360 degree ceo global and economic perspective of the chemicals & materials industry

TRANSCRIPT

1

360 Degree CEO Global and Economic

Perspective Of The Chemicals &

Materials Industry

© 2009 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan.

No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan

2

Chemicals Market - Key End User Industries

Chemicals Customer Needs

Market Growth

Competitive Landscape

Energy&

PowerAerospace&

Defense

Automotive&

Transportation

InformationCommunication

&Technology

HealthcareIndustrial

Automation&

Electronics

Environment&

BuildingControls

Market interdependencies will determine the developments in the Global Chemicals Market

3Chemicals &

Materials

Effect of Downturn on the Global Chemicals & Materials Market

Automotive giants are hit hard by economic recession and resulting drop in global demand; this directly affects all dependent chemicals and materials markets

Automotive giants are hit hard by economic recession and resulting drop in global demand; this directly affects all dependent chemicals and materials markets

Housing market collapse affected a wide range of chemicals and materials markets

Significant job losses in the industry and plant closures (Dow, BASF, Rohm & Haas and other)

Decline in consumer demand affects end-market pricing, which in turn led to volume reduction

Housing market collapse affected a wide range of chemicals and materials markets

Significant job losses in the industry and plant closures (Dow, BASF, Rohm & Haas and other)

Decline in consumer demand affects end-market pricing, which in turn led to volume reduction

Decline in consumer demand resulted in scaling-down of production and redundancies across all industries.

Construction. automotive and real estate industries and the finance and banking sectors have already been hit, affecting the chemicals and materials markets

Decline in consumer demand resulted in scaling-down of production and redundancies across all industries.

Construction. automotive and real estate industries and the finance and banking sectors have already been hit, affecting the chemicals and materials markets

Hungary and Czech republic were hit hard by the economic stagnation

Poland is still experiencing growth fuelled by the increasing adoption of western-type lifestyle and consumption of relevant products

Hungary and Czech republic were hit hard by the economic stagnation

Poland is still experiencing growth fuelled by the increasing adoption of western-type lifestyle and consumption of relevant products

Russia is affected by the economic downturn but its strong position in oil and gas reserves suggest a quick comebackSome badly hit: Uralkali reduced its production by 6.4 per cent in 2008, with a massive short-term fall in December

Russia is affected by the economic downturn but its strong position in oil and gas reserves suggest a quick comebackSome badly hit: Uralkali reduced its production by 6.4 per cent in 2008, with a massive short-term fall in December

Drastic drop in exports of textiles, leather and other finished goods due to major recession in western economies significantly impact the chemical markets.

Drastic drop in exports of textiles, leather and other finished goods due to major recession in western economies significantly impact the chemical markets.

4Chemicals &

Materials

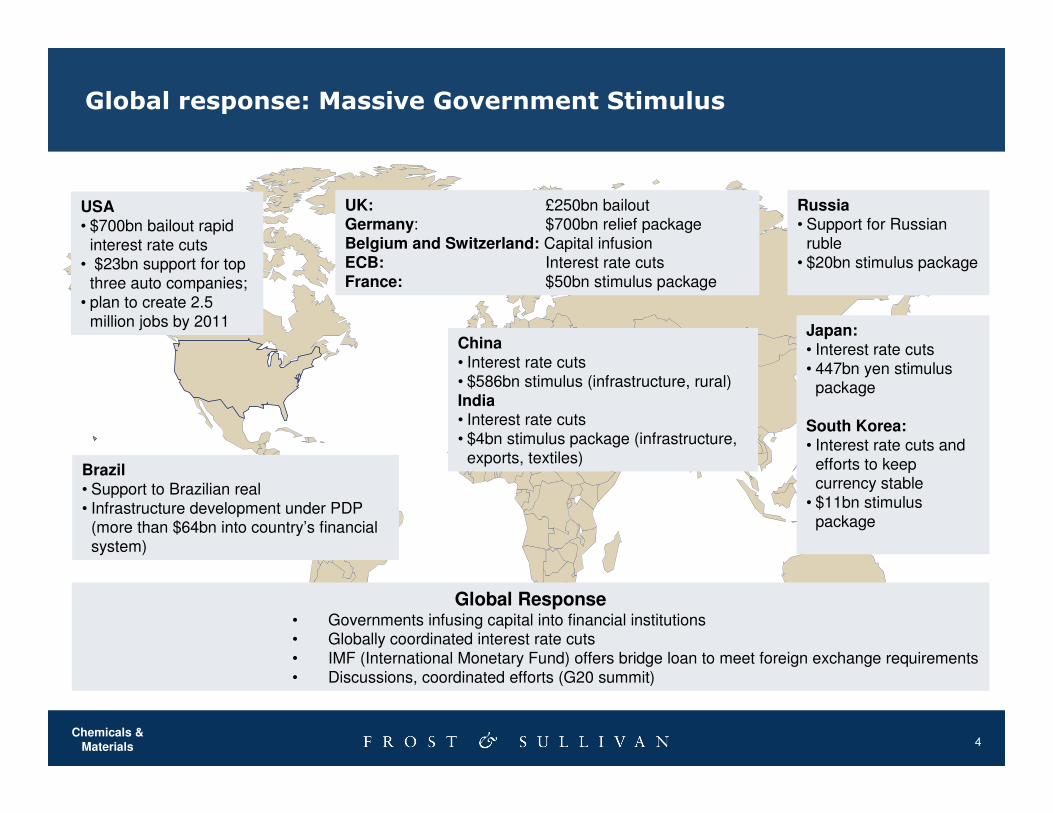

Global response: Massive Government Stimulus

China• Interest rate cuts • $586bn stimulus (infrastructure, rural)India• Interest rate cuts • $4bn stimulus package (infrastructure,

exports, textiles)

Global Response• Governments infusing capital into financial institutions• Globally coordinated interest rate cuts • IMF (International Monetary Fund) offers bridge loan to meet foreign exchange requirements• Discussions, coordinated efforts (G20 summit)

Brazil• Support to Brazilian real• Infrastructure development under PDP

(more than $64bn into country’s financial system)

USA• $700bn bailout rapid

interest rate cuts• $23bn support for top

three auto companies; • plan to create 2.5

million jobs by 2011

UK: £250bn bailoutGermany: $700bn relief packageBelgium and Switzerland: Capital infusionECB: Interest rate cutsFrance: $50bn stimulus package

Japan:• Interest rate cuts• 447bn yen stimulus

package

South Korea:• Interest rate cuts and

efforts to keep currency stable

• $11bn stimulus package

Russia• Support for Russian

ruble• $20bn stimulus package

5<N5AA-F1>

Mega Drivers for Rebound

� Positive economic news around the world; unprecedented focus worldwide on addressing the

economic situation

� Fastest government response in history, primarily driven by massive government fiscal stimulus

package

� New U.S. Government/Obama’s economic growth plan focuses on creating employment

through investments in infrastructure, renewable energy, broadband, and medical technology;

infrastructure alone will create 2 million jobs

� Decline in commodity and oil prices leading to a tax break stimulus in U.S.

� Easing of inflationary and liquidity pressures

� Strong demand from emerging nations will be a factor in reviving the global economy

� Smart money is coming back to the market, with stock exchanges at historic low PE ratios

� “Fear fatigue” and rebound in confidence

6<N5AA-F1>

Growth Imperative in a Weak Economy

Growth investment optimization is paramount during tough economic times

Need to invest wisely is more critical now than ever before

100% focus on cut backs and retrenchments increases risk of failure

Relative growth is as important as absolute growth

Need for more metrics, with greater frequency and accuracy

Risk of inaction greater than risk of action

Revitalizing your growth initiatives at this time

makes sense

�strategically – be well positioned for growth

when the economy turns around

�competitively – be opportunistic while your

competition is busy retrenching

7<N5AA-F1>

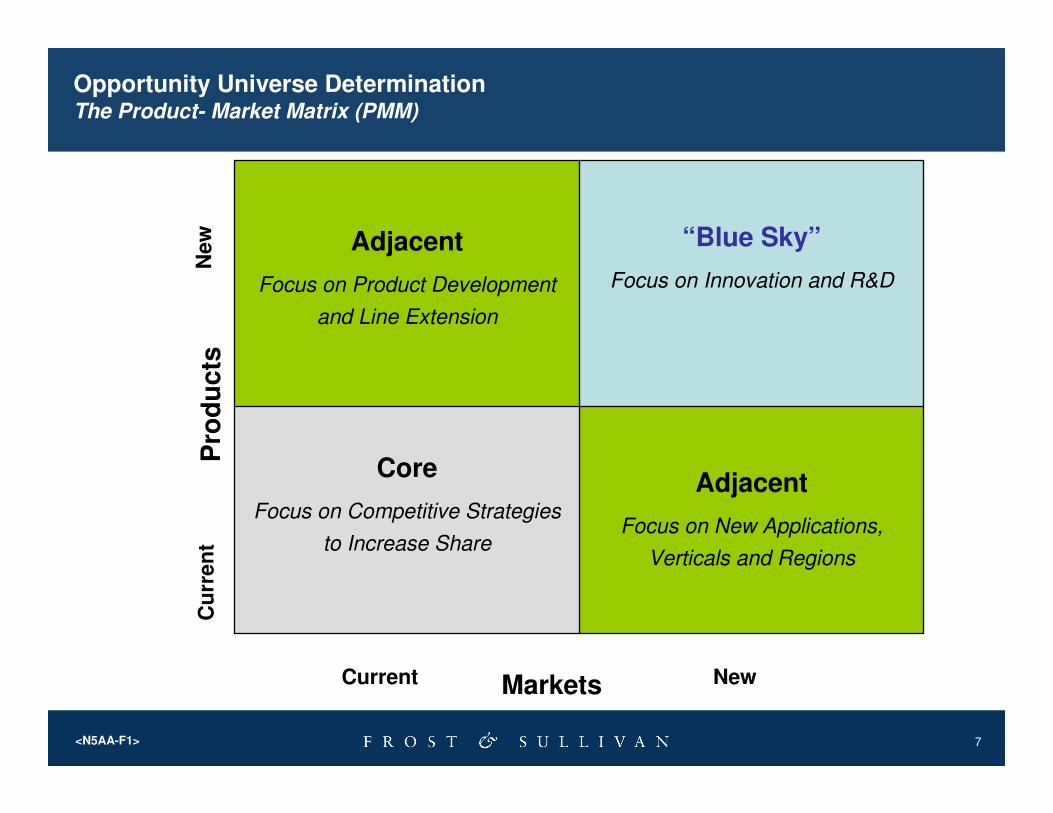

Adjacent

Focus on New Applications,

Verticals and Regions

Core

Focus on Competitive Strategies

to Increase Share

“Blue Sky”

Focus on Innovation and R&D

Adjacent

Focus on Product Development

and Line Extension

Pro

du

cts

New

Cu

rren

t

NewCurrent Markets

Opportunity Universe DeterminationThe Product- Market Matrix (PMM)

8<N5AA-F1>

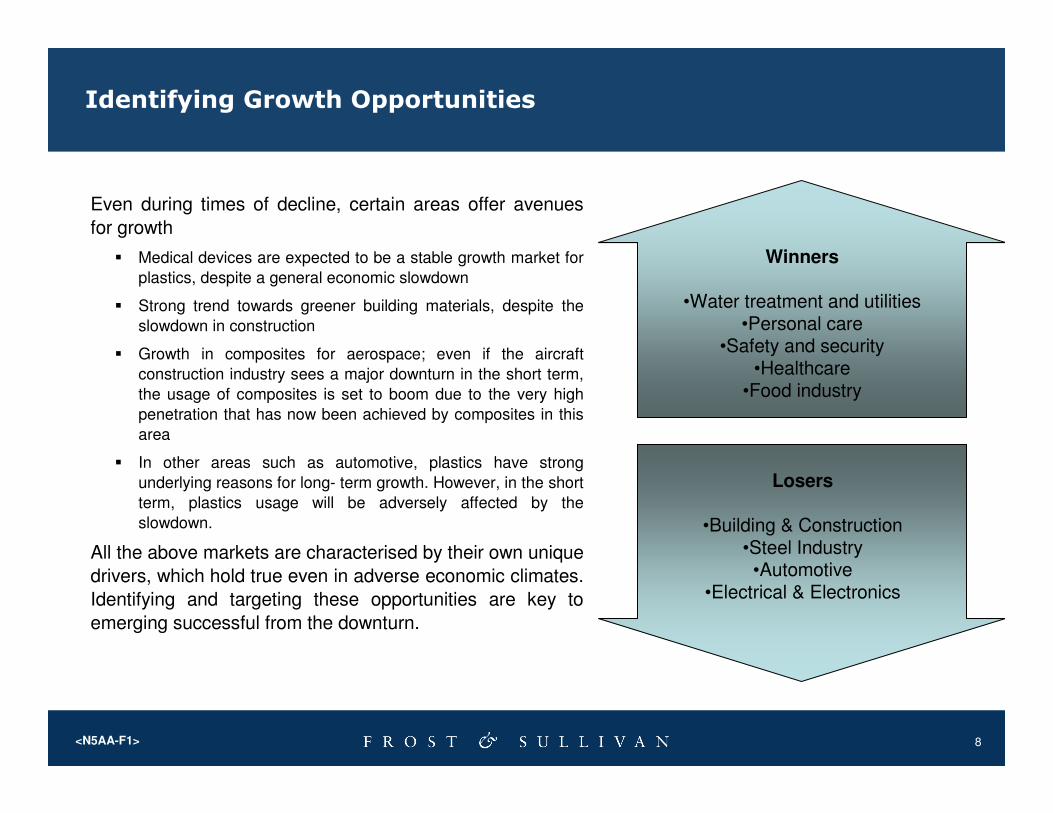

Identifying Growth Opportunities

Even during times of decline, certain areas offer avenues

for growth

� Medical devices are expected to be a stable growth market for

plastics, despite a general economic slowdown

� Strong trend towards greener building materials, despite the

slowdown in construction

� Growth in composites for aerospace; even if the aircraft

construction industry sees a major downturn in the short term,

the usage of composites is set to boom due to the very high

penetration that has now been achieved by composites in this

area

� In other areas such as automotive, plastics have strong

underlying reasons for long- term growth. However, in the short

term, plastics usage will be adversely affected by the

slowdown.

All the above markets are characterised by their own unique

drivers, which hold true even in adverse economic climates.

Identifying and targeting these opportunities are key to

emerging successful from the downturn.

Winners

•Water treatment and utilities•Personal care

•Safety and security•Healthcare

•Food industry

Losers

•Building & Construction•Steel Industry•Automotive

•Electrical & Electronics

9<N5AA-F1>

Sporting & Recreational Goods

Sporting & Recreational Goods

• Tennis Racquet Frames

• Bicycle Frames

• Fishing Goods

• Firearms

• Golf Club Heads

Motor Vehicles &

Engines

Motor Vehicles &

Engines

• Connecting Rods

• Valve Springs

• Intake valves

• Turbocharge impellers

• Turbo Exhaust Systems

MedicalMedical

• Dental Implants

• Crutches

• Wheelchair Frames

• Optical Devices

• Orthopedic Prosthetics

Energy/PowerEnergy/Power

• Steam Turbines

• Power Plan Heat Exchangers

• Superconducting Power

• Down Hole Oil/Gas Drilling

Loggers

• Gas turbine cooler compressor

• Reactor Vessels

• Process Vessels

• Piping

• Heat Exchangers

• Tanks

Chemical Process Industries

Chemical Process Industries

Consumer GoodsConsumer Goods

• Wristwatches

• Jewellery

• Body Piercings

• Mobile Cases

• Earrings

Growth Opportunity UniverseCase Study: Advanced/Specialty Metals

10<N5AA-F1>

Is the right time for growth

opportunities within the chemicals

sector?

Opportunities in the Chemicals Industry

Amidst fiscal challenges, credit crunch and contraction of consumer markets, growth opportunities exist for the chemicals industry and are based on global trends

Credit Crunch

Contraction

Fiscal

Challenges

Green Chemicals

Renewable Sourcing & Feedstock

Logistics and Supply Chain Acquisitions

Food & Beverage Geographic Regions – Russia, CEE

Growth in Profits

11<N5AA-F1>

Supply chain management

Vertical integration is a key theme

• This includes both backwards integration and

gaining greater downstream visibility

• Examples of downstream visibility include:

• additive suppliers taking a direct interest in the

end-markets which use the formulated coatings

or compounded plastics that contain their

additives

• BASF promoting the importance of its products

through TV and newspaper adverts

Strategic sourcing is another key aspect of supply chain

management.

• Frost & Sullivan has identified this as a key

emerging theme across many industries

• Companies are taking a more strategic view of

sourcing, for example by analysing other end-

markets that use the same raw materials to gauge

future availability

How can we manage our sourcing?

How can we manage the way in which our products are used

downstream?

12

Examples of Strategic Sourcing in the Chemical Industry

DSM

� Global sourcing department positioned to fully leverage spend, resources, capabilities and best practices

� Regional representation in Europe, America and Asia-Pacific, allowing DSM to utilize local knowledge to source effectively

� DSM’s strategy is to ensure creation of maximum value as an integral part of the business strategy

DSM

� Global sourcing department positioned to fully leverage spend, resources, capabilities and best practices

� Regional representation in Europe, America and Asia-Pacific, allowing DSM to utilize local knowledge to source effectively

� DSM’s strategy is to ensure creation of maximum value as an integral part of the business strategy

Bayer

� Global sourcing changes them from a good customer to a top account for suppliers, leading to better service (deliveries are on time, problems resolved quickly) which in turn leads to better service for Bayer’s customers

� Global procurement network allows Bayer to leverage spend and ideas, and to identify new suppliers

� Co-ordination of procurement efforts is vital to leverage larger volumes and improve logistics

Bayer

� Global sourcing changes them from a good customer to a top account for suppliers, leading to better service (deliveries are on time, problems resolved quickly) which in turn leads to better service for Bayer’s customers

� Global procurement network allows Bayer to leverage spend and ideas, and to identify new suppliers

� Co-ordination of procurement efforts is vital to leverage larger volumes and improve logistics

Companies have pursued integration with strategic sourcing partners through mergers, acquisitions and joint ventures

13

Mergers and Acquisitions –The definite trend in the chemicals

industry

� At the current challenging economic and financial environment low share prices of chemical companies can instigate hostile takeovers by competitors with available cash

� Private Equity firms are also involved in fund raising and strategic acquisition of chemical companies on a global basis

� Less risky approach to mergers and acquisitions is the bolt-on acquisitions that assist chemical companies to build product portfolios and expand their geographic reach

Improvement of Market Position

Chemical Company

Merger

Large Scale Acquisition

Bolt-on Acquisition

14<N5AA-F1>

M&A Deals by Segment

Protection Equipm ent M ateria ls PFE

Pharm aceutical Excipients PE

Fuel Additives FA

H igh Perform ance Polym ers HPP

Construction Chem icals CC

Electronic Chem icals ECBiofuels B io

Catalyst Cat

Rubber Chem icals RC

Electrical & E lectronic M ateria ls E&E

Lubricants & G reases L&G

Industria l / Specia lty G ases G as

Elastom ers E las

O ilfie ld & M ining Chem icals O &M C

Textile Additives TA

Crop Protection Chem icals CPCW ater treatm ent Chem icals W TC

Pulp & Paper P&P

Plastic Additives PA

Packaging Pack

Inks & Colors (Excepting Food) I&C

Construction M ateria ls CM

Foods & Beverages F&B

Paint and Coating Additives P&CA

Engineering Polym ers EP

Personal Care Chem icals and Household Chem icals PCC&HCAdhesives & Sealants A&S

Agricultural Chem icals & Fertilizers AC&F

APIs & Interm ediates API

Paints & Coatings P&C Com m odity Polym ers CP

8

2734

5160 61 64 65 67 71 71 77 79 83

109 114126

142151 156

172 173 176

192 197208

218

240253

283 288

0

50

100

150

200

250

300

PF

E

PE

FA

HP

P

CC

EC

Bio

Cat

RC

E&

E

L&

G

Gas

Ela

s

O&

MC

TA

CP

C

WT

C

P&

P

PA

Pa

ck

I&C

CM

F&

B

P&

CA

EP

PC

C&

HC

A&

S

AC

&F

AP

I

P&

C

CP

S e gm e nts

Deals

(x)

15<N5AA-F1>

Deals by Time period- Yearly Classification

564

399

349

321

347

469489

468

346

260

(29.3)

(8.0)

4.3

(4.3)

(26.1)

35.2

8.1

(12.5)

250

300

350

400

450

500

550

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 May 2009

Quarters

Deals

(x)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

Gro

wth

(%

)

Deals by Year Year over Year Growth

16<N5AA-F1>

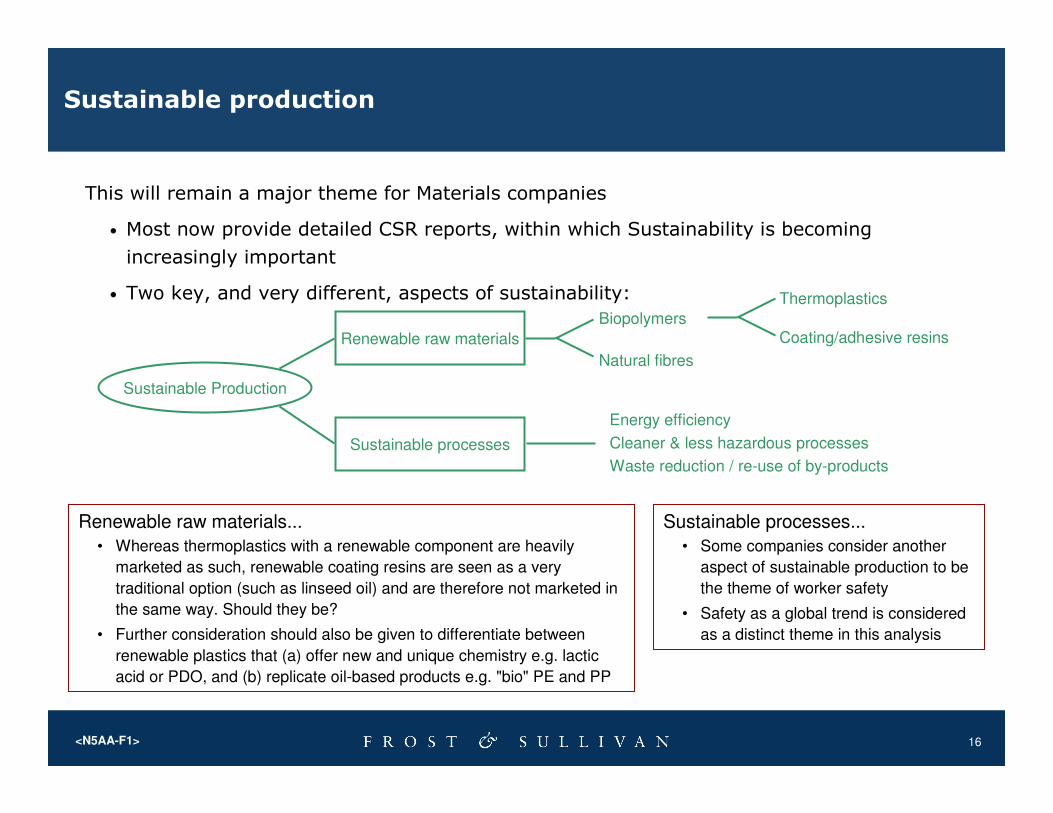

Sustainable production

This will remain a major theme for Materials companies

• Most now provide detailed CSR reports, within which Sustainability is becoming

increasingly important

• Two key, and very different, aspects of sustainability:

Sustainable Production

Renewable raw materials

Sustainable processes

Biopolymers

Natural fibres

Thermoplastics

Coating/adhesive resins

Energy efficiency

Cleaner & less hazardous processes

Waste reduction / re-use of by-products

Renewable raw materials...

• Whereas thermoplastics with a renewable component are heavily

marketed as such, renewable coating resins are seen as a very

traditional option (such as linseed oil) and are therefore not marketed in

the same way. Should they be?

• Further consideration should also be given to differentiate between

renewable plastics that (a) offer new and unique chemistry e.g. lactic

acid or PDO, and (b) replicate oil-based products e.g. "bio" PE and PP

Sustainable processes...

• Some companies consider another

aspect of sustainable production to be

the theme of worker safety

• Safety as a global trend is considered

as a distinct theme in this analysis

17<N5AA-F1>

Green Chemicals - Biobased Sourcing is Alternative to Naphtha Stream

Cellulose/

LignoCellulose

Rapseed,

Soyseed

Production on pilot scale

Current bulk productions

Research Scale

Starch based polymers

Wheat

maize

potatoStarch

C5 and

C6

Sugars

Ethanol

Lactic Acid

3 HP

Succinic

acid

Sorbitol

Acrolein

Allyl alcohol

1,3 Propanediol

Epichlorohydrin

1,2 propanediol

PBS

THF

1,4 Butanediol

1,2 Propanediol

Acrylic acid

Chiral compounds

Poly lactic acid

1,3 Propanediol

Vegetable OilBio Diesel

Glycerol

Natural oil

Polyols

(NOP)

CO2

Acrylic acid

ethylene Vinyl chloride

Sugar

beet,

sugarcane

Levullinic acid

Ethanol

MeMbl

Polyether polyols

Glycols

Isosorbide

Ascorbic acid

polymer

Polyhydroxyalkanoates

Cellulose ethers,

Cellulose esters

and Viscose Fibres

Polyurethanes

Epoxy resins

C5

and

C6

Sugars

Isoprene Polyisopropene

Cellulose/

LignoCellulose

Rapseed,

Soyseed

Production on pilot scale

Current bulk productions

Research Scale

Starch based polymers

Wheat

maize

potatoStarch

C5 and

C6

Sugars

Ethanol

Lactic Acid

3 HP

Succinic

acid

Sorbitol

Acrolein

Allyl alcohol

1,3 Propanediol

Epichlorohydrin

1,2 propanediol

PBS

THF

1,4 Butanediol

1,2 Propanediol

Acrylic acid

Chiral compounds

Poly lactic acid

1,3 Propanediol

Vegetable OilBio Diesel

Glycerol

Natural oil

Polyols

(NOP)

CO2

Acrylic acid

ethylene Vinyl chloride

Sugar

beet,

sugarcane

Levullinic acid

Ethanol

MeMbl

Polyether polyols

Glycols

Isosorbide

Ascorbic acid

polymer

Polyhydroxyalkanoates

Cellulose ethers,

Cellulose esters

and Viscose Fibres

Polyurethanes

Epoxy resins

C5

and

C6

Sugars

Isoprene Polyisopropene

Cellulose/

LignoCellulose

Rapseed,

Soyseed

Production on pilot scale

Current bulk productions

Research Scale

Production on pilot scale

Current bulk productions

Research Scale

Starch based polymers

Wheat

maize

potatoStarch

C5 and

C6

Sugars

Ethanol

Lactic Acid

3 HP

Succinic

acid

Sorbitol

Acrolein

Allyl alcohol

1,3 Propanediol

Epichlorohydrin

1,2 propanediol

PBS

THF

1,4 Butanediol

1,2 Propanediol

Acrylic acid

Chiral compounds

Poly lactic acid

1,3 Propanediol

Vegetable OilBio Diesel

Glycerol

Natural oil

Polyols

(NOP)

CO2

Acrylic acid

ethylene Vinyl chloride

Sugar

beet,

sugarcane

Levullinic acid

Ethanol

MeMbl

Polyether polyols

Glycols

Isosorbide

Ascorbic acid

polymer

Polyhydroxyalkanoates

Cellulose ethers,

Cellulose esters

and Viscose Fibres

Polyurethanes

Epoxy resins

C5

and

C6

Sugars

Isoprene Polyisopropene

Source: Frost & Sullivan

18<N5AA-F1>

Focus on Emerging Markets

Brazil

� Latin American hub for bioethanol and exports to neighboring nations

� Increasing focus in oil and gas exploration – restructure in the state petrochemicals company

� Recognized potential for industrial growth

� Expansion of multinational companies

India

� Highly skilled labor and low costs –attractive market for partnerships

� Agrochemicals companies with global presence

� Growing affluent middle-class with spending power

� Weak IP protection – a concern

China

� Manufacturing hub

� Increasing competency in R&D and high-value added products

� Problems with quality control and corrupt officials

� Improved IP laws – attractive climate for chemicals companies

Japan

� Innovative capability and well developed industry

� More active involvement in the Western financial institutions

USA

� Increasing consolidation in the chemicals industry

� More active involvement of the federal agencies in the regulation of chemicals

Western Europe

� Mature market and increasing consolidation in the chemicals industry

� REACh legislative framework divides the industry

Africa

� Growing construction industry

� Agrochemicals companies with global presence

Central and Eastern Europe

� Growing acceptance of “Western” type lifestyle

� Increasing private healthcare expenditure

� Russia, Poland, Czech Republic and Hungary present healthy R&D opportunities

Middle East

� Geopolitical challenges

� Vast supply of feedstock

� Growing participation in the Western financial institutions and companies

19<N5AA-F1>

Best Practices in the Uncertain Times

Merquinsa

Situation

� Merquinsa is a producer of thermoplastic polyurethanes and operates in a heavily

competitive market dominated by BASF and Bayer.

Action

� To differentiate itself in such a concentrated market, Merquinsa has focused on R&D and

has developed the first-ever TPU from renewable resources to compete against

conventional TPUs based on petroleum feedstock.

Result

� This will help the company carve out its own niche in the market, and will also position

itself firmly for future growth, as environmentally friendly products are the need of the

hour in the materials industry.

� This will also enable to company to faster than the industry average growth rates.

20<N5AA-F1>

LyondellBasell

Situation

� LyondellBasell is an example of a company facing the brunt of the current economic downturn, facing

slackening demand for its polymers in many of its key end user segments

Action

� The company is now restructuring its businesses, and filed for voluntary bankruptcy protection in the

US in January, 2009

� Nevertheless, LyondellBasell is also making changes to its operations in key end user segments. For

example, it is now expanding its footprint worldwide in in the medical devices area, setting up a global

team catering to this segment. This will enable it to supply its customers with local production units

and also spread its regulatory know-how and resources across a wider geographic area.

� Through this globalisation, LyondellBasell is also generating synergies from the merger of Lyondell

and Basell, merging the upstream capabilities of the latter with the immense industry experience of

the latter.

Result

� Through the effective integration of Lyondell and Basell, and the globalisation of its healthcare

operations, LyondellBasell has created a strong value proposition for itself in the healthcare arena.

� Through these measures the company has ensured that it will emerge stronger out of the recession,

when demand for its products picks up again.

Best Practices in the Uncertain Times

21<N5AA-F1>

What Will Catalyze the Turnaround?Food & Beverage Ingredients

• Growing interest and push towards Health & Wellness by consumers. Increased

usage is indicative of many consumers becoming more health and wellness conscious:

nearly 40% of US consumers feel consumption of functional foods and beverages is very

important to maintaining a healthy lifestyle.

• New product introductions. The number of new organic beverages free from chemical

additives, preservatives and pesticides nearly tripled in the last couple of years. To meet this

growing need, functional beverage manufacturers are adding new products on a regular

basis. This is likely to continue in 2009.

• Greater awareness of functional benefits of food ingredients on cognitive/brain, bone,

cardiac, digestive health, and weight management.

• Promotion of nutrients that are difficult to incorporate into a diet. Omega 3 fatty acids

have received a great deal of attention due to their importance in brain development and

heart health. More dietary supplements will be formulated with ingredients such as

glucosamine and chondroitin for healthy joints targeted towards the aging population.

22<N5AA-F1>

What Will Catalyze the Turnaround?Food & Beverage Ingredients

• Demand for alternative delivery formats of dietary supplements like fruit juices, yogurts,

cereal bars and chewing gum among young and mid-age adults will further boost health &

wellness sector growth.

• Functional foods sales are forecast to increase by more than 40% from 2007-2012 driven

by an increase in product availability and consumer usage. Cardiovascular health is the most

popular functional food claim, yet products for the brain/nervous system and for the immune

system are also emerging.

• Functional beverage sales are forecast to rise approximately 30-35% during 2007-2012 as

consumers seek additional nutrition sources to compensate for the lack of foods that address

health-specific problems.

23

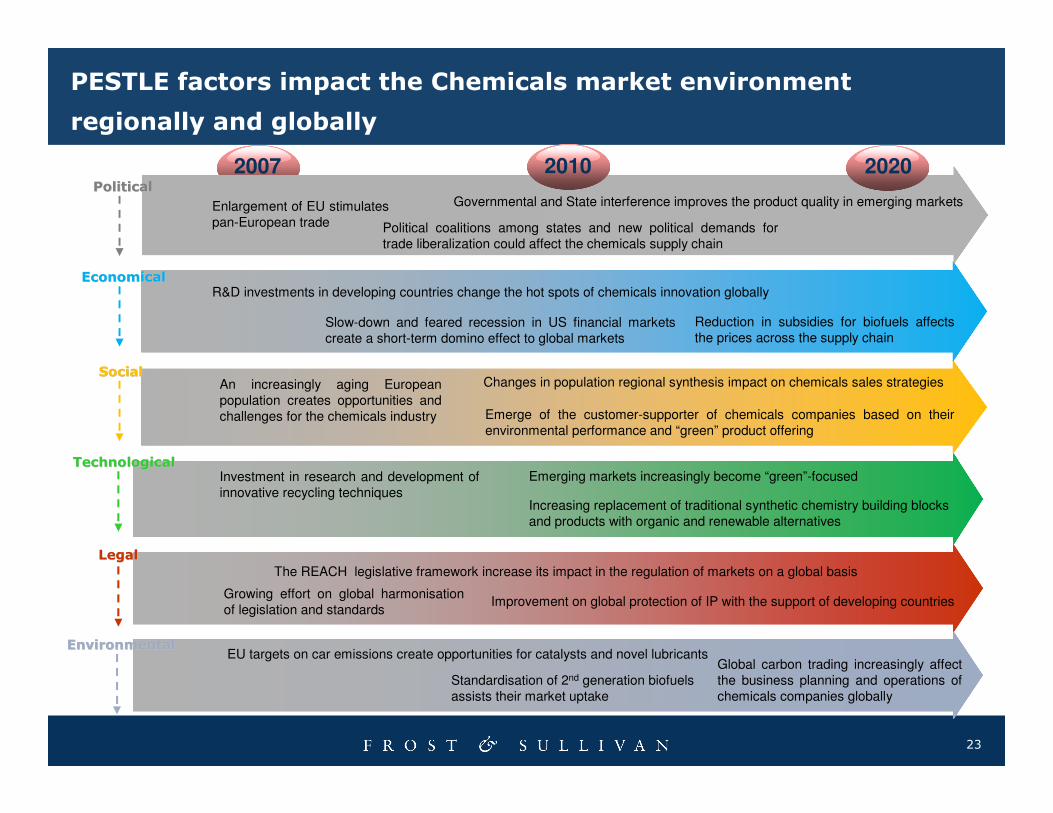

PESTLE factors impact the Chemicals market environment

regionally and globally

2007

Investment in research and development of innovative recycling techniques

Increasing replacement of traditional synthetic chemistry building blocks and products with organic and renewable alternatives

Governmental and State interference improves the product quality in emerging markets

Political coalitions among states and new political demands for trade liberalization could affect the chemicals supply chain

Reduction in subsidies for biofuels affects the prices across the supply chain

Slow-down and feared recession in US financial markets create a short-term domino effect to global markets

Enlargement of EU stimulates pan-European trade

R&D investments in developing countries change the hot spots of chemicals innovation globally

An increasingly aging European population creates opportunities and challenges for the chemicals industry Emerge of the customer-supporter of chemicals companies based on their

environmental performance and “green” product offering

Changes in population regional synthesis impact on chemicals sales strategies

TechnologicalTechnological

SocialSocial

EconomicalEconomical

PoliticalPolitical

2010 2020

Emerging markets increasingly become “green”-focused

Growing effort on global harmonisation of legislation and standards

Improvement on global protection of IP with the support of developing countries

LegalLegal

EU targets on car emissions create opportunities for catalysts and novel lubricants

Standardisation of 2nd generation biofuels assists their market uptake

EnvironmentalEnvironmental

Global carbon trading increasingly affect the business planning and operations of chemicals companies globally

The REACH legislative framework increase its impact in the regulation of markets on a global basis

24

Chemical Trends Impact

Customer-centric product development

2010 20202015

Power Customer

Major Trend

Biorenewables

Recycling

Super-Chem Companies

F/B Integration

Environmental Legislation

Internet Auctions

White Biotechnology

By-products Management

Logistics Excellence

1

2

3

4

5

6

7

8

9

10

Support of companies which usesustainable resources, recycle

Customers increasingly gainaccess to chemicals information

Crops companies get involved more in the chemicals industry Reduction in subsidies

Self-sustained industry

Increased consolidationRise of Mega chemical companies

in China, ME & Russia

10 Super-giant chemicalcompanies globally

Chemical companies pursuebackwards integration

Voluntary publishing of carbon footprints for products and companies

Increased use of auction sitesfor commodity chemicals

Increases in oil and raw materialsprices drive massive logistics costs

Sustainability audit of companiesand trail accounting of products

REACh

Glocalisation – Global companiesresource locally

Recycling an economic, not moral, decisionQuality problems arise

R&D of new and better recycling techniques

Chemical companies leverageand share distribution expertise

First commercial plants successful

Companies in developing countries use itas an easy market entry point

Elimination of waste by 70%

Replacement of traditional syntheticchemistry with organic alternatives

Increasing investment and R&Dinto white biotechnology

Agro companies become forward integrated One-stop shop for entire

supply chain

Chemicals “e-bay”

Increased utilisation of by-productsas feedstock

Research into potential usesfor waste and by-products