4-1 accrual accounting concepts 4 fall 2015 accounting, fifth edition

TRANSCRIPT

4-1

ACCRUAL ACCOUNTING CONCEPTS

4

Fall 2015Accounting, Fifth Edition

4-2

Generally we use a month, a quarter, or a year.

Fiscal year vs. calendar year: The business fiscal year might be the same as a calendar year from Jan 1 to Dec 31, or may start at some other date (July 1 to June 30).

Recall: We can divide the economic life of a business into artificial time periods (the Periodicity Assumption).

Jan. Feb. Mar. Apr. Dec.. . . . .

TimingTiming Issues IssuesTimingTiming Issues Issues

4-3

Accrual Basis Accounting

► Transactions are recorded in the periods in which the

events occur. That means:

► Revenues are recognized (meaning they’re recorded)

when earned, even if cash was not immediately

received (cash is received sometime later).

► Expenses are recognized (meaning they’re recorded)

when incurred, even if cash was not immediately paid

(cash is paid out sometime later).

Timing IssuesTiming IssuesTiming IssuesTiming Issues

Accrual versus Cash Basis of Accounting

4-4

Cash Basis Accounting - This method of accounting is

frequently used but is not allowed (prohibited) under

generally accepted accounting principles (GAAP).

►Revenues are recognized only when cash is actually

received.

►Expenses are recognized only when cash is actually

paid.

►The problem: you can influence when you receive or pay

out cash to manipulate the Income Statement

Timing IssuesTiming IssuesTiming IssuesTiming Issues

Accrual versus Cash Basis of Accounting

4-5

Timing IssuesTiming IssuesTiming IssuesTiming Issues

The Revenue Recognition Principle is part of the Accrual Basis of Accounting

Companies recognize revenue

in the accounting period in which

it is earned. Recognized simply

means the activity is recorded in

the journal.

In a service enterprise, revenue

is earned and recognized at the

time the service is performed.

(mow lawn today and record

revenue today, even if you don’t

get paid until next month).

4-6

Timing IssuesTiming IssuesTiming IssuesTiming Issues

Papa Ron’s Lawn Mowing Service mows a lawn (performs

the service) on June 30, but… does not get paid until

July 11. There are 2 J/Es involved here, one on each date:

30

11

Accounts Receivable

June 30 200 July 11 200

Balance 0

Cash

July 11 200

Service Revenue

June 30 200

4-7

Adjusting entries are needed every time a

company wants to prepare their F/S (monthly,

quarterly or yearly) to ensure the revenue and

expense recognition principles are followed.

Adjusting entries Include one I/S account and

one B/S account which makes it possible to

report correct amounts on the I/S and the B/S.

The Basics of The Basics of AdjustingAdjusting Entries EntriesThe Basics of The Basics of AdjustingAdjusting Entries Entries

4-8

Get Paid $300 in May to mow lawns

over the summer

Cash 300 UnE Rev 300

Mow LawnIn June

Earn $100

UnE 100 Rev 100

Adjusting Entries - Deferrals

Mow LawnIn July

Earn $100

UnE 100 Rev 100

Mow LawnIn AugustEarn $100

UnE 100 Rev 100

Lawns are all mowed and the $300 has all

been earnedNo entry needed here!

Pay $800 in May to pre-pay rent (an asset)

For two months

Prepaid Rent 800 Cash 800

Stay in Apt.In June

Expense $400

Rent Exp. 400 Prepaid Rent 400

Stay in Apt.In July

Expense $400

Rent Exp. 400 Prepaid Rent 400

You’ve used up the $800 by staying in

the Apt.No entry needed

here!

1. Cash Out Now - Expense is “deferred” over time1. Cash Out Now - Expense is “deferred” over time

2. Cash In Now - Revenue is “deferred” over time2. Cash In Now - Revenue is “deferred” over time

4-9

You agree to mow lawns over summer but… you don’t get

paid until Sept.

No entries yet!

Mow LawnIn JuneRev 200

A/R 200 Rev 200

Adjusting Entries - Accruals

Mow LawnIn July

Rev $200

A/R 200 Rev 200

Mow LawnIn AugustRev $200

A/R 200 Rev 200

Sept. - Lawns are all mowed and now you

collect $600

Cash 600 A/R 600

Stay at an Apt. for 2 months @ $450 a

month… pay after the 2 month stay

No entries yet!

Stay in Apt.In June

Expense is $450

Rent Exp. 450 A/P 450

Stay in Apt.In July

Expense is $450

Rent Exp. 450 A/P 450

You stayed in the Apt, and now you pay $900

A/P 900 Cash 900

4. Expense is “accrued” when incurred – Cash Out Later4. Expense is “accrued” when incurred – Cash Out Later

3. Revenue is “accrued” when earned – Cash In Later3. Revenue is “accrued” when earned – Cash In Later

4-10

Types and Examples of Adjusting EntriesTypes and Examples of Adjusting EntriesTypes and Examples of Adjusting EntriesTypes and Examples of Adjusting Entries

Deferrals: CASH now, revenues & expenses deferred to later

1. Prepaid expenses: You pay the rent for 2 months before you move in; debit the asset “Pre-paid Rent” and credit “Cash”

2. Unearned revenues: You get paid before mowing the lawn; debit “Cash” and credit “Unearned Mowing Revenue”

Accruals: revenues & expenses accrued now, CASH later

3. Accrued revenues: You get paid after you mow the lawn; debit “Accounts Receivable” and credit “Mowing Revenue”

4. Accrued expenses: You pay the rent after 2 months of use; debit “Rent Expense” and credit “Accounts Payable”

4-11

Original Entries Adjusting Entries

1. Pre-paid Rent 800 Rent Expense 400

Cash 800 Pre-paid Rent 400

______________________________________________

2. Cash 300 Unearned Rev 100

Unearned Rev 300 Revenue 100

______________________________________________

3. Accts Rec 600 Cash 600

Revenue 600 Accts Rec 600

______________________________________________

4. Rent Expense 900 Accts Pay 900

Accts Pay 900 Cash 900

______________________________________________________________________________________________

Original Entries 1st - Adjusting Entries 2ndOriginal Entries 1st - Adjusting Entries 2nd

4-12

11. Adjusting Entries for “. Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””11. Adjusting Entries for “. Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

Supplies (usage)

Pre-paid Insurance (time)

Pre-paid Advertising (time)

Cash PaymentCash Payment Expense RecordedExpense RecordedBEFORE

Pre-paid Rent (time)

Equipment (long time)

Buildings (long time)

Prepayments often occur in regard to:

These start off as assets! Pay cash and record the

expense initially as an asset, it turns into an expense

either with the passage of time or through use. The

adjusting entry increases (a debit) an expense and a

decreases (a credit) an asset. Note: not all accounts use

the term “pre-paid” in their title.

4-13

Usage Adjustment: Sierra purchased supplies costing $2,500 on

October 5 recording the purchase by increasing (debiting) the asset Supplies

and crediting cash (not shown here). The balance of $2,500 on the October

31 trial balance needs to be adjusted because an inventory count at the close

of business on October 31 reveals that only $1,000 of supplies are still on

hand. This means $1,500 has been used up (2,500 – 1,000 = 1,500)

Supplies (the asset) 1,500

Supplies Expense 1,500Oct. 31

1.1. Adjusting Entries for “ Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””1.1. Adjusting Entries for “ Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

4-14

Over Time Adjustment: October, 1 Sierra pre-paid a $600 expense

for a one-year fire insurance policy with cash. Sierra recorded the payment by

increasing (debiting) the asset Prepaid Insurance. This account shows a

balance of $600 in the October 31 trial balance. However, insurance of $50

($600 ÷ 12) expires each month. So…. on Oct 31, the account needs a $50

adjustment!

Prepaid Insurance (the asset) 50

Insurance Expense 50Oct. 31

1.1. Adjusting Entries for “ Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””1.1. Adjusting Entries for “ Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

4-15

Depreciation of Long-Lived Assets

Buildings, equipment, and vehicles (long-lived assets –

meaning used over years) are initially recorded as

assets, rather than expenses, in the year acquired.

Companies report a portion of the cost of the asset as

an expense (called depreciation expense) during each

period of the asset’s useful life. With each passing year

the total amount of depreciation is kept in an account

called accumulated depreciation.

Note: Depreciation does not attempt to report the actual

change in the market value of the asset.

1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

4-16

Over A Long Time Adjustment: Oct 2 paid $5,000 cash for Equipment.

Assume the depreciation on $5,000 is $40 per month ($480 yearly). Each month

the I/S will have a $40 expense. The B/S will accumulate the monthly expenses

by adding $40 to the Accumulated Depreciation account each month until it

reaches the total of $5,000 (when the equipment is fully depreciated)

Accumulated Depreciation-Equip. (B/S) 40

Depreciation Expense (I/S) 40Oct. 31

1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

4-17

B/S Presentation for Depreciation

Accumulated Depreciation-Equipment is a contra asset account. It

shows up as a credit and thus subtracted from the related asset which

has a debit balance (see example below).

It appears on the B/S just after the account it offsets (Equipment). The

$4,960 (see below) is referred to as the book value of the equipment.

Book value is not the same as its market value (what it would sell for

on the current open market). Look at slide 32 to see how this would

appear on the Balance Sheet.

1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””1. 1. Adjusting Entries for “Adjusting Entries for “Prepaid ExpensesPrepaid Expenses””

Book Value =

4-18

22. Adjusting Entries for “. Adjusting Entries for “Unearned RevenuesUnearned Revenues””22. Adjusting Entries for “. Adjusting Entries for “Unearned RevenuesUnearned Revenues””

rent

airline tickets

mowing lawns

Cash ReceiptCash Receipt Revenue RecordedRevenue RecordedBEFORE

magazine subscriptions

customer deposits

shoveling snow

Unearned revenues often occur in regard to:

These start off as liabilities (obligations). The original receipt of

cash (debit) is recorded along with a liability (credit) because the

revenue has not been earned yet. The adjusting entry records

any revenue that has been earned and shows any liability that

might remain. The adjusting entry shows a decrease (a debit) to

a liability and an increase (a credit) to a revenue.

4-19

2. 2. Adjusting Entries for “Adjusting Entries for “Unearned RevenuesUnearned Revenues””2. 2. Adjusting Entries for “Adjusting Entries for “Unearned RevenuesUnearned Revenues””

Illustration: Sierra Corporation received $1,200 cash in advance on

October 2 from R. Knox for guide services for multi-day trips expected

to be completed by December 31. Unearned Service Revenue shows

a balance of $1,200 in the October 31 trial balance. For services

performed for Knox during October, Sierra determines that it has

earned $400 (of the $1,200) in October.

Service Revenue 400

Unearned Service Revenue 400Oct. 31

4-20

3. 3. Adjusting Entries for “Adjusting Entries for “Accrued RevenuesAccrued Revenues””3. 3. Adjusting Entries for “Adjusting Entries for “Accrued RevenuesAccrued Revenues””

rent

interest

services performed (mowing lawns, shoveling snow)

BEFORE

Accrued revenues often occur in regard to:

Cash ReceiptCash ReceiptRevenue RecordedRevenue Recorded

These start off with receivables! The revenues have

been earned and need to be recorded, but the cash

hasn’t been received yet. This adjusting entry results

in a debit to accounts receivable and a credit to

some type of revenue.

4-21

Illustration: In October, Sierra earned $200 for performing guide

services but was not immediately paid. Sierra sent out bills for these

services but the bill wasn’t mailed out until the first week of

November. An adjusting entry is needed at the end of Oct. to record

the revenue and the receivable.

Service Revenue 200

Accounts Receivable 200Oct. 31

3. 3. Adjusting Entries for “Adjusting Entries for “Accrued RevenuesAccrued Revenues””3. 3. Adjusting Entries for “Adjusting Entries for “Accrued RevenuesAccrued Revenues””

What if someone owed you Interest Receivable XXX Interest that you’ve earned? Interest Revenue XXX

4-22

4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””

BEFORE

Accrued expenses often occur in regard to:

Cash PaymentCash PaymentExpense RecordedExpense Recorded

taxes

salaries

rent

interest

These start off with payables! These expenses have

been incurred and need to be recorded, but the cash

hasn’t been paid yet. The adjusting entry results in a

debit to an expense and a credit to a liability (e.g.,

accounts payable).

4-23

4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””

Illustration: Sierra signed a 3 month note payable of $5,000 on Oct.1. The note requires Sierra to pay interest at an annual rate of 12%. First we multiply $5,000 by 12%. Then multiply by the fraction of the year being calculated (if 1 month multiply by 1/12,; if 2 months use 2/12; and so on)

Interest Payable 50

Interest Expense 50Oct. 31

4-24

4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””

Illustration: Sierra Corporation last paid salaries on October 26; the

next payment of salaries will not occur until November 9 (every two

weeks). The employees earn $400 a day ($2,000 for a 5 day work

week. This means accrued salaries at October 31 are $1,200 ($400 ×

3 days). See the next slide for the adjusting journal entry.

4-25

4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””4. 4. Adjusting Entries for “Adjusting Entries for “Accrued ExpensesAccrued Expenses””

Illustration: Sierra Corporation last paid salaries on October 26;

the next payment of salaries will not occur until November 9. The

employees receive total salaries of $2,000 for a five-day work

week, or $400 per day. Thus, accrued salaries at October 31 are

$1,200 ($400 x 3 days).

Salaries Payable 1,200

Salaries Expense 1,200Oct. 31

4-26

The Trial Balance “Before” Adjustments(this is from Chapter 3)

The Trial Balance “Before” Adjustments(this is from Chapter 3)

4-27

Summary of all the Summary of all the AdjustingAdjusting Journal Entries Journal EntriesSummary of all the Summary of all the AdjustingAdjusting Journal Entries Journal Entries

4-28

After all adjusting entries are journalized and posted the

company prepares another trial balance from the ledger

accounts: The “Adjusted” Trial Balance.

The adjusted trial balance’s purpose is to prove the

equality of debit balances and credit balances in the

ledger and is the primary basis for preparing the

Financial Statements!

The The AdjustedAdjusted Trial Balance Trial BalanceThe The AdjustedAdjusted Trial Balance Trial Balance

4-29

The The Adjusted Trial BalanceTrial BalanceThe The Adjusted Trial BalanceTrial Balance

SO 6SO 6

4-30

F/S are prepared directly from the

Adjusted Trial Balance - in this Order!

F/S are prepared directly from the

Adjusted Trial Balance - in this Order!

Balance Sheet

A = L & E

Income Statement

Rev - Exp

Retained Earnings

Statement

Any Div?

Preparing Financial StatementsPreparing Financial StatementsPreparing Financial StatementsPreparing Financial Statements

4-31

Preparing Financial StatementsPreparing Financial StatementsPreparing Financial StatementsPreparing Financial Statements

4-32

Preparing Financial StatementsPreparing Financial StatementsPreparing Financial StatementsPreparing Financial Statements

4-33

At the end of the accounting period, companies transfer the temporary

account balances to the permanent stockholders’ equity account -

Retained Earnings. At the beginning of the next period these balances

start over with zero balances. Closing entries should not be confused

with adjusting entries.

Closing the BooksClosing the BooksClosing the BooksClosing the Books

Common StockRetained Earnings

These 3 all get transferred to Retained Earnings

4-34

1. Service Revenue 10,600

Retained Earnings 10,600 Sierra’s

_________________________________ Retained Earnings

Beg Bal 0

2. Retained Earnings 7,740 10,600

Salaries Expense 5,200 7,740

Supplies Expense 1,500 500

Rent Expense 900 _______________

Insurance Expense 50 $ 2,360

Interest Expense 50

Depreciation Expense 40 Example: look at slide 25!

_________________________________ The Sal/Exp is credited to

transfer the balance to R/E

3. Retained Earnings 500 Sal/Exp is now 0 and starts

Dividends 500 over in the next period

Sierra’s Closing EntriesSierra’s Closing Entries

4-35

The purpose of the post-closing trial balance is to prove the equality of

the permanent account balances that the company carries forward into

the next accounting period. But remember the adjusted trial balance is

the the primary basis for the F/S preparation

Preparing a Post-Closing Trial BalancePreparing a Post-Closing Trial BalancePreparing a Post-Closing Trial BalancePreparing a Post-Closing Trial Balance

All temporary accounts will have zero balances.

These 3 have been reduced to Zero by being closed out

to Retained Earnings!

Common StockRetained Earnings

4-36

Summary of the Accounting Cycle of the Accounting CycleSummary of the Accounting Cycle of the Accounting Cycle

1. Analyze business transactions1. Analyze business transactions

2. Journalize the transactions

2. Journalize the transactions

6. Prepare an adjusted trial balance

6. Prepare an adjusted trial balance

7. Prepare financial statements

7. Prepare financial statements

8. Journalize and post closing entries

8. Journalize and post closing entries

9. Prepare a post-closing trial balance

9. Prepare a post-closing trial balance

4. Prepare a trial balance4. Prepare a trial balance

3. Post to ledger accounts3. Post to ledger accounts

5. Journalize and post adjusting entries:Deferrals/Accruals

5. Journalize and post adjusting entries:Deferrals/Accruals

4-37

Once again, the Debit Credit Summary

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Chapter 3-23

AssetsAssets

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-24

LiabilitiesLiabilities

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

StockholdersStockholders’’ EquityEquity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Common StockCommon Stock

Chapter 3-23

DividendsDividends

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

= +

Assets, Expenses & Dividends all go up with DebitsLiabilities, Owners Equity (Common Stock & Retained Earnings)

& Revenues all go up with Credits

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Retained EarningsRetained Earnings

DEAD = Debits increase Expenses, Assets, and Dividends

CLEaR = Credits increase Liabilities, Equity (Common Stock

& Retained Earnings) and Revenues

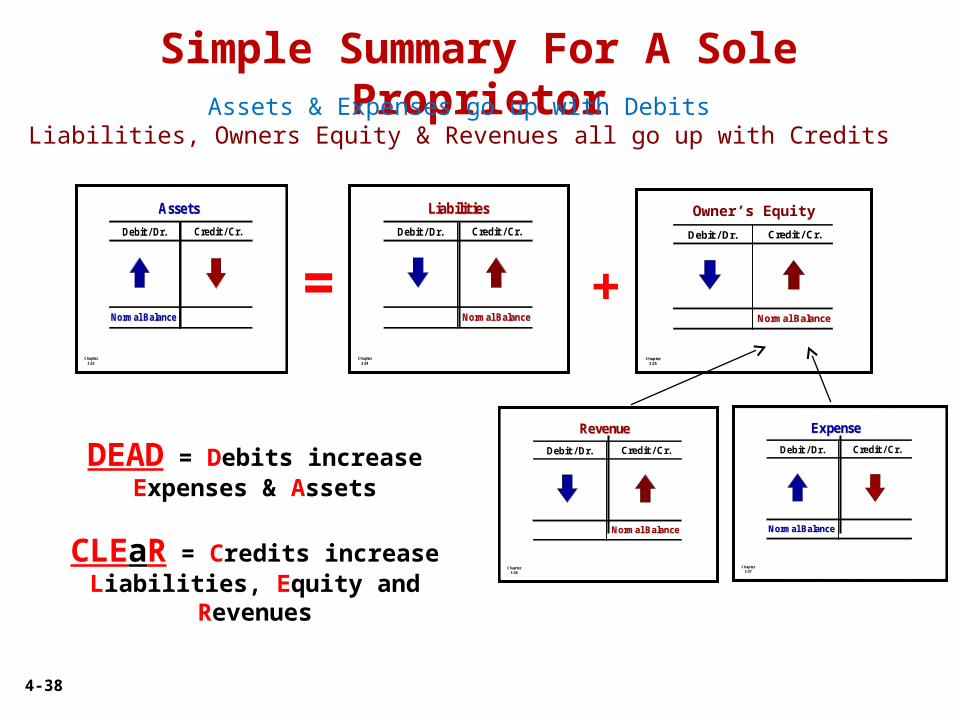

4-38

Simple Summary For A Sole Proprietor

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Chapter 3-23

AssetsAssets

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-24

LiabilitiesLiabilities

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

StockholdersStockholders’’ EquityEquity

= +

Assets & Expenses go up with DebitsLiabilities, Owners Equity & Revenues all go up with Credits

DEAD = Debits increase Expenses & Assets

CLEaR = Credits increase Liabilities, Equity and Revenues

Owner’s Equity