3 8 2011 estate planning power point

DESCRIPTION

"How to transfer your wealth to the next generation through estate planning" took place on April, 8th at the Tower Club, Vienna, VA. Our special guests were Mr. Milton Buffington and Mr. Saeid B. Amini, two well known experts that shared, for two hours, their experience on identifying legal issues and mechanisms that businesses and individuals can use to transfer their wealth and assets more efficiently, to the next generation.This was a complimentary seminar hosted by Saeid B. Amini and Milton Buffington through the courtesy of Provanedge Financial and Richard B. Osmann, Ed.D.TRANSCRIPT

Milton P. Buffington, J.D.

Saeid B. Amini, JD, Ph.D., MBA 3/9/2011, Tower Club, Vienna, VA

ESTATE PLANNING HOW TO TRANSFER WEALTH

TO NEXT GENERATION

Wealth transfer is the process of moving assets between generations. It includes a number of activities: . estate planning. estate document preparation. implementation and monitoring Wealth transfer planning normally happens in phases and evolves over time.

WEALTH TRANSFER & ESTATE PLANNING

Who needs it?No matter your net worth, it’s important to have a basic estate plan in placeWhen should it be done? During life but can be set up to be effective at death

ESTATE PLANNING

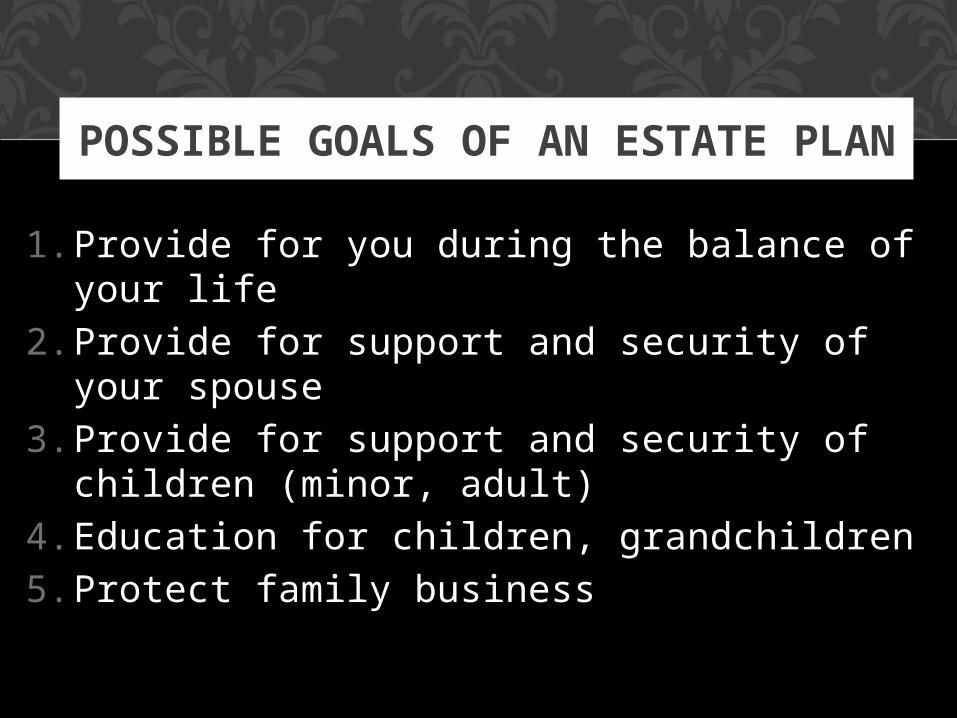

1. Provide for you during the balance of your life

2. Provide for support and security of your spouse

3. Provide for support and security of children (minor, adult)

4. Education for children, grandchildren5. Protect family business

POSSIBLE GOALS OF AN ESTATE PLAN

1. Assure that assets are distributed per your wish

2. Make final charitable gifts3. Minimize death taxes, federal estate taxes,

state inheritance and estate taxes4. Minimize or avoid probate expenses after

death5. Creditor protection

POSSIBLE GOALS OF AN ESTATE PLAN

continued

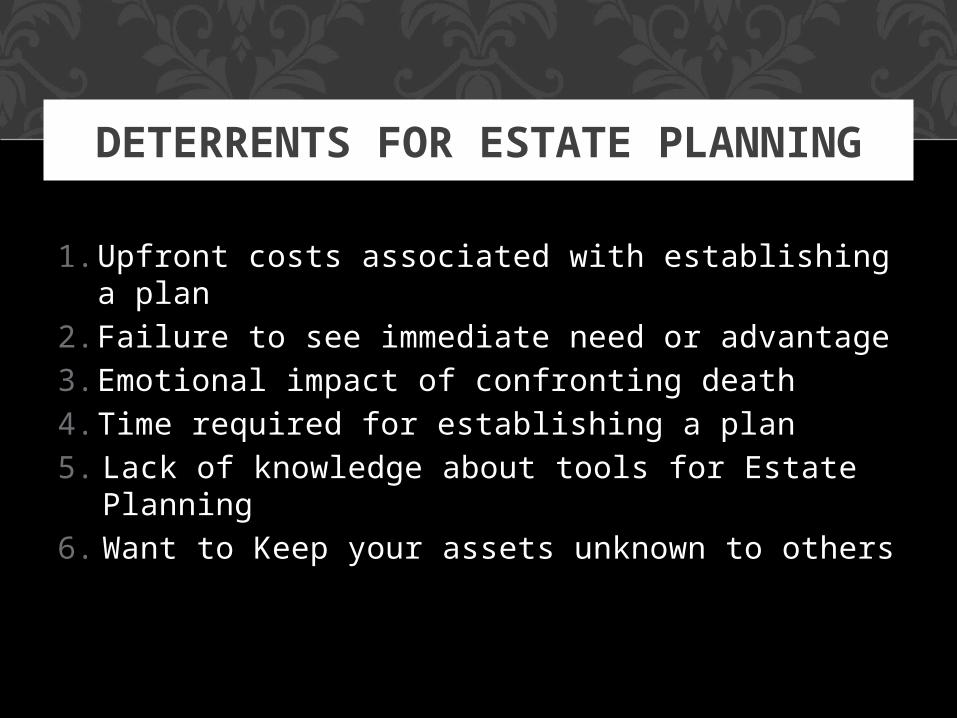

1. Upfront costs associated with establishing a plan

2. Failure to see immediate need or advantage3. Emotional impact of confronting death 4. Time required for establishing a plan5. Lack of knowledge about tools for Estate

Planning6. Want to Keep your assets unknown to others

DETERRENTS FOR ESTATE PLANNING

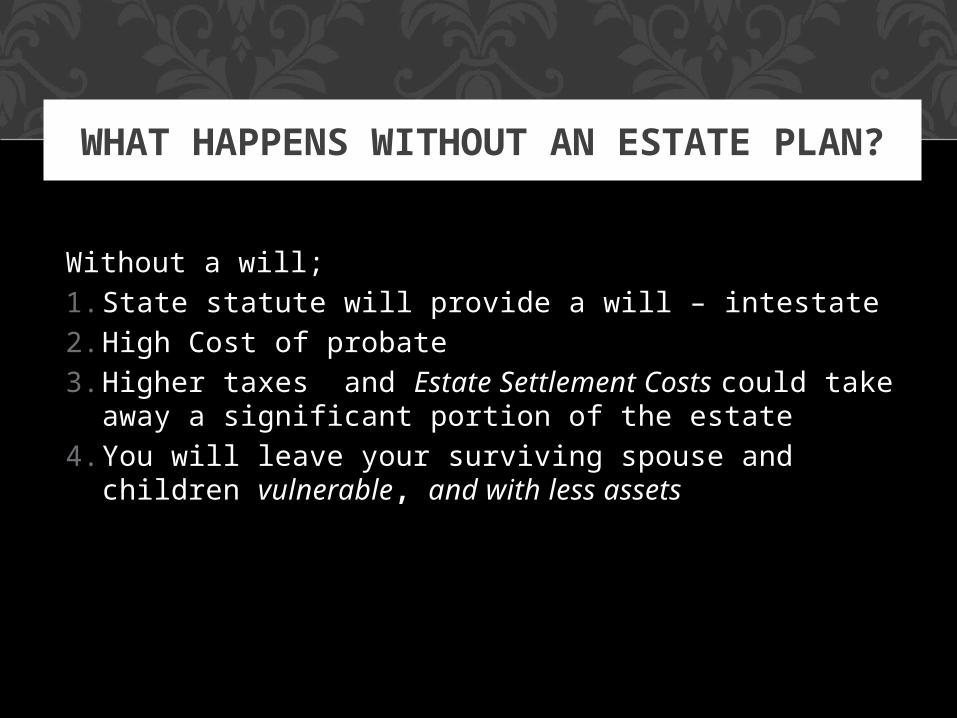

Without a will; 1. State statute will provide a will – intestate2. High Cost of probate3. Higher taxes and Estate Settlement Costs could

take away a significant portion of the estate4. You will leave your surviving spouse and

children vulnerable, and with less assets

WHAT HAPPENS WITHOUT AN ESTATE PLAN?

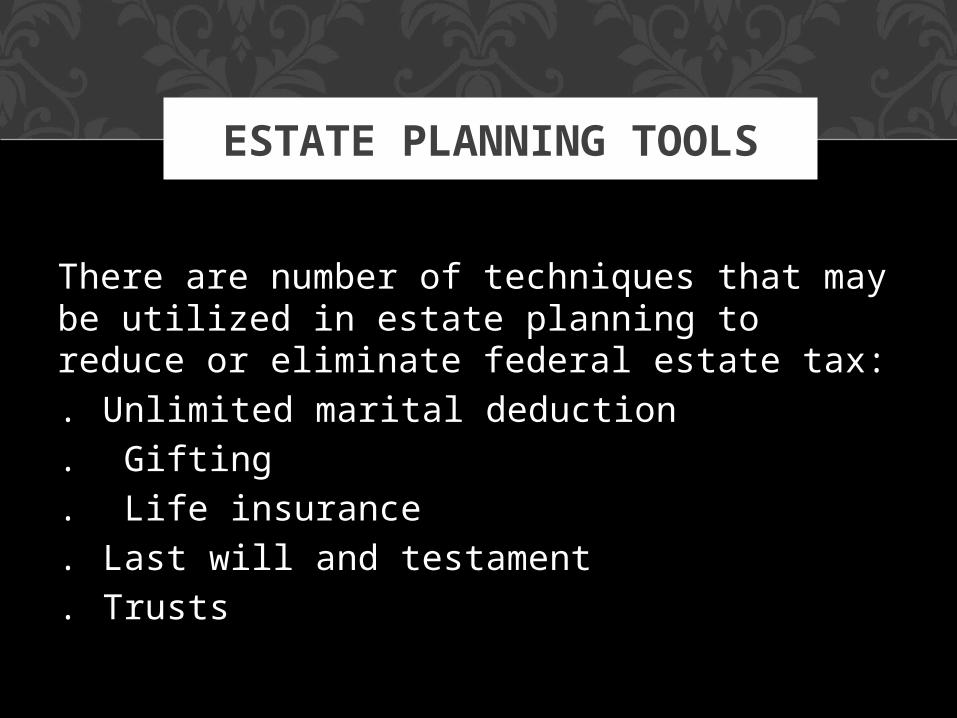

There are number of techniques that may be utilized in estate planning to reduce or eliminate federal estate tax: . Unlimited marital deduction. Gifting . Life insurance. Last will and testament. Trusts

ESTATE PLANNING TOOLS

• A trust is a relationship whereby property (including real, tangible and intangible) is managed by one person (or persons, or organizations) for the benefit of another.

• A trust is created by a settlor, who entrusts some or all of their property to people of their choice (the trustees).

• The trustees hold legal title to the trust property (or trust corpus), but they are obliged to hold the property for the benefit of one or more individuals or organizations (the beneficiary).

• The trustees owe a fiduciary duty to the beneficiaries, who are the "beneficial" owners of the trust property.

• The trust is governed by the terms of the trust document

TRUST

1. Living trust (Inter vivos Trust)

• A trust that one creates while he/she is alive

• A trust that comes into existence immediately

2. Testamentary Trust (Will Trust)

• A trust which arises upon the death of the testator, it is specified in the will

• A will may contain more than one testamentary trust, and may address all or any portion of the estate.

TWO BROAD TYPES OF TRUSTS

• With a living trust, the grantor transfers assets into the trust during life

• The grantor can also be the trustee • If the grantor becomes incapacitated, a

successor trustee, named in a will or living will, takes over and manages the grantor's financial affairs

• Property held in a living trust does not normally go through probate

1. LIVING TRUST

1. Revocable Living" Trust - created during the lifetime of a grantor that can be;• altered• changed• modified, Or• revoked

2. Irrevocable Trust - A Trust that cannot be altered, changed, modified or revoked after its creation (absent extreme extenuating circumstances). • Once a grantor transfers property to an

irrevocable Trust, the grantor can no longer take the property back from the Trust

TWO MAJOR TYPES OF LIVING TRUST

Express Trusts - are those specifically created by the grantor under a Trust agreement or declaration of Trust.

Implied Trusts - arise from particular facts and circumstances in which courts determine that although there was not any formal declaration of a Trust, there was an intention on the part of the property owner that the property be used for a particular purpose or go to a particular person. For example, if a neighbor asks you to take care of her car for her when she is on vacation, and never returns, there was an implied Trust, as she was not making you a gift of the car.

EXPRESS AND IMPLIED TRUSTS

Constructive Trust - An implied Trust established by operation of law. Resulting Trust - A Trust that arises from, or is created by operation of law, when the legal title to property is transferred, but the beneficial interest is to be enjoyed by someone other than the person who got the legal title.

COURT IMPOSED TRUSTS

Spendthrift Trust - A Trust that is established for a beneficiary which does not allow the beneficiary to sell or pledge away his or her interests in the Trust. A spendthrift Trust is beyond the reach of the beneficiaries creditors, until such time as the Trust property is distributed out of the Trust and placed in the hands of the beneficiary.

OTHER USEFUL TRUSTS

Tax By-Pass Trust - A type of Trust that is created to allow one spouse to leave money to the other, while limiting the amount of Federal Estate tax bite that would be payable on the death of the second spouse. Totten Trust - A Trust that is created during the lifetime of the grantor by depositing money into an account at a financial institution in his or her name as the Trustee for another. This is a type of revocable Trust in which the gift is not completed until the grantor's death, or an unequivocal act reflecting the gift during the grantor's lifetime.

OTHER USEFUL TRUSTScontinued

• Asset Protection Trust - A Trust that is designed to protect a person's assets from claims of future creditors – usually established in foreign countries.

• Charitable Trust - Typically charitable Trusts are established as part of an estate plan to lower or avoid imposition of Federal (and some states') estate and gift taxes.

• Special Needs Trust - A Trust that is established for a person who receives government benefits so as not to disqualify the beneficiary from such government benefits.

OTHER TRUSTS

Ordinarily when a person is receiving government benefits, an inheritance or receipt of a gift could reduce or eliminate the person's eligibility for such benefits. By establishing a Trust which provides for luxuries or other benefits which otherwise could not be obtained by the beneficiary, the beneficiary can obtain the benefits from the Trust without defeating his/her eligibility for government benefits. Often a Special Needs Trust includes a trigger which terminates the Trust in the event that it could be used to make the beneficiary ineligible for government benefits.

OTHER TRUSTScontinued

• Most commonly used trusts• Established by the terms of a will• Revocable when the testator is alive• Irrevocable after the death of the testator

It is useful if the testator wishes to set aside funds for the education of children who are minors or have just reached the age of majority.

• The trust is placed in the hands of a trustee, who may be an individual or a bank trust department.

2. TESTAMENTARY TRUST (WILL TRUST) - CAUSA MORTIS

• Life Insurance Trust. You create a life insurance trust so that the trust — and not you — owns your life insurance policies.

• Trust for Children. Should you and your spouse both die, a testamentary trust can hold your assets for your children until they reach a certain age. If your children are minors, such a trust avoids the need for a court to appoint a guardian or conservator for your children’s inherited property.

• Bypass (Family) or Credit Shelter Trust. You can use a bypass trust to minimize the tax on your surviving spouse’s estate, leaving more for your children.

COMMON TYPES OF TESTAMENTARY TRUSTS

• Marital Trust. A well-constructed marital trust lets you provide lifetime support to your spouse without leaving your assets directly to him or her. Property in the marital trust qualifies for the estate-tax marital deduction. Marital trusts are often used with bypass trusts in an estate planning arrangement known as the two-trust estate plan.

• Qualified Terminable Interest Property (QTIP) Trust. A QTIP trust is a type of marital trust that gives you complete control — through your trust agreement — over who will receive the trust property at your surviving spouse’s death.

COMMON TYPES OF TESTAMENTARY TRUSTS

continued

• Design flexibility. You can set up your trust with as much flexibility as you wish. You can limit the power of trustee, beneficiaries and even creditors.

• Longevity. A testamentary trust can be set up to benefit several generations of beneficiaries.

• Future cost savings. Your testamentary trust may reduce future probate expenses and federal estate taxes that might otherwise be incurred by your beneficiaries’ estates.

• Professional asset management. If you wish, you can name someone with professional asset management and investment experience to act as trustee or co-trustee.

OTHER BENEFITS OF TESTAMENTARY TRUSTS

A trust is only as effective as the trustee you select to administer it. A well-qualified trustee is someone who has the knowledge and experience necessary to perform all the duties associated with managing and distributing trust assets — duties such as: • Safeguarding the trust’s investment

assets • Maintaining accurate records of all trust

transactions • Distributing trust income and principal

according to the directions in your will

CHOOSING THE RIGHT TRUSTEE

• Providing information to your beneficiaries concerning the trust

• Handling day-to-day financial matters for beneficiaries

• Reporting to the probate court, when necessary

• Providing detailed statements of account and tax reports to the trust’s beneficiaries

• Filing the trust’s income-tax returns

CHOOSING THE RIGHT TRUSTEE

continued

Thank you for your time

Milton P. Buffington, J.D. 202-256-1700Saeid B. Amini, JD, Ph.D., MBA 202-306-9444

Address:730 2th Street, NW, Suite OneWashington DC 20037

QUESTIONS?