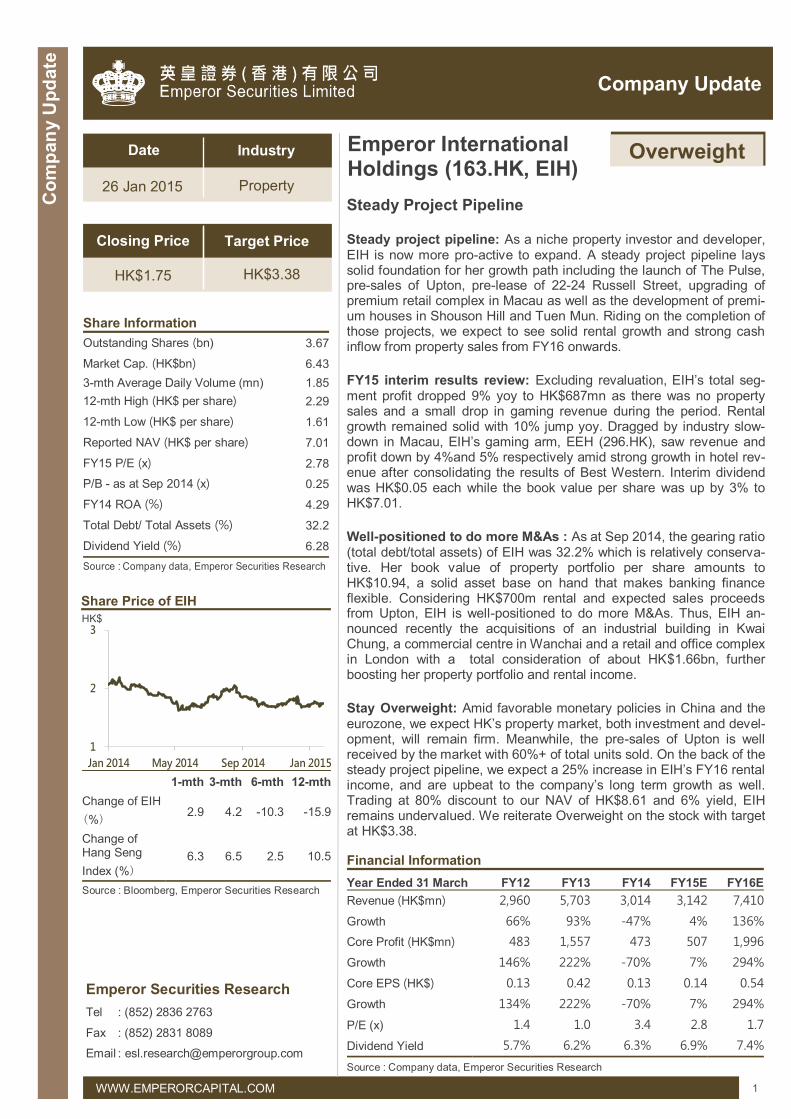

26 jan 2015 property steady project pipeline · steady project pipeline: as a niche property...

TRANSCRIPT

1

Company Update

Co

mp

an

y U

pd

ate

WWW.EMPERORCAPITAL.COM

Steady Project Pipeline

Steady project pipeline: As a niche property investor and developer, EIH is now more pro-active to expand. A steady project pipeline lays solid foundation for her growth path including the launch of The Pulse, pre-sales of Upton, pre-lease of 22-24 Russell Street, upgrading of premium retail complex in Macau as well as the development of premi-um houses in Shouson Hill and Tuen Mun. Riding on the completion of those projects, we expect to see solid rental growth and strong cash inflow from property sales from FY16 onwards.

FY15 interim results review: Excluding revaluation, EIH’s total seg-ment profit dropped 9% yoy to HK$687mn as there was no property sales and a small drop in gaming revenue during the period. Rental growth remained solid with 10% jump yoy. Dragged by industry slow-down in Macau, EIH’s gaming arm, EEH (296.HK), saw revenue and profit down by 4%and 5% respectively amid strong growth in hotel rev-enue after consolidating the results of Best Western. Interim dividend was HK$0.05 each while the book value per share was up by 3% to HK$7.01.

Well-positioned to do more M&As : As at Sep 2014, the gearing ratio (total debt/total assets) of EIH was 32.2% which is relatively conserva-tive. Her book value of property portfolio per share amounts to HK$10.94, a solid asset base on hand that makes banking finance flexible. Considering HK$700m rental and expected sales proceeds from Upton, EIH is well-positioned to do more M&As. Thus, EIH an-nounced recently the acquisitions of an industrial building in Kwai Chung, a commercial centre in Wanchai and a retail and office complex in London with a total consideration of about HK$1.66bn, further boosting her property portfolio and rental income.

Stay Overweight: Amid favorable monetary policies in China and the eurozone, we expect HK’s property market, both investment and devel-opment, will remain firm. Meanwhile, the pre-sales of Upton is well received by the market with 60%+ of total units sold. On the back of the steady project pipeline, we expect a 25% increase in EIH’s FY16 rental income, and are upbeat to the company’s long term growth as well. Trading at 80% discount to our NAV of HK$8.61 and 6% yield, EIH remains undervalued. We reiterate Overweight on the stock with target at HK$3.38.

Date Industry

26 Jan 2015 Property

Closing Price Target Price

HK$1.75 HK$3.38

Share Information

Outstanding Shares (bn) 3.67

Market Cap. (HK$bn) 6.43

3-mth Average Daily Volume (mn) 1.85

12-mth High (HK$ per share) 2.29

12-mth Low (HK$ per share) 1.61

Reported NAV (HK$ per share) 7.01

FY15 P/E (x) 2.78

P/B - as at Sep 2014 (x) 0.25

FY14 ROA (%) 4.29

Total Debt/ Total Assets (%) 32.2

Dividend Yield (%) 6.28

Source : Company data, Emperor Securities Research

1-mth 3-mth 6-mth 12-mth

Change of EIH

(%) 2.9 4.2 -10.3 -15.9

Change of Hang Seng

Index (%) 6.3 6.5 2.5 10.5

Source : Bloomberg, Emperor Securities Research

Share Price of EIH

Financial Information

Year Ended 31 March FY12 FY13 FY14 FY15E FY16E

Revenue (HK$mn) 2,960 5,703 3,014 3,142 7,410

Growth 66% 93% -47% 4% 136%

Core Profit (HK$mn) 483 1,557 473 507 1,996

Growth 146% 222% -70% 7% 294%

Core EPS (HK$) 0.13 0.42 0.13 0.14 0.54

Growth 134% 222% -70% 7% 294%

P/E (x) 1.4 1.0 3.4 2.8 1.7

Dividend Yield 5.7% 6.2% 6.3% 6.9% 7.4%

Source : Company data, Emperor Securities Research

Emperor Securities Research

Tel : (852) 2836 2763

Fax : (852) 2831 8089

Email : [email protected]

Emperor International Holdings (163.HK, EIH)

Overweight

HK$

1

2

3

Jan 2014 May 2014 Sep 2014 Jan 2015

2

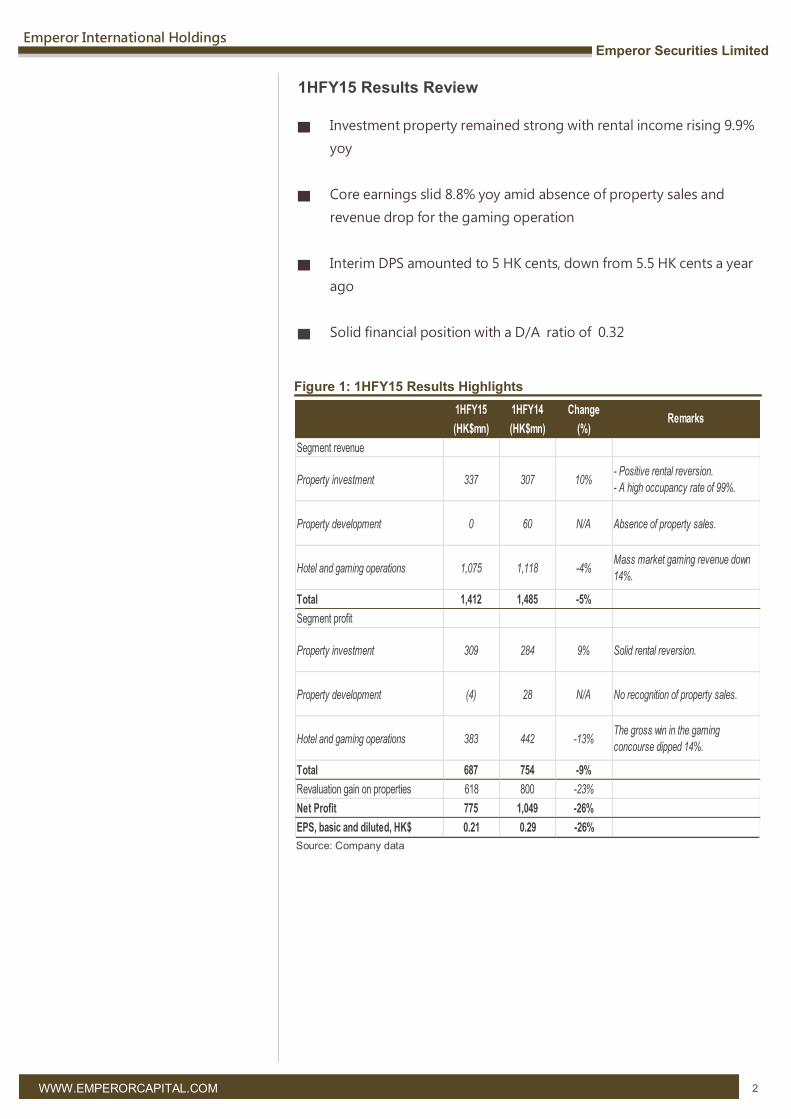

1HFY15 Results Review

▇ Investment property remained strong with rental income rising 9.9%

yoy

▇ Core earnings slid 8.8% yoy amid absence of property sales and

revenue drop for the gaming operation

▇ Interim DPS amounted to 5 HK cents, down from 5.5 HK cents a year

ago

▇ Solid financial position with a D/A ratio of 0.32

WWW.EMPERORCAPITAL.COM

Emperor International Holdings Emperor Securities Limited

Source: Company data

Figure 1: 1HFY15 Results Highlights

1HFY15 1HFY14 Change

(HK$mn) (HK$mn) (%)

Segment revenue

Property investment 337 307 10%- Positive rental reversion.

- A high occupancy rate of 99%.

Property development 0 60 N/A Absence of property sales.

Hotel and gaming operations 1,075 1,118 -4%Mass market gaming revenue down

14%.

Total 1,412 1,485 -5%

Segment profit

Property investment 309 284 9% Solid rental reversion.

Property development (4) 28 N/A No recognition of property sales.

Hotel and gaming operations 383 442 -13%The gross win in the gaming

concourse dipped 14%.

Total 687 754 -9%

Revaluation gain on properties 618 800 -23%

Net Profit 775 1,049 -26%

EPS, basic and diluted, HK$ 0.21 0.29 -26%

Remarks

3

Latest Update on The Premium Projects

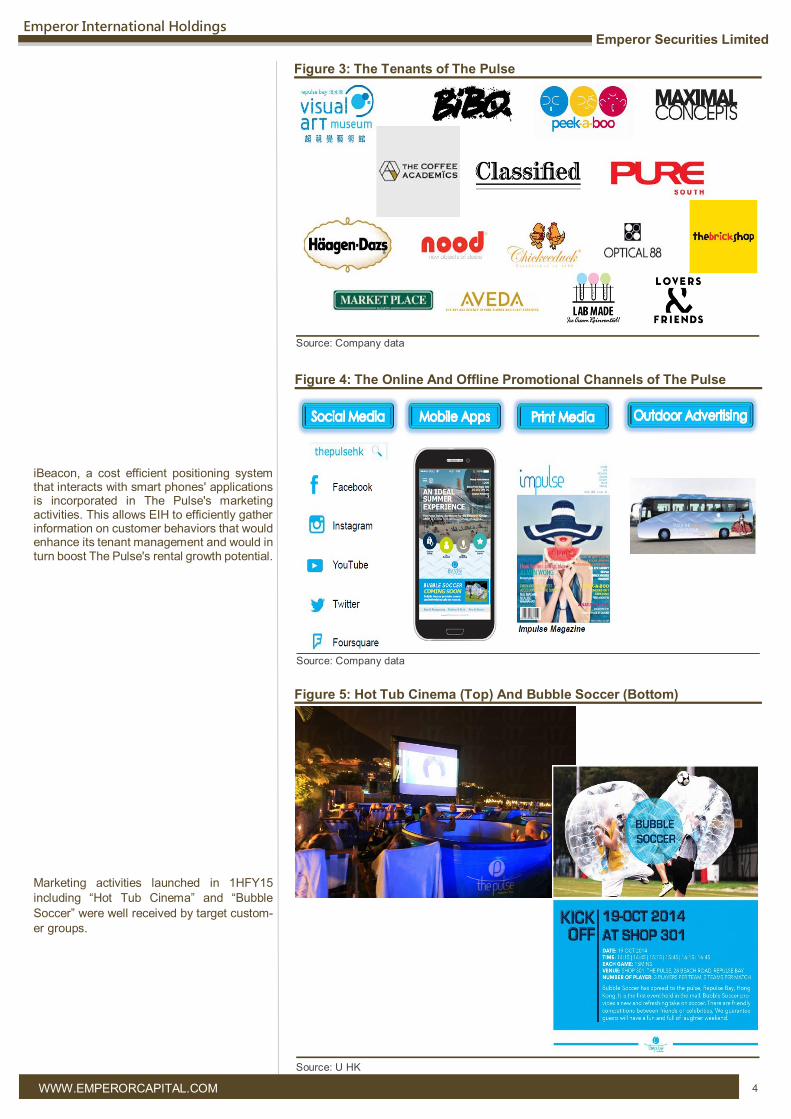

The Pulse

The Pulse, a 4-storey shopping complex with a GFA of 167k sq. ft. located in Repulse Bay was soft-launched in 1HFY15, and currently sees an encouraging occupancy rate of 85%. 50% of the tenants have already commenced operations in this new development and we expect 70%+/ 90%+ of the lessees to be operational by Dec 14/ Feb 15 respectively given the completions of their installations in the months ahead.

Leveraging on the 800 feet Repulse Bay Beach (see figure 2), The Pulse offers a unique blend of bayside shopping, gourmet dining and a 180 degree panorama sea view to both tourists and residents. The property targets for an image of fresh, fun and family-friendly, and it correspondingly holds a diversified tenant mix which comprises fine-diners, lifestyle merchandisers, playground runners, a gymnasium and a premier superstore (see figure 3). It will soon undergo a series of marketing campaigns to boost public recognition and be further promoted at both online and offline channels (see figure 4). Given the know-how as proven by the successful promotional activities launched in 1HFY15 (see figure 5), we are optimistic on the results of the upcoming marketing campaigns which will lay a foundation for the rise of occupancy rate in the years ahead.

WWW.EMPERORCAPITAL.COM

Emperor International Holdings Emperor Securities Limited

Source: Company data, Letsdochina

Figure 2: The Pulse (Top) and Repulse Bay Beach (Bottom)

4

WWW.EMPERORCAPITAL.COM

Emperor International Holdings Emperor Securities Limited

Source: Company data

Figure 3: The Tenants of The Pulse

Source: Company data

Figure 4: The Online And Offline Promotional Channels of The Pulse

iBeacon, a cost efficient positioning system that interacts with smart phones' applications is incorporated in The Pulse's marketing activities. This allows EIH to efficiently gather information on customer behaviors that would enhance its tenant management and would in turn boost The Pulse's rental growth potential.

Source: U HK

Figure 5: Hot Tub Cinema (Top) And Bubble Soccer (Bottom)

Marketing activities launched in 1HFY15

including “Hot Tub Cinema” and “Bubble

Soccer” were well received by target custom-

er groups.

5

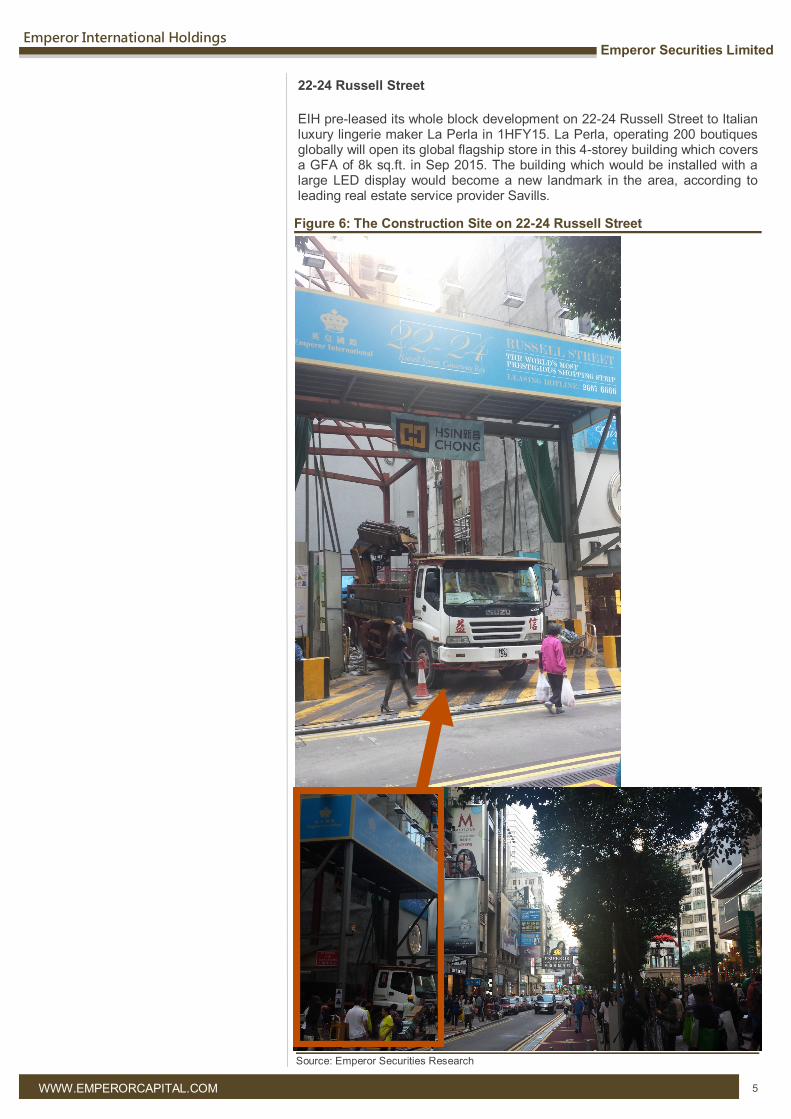

22-24 Russell Street

EIH pre-leased its whole block development on 22-24 Russell Street to Italian luxury lingerie maker La Perla in 1HFY15. La Perla, operating 200 boutiques globally will open its global flagship store in this 4-storey building which covers a GFA of 8k sq.ft. in Sep 2015. The building which would be installed with a large LED display would become a new landmark in the area, according to leading real estate service provider Savills.

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Emperor Securities Research

Figure 6: The Construction Site on 22-24 Russell Street

6

181-183 Oxford Street, London

EIH has just acquired a freehold 7-storey retail and office complex in London, UK with £35mn (equivalent to HK$425mn) cash. This development which covers a GFA of 12.7k sq. ft. is located on Oxford Street, one of most popular shopping destinations in the metropolis. Given the promising pedestrian traffic in the area, we expect solid rental income from the newly acquired property and see its potential for capital appreciation in the years ahead.

71-75 Avenida do Infante D. Henrique & 514-540 Avenida da Praia

Grande, Macau

In Macau, the construction work at Nos. 71-75 Avenida do Infante D. Henrique & Nos. 514-540 Avenida da Praia Grande is currently underway. A multi-storey premium retail complex with a GFA of 30k sq. ft. is expected to be completed in 2015.

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data

Figure 7: The Location of The Newly Acquired Property on Oxford Street

Source: Company data

Figure 8: The Construction Site on 71-75 Avenida do Infante D. Henrique & 514-540 Avenida da Praia Grande

7

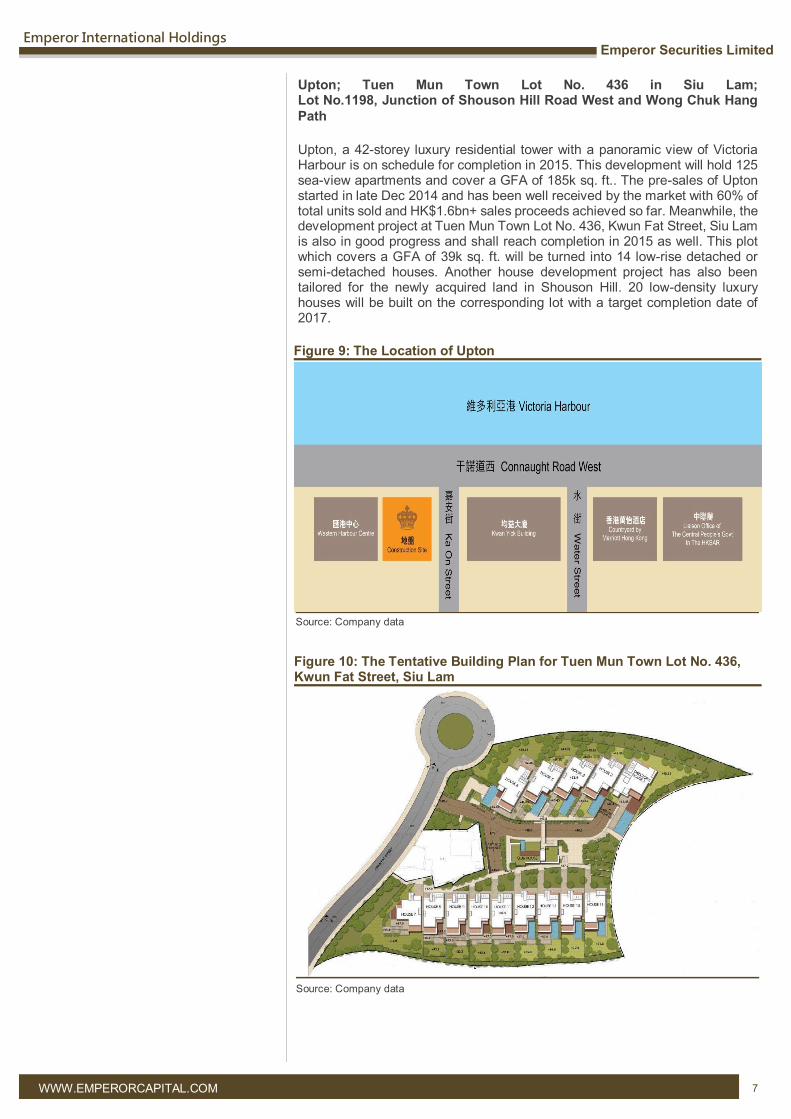

Upton; Tuen Mun Town Lot No. 436 in Siu Lam; Lot No.1198, Junction of Shouson Hill Road West and Wong Chuk Hang

Path

Upton, a 42-storey luxury residential tower with a panoramic view of Victoria Harbour is on schedule for completion in 2015. This development will hold 125 sea-view apartments and cover a GFA of 185k sq. ft.. The pre-sales of Upton started in late Dec 2014 and has been well received by the market with 60% of total units sold and HK$1.6bn+ sales proceeds achieved so far. Meanwhile, the development project at Tuen Mun Town Lot No. 436, Kwun Fat Street, Siu Lam is also in good progress and shall reach completion in 2015 as well. This plot which covers a GFA of 39k sq. ft. will be turned into 14 low-rise detached or semi-detached houses. Another house development project has also been tailored for the newly acquired land in Shouson Hill. 20 low-density luxury houses will be built on the corresponding lot with a target completion date of 2017.

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data

Figure 9: The Location of Upton

Source: Company data

Figure 10: The Tentative Building Plan for Tuen Mun Town Lot No. 436, Kwun Fat Street, Siu Lam

8

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data

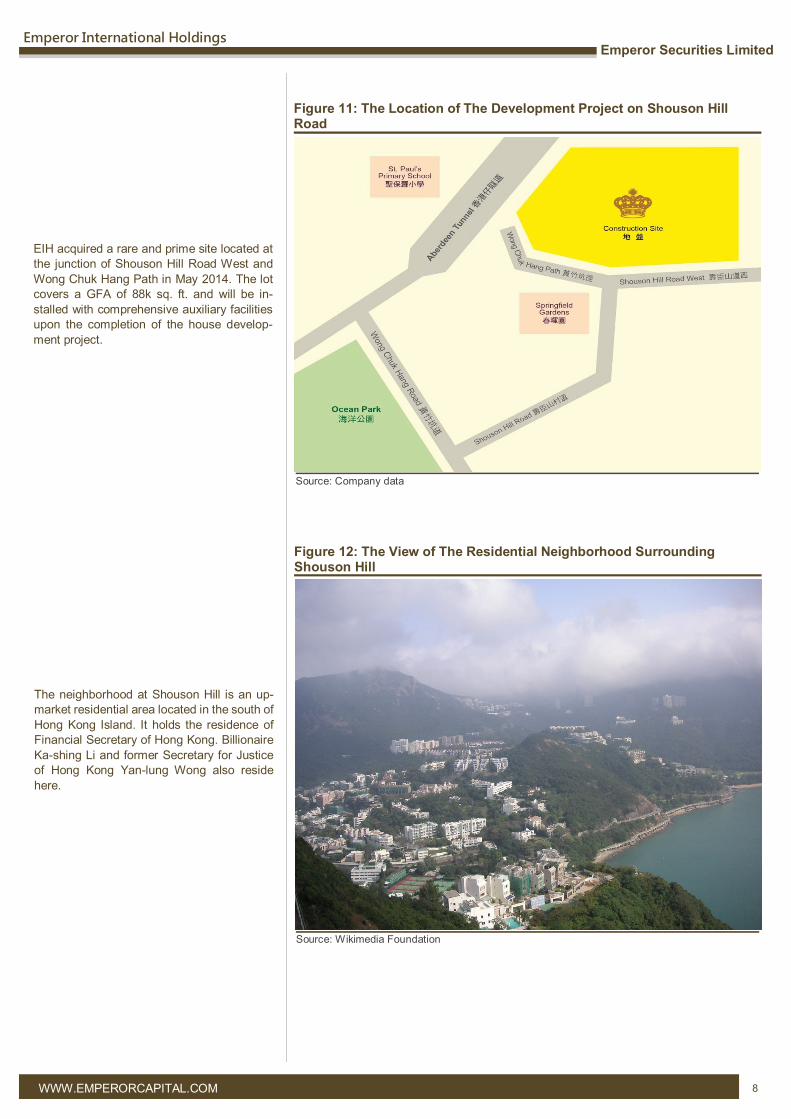

Figure 11: The Location of The Development Project on Shouson Hill Road

Source: Wikimedia Foundation

Figure 12: The View of The Residential Neighborhood Surrounding Shouson Hill

EIH acquired a rare and prime site located at

the junction of Shouson Hill Road West and

Wong Chuk Hang Path in May 2014. The lot

covers a GFA of 88k sq. ft. and will be in-

stalled with comprehensive auxiliary facilities

upon the completion of the house develop-

ment project.

The neighborhood at Shouson Hill is an up-

market residential area located in the south of

Hong Kong Island. It holds the residence of

Financial Secretary of Hong Kong. Billionaire

Ka-shing Li and former Secretary for Justice

of Hong Kong Yan-lung Wong also reside

here.

9

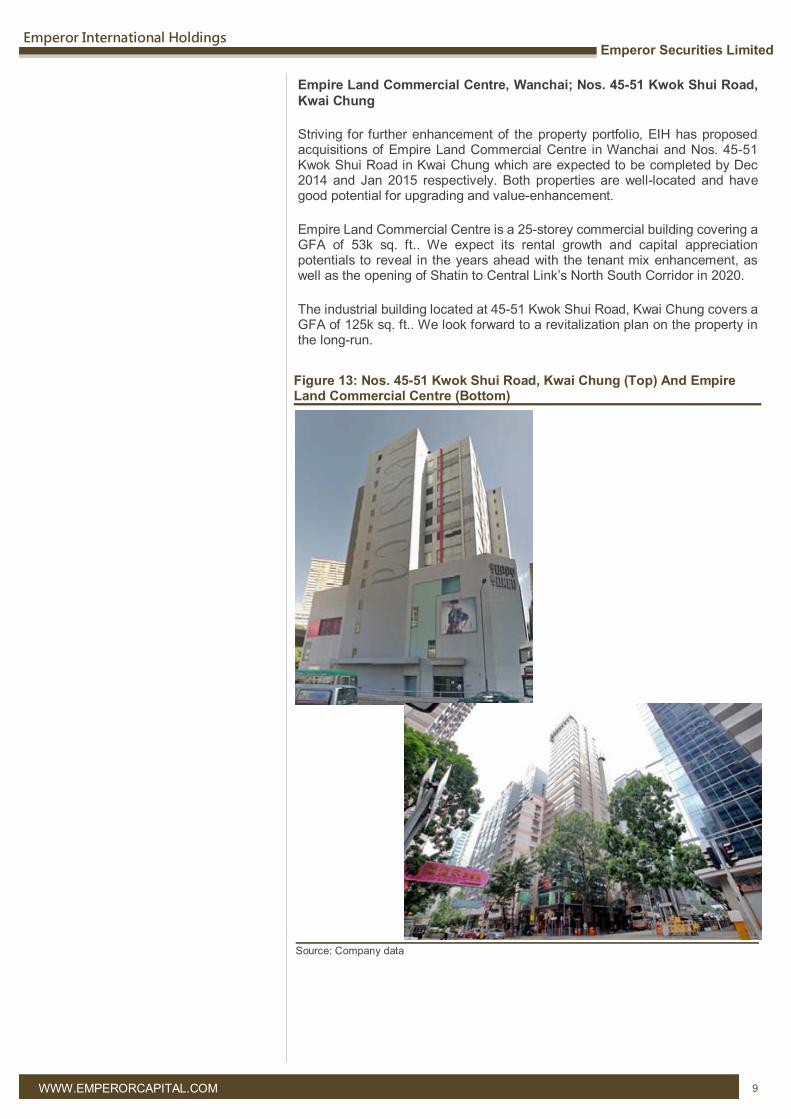

Empire Land Commercial Centre, Wanchai; Nos. 45-51 Kwok Shui Road,

Kwai Chung

Striving for further enhancement of the property portfolio, EIH has proposed acquisitions of Empire Land Commercial Centre in Wanchai and Nos. 45-51 Kwok Shui Road in Kwai Chung which are expected to be completed by Dec 2014 and Jan 2015 respectively. Both properties are well-located and have good potential for upgrading and value-enhancement.

Empire Land Commercial Centre is a 25-storey commercial building covering a GFA of 53k sq. ft.. We expect its rental growth and capital appreciation potentials to reveal in the years ahead with the tenant mix enhancement, as well as the opening of Shatin to Central Link’s North South Corridor in 2020.

The industrial building located at 45-51 Kwok Shui Road, Kwai Chung covers a GFA of 125k sq. ft.. We look forward to a revitalization plan on the property in the long-run.

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data

Figure 13: Nos. 45-51 Kwok Shui Road, Kwai Chung (Top) And Empire Land Commercial Centre (Bottom)

10

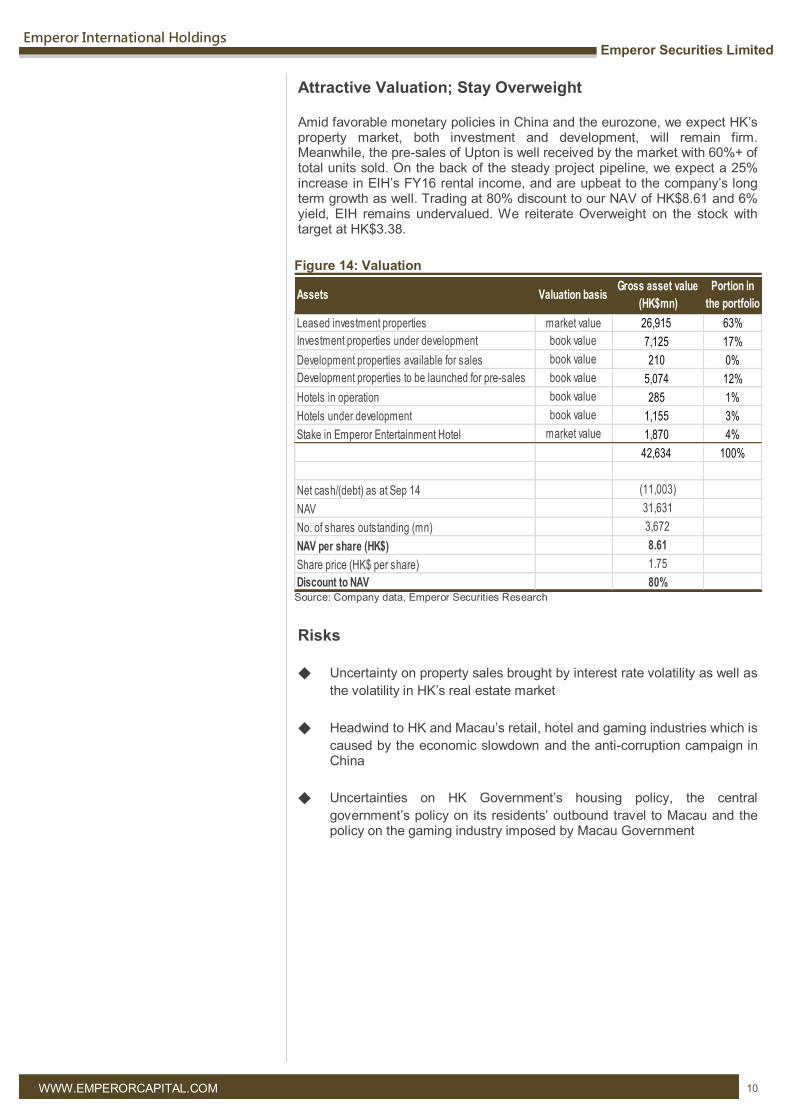

Attractive Valuation; Stay Overweight

Amid favorable monetary policies in China and the eurozone, we expect HK’s property market, both investment and development, will remain firm. Meanwhile, the pre-sales of Upton is well received by the market with 60%+ of total units sold. On the back of the steady project pipeline, we expect a 25% increase in EIH’s FY16 rental income, and are upbeat to the company’s long term growth as well. Trading at 80% discount to our NAV of HK$8.61 and 6% yield, EIH remains undervalued. We reiterate Overweight on the stock with target at HK$3.38.

Risks

◆ Uncertainty on property sales brought by interest rate volatility as well as

the volatility in HK’s real estate market

◆ Headwind to HK and Macau’s retail, hotel and gaming industries which is

caused by the economic slowdown and the anti-corruption campaign in China

◆ Uncertainties on HK Government’s housing policy, the central

government’s policy on its residents’ outbound travel to Macau and the policy on the gaming industry imposed by Macau Government

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data, Emperor Securities Research

Figure 14: Valuation

Assets Valuation basisGross asset value

(HK$mn)

Portion in

the portfolio

Leased investment properties market value 26,915 63%

Investment properties under development book value 7,125 17%

Development properties available for sales book value 210 0%

Development properties to be launched for pre-sales book value 5,074 12%

Hotels in operation book value 285 1%

Hotels under development book value 1,155 3%

Stake in Emperor Entertainment Hotel market value 1,870 4%

42,634 100%

Net cash/(debt) as at Sep 14 (11,003)

NAV 31,631

No. of shares outstanding (mn) 3,672

NAV per share (HK$) 8.61

Share price (HK$ per share) 1.75

Discount to NAV 80%

11

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

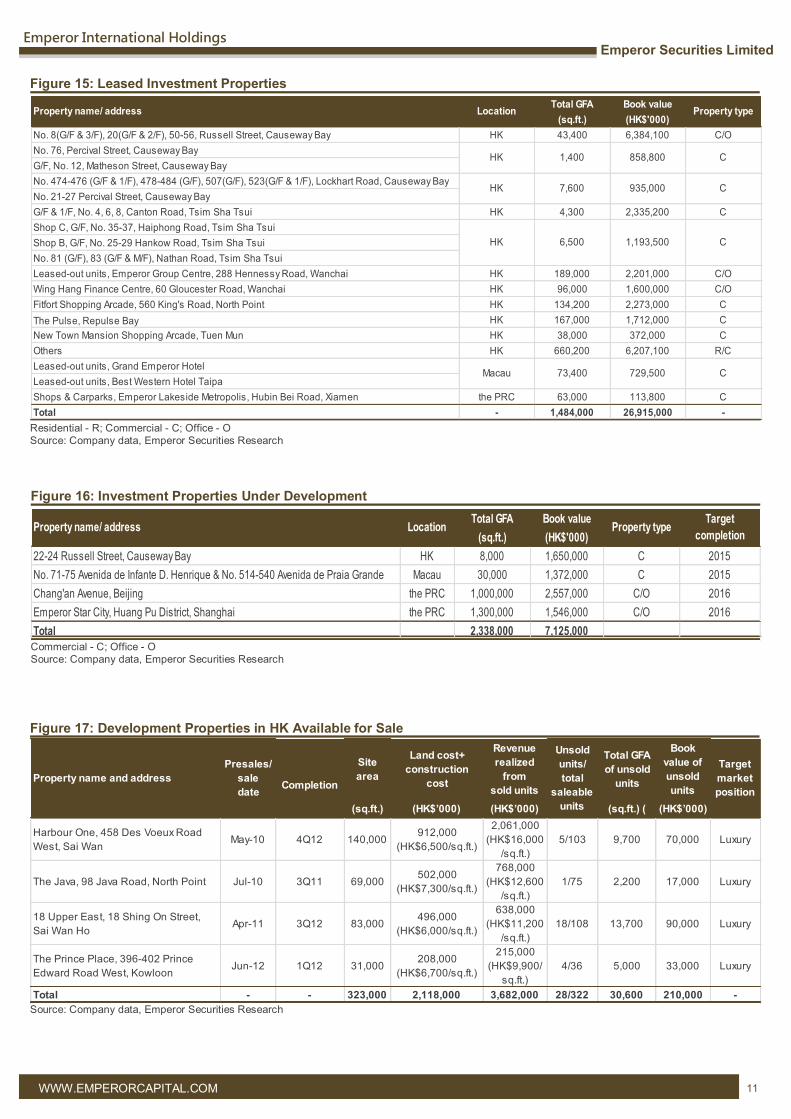

Residential - R; Commercial - C; Office - O

Source: Company data, Emperor Securities Research

Figure 15: Leased Investment Properties

Commercial - C; Office - O

Source: Company data, Emperor Securities Research

Figure 16: Investment Properties Under Development

Source: Company data, Emperor Securities Research

Figure 17: Development Properties in HK Available for Sale

Total GFA Book value

(sq.ft.) (HK$'000)

22-24 Russell Street, Causeway Bay HK 8,000 1,650,000 C 2015

No. 71-75 Avenida de Infante D. Henrique & No. 514-540 Avenida de Praia Grande Macau 30,000 1,372,000 C 2015

Chang'an Avenue, Beijing the PRC 1,000,000 2,557,000 C/O 2016

Emperor Star City, Huang Pu District, Shanghai the PRC 1,300,000 1,546,000 C/O 2016

Total 2,338,000 7,125,000

Target

completionProperty name/ address Location Property type

Site

area

Land cost+

construction

cost

Revenue

realized

from

sold units

Total GFA

of unsold

units

Book

value of

unsold

units

(sq.ft.) (HK$’000) (HK$’000) (sq.ft.) ( (HK$’000)

Harbour One, 458 Des Voeux Road

West, Sai WanMay-10 4Q12 140,000

912,000

(HK$6,500/sq.ft.)

2,061,000

(HK$16,000

/sq.ft.)

5/103 9,700 70,000 Luxury

The Java, 98 Java Road, North Point Jul-10 3Q11 69,000502,000

(HK$7,300/sq.ft.)

768,000

(HK$12,600

/sq.ft.)

1/75 2,200 17,000 Luxury

18 Upper East, 18 Shing On Street,

Sai Wan HoApr-11 3Q12 83,000

496,000

(HK$6,000/sq.ft.)

638,000

(HK$11,200

/sq.ft.)

18/108 13,700 90,000 Luxury

The Prince Place, 396-402 Prince

Edward Road West, KowloonJun-12 1Q12 31,000

208,000

(HK$6,700/sq.ft.)

215,000

(HK$9,900/

sq.ft.)

4/36 5,000 33,000 Luxury

Total - - 323,000 2,118,000 3,682,000 28/322 30,600 210,000 -

Presales/

sale

date

Target

market

position

Unsold

units/

total

saleable

units

CompletionProperty name and address

Total GFA Book value

(sq.ft.) (HK$'000)

No. 8(G/F & 3/F), 20(G/F & 2/F), 50-56, Russell Street, Causeway Bay HK 43,400 6,384,100 C/O

No. 76, Percival Street, Causeway Bay

G/F, No. 12, Matheson Street, Causeway Bay

No. 474-476 (G/F & 1/F), 478-484 (G/F), 507(G/F), 523(G/F & 1/F), Lockhart Road, Causeway Bay

No. 21-27 Percival Street, Causeway Bay

G/F & 1/F, No. 4, 6, 8, Canton Road, Tsim Sha Tsui HK 4,300 2,335,200 C

Shop C, G/F, No. 35-37, Haiphong Road, Tsim Sha Tsui

Shop B, G/F, No. 25-29 Hankow Road, Tsim Sha Tsui

No. 81 (G/F), 83 (G/F & M/F), Nathan Road, Tsim Sha Tsui

Leased-out units, Emperor Group Centre, 288 Hennessy Road, Wanchai HK 189,000 2,201,000 C/O

Wing Hang Finance Centre, 60 Gloucester Road, Wanchai HK 96,000 1,600,000 C/O

Fitfort Shopping Arcade, 560 King's Road, North Point HK 134,200 2,273,000 C

The Pulse, Repulse Bay HK 167,000 1,712,000 C

New Town Mansion Shopping Arcade, Tuen Mun HK 38,000 372,000 C

Others HK 660,200 6,207,100 R/C

Leased-out units, Grand Emperor Hotel

Leased-out units, Best Western Hotel Taipa

Shops & Carparks, Emperor Lakeside Metropolis, Hubin Bei Road, Xiamen the PRC 63,000 113,800 C

Total - 1,484,000 26,915,000 -

HK 7,600 935,000 C

729,50073,400 C

CHK 1,400

Property type

1,193,500 C

Macau

LocationProperty name/ address

HK 6,500

858,800

12

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

Source: Company data, Emperor Securities Research

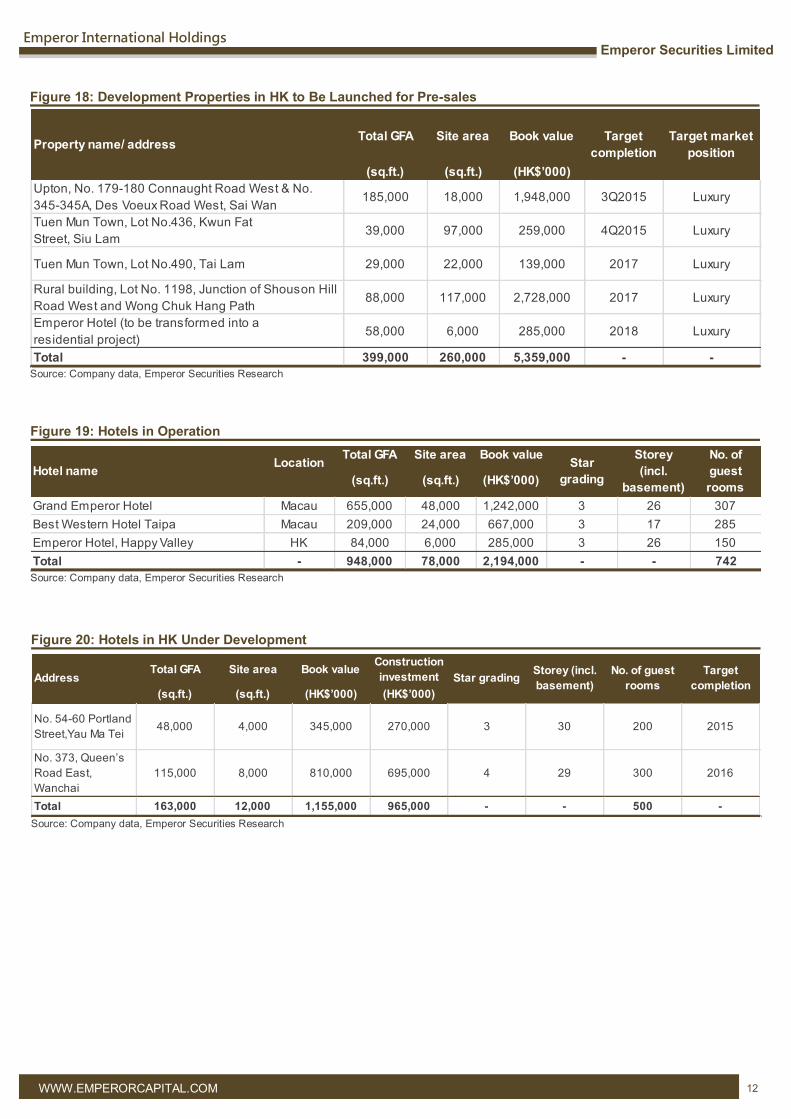

Figure 18: Development Properties in HK to Be Launched for Pre-sales

Source: Company data, Emperor Securities Research

Figure 19: Hotels in Operation

Total GFA Site area Book value

(sq.ft.) (sq.ft.) (HK$’000)

Grand Emperor Hotel Macau 655,000 48,000 1,242,000 3 26 307

Best Western Hotel Taipa Macau 209,000 24,000 667,000 3 17 285

Emperor Hotel, Happy Valley HK 84,000 6,000 285,000 3 26 150

Total - 948,000 78,000 2,194,000 - - 742

LocationNo. of

guest

rooms

Star

gradingHotel name

Storey

(incl.

basement)

Source: Company data, Emperor Securities Research

Figure 20: Hotels in HK Under Development

Total GFA Site area Book valueConstruction

investment

(sq.ft.) (sq.ft.) (HK$’000) (HK$’000)

No. 54-60 Portland

Street,Yau Ma Tei48,000 4,000 345,000 270,000 3 30 200 2015

No. 373, Queen’s

Road East,

Wanchai

115,000 8,000 810,000 695,000 4 29 300 2016

Total 163,000 12,000 1,155,000 965,000 - - 500 -

Target

completion

Storey (incl.

basement)

No. of guest

roomsStar gradingAddress

Total GFA Site area Book value

(sq.ft.) (sq.ft.) (HK$’000)

Upton, No. 179-180 Connaught Road West & No.

345-345A, Des Voeux Road West, Sai Wan185,000 18,000 1,948,000 3Q2015 Luxury

Tuen Mun Town, Lot No.436, Kwun Fat

Street, Siu Lam39,000 97,000 259,000 4Q2015 Luxury

Tuen Mun Town, Lot No.490, Tai Lam 29,000 22,000 139,000 2017 Luxury

Rural building, Lot No. 1198, Junction of Shouson Hill

Road West and Wong Chuk Hang Path88,000 117,000 2,728,000 2017 Luxury

Emperor Hotel (to be transformed into a

residential project)58,000 6,000 285,000 2018 Luxury

Total 399,000 260,000 5,359,000 - -

Target

completion

Target market

positionProperty name/ address

13

WWW.EMPERORCAPITAL.COM

Emperor International Holdings

Emperor Securities Limited

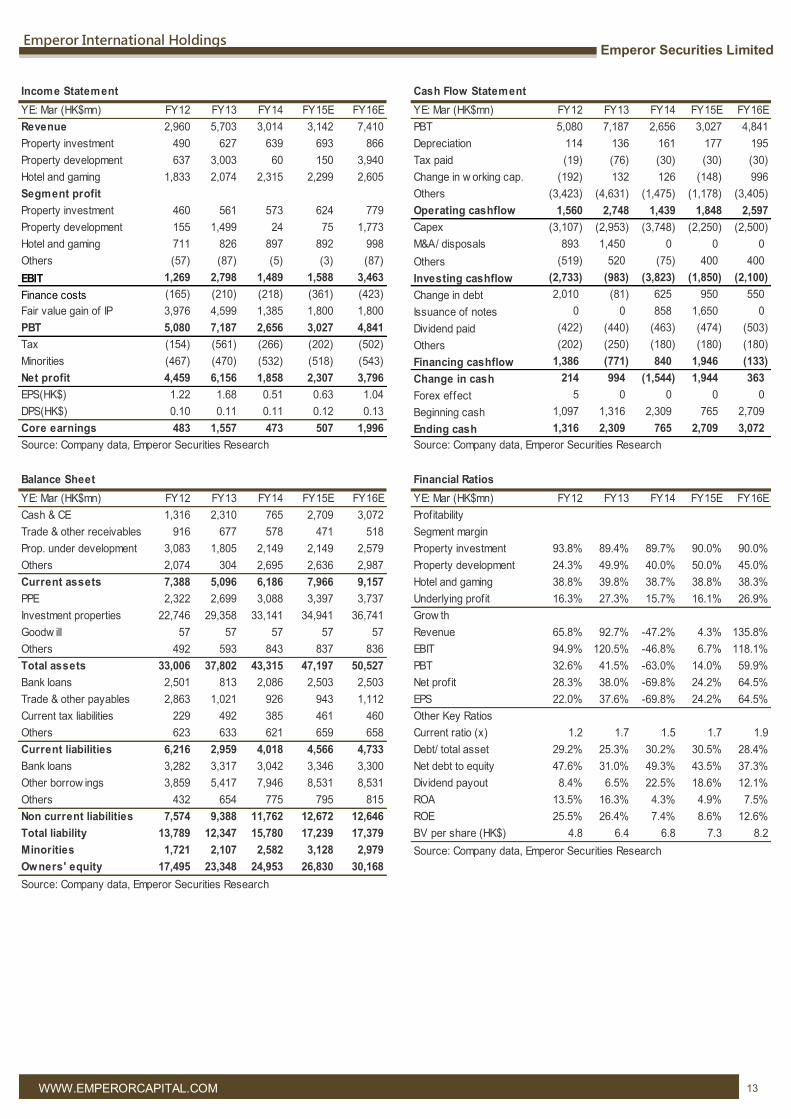

Income Statement Cash Flow Statement

YE: Mar (HK$mn) FY12 FY13 FY14 FY15E FY16E YE: Mar (HK$mn) FY12 FY13 FY14 FY15E FY16E

Revenue 2,960 5,703 3,014 3,142 7,410 PBT 5,080 7,187 2,656 3,027 4,841

Property investment 490 627 639 693 866 Depreciation 114 136 161 177 195

Property development 637 3,003 60 150 3,940 Tax paid (19) (76) (30) (30) (30)

Hotel and gaming 1,833 2,074 2,315 2,299 2,605 Change in w orking cap. (192) 132 126 (148) 996

Segment profit Others (3,423) (4,631) (1,475) (1,178) (3,405)

Property investment 460 561 573 624 779 Operating cashflow 1,560 2,748 1,439 1,848 2,597

Property development 155 1,499 24 75 1,773 Capex (3,107) (2,953) (3,748) (2,250) (2,500)

Hotel and gaming 711 826 897 892 998 M&A/ disposals 893 1,450 0 0 0

Others (57) (87) (5) (3) (87) Others (519) 520 (75) 400 400

EBIT 1,269 2,798 1,489 1,588 3,463 Investing cashflow (2,733) (983) (3,823) (1,850) (2,100)

Finance costs (165) (210) (218) (361) (423) Change in debt 2,010 (81) 625 950 550

Fair value gain of IP 3,976 4,599 1,385 1,800 1,800 Issuance of notes 0 0 858 1,650 0

PBT 5,080 7,187 2,656 3,027 4,841 Dividend paid (422) (440) (463) (474) (503)

Tax (154) (561) (266) (202) (502) Others (202) (250) (180) (180) (180)

Minorities (467) (470) (532) (518) (543) Financing cashflow 1,386 (771) 840 1,946 (133)

Net profit 4,459 6,156 1,858 2,307 3,796 Change in cash 214 994 (1,544) 1,944 363

EPS(HK$) 1.22 1.68 0.51 0.63 1.04 Forex effect 5 0 0 0 0

DPS(HK$) 0.10 0.11 0.11 0.12 0.13 Beginning cash 1,097 1,316 2,309 765 2,709

Core earnings 483 1,557 473 507 1,996 Ending cash 1,316 2,309 765 2,709 3,072

Source: Company data, Emperor Securities Research Source: Company data, Emperor Securities Research

YE: Mar (HK$mn) FY12 FY13 FY14 FY15E FY16E YE: Mar (HK$mn) FY12 FY13 FY14 FY15E FY16E

Cash & CE 1,316 2,310 765 2,709 3,072 Profitability

Trade & other receivables 916 677 578 471 518 Segment margin

Prop. under development 3,083 1,805 2,149 2,149 2,579 Property investment 93.8% 89.4% 89.7% 90.0% 90.0%

Others 2,074 304 2,695 2,636 2,987 Property development 24.3% 49.9% 40.0% 50.0% 45.0%

Current assets 7,388 5,096 6,186 7,966 9,157 Hotel and gaming 38.8% 39.8% 38.7% 38.8% 38.3%

PPE 2,322 2,699 3,088 3,397 3,737 Underlying profit 16.3% 27.3% 15.7% 16.1% 26.9%

Investment properties 22,746 29,358 33,141 34,941 36,741 Grow th

Goodw ill 57 57 57 57 57 Revenue 65.8% 92.7% -47.2% 4.3% 135.8%

Others 492 593 843 837 836 EBIT 94.9% 120.5% -46.8% 6.7% 118.1%

Total assets 33,006 37,802 43,315 47,197 50,527 PBT 32.6% 41.5% -63.0% 14.0% 59.9%

Bank loans 2,501 813 2,086 2,503 2,503 Net profit 28.3% 38.0% -69.8% 24.2% 64.5%

Trade & other payables 2,863 1,021 926 943 1,112 EPS 22.0% 37.6% -69.8% 24.2% 64.5%

Current tax liabilities 229 492 385 461 460 Other Key Ratios

Others 623 633 621 659 658 Current ratio (x) 1.2 1.7 1.5 1.7 1.9

Current liabilities 6,216 2,959 4,018 4,566 4,733 Debt/ total asset 29.2% 25.3% 30.2% 30.5% 28.4%

Bank loans 3,282 3,317 3,042 3,346 3,300 Net debt to equity 47.6% 31.0% 49.3% 43.5% 37.3%

Other borrow ings 3,859 5,417 7,946 8,531 8,531 Dividend payout 8.4% 6.5% 22.5% 18.6% 12.1%

Others 432 654 775 795 815 ROA 13.5% 16.3% 4.3% 4.9% 7.5%

Non current liabilities 7,574 9,388 11,762 12,672 12,646 ROE 25.5% 26.4% 7.4% 8.6% 12.6%

Total liability 13,789 12,347 15,780 17,239 17,379 BV per share (HK$) 4.8 6.4 6.8 7.3 8.2

Minorities 1,721 2,107 2,582 3,128 2,979 Source: Company data, Emperor Securities Research

Owners' equity 17,495 23,348 24,953 26,830 30,168

Source: Company data, Emperor Securities Research

Balance Sheet Financial Ratios

14

The information contained in this report has been compiled from sources believed to be reliable and has been compiled with high integrity, but Emperor

Securities Limited (“Emperor Securities”) or any member of Emperor Capital Group (“ECG”) does not make any representation or warranty as to its accuracy,

completeness or correctness. The information and opinions contained in this report are or may be subject to change or revision without any notice. This report is

for information purposes only. No representation, warranty or guarantee whatsoever, whether expressed or implied, is made as to its accuracy or completeness

and should not be construed as an offer to buy or sell or the solicitation of an offer to buy or sell the securities mentioned. Emperor Securities and ECG do not

accept any responsibility or liability whatsoever for any direct or consequential loss or damage of whatsoever nature arising from or as a result of the use in whole

or in part of this report or any of its contents.

The research analyst(s) who prepared this report hereby confirm the views expressed in this report only reflect the personal views of the research analyst(s) about

the subject company(ies) and their securities. The research analyst(s) also confirm the research analyst(s) were not, are not, and will not be receiving any direct or

indirect compensation or other benefits for expressing the specific recommendation(s) or view(s) in this report. Emperor Securities is a wholly-owned subsidiary

of ECG. Both ECG and Emperor International Holdings Limited are companies listed on the Hong Kong Stock Exchange and with a common controlling

shareholder. Apart from that, Emperor Securities and ECG and their respective directors, officers, partners, representatives, or employees may have positions or

otherwise be directly or indirectly interested in the securities mentioned in this report or may buy, sell, or deal or offer to buy, sell, or deal in or with such

securities from time to time, whether as principal for its or their own account or as agent or in any other capacity for or on behalf of another person.

Copyright protection and other rights exist or subsist in this report, which may accordingly not be used for any other purpose, nor sold, distributed, published, or

reproduced in any manner without the express consent of Emperor Securities.

WWW.EMPERORCAPITAL.COM

Disclaimers And Disclosures

Emperor International Holdings

Emperor Securities Limited

Emperor Securities Research Stanley Chan

Associate Director

Tel : (852) 2836 2733

Email : [email protected]

Frankie Chan

Research Analyst

Tel : (852) 2836 2566

Email : [email protected]

David Yuen

Senior Research Analyst

Tel : (852) 2836 2797

Email : [email protected]

Ian Lam

Research Analyst

Tel : (852) 2836 2763

Email : [email protected]

15

WWW.EMPERORCAPITAL.COM

Contact Us

Emperor International Holdings

Emperor Securities Limited

Emperor Securities Limited

New Territories Headquarters

23-24/F, Emperor Group Centre, 288 Hennessy Road, Wan Chai, HK

Tel : Hong Kong Hotline (852) 2919 2919

Northern China Toll-free Hotline 10800 852 1674

Southern China Toll-free Hotline 10800 152 1674

Fax : Hong Kong Fax (852) 2893 1540

Northern China Toll-free Fax 10800 852 1673

Southern China Toll-free Fax 10800 152 1673

16/F, Hang Seng Tsuen Wan Building, No.289 Sha Tsui Road, Tsuen Wan

Tel : (852) 2838 2939

Fax: (852) 2412 0249

Shop 2, G/F Kam Wo Bu & Kam Hing Building, No . 3 -15 Shun Lung Street Sha Tau

Kok

Tel : (852) 2659 7668

Fax : (852) 2659 7381

G/F, 19 Tai Wai Road, Tai Wai Tel : (852) 2699 8226

Fax : (852) 2699 8749

Shop B7, G/F, Kar Ho Building, 27-31 Hong Lok Road, Yuen Long

Tel : (852) 2479 9820

Fax: (852) 2470 5280

Emperor Financial Services Centre

Shops 2-6, G/F, East Ocean Court, 525 Shanghai Street, Mongkok, Kowloon

Tel : Hong Kong Hotline (852) 3966 0668

Northern China Toll-free Hotline 10800 852 1805

Southern China Toll-free Hotline 10800 152 1805

Fax : Hong Kong Fax (852) 2919 2938

Northern China Toll-free Fax 10800 852 1804

Southern China Toll-free Fax 10800 152 1804

Mainland Information Centres Guangzhou

Room 2111, R&F To-Win Building, No. 30 Huaxia Road, Tianhe District, Guangzhou

Tel : (86) 10 3836 9380

Fax : (86) 10 3836 9856

Shanghai

2202, City Gateway, 398 Caoxi Road (North), Shanghai

Tel : (86) 21 5396 6228 / (86) 21 5396 6218

Fax : (86) 21 6386 6280

Beijing

Room 607, Block A, Jian Wai Soho Building, No. 39 East 3rd-Ring Middle Road,

Chao Yang District, Beijing

Tel : (86) 10 5900 0858

Fax : (86) 10 5900 0602

Hong Kong Island

Shop 67, G/F, Fortuna Building, 63-69 Wellington Street, Central

Tel : (852) 2522 1181

Fax : (852) 2522 2919 Emperor Wealth Management Limited Shops 2-6, G/F, East Ocean Court, 525 Shanghai Street, Mongkok, Kowloon

Tel : (852) 2919 2913

Fax : (852) 2919 2930

Room 705-6, Tai Yau Building, 181 Johnston Road, Wanchai

Tel : (852) 2818 7278

Fax : (852) 2838 8368 Emperor Securities Research Tel :(852) 2836 2763

Fax :(852) 2831 8089

Email : [email protected]

Shop E, G/F 983-987A King’s Road, Quarry Bay

Tel : (852) 2911 0778

Fax : (852) 2911 0378

Email Addresses Emperor Securities Limited

Emperor Futures Limited

Emperor Wealth Management Limited

Kowloon

Shop C, G/F, No. 53-59 Wuhu Street, Hung Hom Tel : (852) 2364 9213 Fax : (852) 2765 8425

G/F, Full Art Court, 149 Kweilin Street, Sham Shui Po Tel : (852) 2725 7883 Fax : (852) 2728 6257

Shop 4, G/F, No.132-134 Nga Tsin Wai Road, Kowloon City Tel : (852) 2383 2262 Fax : (852) 2383 2246

Shop A, G/F, 150-152, Prince Edward Road West, Prince Edward Tel : (852) 2827 1188 Fax : (852) 2838 2319