4th quarter 2010 ezomnotho - kzn treasury fiscal resource... · e-mail: [email protected]...

TRANSCRIPT

EZOMNOTHOTHE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

Department of EconomicDevelopment and TourismUmnyango Wezokuthuthukiswa

Komnotho Nezokuvakasha

KWAZULU-NATAL PROVINCIAL GOVERNMENT

th4 Quarter 2010

This report is for informational purposes and any comments or statements made herein do not necessarily

reflect the views of the KwaZulu-Natal Department of Economic Development and Tourism and its

collaborative partners. The information is intended for the recipient's use only and should not be cited,

reproduced or distributed to any third party without the prior consent of the author. Although great care is

taken to ensure accuracy of information, the author nor KwaZulu-Natal Department of Economic

Development and Tourism, cannot be held responsible for any decision made on the basis of the

information cited.

For enquires about this publication please contact the following:

Department of Economic Development and Tourism

Cosmas Hamadziripi

Economist, Policy and Planning Unit (Economic Planning)

Tel: +27(0) 33 264 2781

82 520 8715

Email: [email protected]

Website: http://www.kznded.gov.za

Eddie Musasiwa

Economist

33 264 2699

Cell : +27 (0) 82 771 8125

E-Mail: [email protected]

Website:

Trade and Investment KZN

Felleng Mahlatsi

Economist

31 368 9662

Fax : +27 (0) 86 501 0682

Cell : +27 (0) 78 456 4891

E-Mail: [email protected]

Website: www.tikzn.co.za

KZN Provincial Treasury

Nokuthemba Lembethe

Economist, Economic Analysis Unit

Tel: +27(0) 33 897 4444

Cell: +27(0) 82 059 0666

Email: [email protected]

Website: www.kzntreasury.gov.za

Cell : +27 (0)

Department of Economic Development and Tourism

Tel: +27(0)

http://www.kznded.gov.za

Tel: +27(0)

http://

http://

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW 1

1. INTRODUCTION ........................................................................................5

2. GLOBAL ECONOMIC DEVELOPMENTS AND OUTLOOK...........................6

3. DOMESTIC ECONOMIC DEVELOPMENTS................................................14

4. LABOUR MARKET TRENDS......................................................................22

5. EXCHANGE RATE .....................................................................................28

6. INFLATION ...............................................................................................29

1.1 Introduction .....................................................................................................................................5

1.2 Authorship of the publication ..........................................................................................................5

2.1 Global Economic Activity..................................................................................................................6

2.2 Trade Wars .......................................................................................................................................6

2.3 European debt crisis.........................................................................................................................6

2.4 Global economic growth trends.......................................................................................................7

2.4.1 Advanced Economies .........................................................................................................7

2.4.2 Emerging Economies ..........................................................................................................9

2.5 Unemployment, interest rates and inflation ..................................................................................11

2.6 International exchange rates..........................................................................................................12

2.7 Commodities ..................................................................................................................................12

2.7.1 Brent crude oil..................................................................................................................12

2.7.2 Platinum and gold ............................................................................................................13

3.1 Economic performance in South Africa..........................................................................................14

3.1.1 Quarter-on-quarter Gross Domestic Product (GDP) growth rates ...................................14th3.1.2 4 Quarter sectoral drivers of GDP growth ......................................................................14

3.1.3 2010 Growth Trends.........................................................................................................15th3.2 Regional growth developments: 4 quarter 2010..........................................................................16

3.2.1 Quarter-on-quarter GDP growth rates .............................................................................16

3.2.2 KwaZulu-Natal Quarter-on-quarter sectoral growth trends.............................................17

3.2.3 KwaZulu-Natal Annual Growth Trends .............................................................................18

3.2.4 KwaZulu-Natal Sectoral Annual Growth Trends................................................................18

3.2.5 Regional Annual 2010 Growth Rates................................................................................19

3.3 KwaZulu-Natal Growth Trends in Major Cities ...............................................................................19

3.3.1. Durban .............................................................................................................................20

3.3.2. Pietermaritzburg ..............................................................................................................20

3.3.3. Richards Bay .....................................................................................................................21

4.1 Labour market indicators – South Africa........................................................................................22

4.1.1 Employment trends in South Africa .................................................................................22

4.1.2 Unemployment trends in South Africa.............................................................................22

4.2 Provincial unemployment rates .....................................................................................................23

4.3 Comparative Provincial Employment Trends .................................................................................25th4.4 4 Quarter Employment Creation vis-à-vis Unemployment Increase Paradox ..............................25

4.5 Employment Creation per province ...............................................................................................26

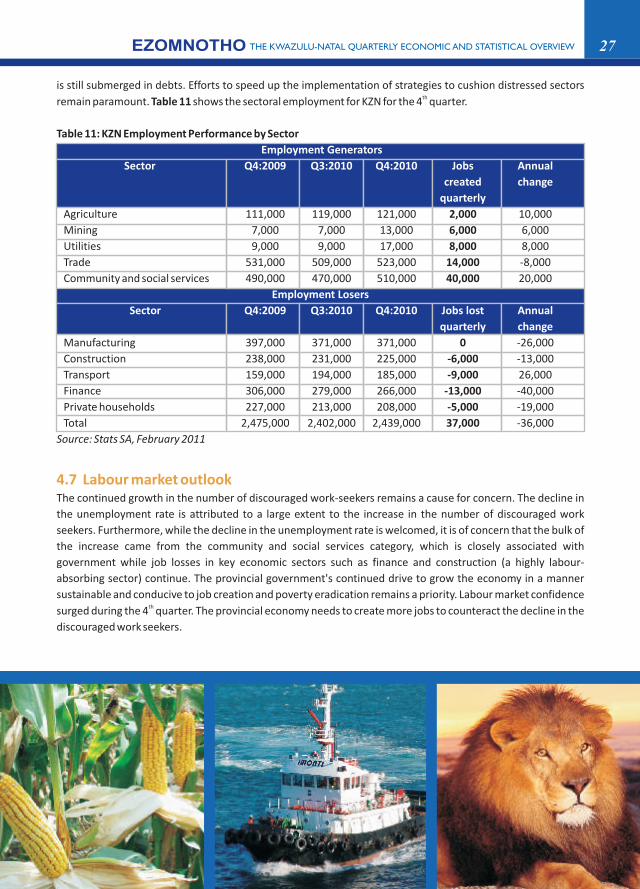

4.6 KZN employment levels by sector ..................................................................................................26

4.7 Labour market outlook...................................................................................................................27

5.1 Recent Exchange Rate Development..............................................................................................28

5.2 Implications for Exchange Rate Volatility .......................................................................................28

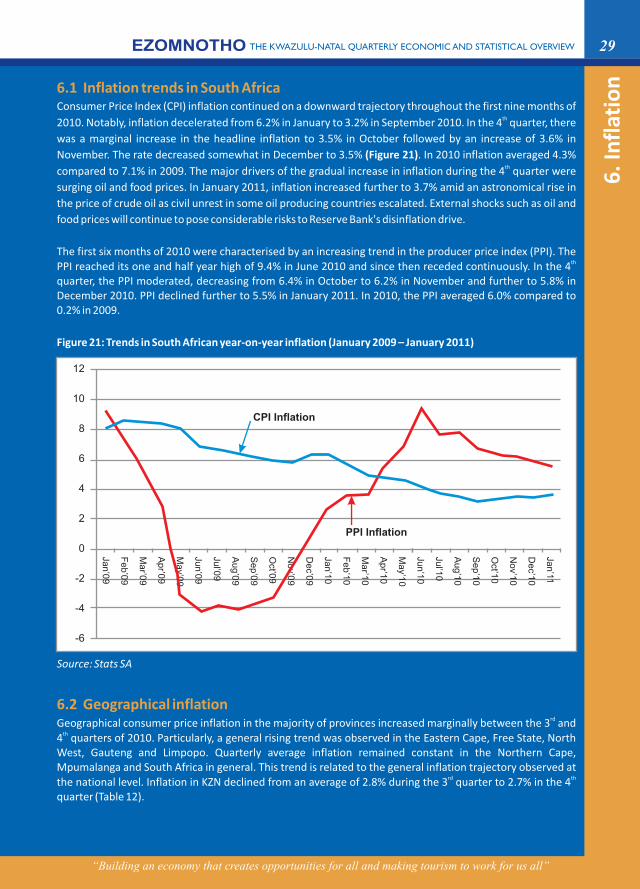

6.1 Inflation trends in South Africa ......................................................................................................29

6.2 Geographical inflation....................................................................................................................29

Tab

le O

f C

on

ten

ts

“Building an economy that creates opportunities for all and making tourism to work for us all”

6.3 Inflation outlook.............................................................................................................................30

7. INTERNATIONAL TRADE..........................................................................31

8. FOREIGN AND DOMESTIC INVESTMENT DEVELOPMENTS ...................33

9 OTHER ECONOMIC INDICATORS .............................................................37

10 2011/12 KWAZULU-NATAL PROVINCIAL BUDGET AT A GLANCE............45

11. POLICY ENVIRONMENT 2011/12............................................................48

12 REFERENCES.......................................................................................53

th7.1 South African Trade Performance: 4 quarter 2010.......................................................................31

7.2 Imports .........................................................................................................................................31

7.3 Exports .........................................................................................................................................31

7.4 South Africa Trade Highlights by World Zone: January 2011 .........................................................32

8.1 Domestic Investment Developments .............................................................................................33

8.2 KwaZulu-Natal investment performance, Q4 2010 ........................................................................34

8.2.1 Foreign Direct Investment Announcements.....................................................................35

8.2.2 Other investment projects in KwaZulu-Natal ...................................................................35

8.2.3 Latest Developments........................................................................................................35

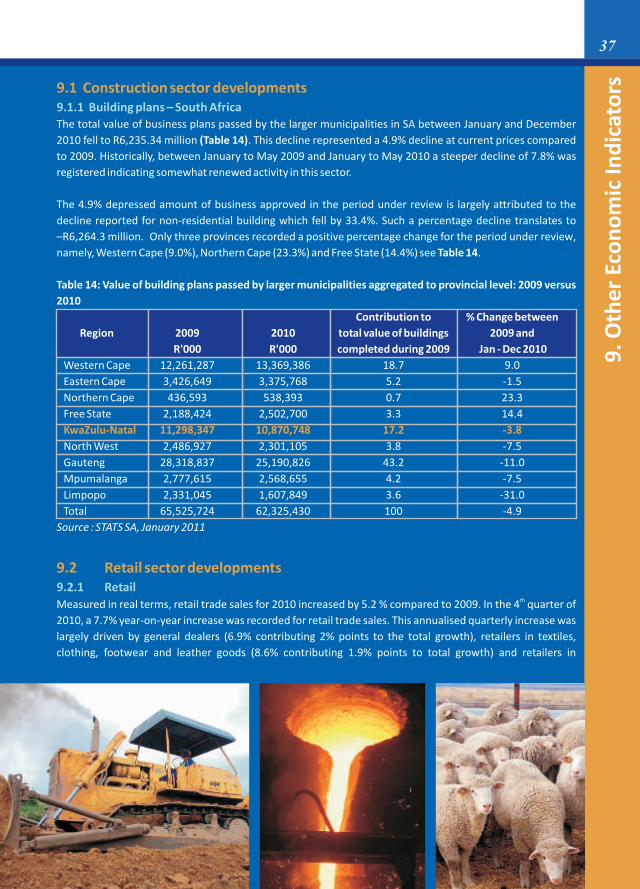

9.1 Construction sector developments ................................................................................................37

9.1.1 Building plans – South Africa............................................................................................37

9.2 Retail sector developments............................................................................................................37

9.2.1 Retail ................................................................................................................................37

9.2.2 Retail sales outlook ..........................................................................................................38

9.3 Motor sales developments.............................................................................................................38

9.4 Consumer debt developments.......................................................................................................39

9.4.1 Regional debt developments............................................................................................40

9.5 Liquidations and insolvency ...........................................................................................................41

9.6 Tourism developments...................................................................................................................41

9.6.1 International tourism developments ...............................................................................41

9.6.2 South African Tourism Developments ..............................................................................42

9.6.3 Tourism Accommodation .................................................................................................43

9.6.4 Tourism Migration ............................................................................................................44

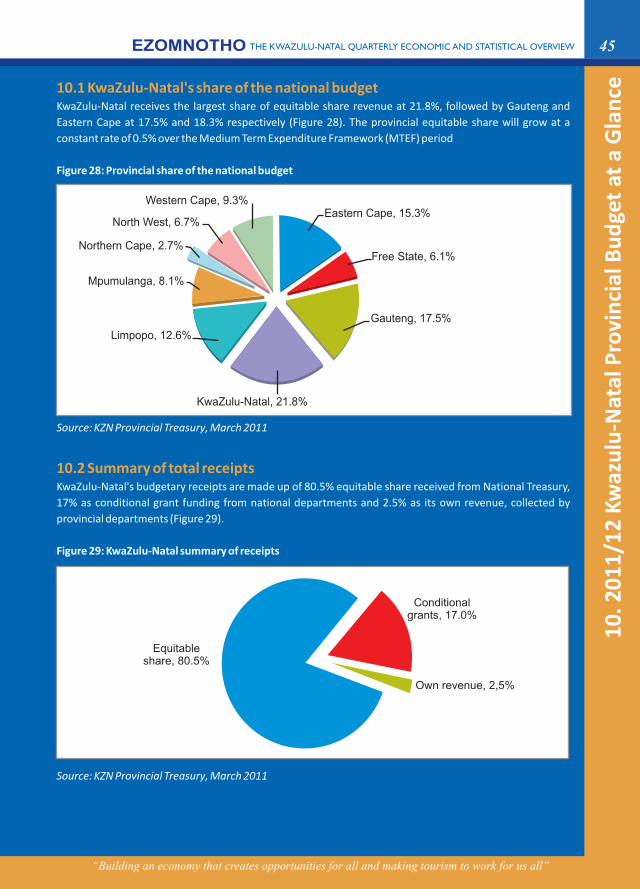

10.1 KwaZulu-Natal’s share of the national budget ...............................................................................45

10.2 Summary of total receipts..............................................................................................................45

10.3 KZN Budget Summary: Allocation by Department .........................................................................46

10.4 Budget Allocation per Department ................................................................................................46

10.5 Summary of infrastructure spending by Departments...................................................................47

11.1 National Policy Priorities ................................................................................................................48

11.1.1 New Growth Path (NGP)...................................................................................................48

11.1.2 Industrial Policy Action Plan (IPAP2).................................................................................48

11.1.2.1 IPAP2 Sector Priorities ..................................................................................49

11.2 KwaZulu-Natal Economic Policy Reviews and Policy Pronouncements ..........................................50

11.3 2011/12 KwaZulu-Natal Provincial Budget Policy Priorities ...........................................................50

11.3.1 Flagship programme.........................................................................................................50

11.3.2 Education .........................................................................................................................51

11.3.3 Health...............................................................................................................................51

11.3.4 Agrarian Reform ...............................................................................................................52

11.3.5 Decent Employment.........................................................................................................52

11.3.6 Crime................................................................................................................................52

2 EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

3

Table 1: World economic growth (%) outlook projections (January 2011) ...................................................10thTable 2: Unemployment, interest and inflation rates (%): 4 quarter 2010.................................................11

Table 3: Foreign exchange rates 4rd quarter of 2010- monthly averages ....................................................12

Table 4: Quarter-on-quarter change in GDP (seasonally adjusted) per sector at constant 2005 prices for South Africa (%) ............................................................................15

Table 5: 2010 real growth rates (%) per sector .............................................................................................15

Table 6: KZN quarter-on-quarter real growth rate per sector (%).................................................................18

Table 7: KwaZulu-Natal sectoral growth trends per annum ..........................................................................19

Table 8: Labour market indicators in KZN and comparative regions .............................................................23

Table 9: Unemployment rates per province (%)............................................................................................24

Table 10: SA regional employment by province (000s) .................................................................................26

Table 11: KZN Employment Performance by Sector......................................................................................27thTable 12: 4 Quarter geographical headline inflation ...................................................................................30

thTable 13: SA trade statistics, 4 Quarter 2010 and January 2011 (R billion) .................................................31

Table 14: Value of building plans passed by larger municipalities aggregated to provincial level: 2009 versus 2010............................................................................................37

Table 15: Contribution of each retailer to % change in retail sales (constant 2008).....................................38

Table 16: Contribution by activity type to change in motor trade sales .......................................................39

Table 17: Civil cases for debt .........................................................................................................................40

Table 18: Number of civil cases recorded according to selected magistrates' offices...................................40

Table 19: Number of SA residents and foreign travellers by mode of travellers ...........................................43

Table 20: Tourist accommodation .................................................................................................................43

Table 21: SA residents and foreign travellers by direction ............................................................................44

Table 22: Infrastructure spending by Departments ......................................................................................47

List

Of

Tab

les

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

Figure 1: Growth trends in sovereign indebted countries (quarter-on-quarter).............................................7rdFigure 2: OECD 3 quarter and 4 quarter growth trends...............................................................................7

Figure 3: Growth trends in major advanced countries (quarter-on-quarter)..................................................9

Figure 4: Growth trends in major emerging countries (quarter-on-quarter)................................................10

Figure 5: Price of crude oil (US$) - (March 2009 - December 2010) .............................................................13

Figure 6: Price of gold and platinum (US$) - (January 2009 – December 2010) ...........................................13

Figure 7: Annualised quarterly growth in GDP in South Africa (%) ...............................................................14

Figure 8: Sector contribution to SA GDP in 2010 ..........................................................................................16st thFigure 9: KZN quarter-on-quarter real GDP growth rate (1 Quarter 2008 - 4 2010) ..................................17

thFigure 10: 4 Quarter 2010 national and regional growth rates (%) .............................................................17

Figure 11: KwaZulu-Natal annual GDP Growth (%)- (2001-2010)..................................................................18

Figure 12: 2010 national and regional average growth rates (%)..................................................................19

Figure 13: Durban quarter-on-quarter and annualised GDP growth trends (seasonally adjusted) ..............20

Figure 14: Pietermaritzburg quarter-on-quarter and annualised GDP growth trends (seasonally adjusted)21

Figure 15: Richards bay quarter-on-quarter and annualised GDP growth trends (seasonally adjusted) ......21nd thFigure 16: Employment trends in South Africa (2 quarter of 2008 to 4 quarter of 2010) .........................22

nd thFigure 17: Trends in South African unemployment rate (%) - (2 quarter of 2008 to 4 quarter of 2010)...23ndFigure 18: Trends in comparative unemployment rates (2 quarter of 2008 to 4th quarter of 2010) .........24

ndFigure 19: Comparative employment trends (2 quarter of 2008 to 4th quarter of 2010) ..........................25

Figure 20: Trends in South African nominal exchange rates .........................................................................28

Figure 21: Trends in South African year-on-year inflation (January 2009 – January 2011)...........................29st rdFigure 22: Gross fixed capital formation by economic sector; 1 Quarter 2009 – 3 Quarter 2010

(annual % change) ....................................................................................................................33

Figure 23: Gross fixed capital formation in construction, and by business category; st rd1 quarter 2009 – 3 Quarter 2010 (annual % change) ............................................................34

stFigure 24: Share (%) of Gross fixed capital formation by business category (1 quarter 2009 – rd3 quarter 2010) .......................................................................................................................34

Figure 25: New and used vehicle sales in 2010 (year on year % change) .....................................................39

Figure 26: South African number of liquidations (2008-2010)......................................................................41

Figure 27: Total income and occupancy rate trends (2010) .........................................................................44

Figure 28: Provincial share of the national budget .......................................................................................45

Figure 29: KwaZulu-Natal summary of receipts ............................................................................................45

Figure 30: Percentage share of the total budget for 2011/12 Financial Year................................................46

th

List

Of

Figu

res

4 EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

5

1. I

ntr

od

uct

ion1.1 Introduction

1.2 Authorship of the publication

The publication aims to present economic trends for the province to our respective stakeholders and policy makers. Notably, the publication provides detailed statistics on Gross Domestic Product (GDP), employment, inflation, foreign and domestic investment and international trade. Furthermore, the publication highlights developments in the South African and the provincial economies with emphasis on priority sectors in KwaZulu-Natal (KZN) Province.

The main data sources used are Statistics South Africa (Stats SA) and the Reserve Bank (SARB). Other data sources used in this report are Quantec, Global Insight, Naamsa, and Department of Trade and Industry, the National Treasury, and the Financial Times.

Ezomnotho is a collaborative effort by the KwaZulu-Natal Department of Economic Development and Tourism (KZNDEDT), Economic Planning Programme; KwaZulu-Natal Provincial Treasury, Macro-Economic Analysis Unit; and Trade and Investment KwaZulu-Natal (TIKZN).

The Economic Planning Programme is critical to enhance efficiency and effectiveness of the KZNDEDT. This is mainly through facilitation and promotion of economic development policies, strategies and programmes. The programme is made up of four sub-programmes; Policy and Planning, Research and Development, Knowledge Management, and Monitoring and Evaluation.

Its purpose is pivoted around the following:

• Provision of economic and investment opportunity information to various stakeholders.

• Provision of leadership and guidance in the development of provincial economic policies and strategies.

• Monitoring the implementation of economic policies and strategies, and periodically evaluating them with a view to determining their effectiveness.

• Providing management with information on which strategic decision making processes are based to enhance the overall efficiency and effectiveness of the Department.

The purpose of the KZN Treasury's Macro-Economic Analysis Unit is to determine and evaluate economic parameters and socio-economic imperatives within a provincial, local, and national macro-economic context. It also provides the KwaZulu-Natal Treasury and Executive with sound statistical information for decisions on the Medium Term Expenditure Framework (MTEF) and budget framework allocations.

TIKZN is a provincial trade and investment promotion agency, developed to promote the province of KwaZulu-Natal (KZN) as an investment destination. It facilitates trade by assisting local companies to identify markets and export their products. Part of TIKZN's strategic objectives is strengthening the organisation's knowledge management capabilities, through production and dissemination of new knowledge outputs, and development of investment packages for potential domestic and international investments by means of packaging sector opportunities.

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

2.1 Global Economic Activity

2.2 Trade Wars

2.3 European debt crisis

Global economic activity increasingly gained momentum in 2010, with emerging markets and developing

countries being the major drivers of growth. The global economy benefited largely from the humongous

monetary and fiscal stimuli undertaken in most parts of the world. The year also witnessed fears of double-dip

recession brought about by the euro area debt crisis which emanated from Greece. Despite these fears, global

economic recovery continued apace in 2010 amid convincing signs that growth momentum in the global

economy will remain largely sustained. As a result, growth in most industrialised countries especially the Euro tharea remained modest. In the 4 quarter of 2010, global economic growth continued to be characterised by a

two-speed recovery. In advanced economies, economic growth remained largely subdued against a backdrop of

lacklustre consumer demand, bad weather and the euro debt crisis. Consequently, growth in the advanced

economies is expected to be moderate in 2011.

In many emerging economies, activity remained buoyant, inflation pressures are emerging, and there are now

some signs of overheating, driven in part by strong capital inflows. Most developing countries, particularly in sub-

Saharan Africa, are also growing strongly anchored mainly by exports growth as consumer confidence rebound

globally. IMF expects global output to expand by 4.4% and 4.5% in 2011 and 2012 respectively (Table 1).

The year 2010 was characterized by looming trade wars especially between the US and China as competition for

subdued global markets remained solid. Lacklustre growth in consumer confidence inherently made export

recovery in most countries unattainable. Resultantly, countries have resorted to exchange rate manipulation and

other tactics to remain competitive. In addition, increased capital inflows experienced in emerging markets

exerted pressure on their currencies and eventually hurt export competiveness. Poor performance of exports in

a number of countries have seen Central Banks worldwide intervening through tightening monetary policies and

exchange rate manipulation in an endeavour to increase export competitiveness. This practice has been viewed

by several economists as highly distortionary and a major cause for global trade imbalances. Such tendencies

have led to the so called currency war which culminated into trade war. In particular, China and the US had a

series of conflicts on currency or exchange rate manipulation. The world perceives these two as the worst

offenders to such practices. In response to these wars, the International Monetary Fund (IMF) suggested the

need for rules to govern the use of capital controls.

China was blamed by many countries for excessively under-valuing the Yuan in favour of their exports. The robust

economic growth recorded in China during the recession is attributed to uninterrupted export growth during the

recession. China continues to enjoy favourable terms of trade against its trading partners. Brazil on the other

hand, launched controls on foreign investment inflows in September 2010, in an attempt to reduce impact on its

exchange rate. It further envisages lobbying the World Trade Organisation (WTO) to classify exchange-rate

manipulation as a form of export subsidy. Trade wars continue to be topical and are one of the priority issues on

the G20 agenda for 2011.

Global economic recovery suffered a major hindrance with the turmoil of sovereign debt markets which started stduring the 1 quarter of 2010. The European debt crisis sent major jitters to worldwide markets and slowed

down economic recovery in a number of countries. The Euro Area sovereign debt problems stemmed from the

insolvency of the Greek government. Contagion effects of Greece's debt crisis were felt in many other countries

with Spain, Portugal and Ireland being the worst affected. Ireland is the second EU country which received bailout

in 2010 after Greece. Spain and Portugal were also in the spotlight as their debt-laden governments battle to

contain economic woes bedevilling their economies. The continued bailout of European countries is an

indication of the devastating impact of the global economic recession. Economic growth in these countries 1remains highly subdued (Figure 1).

2. G

lob

al E

con

om

ic D

eve

lop

me

nts

an

d O

utl

oo

k6 EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

th1. 4 Quarter data for Ireland was not available at the time of printing

“Building an economy that creates opportunities for all and making tourism to work for us all”

Source: Trading Economics, February 2011

Economic growth in most industrialised countries especially in the Euro area remained modest despite fiscal

expansion in 2010. IMF reported that economic growth in the advanced economies averaged 3.0% in 2010.

Growth in industrialised economies is expected to average 2.5% in both 2011 and 2012.

thGross domestic product (GDP) in the OECD area grew by 0.4% in the 4 quarter of 2010, down from 0.6%

recorded in the previous quarter (Figure 2).

rd thFigure 2: OECD 3 quarter and 4 quarter GDP growth trends

Source: OECD Statistics

thDuring the 4 quarter of 2010, US GDP increased by about 2.8% compared with the previous quarter (2.6% in the rd th rd3 quarter) see Figure 3. Compared with the 4 quarter of 2009, US GDP rose by 2.8% (after 3.2% in the 3

2.4 Global economic growth trends2.4.1 Advanced Economies

Organisation for Economic Co-operation and Development (OECD)

United States of America (US)

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

%

OE

CD

-To

tal

Eu

rop

ea

n U

nio

n

Eu

ro a

rea

Ma

jor

se

ve

n

Ca

na

da

Fra

nce

Ge

rma

ny

Ita

ly

Ja

pa

n

Un

ite

d K

ing

do

m

Un

ite

d S

tate

s

2010: Q3 2010: Q4

Figure 1: Growth trends in sovereign indebted countries (quarter-on-quarter)

7

2

0

-2

-4

-6

-8

-10

2010:Q1

2010:Q2

2009:Q3

2010:Q3

2009:Q4

2010:Q4

2009:Q2

2009:Q1

2008:Q4

2008:Q3

2008:Q2

2008:Q1

Ireland Greece Spain Portugal

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

8

thquarter). The acceleration in real GDP in the 4 quarter primarily reflected a sharp downturn in imports, an

increase in personal consumption expenditures (PCE), and an upturn in residential fixed investment that were

partly offset by downturns in private inventory investment and in government spending and a deceleration in

nonresidential fixed investment. Economic growth in 2010, thus averaged 2.8% compared to a decrease of 2.6%

registered in 2009. IMF expects average GDP growth rates of 3.0% and 2.7% in 2011 and 2012 respectively.

thThe Japanese economy contracted by 0.3% in the 4 quarter of 2010, amid slowing exports and weak domestic

demand (Figure 3). Private consumption declined by 0.7%, partly due to the expiry of state subsidies for buyers

of “environmentally friendly” automobiles and other economy-boosting government measures . Exports fell by th0.7% resulting in net trade making a negative contribution to 4 quarter growth. This contraction was equivalent

to a 1.1% annualized decline and was Japan's first in more than a year and came after the expiry of government

subsidies on consumer goods. Analysts view this data as providing sufficient evidence that China has decisively

surpassed Japan as the world's second largest economy after the US in dollar terms. These developments

caused the Japanese economy to grow at 3.9% in 2010 lower than the 4.3% projected by IMF. IMF projected

growth outlook is 1.6% and 1.8% in 2011 and 2012 respectively.

thGDP increased by 0.3% in the Euro Area (EA16) and by 0.2% in the EU27 during the 4 quarter of 2010, rdcompared with the previous quarter . In the 3 quarter of 2010, growth rates were 0.4% in both zones. The Euro

area posted an average growth of 1.8% in 2010 following a 4.1% decline in 2009. Economic growth in the Euro

area is expected to average 1.5% and 1.7% in 2011 and 2012 respectively.

th rdThe German economy expanded by 0.4% in the 4 quarter following a 0.8% growth in the 3 quarter (Figure 3).

In 2010, the German economy grew by 3.6% compared to 4.7% contraction in 2009. Buoyant growth in 2010 was

boosted strongly by increased exports to China and other Asian countries. The IMF expects growth to average

2.2% and 2.0% in 2011 and 2012 respectively.

thUK GDP shrank by 0.6% in the 4 quarter of 2010, compared with an increase of 0.7% in the previous quarter th(Figure 3). The GDP estimate was significantly affected by the bad weather in December. The decline in the 4

quarter is due to decreases in services and construction output. The largest contributor to the decline in this thquarter was from business services and finance. Construction output decreased by 3.3% in the 4 quarter

compared with a rise of 3.9% in the previous quarter. IMF reports that real GDP in the U.K averaged 1.7% in 2010.

thFrance GDP expanded by 0.3% in the 4 quarter of 2010. On an annual basis, a growth rate of 1.5% was recorded.

The IMF expects the French economy to grow by 1.6% in 2011 and 1.8% in 2011 and 2012 respectively. The

lacklustre growth projections for France indicate that the Euro zone economy is still struggling to emerge out of

the recession.

Japan

Euro Area

Germany

United Kingdom (UK)

France

2

4

5

3

Growth rates of 2.0% and 2.3% are expected in 2011 and 2012 respectively.

2. Trading Economics 2011

3. The Euro Area (EA16) consists of Belgium, Germany, Ireland, Greece, Spain, France, Italy, Cyprus, Luxembourg, Malta, the Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland.

4.The EU27 includes Belgium, Bulgaria, the Czech Republic, Denmark, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Latvia, Lithuania, Luxembourg, Hungary, Malta, the Netherlands, Austria, Poland, Portugal, Romania, Slovenia, Slovakia, Finland, Sweden and the United Kingdom.

5. Flash estimates published by Eurostat, the statistical office of the European Union.

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

9

Figure 3: Growth trends in major advanced countries (quarter-on-quarter)

Source: Trading Economics , February 2011

Robust economic growth in most emerging and developing countries continue to be a force behind buoyant

global economic growth in 2010. It averaged 7.1% in 2010. IMF expects growth rates of 6.5% in both 2011 and

2012. High economic growth rates in 2010 were recorded in countries such as China, India and Brazil. Robust

growth in exports and strong consumer demand were the major drivers of economic activity.

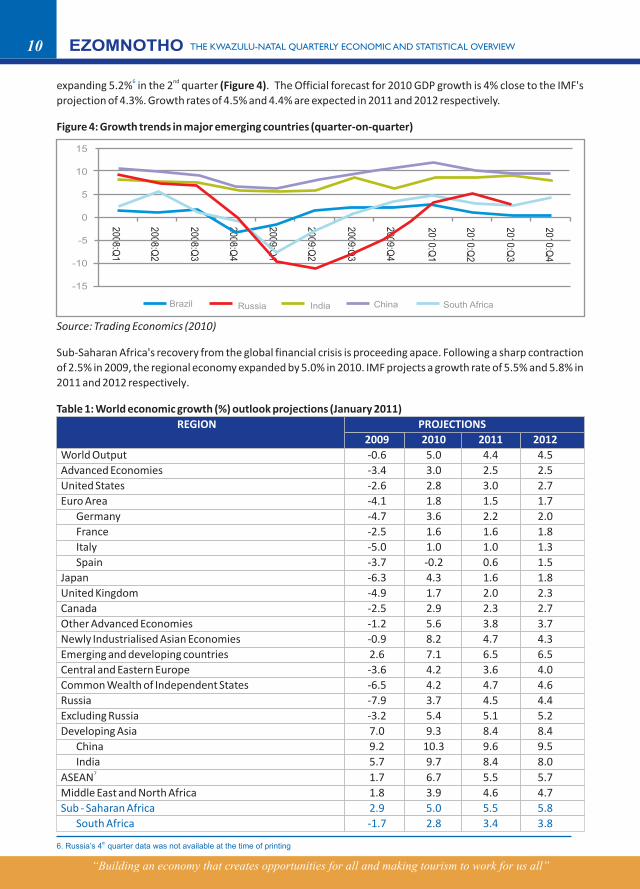

thChina's real GDP growth sped up unexpectedly in the 4 quarter despite a series of tightening measures by the th rdGovernment. China's GDP grew by 9.8% in the 4 quarter, faster than the 3 quarter's 9.6% (Figure 4). Economic

growth in 2010 largely reflects buoyant industrial output supported by rebound global demand. China's

industrial value-added output was up 15.7% for 2010 compared to 4.7% in 2009. China runs a trade surplus with

almost all of its major trading partners. China's GDP grew by 10.3% in 2010, above 2009's 9.2% expansion

(Table 1).

thReal GDP in India expanded by 8.2% in the 4 quarter of 2010 (Figure 4). This was the fourth successive quarter

of GDP growth in excess of 8%. Drivers of Indian growth during 2010 were strong domestic demand, rising

exports and expanding services. Exports grew by 16.2% year-on-year, private consumption expanded by 9%,

while business investment grew by 6%. Analysts believe that India's growth rate is set to rival China's in 2011.

IMF expects India's growth rate to average 8.4% in 2011 and 8.0% in 2012.

thBrazilian economy expanded slower than expected in the 4 quarter, though the rate of growth accelerated

from the previous quarter. The seasonally adjusted gross GDP grew by 0.7% quarter-on-quarter in the rd(Figure 4). This follows a 0.4% expansion in the 3 quarter, revised from

steady growth rate of 7.5% compared to 2009. According to the

Brazilian statistical office, the 2010 growth rate is the highest annual rate since 1986. IMF expects economic

growth to average 4.5% and 4.1% in 2011 and 2012 respectively.

Russia's economy grew at its slowest pace in 2010 against a backdrop of record heat that triggered crop losses, rdforced manufacturers to halt output and crippled consumer demand. GDP grew 2.7% in the 3 quarter after

2.4.2 Emerging Economies

China

India

Brazil

Russia

th 4 quarter

0.5% rise reported initially. Year-on-year, rdthe GDP growth eased to 5% from 6.7% in the 3 quarter, while economists had forecast a slowdown to 5.2%. In

2010, the economy maintained an expected

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

2010:Q1

2010:Q2

2009:Q3

2010:Q3

2009:Q4

2010:Q4

2009:Q2

2009:Q1

2008:Q4

2008:Q3

2008:Q2

2008:Q1

6

4

2

0

-2

-4

-6

-8USA Japan UK Germany France

“Building an economy that creates opportunities for all and making tourism to work for us all”

10

ndexpanding 5.2% in the 2 quarter (Figure 4). The Official forecast for 2010 GDP growth is 4% close to the IMF's

projection of 4.3%. Growth rates of 4.5% and 4.4% are expected in 2011 and 2012 respectively.

Figure 4: Growth trends in major emerging countries (quarter-on-quarter)

Source: Trading Economics (2010)

Sub-Saharan Africa's recovery from the global financial crisis is proceeding apace. Following a sharp contraction

of 2.5% in 2009, the regional economy expanded by 5.0% in 2010. IMF projects a growth rate of 5.5% and 5.8% in

2011 and 2012 respectively.

Table 1: World economic growth (%) outlook projections (January 2011)

World Output -0.6 5.0 4.4 4.5

Advanced Economies -3.4 3.0 2.5 2.5

United States -2.6 2.8 3.0 2.7

Euro Area -4.1 1.8 1.5 1.7

Germany -4.7 3.6 2.2 2.0

France -2.5 1.6 1.6 1.8

Italy -5.0 1.0 1.0 1.3

Spain -3.7 -0.2 0.6 1.5

Japan -6.3 4.3 1.6 1.8

United Kingdom -4.9 1.7 2.0 2.3

Canada -2.5 2.9 2.3 2.7

Other Advanced Economies -1.2 5.6 3.8 3.7

Newly Industrialised Asian Economies -0.9 8.2 4.7 4.3

Emerging and developing countries 2.6 7.1 6.5 6.5

Central and Eastern Europe -3.6 4.2 3.6 4.0

Common Wealth of Independent States -6.5 4.2 4.7 4.6

Russia -7.9 3.7 4.5 4.4

Excluding Russia -3.2 5.4 5.1 5.2

India 5.7 9.7 8.4 8.0

ASEAN 1.7 6.7 5.5 5.7

Middle East and North Africa 1.8 3.9 4.6 4.7

6

7

REGION PROJECTIONS

2009 2010 2011 2012

Developing Asia 7.0 9.3 8.4 8.4

China 9.2 10.3 9.6 9.5

Sub - Saharan Africa 2.9 5.0 5.5 5.8

South Africa -1.7 2.8 3.4 3.8

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

2010:Q1

2010:Q2

2009:Q3

2010:Q3

2009:Q4

2010:Q4

2009:Q2

2009:Q1

2008:Q4

2008:Q3

2008:Q2

2008:Q1

Brazil Russia India China South Africa

15

10

5

0

-5

-10

-15

th6. Russia’s 4 quarter data was not available at the time of printing

“Building an economy that creates opportunities for all and making tourism to work for us all”

11

Latin America and the Caribbean -1.8 5.9 4.3 4.1

Brazil -0.6 7.5 4.5 4.1

Mexico -6.1 5.2 4.2 4.8

World Trade Volume (goods and services) -10.7 12.0 7.1 6.8

Import

Advanced Economies -12.4 11.1 5.5 5.2

Emerging and Developing Countries -8.0 13.8 9.3 9.2

Exports

Advanced Economies -11.9 11.4 6.2 5.8

Emerging and developing countries -7.5 12.8 9.2 8.8

Source: IMF-World Economic Outlook, January 2011

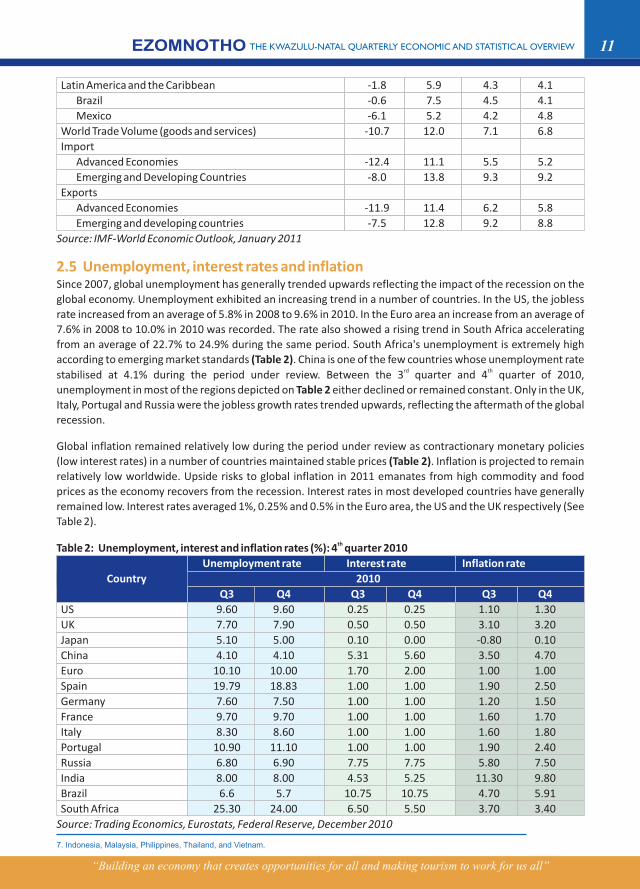

Since 2007, global unemployment has generally trended upwards reflecting the impact of the recession on the

global economy. Unemployment exhibited an increasing trend in a number of countries. In the US, the jobless

rate increased from an average of 5.8% in 2008 to 9.6% in 2010. In the Euro area an increase from an average of

7.6% in 2008 to 10.0% in 2010 was recorded. The rate also showed a rising trend in South Africa accelerating

from an average of 22.7% to 24.9% during the same period. South Africa's unemployment is extremely high

according to emerging market standards (Table 2). China is one of the few countries whose unemployment rate rd thstabilised at 4.1% during the period under review. Between the 3 quarter and 4 quarter of 2010,

unemployment in most of the regions depicted on Table 2 either declined or remained constant. Only in the UK,

Italy, Portugal and Russia were the jobless growth rates trended upwards, reflecting the aftermath of the global

recession.

Global inflation remained relatively low during the period under review as contractionary monetary policies

(low interest rates) in a number of countries maintained stable prices (Table 2). Inflation is projected to remain

relatively low worldwide. Upside risks to global inflation in 2011 emanates from high commodity and food

prices as the economy recovers from the recession. Interest rates in most developed countries have generally

remained low. Interest rates averaged 1%, 0.25% and 0.5% in the Euro area, the US and the UK respectively (See

Table 2).

thTable 2: Unemployment, interest and inflation rates (%): 4 quarter 2010

US 9.60 9.60 0.25 0.25 1.10 1.30

UK 7.70 7.90 0.50 0.50 3.10 3.20

Japan 5.10 5.00 0.10 0.00 -0.80 0.10

China 4.10 4.10 5.31 5.60 3.50 4.70

Euro 10.10 10.00 1.70 2.00 1.00 1.00

Spain 19.79 18.83 1.00 1.00 1.90 2.50

Germany 7.60 7.50 1.00 1.00 1.20 1.50

France 9.70 9.70 1.00 1.00 1.60 1.70

Russia 6.80 6.90 7.75 7.75 5.80 7.50

India 8.00 8.00 4.53 5.25 11.30 9.80

Brazil 6.6 5.7 10.75 10.75 4.70 5.91

South Africa 25.30 24.00 6.50 5.50 3.70 3.40

Source: Trading Economics, Eurostats, Federal Reserve, December 2010

2.5 Unemployment, interest rates and inflation

Unemployment rate Interest rate Inflation rate

Country 2010

Q3 Q4 Q3 Q4 Q3 Q4

Italy 8.30 8.60 1.00 1.00 1.60 1.80

Portugal 10.90 11.10 1.00 1.00 1.90 2.40

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

7. Indonesia, Malaysia, Philippines, Thailand, and Vietnam.

“Building an economy that creates opportunities for all and making tourism to work for us all”

12

2.6 International exchange rates

2.7 Commodities

With the exchange currency war looming and continuing, most of emerging economies currencies

strengthened amid investors' appetite for emerging market assets (equities and bonds). This enormous

appetite for emerging market investments is regarded as downside competitiveness risks. The hunger for

emerging market investment assets is driven primarily by relatively higher returns on investment in emerging

markets vis-à-vis subdued interest rates in advanced economies. SA is one of the countries whose exchange rate ndhas been resilient against the US dollar. In the 2 half of 2010, the Rand appreciated by 17% against the US$,

higher compared to most emerging economies. By the end of 2010, the trade- weighted exchange rate rdstrengthened by 47% and in the 3 quarter of 2010. China and the US currencies have generally stabilised during

ththe 4 quarter of 2010 due to currency manipulation by the two countries. The Euro zone economy somewhat thstabilized, with the Euro strengthening during the 4 quarter. High unemployment in the Euro area remains a

challenge for policy makers.

thTable 3: M Foreign Exchange Rates 4 Quarter 2010

GBP£/USD 0.63 0.63 0. 64

USD/ EUR(€) 1.39 1.37 1.32

JPY(¥)/USD 81.8 82.6 83.4

CNY/USD 6.67 6.65 6.65

6.92 6.98 6.82

Source: http//www.fxtop.com, December 2010

Commodities are on top list of favourable and safe investment vehicles as volatility in the currency market

continues. Commodities such as oil, gold and platinum were largely the most sought after. Lucrative commodity

prices have buoyed economic growth in most emerging markets. Continued rise of commodity prices such as oil

and food is, however, a threat to the disinflation growth path in South Africa. This so given that commodities and

food constitute a relatively large weight on South African Consumer Price Index (CPI)

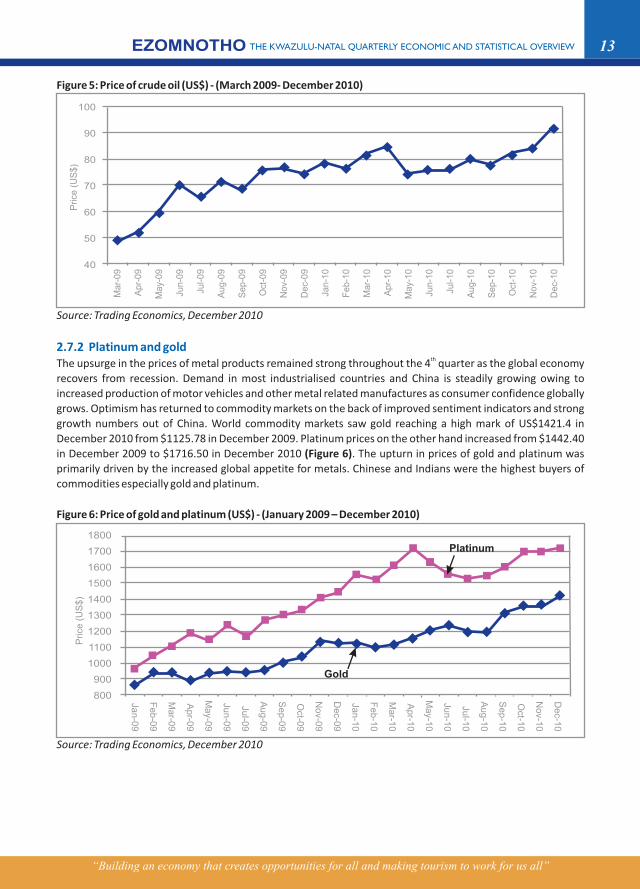

Since May 2010, the price of oil increasingly gained momentum as the global economy recovered. The pace

accelerated due to the winter season in the western countries bringing the price of oil close to $US100 by end of

2010 (Figure 5). The price of oil was expected to rise further as public demonstrations continue in Libya and

parts of the Arab world. Despite Saudi Arabia's promise to increase production in an attempt to bridge output

gap caused by production bottlenecks in Libya, the prices of oil remained above the US$100 mark. The

continued rise in the price of oil is a threat to global economic recovery at a time when the world economy is

battling to contain the aftermath of the recession such as the Euro debt crisis.

onthly Average

Currency October November December

ZAR(R)/USD

2.7.1 Brent crude oil

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

13

Figure 5: Price of crude oil (US$) - (March 2009- December 2010)

Source: Trading Economics, December 2010

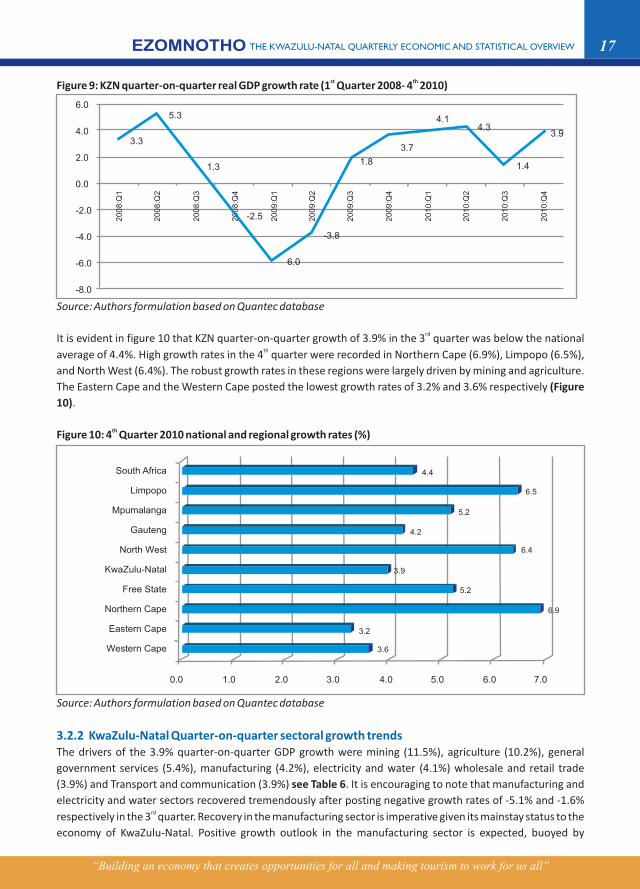

thThe upsurge in the prices of metal products remained strong throughout the 4 quarter as the global economy

recovers from recession. Demand in most industrialised countries and China is steadily growing owing to

increased production of motor vehicles and other metal related manufactures as consumer confidence globally

grows. Optimism has returned to commodity markets on the back of improved sentiment indicators and strong

growth numbers out of China. World commodity markets saw gold reaching a high mark of US$1421.4 in

December 2010 from $1125.78 in December 2009. Platinum prices on the other hand increased from $1442.40

in December 2009 to $1716.50 in December 2010 (Figure 6). The upturn in prices of gold and platinum was

primarily driven by the increased global appetite for metals. Chinese and Indians were the highest buyers of

commodities especially gold and platinum.

Figure 6: Price of gold and platinum (US$) - (January 2009 – December 2010)

Source: Trading Economics, December 2010

2.7.2 Platinum and gold

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

100

90

80

70

60

50

40

Price

(U

S$

)

Ma

r-0

9

Ap

r-0

9

Ma

y-0

9

Jun

-09

Jul-0

9

Au

g-0

9

Se

p-0

9

Oct

-09

No

v-0

9

De

c-0

9

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-1

0

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Price

(U

S$

)D

ec-1

0

No

v-10

Oct-1

0

Se

p-1

0

Au

g-1

0

Jul-1

0

Jun

-10

Ma

y-10

Ap

r-10

Ma

r-10

Fe

b-1

0

Jan

-10

De

c-09

No

v-09

Oct-0

9

Se

p-0

9

Au

g-0

9

Jul-0

9

Jun

-09

Ma

y-09

Ap

r-09

Ma

r-09

Fe

b-0

9

Jan

-09

1800

1700

1600

1500

1400

1300

1200

1100

1000

900

800

Gold

Platinum

“Building an economy that creates opportunities for all and making tourism to work for us all”

“Building an economy that creates opportunities for all and making tourism to work for us all”

143

. Do

me

stic

Eco

no

mic

Dev

elo

pm

en

ts 3.1 Economic performance in South Africa3.1.1 Quarter-on-quarter Gross Domestic Product (GDP) growth rates

th3.1.2 4 Quarter sectoral drivers of GDP growth

thEconomic growth in South Africa accelerated at 4.4% in the 4 quarter of 2010. This follows a 2.7% (revised th thfrom 2.6%) growth rate in the preceding quarter (Figure 7). The robust 4 quarter growth rate is the 6

rdconsecutive positive quarterly growth rate recorded since the end of recession in the 3 quarter of 2009. This

provides sufficient evidence that the economy has fully recovered from the recession. The modest growth in themployment during the 4 quarter further substantiates this observation. However, the stickiness of

unemployment rate around 24% remains a cause for concern for policy makers. IMF expects the South

African economy to register a growth rate of 3.4% and 3.8% in 2011 and 2012 respectively. Based on these

projections, the output gap in South Africa will remain negative and GDP growth is expected to stay behind

potential over the next two years. Economic growth prospects will depend primarily on strong consumer

confidence and increased government spending on infrastructure. However, there are indications that the

outlook for output growth, while hesitant, is somewhat more positive. Furthermore, the recovery in

household consumption expenditure appears to be sustained.

Figure 7: Annualised quarterly growth in GDP in South Africa (%)

Source: Stats SA, February 2011

thThe 4 quarter economic growth rate was driven by the mining sector (17.1%), contributing 0.9%, followed by

the general government services (5.3%) and contributing 0.7% to growth. The mining sector benefited largely

from favourable metal prices globally and the recently encouraging exchange rate. Although the agriculture

sector seems to have grown robustly by 12.5%, its contribution to GDP growth (0.3%) was inconsequential.

The manufacturing sector also contributed (0.6%) strongly to quarterly GDP, growing at 4.1%. Wholesale,

retail, motor trade and accommodation and the agriculture, forestry and fishing sectors, contributed 0.4% thand 0.3% to the 4 quarter GDP growth respectively (Table 4). Finance, real estate and business services, the

wholesale, retail, motor trade and accommodation industry and the transport, storage and communication

industry each contributed 0.4% on growth based on growth rates of 1.7%, 3.5% and 4.2% respectively.

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

8.0

6.0

4.0

2.0

-

(2.0)

(4.0)

(6.0)

(8.0)

2007

:Q1

2007

:Q2

2007

:Q3

2007

:Q4

2008

:Q1

2008

:Q2

2008

:Q3

2008

:Q4

2009

:Q1

2009

:Q2

2009

:Q3

2009

:Q4

2010

:Q1

2010

:Q2

2010

:Q3

2010

:Q4

6.2

5.1

3.1 2.9

4.7

0.9

(1.8)

(2.8)

3.1

0.9

(5.9)

4.84.4

2.72.8

6.5

15

Table 4: Quarter-on-quarter change in GDP (seasonally adjusted) per sector at constant 2005 prices for South

Africa (%)

Agriculture, forestry and fishing -8.1 -18.7 -13.7 -11.0 4.9 13.6 16.3 12.5

Mining and quarrying -22.9 16.9 -3.7 7.7 18.7 -24.5 33.7 17.1

Manufacturing -24.3 -10.7 8.2 10.8 8.3 5.7 -4.9 4.1

Electricity, gas and water -4.5 1.7 3.6 2.7 4.9 -1.7 -2.2 5.6

Construction 15.6 5.5 2.9 1.2 1.3 1.0 0.8 0.2

Wholesale & retail trade, hotels & restaurants -1.6 -4.6 -0.3 -0.1 3.1 6.0 3.3 3.5

Transport, storage and Communication -1.6 -0.4 2.4 3.0 2.4 4.5 3.0 4.2

Finance, real estate and business services -0.1 -3.4 -0.6 1.8 3.2 4.0 1.4 1.7

General government services 3.5 4.1 2.0 5.2 1.2 4.6 0.4 5.3

Personal services -0.1 -1.5 -4.2 -4.4 3.5 3.6 3.1 3.3

Total value added -5.9 -2.3 1.0 3.2 4.6 2.7 2.6 4.5

Taxes less subsidies -5.4 -7.6 0.2 1.9 6.5 4.0 3.9 4.3

GDP at market prices -5.9 -2.8 0.9 3.1 4.8 2.8 2.7 4.4

Source: Stats SA, February 2011

On an annual basis, the economy grew by 2.8% in 2010 compared to -1.7% in 2009. South Africa's 2010 growth

rate remained low compared to other emerging markets especially other BRICSA countries. The manufacturing

sector grew by 5% compared to -10.4% in 2009 (Table 5). It was the largest contributor to GDP (0.7%) followed

by general government services which grew by (3.0%), contributing 0.4% to the annual growth rate. Other

sectors which contributed strongly to the annual growth rate were finance and business services (0.7%) and

grew by 1.9%. The manufacturing sector remains the backbone of the South African economy in terms of

employment and contribution to GDP. Growth of this sector remains critical to achieve higher employment. The

sector is set to benefit tremendously in 2011 owing to the recently launched R20 billion expansion grants by

Government.

In 2010, factors that weighed down the manufacturing sector were strong exchange rate and the generally

lacklustre consumer demand. It is also evident from this analysis that government services played a pivotal role

in the economy in 2010. The government's drive to embark on a sustainable growth path conducive to

employment generation was critical to ensuring this growth. The Government's planned infrastructural projects

in 2011 are expected to bolster growth prospects in 2011.

Table 5: 2010 real growth rates (%) per sector

Agriculture, forestry and fishing 16.1 -3 0.9

Mining and quarrying -5.6 -4.2 5.8

Manufacturing 2.6 -10.4 5.0

Electricity, gas and water -3.1 -1.6 2.0

Construction 9.5 7.4 1.5

Wholesale, retail, motor trade and accommodation 0.8 -2.5 2.2

Transport, storage and communication 3.4 0.6 2.9

Finance, real estate and business services 7.3 0.9 1.9

General government services 4.5 4.1 3.0

Personal services 3.9 -0.3 0.6

Industry 2009 2010

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Industry 2008 2009 2010

3.1.3 2010 Economic Growth Trends

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

“Building an economy that creates opportunities for all and making tourism to work for us all”

16

Total value added 3.7 -1.5 2.8

Taxes less subsidies on products 2.6 -2.9 3.0

GDP at market prices 3.6 -1.7 2.8

Source: Stats SA, February 2011

The relative size of each sector is shown in Figure 8 below. The Finance, real estate and business services

remains the largest sector in South Africa, contributing 21.2% to GDP, followed by the manufacturing sector

(15%).

Figure 8: Sector contribution to SA GDP in 2010

Source: Stats SA, February 2011

thEstimates show that the KZN economy posted a growth rate of 3.9% in the 4 of quarter of 2010. This compares rdbuoyantly to the 1.4% registered in the 3 quarter (Figure 9). The national growth rate of 4.4% was anchored

largely by the mining sector which grew by 17.1% and contributed to 0.9% points to growth. The mining sector

in KZN contributes an infinitesimal 1.1% to provincial GDP as compared to an average of 5.3% for South Africa

as a whole.

th3.2 Regional growth developments: 4 quarter 20103.2.1 Quarter-on-quarter GDP growth rates

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

Personal services

General government services

Finance, real estate and business services

Transport, storage and communication

Wholesale, retail, motor trade and...

Construction

Electricity, gas and water

Manufacturing

Mining and quarrying

Agriculture, forestry and fishing

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

5.7%

13.6%

21.2%

9.1%

12.0%

3.2%

1.9%

15.0%

5.3%

2.3%

17

st thFigure 9: KZN quarter-on-quarter real GDP growth rate (1 Quarter 2008- 4 2010)

Source: Authors formulation based on Quantec database

rdIt is evident in figure 10 that KZN quarter-on-quarter growth of 3.9% in the 3 quarter was below the national thaverage of 4.4%. High growth rates in the 4 quarter were recorded in Northern Cape (6.9%), Limpopo (6.5%),

and North West (6.4%). The robust growth rates in these regions were largely driven by mining and agriculture.

The Eastern Cape and the Western Cape posted the lowest growth rates of 3.2% and 3.6% respectively (Figure

10).

thFigure 10: 4 Quarter 2010 national and regional growth rates (%)

Source: Authors formulation based on Quantec database

The drivers of the 3.9% quarter-on-quarter GDP growth were mining (11.5%), agriculture (10.2%), general

government services (5.4%), manufacturing (4.2%), electricity and water (4.1%) wholesale and retail trade

(3.9%) and Transport and communication (3.9%) see Table 6. It is encouraging to note that manufacturing and

electricity and water sectors recovered tremendously after posting negative growth rates of -5.1% and -1.6% rdrespectively in the 3 quarter. Recovery in the manufacturing sector is imperative given its mainstay status to the

economy of KwaZulu-Natal. Positive growth outlook in the manufacturing sector is expected, buoyed by

3.2.2 KwaZulu-Natal Quarter-on-quarter sectoral growth trends

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

South Africa

Limpopo

Mpumalanga

Gauteng

North West

KwaZulu-Natal

Free State

Northern Cape

Eastern Cape

Western Cape

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

3.6

3.2

6.9

5.2

3.9

6.4

4.2

5.2

6.5

4.4

“Building an economy that creates opportunities for all and making tourism to work for us all”

6.0

4.0

2.0

0.0

-2.0

-4.0

-6.0

-8.0

20

08

:Q1

20

08

:Q2

20

08

:Q3

20

08

:Q4

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

09

:Q4

20

10

:Q1

20

10

:Q2

20

10

:Q3

20

10

:Q4

5.3

3.3

1.3

-2.5

6.0

-3.8

1.8

3.7

4.14.3

1.4

3.9

18

improved consumer confidence nationally and globally. The modest growth rate in the construction sector is

discouraging given its importance to employment. Construction is expected to receive a boost once

government's infrastructural projects are rolled out as pronounced in both the state of the nation and the state

of the province addresses.

Table 6: KZN quarter-on-quarter real growth rate per sector (%)

Agriculture, forestry and fishing -8.3 -18.7 -13.5 -10.5 4.1 11.2 13.4 10.2

Mining and quarrying -17.1 28.2 7.6 22.5 12.5 -15.9 18.6 11.5

Manufacturing -24.5 -11.0 7.7 10.2 8.0 5.0 -5.1 4.2

Electricity and water -3.4 3.5 6.0 5.6 3.5 -1.2 -1.6 4.1

Construction 11.9 1.4 -1.8 -4.2 1.0 0.7 0.6 0.1

Wholesale & retail trade; hotels & restaurants -0.2 -2.9 1.9 2.6 3.5 6.8 3.8 3.9

Transport and communication -1.1 0.3 3.2 3.8 2.3 4.2 2.7 3.9

Finance, real estate and business services 0.5 -2.6 0.4 3.0 2.5 3.7 1.4 1.7

Community, social & other personal services 0.2 -1.1 -3.7 -3.7 3.4 3.5 3.1 3.2

General government services 3.8 4.4 2.3 5.5 1.2 4.7 0.4 5.4

All industries at basic prices -6.1 -3.4 2.0 3.9 3.9 4.4 1.0 3.9

Taxes less subsidies on products -5.1 -7.3 0.7 2.4 6.1 3.2 4.7 4.1

GDPR at market prices -6.0 -3.8 1.8 3.7 4.1 4.3 1.4 3.9

Source: Quantec, February 2011

KwaZulu-Natal posted a growth rate of 2.6% in 2010 following a decline of 1.8% in 2009 (Figure 11). The

uninspiring growth of 2.6% recorded in 2010 is typical of an economy that is pulling out of a recession. Economic

recovery in KwaZulu-Natal was anchored primarily by increased consumer spending, the 2010 world cup

spending and by improved growth in entirely all the sectors of the economy.

Figure 11: KwaZulu-Natal annual GDP Growth (%)- (2001-2010)

Source: Author's formulation based on estimates by Quantec

Industry/Sector 2009 2010

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

3.2.3 KwaZulu-Natal Annual Growth Trends

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

-1.0

-2.0

-3.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

4.4

2.42.7

4.5

5.8

5.5

5.9

4.0

-1.8

2.6

“Building an economy that creates opportunities for all and making tourism to work for us all”

19

3.2.4 KwaZulu-Natal Sectoral Annual Growth TrendsOn a sectoral basis, the major drivers of growth in 2010 were manufacturing (5.1%), general government

services (3.0%), transport and communication (2.6%) and wholesale, and retail trade, hotels and

accommodation (2.4%) - (Table 7). KZN mining sector contracted by 4.3% in 2010 and was the only sector that

posted a negative growth rate. Increased spending by the provincial government on infrastructure

development is expected to play a dominant role in anchoring higher growth rates in the medium term period.

Table 7: KwaZulu-Natal sectoral growth trends per annum

Agriculture, forestry and fishing 5.2 0.3 -5.8 0.5 4.1 14.6 -3.2 0.6

Mining and quarrying 5.9 2.0 -6.3 -3.3 2.5 -6.5 2.9 -4.3

Manufacturing -0.9 4.7 6.2 6.0 5.3 2.6 -10.6 5.1

Electricity and water -11.5 7.3 6.5 3.3 3.3 -4.0 -0.5 1.6

Construction 4.7 9.4 13.6 7.6 14.4 9.6 4.0 1.1

Wholesale and retail trade; hotels and

restaurants 3.5 5.4 6.5 6.4 5.6 0.9 -1.0 2.4

Community, social and other personal

services 5.6 1.8 3.4 5.3 5.5 3.8 0.0 0.6

General government services 2.2 1.3 4.5 3.0 4.3 4.9 4.4 3.0

All industries at basic prices 2.9 4.5 5.9 5.4 6.0 4.1 -1.7 2.6

Taxes less subsidies on products 1.6 4.8 4.5 6.4 4.9 2.7 -2.6 2.9

GDPR at market prices 2.7 4.5 5.8 5.5 5.9 4.0 -1.8 2.6

Source: Quantec, February 2011

In 2010, KZN again recorded a below average growth rate of 2.6% compared to South Africa's 2.8% (Figure 12). thThis growth rate positioned KwaZulu-Natal as the slowest growing economy during the 4 quarter after the

Eastern Cape (2.3%), Northern Cape (2.3%) and Western Cape (2.5%). Provinces that posted higher growth

rates were Limpopo (3.9%), Mpumalanga (3.3%), Gauteng (3.0%) and North West (3.0%).

Figure 12 : 2010 National and Regional Average Growth Rates (%)

Source: Quantec,

Industry/Sector 2003 2004 2005 2006 2007 2008 2009 2010

Transport and communication 7.0 4.5 5.9 5.2 7.1 3.8 1.2 2.6

Finance, real estate and business services 5.6 7.2 10.6 7.7 7.8 7.3 1.5 1.8

February 2011

3.2.5 Regional Annual 2010 Growth Rates

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

South Africa

Limpopo

Mpumalanga

Gauteng

North West

KwaZulu-Natal

Free State

Northern Cape

Eastern Cape

Western Cape

2.8

3.9

3.3

3.0

3.0

2.6

2.7

2.3

2.3

2.5

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

“Building an economy that creates opportunities for all and making tourism to work for us all”

20

3.3 KwaZulu-Natal Growth Trends in Major Cities3.3.1 Durban

8

3.3.2 Pietermaritzburg

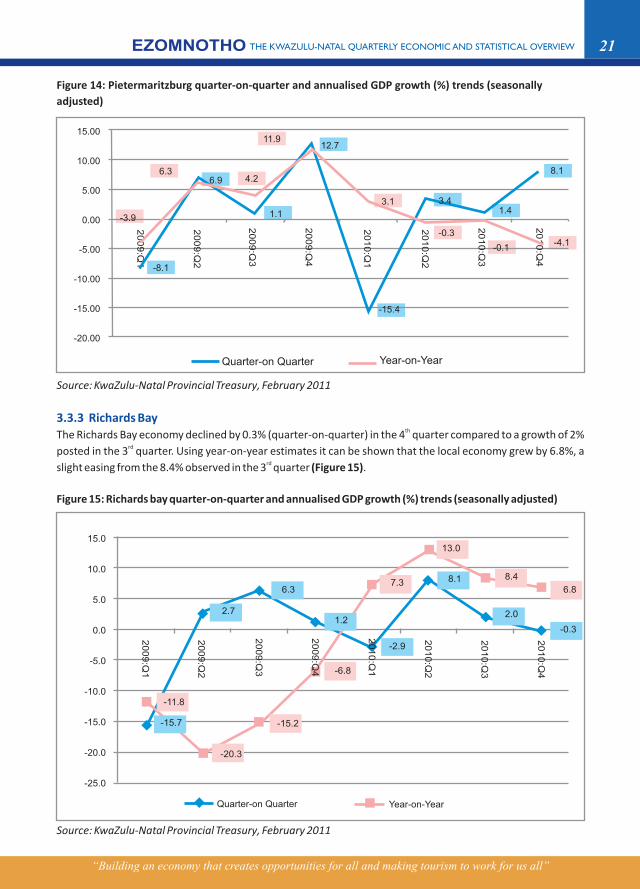

stFigure 13 shows the city of Durban quarter-on-quarter and year-on-year quarterly growth trends between 1 th thquarter of 2009 and 4 quarter of 2009. In the 4 quarter of 2010, the economy of Durban grew by 1.1%

(quarter-on quarter). This compares unfavourably to 3.9% and 4.4% recorded for KwaZulu-Natal and South

Africa respectively .

Source: KwaZulu-Natal Provincial Treasury,

The quarter-on-quarter and year-on-year growth rates for Pietermaritzburg are presented in Figure 14. On a rdyear-on-year basis, Pietermaritzburg exhibited consecutive negative growth rates between the 3 quarter and

th4 quarter. This gloomy picture can be explained by the poor performance of Msunduzi municipal finance since

2009. However, a completely converse picture is depicted when one considers the quarter-on-quarter growth

trends. A highly buoyant growth rate of 8.1% was recorded.

Figure 13: Durban quarter-on-quarter and annualised GDP growth (%) trends (seasonally adjusted)

February 2011

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

8.0

6.0

4.0

2.0

0.0

-2.0

-4.0

-6.0

-8.0

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

09

:Q4

20

10

:Q1

20

10

:Q2

20

10

:Q3

20

10

:Q4

Quarter-on Quarter Year-on-Year

-6.3

-5.1

-6.6

3.1

1.80.6

-1.6

4.90.6

1.1

-5.2

-1.1

3.9

5.74.5

5.0

8. GDP Estimates by KwaZulu-Natal Provincial Treasury are more prudent figures which enable us to track economic developments in KwaZulu-Natal regional economy. These figures also enable us to compare growth trends in major cities in KZN.

21

Figure 14: Pietermaritzburg quarter-on-quarter and annualised GDP growth (%) trends (seasonally

adjusted)

Source: KwaZulu-Natal Provincial Treasury, February 2011

February 2011

3.3.3 Richards BaythThe Richards Bay economy declined by 0.3% (quarter-on-quarter) in the 4 quarter compared to a growth of 2%

rdposted in the 3 quarter. Using year-on-year estimates it can be shown that the local economy grew by 6.8%, a rdslight easing from the 8.4% observed in the 3 quarter (Figure 15).

Figure 15: Richards bay quarter-on-quarter and annualised GDP growth (%) trends (seasonally adjusted)

Source: KwaZulu-Natal Provincial Treasury,

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

10

:Q2

20

10

:Q3

20

10

:Q4

15.0

10.0

5.0

0.0

-5.0

-10.0

-15.0

-20.0

-25.0

Quarter-on Quarter Year-on-Year

20

09

:Q4

20

10

:Q1

-15.7

2.7

6.3

1.2

-2.9

8.1

2.0

-0.3

-11.8

-20.3

-15.2

-6.8

7.3

13.0

8.4

6.8

Quarter-on Quarter Year-on-Year

15.00

10.00

5.00

0.00

-5.00

-10.00

-15.00

-20.00

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

09

:Q4

20

10

:Q1

20

10

:Q2

20

10

:Q3

20

10

:Q4

-3.9

6.36.9 4.2

11.912.7

3.1 3.41.4

-15.4

1.1

8.1

-4.1-0.1

-0.3

-8.1

“Building an economy that creates opportunities for all and making tourism to work for us all”

22

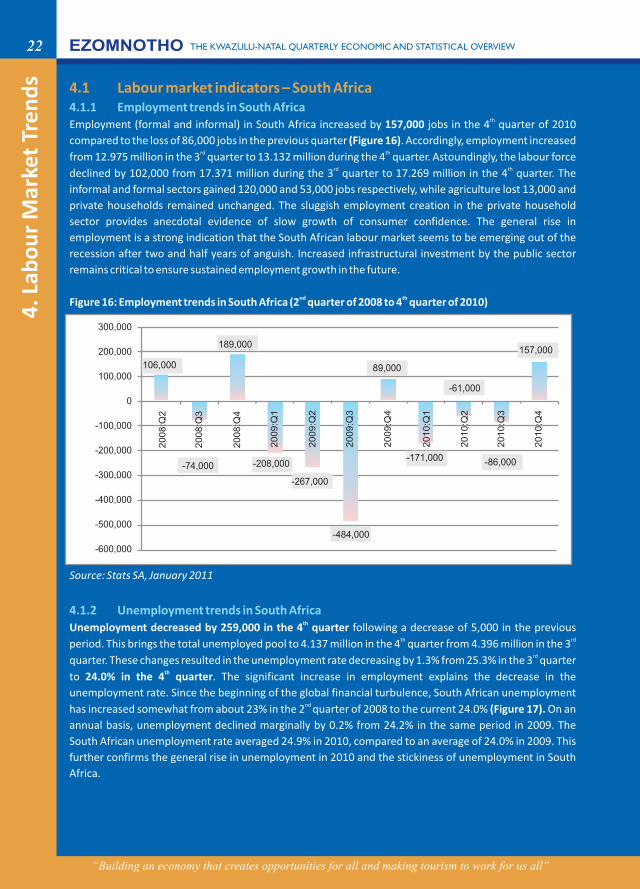

4.1 Labour market indicators – South Africa4.1.1 Employment trends in South Africa

4.1.2 Unemployment trends in South Africa

thEmployment (formal and informal) in South Africa increased by 157,000 jobs in the 4 quarter of 2010

compared to the loss of 86,000 jobs in the previous quarter (Figure 16). Accordingly, employment increased rd thfrom 12.975 million in the 3 quarter to 13.132 million during the 4 quarter. Astoundingly, the labour force

rd thdeclined by 102,000 from 17.371 million during the 3 quarter to 17.269 million in the 4 quarter. The

informal and formal sectors gained 120,000 and 53,000 jobs respectively, while agriculture lost 13,000 and

private households remained unchanged. The sluggish employment creation in the private household

sector provides anecdotal evidence of slow growth of consumer confidence. The general rise in

employment is a strong indication that the South African labour market seems to be emerging out of the

recession after two and half years of anguish. Increased infrastructural investment by the public sector

remains critical to ensure sustained employment growth in the future.

nd thFigure 16: Employment trends in South Africa (2 quarter of 2008 to 4 quarter of 2010)

Source: Stats SA, January 2011

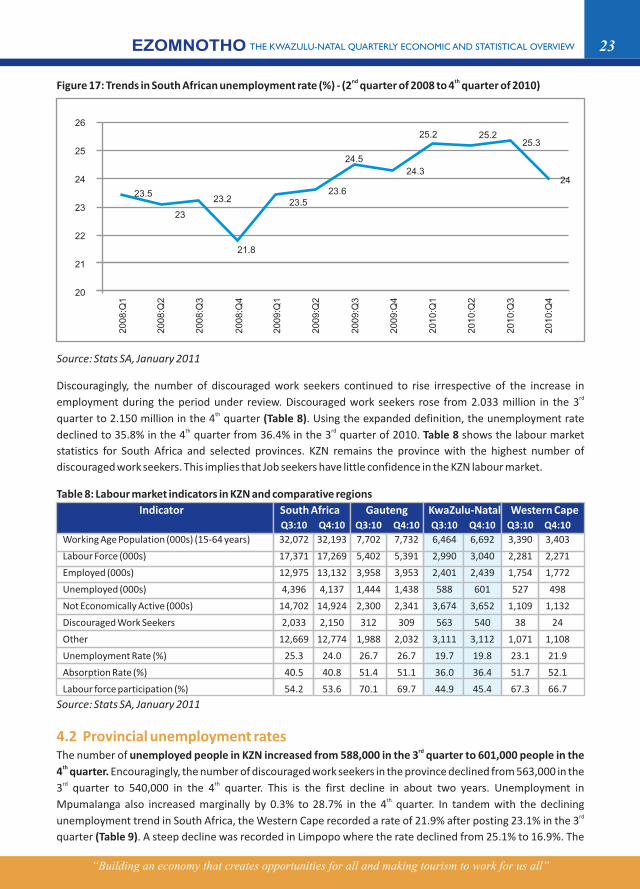

thUnemployment decreased by 259,000 in the 4 quarter following a decrease of 5,000 in the previous th rdperiod. This brings the total unemployed pool to 4.137 million in the 4 quarter from 4.396 million in the 3

rdquarter. These changes resulted in the unemployment rate decreasing by 1.3% from 25.3% in the 3 quarter thto 24.0% in the 4 quarter. The significant increase in employment explains the decrease in the

unemployment rate. Since the beginning of the global financial turbulence, South African unemployment nd has increased somewhat from about 23% in the 2 quarter of 2008 to the current 24.0% (Figure 17). On an

annual basis, unemployment declined marginally by 0.2% from 24.2% in the same period in 2009. The

South African unemployment rate averaged 24.9% in 2010, compared to an average of 24.0% in 2009. This

further confirms the general rise in unemployment in 2010 and the stickiness of unemployment in South

Africa.

4. L

abo

ur

Mar

ket

Tre

nd

sEZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

300,000

200,000

100,000

0

-100,000

-200,000

-300,000

-400,000

-500,000

-600,000

20

08

:Q2

20

08

:Q4

20

09

:Q4

20

10

:Q4

20

08

:Q3

106,000

189,000

-74,000 -208,000

-484,000

89,000

-171,000

-61,000

-86,000

157,000

-267,000

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

10

:Q1

20

10

:Q2

20

10

:Q3

“Building an economy that creates opportunities for all and making tourism to work for us all”

23

nd thFigure 17: Trends in South African unemployment rate (%) - (2 quarter of 2008 to 4 quarter of 2010)

Source: Stats SA, January 2011

Discouragingly, the number of discouraged work seekers continued to rise irrespective of the increase in rdemployment during the period under review. Discouraged work seekers rose from 2.033 million in the 3

thquarter to 2.150 million in the 4 quarter (Table 8). Using the expanded definition, the unemployment rate th rddeclined to 35.8% in the 4 quarter from 36.4% in the 3 quarter of 2010. Table 8 shows the labour market

statistics for South Africa and selected provinces. KZN remains the province with the highest number of

discouraged work seekers. This implies that Job seekers have little confidence in the KZN labour market.

Table 8: Labour market indicators in KZN and comparative regions

Working Age Population (000s) (15-64 years) 32,072 32,193 7,702 7,732 6,464 6,692 3,390 3,403

Labour Force (000s) 17,371 17,269 5,402 5,391 2,990 3,040 2,281 2,271

Employed (000s) 12,975 13,132 3,958 3,953 2,401 2,439 1,754 1,772

Unemployed (000s) 4,396 4,137 1,444 1,438 588 601 527 498

Not Economically Active (000s) 14,702 14,924 2,300 2,341 3,674 3,652 1,109 1,132

Discouraged Work Seekers 2,033 2,150 312 309 563 540 38 24

Other 12,669 12,774 1,988 2,032 3,111 3,112 1,071 1,108

Unemployment Rate (%) 25.3 24.0 26.7 26.7 19.7 19.8 23.1 21.9

Absorption Rate (%) 40.5 40.8 51.4 51.1 36.0 36.4 51.7 52.1

Labour force participation (%) 54.2 53.6 70.1 69.7 44.9 45.4 67.3 66.7

Source: Stats SA, January 2011

rdThe number of unemployed people in KZN increased from 588,000 in the 3 quarter to 601,000 people in the th4 quarter. Encouragingly, the number of discouraged work seekers in the province declined from 563,000 in the rd th3 quarter to 540,000 in the 4 quarter. This is the first decline in about two years. Unemployment in

thMpumalanga also increased marginally by 0.3% to 28.7% in the 4 quarter. In tandem with the declining rdunemployment trend in South Africa, the Western Cape recorded a rate of 21.9% after posting 23.1% in the 3

quarter (Table 9). A steep decline was recorded in Limpopo where the rate declined from 25.1% to 16.9%. The

Indicator South Africa Gauteng KwaZulu-Natal Western CapeQ3:10 Q4:10 Q3:10 Q4:10 Q3:10 Q4:10 Q3:10 Q4:10

4.2 Provincial unemployment rates

EZOMNOTHO THE KWAZULU-NATAL QUARTERLY ECONOMIC AND STATISTICAL OVERVIEW

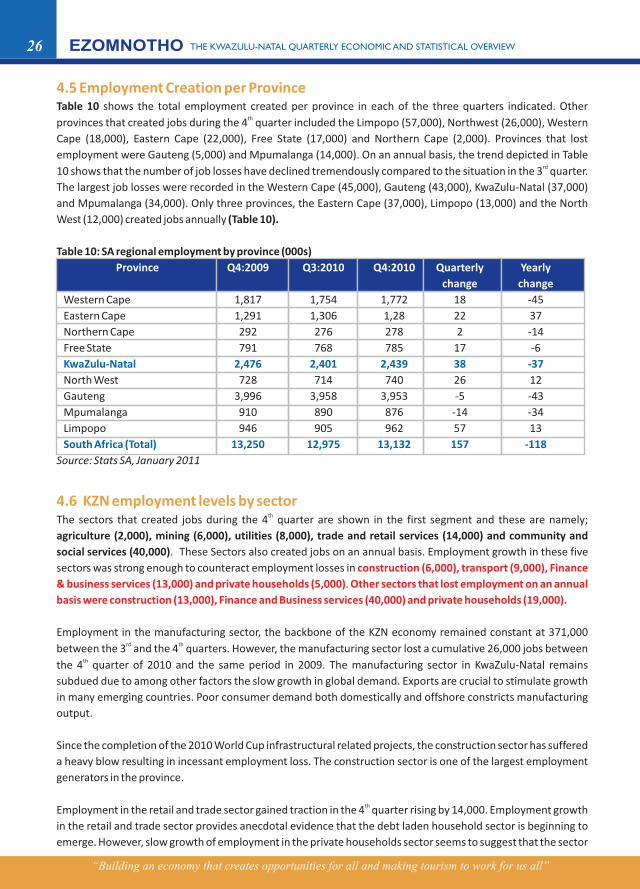

26

25

24

23

22

21

20

20

08

:Q1

20

08

:Q2

20

08

:Q3

20

08

:Q4

20

09

:Q1

20

09

:Q2

20

09

:Q3

20

10

:Q1

20

10

:Q2

20

10

:Q3

20

10

:Q4

23.5

23

23.2

21.8

23.523.6

24.5

24.3

25.2 25.225.3

24

20

09

:Q4

“Building an economy that creates opportunities for all and making tourism to work for us all”

24

decline positioned Limpopo as the regional economy with the lowest unemployment rate in South Africa.

However, this decline is not sustainable as it can be attributed to a significant increase in the number of

discouraged work seekers from 321,000 to 393,000. This is evidence of declining employment opportunities in

Limpopo.

Unemployment remains high and above 30% mark in Northern Cape (34.4%) and Free State (35.5%). In

Gauteng, the unemployment rate remained constant at 26.7%. Using the expanded definition, KZN rd thunemployment rate declined from 38.7% in the 3 quarter to 38.3% in the 4 quarter. The Western Cape

remains the province with the lowest expanded unemployment rate of 24%. Limpopo (42.6%), North West

(41.6%) and Eastern Cape (40%) are the provinces with the highest expanded unemployment rate.

Table 9: Unemployment rates per province (%)

Western Cape 21.4 21.8 21.9 -1.2 0.5

Eastern Cape 27.0 27.2 24.7 -2.5 -2.3

Northern Cape 24.5 25.8 24.3 -1.5 -0.2

Free State 25.1 29.5 27.1 -2.4 0.2

North West 26.9 28.0 24.2 -3.8 -2.7

Gauteng 25.4 26.7 26.7 0.0 1.3

Mpumalanga 26.3 28.4 28.7 0.3 2.4

Limpopo 26.9 25.1 16.9 -8.2 -10.0

South Africa 24.1 25.3 24.0 -1.3 -0.2

Source: Stats SA, January 2011