microdata, National Apartment Association (NAA) Spending, National Association of Realtors, Moody’s Analytics, Home Innovation Research Labs (HIRL), (2) home improvement estimates and forecasts from John Burns’ proprietary studies and consultants; and (3) a custom study conducted among 1,048 consumers who recently completed, started, or were planning but who abandoned or postponed a kitchen or bath remodel project.

NKBA’s 2020 Kitchen & Bath Market Outlook provides a comprehensive view of the U.S. residential kitchen and bath industry. New construction spending estimates include both single family and multi-family units. Remodeling spending estimates include improvements to both owner-occupied and rental properties. All dollar figures cited in this report include both products and labor (installed costs).

In light of the COVID-19 pandemic, this research will be conducted three times per year to continually revise the contents of this report.

Report Contents

Study Overview

Housing Industry Factors Impacting 2020 K&B Growth

Project Details and Financing

4

Impact Of COVID-19 on Consumer Behavior

Appendix:• Detailed Methodology• Historical K&B Market Size• Consumer Demographics

Industry Size and 2020 Growth

5 Executive Summary

8

15

31

48

53

59Impact of COVID-19 on K&B Project Spending

Project Motivations / Obstacles40

Cover Project Designed By: Sarah Robertson, AKBD Photographer: Adam Macchia

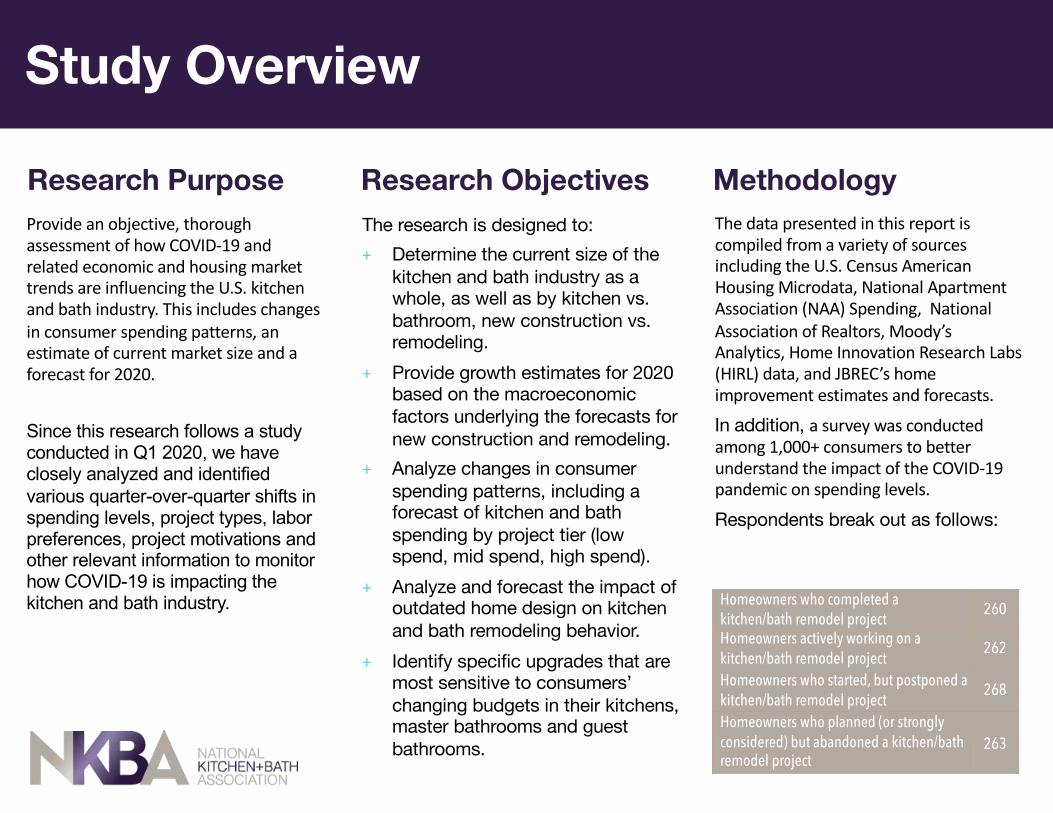

Provide an objective, thorough assessment of how COVID-19 and related economic and housing market trends are influencing the U.S. kitchen and bath industry. This includes changes in consumer spending patterns, an estimate of current market size and a forecast for 2020.

Since this research follows a study conducted in Q1 2020, we have closely analyzed and identified various quarter-over-quarter shifts in spending levels, project types, labor preferences, project motivations and other relevant information to monitor how COVID-19 is impacting the kitchen and bath industry.

The research is designed to:+ Determine the current size of the

kitchen and bath industry as a whole, as well as by kitchen vs. bathroom, new construction vs. remodeling.

+ Provide growth estimates for 2020 based on the macroeconomic factors underlying the forecasts for new construction and remodeling.

+ Analyze changes in consumer spending patterns, including a forecast of kitchen and bath spending by project tier (low spend, mid spend, high spend).

+ Analyze and forecast the impact of outdated home design on kitchen and bath remodeling behavior.

+ Identify specific upgrades that are most sensitive to consumers’ changing budgets in their kitchens, master bathrooms and guest bathrooms.

The data presented in this report is compiled from a variety of sources including the U.S. Census American Housing Microdata, National Apartment Association (NAA) Spending, National Association of Realtors, Moody’s Analytics, Home Innovation Research Labs (HIRL) data, and JBREC’s home improvement estimates and forecasts.

In addition, a survey was conducted among 1,000+ consumers to better understand the impact of the COVID-19 pandemic on spending levels.

Respondents break out as follows:

Homeowners who completed a kitchen/bath remodel project

260

Homeowners actively working on a kitchen/bath remodel project

262

Homeowners who started, but postponed a kitchen/bath remodel project

268

Homeowners who planned (or strongly considered) but abandoned a kitchen/bath remodel project

263

Research Purpose Research Objectives Methodology

Study Overview

Executive Summary

Designer: Gladys Schanstra, CKD, CBDPhotographer: Eric Hausman

The NKBA 2020 Kitchen & Bath Market Outlook – September Update provides a comprehensive review of current kitchen and bath industry conditions and the macroeconomic factors that are expected to impact the industry in 2020.

Executive Summary

6

Key findings from this research include:+ We have revised our 2020 residential kitchen and bath spending forecast upwards based on

improving demand fundamentals in both the new construction and repair and remodeling end-market.+ Spending on residential kitchen and bath products will now decline 6.1% in 2020 from $148.1 billion

in 2019 to $139.1 billion (compared to our previous expectation of -11.7%). It will be driven by a 3% decline in new construction spending and a 9.7% drop in kitchen and bath remodeling.

+ Although spending will decline in 2020, record-low interest rates are driving significant demand in the new home market and shifting lifestyles are inspiring more DIY activity, both of which are helping to offset a general shift to lower price points and smaller-scale kitchen and bath remodels.

+ The kitchen and bath remodeling industry continues to be impacted by project postponements and cancellations as of mid-August, well after state-wide stay-at-home orders ended. The industry reports safety concerns, lack of available professional remodelers, rising project costs and other financial/budgetary concerns as the primary reason for postponing or canceling their remodeling project.

+ One in two households remain optimistic about resuming their previously deferred project yet this year, while 30% say they plan to resume their postponed or canceled project at some point next year.

+ Homeowners who have completed their remodeling projects during the pandemic continue to do so at lower price-points and have been more likely to use do-it-yourself (DIY) labor. In Q2, average project spending declined 48% to $6,000 from $12,500 in Q1.

+ Low-priced kitchen and bath product spending will outperform all other price tiers, declining only 1% in 2020 compared to -6.1% across all price points. In contrast, mid-priced spending will decrease by the greatest amount, -10.1%, as most American consumers broadly shift to more affordable products and finishes to save money during uncertain economic times.

+ These spending trends represent a clear reversal from overall industry growth of 3.8% in 2019, driven by growth of 7.5% for remodeling and 0.7% for new construction before the pandemic hit.

+ Prior to the pandemic consumers reported primary motivations for kitchen and bath remodeling were increasing the home’s value (24%) and personalizing the home’s design (23%). During the pandemic, however, households report being motivated primarily by repair/replacement needs than by design enhancement desires.

+ Consumers increasingly cite needing “more functional space” as a primary motivation to remodel. Not surprising as nine in 10 households who had an adult working from home during Q1 report they are still working from home “most of the time."

+ An aging stock of homes 40+ years old and outdated designs in homes built or remodeled in the mid-2000s, however, should drive demand for full-scale kitchen and bath remodeling next year and beyond. Kitchen and bath designs become outdated after 15 years, with cabinets and faucets being the first product categories to be outdated (relative to current trends).

+ Homeowners still primarily fund their kitchen or primary bath remodel with cash from their savings (64%).

Executive Summary

7

Kitchen & Bath Industry Size and Growth

Designer: Courtney J. SeavallPhotographer: Stacy Gillespie

9

2020 ForecastProjected Growth by Construction Type

$77.1

$62.0

$139.1

Remodel

Residential Kitchen and Bath Spending ($ Billions)

New Construction

2020 Spending Growth% change vs. prior year

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Sep 2020)All dollars include both products and labor (installed costs). Definitions and methodology pertaining to New Construction and Remodeling can be found on page 53.

-9.7%

-3%

-6.1%

Kitchens$62.0

Bathrooms$77.1

2020 ForecastProjected Value by Segment

$62.0

$77.1

$139.2Kitchens

Bathrooms

Residential Kitchen and Bath Spending ($ Billions)

10

New Construction

$34.5Remodel

$27.5

New Construction

$42.6

Remodel$34.5

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Sep 2020)Notes: All dollars include both products and labor (installed costs). Definitions and methodology pertaining to New Construction and Remodeling can be found on page 53.

$62.0

$77.1

Kitchens

Bathrooms

11

2020 ForecastProjected Value by Segment

Residential Kitchen and Bath Spending ($ Billions)

2020 Spending Growth% change vs. prior year

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Sep 2020)All dollars include both products and labor (installed costs).

-0.5%

-12.1%

• Minor "update" remodels, often DIY.

• Low-cost products often found in new "starter" homes.

• Usually funded out-of-pocket.

12

Kitchen & Bath Activities by Spend Level

L O W

$$ $$$$

M E D I U M H I G H

• Medium-scale kitchen and bath remodels.

• Products in first or second "move-up" homes.

• Partially funded from cash proceeds from home sale, investments, etc.

• Major full-service remodels, usually using a designer and showroom.

• High-end products in new luxury homes.

• Upgrades financed via bank loan or HELOC, in addition to funding from other sources.

Low-spend Price Point

High-spend Price Point

Mid-spend Price Point

13

Spending in Mid-Price Point Segment Will Decline MoreThan Low-Price and High-Price Point Tiers

$130.8

2020

Gro

wth

Residential Kitchen and Bath Spending ($ Billions)

$36.8 $53.7 $48.5

$ $$ $$$

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Sep 2020)

Note: Low-Spend, Mid-Spend and High-Spend price point estimates were computed using averages based on these project scale definitions: Small scale: <$1,600 for bathrooms and <$2,200 for kitchens; Medium-scale: $1,600-$13,600 for bathrooms and $2,200-$17,700 for kitchens; Large-scale: >$13,600 for bathrooms and >$17,700 for kitchens. As a result, the market size estimates for these three price points do not exactly total $139.1 billion.

-1.0% -10.1% -5.2%-6.1%

14

Kitchen and Bath Spending was Increasing Steadily Prior to the Pandemic

Residential Kitchen and Bath Spending ($ Billions) by Spend Level

Before COVID-19 caused spending to drop in 2020, total residential kitchen and bath spending grew 9% in 2018 and 4% in 2019, with growth in all spend levels.

Sources: Census AHS Microdata, NAA, John Burns Real Estate Consulting LLC (Pub: Sep 2020)

Note: Low-Spend, Mid-Spend and High-Spend price point estimates were computed using averages based on these project scale definitions: Small scale: <$1,600 for bathrooms and <$2,200 for kitchens; Medium-scale: $1,600-$13,600 for bathrooms and $2,200-$17,700 for kitchens; Large-scale: >$13,600 for bathrooms and >$17,700 for kitchens. As a result, the market size estimates for these three price points do not total $130.8 billion.

$33

$53 $45

$36

$57 $50

$37

$60 $51

$37

$54 $49

$0

$10

$20

$30

$40

$50

$60

$70

Low Mid High

2017 2018 2019 2020

Key Housing Industry Factors Impacting2020 Kitchen & Bath Industry Growth

Designer: Janice J. Page, CKDPhotographer: Rob Karosis

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Real GDP Fell 33% YOY in Q2 on an Annualized Basis

16

Real GDP – % Change Quarter-Over-Quarterseasonally adjusted (annualized) real GDP declined 33% in Q2

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Housing and Home Improvement is Leading Economy Out of the Recession, Just Like the 2002 Recovery

17

Housing as a percentage of GDP is now 21.7%

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Total Employment Rose to 140M in July, Up 1.8M Jobs from June; US Employment Still Down 12M From Cycle Peak

18

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

129M

131M

133M

135M

137M

139M

141M

143M

145M

147M

149M

151M

153M

2000

2000

2001

2001

2002

2002

2003

2004

2004

2005

2005

2006

2007

2007

2008

2008

2009

2009

2010

2011

2011

2012

2012

2013

2014

2014

2015

2015

2016

2016

2017

2018

2018

2019

2019

2020

Total US Payroll Employment

Jobs at Cycle High

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

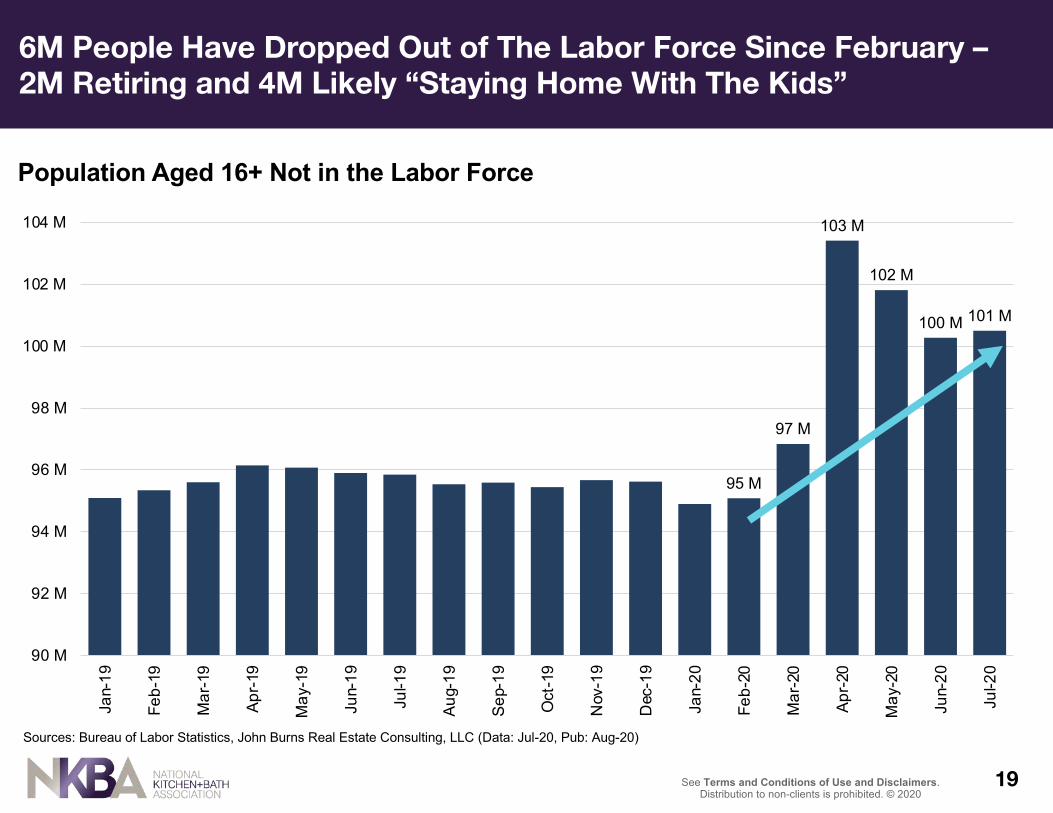

6M People Have Dropped Out of The Labor Force Since February –2M Retiring and 4M Likely “Staying Home With The Kids”

19

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

95 M

97 M

103 M

102 M

100 M 101 M

90 M

92 M

94 M

96 M

98 M

100 M

102 M

104 M

Jan-

19

Feb-

19

Mar

-19

Apr-1

9

May

-19

Jun-

19

Jul-1

9

Aug-

19

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr-2

0

May

-20

Jun-

20

Jul-2

0

Population Aged 16+ Not in the Labor Force

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Primary Homeowner Cohort (Aged 35 to 54) Have Lower Unemployment Rates Relative to Historical Avgs Than Young Workers

20

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

17.9%

10.3%

6.3%4.8% 4.2% 4.0%

19.3%18.3%

11.4%

8.1% 7.8%8.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

16-19 years 20-24 years 24-34 years 35-44 years 45-54 years 55+ years

July 2020 Unemployment Rate vs. Historical Average by AgeHistorical Average July Unemployment

Younger workers, who typically rent, have been hit much harder by layoffs than those aged 35 to 54.

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Low-Income Sectors Like Leisure/Hospitality and Retail See More Job Losses Relative to Higher Income Sectors

21

Cumulative Q2 Job Losses by Employment Sector

-292K-317K-433K

-795K-1.0M

-1.5M-2.0M

-3.1M-3.2M-3.4M

-5.3M-5.4M-5.5M

-19.4M

-25 M -20 M -15 M -10 M -5 M 0 M

Utilities

Mining

Financial Activities

Information

Wholesale Trade

Transportation and Warehousing

Construction

Other Services

Manufacturing

Government

Retail Trade

Professional Business Services

Education and Health Services

Leisure and HospItality

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Most US Job Losses Have Been Temporary; Permanent Job Losses Thus Far Up Only 1.6 Million from Pre-COVID Level

22

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

0.8 1.8

18.115.3

10.6 9.2

0.62.1

8.1

5.4

2.82.5

1.44.0

26.1

20.8

13.411.7

0 M

5 M

10 M

15 M

20 M

25 M

30 M

February March April May June July

Employed but not at work for "other reasons" Temporary Layoff

1.3 1.5 2.0 2.3 2.9 2.9

0 M

5 M

10 M

15 M

20 M

25 M

30 M

February March April May June July

Temporary Job Losses Permanent Job Losses

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

‘Permanent’ Unemployment Low Compared to Prior Recessions

23

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

7.1%

4.0%

6.5%

4.6%

10.5%

3.7%

5.9%

5.6%

3%

4%

5%

6%

7%

8%

9%

10%

11%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Permanent Unemployment

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Small Business Hiring Plans Have Returned to Normal

24

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

Small business hiring plans now above long-term average

0

10

20

30

40

50

60

70

80

90

100

2.0% 3.0% 4.0% 5.0% 6.0% 7.0%Mortgage Rate

$200k Mortgage $400K Mortgage $600K Mortgage

Num

ber o

f Hou

seho

lds

Who

Can

Qua

lify

Source: John Burns Real Estate Consulting, LLC (Data: Aug-20, Pub: Aug-20)

National Mortgage Rate Sensitivity

Current Rate: 2.88%

Lower mortgage rates will drive home prices higher in 2020 as more consumers qualify to buy homes. An estimated 4.5 million additional households will meet criteria for obtaining a $200K mortgage.

~1% Lower Mortgage Rates Than 1 Year Ago Driving Increased Demand for Homes Across Buyer Segments

number of households in millions

4.5M morehouseholds now qualify mortgage rates are -87bp

lower than last year

25

Applications to Purchase a Home Rebounded to Pre-COVID Levels in June and July After Severe Initial Decline in April

180

200

220

240

260

280

300

320

340

Jan-

18

Feb-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct

-18

Nov

-18

Dec

-18

Jan-

19

Feb-

19

Mar

-19

Apr-1

9

May

-19

Jun-

19

Jul-1

9

Aug-

19

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr-2

0

May

-20

Jun-

20

Jul-2

0

Source: MBA (Data: Jul-20, Pub: Sep-20)

Purchase Mortgage Application Indexseasonally adjusted weekly values

26

Note: The index does not capture cash transactions and thus understates actual total home buying activity.

Share of Loans in Forbearance Has Steadily Fallen Since May;Re-Hiring Activity Should Drive Share Below 7.2% in Near Term

27

6.4%4.9%

8.6%7.2%

10.9%

10.3%11.7%

9.5%

0%

2%

4%

6%

8%

10%

12%

14%

March 8

March 1

5

March 2

2

March 2

9Apri

l 5

April 1

2

April 1

9

April 2

6May

3

May 10

May 17

May 24

May 31

June

7

June

14

June

21

June

28Ju

ly 5

July

12

July

19

July

26

Augus

t 2

Augus

t 9

Loans in Forbearance as % Share of Servicing PortfolioFannie Mae and Freddie Mac Total Private label and portfolio loans Ginnie Mae

Source: Mortgage Bankers Association (Data: Aug-20; Pub: Aug-20)

5%

7%

-5%

-7%

-18%

-17% -1

3%

-12%

-6%

-8% -4

%

-8% -3

%

3%

10% 14

%

29%

28%

21%

15%

-3%

-30%

-3%

17%

33%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jul-1

8

Aug-

18

Sep-

18

Oct

-18

Nov-

18

Dec-

18

Jan-

19

Feb-

19

Mar

-19

Apr-1

9

May

-19

Jun-

19

Jul-1

9

Aug-

19

Sep-

19

Oct

-19

Nov-

19

Dec-

19

Jan-

20

Feb-

20

Mar

-20

Apr-2

0

May

-20

Jun-

20

Jul-2

0

YOY Burns National Starts Index

*Note: The above chart shows YOY comparisons only for builders who participated in the survey one year prior. For the July survey, YOY comparisons include 235 responses.

Source: John Burns Real Estate Consulting, LLC, independent survey of ~23% of all US new home sales, NSA (Data: Jul -20, Pub: Aug-20)

July’s 33% YOY Increase in New Home Starts Reflects the Largest Increase Since 2015; Kitchen & Bath Installs Lag Starts by 2-3 Months

28

Kitchen and bath product installations typically lag starts by 2-3 months

Record Low For-Sale Inventory Indicates Housing Stock is Set for Price Appreciation – a Tailwind for Large-Scale Remodels

1.4M

1.8M

2.3M

2.7M

3.2M

3.6M

4.0M

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Existing inventory = 1.53 mil (-20% YOY)Historical average* = 2.37 mil

Sources: NAR; John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20)

Existing Home Inventory for Sale3-month average (non seasonally adjusted)

*Historical Average: Jun-82 through current

29

See Terms and Conditions of Use and Disclaimers.Distribution to non-clients is prohibited. © 2020

Real Income Growth of 6.6% YOY in July Will Drive Increased Spending on Both Big and Small Remodeling Projects

-5%

0%

5%

10%

15%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Real Personal Income Growth = 6.6%Real Personal Income (RPI) YOY % change

Source: St. Louis Fed; John Burns Real Estate Consulting (Data: Jul-20, Pub: Aug-20)

30

Impact of COVID-19 on Kitchen and Bath Project Spending

Designer: Dvira Ovadia Photographer: Valerie Wilcox

Homeowners report in Q2 that most (64%) of the kitchen and bath projects they planned for 2020 have been either cancelled or postponed as of July 2020, even after most US markets “re-opened the economy” at the end of May. In Q2, however, the percentage of homeowners actively working on their project nearly doubled, a strong improvement on a quarter-over-quarter basis.

Q2 Project Statuses Improve; 36% of Homeowners Now Actively Working on Their Projects, Fewer Canceled or Postponed Projects

Source: John Burns Real Estate Consulting LLC (Data: Jul-20, Pub: Sep 2020)Includes homeowners age 24+. ‘Planned a project’ includes those who started their project as well as those who strongly considered a project for 2020 but had to cancel.

Actively Working On It19%

Actively Working On It36%

Postponed40%

Postponed31%

Canceled41%

Canceled33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2020 Q2 2020

8% improvementover Q1 2020

15% improvementover Q1 2020

Status of “Planned Projects” – Q1 vs Q2

32

Homeowners that remodeled during Q2 spent less overall than homeowners who remodeled during Q1. Total project spending on active projects in Q2 averaged $6,000 or 48% lower than Q1 average total spending per project of $12,500. Many consumers report doing more labor themselves (DIY) and selecting more affordable finishes as deliberate measures taken to bring overall project costs down.

Q1 Average Project Spending

$- $2,000 $4,000 $6,000 $8,000

$10,000 $12,000 $14,000 $16,000

Active Postponed /Cancelled

Source: John Burns Real Estate Consulting LLC (Data: Apr-20, Pub: June 2020)Notes: Excludes whole house remodels / other category. Spend levels refer to spending consumers budgeted for 2020 before their plans were impacted by COVID-19.

Average Spend on K&B Projects Declined in Q2

Q2 Average Project Spending

$- $2,000 $4,000 $6,000 $8,000

$10,000 $12,000 $14,000 $16,000

Active Postponed /Cancelled

33

Source: John Burns Real Estate Consulting LLC (Data: Apr-20, Pub: Sep 2020)Includes all homeowners whose project was in any way impacted by COVID-19 among those who were actively working on, completed, or who had postponed a project.

24%

21%

19%

18%

10%

10%

Our finances/budget became more limited

Project materials were not available

I became more involved in project design/planning

We had more time to pursue do-it-yourself (DIY) work

Scope of project was reduced

The pandemic motivated us to undertake the project

Limited Household Finances, Lack of Product Availability Negatively Impacting Projects in 2020

Impact of COVID-19 on Remodeling Households Included:

In addition to projects being postponed and delayed by the pandemic, households that were planning projects for 2020 continue to cite other negative impacts: more limited budgets/finances (24%), lack of project materials (21%) and reduced project scope (10%). Yet others reported positives, like more time for DIY work (18%) and greater involvement in project design/planning (19%).

34

35%

22%18%

25%

16%

38%

9%

36%36%32%

16% 16%

I will do all the work myself (DIY) I will hire a pro to do all the work(not a friend or family member)

A friend or family member willdo all the work for me

I will rely on a combination of DIYand a professional or friend/family

Actively working Postponed Completed earlier this year

35% of Remodeling Jobs in Q2 Were DIY Projects, Households Postponing Projects Still Expect to Primarily Use Professionals

Labor Type by Project Status (Active vs Postponed vs Completed)

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

35

The primary labor type of remodeling households in Q2 2020 was DIY (35% of all households actively working on a project). Twenty-five percent of households did some of the labor themselves (DIY) and relied on a professional remodeler or a friend/family member for the remainder of the work, while 22% relied solely on a professional contractor or remodeler for their project. Most households who have postponed their remodel still expect to use a pro for the entire project (38% of households who postponed a project).

25%

35%

6%

34%35%

22%18%

25%

I will do all the work myself (DIY) I will hire a pro to do all the work(not a friend or family member)

A friend or family member willdo all the work for me

I will rely on a combination of DIYand a professional or friend/family

Q 1 Q 2 Q 1 Q 2 Q 1 Q 2

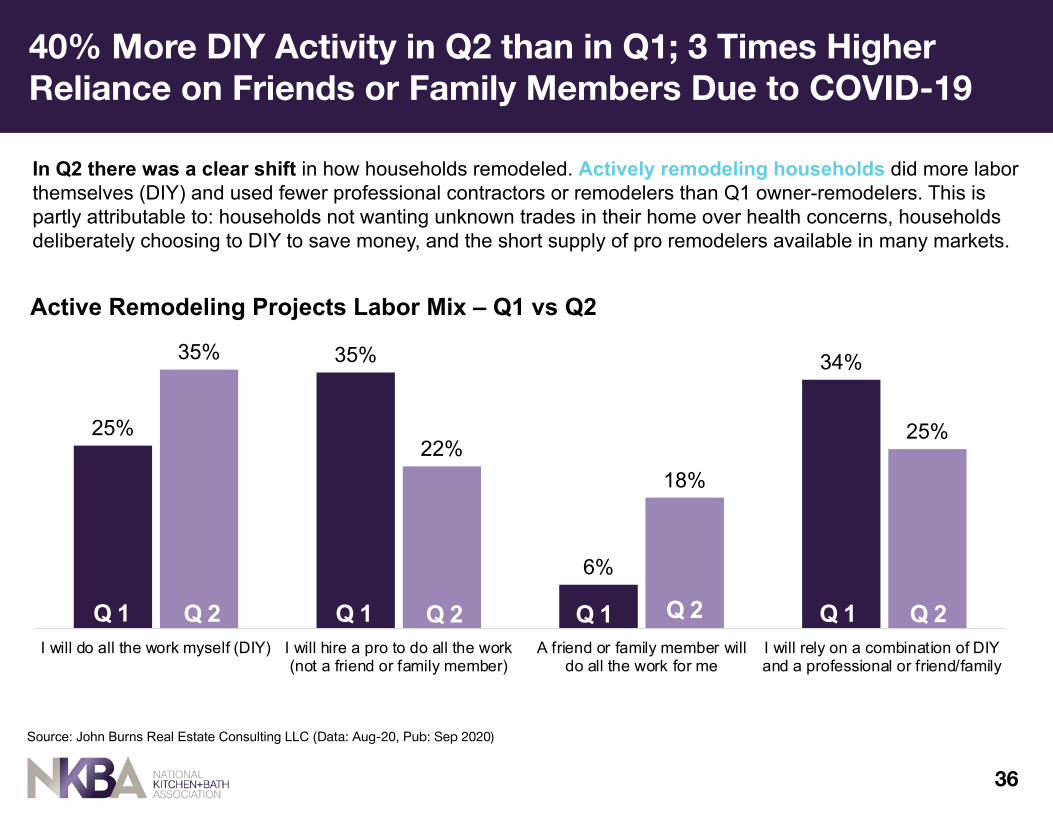

40% More DIY Activity in Q2 than in Q1; 3 Times Higher Reliance on Friends or Family Members Due to COVID-19

Active Remodeling Projects Labor Mix – Q1 vs Q2

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

36

Q 1 Q 2

In Q2 there was a clear shift in how households remodeled. Actively remodeling households did more labor themselves (DIY) and used fewer professional contractors or remodelers than Q1 owner-remodelers. This is partly attributable to: households not wanting unknown trades in their home over health concerns, households deliberately choosing to DIY to save money, and the short supply of pro remodelers available in many markets.

Households Say They Shifted to DIY Over Health Concerns, Financial Reasons and Timeline Constraints

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

37

Q 1 Q 2

Households Tell Us Why They’ve Shifted to DIY“With the coronavirus health risks we decided just to do the replacements ourselves.”

“I don't want strangers in my home during the virus.”

“Due to COVID, we didn’t want people in our home.”

“The new tub, surround, plumbing and tile floor installation needs a contractor because I want it done right, but I decided I could do the rest to save money. It was the right decision as I work in the airline industry.”

“Originally was going to hire a contractor, but decided it was smart to save $5,000 right now.”

“I wanted to save money because I am worried about the economy so I asked my dad to help.”

“I need to preserve cash right now because my wife stopped working to watch the kids.”

“Labor quotes were over $15,000!! We decided to rely on YouTube to DIY.”

“The companies I called never called back and we couldn’t wait forever to do the project.”

“Remodelers are too busy right now and we needed to get a bathroom done for the kids.”

“Couldn’t get a contractor to fit us in so we did it ourselves.”

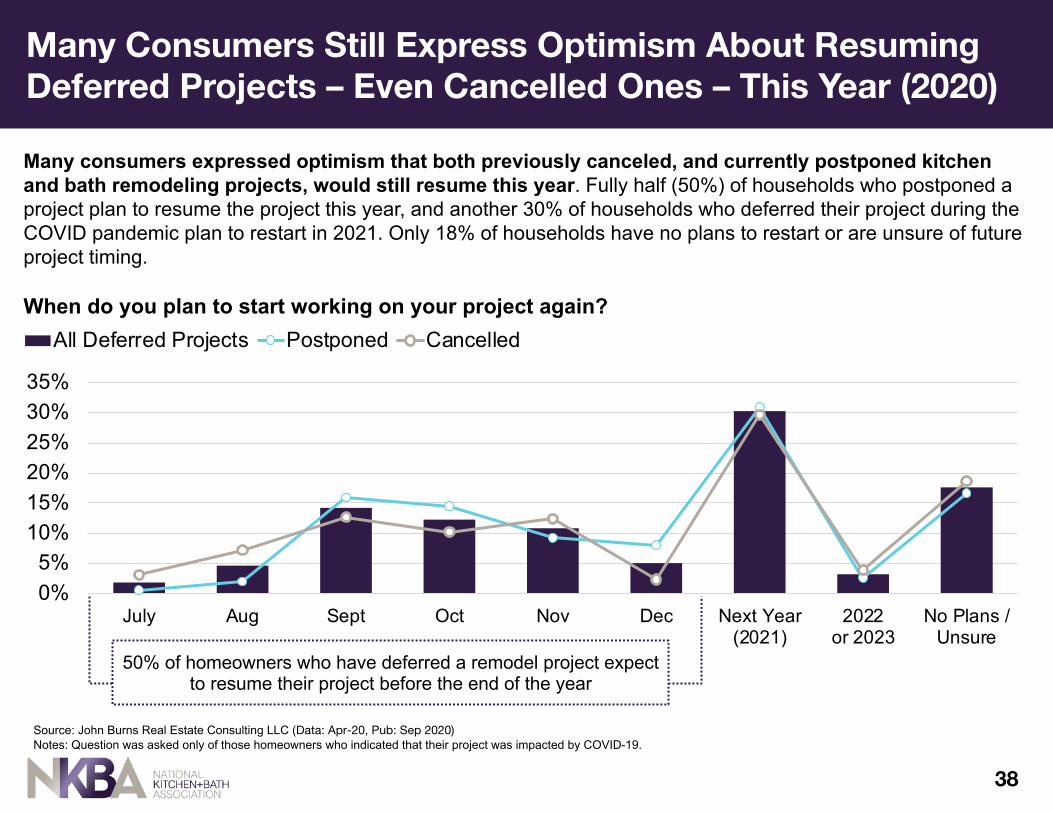

Many consumers expressed optimism that both previously canceled, and currently postponed kitchen and bath remodeling projects, would still resume this year. Fully half (50%) of households who postponed a project plan to resume the project this year, and another 30% of households who deferred their project during the COVID pandemic plan to restart in 2021. Only 18% of households have no plans to restart or are unsure of future project timing.

Many Consumers Still Express Optimism About Resuming Deferred Projects – Even Cancelled Ones – This Year (2020)

When do you plan to start working on your project again?

0%5%

10%15%20%25%30%35%

July Aug Sept Oct Nov Dec Next Year(2021)

2022or 2023

No Plans /Unsure

All Deferred Projects Postponed Cancelled

50% of homeowners who have deferred a remodel project expect to resume their project before the end of the year

Source: John Burns Real Estate Consulting LLC (Data: Apr-20, Pub: Sep 2020)Notes: Question was asked only of those homeowners who indicated that their project was impacted by COVID-19.

38

While 37% of homeowners completing projects in the second quarter of 2020 hired a designer, only 26% of those still actively working on a project did so. Designers were less likely to be utilized across kitchen and bathroom projects alike as households tighten budgets in an uncertain economic environment.

Designer Usage Declined During Pandemic

% of Homeowners Hiring Pro Designers

We are saving in every area we can right now. We don’t have the extra cash for a designer.”

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

26%

22%19%

32% 30% 30%

37% 36%34%

0%

5%

10%

15%

20%

25%

30%

35%

40%

All Projects Bathroom Kitchen

Actively working Postponed Completed

% of Active Projects Involving a Pro Designer

26%

74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Yes No

39

Project Motivations / Obstacles

Designer: Jaque BethkePhotographer: John Magnoski

Top Reasons Consumers Remodeled a Kitchen or Bath in Q2

Among consumers who recently remodeled their kitchen or bathroom, 20% said “to replace worn-out features” was their primary motivation. Another 15% cited “to repair damage” as their primary project motivation, followed by “update my home’s design” (14%). Compared to prior quarter, responses show consumers are increasingly focusing on replacements and repairs than full-scale remodels where updating design, home value creation, and adding luxury features have typically been the primary project motivations.

Households Increasingly Motivated by Repair and Replacement Needs than by Remodel or Design Factors

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

20%

15%14% 13% 13%

6%4% 4% 4% 3% 3% 2%

0%

5%

10%

15%

20%

25%

To replaceworn-outfeatures

To repairdamage

To update myhome's design

To increase myhome's value

To add luxury tomy home

To add morefunctional space

To increaseenergy

efficiency

To make myhome easier to

age-in-place

To restore myhome to it's

original design

To incorporatesmart home

products

To protect myfamily fromCoronavrius

To prepare myhome for sale

41

Top Obstacles Consumers Historically Face When Remodeling Their Kitchen or Bath

26%

20% 20%

12%10%

8%

3% 2%

0%

5%

10%

15%

20%

25%

30%

Choosing the rightmaterials or

products

Obtaining thefunds to start the

project

Finding the time tocomplete the

project

Finding the rightpeople to do the

job (labor)

Dealing withunexpected

problems relatedto the project

Staying within mybudget

Learning how todo things myself

Staying onschedule with

deadlines

Prior to the pandemic, more than one-quarter of all homeowners reported that the biggest obstacle they faced when remodeling their kitchen or bath was ‘‘choosing the right materials or products.” Obtaining funds to start the project was the next largest obstacle (20%) along with finding time to do the work (20%).

Top Obstacles Consumers Face When Remodeling

Source: NKBA/ JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Nov-19, Pub: Sep 2020)

42

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)Includes all homeowners whose project was in any way impacted by COVID-19 among those who were actively working on, completed, or who had postponed a project.

55%

34%

20%

12%

12%

12%

9%

8%

Project was delayed or postponed due to COVID-19

Cost of project outside my budget

Timing is bad for other reasons un-related to the pandemic

Dealing with unexpected problems related to the project

Dealing with unexpected problems not related to the project

Decided to focus on improving different part of home instead

Could not find the right people to do the job

Could not get financing

Project Cost Increasingly the Main Reason for Cancellations

Primary Reasons for Project Cancellation in Q2

More than half of households (55%) with cancelled projects report the pandemic remains the primary reason they were unable to complete their project. Compared to prior quarter, households increasingly selected cost as the primary reason they were unable to complete their project; 34% of households selected ‘cost of project outside my budget” as the main barrier to completion vs 27% of households in Q1.

43

40 yrs or older

There was a noticeable increase in Q2 remodeling activity in homes under 20 years old. Typically, over 50% of kitchen and bath remodeling activity is done in homes over 40 years old; however, in Q2, there was a clear shift towards homeowners doing smaller-scale kitchen and bath updates to homes built in the mid-2000s and fewer large-scale, high-budget remodels typically seen in more outdated/ much older homes.

10 - 20 yrs 30 - 40 yrs< 10 yrs 20 - 30 yrs

25%

17% 16%

8%

35%

22%20%

12% 13%

33%

8%

27%

11%

24%29%

0%

10%

20%

30%

40%

50%

Q2 Remodels Completed by Age of Home and Project Type

44

Most Q2 Kitchen and Bath Repair/Remodel Projects Still Occurred in Homes 40+ Years or Older

Kitchen Primary Bathroom Secondary Bathroom

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

44

K&B Designs Become Outdated After 15 Years

0%

-23%-27%

-72%-79%

0%

-10%

-23%

-43%

-78%

0%

-21%

-39%

-61%

-80%

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%< 2 Years Old 3-5 Years Old 6-10 Years Old 11-15 Years Old 16-20 Years Old

Cabinets Faucets Plumbing Fixtures

Kitchen and Bath Design Obsolescence Progression

Sources: JBREC calculations of HIRL data, John Burns Real Estate Consulting LLC (Pub: Sep 2020)

16 to 20 years after kitchens and baths are installed, 80% of the design features will have changed compared to current trends

45

0%

-23%-27%

-72%-79%

0%

-10%

-23%

-43%

-78%

0%

-21%

-39%

-61%

-80%

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%< 2 Years Old 3-5 Years Old 6-10 Years Old 11-15 Years Old 16-20 Years Old

Cabinets Faucets Plumbing Fixtures

Cabinets:Shift from raised-panel to flat-panel 10 years ago

Sources: JBREC calculations of HIRL data, John Burns Real Estate Consulting LLC (Pub: Sep 2020)

Cabinets and Faucets are First to be Outdated

Faucets:Shift away from chrome over last 15 years

Kitchen and Bath Design Obsolescence Progression

46

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Housing Starts

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Big Project Remodels

20 Years Outdated

Peak Housing Starts from Mid-2000s Outdated

Favorable Tailwinds for Discretionary K&B Spending:

• Peak housing starts ofmid-2000s are now 15 to 20 years old, due for kitchen and bath remodels.

• Wave of major remodels in 2005 to 2008, now 12 to 15 years old, will soon boost K&B demand in the next few years.

Wave of Outdated New Homes and Remodels from Early 2000 are Now Eligible for Upgrades

20 Years Outdated

Wave of Major Remodels from Mid-2000s Due For

Update

Sources: John Burns Real Estate Consulting LLC (Pub: Sep 2020)

47

Project Details and Financing

Designer: Christopher HooverPhotographer: Jacob Elliott

6154 49

37 34 3223 19

13 11

7974

56 5459

29 26

50

32

50

102030405060708090

100

Paint Flooring Lighting Cabinets Tile Plumbing Shelving Countertops Appliances Smart HomeTech

<$4000 >$4000+

Kitchen upgrades become less common across all categories when consumers’ budgets fall below $4,000. Big-ticket items, like countertops, cabinets and appliances generally have the most significant downticks. In Q2, kitchen upgrades dropped across categories with big-ticket upgrades dropping more than small ticket categories.

Number of Upgrades per 100 Completed Kitchen Remodels

Big-Ticket Categories like Cabinets, Countertops and Appliances are Less Likely Upgrades with Smaller Budgets

49

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

Upgrades in the primary bath become less common across all categories when budgets fall below $4,500. Flooring, lighting, countertops and cabinets have the most significant downticks, while the small-ticket item of paint remains virtually unchanged. Small ticket upgrades remained common in Q2 as households did more DIY.

Number of Upgrades per 100 Completed Primary Bath Remodels

Small Ticket Upgrades like Flooring, Paint, Tile, Lighting Common in Q2 as Households Shift to Smaller Budgets & DIY

50

68

5445 44

3628

23 21 17 14

7972 69

78

3544 48 48

20

8

0102030405060708090

100

Flooring Paint Tile Lighting Fixtures Faucets BathroomCabinets

Countertops MirroredCabinet

Smart HomeTech

<$4,500 >$4,500+

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

Number of Upgrades per 100 Completed Secondary Bath Remodels

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

51

6254 50

43 41 3933

19 1510

73

52

70

58 56 57 6055

22

10

0102030405060708090

100

Paint Faucets Flooring Fixtures Countertops Lighting Tile BathroomVanity

MedicineCabinet

Smart HomeTech

< $3,500 > $3,500

Small Ticket Upgrades like Paint, Faucets, Flooring Common in Q2 as Households Shift to Smaller Budgets and DIY

Upgrades in the secondary bath also become less common across all categories when budgets fall below $4,500. Small-ticket upgrades in secondary baths remain virtually unchanged with larger budgets. In Q2, categories like paint, faucets and flooring benefitted as households focused on small-scale, DIY-friendly projects.

Primary Source of Project Financing for Projects Completed in Q2

The primary way consumers funded a kitchen or primary bath remodel in Q2 of 2020 continued to be with cash from their savings or checking accounts (64%). Coming in a distant second,13% said they primarily paid for their remodel on their credit card, slightly higher than the Q1 report. This mix overall is largely unchanged from Q1 financing sources.

Cash Remains the Primary Means of Financing Kitchen and Bath Projects in Q2 2020

64%13%

8%8%7%

7%4%

4%3%3%

2%2%2%

0% 10% 20% 30% 40% 50% 60% 70%

Cash from savings or checking

Credit card

Cash from home refinance

Cash from a work bonus or profit share

Income tax return

Cash from investment liquidation

Cash from an inheritance or gift

Cash from a home sale

Financing through contractor or remodeler

Homeowners insurance settlement

Financing through retailer

Home equity loan or line of credit (HELOC)

Cash from a life insurance policy

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

52

Impact of COVID-19 on Consumer Behavior

58%

34%

8%

We are highly cautious,making major changes to

our lifestyle

We are somewhat cautious,making some limited

changes to our lifestyle

We are generally notfearful of the virus

COVID-19 Still Has Households Highly Cautious About Their Lifestyles; Most Continue to Make Major Day-to-Day Changes

Household Sentiment Related to the COVID-19 Pandemic and Lifestyle Changes

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

54

Cooking all meals at home to save money and to limit our time in public spaces.

My husband and I are both working from home and we are not sending the kids to school for safety reasons. We need more functional space.

Time at home has made us aware of all the things we don’t like about our house. We want our high-touch areas to be easy to clean.

Household Sentiment Related to the COVID-19 Pandemic and Lifestyle Changes

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

55

55%

46%

45%

30%

18%

16%

7%

6%

0% 10% 20% 30% 40% 50% 60%

Cooking / eating more at home

Disinfect spaces more frequently

Spend more time in the kitchen

Buying / storing more supplies in bulk

Decontaminate mail / packages / groceries more

Spend more time in the bathroom

Use the kitchen to work remotely

Use the kitchen for remote schooling from home

Households are Cleaning Kitchens and Baths Often, Limiting Time in Public Spaces, and Working/Schooling at Home More

All the Time53%

Most of the Time24%

Occasionally13%

Not Anymore10%

54% of Households Did Not Have an Adult Working from Home During COVID, but Most Who Did Still Are “All the Time”

% of Households Working at Home During COVID-19 Shutdowns

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

56

Work from Home Status Now

46%

54%

Yes No

71%

22%

5%

3%

0% 10% 20% 30% 40% 50% 60% 70% 80%

We generally like living here and want to stay

We need to renovate our home to feel comfortable staying here

We feel uncomfortable here, but can't move soon

We feel uncomfortable here and plan to move

Amid the Covid-19 Pandemic, 9 out of 10 Households Have No Plans to Move Anytime Soon but 22% Want to Remodel Soon

Household Sentiment Related to the COVID-19 Pandemic and Lifestyle Changes

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

57

52%48%

47%

38% 38% 37%

30%

36%40% 40%

48% 49% 49%

53%

12%13% 13% 14% 13% 14%

17%

0%

10%

20%

30%

40%

50%

60%

Backyard Bathroom Kitchen Bedroom Living Room Home Office Guest Room

Almost Half of Households Report More Interest in Remodeling Baths (48%) and Kitchens (47%) Today than Prior to the Pandemic

Household Interest in Remodeling by Room Type “Post-Pandemic”

Source: John Burns Real Estate Consulting LLC (Data: Aug-20, Pub: Sep 2020)

58

More Less Same More Less Same More Less Same More Less Same More Less Same More Less Same More Less Same

Appendix

Designer: Hannah Hacker, AKBDPhotographer: Caleb Vandermeer

New-Construction: John Burns Real Estate Consulting (JBREC) analyzed construction costs for new-construction spending by category within new home kitchens and bathrooms. Homes were segmented by size and price point. Due to regional differences in home price points, segmentation was conducted by nine census divisions, then rolled up. All figures include both products and labor (installed costs).

Kitchen and Bath Remodel: Spending values are JBREC calculations from tabulations of U.S. Census American Housing Survey home-improvement projects microdata, NAA spending (rental), JBREC home-improvement estimates, and forecasts of single-family rental renovation spending. All values include labor and materials, including all major elements within kitchen and bath spending (plumbing fixtures, faucets, tile, vanities, countertops, lighting, showers and baths, etc.).

To better understand project activity in light of COVID-19, a total of 1,048 online surveys were conducted in August of 2020 among consumers inquiring about their household remodel/renovation projects for either kitchen or bathrooms.

• Completed a kitchen/bath remodel project (250 responses total) or• Actively working on a kitchen/bath remodel project (250 responses total) or• Planned, or strongly considered, a kitchen/bath remodel project, but abandoned it (250 responses total) or• Started, but postponed, a kitchen/bath remodel project (250 responses total).

Respondents were equally represented across six noncontiguous U.S. regions as defined below:• Northeast: Maine, Massachusetts, Rhode Island, Connecticut, New Hampshire, Vermont, New York, Pennsylvania, New Jersey, Delaware, Maryland• Southeast: West Virginia, Virginia, Kentucky, Tennessee, North Carolina, South Carolina, Georgia, Alabama, Mississippi, Arkansas, Louisiana, Florida• Midwest: Ohio, Indiana, Michigan, Illinois, Missouri, Wisconsin, Minnesota, Iowa, Kansas, Nebraska, South Dakota, North Dakota• Southwest: Texas, Oklahoma, New Mexico, Arizona• West: Colorado, Wyoming, Montana, Idaho, Washington, Oregon, Utah, Nevada, California, Alaska, Hawaii

Source: NKBA/ JBREC Online Survey Panel; n= 1,048 60

Detailed Methodology

$ 3 9 B$ 4 B

$ 2 6 B$ 9 B

$ 2 8 B$ 6 B

$ 2 1 B

$77$62

$77

$62

NEW CONSTRUCTION

REMODEL

$139

KITCHEN

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: 2020)

61

Residential K&B Spending Overview

($ Bill ions)

$ 7 B

Single Family

Multi-Family

Owner Repair / Remodel

Rental Repair / Remodel

BATH

Due to rounding, sub-categories do not always exactly sum to the rounded totals.

$131B $143B $148B $139B

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: 2020)

62

Historical Kitchen and Bath Spending

2017 2018 2019 2020P

+

$

8.8%3.8%

-6.1%

Source: NKBA/ JBREC Online Survey Panel; n=1,047; *Indicated Parents and/or Grandparents lived with them full-time.Notes: Unweighted data shown. Tabulations involving spending estimates were weighted to ensure income distribution matched the U.S. Census Bureau, 2018 ACS.

31%

8% 7% 9%13%

9%6% 7%

3% 2% 3%0%

10%

20%

30%

≤ $40k $40K -$49.9k

$50K -$59.9k

$60K -$69.9k

$70K -$99.9k

$100K -$124.9K

$125K -$149.9K

$150K -$199.9K

$200K -$249.9K

$250K -$299.9K

≥ $300k

7% 9% 6%12% 9% 10% 10% 10%

27%

0%

10%

20%

30%

40%

Under 30 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65 or over

Consumer Demographics

Age Range

Annual Household Income Distribution

47%

36%

8% 9%

0%

25%

50%

Entry-LevelUp to $250k

Move-Up$250k - $500k

2nd Move-Up$500k - $750k

Luxury$750k+

Consumer Demographics

Home Price Ranges

14%19% 16% 17%

34%

0%

25%

50%

< 10 yrs 10-20 yrs 20-30 yrs 30-40 yrs 40+ yrs

Age of Home

7%14%

18%25%

36%

0%

25%

50%

<2 yrs 2-5 yrs 5-10 yrs 10-20 yrs 20+ yrs

Length of Home Ownership

25%

44%

21%

10%

0%

25%

50%

< 1,500 1,500-2,500 2,500-3,500 3,500+

Size of Home (sq. ft.)

Source: JBREC Online Survey Panel; n=1,047Notes: Unweighted data shown. Tabulations involving spending estimates were weighted to ensure income distribution matched the U.S. Census Bureau, 2018 ACS.

The conclusions and recommendations presented in this report are based on our analysis of the information available tous from our research as of the date of this report. We assume that the information is correct and reliable and that wehave been informed about any issues that would affect project marketability or success potential.

Our conclusions and recommendations are based on current and expected performance of the national, and/or localeconomy and real estate market. Given that economic conditions can change and real estate markets are cyclical, it iscritical to monitor the economy and real estate market continuously, and to revisit key project assumptions periodically toensure that they are still justified.

The future is difficult to predict, particularly given that the economy and housing markets can be cyclical, as well assubject to changing consumer and market psychology. There will usually be differences between projected and actualresults because events and circumstances frequently do not occur as expected, and the differences may be material. Wedo not express any form of assurance on the achievability of any pricing or absorption estimates or reasonableness of theunderlying assumptions.

In general, for projects out in the future, we are assuming “normal” real estate market conditions, and not a condition ofeither prolonged “boom” or “bust” market conditions. We do assume that economic, employment, and household growthwill occur more or less in accordance with current expectations. We are not taking into account major shifts in the level ofconsumer confidence; in the ability of developers to secure needed project entitlements; in the cost of development orconstruction; in tax laws that favor or disfavor real estate markets; or in the availability and/or cost of capital andmortgage financing for real estate developers, owners and buyers. Should there be such major shifts affecting real estatemarkets, this analysis should be updated, with the conclusions and recommendations summarized herein reviewed andreevaluated under a potential range of build-out scenarios reflecting changed market conditions.

We have no responsibility to update our report analysis for events and circumstances occurring after the date of ourreport. This analysis represents just one resource that should be considered when assessing a market opportunity.

65

Limiting Conditions

All NKBA market research reports are available through the NKBA Store at https://store.nkba.org/collections/research

About the National Kitchen & Bath AssociationThe National Kitchen & Bath Association (NKBA) is the not-for-profit trade association that owns the Kitchen & Bath Industry Show® (KBIS), as part of Design and Construction Week® (DCW). With nearly 50,000 members in all segments of the kitchen and bath design and remodeling industry, the NKBA has educated and led the industry since the association’s founding in 1963. The NKBA envisions a world where everyone enjoys safe, beautiful and functional kitchen and bath spaces. The mission of the NKBA is to inspire, lead and empower the kitchen and bath industry through the creations of certifications, specialty badges, marketplaces and networks. For more information, visit www.nkba.org or call 1-800-THE-NKBA (843-6522).

KBIS® and NKBA® are registered trademarks of the National Kitchen & Bath Association.

Designer: Sarah Robertson, AKBDPhotographer: Adam Macchia