2nd annual clients & friends breakfast sponsored by:this presentation is available for download:

TRANSCRIPT

2nd Annual Clients & Friends Breakfast

Sponsored by: This presentation is available for download:

www.alphabenefits.com/seminar

401(k) Update

Presented by:

Tim MorrisonPresident

Alpha Benefit Administrators

Agenda

Overview of fiduciary responsibility

Minimizing fiduciary liability

Investment policy statement

Due Diligence

Department of labor audits – the real world

Recent Trends

Increased scrutiny of retirement plans due to recent news makers in the economic and business world has

plan sponsors asking: How are we going to protect ourselves and our participants? How can we monitor our investment choices? Where do we invest going forward?

Focus on the actions of fiduciaries, particularly in the area of investment

Who is a Fiduciary?

Under ERISA, a person is a fiduciary to a plan to the extent they:

Exercise any discretionary authority of discretionary control respecting management of such a plan or exercise any authority or control respecting management or disposition of plan assets… Render investment advice for a fee or other compensation with respect to plan assets… Have any discretionary authority or responsibility in the administration of such plan.

Who is a Fiduciary?

Persons who are commonly fiduciaries include: Plan Sponsors

Plan Administrators as defined in ERISA

Trustees

Investment Managers

What Defines a Fiduciary?

Individuals who have, at any time, exercised authority over what investments should be offered under a plan

Sports analogy: You have to know what game is being played.

You have to know the rules and how to keep score.

You have to know what the score is at all times.

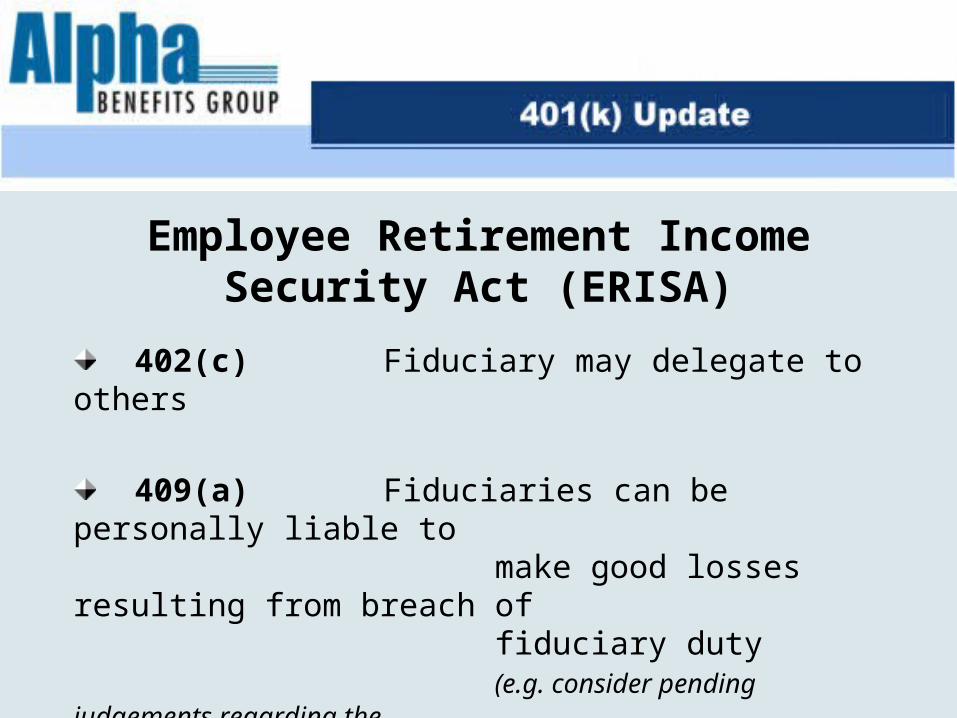

Employee Retirement Income Security Act (ERISA)

402(c) Fiduciary may delegate to others

409(a) Fiduciaries can be personally liable to make good losses resulting from breach of fiduciary duty (e.g. consider pending judgements regarding the Enron scandal)

Fiduciary Duties and Obligations:Common Steps to Follow

Execute responsibilities with care, skill, prudence, and

diligence of a prudent expert

Make decisions solely in the interest of plan participants and beneficiaries

Prudently diversify investments

Avoid engaging in prohibited transactions

Follow the plan documents

Fiduciaries and Plan Assets

Fiduciary must be covered by a fidelity bond to help protect plan’s assets from fraudulent activity (ERISA requirement)

Coverage must be at least 10% of plan assets Minimum $1,000

Generally up to a maximum of $500,000

Bond helps protect the plan’s assets, NOT the fiduciary

Individual fiduciaries have the choice to purchase fiduciary liability insurance.

Ways to Help Minimize Fiduciary Liability for Plan Investments

Adopt and adhere to an Investment Policy Statement

Control total costs and fees of the plan

Promote appropriate diversification of the funds

Exercise due diligence when executing duties

Document, in writing, your actions and decisions

Implement ERISA 404(c) procedures

Monitor investment funds for performance and adhere to investment objectives and policies

Steps to Help Minimize Financial Liability

Offer plan participants option of daily account changes

Offer appropriate fund menu for employee demographics

Fully document reasons for change in investment advisiors

Craft a strategic investment strategy (i.e., Investment Policy Statement (IPS)) explaining the plan’s objectives and distribute it to participants

Steps to Help Minimize Financial Liability (continued)

Avoid “doubletalk” or technical jargon in IPS

Get a second look from an independent broker to review current plan investments/fees to see if competitive in marketplace and document these findings along with annual review processes

Consider asking a select group of employees/plan participants to be involved with the plan’s fund selection processes

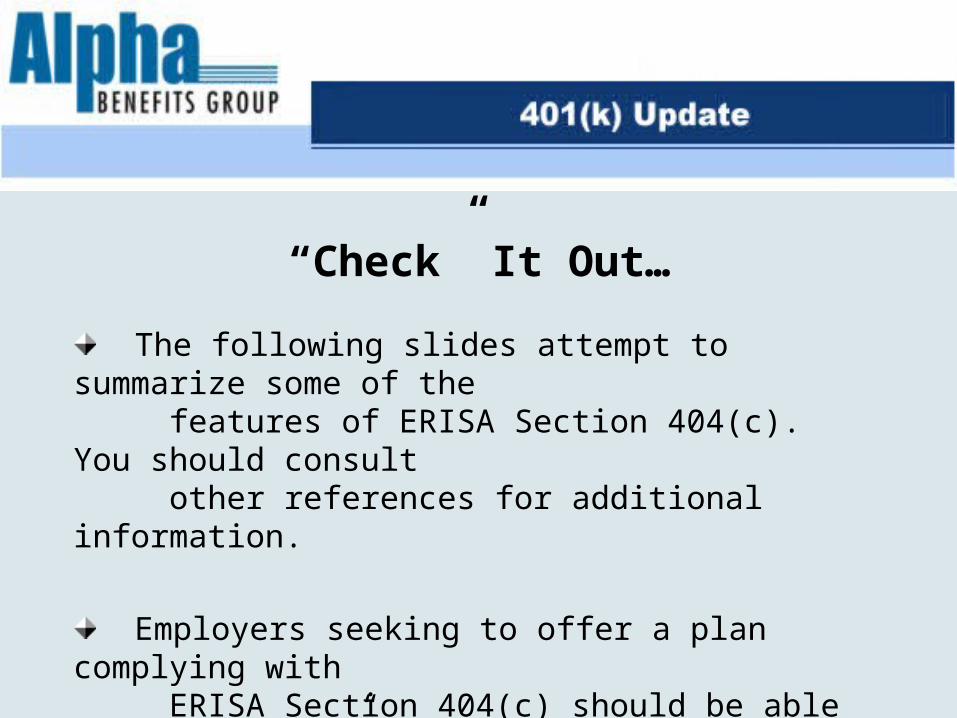

“Check” It Out…

The following slides attempt to summarize some of the

features of ERISA Section 404(c). You should consult

other references for additional information.

Employers seeking to offer a plan complying with ERISA Section 404(c) should be able to answer “yes” to all of the following questions…

Choosing Investments

Are at least three investment choices provided, each with materially different risk/return characteristics?

Can participants choose their own investments?

Can each investment option be classified as a “prudent” investment?

Can participants change their investment allocations and transfer among investment accounts at least once every calendar quarter?

Have Participants Been Provided With…

A statement that the plan intends to comply with ERISA Section 404(c) regulations?

Descriptions of each investment option, including:

Directions on how to select investments and change investment selections along with access to:

Prospectuses?

Periodic account statements?

Objective Asset diversification Performance Sales charges

Risk/return characteristics Plan fiduciary identification Identity of the portfolio manager

What About Fees?

ERISA does not set a specific level of fees, but requires fees charged to a plan be “reasonable”

“Reasonable” must be determined in each case

Ongoing due diligence is critical

401(k) Plan Fee Disclosure Form

(www.dol.gov/ebsa/publications)

Website URL may change. URL referenced above is valid as of 12/04.

Watch Out for Hidden Fees

A 1% increase in fees on a $100,000 investment can reduce a portfolio’s gain

by $66,254 over 20 years, assuming a 7% return.

When Evaluating Fees…

Make informed decisions

Remember fees are just one of several factors

Assess the plan’s performance over time for each investment option

Look at the full value of services

Consider all plan fees because it is not only about fund expenses

Choosing lower fees doesn’t necessarily mean a better performing fund

When Evaluating Fees… (continued)

Compare all services received with total cost

Remember that some investments, due to their nature, may have higher fees

Ask which services the fees cover

Find out which fees are charged directly to the plan or to the employer, and which ones are deducted from investment returns

What is an Investment Policy Statement (IPS)?

Defines how investments and managers are selected, monitored, and evaluated

Describes how investment decisions are related to a plan’s objectives, as well as the strategic vision for the

investments

What Should an IPS Do?

Reflect the employer’s attitudes and philosophy

Recognize the participants’ needs, circumstances and

goals

Document the plan’s goals and demonstrate the foundation for investment decisions

Address the quantity and quality of funds provided and determine the benchmarks and selection criteria

How much discretion will the sponsor have in the final fund selection

What Should an IPS Do?(continued)

Provide a policy method to objectively evaluate fund managers

Help prudently manage plan assets and conduct due diligence

Provide continuity in decision-making as fiduciaries change

Key IPS Components for 401(k) Plans

Describe the purpose of the plan

State the document’s purpose

Identify the duties of each party involved

Explain plan’s investment philosophy

Identify asset classes being offered

Establish criterion for manager selection

Describe monitoring methodology and frequency

Describe methods for replacing or adding funds

Procedural Due Diligence

Analyze investment documents

Review investment compatibility with the IPS

Review historical performance

Evaluate reasonableness of fees

Obtain competitive bids

Establish review schedule and procedures

Document each step along the way

Time consuming

Department of Labor (DOL)Audit Cases (The Real World)

“A pure heart and an empty head are not enough to defend against a fiduciary breach.”

- ERISA Cliché

Source: Tess J. Ferrera, Esq., Kilpatrick Stockton, LLP. “What Third Party Administrators Should KnowAbout ERISA Liability and Department of Labor Investigations”, Donovan v. Cunningham, 716 F.2d 1455 (5th Cir. 1983), cert denied, 467 U.S. 1251 (1984).

Update on the Health Insurance Market

Presented by:

Todd HonsVice President

Alpha Benefits Group

High Deductible Options

Health Savings Accounts (HSA’s)

Health Reimbursment Arrangements (HRA’s)

Medical Expense Reimbursement Accounts (MERP’s)

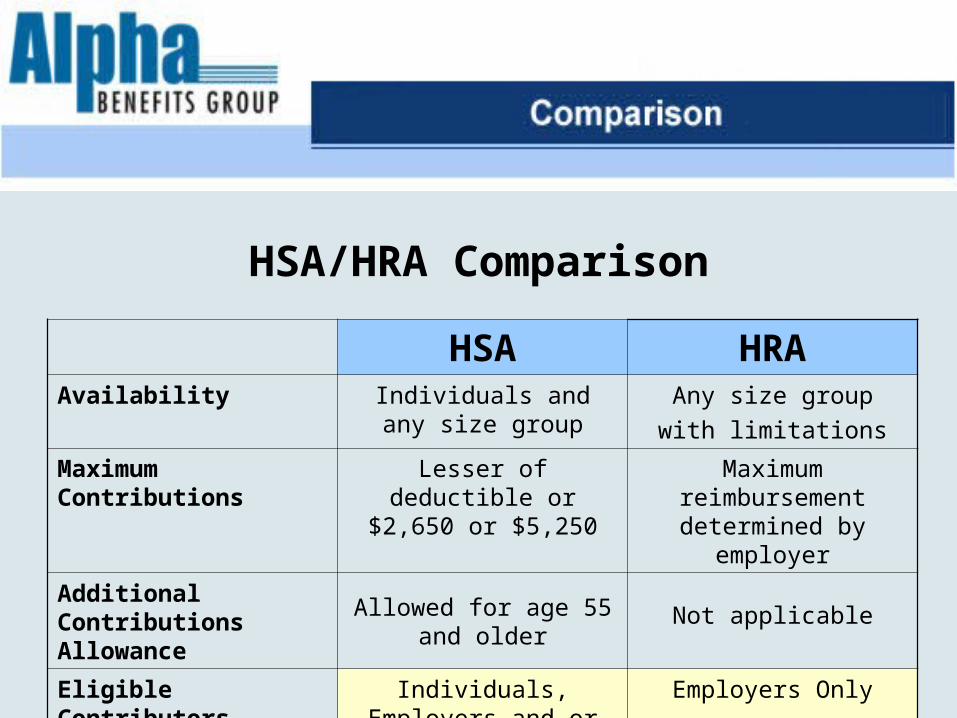

HSA/HRA Comparison

HSA HRAAvailability Individuals and any size

groupAny size group

with limitations

Maximum Contributions

Lesser of deductible or $2,650 or $5,250

Maximum reimbursement determined by employer

Additional Contributions Allowance

Allowed for age 55 and older

Not applicable

Eligible Contributors Individuals, Employers and or Employees

Employers Only

HSA HRATax Deductibility – Employer

Contributions are tax deductible

Reimbursements are tax deductible

Tax Deductibility – Employee

Contributions are pre-tax if offered through a

cafeteria planNot Applicable

Fund or Account Ownership

Employee Employer

Portable Yes No

Rollover of Funds Yes Employer determines if allowed and can set caps

Funding Required Yes No

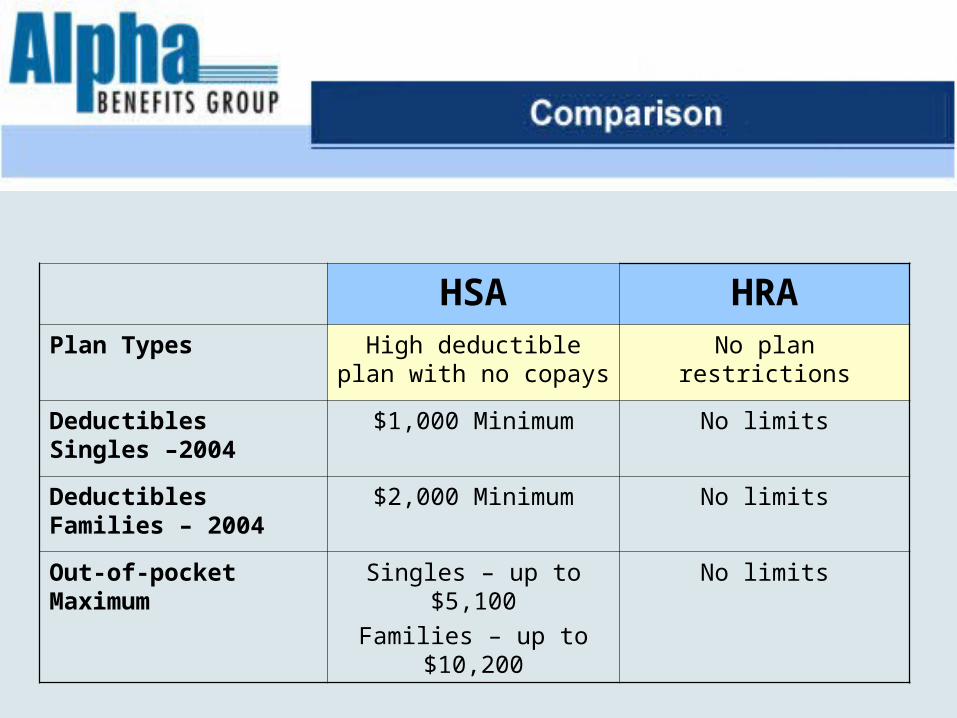

HSA HRAPlan Types High deductible plan with

no copaysNo plan restrictions

Deductibles Singles –2004

$1,000 Minimum No limits

Deductibles Families – 2004

$2,000 Minimum No limits

Out-of-pocket Maximum

Singles – up to $5,100

Families – up to $10,200

No limits

High Deductible PlansOn paper, they make sense.

Larger employee out of pocket reduces employer cost

Turns employee into consumer

Employees that utilize medical plan pay more

Isn’t insurance designed to pay for catastrophic?

Why Haven’t HRA’s/HSA’s Taken Off?

Major insurance carriers slow to adopt plan design

Not enough of a discount in rates

Employee communication issues

Confusion over regulations

Employers view this as just a “cost shifting” method as opposed to a way to reduce overall costs

Some Areas of Confusion

Not enough money in account early on

Make sure to receive carrier discount at time of service

Paying for non-medical expenses through HSA accounts

High Deductibles Plans

Carriers now offering a full complementof HSA/HRA’s. Most are available effective

January 1, 2005.

Medical Expense Reimbursement Plans (MERP)

Stepping stone to HSA’s?

Medical Expense Reimbursement Plans (MERP)

Governed by IRC Section 105

Utilized with an insurance carrier’s high deductible plan

Permits employers to self-insure certain medical expense costs

Strategy Employer secures high deductible plan (i.e. $2,000) for major

expenses (In/Out patient surgery, etc.) from carrier

Generally less than 20% of employees utilize these type of expenses

Communicate lower deductible (i.e. $250) to employees

Employer self insures from $250 to $2,000, only if actually incurred

Employer utilizes premium discount savings to fund the self insured portion

Typically part of PPO plan with office visit co-pay and drug card

Insured Claims Experience

80% of insureds have claims < $3,000

70% of insureds have claims < $2,000

55% of insureds have claims < $1,000

Milliman USA (2002)

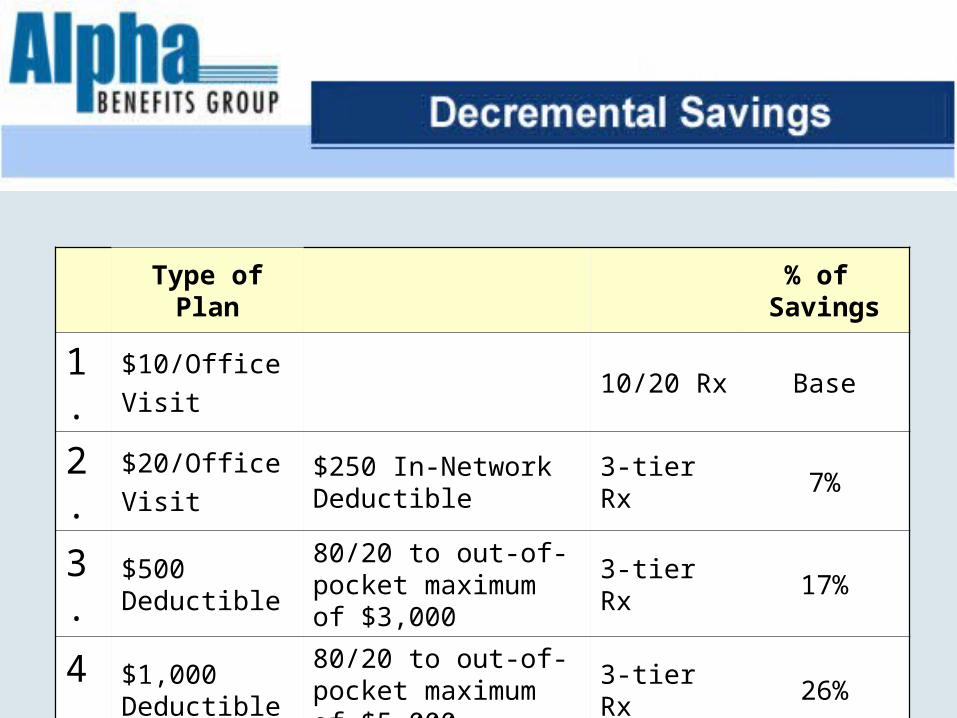

Type of Plan% of

Savings

1.$10/Office

Visit10/20 Rx Base

2.$20/Office

Visit$250 In-Network Deductible

3-tier Rx 7%

3. $500 Deductible

80/20 to out-of-pocket maximum of $3,000

3-tier Rx 17%

4. $1,000 Deductible

80/20 to out-of-pocket maximum of $5,000

3-tier Rx 26%

Additional Points

Alpha Benefit Administrators administers the self funded portion for the employer

Advantage over HSA in that employee can retain the doctor visit copays and Rx copay card while still having PPO arrangement for service

All expenses over the $2,000 are the responsibility of the insurance carrier

Additional Points

Serves as a starting point for getting into high deductible plans without having to communicate a complicated process to employees

Alpha Benefits Administrators can provide proposal on

savings and costs

Carrier Update Aetna

Reading Hospital

Oxford/United Healthcare/Mamsi

HealthAmerica and HealthAssurance Dr’s St. Lukes

Gnadden Hutten/Palmerton Hospital 1/1/2005

Capital BlueCross/Keystone Demographic under 45 employees 1/1/2005

Integration Keystone/Cross

New PPO Plan Designs

Carrier Update HealthGuard

Ending 12/31/2005

Highmark New PPO plan designs

Calendar Year Deductibles

Company Plan Year Calendar Year

HighmarkNew Business – 1/1/05

Renewals – Upon Renewal

HealthAmerica 10/1/2004

Capital BlueCross

Thank you for attending!

This presentation is available for download at:

www.alphabenefits.com/seminar