3g rollout status rapport om 3gutvecklingen i europa pts_er_2002_22 oktober 2002

DESCRIPTION

3g rolloutTRANSCRIPT

REPORT NUMBER PTS-ER-2002:22 ISSN 1650-9862

3G rollout status Version 1.2 4 October 2002 Prepared by Northstream for The Swedish National Post and Telecom Agency (Post- och Telestyrelsen) Northstream AB www.northstream.se +46 8 564 84 800

3G rollout status 2 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Executive Summary

This report provides a descriptive and analytical overview of the status of 3G rollout in the European Union and Norway. It focuses on potential modifications of licence distribution and conditions and the changing market outlook for 3G services in Europe. The European Commission and national regulators share powers of regulation over the mobile telecommunications sector in Europe. While many regulators have made no alterations, at national regulator level licence conditions that have been altered/clarified include timing of service launch, timing of coverage milestones, network sharing, extension of the licence period and revision of payments for fees associated with the licence. These indicate there is some limited flexibility to the industry, and a slight change of regulatory focus from market liberalisation to 3G market facilitation. Regarding availability of equipment, potential showstoppers from a network functionality perspective include: Plain software stability of some of the nodes required for offering reasonable

service functionality. Interoperability between terminals and infrastructure. Interoperability between network nodes in case of multiple vendors. Handover and cell reselection between 2G and 3G.

Availability of handsets is strongly linked to interoperability testing of handsets on networks. Access to handsets is not straightforward for operators, and possibly less so for those in less influential markets. Operators are more likely to cite handset delays than network delays, in order to maintain their relationship with their equipment vendor. However, actual reasons for delay rest on a balance between handset availability and network functionality. In Europe the number of operators has generally increased in comparison to the 2G market situation, but not to the extent that was anticipated at the time of 3G licensing. There is a Europe-wide trend for fewer 3G operators than originally anticipated. Operator announcements show that 3G is delayed across Europe; operators expect initial launches in mid-2003. Some operators indicate ‘soft launches’, i.e. non-mass market launches, without major revenues at that stage. Multi-national operator groups tend to co-ordinate delays. Regarding operators’ financial situation - with reduced credit ratings, and lower than anticipated profits, operators find that the 3G commitments they’ve previously committed to will require greater external financing, at a higher cost. This impacts their capacity to rollout networks. In the current European market the variety of services is lower than expected, with service development increasingly dependent on operators. This is reflected in changed industry expectations - revenue forecasts made in 2002 are approximately 25% lower than those made in 2001. Industry forecasts from 2001 to 2002 show a slower 2G /3G conversion pace than originally anticipated. Market take up is heavily dependent on handset and service availability. Incumbent operators are likely to be

3G rollout status 3 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

less impacted by the delay than new entrants, as new entrants still have to secure a customer base. In both Europe and Asia, there is little evidence of 3G-specific services. However in Korea, there are limited grounds for optimism. While there is little difference in the successful data services on 2.5G and 3G in these markets, there is an indication that more sophisticated handset features stimulate greater usage of these features, and greater revenues. In addition, these operators are growing the non-traffic based proportion of their data revenues. However, it is likely this is due to the large content communities that are in place, which European operators have not successfully stimulated. Finally, Northstream concludes that evidence confirms that the European 3G market is delayed, with many players waiting to roll-out ‘soft-launches’ in mid 2003. In addition that market has qualitatively changed. There are differences from original expectations in terms of competitors, services and revenues, which show that operators are operating in an unanticipated market environment.

3G rollout status 4 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Contents

1 INTRODUCTION ....................................................................... 6

2 3G LICENSING – STATUS AND CHANGES.................................. 6

2.1 European Commission activities .............................................................................6

2.2 Service launch according to licence requirements ...............................................7

2.3 Coverage requirement ...............................................................................................9

2.4 Network sharing obligation and potential ..........................................................15

2.5 Other ...........................................................................................................................20 2.5.1 Some operator interest in greater flexibility for transfer of licence ............20 2.5.2 Spectrum trading ...............................................................................................20 2.5.3 Licence period extended by some national regulators.................................21 2.5.4 Fees/price have been altered ...........................................................................22

3 TECHNOLOGY STATUS AND CHANGES .................................... 22

3.1 Handset aspects.........................................................................................................22

3.2 Network functionality .............................................................................................25

4 3G ROLLOUT STATUS AND PLANS .......................................... 29

4.1 Effective no. of 3G operators ..................................................................................29

4.2 3G rollout and launch status ..................................................................................31

4.3 Deployment aspects .................................................................................................35 4.3.1 Network Sharing................................................................................................35 4.3.2 National Roaming..............................................................................................37

5 MARKET STATUS AND EVOLUTION ......................................... 38

5.1 Service aspects...........................................................................................................38

5.2 Revenue and profitability.......................................................................................39

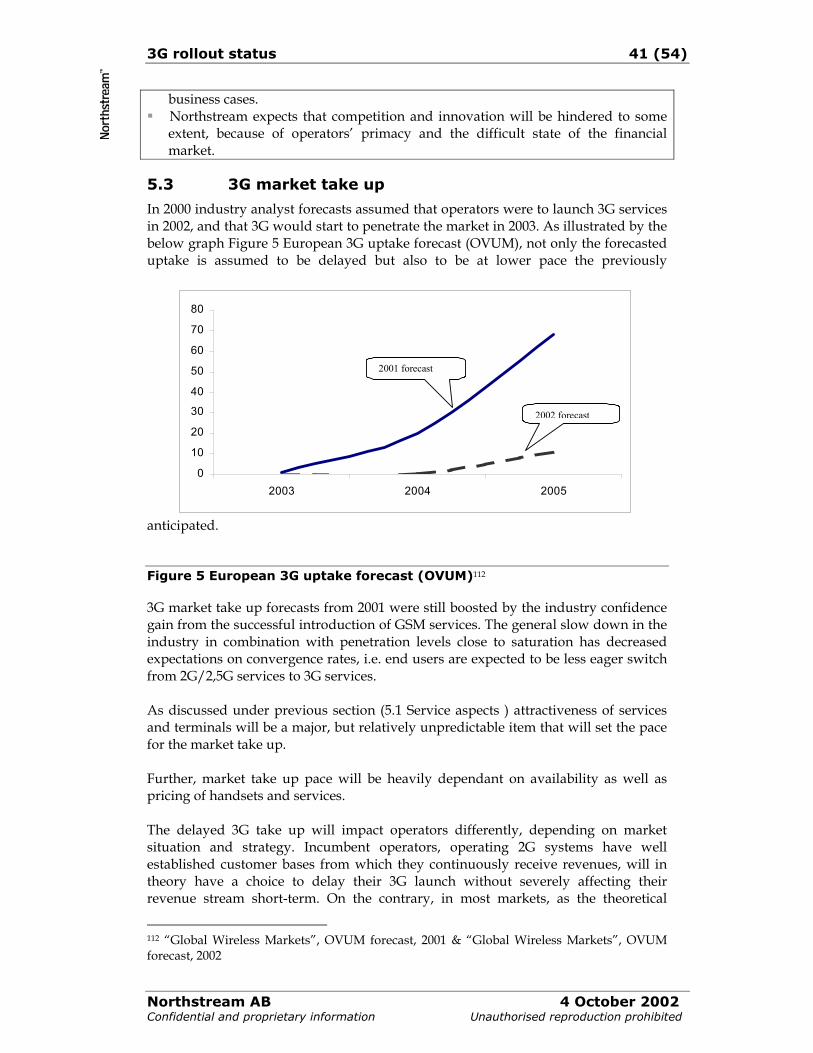

5.3 3G market take up ....................................................................................................41

6 FINANCIAL SITUATION.......................................................... 42

7 3G IN JAPAN AND KOREA....................................................... 44

7.1 Operators....................................................................................................................44

3G rollout status 5 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

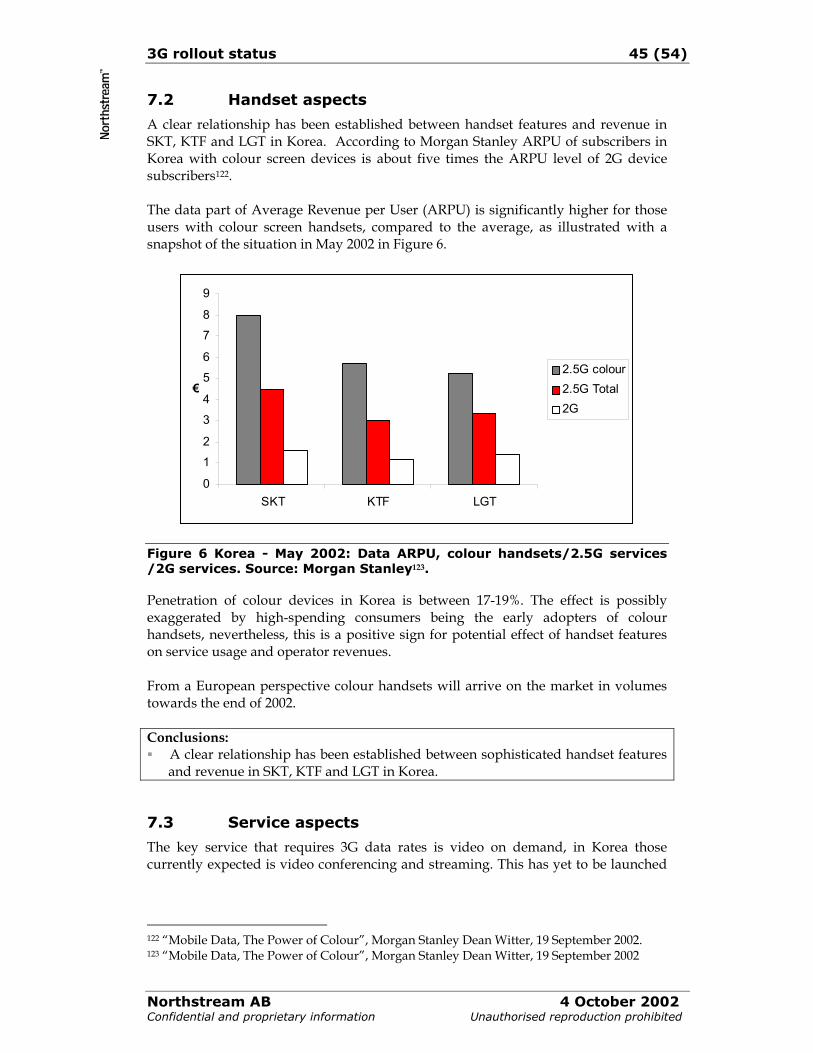

7.2 Handset aspects.........................................................................................................45

7.3 Service aspects...........................................................................................................45

8 CONCLUSIONS ....................................................................... 46

8.1 Slight change in regulatory perspective...............................................................46

8.2 The European 3G market is delayed.....................................................................47

8.3 Qualitative differences in the current 3G market outlook ...............................48

APPENDIX A: ............................................................................... 49

REFERENCES:............................................................................... 51

3G rollout status 6 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

1 Introduction

This report provides a descriptive and analytical overview of the status of 3G rollout in the European Union and Norway. It focuses on potential modifications of licence distribution and conditions and the changing market outlook for 3G services in Europe. Section 2 describes the changes or potential for change in 3G licence distribution and conditions from a regulatory perspective. Section 3 outlines status of the WCDMA technology from a handset and network functionality perspective. The outcome of the licensing process is described at Section 4, and outlines reasons cited by operators for delays. How the changed environment for 3G in Europe will impact expected market take up is outlined at Section 5. Section 6 describes how the current financial situation of operators can reasonably be said to impact the rollout of 3G. In response to the key issues raised in the European market outlook at Section 5, Section 7 highlights some relevant aspects of 3G in Japan and South Korea.

2 3G Licensing – status and changes

Section 2.1 outlines the EU level activities that have impacted the mobile communications sector. Sections 2.2 to 2.5 focus on the changes to 3G licence conditions laid down by regulators in the European Union and Norway. These sections also highlight activities on behalf of the regulator/government ministry that indicate movement based on a flexible interpretation/clarification of original requirements. By end September 2002, all EU member states are expected to have finalised the 3G licensing process.

2.1 European Commission activities

Two elements of the European Commission have an influential role in mobile communications, the Competition Directorate-General and the Information Society Directorate-General with responsibilities that include mobile communications. 1998 marked the movement of many European markets into a fully liberalised telecommunications market, and management of that transition has been the focus of much EU operations - by progressively liberalising a sector that had formerly consisted of many state monopolies, harmonising conditions between market players, and promotion of competition.1 The scope of the telecommunications area includes setting a licensing framework that is then implemented, in a variety of ways, by national telecommunication regulators. In a June 2002 study of the barriers to 3G rollout, the EU Commission outlined a supportive position to the mobile telecommunications industry, and recommended to national regulators that "the licensing conditions should not be changed because

1 “Europe’s liberalised telecommunications market – a guide to the rules of the game”, Commission staff working document. http://europa.eu.int/ISPO/infosoc/telecompolicy/en/userguide-en.pdf

3G rollout status 7 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

the sector is best served by a predictable environment"2, and that where changed they should be harmonised across the EU. Comments regarding potential changes include:

An acknowledgement that rollout obligations may need to be changed – on the basis of an open and public consultation.

Extension of licence duration is not viewed as having a short-term impact on rollout.

It believes that changes in fees could have an effect to make the business case unpredictable, and does not recommend changing at this time.

It acknowledges that network infrastructure sharing has resulted in the need for local regulatory clarification.

It should be noted that the status of this report is unclear, as a new report has been commissioned for December 2002. A recent study by McKinsey for the EU Commission, examined the impact of EU 3G licensing and recommended guiding principles for future licensing procedures.3 Industry comments on that report indicated that operators would like to see measures introduced to tackle the current 3G rollout situation, rather than purely focus on preparing for future licensing procedures4. Such comments are referred to under sections 2.2 – 2.5, where relevant. Conclusions: The European Commission’s Competition Directorate-General and Information

Society Directorate-General have powers of regulation over the mobile telecommunications sector.

There are some indications of an EU-level shift toward supporting the sector, a slight movement from the premier focus on promoting competition.

2.2 Service launch according to licence requirements

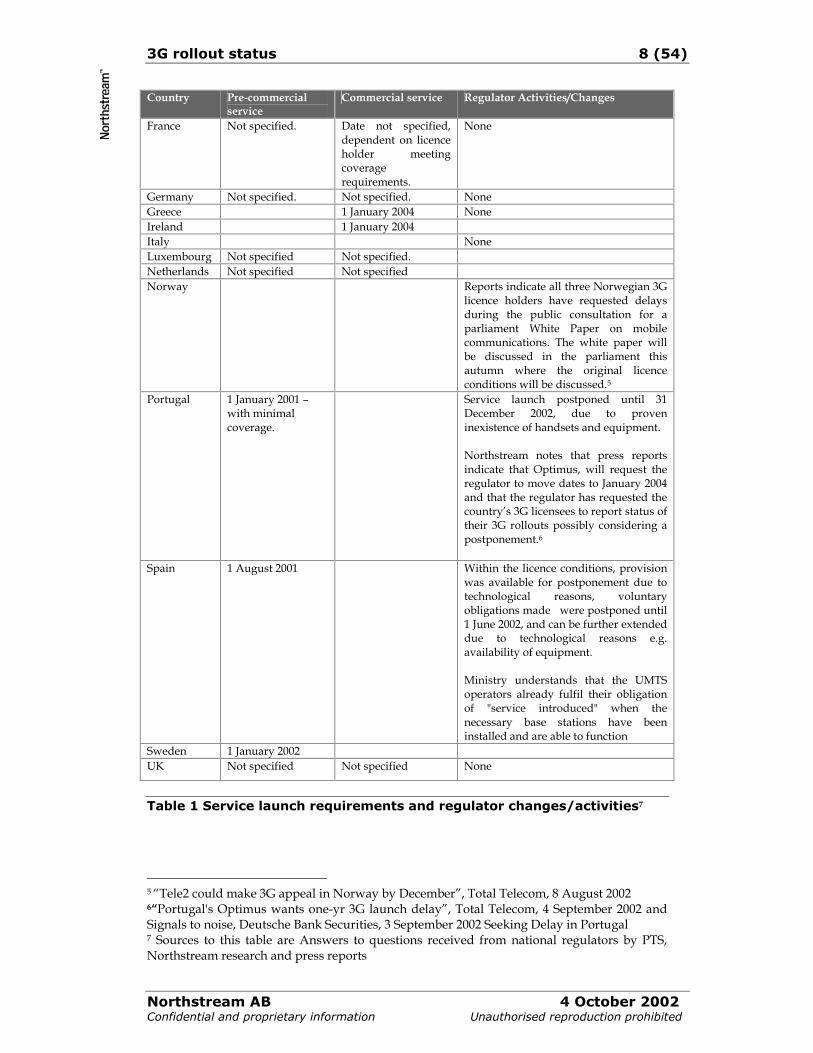

Table 1 summarises the service launch requirements from a regulatory perspective. It highlights changes that have been made to the original launch dates. Country Pre-commercial

service Commercial service Regulator Activities/Changes

Austria 31 December 2003 140kbit/s

None

Belgium 1 September 2002 Commercial opening and rollout time limits postponed by one year. Service launch: 1 September 2003. – 2.5yr from date of licence award.

Denmark Not specified Not specified None Finland 1 January 2002 Based on availability

of handsets. Date for operation in Åland moved by one year to 1 January 2003

2 ”Towards the Full Roll-Out of Third Generation Mobile Communications”, June 2002, Commission of the European Communities. 3 “Comparative Assessment of the Licensing Regimes for 3G Mobile Communications in the European Union and their Impact on the Mobile Communications Sector”, McKinsey report for European Commission Directorate-General Information Society, 25 June 2002 (“McKinsey”) 4 “Spectrum trading takes central stage”, Total Telecom, 18 September 2002

3G rollout status 8 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Country Pre-commercial service

Commercial service Regulator Activities/Changes

France Not specified. Date not specified, dependent on licence holder meeting coverage requirements.

None

Germany Not specified. Not specified. None Greece 1 January 2004 None Ireland 1 January 2004 Italy None Luxembourg Not specified Not specified. Netherlands Not specified Not specified Norway Reports indicate all three Norwegian 3G

licence holders have requested delays during the public consultation for a parliament White Paper on mobile communications. The white paper will be discussed in the parliament this autumn where the original licence conditions will be discussed.5

Portugal 1 January 2001 – with minimal coverage.

Service launch postponed until 31 December 2002, due to proven inexistence of handsets and equipment. Northstream notes that press reports indicate that Optimus, will request the regulator to move dates to January 2004 and that the regulator has requested the country’s 3G licensees to report status of their 3G rollouts possibly considering a postponement.6

Spain 1 August 2001 Within the licence conditions, provision was available for postponement due to technological reasons, voluntary obligations made were postponed until 1 June 2002, and can be further extended due to technological reasons e.g. availability of equipment. Ministry understands that the UMTS operators already fulfil their obligation of "service introduced" when the necessary base stations have been installed and are able to function

Sweden 1 January 2002 UK Not specified Not specified None

Table 1 Service launch requirements and regulator changes/activities7

5 “Tele2 could make 3G appeal in Norway by December”, Total Telecom, 8 August 2002 6“Portugal's Optimus wants one-yr 3G launch delay”, Total Telecom, 4 September 2002 and Signals to noise, Deutsche Bank Securities, 3 September 2002 Seeking Delay in Portugal 7 Sources to this table are Answers to questions received from national regulators by PTS, Northstream research and press reports

3G rollout status 9 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

As shown in Table 1 the dates defined in the licence requirements for service launch ranged in time, and in whether preliminary or commercial service dates were specified. Regulators will naturally wish to confirm if operators have met the requirements they have laid down. ‘Service launch’ may be defined in a number of ways, which permits regulators a degree of flexibility in determining if their requirements have been met. A regulator may wish to check the availability of the network to ensure that rollout is ongoing, rather than force an operator to demonstrate commercial availability of a service. In addition the definition of service launch may extend to provision of commercial services to subscribers. Some regulators/government ministries have responded to requests raised by operators for changes to the milestone dates. Looking at the market, it currently appears that where specific dates for a service launch have been set, and the time has already passed, either regulators have agreed to change the date (e.g. Belgium, Portugal, Spain) or a minimal, preliminary service ‘availability’ has been accepted as sufficient to meet pre-commercial availability requirements (e.g. Sweden, Finland). See also Section 2.3 for details of coverage requirements. In some cases facilities were in place within the original licence specification that would allow for extensions to originally specified deadlines e.g. if it can be established that handsets or equipment are unavailable – e.g. Spain, Finland. Therefore such altered dates, in some cases may not strictly be categorised as changes to the actual licence conditions, although they reflect movement from regulators in response to changes in the expectations of regulators and operators. Conclusions: Flexible definitions (if any) of ‘service launch’ enable operators still to comply

with licence requirements. Some regulators/ministries are agreeing to postponement of service launch dates

and seem reluctant to fail and penalise operators.

2.3 Coverage requirement

Table 2 summarises the licence requirements for population coverage, with a focus on changes in requirements. This allows for a like-with-like comparison across countries.

3G rollout status 10 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

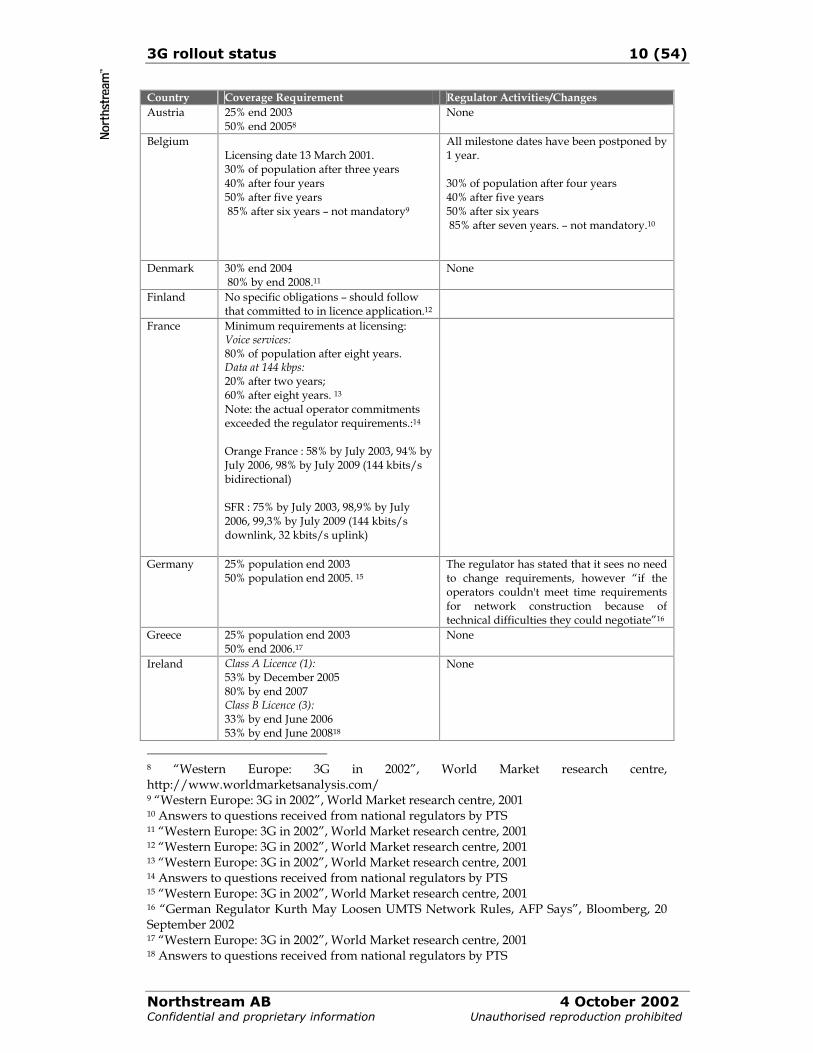

Country Coverage Requirement Regulator Activities/Changes Austria 25% end 2003

50% end 20058 None

Belgium Licensing date 13 March 2001. 30% of population after three years 40% after four years 50% after five years 85% after six years – not mandatory9

All milestone dates have been postponed by 1 year. 30% of population after four years 40% after five years 50% after six years 85% after seven years. – not mandatory.10

Denmark 30% end 2004 80% by end 2008.11

None

Finland No specific obligations – should follow that committed to in licence application.12

France Minimum requirements at licensing: Voice services: 80% of population after eight years. Data at 144 kbps: 20% after two years; 60% after eight years. 13 Note: the actual operator commitments exceeded the regulator requirements.:14 Orange France : 58% by July 2003, 94% by July 2006, 98% by July 2009 (144 kbits/s bidirectional) SFR : 75% by July 2003, 98,9% by July 2006, 99,3% by July 2009 (144 kbits/s downlink, 32 kbits/s uplink)

Germany 25% population end 2003 50% population end 2005. 15

The regulator has stated that it sees no need to change requirements, however “if the operators couldn't meet time requirements for network construction because of technical difficulties they could negotiate”16

Greece 25% population end 2003 50% end 2006.17

None

Ireland Class A Licence (1): 53% by December 2005 80% by end 2007 Class B Licence (3): 33% by end June 2006 53% by end June 200818

None

8 “Western Europe: 3G in 2002”, World Market research centre, http://www.worldmarketsanalysis.com/ 9 “Western Europe: 3G in 2002”, World Market research centre, 2001 10 Answers to questions received from national regulators by PTS 11 “Western Europe: 3G in 2002”, World Market research centre, 2001 12 “Western Europe: 3G in 2002”, World Market research centre, 2001 13 “Western Europe: 3G in 2002”, World Market research centre, 2001 14 Answers to questions received from national regulators by PTS 15 “Western Europe: 3G in 2002”, World Market research centre, 2001 16 “German Regulator Kurth May Loosen UMTS Network Rules, AFP Says”, Bloomberg, 20 September 2002 17 “Western Europe: 3G in 2002”, World Market research centre, 2001 18 Answers to questions received from national regulators by PTS

3G rollout status 11 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

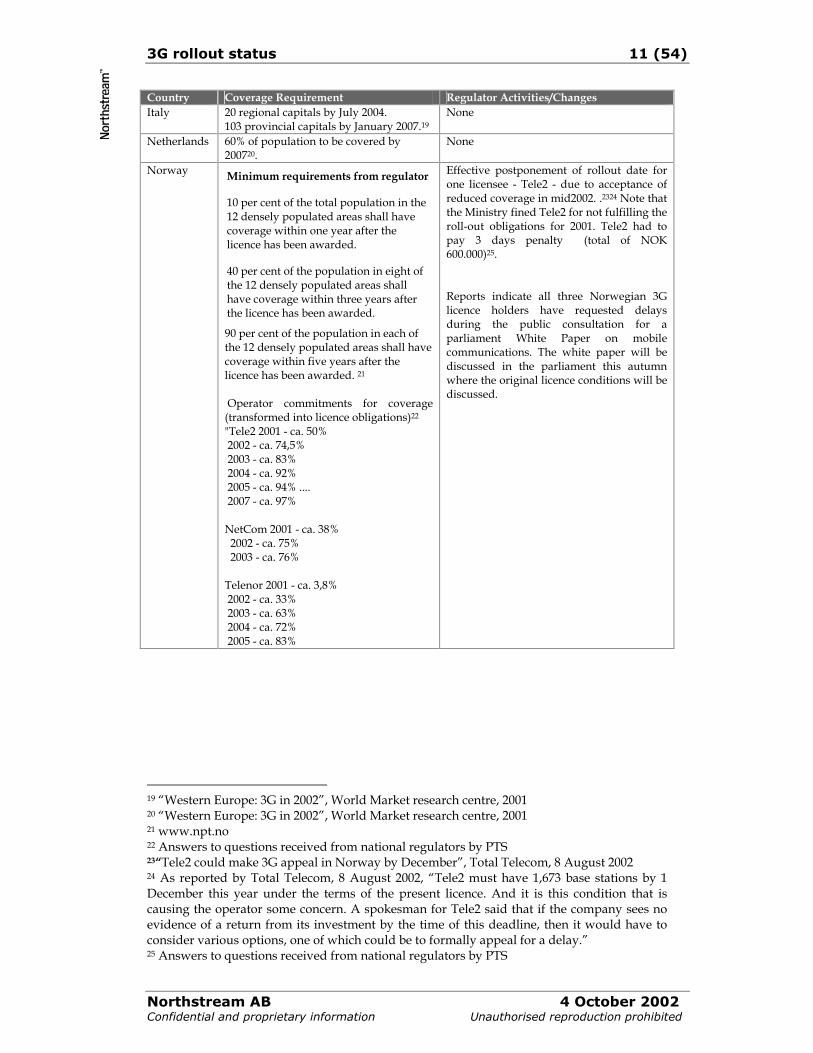

Country Coverage Requirement Regulator Activities/Changes Italy 20 regional capitals by July 2004.

103 provincial capitals by January 2007.19 None

Netherlands 60% of population to be covered by 200720.

None

Norway Minimum requirements from regulator

10 per cent of the total population in the 12 densely populated areas shall have coverage within one year after the licence has been awarded.

40 per cent of the population in eight of the 12 densely populated areas shall have coverage within three years after the licence has been awarded.

90 per cent of the population in each of the 12 densely populated areas shall have coverage within five years after the licence has been awarded. 21 Operator commitments for coverage (transformed into licence obligations)22 "Tele2 2001 - ca. 50% 2002 - ca. 74,5% 2003 - ca. 83% 2004 - ca. 92% 2005 - ca. 94% .... 2007 - ca. 97% NetCom 2001 - ca. 38% 2002 - ca. 75% 2003 - ca. 76% Telenor 2001 - ca. 3,8% 2002 - ca. 33% 2003 - ca. 63% 2004 - ca. 72% 2005 - ca. 83%

Effective postponement of rollout date for one licensee - Tele2 - due to acceptance of reduced coverage in mid2002. .2324 Note that the Ministry fined Tele2 for not fulfilling the roll-out obligations for 2001. Tele2 had to pay 3 days penalty (total of NOK 600.000)25. Reports indicate all three Norwegian 3G licence holders have requested delays during the public consultation for a parliament White Paper on mobile communications. The white paper will be discussed in the parliament this autumn where the original licence conditions will be discussed.

19 “Western Europe: 3G in 2002”, World Market research centre, 2001 20 “Western Europe: 3G in 2002”, World Market research centre, 2001 21 www.npt.no 22 Answers to questions received from national regulators by PTS 23“Tele2 could make 3G appeal in Norway by December”, Total Telecom, 8 August 2002 24 As reported by Total Telecom, 8 August 2002, “Tele2 must have 1,673 base stations by 1 December this year under the terms of the present licence. And it is this condition that is causing the operator some concern. A spokesman for Tele2 said that if the company sees no evidence of a return from its investment by the time of this deadline, then it would have to consider various options, one of which could be to formally appeal for a delay.” 25 Answers to questions received from national regulators by PTS

3G rollout status 12 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Country Coverage Requirement Regulator Activities/Changes Portugal August 2001

20% pop covered 2003 40% 2005 60%26

Operator commitments: Telecel: 50.4%/38.5%, TMN: 50.7%/7.4%, OniWay: 90.5%/11%, Optimus: 24.7%/16.2%27 Delayed more than a year, in line with service launch delays.

Spain All cities with more than 250,000 inhabitants to be covered by August 200128

Delayed until June 1st 2002, with flexibility should equipment not be available. Justified within original licence conditions due to lack of equipment.

Sweden 8 860 000 persons, corresponds to 99% of the population. End of 200329

None

UK 80% of population to be covered by end 200730

None

Table 2 Coverage requirements and regulator changes/activities

Service availability is key to any service take up and coverage requirements will drive different markets differently. Figure 1 and Figure 2 indicate differences in population coverage rollout over time in EU and Norway.

Sweden

Tele2 (

No)

NetCom

(No)

Teleno

r (No)

Portug

al

SFR (Fr)

Orange

(Fr)

Irelan

d A

Irelan

d B

Finlan

d2002

20052008

0%10%20%30%40%50%60%70%80%90%

100%

Figure 1 3G licence beauty contest market: Comparison graph of requirements for population coverage. Graphical illustration of content in Table 2

26 Northstream research 27 Answers to questions received from national regulators by PTS 28 “Western Europe: 3G in 2002”, World Market research centre, 2001 29 PTS 30 “Western Europe: 3G in 2002”, World Market research centre, 2001

3G rollout status 13 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Note that for France and Norway, actual operator commitments for population coverage are higher than the minimum requirements as shown in Table 2. Figure 1 displays the operators’ actual commitment for coverage rollout. Throughout the European markets there is a wide difference in requirements for the percentage of the population to be covered and the timing of the milestones. The highest requirements for population coverage are shown in Norway and Sweden. These countries also have requirements for population coverage that are to be met earlier than other markets. This means these operators have committed to a greater rollout pace. Figure 2 shows the requirements for markets where the licences were awarded by auction.

German

y

Greece

Austria

Belgium

Denmark

Netherl

ands UK

2002

20042006

2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Figure 2 3G licence auction markets: comparison graph of requirements for population coverage. Graphical illustration of content in Table 2

Note that the requirement for population coverage in Belgium - 85% in year 7 - is not mandatory. In some of these markets, the population coverage requirements are relatively modest. This doesn’t of course mean that these figures are the actual population coverage operators will roll out, but rather that in these markets operators have some discretion, so effectively population coverage will be linked to market demand for services. Note that these include operators in some of the major European markets – Germany, UK and Italy – who together form almost half the European market, in terms of population31. Therefore 3G services in these markets will be slightly less driven by regulator requirements, and more by market demand. This is of interest when discussing overall European 3G market, and 3G service take-up, in sections 4.2 and 5.3.

31 Dagens Nyheter, 19 September 2002

3G rollout status 14 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Regarding changes to the requirements, highlighted in Table 2, in general, the regulatory changes shown refer to postponement of dates when requirements are to be met rather than qualitative changes to the overall coverage. Operators in Portugal and Spain have indicated that they will not meet licence requirements regarding coverage build out, even if the coverage requirements were comparably modest. Actions were taken in 2001 to delay the requirements for coverage until June 2002, and in the absence of technology (i.e. equipment or handsets), there is discretion for further delay. The actual rollout of the network will in most cases exceed the required coverage rollout at any one time. For commercial reasons to launch services, service will have to be provided to a critical amount of the population, i.e. population coverage would have to exceed at a minimum approximately 30%. Some (Sweden and Finland), operators complied with early rollout obligations, albeit by setting up minimal network configurations used for functionality testing, rather than for commercial service purposes. In the majority of EU countries, rollout obligations specified later deadlines, hence the verification of such obligations does not come up at this stage. Norway’s regulator has fined Tele2 600,000 NOK for not meeting roll-out obligations for 2001. In general, the degree of flexibility to an interpretation of service launch, is not available regarding coverage requirements. Conclusions: Coverage milestones are clearly defined and there is little room for ’flexible

interpretation’. Generally, % population coverage requirements have not been changed by

regulators. Where change has occurred it has been in the timing of coverage milestones. In comparison to other countries examined, Sweden and Norway have very high

and very early requirements for coverage. In some major markets such as, UK, Germany and Italy, coverage requirements

are relatively modest, coverage is instead driven by market demand.

3G rollout status 15 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

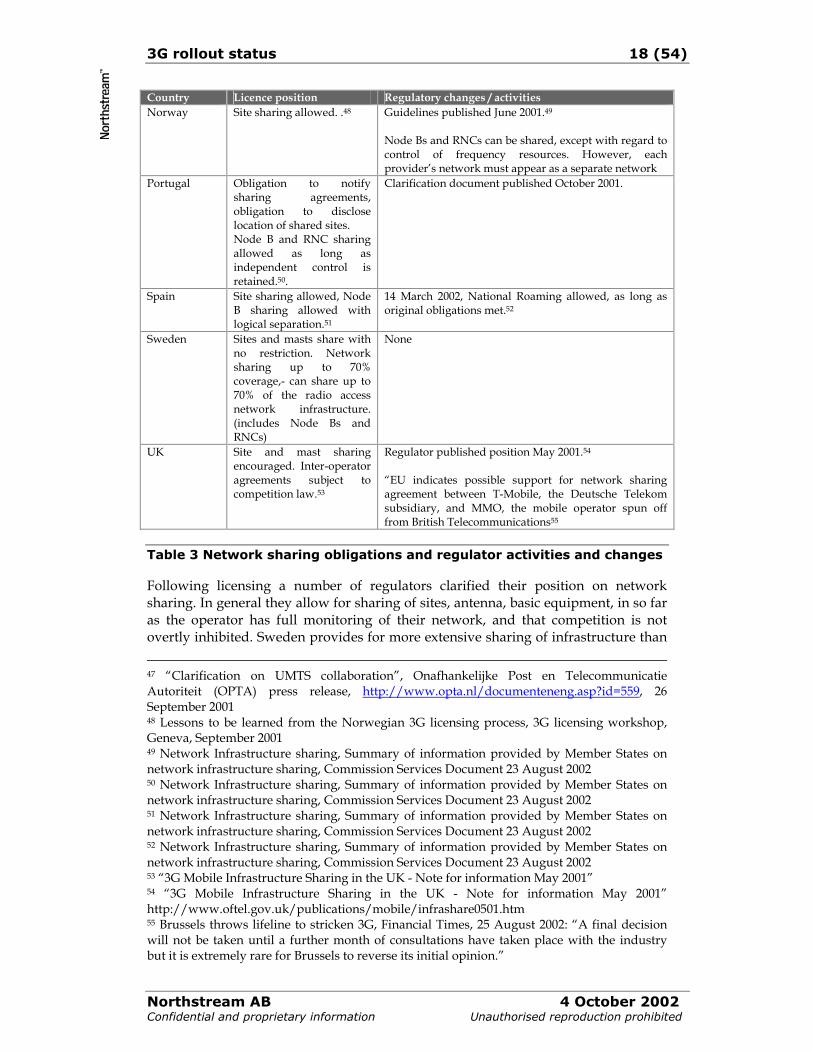

2.4 Network sharing obligation and potential

Table 3 highlights the licence requirements related to network sharing, and describes regulator changes or clarifications to those licence requirements. Commercial implementations of network sharing are described at Section 4.3.1. Sharing of a 3G network has a number of levels. The EU competition Directorate ranks the levels as follows32: sites, which ranges from sharing individual mast sites up to grid sharing

(requiring a uniform layout of networks), and may include site support infrastructure, such as site support cabinets (SSC),

base stations (Nodes B) and antennas, radio network controllers (‘RNCs’), core networks, including mobile switching centres (‘MSCs’) and various

databases, frequencies

A key driver for network sharing is that it allows operators to make significant cost savings. Civil works and site rental can make up 30% and 20% of network capex and opex respectively. Another advantage of site sharing is that it is applicable on existing GSM sites. It also reduces visual pollution by the multitude of wireless masts in the countryside. However for consideration is whether site sharing would have a short term impact on rollout speed. On the contrary obliged site sharing between 2G and 3G operators may add time to rollout due to commercial discussions and competitive manoeuvring. Limitations include non-competition from a coverage perspective, and opportunities for creation of an oligopoly.

32“BT Cellnet & BT3G/One2One Personal Communications (United Kingdom Agreement)”, 10 September 2002.

3G rollout status 16 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

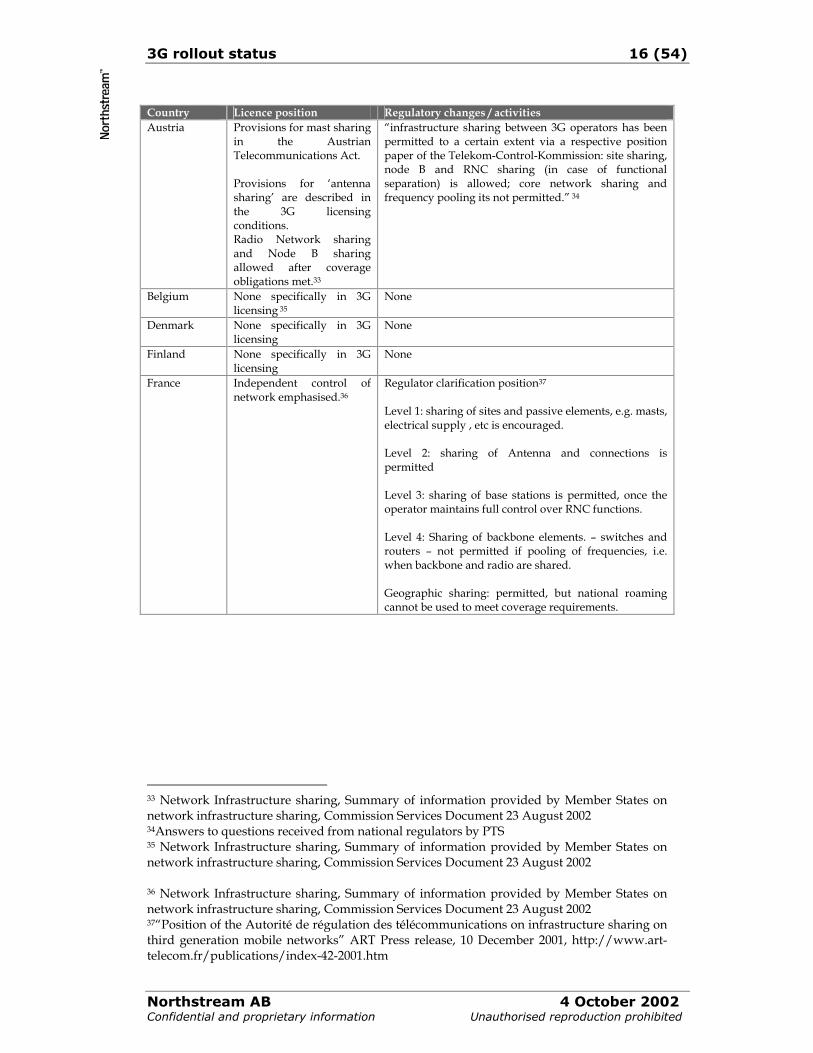

Country Licence position Regulatory changes / activities Austria Provisions for mast sharing

in the Austrian Telecommunications Act. Provisions for ‘antenna sharing’ are described in the 3G licensing conditions. Radio Network sharing and Node B sharing allowed after coverage obligations met.33

“infrastructure sharing between 3G operators has been permitted to a certain extent via a respective position paper of the Telekom-Control-Kommission: site sharing, node B and RNC sharing (in case of functional separation) is allowed; core network sharing and frequency pooling its not permitted.” 34

Belgium None specifically in 3G licensing 35

None

Denmark None specifically in 3G licensing

None

Finland None specifically in 3G licensing

None

France Independent control of network emphasised.36

Regulator clarification position37 Level 1: sharing of sites and passive elements, e.g. masts, electrical supply , etc is encouraged. Level 2: sharing of Antenna and connections is permitted Level 3: sharing of base stations is permitted, once the operator maintains full control over RNC functions. Level 4: Sharing of backbone elements. – switches and routers – not permitted if pooling of frequencies, i.e. when backbone and radio are shared. Geographic sharing: permitted, but national roaming cannot be used to meet coverage requirements.

33 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 34Answers to questions received from national regulators by PTS 35 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 36 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 37“Position of the Autorité de régulation des télécommunications on infrastructure sharing on third generation mobile networks” ART Press release, 10 December 2001, http://www.art-telecom.fr/publications/index-42-2001.htm

3G rollout status 17 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

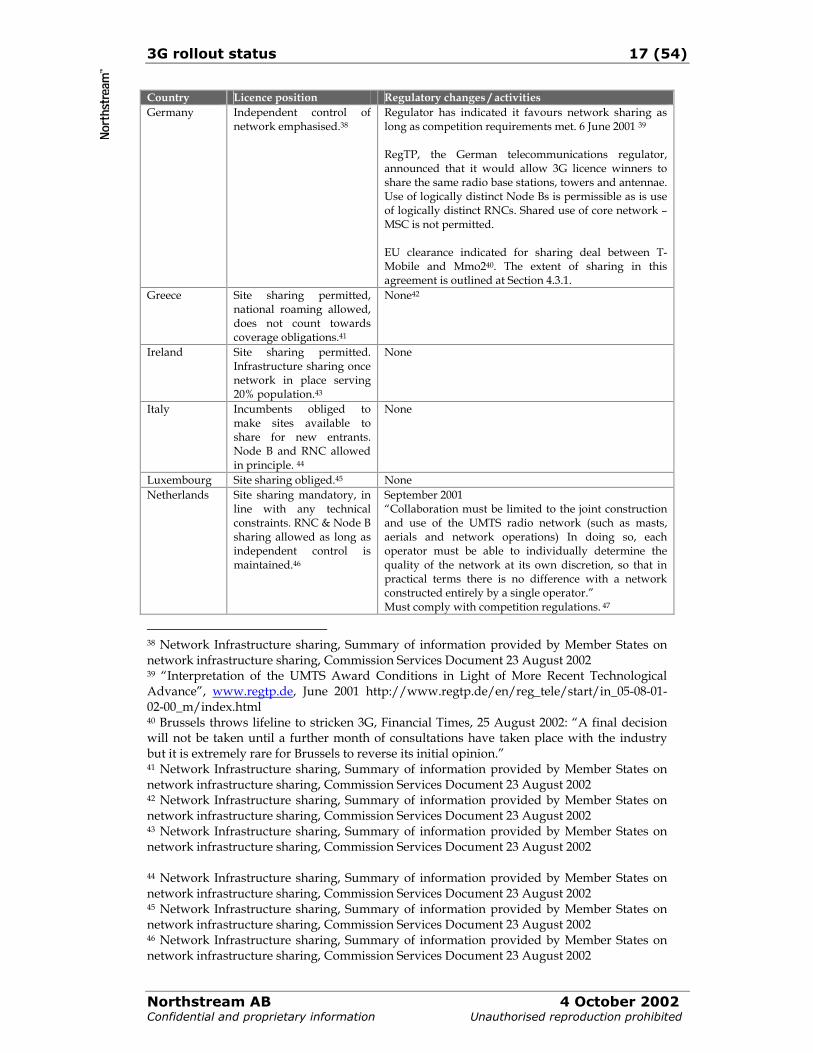

Country Licence position Regulatory changes / activities Germany Independent control of

network emphasised.38 Regulator has indicated it favours network sharing as long as competition requirements met. 6 June 2001 39 RegTP, the German telecommunications regulator, announced that it would allow 3G licence winners to share the same radio base stations, towers and antennae. Use of logically distinct Node Bs is permissible as is use of logically distinct RNCs. Shared use of core network – MSC is not permitted. EU clearance indicated for sharing deal between T-Mobile and Mmo240. The extent of sharing in this agreement is outlined at Section 4.3.1.

Greece Site sharing permitted, national roaming allowed, does not count towards coverage obligations.41

None42

Ireland Site sharing permitted. Infrastructure sharing once network in place serving 20% population.43

None

Italy Incumbents obliged to make sites available to share for new entrants. Node B and RNC allowed in principle. 44

None

Luxembourg Site sharing obliged.45 None Netherlands Site sharing mandatory, in

line with any technical constraints. RNC & Node B sharing allowed as long as independent control is maintained.46

September 2001 “Collaboration must be limited to the joint construction and use of the UMTS radio network (such as masts, aerials and network operations) In doing so, each operator must be able to individually determine the quality of the network at its own discretion, so that in practical terms there is no difference with a network constructed entirely by a single operator.” Must comply with competition regulations. 47

38 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 39 “Interpretation of the UMTS Award Conditions in Light of More Recent Technological Advance”, www.regtp.de, June 2001 http://www.regtp.de/en/reg_tele/start/in_05-08-01-02-00_m/index.html 40 Brussels throws lifeline to stricken 3G, Financial Times, 25 August 2002: “A final decision will not be taken until a further month of consultations have taken place with the industry but it is extremely rare for Brussels to reverse its initial opinion.” 41 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 42 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 43 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 44 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 45 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 46 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002

3G rollout status 18 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Country Licence position Regulatory changes / activities Norway Site sharing allowed. .48 Guidelines published June 2001.49

Node Bs and RNCs can be shared, except with regard to control of frequency resources. However, each provider’s network must appear as a separate network

Portugal Obligation to notify sharing agreements, obligation to disclose location of shared sites. Node B and RNC sharing allowed as long as independent control is retained.50.

Clarification document published October 2001.

Spain Site sharing allowed, Node B sharing allowed with logical separation.51

14 March 2002, National Roaming allowed, as long as original obligations met.52

Sweden Sites and masts share with no restriction. Network sharing up to 70% coverage,- can share up to 70% of the radio access network infrastructure. (includes Node Bs and RNCs)

None

UK Site and mast sharing encouraged. Inter-operator agreements subject to competition law.53

Regulator published position May 2001.54 “EU indicates possible support for network sharing agreement between T-Mobile, the Deutsche Telekom subsidiary, and MMO, the mobile operator spun off from British Telecommunications55

Table 3 Network sharing obligations and regulator activities and changes

Following licensing a number of regulators clarified their position on network sharing. In general they allow for sharing of sites, antenna, basic equipment, in so far as the operator has full monitoring of their network, and that competition is not overtly inhibited. Sweden provides for more extensive sharing of infrastructure than 47 “Clarification on UMTS collaboration”, Onafhankelijke Post en Telecommunicatie Autoriteit (OPTA) press release, http://www.opta.nl/documenteneng.asp?id=559, 26 September 2001 48 Lessons to be learned from the Norwegian 3G licensing process, 3G licensing workshop, Geneva, September 2001 49 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 50 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 51 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 52 Network Infrastructure sharing, Summary of information provided by Member States on network infrastructure sharing, Commission Services Document 23 August 2002 53 “3G Mobile Infrastructure Sharing in the UK - Note for information May 2001” 54 “3G Mobile Infrastructure Sharing in the UK - Note for information May 2001” http://www.oftel.gov.uk/publications/mobile/infrashare0501.htm 55 Brussels throws lifeline to stricken 3G, Financial Times, 25 August 2002: “A final decision will not be taken until a further month of consultations have taken place with the industry but it is extremely rare for Brussels to reverse its initial opinion.”

3G rollout status 19 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

many other authorities – available at each of the sharing levels outline above. This applies to 70% of the infrastructure built to meet the coverage requirements. The EU Commission has indicated that it will treat network sharing cases as a priority – and there are some indications that it now views network sharing favourably.56 It has recently made decisions/indications that are favourable to MMO2 and T-Mobile network sharing operations in Germany and the UK, (see Section 2.4 for an outline of this). It has reserved judgement on potential to share the radio access network, until the operators indicate they plan to proceed with this aspect of the agreement. The EU has indicated that the financial situation of operators has influenced their approach, ‘"From a competition law point of view, network sharing reduces competition," said a lawyer close to the issues. "But there is a recognition by the Commission that something has to be done for the mobile industry."’57 In making the competition judgements, the authority will take into account the number of operators in the market and the depth of co-operation. Reports indicate that “if companies are sure that network-sharing deals do not significantly differ from the German or British agreements, they could simply proceed with those deals without notifying the Commission.”58 This would facilitate operators, without undergoing similar clearance from the EU. Conclusions: In response to the industry situation some regulators published positions on

network sharing following the original licensing process. In general European authorities allow for sharing of sites, antenna, basic

equipment, in so far as the operator has full monitoring of their network, and that competition is not overtly inhibited. Sweden provides for more extensive sharing of infrastructure than many other authorities.

Financial situation forces regulatory movement, as network sharing can reduce capex and opex.

It is reasonable to conclude that competition has been placed at a lower priority to facilitate the 3G market.

56“Commission intends to clear 3G network sharing agreements between T-Mobile and MM02 in the UK and Germany. September 10 2002”, Brussels, 10 September 2002 57 “Brussels throws lifeline to stricken 3G2, Financial Times, 25 August 2002 58 “Brussels moves on network links” Financial Times, 10 September 2002

3G rollout status 20 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

2.5 Other

2.5.1 Some operator interest in greater flexibility for transfer of licence

In a market where some operators are postponing launch, and therefore jeopardising the ability to meet licence conditions and some are effectively mothballing 3G operations (see Section 4.1), the ability to transfer licences is of interest to operators. From a regulatory perspective the current situation is as follows: Licence transfer is not explicitly permitted in Austria, Belgium (ownership approved by authority), Finland, France, Germany, Luxembourg, UK. Licence transfer is explicitly permitted in Denmark (regulator discretion), Greece (approval by regulator), Ireland (consent of regulator), Italy (only following 4 years and subject to approval), the Netherlands (ministerial consent), Portugal (authorisation of government), Spain (after 4 years with ministerial consent).59 In Finland, two 3G licensees are merging of companies (Sonera and Telia). The merged entity can hold only one 3G licence, so the Telia 3G licence will therefore revert to the regulator. The regulator will then conduct a separate process whereby applications are welcomed for this licence. 60 In Italy, the Telefonica/Sonera joint venture, IPSE, has requested that it can hand its licence back to the government and recoup its original investment, however as that is inside the original four years limit a decision has not been taken. Conclusions: There is a diversity of treatment across Europe. There is no direct indication that these conditions will be changed.

2.5.2 Spectrum trading

In a market environment where some operators have mothballed operations, and industry consolidation could be an increasing likelihood, the ability to trade spectrum, in effect dispose of the 3G licence assets, may become a key issue. Traditionally the only way to exchange spectrum has been through merger or acquisition of the service licensee, or via the regulator. Some operators have publicly expressed an interest in the possibility for trading of spectrum. Telefonica Moviles, with postponed operation in Italy and Germany have indicated they “would also consider spectrum trading if that became a possibility61” The CEOs of European mobile operator members of the GSM Association submitted a recommendation to the European Commission to “Launch as soon as possible with regulators and industry discussions on spectrum trading and the conditions

59 McKinsey 60“Hutchison eyes Finnish 3G”, Financial Times, August 26 2002 61 “Group 3G set to lose up to 800 staff – sources” , Total Telecom, 27 August 2002

3G rollout status 21 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

appropriate for its introduction”62. In commenting on the McKinsey review of 3G licensing in Europe, Vodafone states that it “would like to see the emphasis of future Government, regulatory and Commission action on the introduction of spectrum trading to provide a means for the market to correct for changing valuations of spectrum”63. It appears that a new regulatory regime due for introduction in June 2003 will allow for greater flexibility in spectrum trading according to a number of procedures. A paper published by the Commission in June shows an indication of greater future flexibility for trading of spectrum, which had previously been linked to service licences. “Using the mechanisms provided for by the Spectrum Decision, the Commission intends to establish a dialogue with industry and national regulators on secondary trading of radio spectrum and its implications. This will include a discussion of harmonised spectrum trading conditions and the debate on introduction timing in different Member States which would avoid distortions in the assignment process for services of Community coverage or interest.“64 However reports indicate that this paper has been noted by the Commission. The status of its recommendations are not fully clear and it should not be assumed that it can be applied to spectrum assigned during the 3G licence process. Conclusions: Driven by potential consolidation, there is pressure from operators to increase

flexibility in spectrum trading. The EU has indicated that secondary trading of spectrum will be facilitated under

a new regime. The actual procedures and methods for this remain to be clarified. It is unclear if new procedures regarding spectrum trading will be applicable to

3G licences.

2.5.3 Licence period extended by some national regulators

Despite discouragement from the Commission, some regulators have extended the period of the licence. This is driven by a belief that it gives operators a greater period to recoup their investment. The French and Italian regulators have extended their licence period.65 The French licence period of validity has been extended from 15 to 20 years, as has the Italian licence period. Conclusions: Some national regulators have extended the licence period. This reduction will have minimal short-term impact on 3G rollout, it aims to help

in business case viability.

62 Recommendations from GSM Europe Members to the European Commission on actions for the success of 3G deployment, May 2002, http://www.gsmworld.com/gsmeurope/presentations/recommendations_ec.pdf 63 “Response of Vodafone” Comparative Assessment of the Licensing Regimes for 3G Mobile Communications in the European Union and their Impact on the Mobile Communications Sector, 2 September 2002 64 ”Towards the Full Roll-Out of Third Generation Mobile Communications”, June 2002, Commission of the European Communities. 65 “German regulator denies Telefonica licence talks”, Total Telecom, 28 August 2002

3G rollout status 22 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

2.5.4 Fees/price have been altered

The Commission didn’t specifically recommend this type of adjustment, as it could introduce a degree of unpredictability into the industry sector. Some regulators have altered fees, and costs associated with the 3G licence. At the end of 2001 the French regulator revised the taxes from 4.95 billion euros to 619 million euros + 1% fee on 3G revenue with the aim of tying payment to actual market demand. The Spanish regulator also reduced spectrum fees, in an agreement with the operators in response to legal action, as fees had been increased directly following the original licence competition.66 More recently reports indicate that the Science and Technology Ministry were “considering changing the terms of the contracts for third-generation licences, which he said could otherwise hinder investment in a crucial sector. "We are going to be flexible and pragmatic in asking the sector for specific obligations," Pique said. "Not just with the guarantees, but also by softening investment requirements." “67 Conclusions: These cases have limited impact on short term rollout, but rather indicate a

degree of flexibility on behalf of regulators and government ministries.

3 Technology status and changes

3.1 Handset aspects

3G handsets represent a technical evolution step in mobile device development. Handset development life-cycle may take up to 3 years, if a vendor is developing products in-house. Therefore, it is reasonable to believe that planning for 3G handsets has been ongoing for at least this time period. Of course attractive applications and services are needed to make people to buy and use the latest implemented technology. 3G handsets brought to market will compete with 2.5G (GPRS) handsets already on the market. Basic requirements such as a handset of about the same physical size as 2G handsets, an appealing industrial design, a high quality colour screen, etc. are therefore necessary. In addition for the European market, dual-mode (2G GSM/GRPS and 3G WCDMA) will be necessary for users. They will enable continuity of service between 3G and 2G coverage areas. See Section 3.2 for description of network functionality required for 3G / 2G handover. Figure 3 outlines forecasts for the number of WCDMA handsets shipped globally. It shows the change in industry expectations of that took place between February 2001 and September 2002.

66 “Spain tax deal with mobile phone operators”, Financial Times, 28 November 2001, 67 “Spain to freeze radio spectrum tax in 2003 – report”, Total Telecom, 23 September 2002

3G rollout status 23 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

0

20

40

60

80

100

120

2001E 2002E 2003E 2004E 2005E 2006E

MillionsFebruary 2001sep-02

Figure 3 Global WCDMA handset uptake forecasts February 2001 vs. September 2002. Source: Morgan Stanley Dean Witter.68

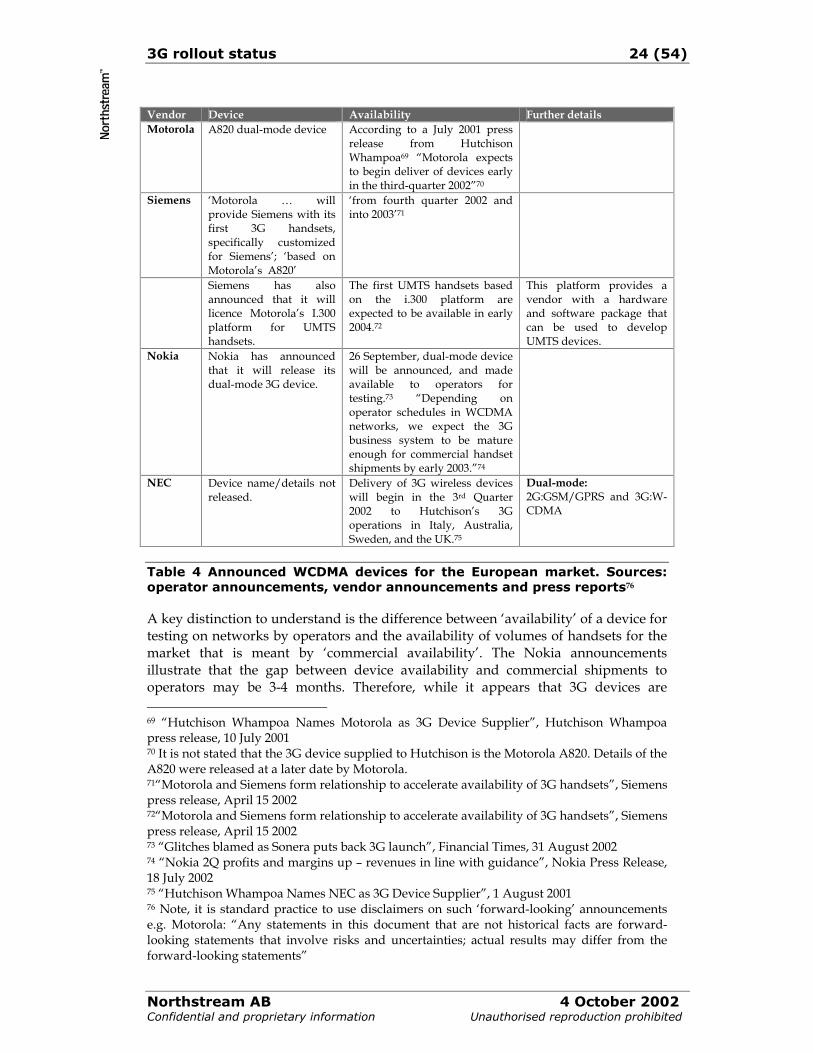

These global figures also include the Japanese WCDMA market, however it is a clear indication that in Western Europe, expectations for take up have changed significantly. Mobile vendors are naturally cautious about announcing product availability, for competitive reasons. In addition, when timing the launch of products, mobile vendors will take expected market demand into account, as well as the coherence of their own product portfolio. Current vendor announcements for 3G devices in Western Europe are outlined at Table 4:

68 “Lower industry forecasts, Lower Nokia forecasts”, Morgan Stanley Dean Witter; 27 February 2001 “First signs of colour/camera phone potential”, Morgan Stanley Dean Witter, 10 September 2002

3G rollout status 24 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Vendor Device Availability Further details Motorola A820 dual-mode device According to a July 2001 press

release from Hutchison Whampoa69 “Motorola expects to begin deliver of devices early in the third-quarter 2002”70

Siemens ‘Motorola … will provide Siemens with its first 3G handsets, specifically customized for Siemens’; ‘based on Motorola’s A820’

‘from fourth quarter 2002 and into 2003’71

Siemens has also announced that it will licence Motorola’s I.300 platform for UMTS handsets.

The first UMTS handsets based on the i.300 platform are expected to be available in early 2004.72

This platform provides a vendor with a hardware and software package that can be used to develop UMTS devices.

Nokia Nokia has announced that it will release its dual-mode 3G device.

26 September, dual-mode device will be announced, and made available to operators for testing.73 “Depending on operator schedules in WCDMA networks, we expect the 3G business system to be mature enough for commercial handset shipments by early 2003.”74

NEC Device name/details not released.

Delivery of 3G wireless devices will begin in the 3rd Quarter 2002 to Hutchison’s 3G operations in Italy, Australia, Sweden, and the UK.75

Dual-mode: 2G:GSM/GPRS and 3G:W-CDMA

Table 4 Announced WCDMA devices for the European market. Sources: operator announcements, vendor announcements and press reports76

A key distinction to understand is the difference between ‘availability’ of a device for testing on networks by operators and the availability of volumes of handsets for the market that is meant by ‘commercial availability’. The Nokia announcements illustrate that the gap between device availability and commercial shipments to operators may be 3-4 months. Therefore, while it appears that 3G devices are 69 “Hutchison Whampoa Names Motorola as 3G Device Supplier”, Hutchison Whampoa press release, 10 July 2001 70 It is not stated that the 3G device supplied to Hutchison is the Motorola A820. Details of the A820 were released at a later date by Motorola. 71“Motorola and Siemens form relationship to accelerate availability of 3G handsets”, Siemens press release, April 15 2002 72“Motorola and Siemens form relationship to accelerate availability of 3G handsets”, Siemens press release, April 15 2002 73 “Glitches blamed as Sonera puts back 3G launch”, Financial Times, 31 August 2002 74 “Nokia 2Q profits and margins up – revenues in line with guidance”, Nokia Press Release, 18 July 2002 75 “Hutchison Whampoa Names NEC as 3G Device Supplier”, 1 August 2001 76 Note, it is standard practice to use disclaimers on such ‘forward-looking’ announcements e.g. Motorola: “Any statements in this document that are not historical facts are forward-looking statements that involve risks and uncertainties; actual results may differ from the forward-looking statements”

3G rollout status 25 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

available beginning of 2004, in general, when introducing mobile handsets, it is standard practice for operators to use some months in testing devices on networks. Some of the reasons for such testing challenges are outlined at Section 3.2 under ‘Interoperability between handsets and infrastructure’. Industry practice is that handsets reach different markets at different times. Factors which influence accessibility of handsets to operators include the market size, and whether the operator is multi-national and therefore able to exercise its purchasing power on a multi-national basis. Also, a multi-national group is naturally free to prioritise terminal or service launch for certain operators in its own group. Established vendor/operator relationships are also key to acquiring sufficient volumes of devices, as anyway devices may need to be customised for local markets. Therefore, a smaller operator in a small market may have extra challenges in accessing handsets. On the other hand, such markets can be used as trial markets – to test out innovative products. However the situation and accessibility of handsets to operators is not straightforward. While services can be launched with a single device, such a launch will not have the same potential to attract a range of consumers as one where a variety of handsets are available that are attractive to a variety of consumer segments. Operators may need a number of devices to really drive uptake of new services, and choice for consumers. In addition, introduction of a new technology, has, e.g. with WAP and GPRS devices, resulted in a number of ‘trial-like’ product launches prior to mass-market take up. For example the Ericsson R520 GPRS device was a useful tool to test GPRS functionality, but was not a mass-market driver for GPRS. It is possible that the initial 3G devices will play a similar role, and that a second wave of as yet unannounced devices will play the key role in driving a mass-market take up. Conclusions: Industry expectations on handset sales and uptake have significantly altered in

the past 19 months – indicating that WCDMA handsets are not commercially available as originally expected.

Accessibility of operators to initial handsets is not straightforward – there are many influencing factors: such as market size, operator group size and purchasing power and strength of established vendor/operator relationship.

Testing of handset capabilities, and service usage are essential to ensure a high quality of service for users.

3.2 Network functionality

A WCDMA network is a very complex suite of equipment, with numerous interfaces and hard requirements on reliability and functionality. When developing such equipment, it is obvious that much of the functionality envisaged for the mature network cannot be provided in early releases of the products. Instead, in line with convention, increasingly advanced hardware and software releases will follow the first product shipments. However, while accepting such product roadmap with an incremental functionality ramp-up, the network operator sets some hard requirements on core functionality that must be in place to enable launch of the 3G operations. For some of this functionality, problems have been reported, and below we therefore focus on these and discuss the extent to which this is likely to affect 3G timelines.

3G rollout status 26 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

From the 3G operator perspective, Northstream has identified the following functionality as major challenges, and whose nature is so critical that they could delay a 3G launch and subscriber uptake if not supported. Plain software stability of some of the nodes required for offering reasonable

service functionality. Fixed telephony and GSM systems have made operators and users alike used to very high reliability of the service offered. This translates into high requirements on mature and stable software in all nodes involved. For a meaningful 3G launch, the operator will require that both circuit switched voice and packet switched data services are offered in a stable manner, and therefore virtually all 3G network nodes have to provide software stability. For example, a 3G network which supports voice and circuit-switched data, but for which packet switched data functionality is not stable, will not allow a meaningful 3G launch. Generally, operators and suppliers have not disclosed information about the software stability status as cause of 3G delays, other than in general terms mentioning lack of technology maturity77. The European Union Commission considers that “In conclusion, 3G technology seems to be stable today, despite reported technical difficulties (such as dropped calls, glitches in the terminal software, and reported insufficient battery capacity) that must be seen as normal difficulties encountered when introducing new products of considerable technological innovation.”78 Indeed, the term ‘stability’ can be used in different ways, but in order to launch commercial services on a 3G network without hurting the operator brand, the operator will not accept systematically dropped calls due to lack of stability. The EU statement should therefore not be interpreted as claiming that 3G networks already provide stable enough functionally to allow commercial use.

Interoperability between handsets and infrastructure. Naturally, this is a

problem spanning both handsets and network: software upgrades are needed on both sides of the radio interface. Terminal availability aspects of this are discussed in Section 3.1. In the networks, while support of one or two terminal types may be fairly straightforward (since testing has been ongoing for some time), a main challenge is to support a larger variety of handsets. This problem is related to the 3GPP standard, which is rich in options and also so complex that it may often be interpreted in different ways. The current situation is therefore that different handsets have implemented different options within the standard, and also made different implementations of critical mandatory functionality. This has even lead 3GPP to discuss the necessity for the terminal to signal its type and software version, to allow the network to adapt its behaviour accordingly79. It is a clear indication that interoperability testing (IOT) is still not finalised by far for the first generation handsets, and that the network will need further upgrades to support the whole terminal population. Although this is generally viewed as a

77 “Sonera To Launch 3G Mobile Communications Services In Finland On September 26” Sonera press release, 30 August 2002: ”Commercial UMTS mobile communications will be started on Sonera’s network in 2003 as soon as […] this is feasible in view of the maturity of the network technology” 78 ”Towards the Full Roll-Out of Third Generation Mobile Communications”, June 2002, Commission of the European Community. 79 “Summary of RAN email discussion for handling of early mobiles”, 3GPP contribution RP-020466, September 2002

3G rollout status 27 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

main contributor to launch delays, little information has been disclosed publicly. Sonera’s statement on the lack of ‘maturity of the network technology’80 was interpreted by the Financial Times to mean interoperability problems81. Worth mentioning though is that operators will typically launch 3G operations with only a few terminal types, and therefore some operators may be fortunate to have chosen a terminal-network supplier combination where testing has been relatively successful, and where initial launch therefore is not severely hampered.

Interoperability between network nodes in case of multiple vendors. Many

operators have chosen to include infrastructure equipment from multiple vendors in their networks. This implies multi-vendor interfaces, typically between different parts of the radio access network (Iur interface) and/or between the radio access network and the core network (Iu interface). Generally, little information has been disclosed about the status of multi-vendor interoperability, but considering that networks have been deployed for testing for quite some time, and also considering the limited number of supplier combinations, this problem should be less severe than interoperability with handsets.

Handover and cell reselection between 2G and 3G. We view the ability for a 3G

session (whether it is a voice call or a data session) to be handed over to GSM/GPRS in case of insufficient 3G coverage as critical for a meaningful 3G launch. Used to the service quality levels of GSM, subscribers will have no mercy with operators who fail to deliver basic service quality. For operators with a GSM network, this means that the signaling between the handsets and the GSM and WCDMA networks must be stable and fast enough for a good user experience, which is challenging both from standards and implementation perspectives. With a few exceptions, little information on this topic has been disclosed publicly. For example, in Hong-Kong, Hutchison 3G has delayed its WCDMA launch citing dropped calls between 2G and 3G networks82. JP Morgan interprets Sonera’s recent statement about lack of ‘maturity of the network technology’83 as related to handover between 2G and 3G networks84. For greenfield WCDMA operators, the challenge to provide handover to GSM is even higher, since it implies the existence of a national roaming agreement with a GSM operator, and also special network functionality to enable the handover of ongoing sessions (inter-PLMN handover). Some of this functionality needs to be implemented in the GSM operator’s network, and it is difficult to see the incentive for it to do so unless forced to by regulation. The greenfield 3G operators’ plans whether to support handover of sessions at time of launch are

80“Sonera To Launch 3G Mobile Communications Services In Finland On September 26” Sonera press release, 30 August 2002 81“Glitches blamed as Sonera puts back 3G launch”, Financial Times, August 31 2002: ”Sonera pointed to problems with handset availability and network inter-operability as the two main reasons for the delay.” 82 GSM Strategist, 5 September 2002. 83 “Sonera To Launch 3G Mobile Communications Services In Finland On September 26” Sonera press release, 30 August 2002 84 “Glitches blamed as Sonera puts back 3G launch”, Financial Times, August 31 2002: ”"The continued delay is no surprise, given the geographical and frequency handover challenges between 2G and 3G networks."

3G rollout status 28 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

not fully public. Financial Times quotes Hutchison 3G in UK stating that users could experience dropped calls when roaming from its 3G network to the 2G networks of its partner operators85, which indicates that they do not expect to support handover to GSM. Without the ambition to support handover, networks failing to support will of course not impact the operator launch directly, but on the other hand, to avoid a bad user experience the WCDMA coverage must be extremely good from day one, which may in turn delay the feasible launch date.

One observation, on analysis of these network problems, is that operators and suppliers are not inclined to publicly make references to such problems. This is easily understood: any such references immediately cast a shadow on the involved infrastructure supplier(s) and on the operator’s own ability to run its network, which is unnecessary when launch delays can conveniently be blamed on unavailability of handsets. Summarising the current situation regarding 3G network problems, it would appear that – even though all problem areas listed above currently exist - a main problem is IOT of handsets/network. The IOT and consequential handsets and network software updates will take significant time yet to complete, even for the first generation of handsets, and in the public debate the slogan will likely be ‘terminal unavailability’, with the challenging IOT being only one reason for the unavailability (See further Section 3.1 on terminal availability). While public information to date does not make predictions on timing for solution of the other listed network related problems, one can assume that the essential problems will have been solved before the currently planned launches (mid 2003). While this means that these network problems will not be a bottle-neck for 3G launch, it is still a considerable difference compared with the views set out in 1999-2000, when it was generally believed that networks would be working in 200186. Conclusions: While unavailability of many network features is not a critical problem for 3G,

there are currently problems with key network functionality to enable 3G launch. One key area is interoperability testing (IOT) between handsets and networks. Other listed key network problems – software stability, infrastructure multi-

vendor interoperability and handover between 2G and 3G – are likely to be solved before terminal IOT is completed, and are thus not reasons for launch delay in their own right.

There is a general unwillingness to make public statements about network problems – operators and suppliers appear to find it more convenient to blame 3G delays on terminal unavailability.

85 “Hutchison 3G on target for launch”, Financial Times, July 30 2002: “Hutchison admitted that some of its users could experience "dropped calls" where they roamed from its 3G network to the 2G networks of its partner operators.” 86 Note that original service launch dates in Spain and Portugal were in 2001.

3G rollout status 29 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

4 3G rollout status and plans

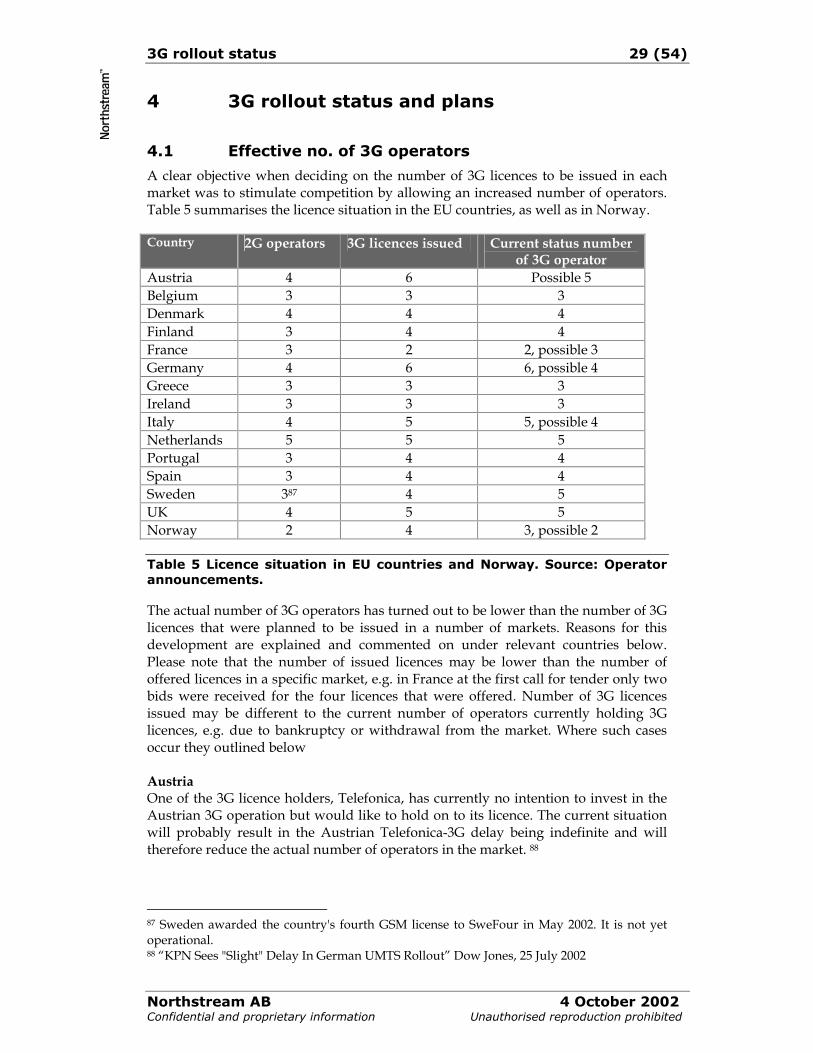

4.1 Effective no. of 3G operators

A clear objective when deciding on the number of 3G licences to be issued in each market was to stimulate competition by allowing an increased number of operators. Table 5 summarises the licence situation in the EU countries, as well as in Norway. Country 2G operators 3G licences issued Current status number

of 3G operator Austria 4 6 Possible 5 Belgium 3 3 3 Denmark 4 4 4 Finland 3 4 4 France 3 2 2, possible 3 Germany 4 6 6, possible 4 Greece 3 3 3 Ireland 3 3 3 Italy 4 5 5, possible 4 Netherlands 5 5 5 Portugal 3 4 4 Spain 3 4 4 Sweden 387 4 5 UK 4 5 5 Norway 2 4 3, possible 2

Table 5 Licence situation in EU countries and Norway. Source: Operator announcements.

The actual number of 3G operators has turned out to be lower than the number of 3G licences that were planned to be issued in a number of markets. Reasons for this development are explained and commented on under relevant countries below. Please note that the number of issued licences may be lower than the number of offered licences in a specific market, e.g. in France at the first call for tender only two bids were received for the four licences that were offered. Number of 3G licences issued may be different to the current number of operators currently holding 3G licences, e.g. due to bankruptcy or withdrawal from the market. Where such cases occur they outlined below Austria One of the 3G licence holders, Telefonica, has currently no intention to invest in the Austrian 3G operation but would like to hold on to its licence. The current situation will probably result in the Austrian Telefonica-3G delay being indefinite and will therefore reduce the actual number of operators in the market. 88

87 Sweden awarded the country's fourth GSM license to SweFour in May 2002. It is not yet operational. 88 “KPN Sees "Slight" Delay In German UMTS Rollout” Dow Jones, 25 July 2002

3G rollout status 30 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Germany Telefonica and Sonera controlled German 3G licence holder, Group 3, who suspended its 3G operations in July 2002. It's not clear what measures, if any, Telefonica and Sonera will take to ensure that Group 3G, does not breach the 3G licence conditions. A key condition is that licence holders must achieve 25% coverage by the end of 2003. The head of the regulatory agency, RegTP, seems to be reluctant to change 3G licence conditions in Germany in favour to Sonera and Telefonica.89 This may result just five 3G operators. Mobilcom’s financial situation is unclear based on France Telecom’s decision to abandon the investment. The German government has taken a positive position to guarantee financial support to the company, but there still remains a number of issues to resolve in order to secure the Mobilcom’s future. The case will be subject to the EU Commission’s decision90. The Finnish ministry of telecommunication has reacted negatively to the German government’s actions and claims Sonera’s rights to a refund their German 3G licence fee. If Mobilcom does not succeed in reconstructing the company, the number of German 3G operators would be down to 4. Italy The Telefonica controlled Italian 3G licence holder, Ipse, has declared that it has no firm commitment to launch 3G services in Italy.91 Further, one of the Italian 2G operators that was not awarded a 3G licence has with-drawn from the market. This results in the market competition in terms of number of service providers being unchanged in the longer perspective, but has currently decreased due to the decreased number of 2G operators. Norway Four licences were originally issued, but Broadband Norway’s operation was dissolved in 2001 and the licence was handed back in August 2001. The government has plans to auction off this licence in autumn, but the decision will be subject to parliamentary approval. Further, Tele 2 has recently entered a MVNO operation agreement with Telenor, which may lead to that they will try to escape the obligations under their 3G licence agreement. This will reduce the number of effective 3G network operators to 2 in Norway. 92 In France, Belgium, Greece and Luxembourg and Ireland there was not a sufficient number of interested parties to issue all offered licences. This has lead to a situation where the amount of spectrum made available for 3G will remain unused for the time being. In France bids for the remaining licences were invited in December 2001, but only one application was received by the deadline of May 2002 - from Bouygues

89 “German regulator denies Telefonica license talks” Total Telecom, 28 August 2002 90 “EU gives Germany 20 days for details on MobilCom aid”, Total Telecom, 19 September 2002 91 “Telecoms bow to the reality of 3G” Yahoo news, 26 July 2002 92 “Tele2 may return Norway 3G licence”, Total Telecom, 17 September 2002

3G rollout status 31 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Telecom.93 The results of the second round will be formally announced by September 30 2002. Only three of the four intended Greek licences were awarded, because there were only three applicants. It is unclear what will happen to the remaining licence, but the spectrum cannot be reallocated until at least five years after the end of the auction. The above overview only considers operators operating their own networks. MVNOs without a large established customer base will play a similar role in the 3G markets as they do in the 2G markets. However requirements on service provision, advanced billing facilitates etc, will to some extent decrease the MVNO opportunity in comparison with the market for 2G services. In contrary to earlier market expectations, Northstream’s analysis concludes that new virtual operators without an existing customer base are currently a minimal threat. The Swedish situation is unusual as the cooperation between Tele 2 and Telia will have the effect that competition in the market will be more intense than originally foreseen. The financial situation (see later section for more details) in the telecom market might force operators to closer cooperation, and thereby either directly or indirectly decrease the effective number of operators in the market. Conclusions: Europe wide trend for markets is that there are fewer operators than originally

anticipated, for a variety of reasons: o low impact of virtual operations on the market o some licences being put in abeyance o some licences not taken up in the original competition.

Competition generally increased in comparison to 2G market situation, but not to the extent that was anticipated.

Some situations go against this trend – e.g. Swedish situation is unusual – incumbent Telia means 5 effective operations.

Germany is the single most affected market in terms of decreased number of 3G operators.

Current financial situation may force operators to cooperate or merge in order to safe guard investment commitment.

4.2 3G rollout and launch status

As stated above, in some major markets (UK, Germany and Italy) the lower coverage requirements results in the rollout of 3G network being driven by market demand rather than regulatory requirements. Actual rollout plans are confidential information, and the below table is a summary of publicly available information on European operators plans to launch services. Announced delays reflect both lack of available technology, financial constraints as well as the general current low demand for new technology. For details, see the below country-by-country commentary.

93“SURVEY - FT TELECOMS: Formidable challenges Having spent huge sums on 3G licences, big European telecom operators are plagued by fears regarding viability”, Financial Times, 15 May 2002

3G rollout status 32 (54)

Northstream AB 4 October 2002 Confidential and proprietary information Unauthorised reproduction prohibited

Country Wireless Operator Delayed? Orig. Launch Date 3G Revised Launch Date

Austria 3G Mobile yes No commitment Belgium KPN Orange (KPN

NV / Orange JV) Yes autumn 2002 autumn 2003

Belgium Mobistar (majority France Telecom's Orange)

Yes autumn 2002 autumn 2003

Belgium Proximus (majority Belgacom, 25% Vodafone)

Yes autumn 2002 autumn 2003

Finland Radiolinja Yes Finland Sonera Yes Sept. 26, 2002 2003? Finland Suomen 3G Yes TBD France SFR (holding company

Cegetel) Yes 2H03 2004 or late

Germany Group 3G/Quam (Sonera / Telefonica Moviles JV)

Yes 2003 exit

Germany MobilCom Yes 1H02 2H02 (2003) Germany T-Mobil (Deutsche

Telekom unit) Yes 2H02 2H03

Germany Viag Interkom (mm02 unit)