27 may 2005, issue 8 t the post andersens ... post andersens environment across europe on 4 march...

TRANSCRIPT

THE POST ANDERSENS

ENVIRONMENT ACROSS EUROPE

On 4 March 2005, the European Court of Justice (‘the ECJ’) ruled in the case of Arthur Andersen & Co. (‘Andersens’) that Article 13B(a) of the EC Sixth VAT Directive must be interpreted as meaning that “back office” activities, consisting in rendering services, for payment, to an insurance company do not constitute the performance of services relating to insurance transactions carried out by an insurance broker or an insurance agent within the meaning of that provision.

The purpose of this FS VAT alert is to provide a brief update on the general impact of the decision across Europe. This VAT alert should not be used as a substitute for actual local VAT advice, since the impact of Andersens on some companies will differ from the national trend.

Summary

There has clearly been an uneven playing field in the European insurance sector. This is shown by the already diverse nature of responses to the impact of Andersens. The full impact of the decision is, in many countries, as yet unrealised, since it will take time for the tax authorities to release guidance/amend legislation, where required. However, it remains clear that Andersens will shake-up the European insurance industry, and begin to address the uneven interpretation of Article 13B(a) across Europe.

Please feel free to contact your local PwC representative for further advice, commentary and updates on developments in the insurance sector post-Andersens.

Country Reports

AustriaThere has only been a limited reaction in the market place to date. The Austrian Ministry of Finance has not received any inquiries. However the decision may well lead to a change in local legislation resulting in a stricter interpretation of the VAT exemption. For example, the Austrian administrative guidelines currently state that the procurement of insurance is exempt and that it is not decisive, whether the customer can exercise its right against the insurance company or against a third company. This treatment does not follow the ruling in Andersens and so may have to change.

BelgiumAndersens clearly has implications in the local market for both insurers, outsourcers as well as insurance intermediaries (be they recognised as such or not). In some cases, the benefit of outsourcing may be lost for insurers, i.e. 'consumed' by the 21% VAT rate. For instance, in Belgium it is not uncommon for insurance companies in 'run off' to outsource various functions (such as claims management or administration) to 3rd parties. VAT is not always applied on the outsourced services as - in the concerned parties' view - the services qualify as exempt insurance linked intermediary services.

27 May 2005, Issue 8

Fina

ncia

l Ser

vice

s VA

T Al

ert

*connectedthinking™

It should be checked on a case-by-case basis whether the non-application of VAT is 'still' correct in light of Andersens.

Also duly recognised insurance intermediaries could be affected by Andersens. Over the years, the business of some of these intermediaries has evolved from traditional brokerage to full servicing, including consultancy and sometimes their services do not involve the prospecting and introduction of clients, i.e. the essential elements for VAT exemption under Andersens.

The Tax Authorities have now taken a formal decision on Andersens which 'prima facie' is in line with the ECJ decision. Although the decision leaves room for interpretation, the Tax Authorities seem to be restricting their traditionally liberal (and officially published) interpretations of the VAT exemption for insurance related services. They urge the concerned parties to take 'remedial action' and comply by 1 July 2005. PwC is working with clients to take appropriate action. .

CyprusThere are serious concerns from local proxy agents representing multinational insurance companies. They are concerned that VAT will now be chargeable on some of the services that they provide. This will increase costs for the insurers and be an administrative burden for them.

Czech RepublicMany local insurers do not outsource to a great extent, so the reaction to the case is yet to be realised. The current drafting of the Czech legislation in relation to the insurance exemption is quite broad and not very specific (for example, referring simply to intermediary services relating to insurance). However, the Ministry of Finance has not suggested that the local legislation will change. The Ministry of Finance does want to introduce some other changes relating to the recharging of insurance, but this is a separate issue.

DenmarkThe Andersens case does not appear to cause major concerns for the industry. This could be linked to the fact that outsourcing has been applied in a rather limited number of cases. Moreover the outsourcing that has actually been undertaken is already treated as taxable. The Danish industry body ‘Forsikring & Pension’ is currently 100% focused on agreeing with the tax authorities on a pro rata calculation method.

FinlandThe Andersens case is likely to have a significant impact on the market, due to the liberal interpretation of the insurance exemption. Exempt insurance services previously included services in relation to the compilation of statistics in relation to pensions and insurance benefits; services in relation to the forecasting of pension liability; and services in relation to the assessment of insured losses and damages. Andersens suggests that such services may now be taxable.

FranceThe impact of the Andersens case in the French market has been mixed. The administrative doctrine (3 A 3181 of 20 October 1999) grants the VAT exemption to insurance businesses and intermediaries that are officially allowed by French law to carry out such activities. This administrative doctrine remains unchanged post-Andersens, and can still in principle be used by businesses against the tax authorities where necessary. Fi

nanc

ial S

ervi

ces

VAT

Ale

rt

GermanyAccording to the current jurisdiction of the German Federal Fiscal Court and the VAT Guidelines issued by the German Federal Ministry of Finance, no direct contact with the insured is necessary to get the VAT exemption (e.g. training and controlling insurance agents qualifies for the VAT exemption). The concern is, that this view will change due to Andersens and that new VAT Guidelines will be adopted so that direct contact with both the insurer and the insured will be necessary in order to qualify for the exemption.

GreeceIt is not expected that the decision will have any impact. The exemption is interpreted in circular Pol 1087/1998, which links the exemption closely to insurance business functions as described in insurance law 1569/1985 after its amendment through L 2170/93. As verbally confirmed with the VAT department of the Greek MoF, back office services as in the Andersens case are considered taxable.

HungaryThe Hungarian VAT legislation is expected to be amended in the following months but there is no definite guidance at this time.

IrelandThe decision will, undoubtedly, have an impact on services provided by insurance intermediaries where the intermediary does not have the customer facing role envisaged by the Court. Perhaps the greatest impact will be for the life assurance companies that have established in Ireland on a freedom of services basis. These companies typically outsource to a very significant extent the end to end management of their operations to third party service providers; previously Irish Revenue accepted that these services, where the service provider, like Andersen, had the ability to put the life company on risk, qualified as VAT exempt insurance intermediary services. Andersens would suggest that these services are liable to VAT.

Shortly after the decision, the Irish Revenue issued a statement indicating that they would engage in a consultation process with key informants/industry players to evaluate impact etc. but that the existing treatment of such contracts would continue pro tem. This consultation process is still ongoing.

ItalyThe Andersens case does not appear to cause major concerns in the marketplace. Such back-office functions have always been treated as taxable.

LatviaThere are concerns in the industry about what impact Andersens will have, especially in respect of brokers. The current thinking is that brokerage paid as part of premium should still be VAT exempt but that there are potential problems when brokerage is shared in any way, as at that stage, the person is one-stage removed from the insurance company. This might affect claims adjusters. There are also concerns in the market about the VAT treatment of additional services provided by brokers after an agreement has been signed in order to support a premium. The tax authorities have not released any guidance, although the Insurance Supervisor is fully informed.

LithuaniaThe impact of Andersens has not yet been fully realised. According to the Commentary of the Law on VAT issued by the Tax Authorities, exempt insurance services currently include the administration of insurance con-tracts. Andersens may restrict the scope of the exemption for such services, when performed by third parties that do not act for both insurer and insured.

Fina

ncia

l Ser

vice

s VA

T A

lert

LuxembourgDue to the very restrictive approach taken by the insurance regulatory authorities, the outsourcing as performed by Andersens does not in principle exist. In the limited cases where insurers have outsourced, such as the management of insurance captives, the outsourcers usually charge VAT.

MaltaThe exemption for insurance services was already rather restrictive under the Maltese VAT Act. Therefore, Andersens should have little impact locally, par-ticularly if the outsourcing is done to non-licensed entities – in which case, such services are already subject to VAT.

NetherlandsThe decision has been a wake up call to the insurance industry. It is clear that insurers and service providers have been complacent about the VAT exempt status of some services in the insurance sector. It is also clear that the Tax Authorities have not been alert to insurance-related supplies. The true impact of the decision is unlikely to be felt until the Dutch High Court eleases its final judgement in Andersens (now that the ECJ has responded to the questions referred)

PolandThere are limited concerns in the market due to the restrictive text of the domestic legislation.

PortugalThere appears to be only a limited impact on the market.

SloveniaThe Andersens case does not appear to cause major concerns for the industry. This could be linked to the fact that outsourcing has been applied in a rather limited number of cases. Moreover the outsourcing that has actually been undertaken is already treated as taxable.

SpainThere has been no real impact in Spain because outsourcing is not common in the insurance sector.

SwedenThere has been no real impact in Sweden because the tax courts previously adopted the position ruled in Andersens.

United KingdomThe decision has had a drastic impact on agents and service providers. Traditional broking services are likely to be unaffected because they prospect and introduce. It is clear that the exemption has been construed much more widely in the UK than is possible under the Andersens decision so many contracts will be affected. The main concern is that some contracts will no longer be economically viable if VAT is added. In others, the VAT cost is onerous, but not necessarily prohibitive.

The Association of British Insurers is acting for a group of insurers and service providers in consultation with the Tax Authorities, but after some initial discussions, everyone has been waiting for the Tax Authorities to publish their position.

On 18 May 2005, the UK Tax Authorities released their much anticipated Business Brief in respect of Andersens. The Tax Authorities have stated that certain insurance administration services, claims handling services and third party administration services will only fall within the exemption for insurance-related services where the provider had also previously introduced the policyholder to the insurer.

Fina

ncia

l Ser

vice

s VA

T A

lert

The exemption may still apply where the service provider does not itself have direct contact with the customer, provided that it has sub-contracted the introductory services to a sub-agent, and there is a direct contractual link between the principal agent and the agent providing the introductory service.

The Tax Authorities plan to consult the insurance industry before making any amendments to the existing domestic legislation. The consultation paper is due to be issued in July 2005. The consultation will last for 12 weeks.

Taxpayers may rely on current VAT legislation until the consultation is over and the legislation has been amended. This gives businesses some months to clarify affected contracts, re-negotiate terms, lobby the Tax Authorities and to undertake any measures to protect their commercial position.

If you have any questions regarding the mentioned issues or any Financial Services related issues please contact the mentioned author or your local FS VAT Expert:

Austria Christine Sonnleitner +431501883630Belgium Francois Mennig +3227104364CZ Republic Vaclav Patek +420251152569Cyprus Chrysilios Pelekanos +35722555000Denmark Jan Huusmann Christensen +4539459452Estonia Ain Veide +3726141978Finland Juha Laitinen +358922801409France Alain Recoules +33156574405Germany Sylvia Neubert +496995856235Greece Dirk Reinhart +302106874572Hungary Tamas Locsei +3614619358Ireland John Fay +35317048701Italy Pier Luca Mazza +390266995729Jersey Jane Stubbs +1534838244Latvia Helen Barker +3717094421Lithuania Kristina Bartusevisiene +3705392365Luxembourg Michel Lambion +3524948483126Malta David A. Ferry +35625646712Netherlands Frans Oomen +31205684781Norway Yngvar Engelstad Solheim +4795260657Poland Marcin Chomiuk +48225234760Portugal Mario Braz +3512179144053Romania Diana Coroaba +40212028693Slovakia Eva Fricova +421254414101Slovenia Antonia Sheratt +38614750166Spain Miguel Blasco +34915684798Sweden Lars Henckel +46855533326Switzerland Tobias Meier Kern +4116304369United Kingdom Cathy Hargreaves +442072125575

© 2005 PricewaterhouseCoopers. DisclaimerClients receiving this FS VAT Alert should take no action without first contacting their usual PricewaterhouseCoopers Indirect Tax adviser. If you would like to share your views on this FS VAT Alert, please contact Frans Oomen at [email protected].

Fina

ncia

l Ser

vice

s VA

T A

lert

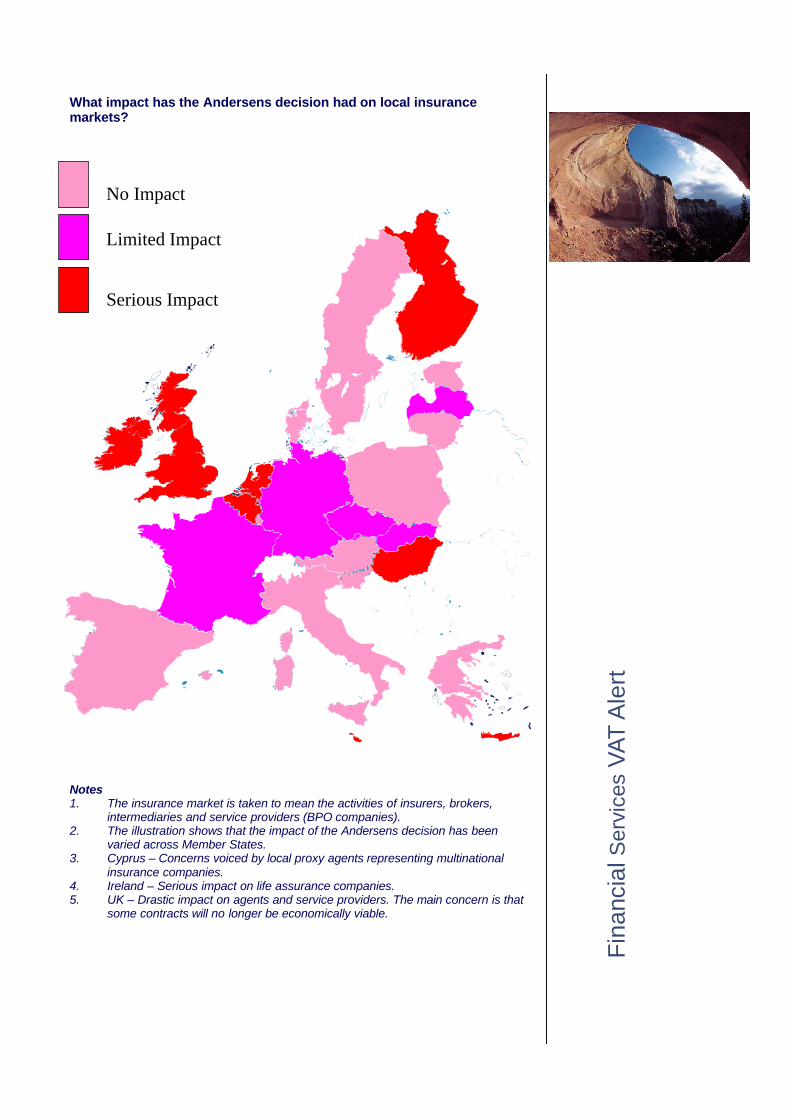

What impact has the Andersens decision had on local insurance markets?

Notes1. The insurance market is taken to mean the activities of insurers, brokers,

intermediaries and service providers (BPO companies).2. The illustration shows that the impact of the Andersens decision has been

varied across Member States.3. Cyprus – Concerns voiced by local proxy agents representing multinational

insurance companies.4. Ireland – Serious impact on life assurance companies.5. UK – Drastic impact on agents and service providers. The main concern is that

some contracts will no longer be economically viable.

Fina

ncia

l Ser

vice

s VA

T A

lert

No Impact

Serious Impact

Limited Impact

Pre-Andersens legislation: Did the text of the local insurance exemption involve a restrictive or liberal interpretation of Article 13(B)(a)?

Notes1. .A restrictive interpretation of Article 13(B)(a) means that it was very difficult for

insurance-related services to achieve exemption.2. A liberal interpretation of Article 13(B)(a) means that it was very easy for a

wide range of insurance-related services to achieve exemption.3. France – The domestic position of the Tax Authorities was both restrictive and

liberal. Restrictive – only intermediaries allowed by French law to carry out such activities. Liberal – portfolio management services.

4. Germany – Both restrictive and liberal. Restrictive – such back office activities would need to be rendered by an authorised broker or agent to achieve ex-emption. Liberal – no direct contact was needed with the insured (i.e training insurance agents achieved exemption).

5. Luxembourg – Due to the very restrictive approach of the insurance regulatory authorities, the outsourcing, as performed by Andersens, did not in principle exist.

Fina

ncia

l Ser

vice

s VA

T A

lert

Restrictive interpretation

Liberal interpretation

Post-Andersens legislation: Is local legislation expected to change?

Notes1. Austria – Currently the procurement of insurance is exempt and it is not deci-

sive whether the customer can exercise its right against the insurance com-pany or against a third party. These rules are likely to change post-Andersens – amendments to the Austrian Administrative Guidelines.

2. Czech Republic – The legislation is drafted widely and is not specific – but there is no talk of amending this.

3. Hungary – The legislation is expected to be amended in the following month and there may be specific changes following Andersens.

4. Ireland – It is not clear whether domestic legislation will need to be changed (it is already quite similar to Article 13) although inevitably some form of practice notes or guidance will need to be issued by the Tax Authorities.

5. Latvia – Legislation change will depend on the actions of the Insurance Super-visor and the reaction of the Brokers Association.

6. UK – Local legislation is expected to change in respect of services provided by insurance agents. The UK legislation may also require amendments if services such as assistance in the administration and performance of insurance con-tracts and claims handling services are considered not to be essential aspects of the work of an insurance agent.

Fina

ncia

l Ser

vice

s VA

T A

lert

No change

Change – Need to amend legislation