30.06.2015 seite 1 kadin – paklim briefing k „business and climate change in indonesia“ 7 july...

Post on 21-Dec-2015

216 views

TRANSCRIPT

18.04.23 Seite 1

KADIN – PAKLIM Briefing k

„Business and Climate Change in Indonesia“

7 July 2011

18.04.23 Seite 2Jakarta, July 2011 2

Overall objective and starting points

Objective

Intensify the cooperation between GIZ/ PAKLIM and KADIN to jointly work on increasing awareness and engaging Indonesian companies in climate change mitigation activities in Indonesia

Starting points

PAKLIM’s commitment to strengthen its private sector engagement and Call for Proposals 2011

Kadin’s White Paper on the issues of Climate Change and Green Growth

18.04.23 Seite 3Jakarta, July 2011 3

Contents

Introduction GIZ / PAKLIM in Indonesia

Climate change in Indonesia Integration of climate change into national development planning Private sector involvement in climate change mitigation Focus: The industry sector and climate change

PAKLIM portfolio on cooperation with the private sector PAKLIM Call for Proposals

Cooperation opportunities between KADIN and PAKLIM

18.04.23 Seite 4Jakarta, July 2011 4

• A 100% federally owned, public-benefit enterprise, that supports the German Government in achieving its development policy goals.

• GIZ’s purpose is to promote international cooperation for sustainable development and international education work.

• Established on 1 January 2011, GIZ brings together under one roof the long-standing expertise of DED, GTZ und InWEnt.

– Implements commissions for the German federal government and other national and international, public and private-sector clients.

– Furthers political, economic, ecological and social development worldwide, and so improves people’s living conditions.

– Provides services that support complex development and reform processes.

• Operates in more than 130 countries worldwide.• Employs approximately 17,000 staff members worldwide, more than 60%

of whom are local personnel.

Who is GIZ?

18.04.23 Seite 5Jakarta, July 2011 5

GIZ in Indonesia at a glance

3 Climate Change programmes:

•Environment: “PAKLIM”•Forest: “FORCLIME”•Transport: “SUTIP”

1975

Indonesian-German development cooperation through GTZ

2007

Government negotiations to renew priority areas

3 priority areas:

•Private Sector Development•Good Governance•Climate Change

18.04.23 Seite 6Jakarta, July 2011 6

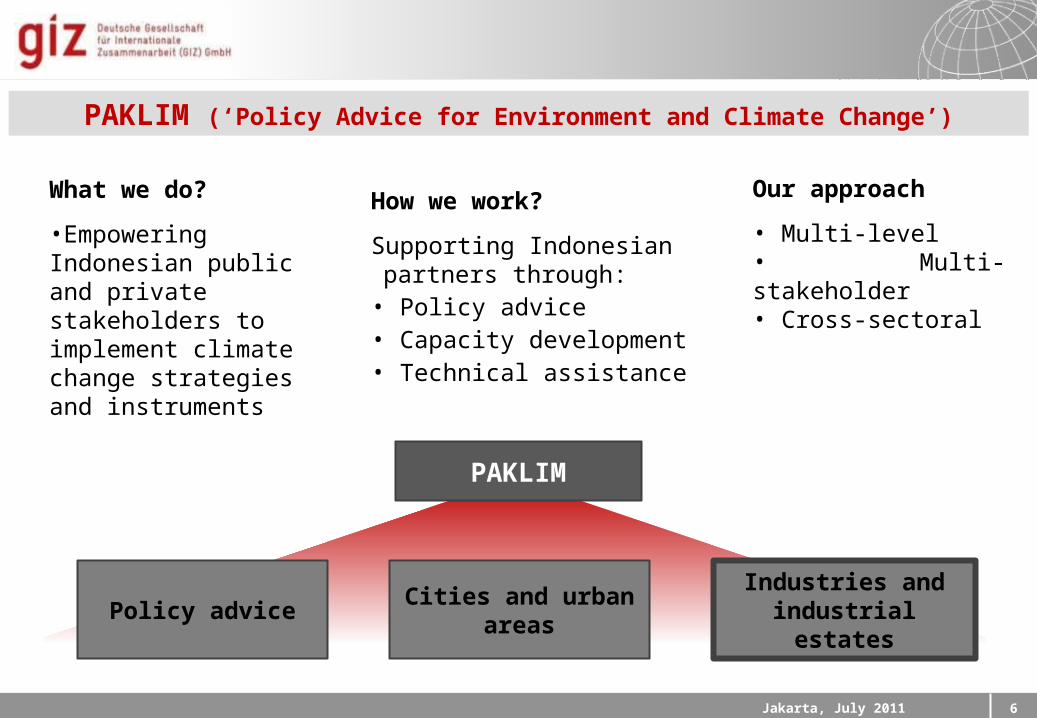

How we work?

Supporting Indonesian partners through:

• Policy advice• Capacity development• Technical assistance

What we do?

•Empowering Indonesian public and private stakeholders to implement climate change strategies and instruments

Our approach

• Multi-level• Multi-stakeholder• Cross-sectoral

PAKLIM (‘Policy Advice for Environment and Climate Change’)

PAKLIM

Policy adviceCities and urban

areasIndustries and

industrial estates

18.04.23 Seite 7Jakarta, July 2011 7

Climate Change

in Indonesia

18.04.23 Seite 8Jakarta, July 2011 8

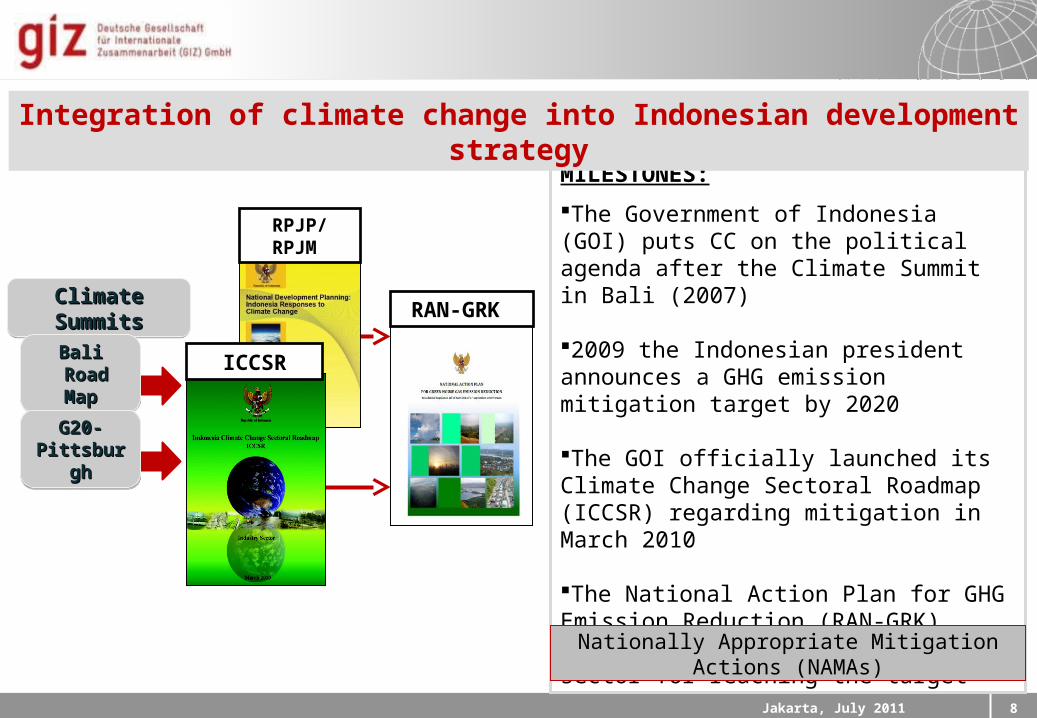

Climate SummitsClimate SummitsClimate SummitsClimate Summits

ICCSR

RPJP/ RPJM

RAN-GRK

BaliBali Road MapRoad Map

BaliBali Road MapRoad Map

G20-G20-PittsburghPittsburgh

G20-G20-PittsburghPittsburgh

MILESTONES:

The Government of Indonesia (GOI) puts CC on the political agenda after the Climate Summit in Bali (2007)

2009 the Indonesian president announces a GHG emission mitigation target by 2020

The GOI officially launched its Climate Change Sectoral Roadmap (ICCSR) regarding mitigation in March 2010

The National Action Plan for GHG Emission Reduction (RAN-GRK) defines the required measures per sector for reaching the target

Nationally Appropriate Mitigation Actions (NAMAs)

Integration of climate change into Indonesian development strategy

18.04.23 Seite 9Jakarta, July 2011 9

President commitment G-20 Pittsburgh and COP15

to reduce te GHG emission in 2020

President commitment G-20 Pittsburgh and COP15

to reduce te GHG emission in 2020

RAN-GRK

Scenario of 2020 GHG emission reduction and RAN GRK

Waste Waste AgricultureEnergy & transport

-26%

-15%

= 41%

Unilateral (without international support)

With international support

Forestry & peat land

Industry

18.04.23 Seite 10Jakarta, July 2011 10

• The Private Sector is the driving force for development and growth in Indonesia (Indonesia is said to soon become the 2nd “I” in BRIC)

• With this growth, however, it is also an increasingly important contributor to Indonesia’s emission levels

– E.g. due to the large amounts of energy consumed for companies’ production activities and daily operations, process-related generation of GHG and waste produced in the various industry sectors, commercial land use conversion

• The Private Sector is expected to play an essential role in Indonesia’s mitigation regime to achieve the national mitigation targets in the defined RAN GRK sectors

Companies predispose of important competences, expertise and largely also financial means for successfully tackling the issues posed by climate change and for helping to reduce GHG emissions by applying the right management and investments approaches

The role of Indonesia’s private sector in climate change mitigation

18.04.23 Seite 11Jakarta, July 2011 11

• Invest in and implement new technologies• Engage in mitigation measures, e.g. energy efficiency improvements,

fuel switching, major process modifications• Esp. multinational corporations (MNCs) and large national companies

to act as “climate champions” for other (national) businesses• Provide qualified personnel, transfer skills and experiences• Show corporate social responsibility (CSR)• Do research and innovate

Public expectations towards the private sector and ‘routes’ for involvement

Routes for involvement

Policies and regulations

Economic and fiscal instruments

Voluntary actions

18.04.23 Seite 12Jakarta, July 2011 12

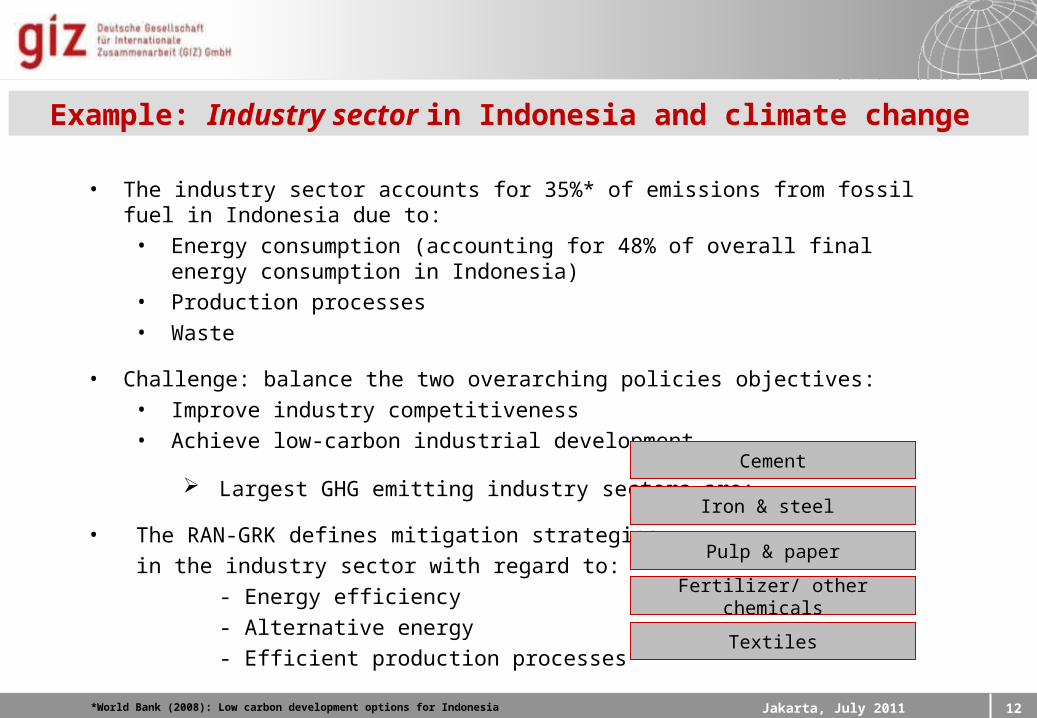

Mitigation Target by 2020Example: Industry sector in Indonesia and climate change

*World Bank (2008): Low carbon development options for Indonesia

• The industry sector accounts for 35%* of emissions from fossil fuel in Indonesia due to:• Energy consumption (accounting for 48% of overall final energy consumption in

Indonesia) • Production processes• Waste

• Challenge: balance the two overarching policies objectives:• Improve industry competitiveness• Achieve low-carbon industrial development

Largest GHG emitting industry sectors are:

• The RAN-GRK defines mitigation strategies

in the industry sector with regard to:

- Energy efficiency

- Alternative energy

- Efficient production processes

Cement

Textiles

Iron & steel

Pulp & paper

Fertilizer/ other chemicals

18.04.23 Seite 13Jakarta, July 2011 13

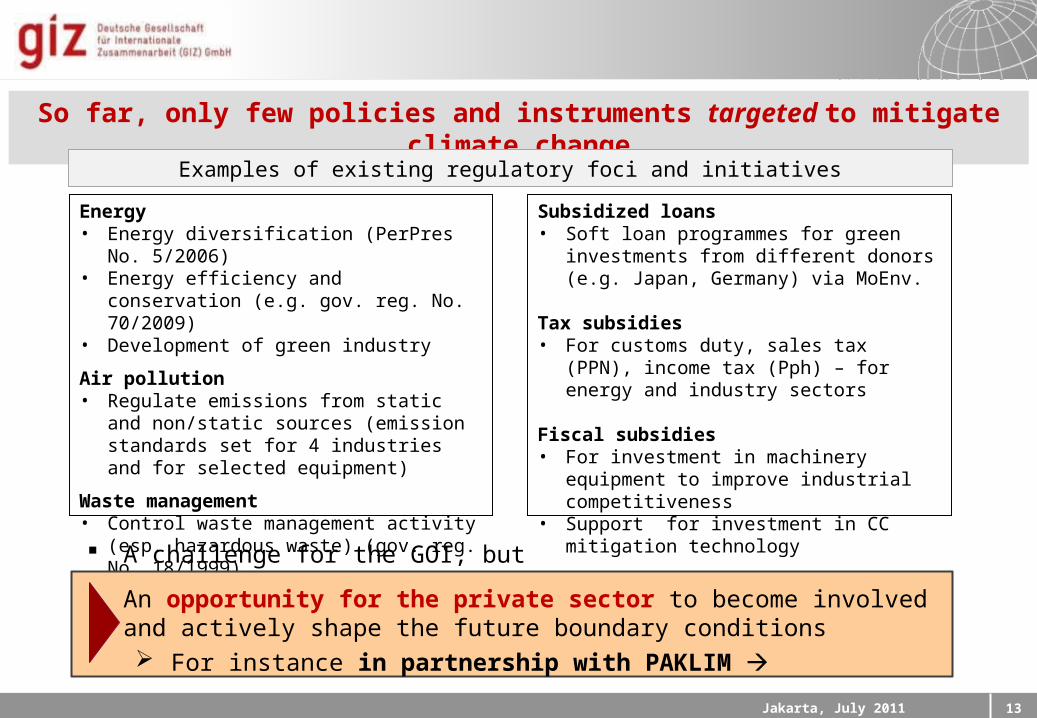

Mitigation Target by 2020So far, only few policies and instruments targeted to mitigate climate change

Energy• Energy diversification (PerPres No. 5/2006)• Energy efficiency and conservation (e.g. gov.

reg. No. 70/2009)• Development of green industry

Air pollution• Regulate emissions from static and

non/static sources (emission standards set for 4 industries and for selected equipment)

Waste management• Control waste management activity (esp.

hazardous waste) (gov. reg. No. 18/1999)• Waste utilization (gov. regulation

No.18/2008)

Subsidized loans• Soft loan programmes for green investments

from different donors (e.g. Japan, Germany) via MoEnv.

Tax subsidies• For customs duty, sales tax (PPN), income

tax (Pph) – for energy and industry sectors

Fiscal subsidies• For investment in machinery equipment to

improve industrial competitiveness• Support for investment in CC mitigation

technology

Examples of existing regulatory foci and initiatives

A challenge for the GOI, but

An opportunity for the private sector to become involved and actively shape the future boundary conditions For instance in partnership with PAKLIM

18.04.23 Seite 14Jakarta, July 2011 14

PAKLIM private sector cooperation – Overview

Projects/ Initiatives

• Merck: “Environmentally Sound Management of Chemical Waste”; 12/09-12/12; 1,4 Mio.€ (STA)

• OSRAM: “Energy Saving Movement”; 12/09-06/11; 400T€

• Merck customers (e.g. laboratories); KLH

• Elementary schools & SMKs, local communities, Indonesian population

• Adidas: “Greening Global Supply Chains – Focus on Energy”; 05/11-05/13; 168T€

• OSRAM: “Energy Efficient Street Lighting / LED Street Lighting”; 05/11-12/12; 184T€

• Service providers, local footwear & apparel suppliers; MoI, ESDM

• Local government; urban population

• “Innovations for a low-carbon future in the Indonesian Industries”

• Technology providers (D, EU)• local MNC, SOE, national companies

• Empirical study on “Business and Climate Change in Indonesia”

• “Green” CSR

• Interviews a.o. with Siemens, SAP, APP, Sinarmas, Martha Tilaar, Chandra Asri, DB Schenker

• local CSR networks, associations; KLH

Partner / Target group

develoPPP.de

integrated DPP

PAKLIM Call for Proposals 2011

Private Sector Dialogues

• NAMA (overall concept and sectors industry, energy, waste, energy efficiency in urban areas)

• Voluntary Partnership Agreements• ICCTF (Indonesia Climate Change Trust Fund), Green

Finance

• Bappenas, MoI, ESDM, MoHA

• MoI; cement industry• Bappenas, MoF; Bank of Indonesia

Policy Advice

18.04.23 Seite 15

PAKLIM Call for Proposals 2011

“Innovations for a low-carbon future

in the Indonesian industries”

Development Partnerships with the Private Sector (DPP)

18.04.23 Seite 16Jakarta, July 2011 16

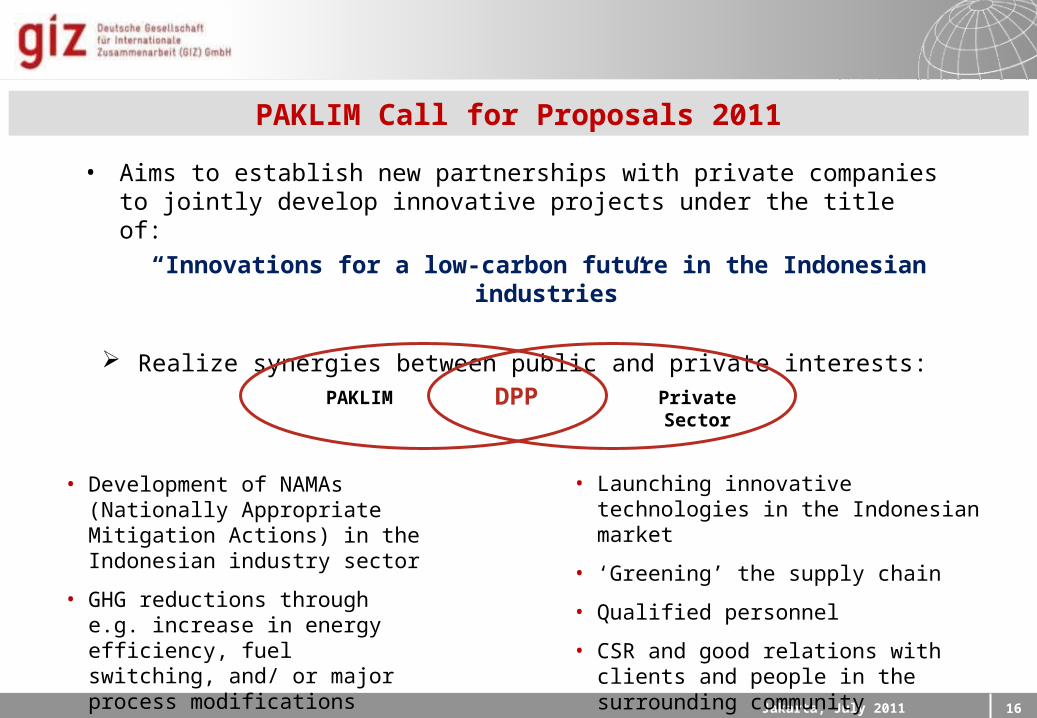

• Aims to establish new partnerships with private companies to jointly develop innovative projects under the title of:

“Innovations for a low-carbon future in the Indonesian industries”

Realize synergies between public and private interests:

PAKLIM Call for Proposals 2011

DPPPAKLIM

• Development of NAMAs (Nationally Appropriate Mitigation Actions) in the Indonesian industry sector

• GHG reductions through e.g. increase in energy efficiency, fuel switching, and/ or major process modifications

Private Sector

• Launching innovative technologies in the Indonesian market

• ‘Greening’ the supply chain

• Qualified personnel

• CSR and good relations with clients and people in the surrounding community

18.04.23 Seite 17Jakarta, July 2011 17

National and international companies already active in Indonesia and interested in:

• Investing and jointly implementing innovative technologies and energy efficiency measures in their own production sites and supply chains.

• Using their CSR funds and experiences for building new climate change business models and with this to help the local community and to become climate 'champions'.

Technology providers interested in entering the Indonesian market and applying innovative technological business models for industrial enterprises and/ or industrial estates, preferably in the areas of:

• Process heat/ heat recovery (CHP), co-generation• Efficient boiler and motor systems; automatisation• Fuel switching; renewable energy applications; recycling, efficient material use

Any company with an innovative proposal for initiating jointly with PAKLIM a model for the implementation of NAMAs in the Indonesian industry sector.

Who should participate?

18.04.23 Seite 18Jakarta, July 2011 18

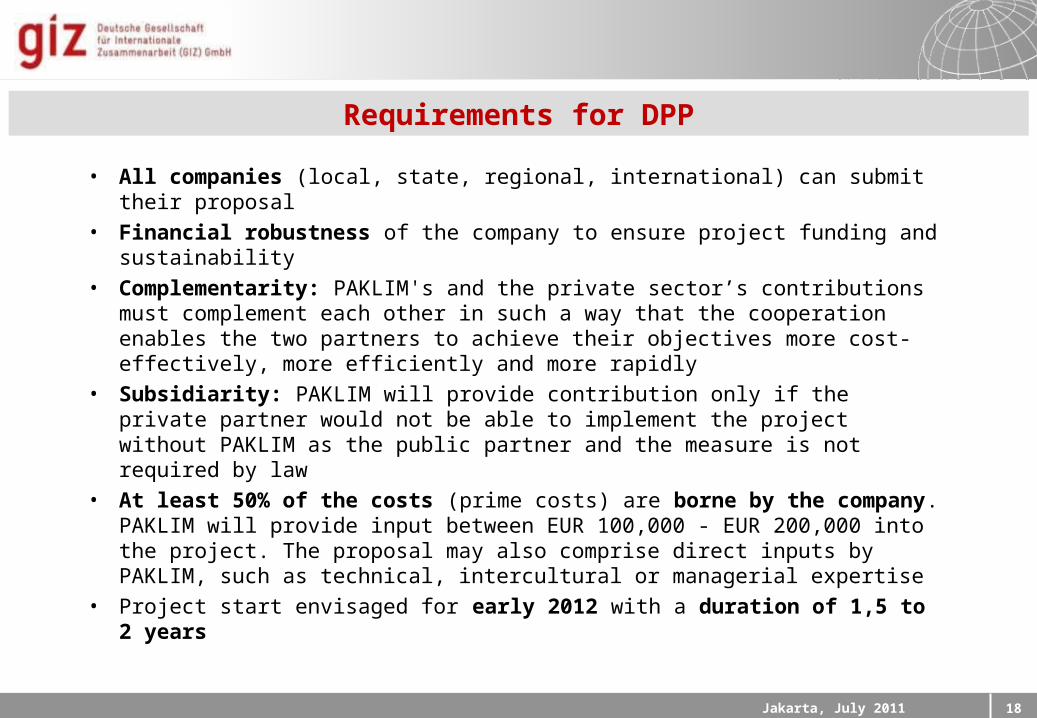

• All companies (local, state, regional, international) can submit their proposal

• Financial robustness of the company to ensure project funding and sustainability

• Complementarity: PAKLIM's and the private sector’s contributions must complement each other in such a way that the cooperation enables the two partners to achieve their objectives more cost-effectively, more efficiently and more rapidly

• Subsidiarity: PAKLIM will provide contribution only if the private partner would not be able to implement the project without PAKLIM as the public partner and the measure is not required by law

• At least 50% of the costs (prime costs) are borne by the company. PAKLIM will provide input between EUR 100,000 - EUR 200,000 into the project. The proposal may also comprise direct inputs by PAKLIM, such as technical, intercultural or managerial expertise

• Project start envisaged for early 2012 with a duration of 1,5 to 2 years

Requirements for DPP

18.04.23 Seite 19Jakarta, July 2011 19

Accordance with development policy

Contribution to the achievement of PAKLIM

objectives

Joint objectives & substantial contribution

of the company

Subsidiarity & competitive neutrality

Criteria for DPP

What are the criteria?

18.04.23 Seite 20Jakarta, July 2011 20

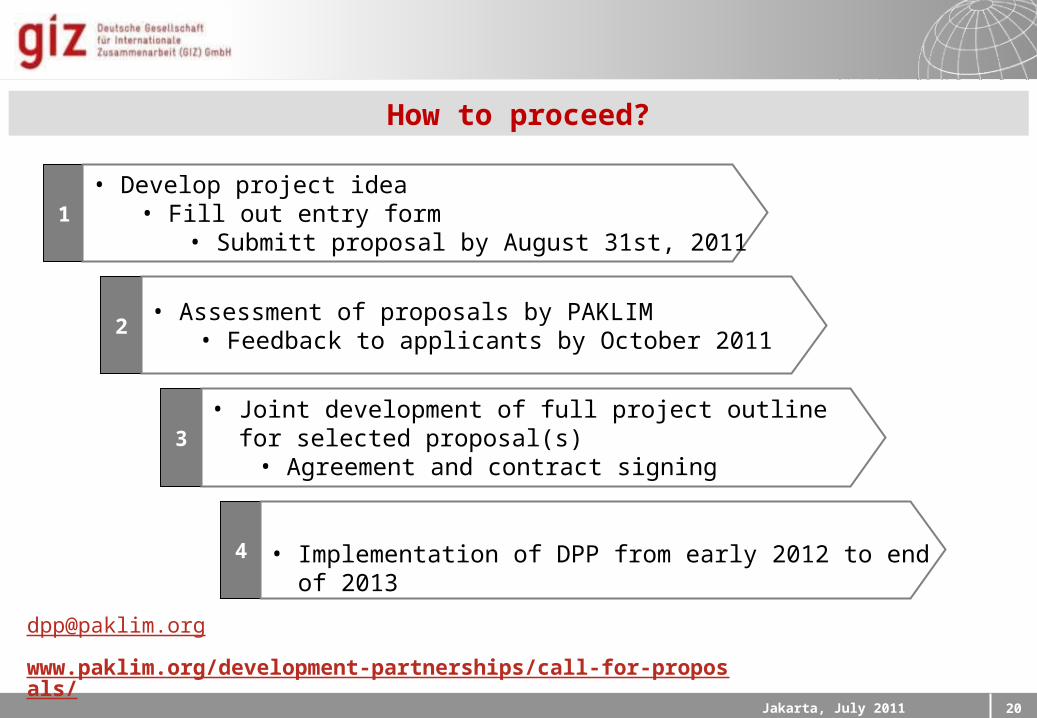

1

2

3

4

• Develop project idea• Fill out entry form

• Submitt proposal by August 31st, 2011

• Assessment of proposals by PAKLIM• Feedback to applicants by October 2011

• Joint development of full project outline for selected proposal(s)

• Agreement and contract signing

• Implementation of DPP from early 2012 to end of 2013

How to proceed?

www.paklim.org/development-partnerships/call-for-proposals/

18.04.23 Seite 21Jakarta, July 2011 21

Participate in stakeholder dialogues and workshops representing the private sector

Support the Call for Proposals for new development partnerships to support the NAMA strategy (energy efficiency, renewable energy applications, greening the supply chains)

Support the public awareness campaigns for a low carbon development

Facilitate Voluntary Partnerships (VP) between the MoInd and enterprises

Participate in the development of a low carbon growth strategy (East Kalimantan, Java)

PAKLIM: KADIN’s opportunities for cooperation

18.04.23 Seite 22Jakarta, July 2011 22

Dr. Dieter BrulezDr. Maren Breuer

PAKLIM - Policy Advice for Environment and Climate Changec/o Kementerian Negara Lingkungan Hidup (KLH)

Gedung B Lt.5, Jl. DI Panjaitan Kav 2413410 Jakarta, Indonesia

T: +62-21-8517186F: +62-21-8516110

E: [email protected] or [email protected]: www.giz.de ; www.paklim.org

Contact details

18.04.23 Seite 23Jakarta, July 2011 23

Project Examples

“Development Partnerships with the Private Sector (DPP)”

18.04.23 Seite 24Jakarta, July 2011 24

Challenge The industry sector accounts for high amounts of GHG emissions

due to energy consumption, inefficient production processes & industrial waste.

High need & potential for energy efficiency (EE) measures.

Approach Capacity building for service providers and training & technical

assistance for 16 suppliers in the apparel & footwear industries.

Energy audits and tools for the measurement, monitoring and reporting of energy performance.

Implementation of financially feasible EE measures.

Indonesia

Greening global supply chains – Focus on energy

Partners:Adidas Group (Sourcing Ltd. Asia)

05/2011 – 05/2013Volume: 268.000 €PAKLIM: 133.000 €

Impact Qualified service providers, enhanced capacities of selected

suppliers and reduction of the factories’ environmental footprint.

Model for the measurement and reporting of climate-related values in supply chains available.

18.04.23 Seite 25Jakarta, July 2011 25

Challenge Lack of efficient energy due to outdated technologies in commercial

and residential buildings as well as public infrastructural services.

High potential for cost and energy savings in urban areas.

Approach Assessment of technical & economic feasibility of LED street

lighting.

Replacement of conventional lights by LED based on an adequate metering system, lighting management, and a consumption-based payment for the energy used by public street lighting.

Identification of financing options for local governments.

Development of a handbook for energy, cost and CO2 savings

through LED street lighting.

Indonesia

Energy Efficient Street Lighting / LED Street Lighting

Partners:PT OSRAM Indonesia

05/2011 – 12/2012Volume: 184.000 €PAKLIM: 92.000 €

Impact Provides a model for NAMA on the energy demand side.

Cities are able to properly measure used energy and reduce local energy costs.

18.04.23 Seite 26Jakarta, July 2011 26

Challenge High environmental impacts from waste, unsafe disposal of

hazardous waste.

Cement industry has high potential to improve waste management by applying co-processing.

Approach Development of a guideline with the requirements and standards for

co-processing.

Transfer of ‘lessons learned’ from developed countries.

Capacity building before launching of co-processing.

Indonesia

Guideline on Co-processingWaste Materials in Cement Production

Partners:Holcim Group, Indocement

11/2006 – 11/2009Volume: 90.000 €Public (ProLH): 30.000€

Impact Decrease the environmental impacts of waste.

Decrease greenhouse gas emissions.

Improve waste management and decrease waste handling costs.

18.04.23 Seite 27Jakarta, July 2011 27

Challenge > 19% of total energy consumption is attributed to the use of

artificial light.

Common use of energy wasting light bulbs.

Approach Integrated approach that includes an upgrade of lighting systems at

selected schools and households combined with educational measures on energy efficiency.

Students participate in math and essay competitions with focus on energy saving.

Nationwide media campaign about energy efficiency.

Indonesia

Energy Saving Movement

Partners:PT OSRAM Indonesia

12/2009 – 06/2011Volume: 400.000 €Public: 200.000€

Impact Energy consumption has successfully been decreased by more

than 50 percent.

The learning module about energy efficiency is being implemented in vocational schools and will be part of lessons for more than 10.000 students.

18.04.23 Seite 28Jakarta, July 2011 28

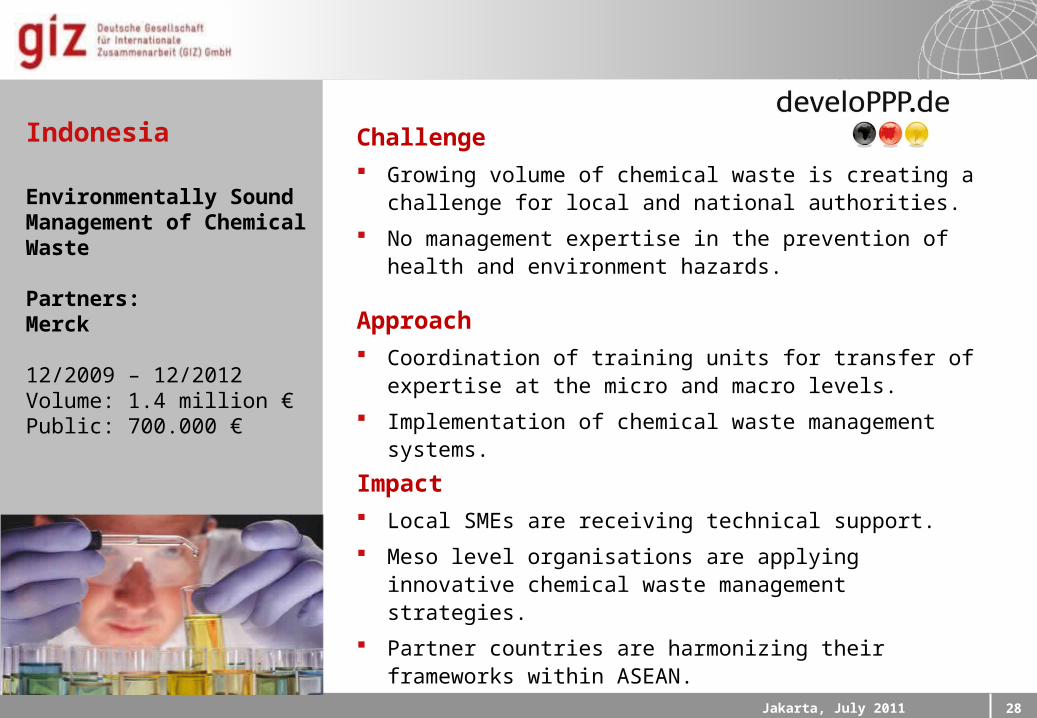

Environmentally Sound Management of Chemical Waste

Partners:Merck

12/2009 – 12/2012Volume: 1.4 million €Public: 700.000 €

Impact Local SMEs are receiving technical support.

Meso level organisations are applying innovative chemical waste management strategies.

Partner countries are harmonizing their frameworks within ASEAN.

Challenge Growing volume of chemical waste is creating a challenge for

local and national authorities.

No management expertise in the prevention of health and environment hazards.

Approach Coordination of training units for transfer of expertise at the

micro and macro levels.

Implementation of chemical waste management systems.

Indonesia

18.04.23 Seite 29Jakarta, July 2011 29

Impact Small hydropower plants receive financing through CER.

Permanent co-financing and improved conditions for Clean Development Mechanisms (CDM).

Challenge The majority of the population, especially in rural areas, has no

or just unsteady access to electric energy.

Current energy sources are not sustainable.

Approach Testing, consulting and training for and documentation of

implementation of co-financing mechanisms through Certified Emission Reductions (CER).

Indonesia, Nicaragua, Honduras, Guatemala

Co-financing mechanisms for hydropower plants

Partners:South Pole

12/2007 – 02/2011Volume: 900.000 €Public: 440.000 €

18.04.23 Seite 30Jakarta, July 2011 30

BACKUP

18.04.23 Seite 31Jakarta, July 2011 31

Portfolio

– Cooperation with the Private Sector on

“Environment and Climate Change”

Details

18.04.23 Seite 32Jakarta, July 2011 32

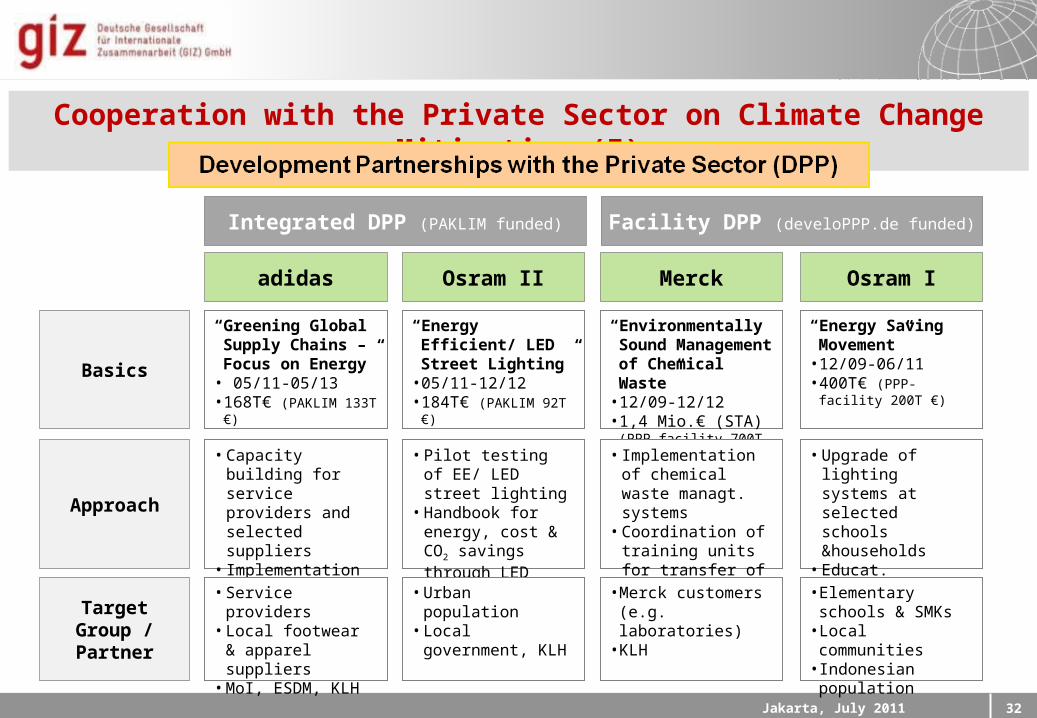

Cooperation with the Private Sector on Climate Change Mitigation (I)

Basics

Approach

Target Group / Partner

“Greening Global Supply Chains – Focus on Energy”

• 05/11-05/13• 168T€ (PAKLIM 133T €)

• Capacity building for service providers and selected suppliers

• Implementation of financially feasible EE measures

• Service providers • Local footwear &

apparel suppliers• MoI, ESDM, KLH

“Energy Efficient/ LED Street Lighting”

• 05/11-12/12• 184T€ (PAKLIM 92T €)

• Pilot testing of EE/ LED street lighting

• Handbook for energy, cost & CO2 savings through LED street lighting

• Urban population• Local government,

KLH

“Environmentally Sound Management of Chemical Waste”

• 12/09-12/12• 1,4 Mio.€ (STA) (PPP-

facility 700T €)

• Implementation of chemical waste managt. systems

• Coordination of training units for transfer of expertise

• Merck customers (e.g. laboratories)

• KLH

“Energy Saving Movement”

• 12/09-06/11 • 400T€ (PPP-facility

200T €)

• Upgrade of lighting systems at selected schools &households

• Educat. measures & nationwide media campaign on EE

• Elementary schools & SMKs

• Local communities• Indonesian

population

adidas Osram II Merck Osram I

Integrated DPP (PAKLIM funded) Facility DPP (develoPPP.de funded)

18.04.23 Seite 33Jakarta, July 2011 33

Cooperation with the Private Sector on Climate Change Mitigation (II)

NAMA - Nationally Appropriate Mitigation Actions

Support development of the overall strategic concept

Give sector specific advice for industry, waste, energy efficiency (EE) in urban areas

Voluntary partnership agreements (VPA)

Facilitate GOI and selected industries to reduce GHG emissions

Policy framework stipulating certain actions, e.g. EE standards or GHG emission limits

Economic and fiscal instruments, incentive schemes to ease private sector participation

ICCTF (Indonesia Climate Change Trust Fund) as a funding mechanism and facility for mitigation and adaptation

Further the transfer of appropriate technologies to be used by the private sector and foster research & development for such innovations in Indonesia itself

18.04.23 Seite 34Jakarta, July 2011 34

Cooperation with the Private Sector on Climate Change Mitigation (III)

Empirical study on “Private sector involvement in climate change activities in Indonesia”

Interviews a.o. with Siemens, SAP, APP, Sinarmas, Martha Tilaar, PT Chandra Asri, DB Schenker, Holcim, PT Indocement, PT Petrokimia Gresik, PT Chandra Asri, PT Semen Gresik

“Green” CSR

Participation in KLH working group on establishing guideline for “green” CSR and criteria for evaluation and official recognition

Initiation of roundtable / stakeholder exchanges on CSR

Implementation and communication of pilot projects and best practices

Provision of information and technical assistance to the private sector

Cooperation with chambers and business associations, e.g. for joint awareness campaigns for a low carbon development