5555 5555 card a. risk 12/12 1234 5678 9012 3456 lance l. lancer12/12 credit: history, types,...

TRANSCRIPT

5555 5555 5555 5555Card A. Risk 12/12

1234 5678 9012 3456

Lance L. Lancer12/12

Credit: History, Types,

Dangers Chapter 10

5555 5555 5555 5555Card A. Risk 12/12

Credit: What is it?

What is credit?

What are the current uses of credit?

Who can obtain credit?

What are the dangers?

5555 5555 5555 5555Card A. Risk 12/12

Credit Discussion: Activity

With a partner, discuss the following questions.

How do people use credit?

What are the positives and negatives of credit?

5555 5555 5555 5555Card A. Risk 12/12

Credit Vs. Debit

Credit Vs. Debit

5555 5555 5555 5555Card A. Risk 12/12

Credit

“Buy now, Pay later”

Purchase Items at present time- pay for it in the future

Purchase items that couldn’t be purchased otherwise

5555 5555 5555 5555Card A. Risk 12/12

Types of CreditOpen (Revolving)

Closed (Installment)

Service

5555 5555 5555 5555Card A. Risk 12/12

Open Credit

Revolving

Amount is charged to account as often as desired (to a certain dollar amount).

Payments are made each month

Ongoing balance can be maintained

Minimum monthly payment required

Ex: Credit Cards

5555 5555 5555 5555Card A. Risk 12/12

Closed Credit

Installment

Amount is set for purchase

Payments are made and balance is paid off in a certain amount of time

Ex: Store accounts (furniture/appliances) Car loans, mortgages

5555 5555 5555 5555Card A. Risk 12/12

Service

Receive service, pay for them later

Utilities

Ex: Electricity, water, sewer, etc.

Odd Ex: Doctor or dentist

Receiving service and paying later

5555 5555 5555 5555Card A. Risk 12/12

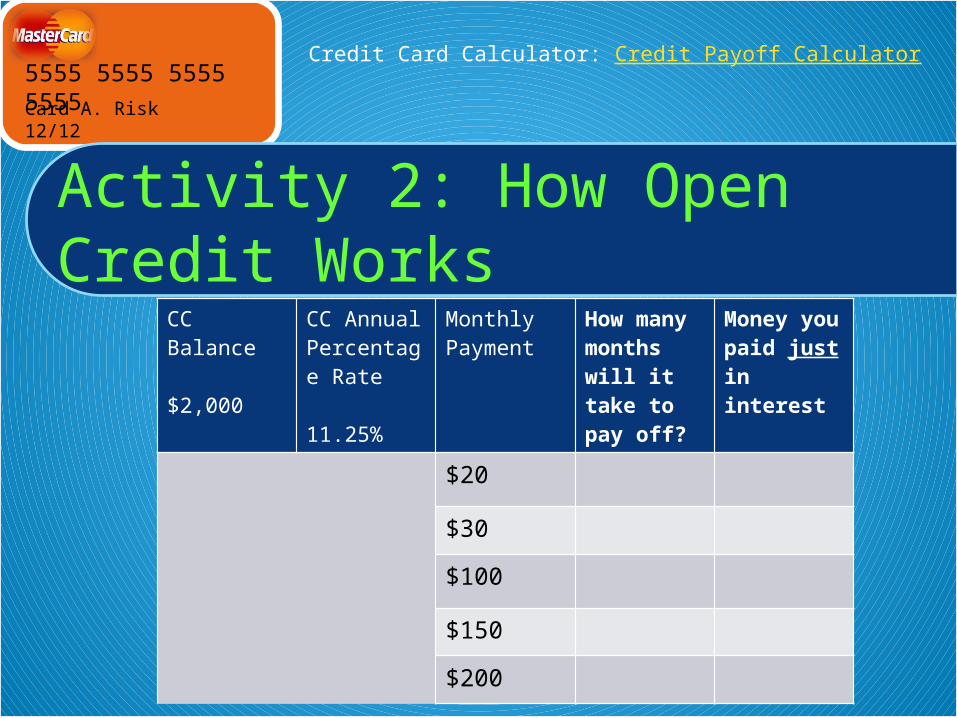

Activity 2: How Open Credit Works

CC Balance

$2,000

CC Annual Percentage Rate

11.25%

Monthly Payment

How many months will it take to pay off?

Money you paid just in interest

$20

$30

$100

$150

$200

Credit Card Calculator: Credit Payoff Calculator

5555 5555 5555 5555Card A. Risk 12/12

Types of Credit: Activity

Enrique is thinking about buying an Ipad. He will need to borrow money to make the purchase. He can arrange the financing ahead of time, or he can use the installment sales plan at the store.

5555 5555 5555 5555Card A. Risk 12/12

Activity Continued

Enrique is thinking about buying an Ipad. He will need to borrow money to make the purchase. He can arrange the financing ahead of time, or he can use the installment sales plan at the store.

1.What are the advantages/disadvantages of borrowing money ahead of time?

2.What are the advantages/disadvantages to the installment plan?

3.What type of credit is the installment plan an example of?

5555 5555 5555 5555Card A. Risk 12/12

3 C’s of Credit

Credit Worthiness

Measure of your reliability to repay a loan.

A lender judge creditworthiness based on 3 factors:

Character

Capacity

Capital

5555 5555 5555 5555Card A. Risk 12/12

Character

Will you repay debt?

Credit history- Do you have a history of paying back debt?

Capacity

Can you repay debt?

Do you have the Income to pay?

3 C’s Of Credit

5555 5555 5555 5555Card A. Risk 12/12

Capital

Is the creditor (lender) fully protected if you fail to repay?

Assets (own)- Liabilities (owe)= payment of debt

5555 5555 5555 5555Card A. Risk 12/12

Credit History

A record of your past borrowing and repayments.

If you paid your bills on time in the past, lenders will be more likely to lend you money in the future.

5555 5555 5555 5555Card A. Risk 12/12

What assets back up your promises to pay?

Car

House

Jewelry

You can sell collateral to pay off debt

Collateral

5555 5555 5555 5555Card A. Risk 12/12

CosignA parent or older person will sign the loan with you . By them signing the loan, they are agreeing to pay if you are unable to.

** Usually this is a way younger people can get loans.

The lender will feel safe in lending you the money.

5555 5555 5555 5555Card A. Risk 12/12

Credit Application - Activity

Examine the sample credit application

Please put false information in the application, do not write in your SSN!

What information do they want from you?

Why do you think they need this?

5555 5555 5555 5555Card A. Risk 12/12

Requirements

What is needed in order to open a credit card?

Credit Card Requirements

5555 5555 5555 5555Card A. Risk 12/12

Credit Card Debt

Credit Debt- A Students Story

5555 5555 5555 5555Card A. Risk 12/12

Credit Rating

A measure of your creditworthiness.

A judgment about whether or not you have the ability and willingness to pay your bills on time.

Lenders will decide to give you a loan usually based on your FICO Score

5555 5555 5555 5555Card A. Risk 12/12

FICO Score

Computerized scoring system.

Score will be between 300 and 850, with 850 being the highest.

The score is based on the following:

Payment history, current debt, length of credit history, new accounts and inquiries, and types of credit used.

5555 5555 5555 5555Card A. Risk 12/12

How do you establish credit?

Open a checking and savings account

Get a small loan in your name (auto loan)

Open up a credit card with a small balance ($500). Use it for gas and pay it off on time every month!

Maintain a low balance on credit cards and pay it off every month!

DO NOT BOUNCE CHECKS!

5555 5555 5555 5555Card A. Risk 12/12

3 Credit Bureau's

Experian

Equifax

Trans Union

5555 5555 5555 5555Card A. Risk 12/12

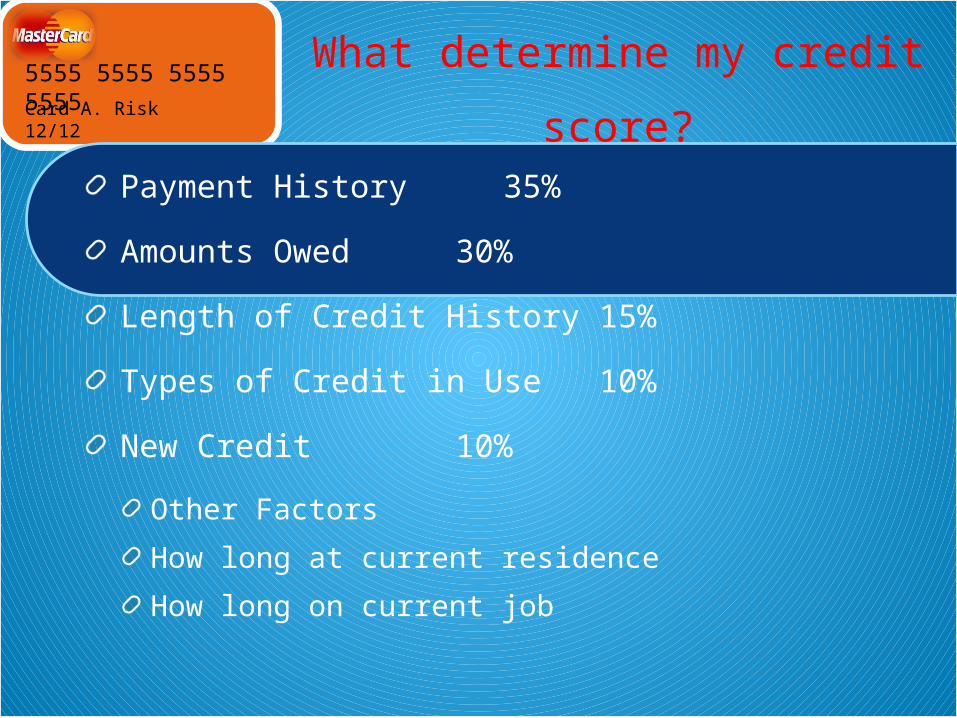

What determine my credit

score?Payment History 35%

Amounts Owed 30%

Length of Credit History15%

Types of Credit in Use 10%

New Credit 10%

Other Factors

How long at current residence

How long on current job

5555 5555 5555 5555Card A. Risk 12/12

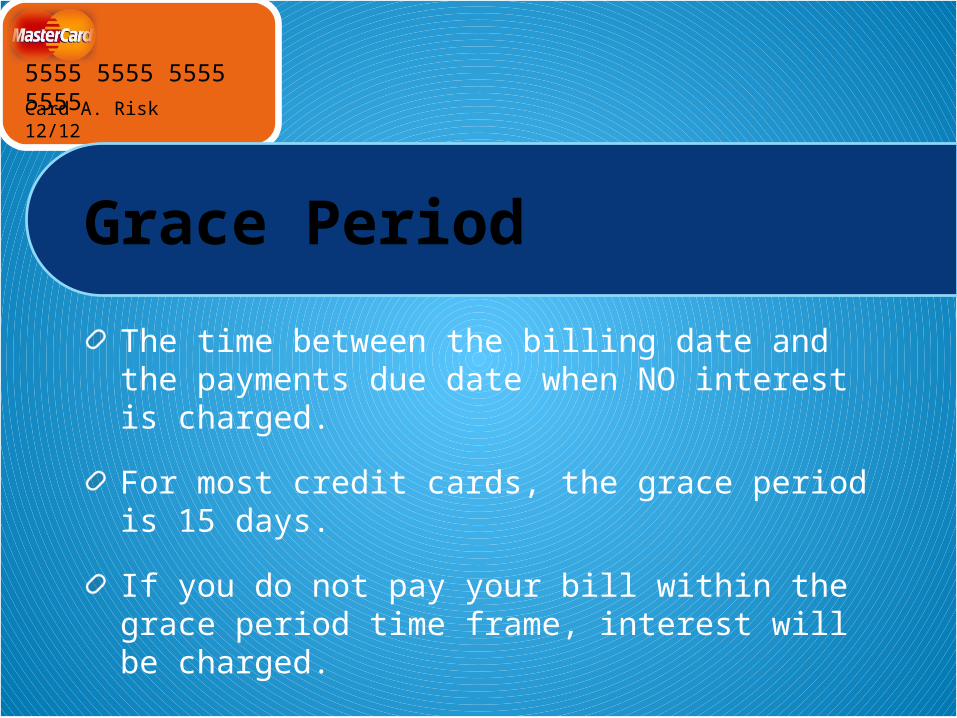

Grace Period

The time between the billing date and the payments due date when NO interest is charged.

For most credit cards, the grace period is 15 days.

If you do not pay your bill within the grace period time frame, interest will be charged.

5555 5555 5555 5555Card A. Risk 12/12

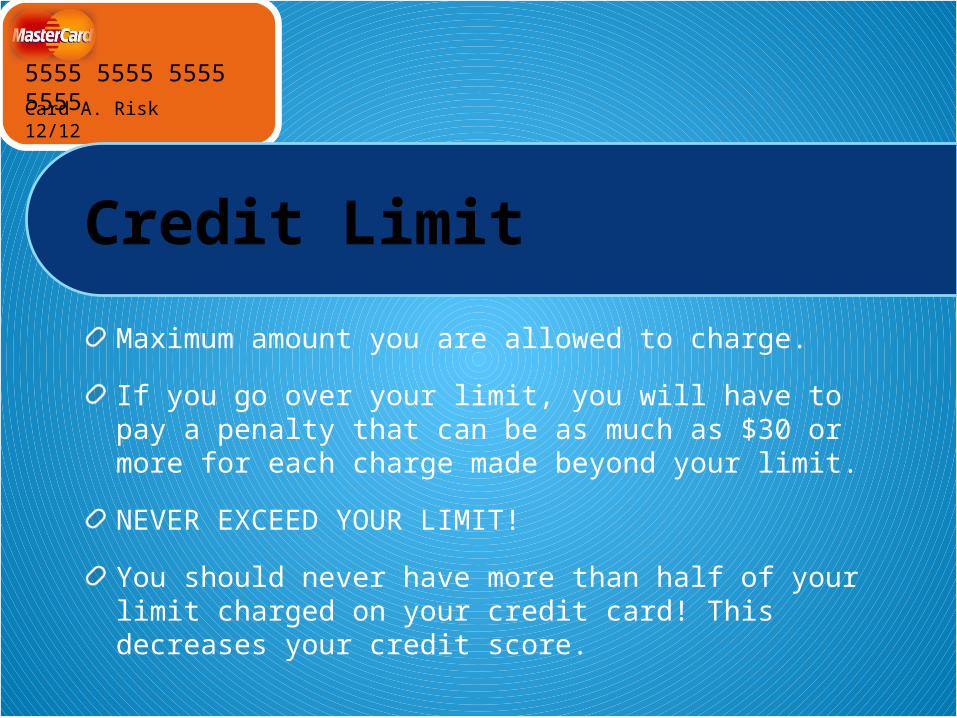

Credit Limit

Maximum amount you are allowed to charge.

If you go over your limit, you will have to pay a penalty that can be as much as $30 or more for each charge made beyond your limit.

NEVER EXCEED YOUR LIMIT!

You should never have more than half of your limit charged on your credit card! This decreases your credit score.

5555 5555 5555 5555Card A. Risk 12/12

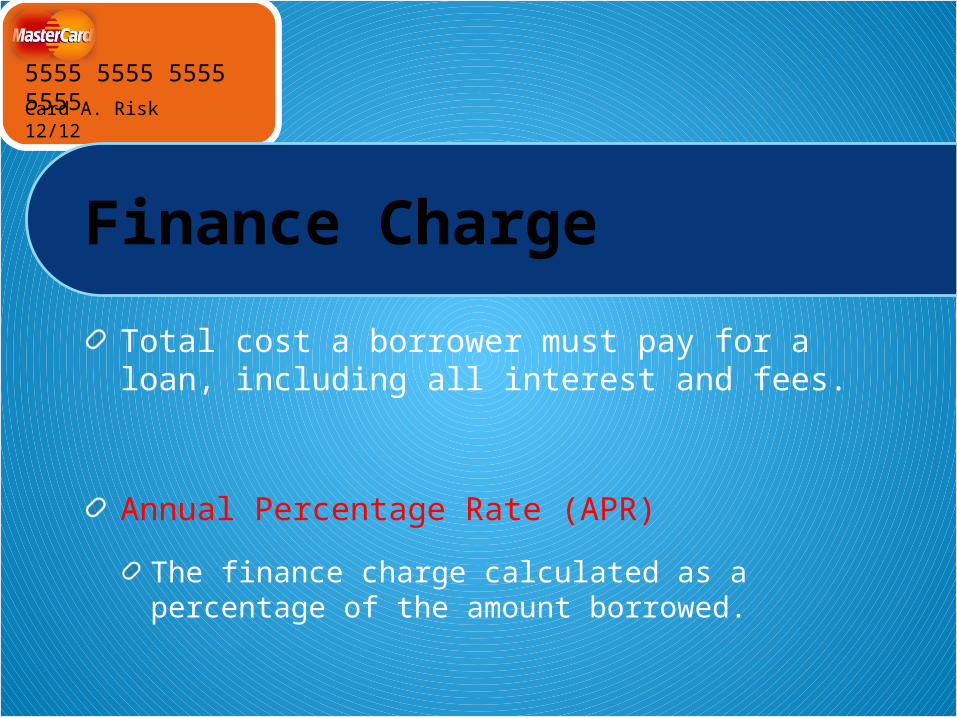

Finance Charge

Total cost a borrower must pay for a loan, including all interest and fees.

Annual Percentage Rate (APR)

The finance charge calculated as a percentage of the amount borrowed.

5555 5555 5555 5555Card A. Risk 12/12

What can hurt your credit score?

Bouncing checks

Not making payment on time

Having too many credit cards

Having a high balance (over 50% of your credit limit).

5555 5555 5555 5555Card A. Risk 12/12

Dangers

Overspending

Identity Theft

High Interest Rates

Ruining Credit Record

Tying up Future Income

5555 5555 5555 5555Card A. Risk 12/12

Identity Theft

Involves using someone else’s identity to get cash or buy products using credit cards, or to access financial accounts that belong to the victim.

60 Minutes Identity Theft

ATM Scam

Children's Identity Stolen

5555 5555 5555 5555Card A. Risk 12/12

How do they become you?

All criminals need your social security number, your driver’s license, or even your credit card number to open charge accounts in your name.

They don’t even have to give a real address, a P.O. Box will work!

5555 5555 5555 5555Card A. Risk 12/12

How to Protect Yourself?

Guard personal documents

NEVER give out your SSN to ANYONE unless absolutely necessary

Keep personal documents in a safe place

Keep track of your bills and what you are spending

5555 5555 5555 5555Card A. Risk 12/12

What to do if your identity is stolen

Report the theft to the three major credit bureaus. They will put a fraud alert on your account.

Report theft to law enforcement

Contact your bank or other organizations you have credit accounts with

Call the FTC