2nd paper (3)

DESCRIPTION

2nd paper (3)TRANSCRIPT

Financial Accounting and Reporting

Unit 10-02

Nicolas, Resalyn Cae S.

2nd year Finance

Mr. Mark Anthony R. Casanova

Assessor

11 December 2013

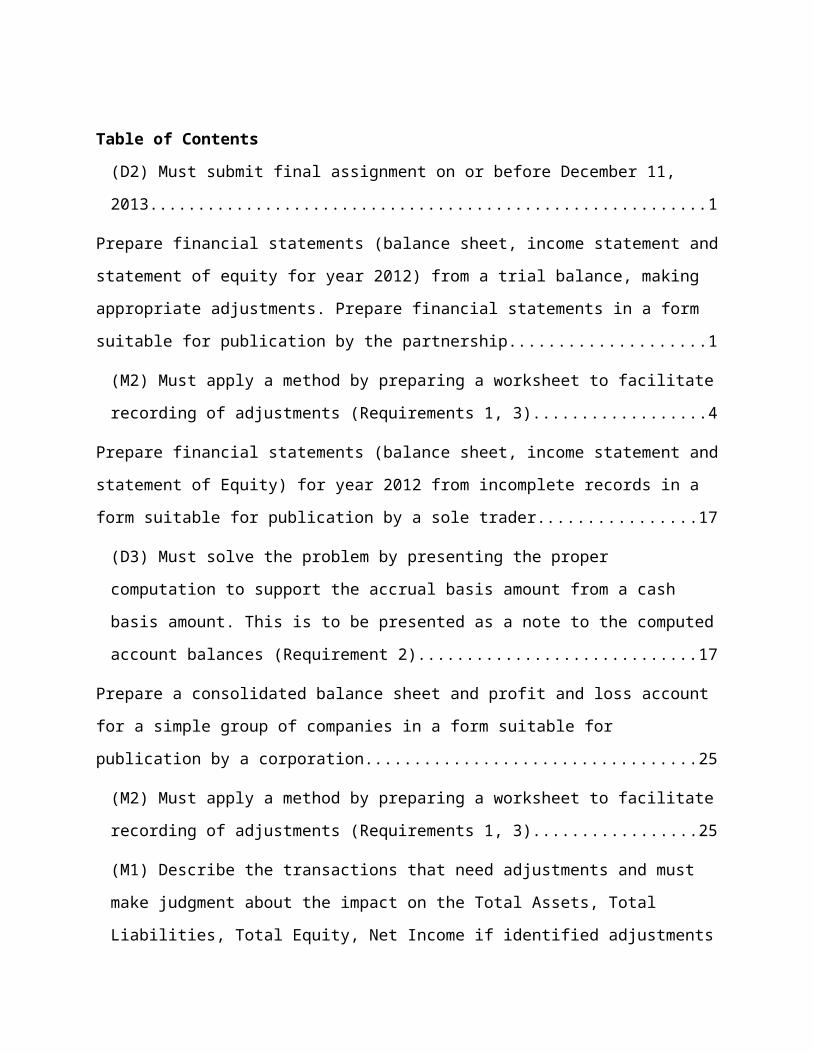

Table of Contents(D2) Must submit final assignment on or before December 11, 2013...........................1

Prepare financial statements (balance sheet, income statement and statement of equity

for year 2012) from a trial balance, making appropriate adjustments. Prepare financial

statements in a form suitable for publication by the partnership......................................1

(M2) Must apply a method by preparing a worksheet to facilitate recording of

adjustments (Requirements 1, 3)..................................................................................4

Prepare financial statements (balance sheet, income statement and statement of

Equity) for year 2012 from incomplete records in a form suitable for publication by a sole

trader..............................................................................................................................17

(D3) Must solve the problem by presenting the proper computation to support the

accrual basis amount from a cash basis amount. This is to be presented as a note to

the computed account balances (Requirement 2)......................................................17

Prepare a consolidated balance sheet and profit and loss account for a simple group of

companies in a form suitable for publication by a corporation.......................................25

(M2) Must apply a method by preparing a worksheet to facilitate recording of

adjustments (Requirements 1, 3)................................................................................25

(M1) Describe the transactions that need adjustments and must make judgment about

the impact on the Total Assets, Total Liabilities, Total Equity, Net Income if identified

adjustments for the year ended December 31, 2012 are not recorded. (Requirement

1).................................................................................................................................30

(D1) Must draw a conclusion about the accumulated misstatement in the income

statement if materiality level is 5% of Net Income before tax. (Requirement 1)..........39

Appendix..........................................................................................................................A

(M3) Must show that an appropriate and structured approach in the preparation of

report has been used. The report presented in powerpoint should cover the nature of

adjustments and a summary of adjustments. (Requirement 1)....................................A

3

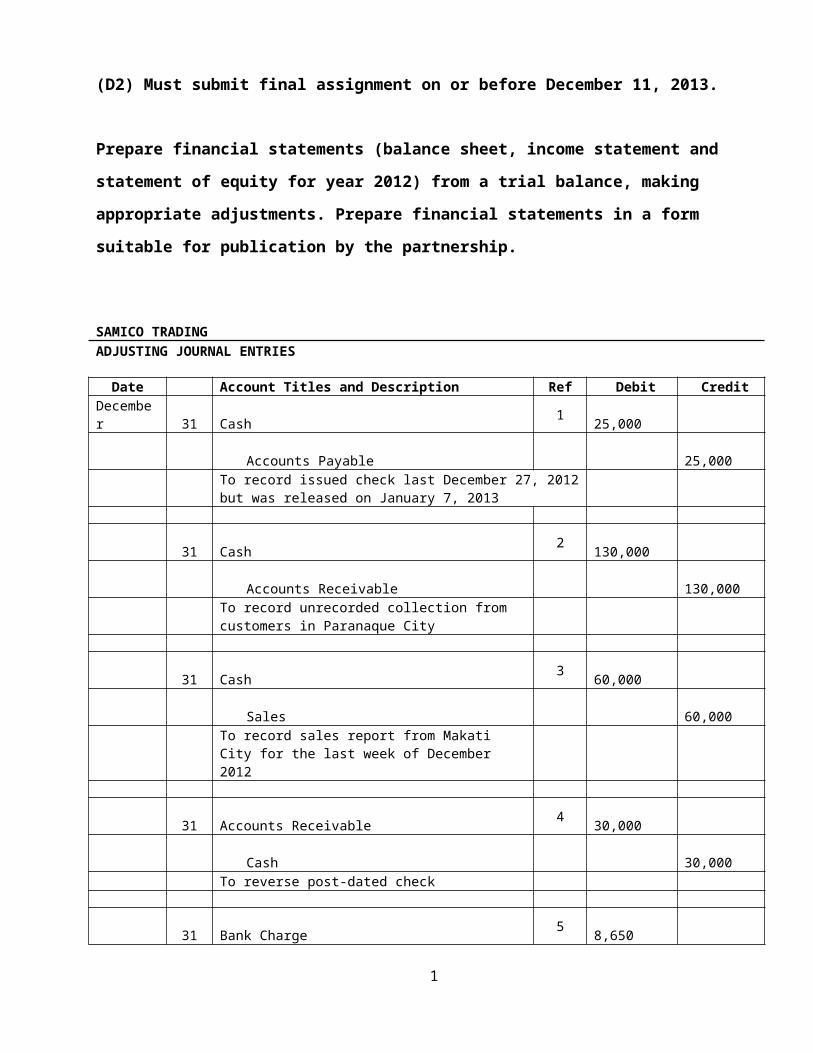

(D2) Must submit final assignment on or before December 11, 2013.

Prepare financial statements (balance sheet, income statement and statement of equity for year 2012) from a trial balance, making appropriate adjustments. Prepare financial statements in a form suitable for publication by the partnership.

SAMICO TRADINGADJUSTING JOURNAL ENTRIES

Date Account Titles and Description Ref Debit CreditDecember 31 Cash 1

25,000

Accounts Payable 25,000

To record issued check last December 27, 2012 but was released on January 7, 2013

31 Cash 2 130,000

Accounts Receivable 130,000

To record unrecorded collection from customers in Paranaque City

31 Cash 3 60,000

Sales 60,000

To record sales report from Makati City for the last week of December 2012

31 Accounts Receivable 4 30,000

Cash 30,000

To reverse post-dated check

31 Bank Charge 5 8,650

Cash 8,650

To record adjustments from bank charge

31 Cash 6 5,000

Other Income 5,000

1

To record other income earned on December 30, 2012

31 Allowance for Doubtful Accounts 7 115,000

Accounts Receivable 115,000

To record allowance for doubtful accounts

31 Doubtful Accounts Expense 8 66,970

Allowance for Doubtful Accounts 66,970

To record provisions on aging receivables

31 Interest Receivable 9 64,000

Interest Income 64,000

To record interest income from a note value dated Oct. 28 which earns interest at 12% to Hi5 Company

31 Ending Inventory 10 2,257,000

Cost of Goods Sold 27,545,000

Beginning Inventory 3,302,000

Purchases

26,500,000

To record the inventory on hand as of December 31, 2012

31 Ending Inventory 11 250,000

Cost of Goods Sold 250,000

To record year-end inventory not included in the count

31 Purchases 12 125,000

Accounts Payable 125,000

Cost of Goods Sold 125,000

Purchases 125,000

To record related invoice of goods received from a vendor on December 25, 2013

2

31 Insurance Expense 13 71,250

Prepayments 71,250

To record monthly prepayments used for car and office insurance

31 Office Supplies Expense 14 20,400

Prepayments 20,400

To record the correct count of office supplies as of year-end

31 Rent Expense 15 300,000

Prepayments 300,000

To record monthly prepayments used for rent expense

31Accumulated Depreciation - Furniture and Fixtures 16

4,000Depreciation Expense - Furniture and

Fixtures 4,000

To correct excess in depreciation expense

31 Transportation Equipment 17 500,000

Office Equipment 225,000

Mico, Capital 362,500

Sam, Capital 362,500

To record cash purchase of vehicle and five desktops from the additional investment by the partners

31 Depreciation Expense 18 82,917

Accumulated Depreciation - Transportation Equipment

41,667

To record depreciation expense of transportation equipments

31 Depreciation Expense 19 Accumulated Depreciation - Office Equipment

41,250

To record depreciation expense of office equipments

31 Accounts Payable 20 120,000

3

Other Income 30,000

Unearned Revenue 90,000

To record received cash on October 1, 2012 from the launched promo service and recognize income for 3 months

31 Telephone Expense 21 61,650

Salaries 154,250

Accrued Expenses 215,900

To record accrued expenses

Total

32,346,087

32,346,087

4

(M2) Must apply a method by preparing a worksheet to facilitate recording of adjustments (Requirements 1, 3)

SAMICO TradingWorksheet

December 31, 2012In Pesos

Unadjusted Adjustments AdjustedDebit Credit Debit Credit Debit Credit

Cash 4,041,556

1

25,000

4,222,906

2

130,000

3

60,000

4

30,000

5

8,650

6

5,000

Accounts Receivable - trade

3,280,000

2

130,000

3,065,000

4

30,000

7

115,000

Allowance for doubtful accounts

126,000

7

115,000

77,970

8

66,970

Interest Receivable 9

64,000

64,000

Notes Receivable 3,000,000

3,000,000

Inventories 3,302,000

10

2,257,000

2,507,000

10

3,302,000

11

250,000

Prepayments 726,000

13

71,250

334,350

2

5

14 0,400 15

300,000

Office Equipment 1,500,000

17

225,000

1,725,000

Transportation Equipment 2,800,000

17

500,000

3,300,000

Furniture and Fixtures 1,200,000

1,200,000

Accumulated Depreciation - Office Equipment

900,000

19

41,250

941,250

Accumulated Depreciation - Transportation Equipment

1,400,00

0

18

41,667

1,441,667

Accumulated Depreciation - Furniture and Fixtures

644,000

16

4,000

640,000

Accounts Payable

2,075,36

2 1 2

5,000 2,10

5,362 12

125,000

20

120,000

Unearned Revenue

20

90,000

90,000

Other Current Liabilities

351,000 35

1,000

Accrued Expenses

21

215,900

215,900

Capital, Mico Montenegro

6,000,00

0

17

362,500

6,362,500

Capital, Sam Westen

6,000,00

0

17

362,500

6,362,500

Drawings, Mico Montenegro

800,000

800,000

Drawings, Sam Westen 800,000

800,000

Sales

35,106,38

8 3 6

0,000 35,16

6,388

Interest Income 9

64,000

64,000

6

Other Income 6

5,000

35,000

20

30,000

Purchases 26,500,000

10

26,500,000

-

12

125,000

12

125,000

Cost of Sales

10

27,545,000

27,420,000

11

250,000

12

125,000

Salaries and Wages 2,173,000

21

154,250

2,327,250

SSS, PHIC, Pagibig

83,130 8

3,130

Taxes and license

62,544 6

2,544

Rent expense 150,000

15

300,000

450,000

Repair and Maintenance 145,000

145,000

Gasoline 124,520

124,520

Light, water & telephone 632,500

21

61,650

694,150

Representation and Entertainment

33,500

33,500

Depreciation Expense 1,104,000

19

41,250

1,182,917

18

41,667

16

4,000

Office Supplies Expense 110,000

1

20,400

130,400

7

4

Bank Charge 5

8,650

8,650

Doubtful Accounts Expense

8

66,970

66,970

Insurance Expense

13

71,250

71,250

Miscellaneous Expense

35,000 3

5,000

Total 52

,602,750

52,602,7

50 32,34

6,087 32,34

6,087 53,85

3,537 53,85

3,537

8

SAMICO TradingSTATEMENT OF FINANCIAL POSITIONAs of December 31, 2012

in PhpAssets Notes 2 0 1 2

Current assets

Cash 4,222,906

Trade and other receivables 1

6,051,030

Inventories 2,507,000

Prepayments 334,350

Total current assets 13,115,286

Non-current assetsProperty and equipment

2

3,202,083

Total Non-current assets 3,202,083

Total Assets 16,317,369

Liabilities and Equity

Current LiabilitiesTrade and other payables

3

2,762,262

Total Liabilities 2,762,262

EquityTotal Partners' Equity

4

13,555,107

Total Liabilities and Partners' Equity

16,317,369

See Accompanying Notes to Financial Statements

-

9

SAMICO TRADINGSTATEMENT OF INCOMEFOR THE YEAR ENDED DECEMBER 31, 2012

Notes in Php2 0 1 2

Revenue 4 35,265,388

Cost of Goods Sold 5 27,420,000

Gross Profit 7,845,388

Less: Operating Expenses 6 5,415,281

Net Income 2,430,107

See Accompanying Notes to Financial Statements

10

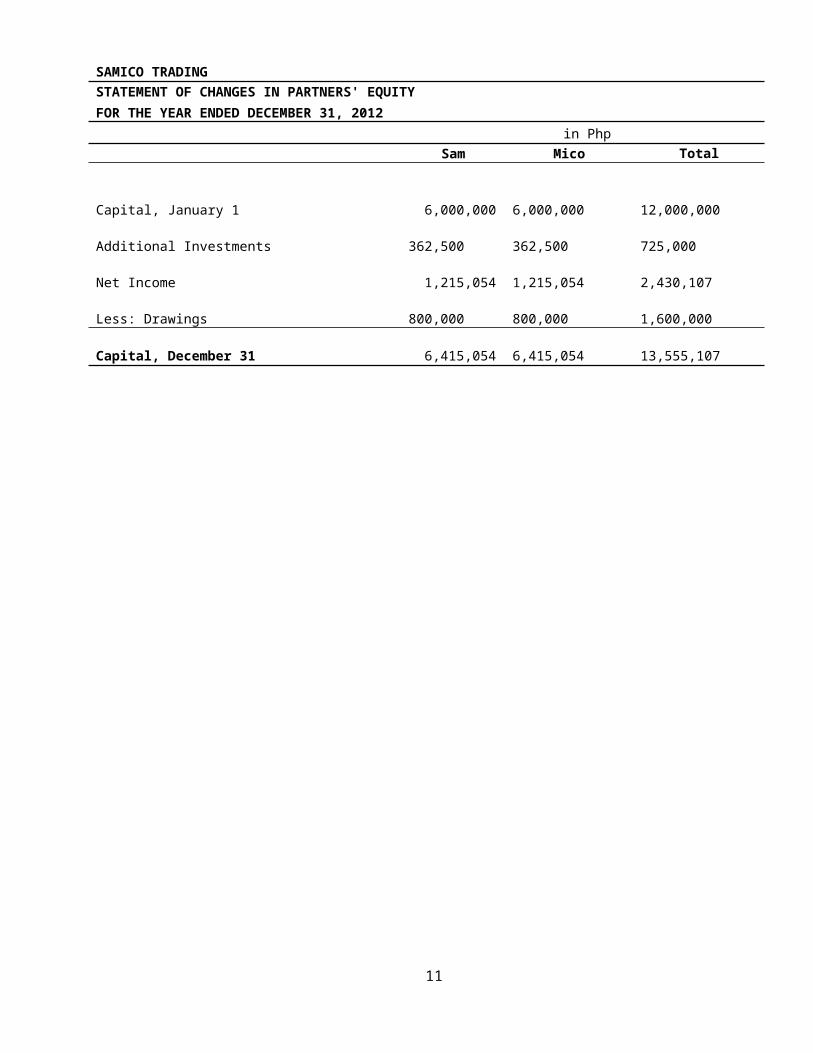

SAMICO TRADINGSTATEMENT OF CHANGES IN PARTNERS' EQUITYFOR THE YEAR ENDED DECEMBER 31, 2012

in PhpSam Mico Total

Capital, January 1 6,000,000 6,000,000 12,000,000Additional Investments 362,500 362,500 725,000Net Income 1,215,054 1,215,054 2,430,107Less: Drawings 800,000 800,000 1,600,000Capital, December 31 6,415,054 6,415,054 13,555,107

11

SAMICO TradingNotes to Financial StatementsAS OF AND FOR THE YEAR ENDED DECEMBER 31, 2012

1. TRADE AND OTHER RECEIVABLESThis content consist of: in Php

2012

Accounts Receivable - trade 3,065,00

0

Less: Allowance for doubtful accounts 77,97

0

Notes Receivable 3,000,00

0

Interest Receivable 64,00

0 6,051,03

0

2. PROPERTY AND EQUIPMENTThis content consist of: in Php

2012

Office Equipment 1,725,00

0

Transportation Equipment 3,300,00

0

Furniture and Fixtures 1,200,00

0 Less:

Accumulated Depreciation - Office Equipment 941,25

0

Accumulated Depreciation - Transportation Equipment 1,441,66

7

Accumulated Depreciation - Furniture and Fixtures 640,00

0 3,202,08

3

3. TRADE AND OTHER PAYABLESThis account consist of: in Php

2012

Accounts Payable 2,105,36

2

Unearned Revenue 90,00

0

Accrued Revenue 215,90

0

Other Current Liabilities 351,00

0 2,762,26

2

4. EQUITY

12

This content consist of: in Php2012

Capital, January 1 12,000,00

0

Additional Investments 725,00

0

Net Income 2,430,10

7

Less: Drawings 1,600,00

0 13,555,10

7

5. REVENUEThis account consist of: in Php

2012

Sales 35,166,38

8

Interest Income 64,00

0

Other Income 35,00

0 35,265,38

8

6. COST OF GOODS SOLDThis account consist of: in Php

2012

Beginning Inventory 3,302,000

Purchases 26,625,000

Total Goods Available for Sale 29,927,000

Less: Ending Inventory 2,507,000 27,420,000

7. OPERATING EXPENSESThis account consist of: in Php

2012

Salaries and Wages 2,327,250

Depreciation Expense 1,182,917

Light, water & telephone 694,150

Rent expense 450,000

Repair and Maintenance

13

145,000

Office Supplies Expense 130,400

Gasoline 124,520

SSS, PHIC, Pagibig 83,130

Insurance Expense 66,970

Doubtful Accounts Expenses 130,400

Taxes and license 62,544

Representation and Entertainment 33,500

Bank Charge 8,650

Miscellaneous Expense 35,000 5,474,431

14

SAMICO TRADINGSTATEMENT OF FINANCIAL POSITION (UNADJUSTED)AS OF DECEMBER 31, 2012

in Php

Assets Note

s 2012

Current assetsCash 4,041,556Trade and other receivables 1 6,154,000Inventories 3,302,000Prepayments 726,000

Total current assets 14,223,556

Non-current assetsProperty and equipment 2 2,556,000

Total Non-current assets 2,556,000

Total Assets 16,779,556

Liabilities and Equity

Current LiabilitiesTrade and other payables 3 2,426,362

Total current liabilities 2,426,362Total Liabilities 2,426,362

EquityTotal Partners' Equity 14,353,194

Total Liabilities and Partners' Equity 16,779,556

See Accompanying Notes to Financial Statements -

15

SAMICO TRADING STATEMENT OF INCOME (UNADJUSTED) FOR THE YEAR ENDED DECEMBER 31, 2012

in Php Notes 2012

Revenue 4 35,106,388 Cost of Goods Sold 5 26,500,000 Gross Profit 8,606,388 Less: Operating Expenses 6 4,653,194 Net Income 3,953,194

See Accompanying Notes to Financial Statements

16

SAMICO TRADINGSTATEMENT OF CHANGES IN EQUITY (UNADJUSTED)FOR THE YEAR ENDED DECEMBER 31, 2012

in Php2 0 1 2

Sam Mico TotalCapital, January 1, 2012 6,000,000 6,000,000 12,000,000Net Income 1,976,597 1,976,597 3,953,194Less: Drawing 800,000 800,000 1,600,000Total Partners' Equity 7,176,597 7,176,597 14,353,194

17

SAMICO TradingNotes to Financial Statements (Unadjusted)AS OF AND FOR THE YEAR ENDED DECEMBER 31, 2012

1. TRADE AND OTHER RECEIVABLESThis account consist of: in Php

2012

Accounts Receivable - trade 3,280,00

0

Less: Allowance for doubtful accounts 126,00

0

Notes Receivable 3,000,00

0 6,154,00

0

2. PROPERTY AND EQUIPMENTThis account consist of: in Php

2012

Office Equipment 1,500,00

0

Transportation Equipment 2,800,00

0

Furniture and Fixtures 1,200,00

0 Less:

Accumulated Depreciation - Office Equipment 900,00

0

Accumulated Depreciation - Transportation Equipment 1,400,00

0

Accumulated Depreciation - Furniture and Fixtures 644,00

0 2,556,00

0

3. TRADE AND OTHER PAYABLESThis account consist of: in Php

2012

Accounts Payable 2,075,36

2

Other Current Liabilities 351,00

0 2,426,36

2

4. REVENUEThis account consist of: in Php

2012

Sales 35,106,38

8 35,106,38

18

8

5. COST OF GOODS SOLDThis account consist of: in Php

2012

Beginning Inventory 3,302,00

0

Purchases 26,500,00

0

Less: Ending Inventory 3,302,00

0 26,500,00

0

6. OPERATING EXPENSESThis account consist of: in Php

2012

Salaries and Wages 2,173,00

0

Depreciation Expense 1,104,00

0

Light, water & telephone 632,50

0

Rent expense 150,00

0

Repair and Maintenance 145,00

0

Gasoline 124,52

0

Office Supplies Expense 110,00

0

SSS, PHIC, Pagibig 83,13

0

Taxes and license 62,54

4

Representation and Entertainment 33,50

0

Miscellaneous Expense 35,00

0 4,653,19

4

19

Prepare financial statements (balance sheet, income statement and statement of Equity) for year 2012 from incomplete records in a form suitable for publication by a sole trader.

(D3) Must solve the problem by presenting the proper computation to support the accrual basis amount from a cash basis amount. This is to be presented as a note to the computed account balances (Requirement 2)

BRUNO EARTH TRADINGSCHEDULE OF COMPUTATIONS

Computation for Net Income

Beginning Capital 498,165.00Add: Net Income 140,385.00Less: Drawing 168,000.00Ending Capital 470,550.00

Schedule 1: Computation of Gross SalesCash Sales 369,000.00Sales on Account Accounts Receivable, December 31 96,000.00 Notes Receivable, December 31 15,000.00 Collection on Accounts Receivable 468,750.00 Collection on Notes Receivables 52,500.00

20

Sales Discount 2,250.00 Accounts Written-Off 600.00 Total 635,100.00 Accounts Receivable, January 1 129,000.00 Notes Receivable, January 1 30,000.00 476,100.00Total Sales 845,100.00

Schedule 2: Computation of Gross PurchasesCash Purchases 228,750.00Purchase on Account Accounts Payable, December 31 96,000.00 Notes Payable, December 31 18,000.00 Payment on Accounts Payable 346,650.00 Payment on Notes Payable 45,000.00 Purchase Discount Taken 1,500.00 Purchase Returns 1,050.00 Total 508,200.00 Accounts Payable, January 1 87,000.00 Notes Payable, January 1 13,500.00 407,700.00Total Purchases 636,450.00

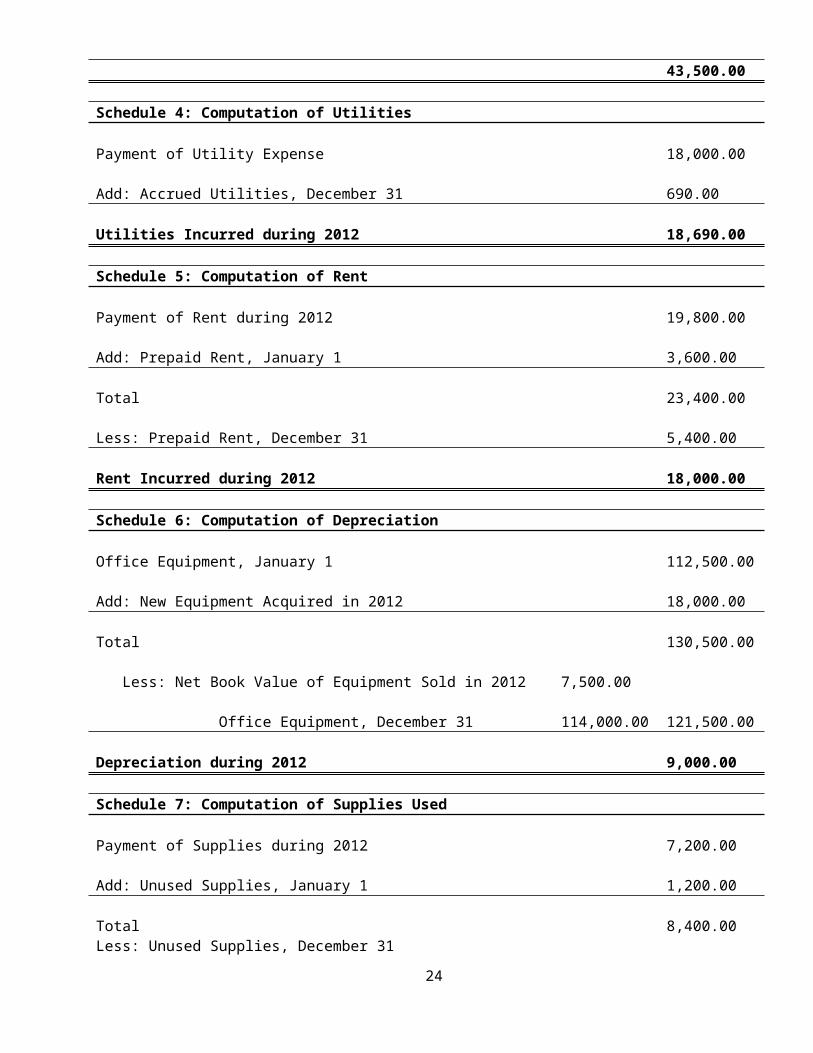

Schedule 3: Computation of TaxesPayment of Taxes during 2012 40,500.00Add: Accrued Taxes, December 31 21,000.00Total 61,500.00Less: Accrued Taxes, January 1 18,000.00Taxes Incurred during 2012 43,500.00

Schedule 4: Computation of UtilitiesPayment of Utility Expense 18,000.00Add: Accrued Utilities, December 31 690.00Utilities Incurred during 2012 18,690.00

Schedule 5: Computation of RentPayment of Rent during 2012 19,800.00Add: Prepaid Rent, January 1 3,600.00Total 23,400.00Less: Prepaid Rent, December 31 5,400.00Rent Incurred during 2012 18,000.00

Schedule 6: Computation of DepreciationOffice Equipment, January 1 112,500.00Add: New Equipment Acquired in 2012 18,000.00Total 130,500.00

21

Less: Net Book Value of Equipment Sold in 2012 7,500.00 Office Equipment, December 31 114,000.00 121,500.00Depreciation during 2012 9,000.00

Schedule 7: Computation of Supplies UsedPayment of Supplies during 2012 7,200.00Add: Unused Supplies, January 1 1,200.00Total 8,400.00Less: Unused Supplies, December 31 1,800.00Supplies Used 6,600.00

Schedule 8: Computation of Commission RevenueReceipt of commission Revenue during 2012 48,000.00Add: Accrued Commission Revenue, December 31 2,250.00Total 50,250.00Less: Accrued Commission Revenue, January 1 3,150.00Commission Revenue Earned during 2012 47,100.00

Schedule 9: Computation of Interest RevenueReceipt of Interest Revenue during 2012 375.00Add: Unearned Interest Revenue, January 1 150.00Total 525.00Less: Unearned Interest Revenue, December 31 75.00Interest Revenue Earned during 2012 450.00

Schedule 10: Computation of Interest ExpensePayment of Interest Expense in 2012 750.00Add: Accrued Interest 360.00Total 1,110.00Less: Accrued Interest Expense, January 1 135.00Interest Expense Incurred during 2012 975.00

Schedule 11: Computation of Loss on Sale of EquipmentOriginal Cost of the Equipment Sold 15,000.00Less: Accumulated Depreciation as of the Date of Sale 7,500.00Net Book Value as of the Date of Sale 7,500.00Less: Proceeds from Sale of Equipment 6,750.00Loss on Sale of Equipment 750.00

22

BRUNO EARTH TRADINGSTATEMENT OF FINANCIAL POSITIONAS OF DECEMBER 31, 2012

in PhpAssets Notes 2 0 1 2

Current assets Cash

1

99,225 113,250 273,000 7,200

Trade and other receivables

Inventories Prepayments

Total current assets 492,675

Non-current assets

Property and equipment

2 114,000

Total Non-current assets 114,000

Total Assets 606,675

Liabilities and Equity

Current Liabilities

Trade and other payables

3 136,125

Total current liabilities 136,125

Total Liabilities 136,125

Equity

Total Stockholders' Equity

4 470,550

Total Liabilities and Stockholders' Equity 606,675

See Accompanying Notes to Financial Statements

23

BRUNO EARTH TRADINGSTATEMENT OF INCOMEFOR THE YEAR ENDED DECEMBER 31, 2012

Notes in Php2 0 1 2

Revenue 4 890,400.00

Cost of Goods Sold 5 590,400.00

Gross Profit 300,000.00

Less: Operating Expenses 6 159,615.00

Net Income 140,385.00

See Accompanying Notes to Financial Statements

24

BRUNO EARTH TRADINGSTATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED DECEMBER 31, 2012

in Php2 0 1 2

Capital, Diego, January 1 498,165.00Net Income 140,385.00Less: Drawings 168,000.00Capital, Diego, December 31 470,550.00

25

BRUNO EARTH TRADINGNotes to Financial StatementsAS OF AND FOR THE YEAR ENDED DECEMBER 31, 2012

1. TRADE AND OTHER RECEIVABLESThis account consist of: Schedule in Php

2012 Accounts Receivable 3,065,000 Notes Receivable 77,970 Accrued Commission Revenue 3,000,000

6,142,970

2. PROPERTY AND EQUIPMENTThis account consist of: in Php

2012 Office Equipment 114,000

114,000

3. TRADE AND OTHER PAYABLESThis account consist of: in Php

2012 Accounts Payable 96,000 Notes Payable 18,000 Accrued Interest Expense 360 Accrued Taxes 21,000 Accrued Utility Expense 690 Unearned Interest Revenue 75

136,125

4. EQUITYThis account consist of: in Php

2012 Diego, Capital, January 1 498,165 Net Income 140,385 Less: Drawings 168,000

470,550

5. REVENUE

26

This account consist of: in Php2012

Sales 1 845,100.00 Less: Sales Discount 2,250.00 Commission Revenue 47,100.00 Interest Revenue 450.00

890,400

6. COST OF GOODS SOLDThis account consist of: in Php

2012 Beginning Inventory 229,500 Purchases 2 636,450 Less: Purchases Discount 1,500 Purchases Returns 1,050 Total Goods Available for Sale 863,400 Less: Ending Inventory 273,000

590,400

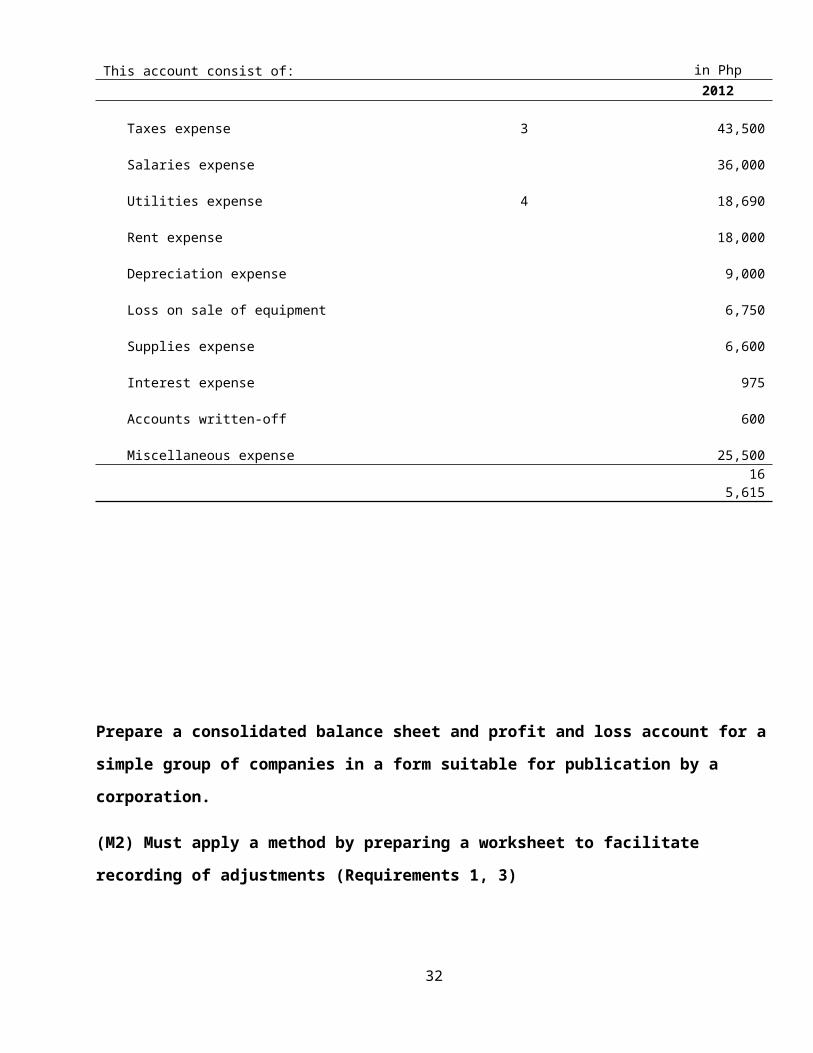

7. OPERATING EXPENSESThis account consist of: in Php

2012 Taxes expense 3 43,500 Salaries expense 36,000

Utilities expense 4 18,690 Rent expense 18,000 Depreciation expense 9,000 Loss on sale of equipment 6,750 Supplies expense 6,600 Interest expense 975 Accounts written-off 600 Miscellaneous expense 25,500

165,615

27

Prepare a consolidated balance sheet and profit and loss account for a simple group of companies in a form suitable for publication by a corporation.

(M2) Must apply a method by preparing a worksheet to facilitate recording of adjustments (Requirements 1, 3)

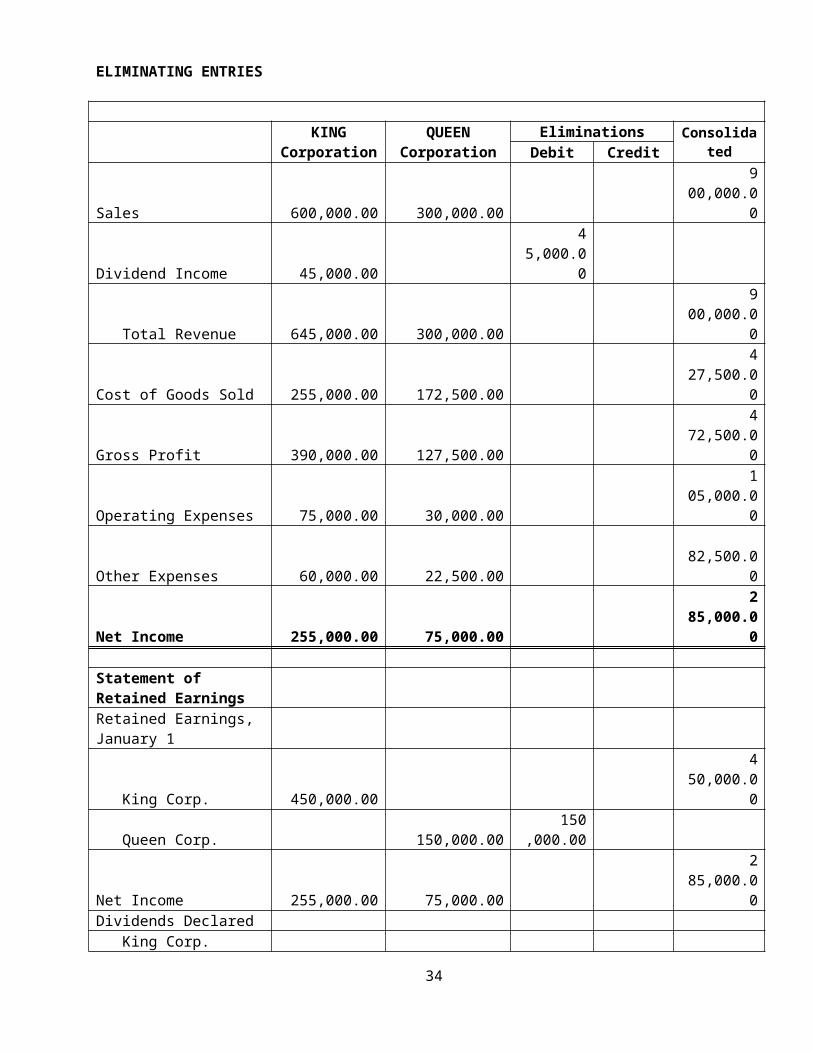

KING CORPORATION AND SUBSIDIARYELIMINATING ENTRIES

KING Corporation

QUEEN Corporation

EliminationsConsolidated

Debit Credit

Sales 600,000.

00 300,000

.00 900,000.

00

Dividend Income 45,000

.00 45,000.

00

Total Revenue 645,000.

00 300,000

.00 900,000.

00

Cost of Goods Sold 255,000.

00 172,500

.00 427,500.

00

Gross Profit 390,000.

00 127,500

.00 472,500.

00

Operating Expenses 75,000

.00 30,000

.00 105,000.

00

Other Expenses 60,000

.00 22,500

.00 82,500.

00

Net Income 255,000.

00 75,000

.00 285,000.

00

Statement of Retained EarningsRetained Earnings, January 1

King Corp. 450,000.

00 450,000.

00

Queen Corp. 150,000

.00 150,000.

00

Net Income 255,000.

00 75,000

.00 285,000.

00Dividends Declared

King Corp. 90,000

.00 90,000.

00

Queen Corp. 45,000

.00 45,000.

00Retained Earnings, 615,000. 180,000 645,000.

28

December 31 00 .00 00

Cash 315,000.

00 112,500

.00 427,500.

00

Accounts Receivable 112,500.

00 75,000

.00 187,500.

00

Inventory 150,000.

00 112,500

.00 262,500.

00Property and Equipment Net

787,500.00

480,000.00

1,267,500.00

Investment in Queen Corp. 450,000.

00 450,000.

00

Total Assets 1,815,000

.00 780,000

.00 2,145,000.

00

Accounts Payable 150,000.

00 150,000

.00 300,000.

00

Loans Payable 300,000.

00 150,000

.00 450,000.

00Common Stock

King Corp. 750,000.

00 750,000.

00

Queen Corp. 300,000

.00 300,000.

00

Retained Earnings 615,000.

00 180,000

.00 645,000.

00

Total Liabilities and Equity 1,815,000

.00 780,000

.00 2,145,000.

00

29

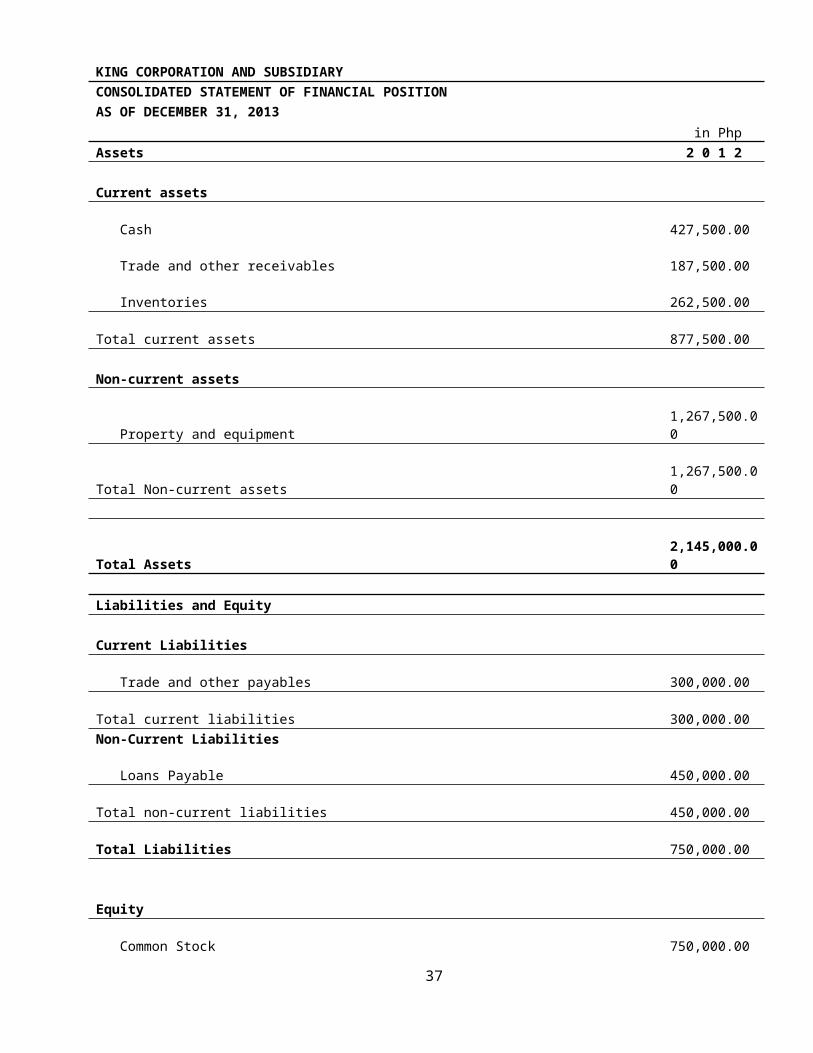

KING CORPORATION AND SUBSIDIARYCONSOLIDATED STATEMENT OF FINANCIAL POSITIONAS OF DECEMBER 31, 2013

in PhpAssets 2 0 1 2

Current assets

Cash 427,500.00

Trade and other receivables 187,500.00

Inventories 262,500.00

Total current assets 877,500.00

Non-current assets

Property and equipment

1,267,500.00

Total Non-current assets

1,267,500.00

Total Assets

2,145,000.00

Liabilities and Equity

Current Liabilities

Trade and other payables 300,000.00

Total current liabilities 300,000.00

Non-Current Liabilities

Loans Payable 450,000.00

Total non-current liabilities 450,000.00

Total Liabilities 750,000.00

Equity

Common Stock 750,000.00

Retained Earnings 645,000.00

Total Stockholders' Equity

30

1,395,000.00

Total Liabilities and Stockholders' Equity

2,145,000.00

See Accompanying Notes to Financial Statements

31

KING CORPORATION AND SUBSIDIARYCONSOLIDATED STATEMENTS OF INCOMEFOR THE YEAR ENDED DECEMBER 31, 2013

in Php2 0 1 3

Revenue 900,000Cost of Goods Sold 427,500Gross Profit 472,500Less: Operating Expenses Operating expenses 105,000 Other expenses 82,500Net Income 285,000See Accompanying Notes to Financial Statements

32

KING CORPORATION AND SUBSIDIARYCONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITYFOR THE YEAR ENDED DECEMBER 31, 2013

in Php2 0 1 2

Common Stock 750,000

Retained Earnings, January 1 450,000Net Income 285,000Dividends Declared 90,000Retained Earnings, December 31

645,000

Total Stockholders' Equity 1,395,000

33

(M1) Describe the transactions that need adjustments and must make judgment about the impact on the Total Assets, Total Liabilities, Total Equity, Net Income if identified adjustments for the year ended December 31, 2012 are not recorded. (Requirement 1)

There were transactions that SAMICO Trading made for the year end December 31, 2012, but

there were some adjustments that need to be noted and adjusted. These transactions are:

1. A check worth of P25,000 issued on December 27, 2012 that was supposed to be paid

to a supplier was only released during January 7, 2013. The original entry made was:

Dec. 27 Accounts Payable 25,000 Cash 25,000

This entry means that SAMICO Trading seems to have recorded the transaction as if

cash from the company was deducted but what the transaction is supposed to mean is

that the company has a payable to a supplier, although check was issued on December

7, 2012, still it was not released therefore no money went out yet from the company and

that there is still liability. Therefore, adjustments should be made. The adjusted entry

made is:

Dec. 31 Cash 25,000 Accounts Payable 25,000

2. A deposited payment of customers in Paranaque City worth P130,000 was not recorded

in the trial balance, therefore, the company’s accounts receivable is overstated, while the

cash account is understated. Having said, adjustments should be made. The adjusting

entry is:

Dec. 31 Cash 130,000 Accounts Receivable 130,000

3. An amount of P60,000 from sales from Makati City for the last week of December 2012

was deposited to the account of SAMICO Trading but was not recorded in the books

resulting to understatement of the company’s cash and sales. Therefore, adjustments

should be made. The adjusting entry is:

34

Dec. 31 Cash 60,000 Sales 60,000

4. A post-dated check amounting to P30,000 was given by a customer dated on January

20, 2013 but was already recorded to be part of sales. Since it is a post-dated check, no

cash were received yet; but in the original entry made, it was recorded as if the company

already received cash:

Therefore, entry made should be reverse. Since no cash was received yet, therefore, it should

be recorded only be recorded a receivable. To reduce the amount of cash, it should be

reversed and be changed into accounts receivable. The adjusting entry is:

Dec. 31 Accounts Receivable 30,000 Cash 30,000

5. Bank made charges to SAMICO Trading amounting to P8,650 which is not yet reflected

in the trial balance, therefore, adjustments are made. Since SAMICO Trading has the

obligation of paying these charges, there will be a decrease in the company’s cash

account. The adjusting entry is:

Dec. 31 Bank Charge 8,650 Cash 8,650

6. Income earned on December 30, 2012 amounting to P5,000 was not recorded on year

end’s trial balance, instead, it was recorded on January 3, 2013. Therefore, resulting to

an understated account for cash. The adjusting entry is:

Dec. 31 Cash 5,000 Other Income 5,000

35

Dec. 20 Cash 30,000 Sales 30,000

7. Within one year, various receivables are still not collected and among these receivables

are five accounts amounting to P115,000 that has a high possibility of being not collected

anymore, therefore, this has to be written-off. SAMICO Trading should set specific

amounts that they could use as allowance for doubtful accounts such as the five

accounts. Having said, this lowers the chances of SAMICO Trading of collecting

accounts receivables. The adjusting entry is:

Dec. 31 Allowance for Doubtful Accounts 115,000 Accounts Receivables 115,000

8. Allowances for doubtful accounts should always be provided depending on the aging of

receivables. For current doubtful accounts, 1% should be for allowances, 2% for over 3

to 6 months, 5% for over 6 months to 1 year, and lastly, 10% for doubtful account for

over 1 year. Having said, the adjusting entry is:

CURRENT:1,777,000 - 130,000 +

30,000 =

1,677,000

X 1%

=

16,770

3-6 MONTHS:

= 650,000

X 2%

=

13,000

6-12 MONTHS:

= 512,000

X 5%

=

25,600

> 1 YEAR: 341,000 - 115,000 = 226,000

X

10%

=

22,600

3,065,000

77,970

ALLOWANCE:

126,000 - 115,000

=

110,000

66,970 77,9

70

Dec. 31 Doubtful Accounts Expenses 66,970 Allowance for Doubtful Accounts 66,970

9. Amount of P3,000,000 was lent out to Hi5 Company supported with a note value dated

on October 28, 2012. As it matures after 90 days, this earns an interest rate of 12% per

36

annum. Therefore, this indicates that there will be income coming from this interest at the

same time, an increase in interest receivable. Having said, the adjusting entry is:

3,000,000

X

12%

X

64360

=

64,000

Dec. 31 Interest Receivable 64,000 Interest Income 64,000

10. In the original trial balance, it shows that there is an inventory of P3,302,000 but it

appears that by the end of the year, the inventory on hand is only P2,257,000. Therefore,

the adjusting entry is:

Dec. 31 Ending Inventory 2,257,000

Cost of Sales 27,545,000

Beginning Inventory 3,302,000

Purchase 26,500,000

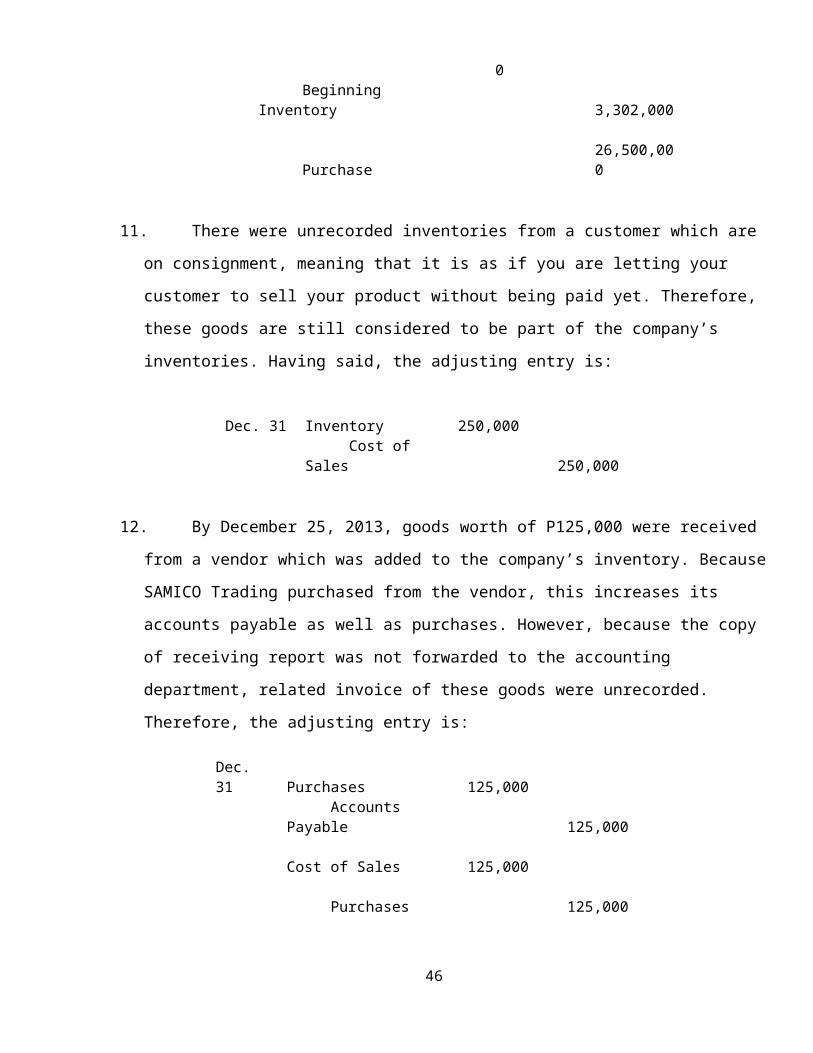

11.There were unrecorded inventories from a customer which are on consignment, meaning

that it is as if you are letting your customer to sell your product without being paid yet.

Therefore, these goods are still considered to be part of the company’s inventories.

Having said, the adjusting entry is:

Dec. 31 Inventory 250,000

Cost of Sales 250,000

12.By December 25, 2013, goods worth of P125,000 were received from a vendor which

was added to the company’s inventory. Because SAMICO Trading purchased from the

vendor, this increases its accounts payable as well as purchases. However, because the

copy of receiving report was not forwarded to the accounting department, related invoice

of these goods were unrecorded. Therefore, the adjusting entry is:

Dec. 31 Purchases

37

125,000

Accounts Payable 125,000

Cost of Sales 125,000

Purchases 125,000

13.SAMICO Trading purchased a 2 non-life policies which covers one year upon premium

payment date. The company paid for its car insurance on September 1, 2012 for

P135,000 while for the fire insurance was paid on October 1, 2012 for P105,000. Since

this is for a year, dividing each premium payment by 12 months and multiplying it to the

number of months consumed. The entry made for this is:

INSURANCE

MONTHS

EXPIRED

1-Sep CAR

135,000 4 = 45,00

0

1-Oct FIRE

105,000 3 = 26,25

0240,00

071,25

0

Dec. 31 Insurance Expense 71,250

Prepayment 71,250

14. In the general ledger, it is recorded that there is P36,000 office supplies, but it appears that by the end of the year, there is only P15,600 left. Meaning, that P20,400 were used and must be recorded as an expense. Therefore, the adjusting entry is:

Dec. 31 Office Supplies 20,400

Prepayment 20,400

15.An annual rent expense of SAMICO Trading was paid on April 30, 2012 amounting to

P450,000. Originally, SAMICO Trading recorded this transaction showing that there is an

increase in prepayment and decrease in the amount of cash. The entry made was:

38

Apr. 30 Prepayment 450,000

Cash 450,000

In this transaction, it shows that the rent has expired for the past eight months, therefore,

it is then considered as an expense. On the other hand, there is a decrease in

prepayment since the company was able to use the space for the said months.

Therefore, the adjusting entry is:

450,000 x8

12 = 300,000

Dec. 31 Rent Expense 300,000

Prepayment 300,000

16.SAMICO Trading purchased furniture and fixtures amounting to P200,000 on January 1,

2012. The estimated useful life of these are five years, therefore, dividing the cost of the

furniture and fixtures to its estimated useful life will result to P40,000 a year. However, it

was recorded that P44,000 was its depreciation expense, meaning that depreciation

expenses is overstated of P4,000. Having said so, adjustments are to be done.

200,000 / 5

= 40,000

44,000

-

40,00

0

= 4,000

Dec. 31 Accumulated Depreciation - Furniture & Fixtures 4,000

Depreciation Expense 4,000

39

17.There is an unrecorded purchase of vehicle and five desktops with amounts P500,000

and P225,000. The money used was an additional investment by partners Sam and

Mico. Given that the equipment increased by P725,000; hence, since partners agree on

50%-50%, therefore each has an equal contribution resulting to an increase in equity as

well.

Dec. 31 Transportation Equipment 500,000

Office Equipment 225,000

Sam, Capital 362,500

Mico, Capital 362,500

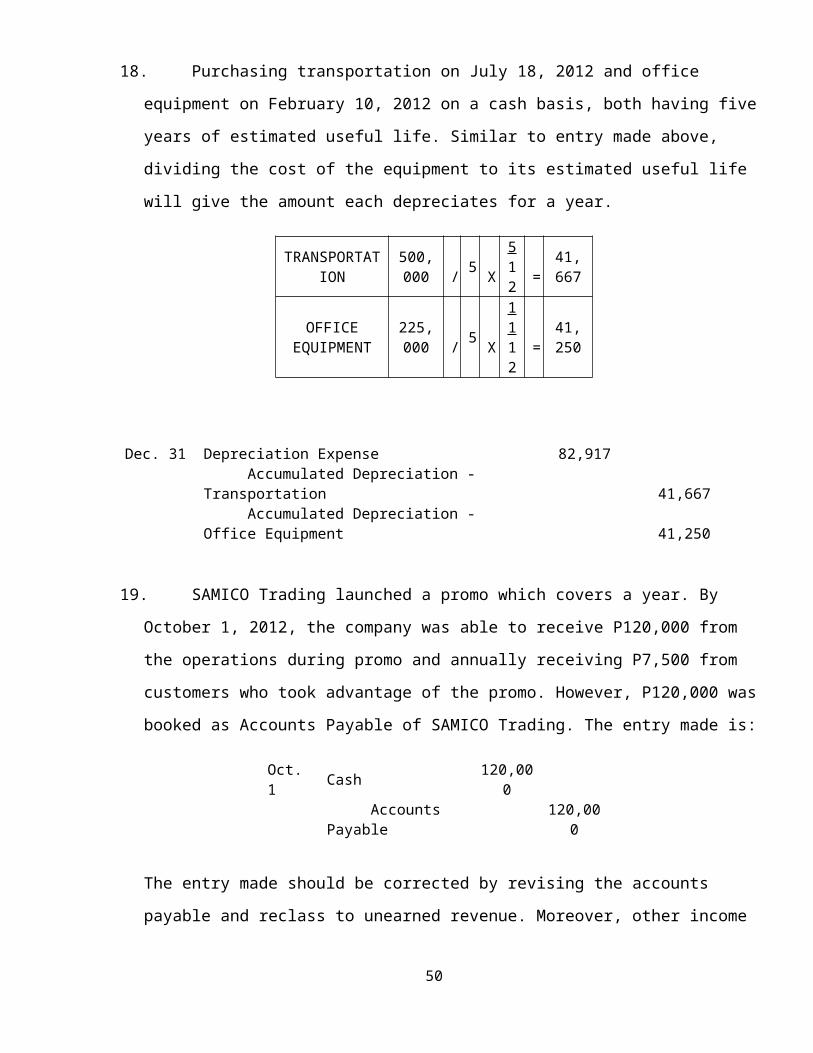

18.Purchasing transportation on July 18, 2012 and office equipment on February 10, 2012

on a cash basis, both having five years of estimated useful life. Similar to entry made

above, dividing the cost of the equipment to its estimated useful life will give the amount

each depreciates for a year.

TRANSPORTATION

500,000

/ 5

X

512

=

41,667

OFFICE EQUIPMENT

225,000

/ 5

X

1112

=

41,250

Dec. 31 Depreciation Expense 82,917

Accumulated Depreciation - Transportation 41,667

Accumulated Depreciation - Office Equipment 41,250

19.SAMICO Trading launched a promo which covers a year. By October 1, 2012, the

company was able to receive P120,000 from the operations during promo and annually

receiving P7,500 from customers who took advantage of the promo. However, P120,000

was booked as Accounts Payable of SAMICO Trading. The entry made is:

40

Oct. 1 Cash 120,000

Accounts Payable 120,000

The entry made should be corrected by revising the accounts payable and reclass to

unearned revenue. Moreover, other income should be recognized for the 3 months in

which SAMICO has already earned. Therefore, the adjusting entry is:

Dec. 31 Accounts Payable 120,000

Other Income 30,000

Unearned Revenue 90,000

20.SAMICO Trading encountered accrued payments or expenses within the year that were

not accrued or recorded at the year-end. There should have been an increase in the

company’s expense and the liability to pay. Therefore, the adjusting entry is:

Dec. 31 Telephone Expense

6,650

Salaries 15

4,250

Accrued Expenses 215,900

If these adjustments are not recorded, the impact in the total assets, total liabilities, total equity, and net income are as follows:

41

IMPACT ON TOTAL ASSETS, LIABILITIES, EQUITY AND NET INCOME

Unadjusted Adjusted Difference

Total Assets 16,779,556

16,317,369

462,187 overstated

Total Liabilities 2,426,362

2,762,262

335,900

understated

Capital 10,400,000

11,125,000

725,000

understated

Net Income 3,953,194

2,430,107

1,523,087 overstated

Total Equity 14,353,194

13,555,107

798,087 overstated

*Note: Total Equity = Capital + Net Income

42

(D1) Must draw a conclusion about the accumulated misstatement in the income statement if materiality level is 5% of Net Income before tax. (Requirement 1)

Comparing the impact of net income from unadjusted and adjusted financial statements, it is

clearly stated that income statement would have been materially misstated if adjustments were

not made. Computing the accumulated misstatement incurred results to overstatement of

P1,523,087 in net income which exceeds the 5% materiality threshold of P197,660 which is the

5% of the unadjusted net income P3,953,194.

43

Appendix

(M3) Must show that an appropriate and structured approach in the preparation of report has been used. The report presented in powerpoint should cover the nature of adjustments and a summary of adjustments. (Requirement 1)

A

B

C

D

E

F

G

H

I

J

K

SAMICO TRADINGADJUSTMENTS

Total Assets Total LiabilitiesTotal

EquityRef Explanation Adjusting Entries Capital Net Income

DR/(CR) DR/(CR) DR/(CR) DR/(CR)

1 To record issued check last December 27, 2012 but was released on January 7, 2013

Cash 25,000

Accounts Payable (25,000)

2 To record unrecorded collection from customers in Paranaque City Cash 130,00

0

Accounts Receivables (130,000)

3 To record sales report from Makati City for the last week of December 2012

Cash 60,000

Sales (60,000)

4 To reverse post-dated check Accounts Receivable 30,000

Cash (30,000)

5 To record adjustments from bank charge Bank Charge 8,65

0

Cash (8,650)

6 To record other income earned on December 30, 2012 Cash 5,00

0

Other Income (5,000)

7 To record allowance for doubtful accounts Allowance for Doubtful Accounts 115,00

0

Accounts Receivables (115,000)

8 To record provisions on aging Doubtful Accounts Expenses 66,97

L

receivables 0 Allowance for Doubtful Accounts

(66,970)

9 To record interest income from a note value dated Oct. 28 which earns interest at 12%

Interest Receivable 64,000

Interest Income (64,000)

10 To record the inventory on hand as of December 31, 2012 Ending Inventory 2,257,00

0 Cost of Sales 27,545,000Beginning Inventory (3,302,000)

Purchase (26,500,000)

11 To record goods that are on consignment year-end inventory not included in the count

Inventory 250,000

Cost of Sales (250,000)

12 To record related invoice of goods received from a vendor on December 25, 2013

Purchases 125,000

Accounts Payable (125,000)

Cost of Sales 125,000

Purchases (125,000)

13 To record monthly prepayments used for car and office insurance Insurance Expense 71,25

0

Prepayment (71,250)

14 To record the correct count of office supplies as of year-end Office Supplies Expenses 20,40

0

Prepayment (20,400)

15 To record monthly prepayments used for rent expense

Rent Expense 300,000

M

Prepayment (300,000)

16 To record excess in depreciation expense

Accumulated Depreciation - Furnitures & Fixtures

4,000

Depreciation Expense (4,000)

17 To record cash purchase of vehicle and five desktops from the additional investment by the partners

Transportation Equipment 500,000

Office Equipment 225,000

Mico, Capital (362,500) Sam, Capital (362,500)

18 To record depreciation expense of transportation equipments Depreciation Expense 41,66

7 Accumulated Depreciation - Transportation Equipment

(41,667)

19 To record depreciation expense of office equipments Depreciation Expense 41,25

0 Accumulated Depreciation - Office Equipment

(41,250)

20 To record received cash on Oct. 1, 2012 from the launched promo service and recognize income for 3 months

Accounts Payable 120,000

Other Income (30,000)

Unearned Revenue (90,000)

21 To record accrued expenses Telephone Expense 61,650

Salaries 154,250

Accrued Expenses (215,900)

Total Impact (462,187

) (335,900

) (725,000) 1,523,08

7

N

O