2021 national income tax workbook

TRANSCRIPT

2021 National Income Tax

Workbook

Chapter 11: Construction Issues

1

• Accounting for Long Term Contracts

•Motor Vehicle Expenses

•Meals and Entertainment

• Employee and Independent Contractors

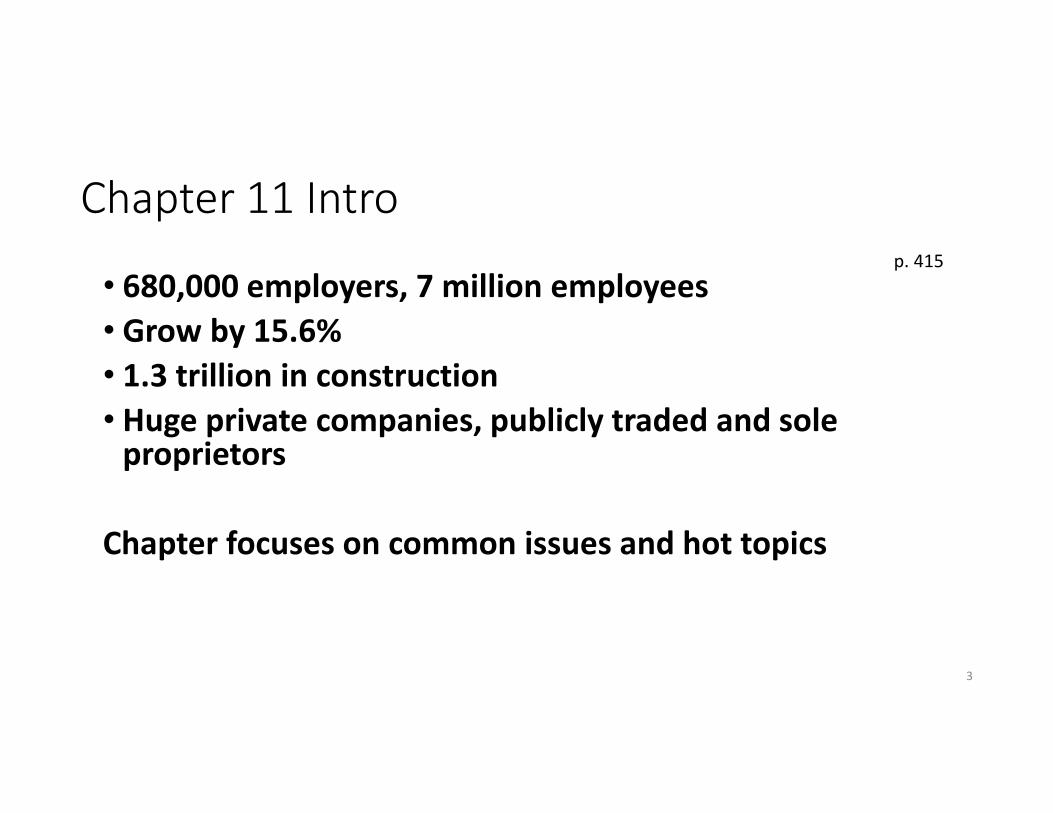

Chapter 11 Intro and learning objectives

p. 415

2

• 680,000 employers, 7 million employees

• Grow by 15.6%

• 1.3 trillion in construction

• Huge private companies, publicly traded and sole proprietors

Chapter focuses on common issues and hot topics

Chapter 11 Intro

p. 415

3

p. 415

Issue #1 Accounting for Long term contractsp. 416

Before 1986 Act 1987 - 2017 After TCJA - 2017

Few restrictions:

Cash

Accrual

Completed contract

Percent completion

Generally required the use

of Percentage Completion.

Large taxpayers:

Generally still required the use

of Percentage Completion.

Small taxpayers and home

construction:

Not required to use the

Percentage Completion.

LongLongLongLong----termtermtermterm contract definedExample

416

Year 1 Year 28/1 1/30 (only 7 months)

better name

“Overlapping tax year contract”

Manufacture, building, installation or construction of real property

• Including integral components

• Improvement to real property

(But, not architects, engineering services, etc…)

REAL PROPERTY?417

Land

Buildings

Inherently permanent structures

• Roadways, dams and bridges

Integral component can be constructed offsite

• Elevators, central heating systems

Construction Contract417

Dates are important:

• Begins on date the contract binds the contractor and

customer

• Contract is completed upon the earlier:

• Customer can use property, 95% of costs incurred

• Contractor completes construction and customer

accepts it

Example 11.1 – which year is contract complete? 417

2019 Nov 2020 Dec 2020 Jan 2021

Casey - Calendar year

Ave gross receipts

30 mil

Enters into a

contract to build

office building

Casey

completes

building

Barbara

move in

Barbara finds

minor

construction

defects

Casey fixes

defects

Casey

determines cost

to fix < 5% of

total

Percentage Completion - Example 11.2418

Year 1

Costs deducted in

year incurred

7 million

estimated total

contract costs

62.5 million

Completion factor:

7 = 11.2% x contract price 100 million = 11,200,000

62.5

less costs (7,000,000)

Income to report 4,200,000

Example 11.3418

Year 1 Year 2

Costs deducted in

year incurred

7 million

estimated total

contract costs

62.5 million

Completion factor:

42 = 67.2% x contract price 100 million = 67,200,000

62.5 less income reported in year 1 (11,200,000)

less year 2 costs (35,000,000)

Income to report in year 2 21,000,000

Costs deducted in

year incurred

35 million

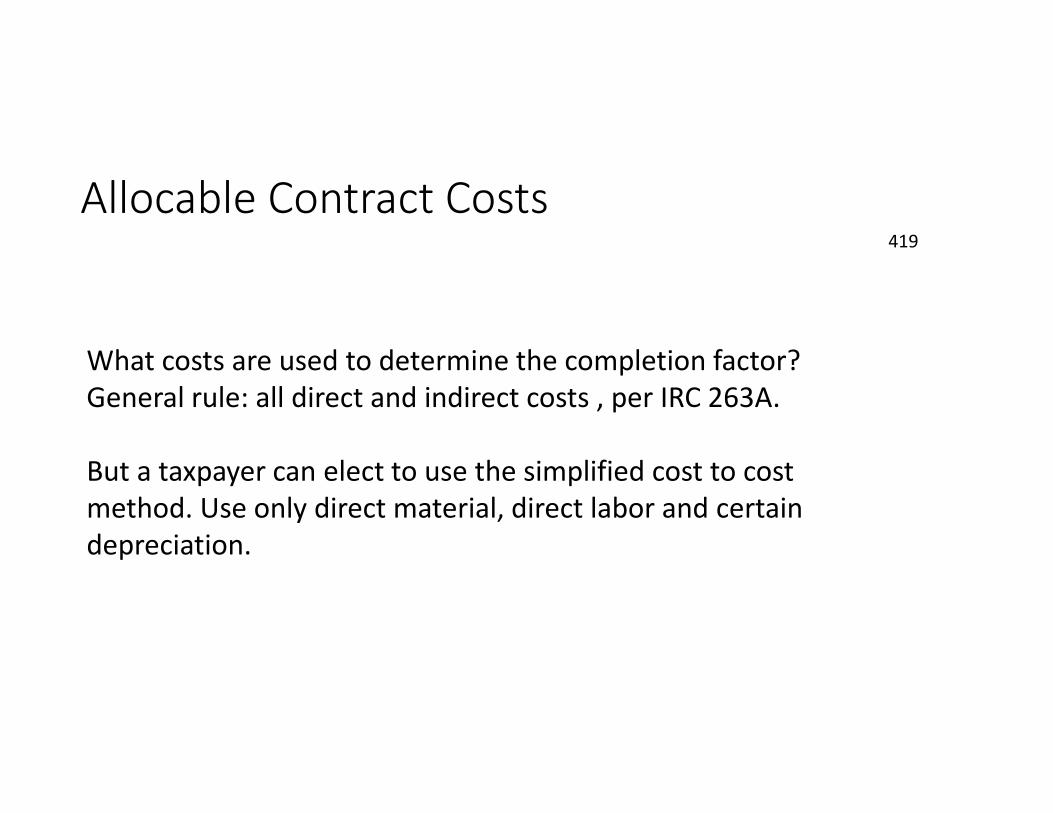

Allocable Contract Costs419

What costs are used to determine the completion factor?

General rule: all direct and indirect costs , per IRC 263A.

But a taxpayer can elect to use the simplified cost to cost

method. Use only direct material, direct labor and certain

depreciation.

Look Back Method – Form 8697419

12/31/21

Costs deducted in

year incurred

100,000

estimated total

contract costs

500,000

Completion factor:

100,000 = 20% x contract price 800,000 = 160,000

500,000

less costs (100,000)

Income to report 60,000

Total Contract Price419

Reasonable expects to receive. Including:

Holdbacks, retainages and cost reimbursements

Contingent payments included when the contractor

can reasonably predict that the amount will be

earned.

?

Post completion income and expenses419

12/31

Contract

Complete

Additional costs incurred?

Changes to contract price?

Don’t adjust any calculations in

year of completion. Report income

and account for costs using any

reasonable method.

10% method419

12/31

Costs incurred < 10%

Total contract costs

Do not report

until 10% of costs

incurred

Home construction contractors419

80% contract costs attributable to construction of:

• Dwelling Unit containing 4 or fewer units

• Provide living accommodations

• Not hotel /motel

• Improvements to real property located on site of dwelling unit

Home vs residential construction420

Home:

Exempt from

Percentage

completion

Residential:

Required to use

percentage completion

Small Contractor Exception420

• Small contractors don’t have to use percentage completion and

can use any permissible method

• What is a small contractor?

• Contracts after 12/31/2017

• Other than tax shelter

• Contracts to be completed within 2 years

• Meet the gross receipts test in year contract entered into

Gross Receipts Test420

2018

2019

2020 Average

< 26,000,000

2021 – small?

460 uses test of 448.

1. Corporation

2. Partnership with C corp

partner

3. Individuals

(discussed later)

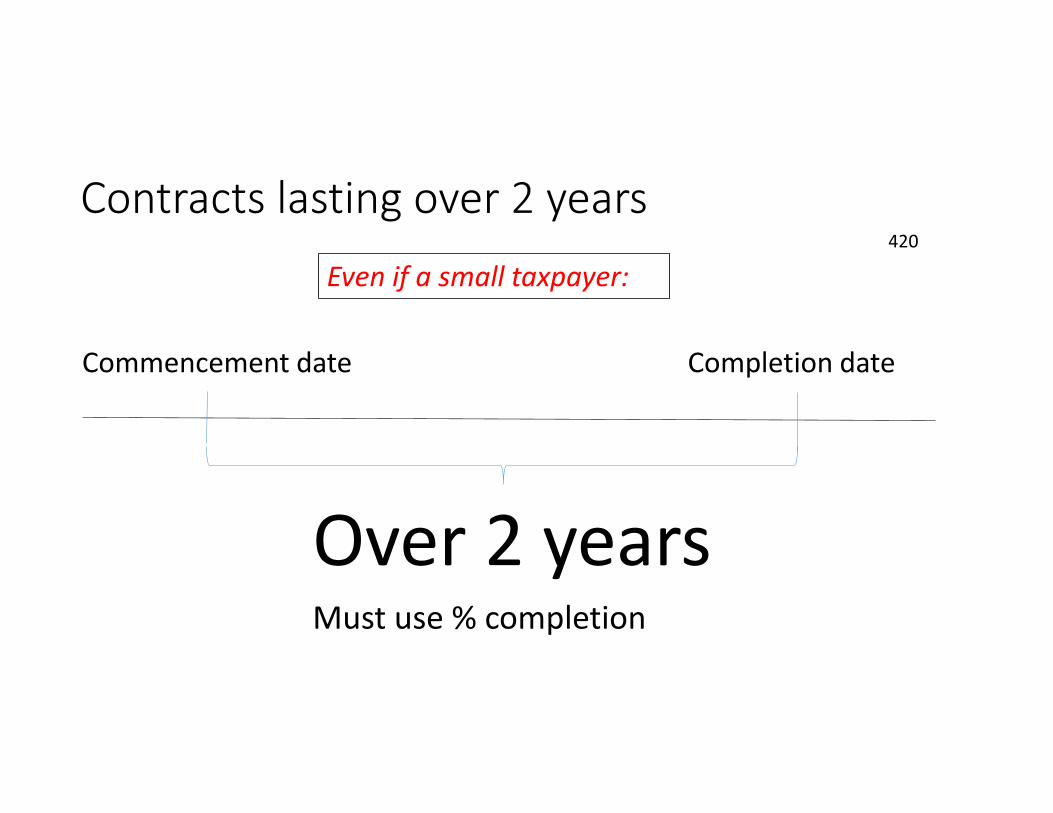

Contracts lasting over 2 years420

Commencement date Completion date

Over 2 years

Even if a small taxpayer:

Must use % completion

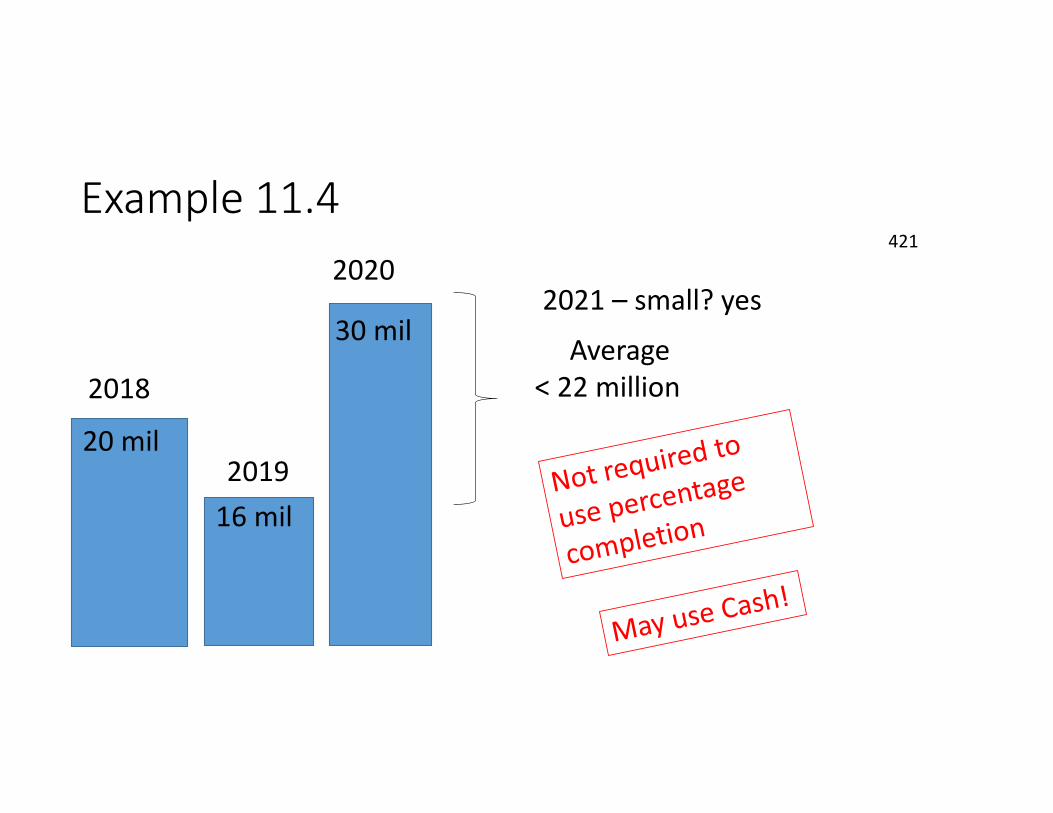

Example 11.4 421

2018

2019

2020

Average

< 22 million

2021 – small? yes

20 mil

16 mil

30 mil

Gross Receipts - individuals 421

Business Business etc.. Wages Social Settlements

security

YES NO

Example 11.5421

Trade or business 1 Trade or business 2

Average 5,000,000 Average 35,000,000

Average 40,000,000

Greater than 26,000,000

1 12 23 3

Exempt Contract Methods421

If not required to use Percentage Completion because of

gross receipts test or home construction test, can use:

Percentage Completion

Exempt Contract Percentage Completion

Completed Contract

Any other permissible method. Ie: Cash, Accrual

Exempt Contract Percentage Completion422

May use a variety of methods to determine percentage

completion factor:

Direct labor to date

Total direct labor

Work performed

Total work to be performed

Any other method of cost comparison!

Completed Contract Method (CCM)422

• Defers income recognition the longest!

• May elect for contracts for which Percentage Completion

not required.

General Rule: inclusion of all contract income and

allocable contract costs are deferred until the

taxable year in which the contract is completed.

Example 11.6422

12/31

Income XX,XXX + XXX,XXX = 500,000

Costs (XX,XXX) + (XXX,XXX) = (350,000)

report no income 150,000

only reflect on

balance sheet

Change of Accounting422

Rev Proc 2019 – 43 permits automatic changes for small businesses:

• Changes from Percentage Completion

• Stop capitalizing costs under IRC 263A

• Overall accrual to overall cash

• Treatment of inventories. Ie: treated as non-deductible material

and supplies

Issue #2 - Transportation Expenses423

262 – personal 162 - business

162 - business

Example 11.7

Making calls while

driving to the office.

Still commuting

Temporary

Workplace

outside

city

Temporary Workplace424

Temporary

Workplace

outside city

Realistically

expected

< 1 year

Residence = principal place of business424

Administrative

Management

No other place

162 - business

Example 11.8

Tyler is an architect. Home office

Drives to project sites 2 or 3 times

per week:

Deductible

DEDUCTING TRANSPORATION EXPENSES 424

Standard Mileage Actual

Rate

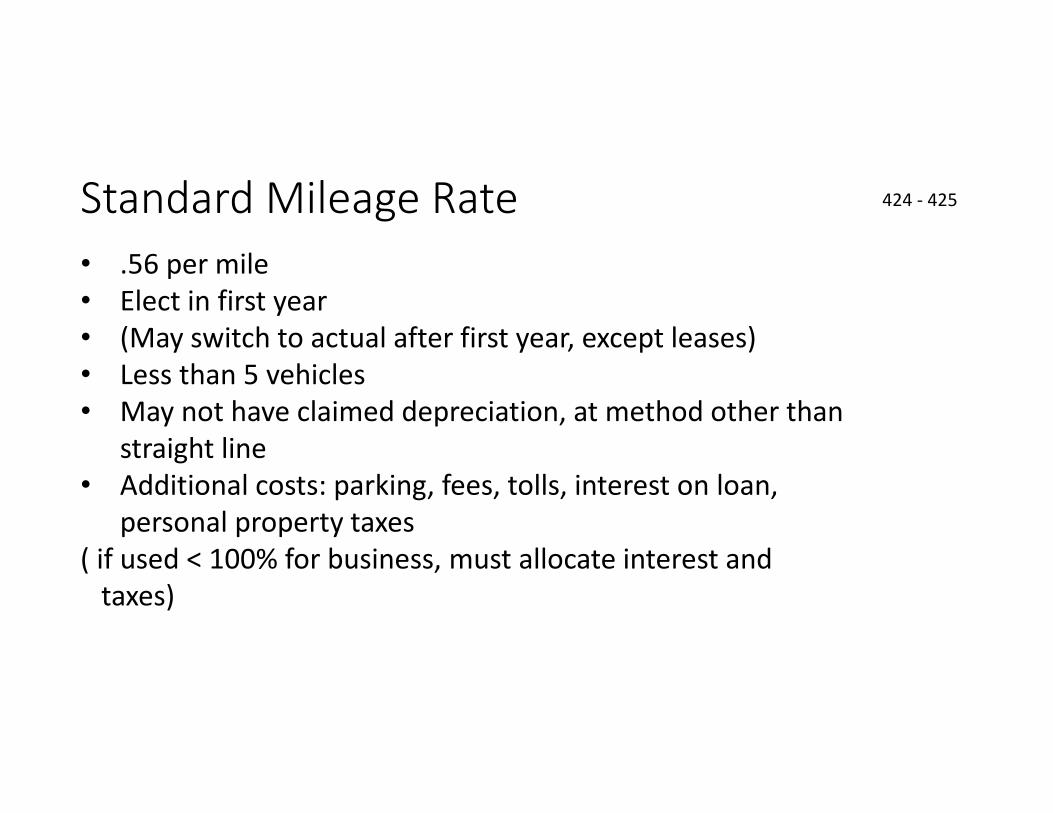

Standard Mileage Rate 424 - 425

• .56 per mile

• Elect in first year

• (May switch to actual after first year, except leases)

• Less than 5 vehicles

• May not have claimed depreciation, at method other than

straight line

• Additional costs: parking, fees, tolls, interest on loan,

personal property taxes

( if used < 100% for business, must allocate interest and

taxes)

Example 11.9425

Interest

1,800

Registration

350

8,000 business miles

10,000 total milesx .80 x .80

8,000 x .56 = 4,480 + 1,440 + 280 = 6,200

SMR – depreciation component 426

For 2021, depreciation component .26 per mile

Example 11.10

Purchased car in 2017 for 34,000

Claimed standard mileage rate

Figure 11.4 shows depreciation per year

1245 gain – 3,653

If after using SMR, switch to actual costs, must use straight line

total me

Cost 2005 52,000 7,700

Current value (3,000) (3,000)

Depreciation 49,000 4,300

Miles 250,000 60,000

Depreciation per mile 19.6 7.1

Actual Cost method426

Gas

and oilMaintenance

and repairs

Fees and

taxes

Loan

interest Insurance

Lease

payments

Depreciation

Garage

rent

Tolls and

parking

Depreciation427

Passenger Automobiles

• General depreciation rule: 5 year MACRS

• May be eligible for bonus and 179, if used over 50%

• 280F(a) limits annual depreciation and 179

• Heavier trucks and vans not subject to these limits

• 179 limited for certain SUVs

IRC 280F(d)(5) limitations

Curb weight Maximum allowable

weight, when fully

loaded

6,000 lbs

427

Passenger Auto?

Depreciation Limits

Depreciation limits- without Bonus:

First Second Third Later

2019 & 2020 10,100 16,100 9,700 5,760

2021 10,200 16,400 9,800 5,860

Example 11.11

SUV for 60,000, 5,800 GVW

No 179 election

Elects out of bonus

MACRS 60,000 x 20% = 12,000

Limited to 10,200

427 & 428

Leased Vehicles428

280F limit applied in a different manner for leased vehicles:

• if FMV > 51,000

• Lease inclusion amount - See Rev Proc 2021 -31

Bonus Depreciation428

• Bonus is mandatory

• Elect out on a class by class basis. Since autos are 5 year

property, must elect out of all 5 year property

• First year bonus is 8,000

First Second Third Later

2021 10,200 16,400 9,800 5,860

Bonus 8,000

Total 18,200 same same same

Bonus and Section 280 Limit428

6/1/21 22 23 24 25 26 27 28 29 30 31 32

18,200_______________

41,800 0 0 0 0 0 5,860/year

basis

60,000 truck purchased

Gap with no depreciation

But, if elected, Rev Proc 2019-13 safe harbor applies- lesser of:

• basis x appropriate factor

• annual limit

Section 179 for autos429

Basics:

• Elect up to 1,050,000

• Phase out starts at 2,620,000 for 2021

• Limited to taxable income

• Order: 179, bonus then regular depreciation

• 280F limit applies – 18,200 for 2021

• Problem: Any basis remaining after the 18,200 can only be

depreciated starting in year 7 (just like bonus)

• BUT NO Rev Proc 2019-13 election available for years 2 - 6

SUVs over 6,000 GVW429

Exempt from 280F limitations

Use regular depreciation rules – may make a 179 election

Over 6,000 LB GVW, but not more than 14,000

Excludes:

• Buses – more than 9 persons

• Pick up truck cargo area at least 6 feet

• Cargo van – fully enclosed drivers area

But, 179 deduction for an SUV is limited to 26,200, but

taxpayer may claim 100% bonus.

Summary 429

Automobiles SUVs over 6,000 lbs Pickups and cargo vans

• Exempt from 280F

limitations

• Excluded from 179

limit, so can claim

full 179

• Can claim full bonus

• Regular 5 year MACRS

• Exempt from 280F

limitations, but:

• 179 limit 26,200

• Can claim full bonus

• Regular 5 year

MACRS

• 280F limitations

apply

• Depr limit 10,200

• Bonus 8,000

Total 18,200

Substantiation430

IRC 6001

Keep records to

substantiate tax

liability

Cohen Rule

1930

Absence of

evidence, can

estimate

274(d)

overrides

Cohen

Must

substantiate

auto expense

Reg 1.274-5T

(c)(2)

Account book,

diary, log,

statement, trip

sheet, etc..

=

Substantiation430

Keep: Account book, diary, log, statement of expenses, trip sheet

To Show: date, destination, mileage and purpose

When: Created at or near time of business use

Employee use of employer vehicle431

If available for personal use, must include in employee’s wages

(income and employment taxes)

Methods:

Cents per mile

Annual Lease Value

Commuting value method

General FMV method – cost to lease

Most common

Cents per mile method431 & 432Basics:

• Expects the vehicle will be used in the employer’s trade or

business (over 50%)

• Or driven over 10,000 miles by employees

• Adopt as of the first day an employee uses the vehicle

• Must continue to use the method

Limitations:

• FMV of vehicle < 51,100

Includes:

• Maintenance, insurance, fuel

Rate:

• .56 per mile

Annual Lease Value method432 & 433

Basics:

• Must be available all year, or prorate

• Amount reduced for amount that is considered a working

condition fringe benefit

• Must continue to use the method (special COVID relief rule

allows employer to switch the cents-per-mile method)

Calculation

Determine FMV – arm’s length purchase price

Use table – page 433

Based on a 4 year lease term

Annual Lease Value433

Year 1 Year 2 Year 3 Year 4 Year 5 etc….

Same Lease Value

used for 4 years

Determine FMV

and use new rate

Includes maintenance and insurance, but not fuel!

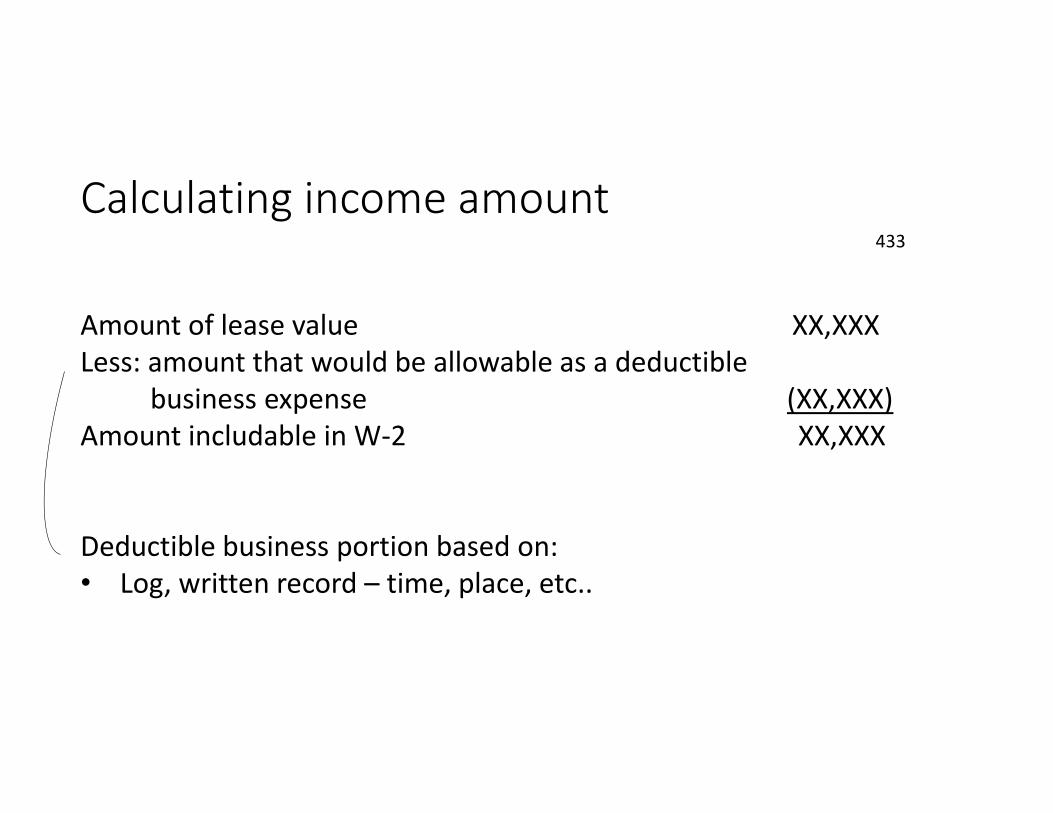

Calculating income amount433

Amount of lease value XX,XXX

Less: amount that would be allowable as a deductible

business expense (XX,XXX)

Amount includable in W-2 XX,XXX

Deductible business portion based on:

• Log, written record – time, place, etc..

Commuting Valuation Rule434

Requirements:

• Bona fide noncompensatory business reasons the employer

requires the employee to commute in the vehicle

• Policy prohibiting personal use, other than commuting

• Employee does not actually use the vehicle for personal use

• Employee is not a control employee- officer who’s

compensation is > 115,000, director, employee > 235,000,

owns 1% or more of company

Valuation: 1.50 per one way commute

Issue #3 Meals and Entertainment435

General Rule435

274 limits or disallows certain meals and entertainment,

even if normally deductible under 162.

Lavish limitation – 274(k)

• Not lavish or extravagant under the circumstances

• Taxpayer (or employee is present)

50% limitation on meals435

General Rule:

Deduction limited to 50% of otherwise deductible food or

beverage. Very broad.

Meals, snacks, de minimus under 132, etc..

BUT: special rule for 2021 and 2022!

100% deduction for food and beverages provided by a

restaurant.

Some exceptions to the limitation - 274(e)

See last year’s book pages 238 - 240

Limitations on Entertainment436

274(a) disallows deduction for entertainment

Except:

• food or beverage furnished on the business premises

to employees

• Certain recreational expenses for employees

• Expenses treated as compensation

• Reimbursed expenses

Work site meals 436

Employees- taxable? Employer – deductible?

FMV of meals taxable, but may

be excluded:

1. De minimis fringe (repealed

in 2017)

2. Convenience of employer:

at place of work

(after 2025, no deduction)

50% deductible until 2025, then

none.

May be able to deduct 100%, if

included in employees income.

(discussed later)

Example 11.12436

20 mile dirt road

Jackson Hole

Job site 50% deductible

Restaurant food

Box lunches100% deductible

excludable

excludable

Business meals and entertainment437

Meals Meals during Entertainment

entertainment?

Meals provided to

business associate:

Customer, Client,

Supplier, Employee,

Agent, Advisor

50% (unless

restaurant)

Amusement, recreation,

bars, theaters, country

clubs, golf and athletic

clubs, hunting, fishing,

vacations, etc..

No deduction

Entertainment does not

include food or bever

unless provided at or

during entertainment &

costs not separately

stated.

50% if purchased

separately.

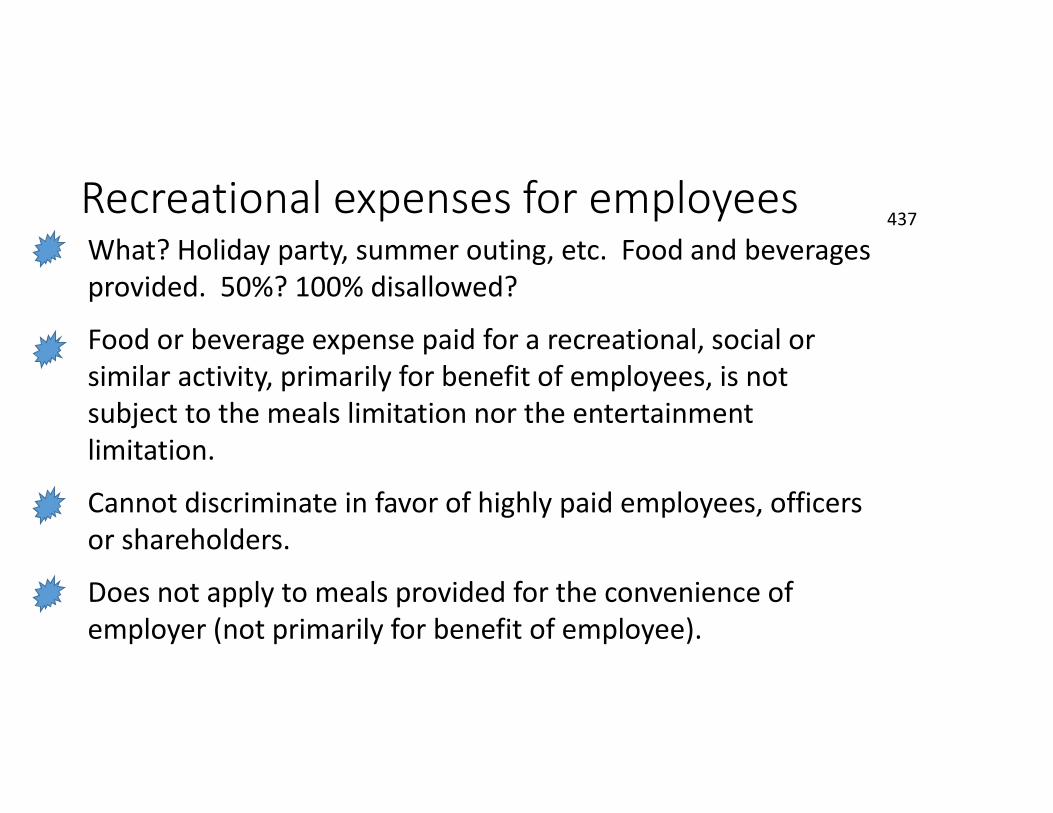

Recreational expenses for employees437

What? Holiday party, summer outing, etc. Food and beverages

provided. 50%? 100% disallowed?

Food or beverage expense paid for a recreational, social or

similar activity, primarily for benefit of employees, is not

subject to the meals limitation nor the entertainment

limitation.

Cannot discriminate in favor of highly paid employees, officers

or shareholders.

Does not apply to meals provided for the convenience of

employer (not primarily for benefit of employee).

Example 11.13 – no discrimination438

Hotel ballroom

buffet open bar

All employees

invited

100% deductible (including food)

Because: recreational, social, for benefit

of non-highly compensated employees

Example 11.14 – discrimination438

Hotel ballroom

buffet open bar

Only highly

compensated

employees Food and Bev - 50% (unless restaurant)

Rental Fees – 100%

Rental xx,xxx

Food & Bev xx,xxx

Total xx,xxx

438Example 11.15 – Client dinner

Landscaper

Invites employee and client to

dinner at a restaurant

Employee’s birthday – special

dessert

Business meal, not primarily for benefit

of employee (even though an employee

social activity occurred)

50% deductible (100% in 2021 & 2022)

Meal treated as compensation439

If cost of meal is included in compensation, the 50% limitation

does not apply. Ie: do not meet definition of a de minimis

fringe or meals provided for convenience of employer.

(Could be for an employee or independent contractor)

Example 11.16 Gator Builders provides meals at construction

site.

• Meals do not meet definition of de minimis fringe or meals

provided for convenience of employer.

• Costs includes in W-2

• 100% deductible

Example 11.17 Employee partially pays439

Same facts as 11.16, except employees pay 8.00/Day

FMV of meals 10.00

Amount reimbursed (8.00)

Amount included in W-2 2.00

Cost of meals 9.00

100% deductible

Part reimbursed

Part included in

income

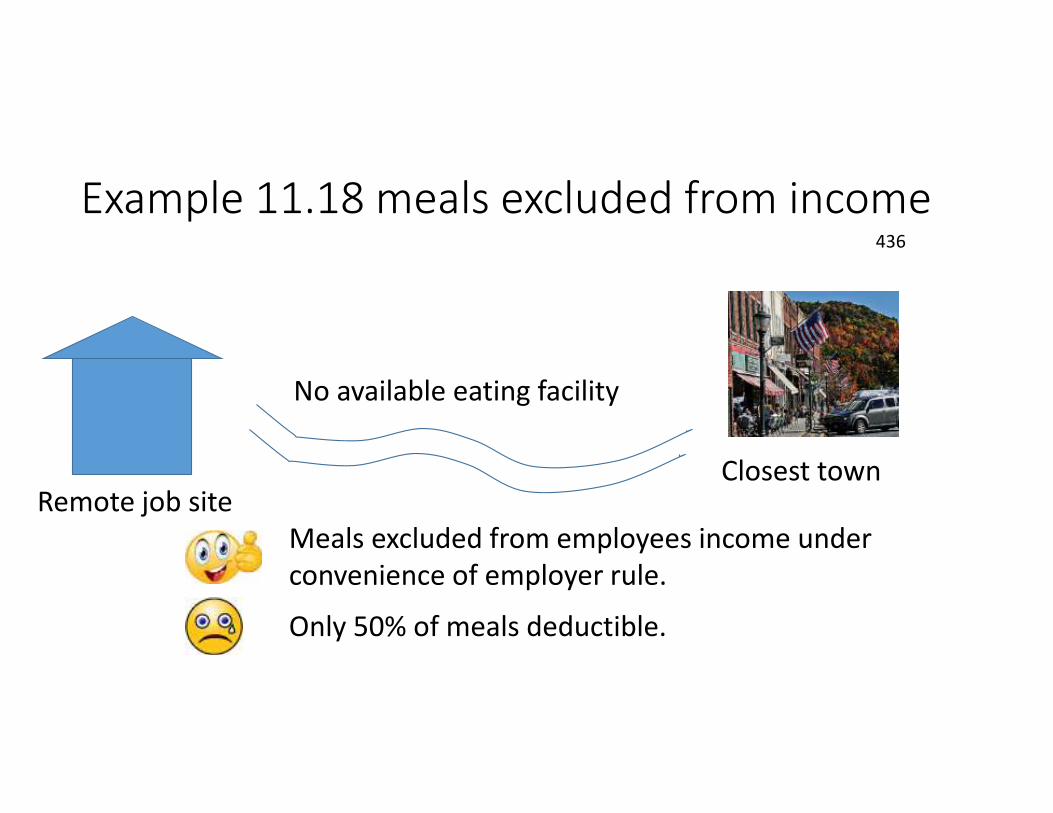

Example 11.18 meals excluded from income436

No available eating facility

Remote job site

Meals excluded from employees income under

convenience of employer rule.

Closest town

Only 50% of meals deductible.

Reimbursed meal expenses 440

Employer EmployeeIncurred

expense

reimbursed

If not treated as

compensation:

employer subject

to limitation

If treated as

compensation:

employee subject to

limitation

Reimbursed meal expenses 440

EmployerIndependent

contractor

Incurred

expense

reimbursed

Identifies party subject

to the limitation

If silent, depends if it’s an accountable plan

Issue 4 – Employee vs Independent contractor 441

Employee Independent Contractor

Withhold income tax, FICA

Match FICA

Fed and State unemployment

Worker’s Comp

Health coverage (?)

Issue Form 1099- NEC

Worker pays their own

income and Self-employment

tax

Common Law Factors441

Right to control

- Result

- Detail and means

- Rev Rul 87-41: 20 Common law factors

Categories:

BEHAVIORAL FINANCIAL RELATIONSHIP

Behavioral Control441

Right to direct or control

What

should be

done?

Choose where to

purchase

supplies, hire

assistance

What tools, how,

where or when

to do the work?

How will worker

be evaluated?

Only end result?

Business

provide the

training?

Financial Control442

Control financial aspects

of the job

Who purchases

tools and

equipment

Who pays the

expenses

Opportunity for

profit or loss

Relationship of the parties442

Written Contract?

Employee

type fringe

benefits Worker

advertise?

Business

location?

Services provided

a key aspect of

payer’s business

Services provided

available to othersHow long of a

relationship?

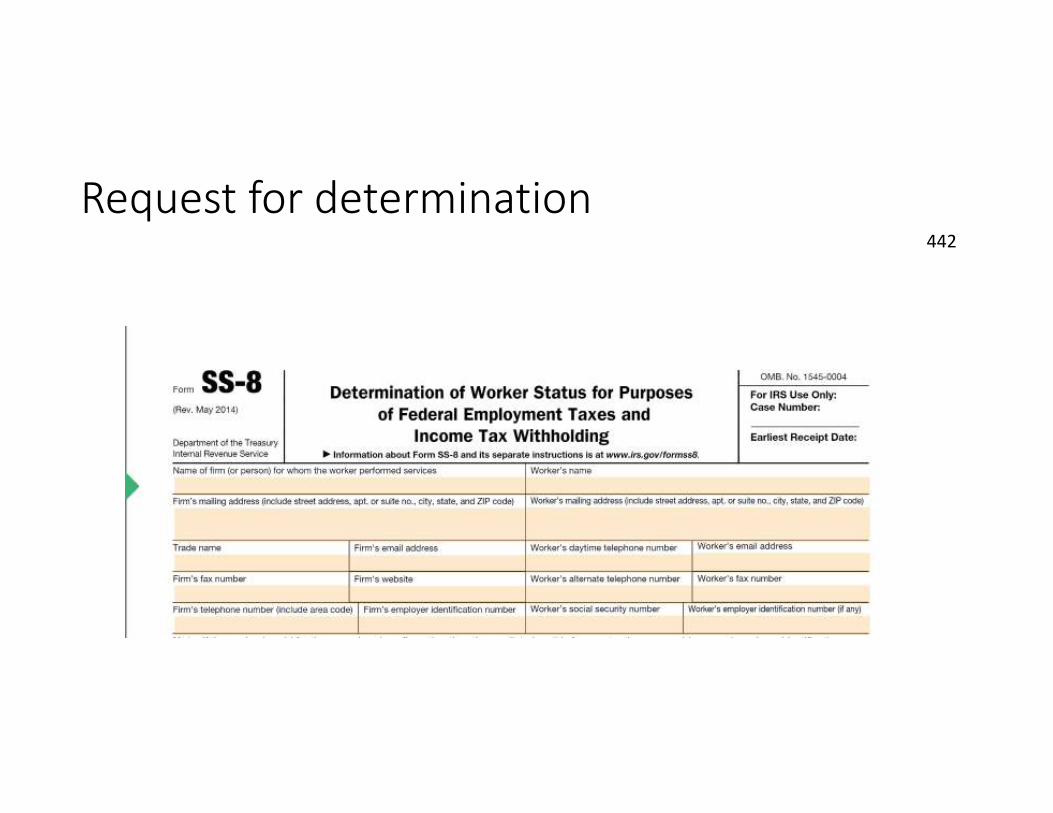

Request for determination 442

Kurio442 & 443

Builder Kurio Workers

Fabricated drywall material into walls

Furnished own tools

No right to determine particular worker

No right to determine hours

No right to control manner or means of accomplishing work

Opportunity for profit or loss

Jobs short duration. Workers free to accept other jobs

No permanent relationship

?

Tristate Developers443

Installs siding and roofing

Tristate

Sales

personsApplicators

Timing up to applicators

Tristate controls results, not manner or method

Applicators can accept work from competitors

Applicators had own tools

Applicators employed their own workers

Tristate had job expeditors – assess problems, keep job moving

?

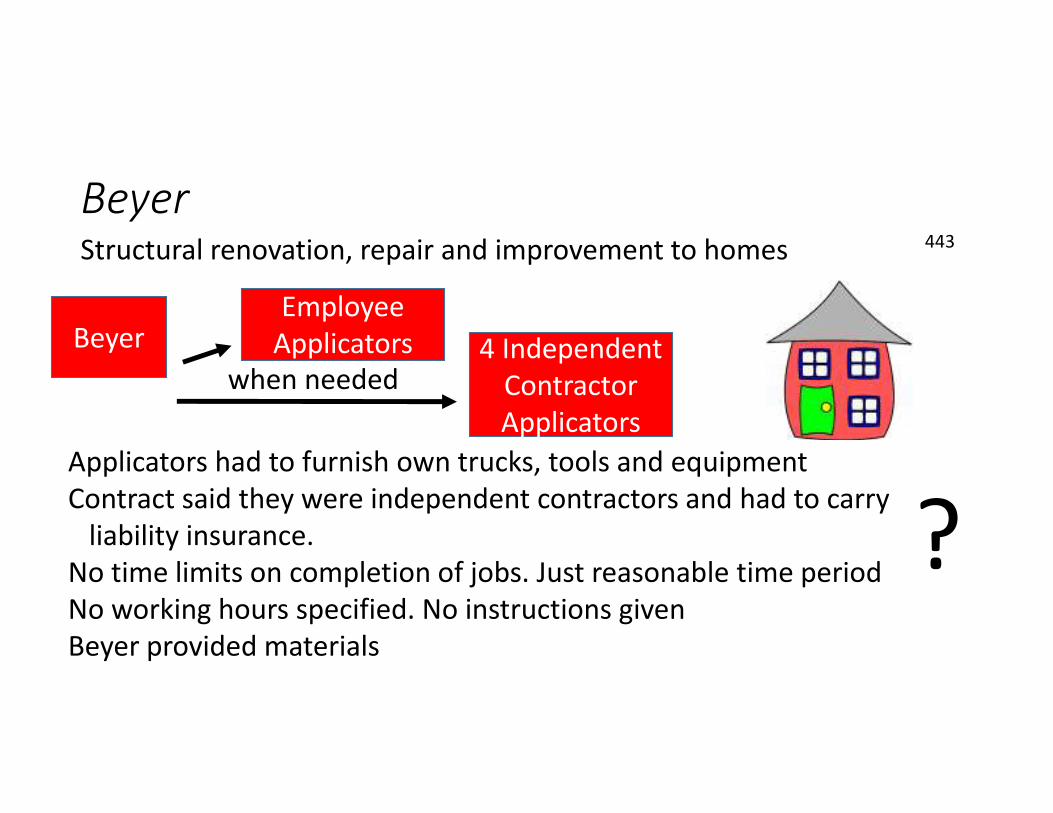

Beyer443Structural renovation, repair and improvement to homes

BeyerEmployee

Applicators 4 Independent

Contractor

Applicators

when needed

Applicators had to furnish own trucks, tools and equipment

Contract said they were independent contractors and had to carry

liability insurance.

No time limits on completion of jobs. Just reasonable time period

No working hours specified. No instructions given

Beyer provided materials

?

Chase444

Home improvement business – aluminum siding

ChaseHelp

WantedApplicators

No training provided or give instructions.

Did not inspect jobs prior to completion.

Applicators provided tools, equipment, truck.

Applicators paid by the job, based on quantity of material used

Applicators determined their own hours

Applicators did not advertise their work. Some worked solely for Chase

Chase carried workers comp and liability insurance

?

Chase444

Home improvement business – aluminum siding

Chase Applicators

Employee! Why?

• Workers worked almost exclusively for company

• Profits not dependent on their own management skills, but number

of jobs performed.

Help

Wanted

Klingler445

Klingler carpentersPaid hourly,

occasionally by job

Provided major tools

Suggested methods

Trained inexperienced

Supervised

Moved workers around

Provided liability insurance

Provided hand tools

Generally worked

full time

One owned own

carpentry business –

independent contractor

Rest - employees

McCombs445

Home improvement business – aluminum siding & roofing

McCombs Applicators

Contracts oral. No guarantees

Applicators could work for other contractors

Materials delivered to jobsite

Tools lent to workers, if needed

Applicators wore uniforms

Salaried supervisors

Paid part of the premiums for applicators in health plan

Received bonuses called vacation pay

?

Piece work basis

Every Friday

Reporting445 & 446

1099 – NEC• 600 per year

• And those with back up withholding

• By January 31

Section 530• 1978

• May grant relief if reasonable basis

• Must file 1099-NEC