601 mitigating-fcpa-risk-in-ma-revised

TRANSCRIPT

Presented By:

Mitigating FCPA Risk in M&A

Presented By:

Presenters • Mary Britton, Vice President and Chief Counsel, Litigation, Danaher Corporation

• Elizabeth Donley, Partner, Hogan Lovells US LLP• Martha Ha, Vice President Corporate Secretary, General Counsel – Corporate and International, DaVita HealthCare Partners, Inc.

• Janet Wright, Vice President – Corporate, Securities and Finance Counsel, Dell Inc.

Presented By:

Agenda • FCPA Overview • Due Diligence • Transaction Documentation • Structuring Transactions • Post‐Closing Integration • Q&A

Presented By:

Mitigating FCPA Risk in M&A ‐ Overview

Presented By:

FCPA Overview • What is the Foreign Corrupt Practices Act (FCPA)?

• Who is subject to the FCPA?• Anti‐Bribery Provisions• Exceptions and Defenses • Accounting Provisions• Enforcement and Penalties

Presented By:

What is the FCPA?• The Foreign Corrupt Practices Act (FCPA) is a United States law enacted in 1977

• Two primary components:– Anti‐Bribery Provisions: Prohibit bribery of foreign officials

– Accounting Provisions: Require companies to keep accurate books and records and maintain adequate internal controls

Presented By:

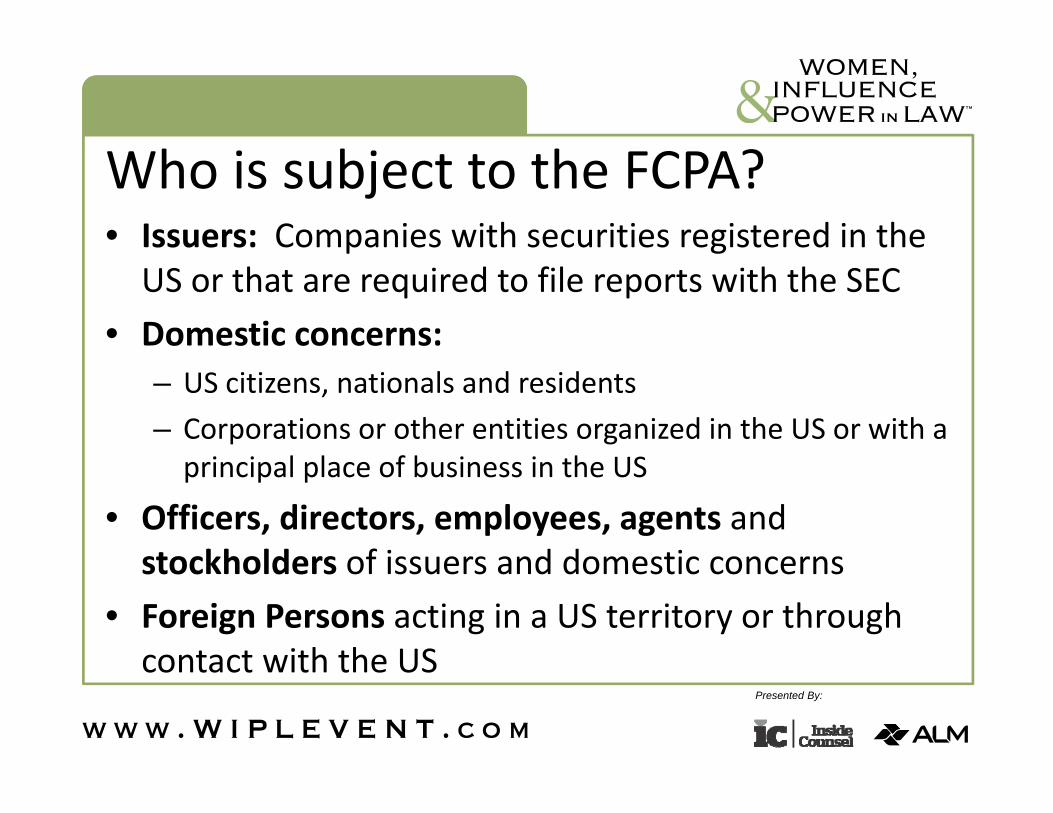

Who is subject to the FCPA?• Issuers: Companies with securities registered in the US or that are required to file reports with the SEC

• Domestic concerns:– US citizens, nationals and residents– Corporations or other entities organized in the US or with a principal place of business in the US

• Officers, directors, employees, agents and stockholders of issuers and domestic concerns

• Foreign Persons acting in a US territory or through contact with the US

Presented By:

Anti‐Bribery Provisions • The FCPA prohibits any:

– Offer, payment, gift, promise – Of money or anything of value – To a foreign official – With corrupt intent to influence acts or decisions – To obtain, retain or direct business or gain a business advantage

• Also prohibits indirect bribes paid to third parties while “knowing” that the payment will be used directly or indirectly to bribe foreign officials

Presented By:

Exceptions and Defenses • Routine Governmental Action Exception

– Facilitating or expediting payments

• Local Law Defense – Lawful under the written laws of the foreign jurisdiction

• Reasonable and Bona Fide Expenditures• Extortion or Duress

– Distinguished from economic coercion

Presented By:

Accounting Provisions • Books and Records

– keep books, records, and accounts– reasonable detail– accurately reflect transactions and dispositions of assets

• Internal Controls – Management authorization – Proper recording – System for revealing and addressing discrepancies

Presented By:

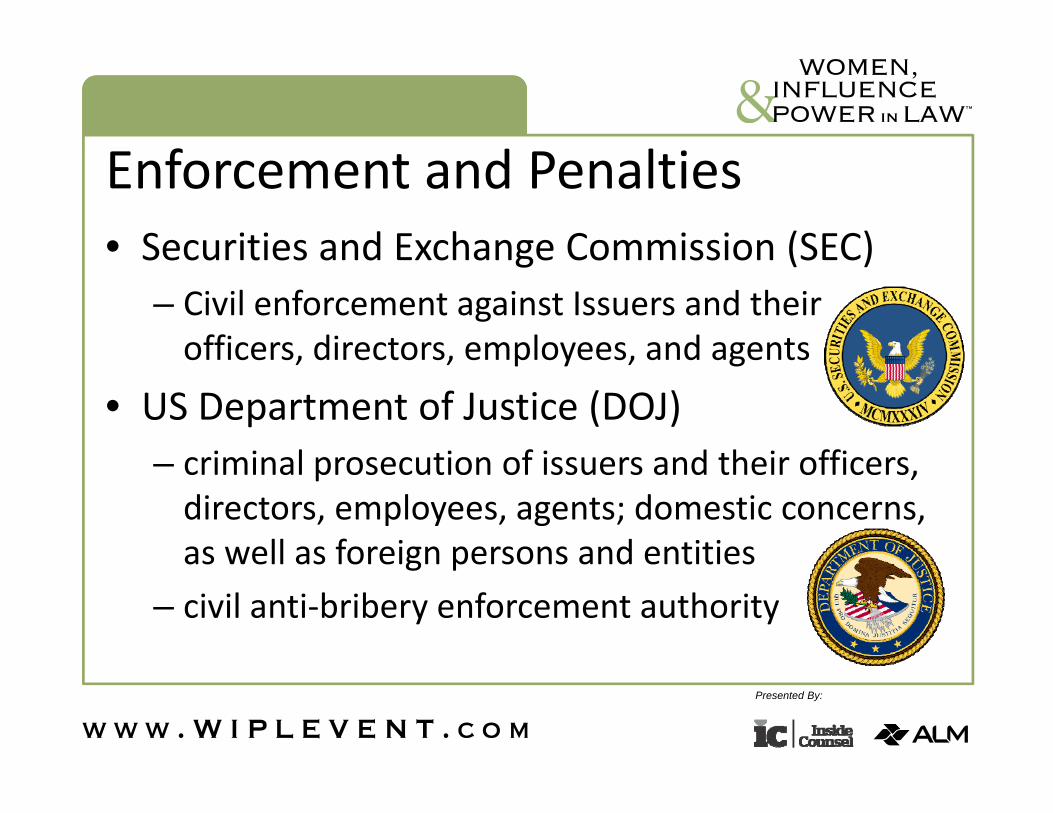

Enforcement and Penalties • Securities and Exchange Commission (SEC)

– Civil enforcement against Issuers and their officers, directors, employees, and agents

• US Department of Justice (DOJ)– criminal prosecution of issuers and their officers, directors, employees, agents; domestic concerns, as well as foreign persons and entities

– civil anti‐bribery enforcement authority

Presented By:

Enforcement and Penalties (cont.) • Violations of the FCPA may also constitute violations of other US and foreign laws, including securities and criminal laws, e.g.: – Money laundering – Mail and wire fraud – SEC reporting violations – Tax violations

Presented By:

Enforcement and Penalties (cont) • Imprisonment • Criminal fines and civil penalties • Disgorgement and restitution • Suspension and disbarment • Oversight and monitoring

Presented By:

Mitigating FCPA Risk in M&A – Due Diligence

Presented By:

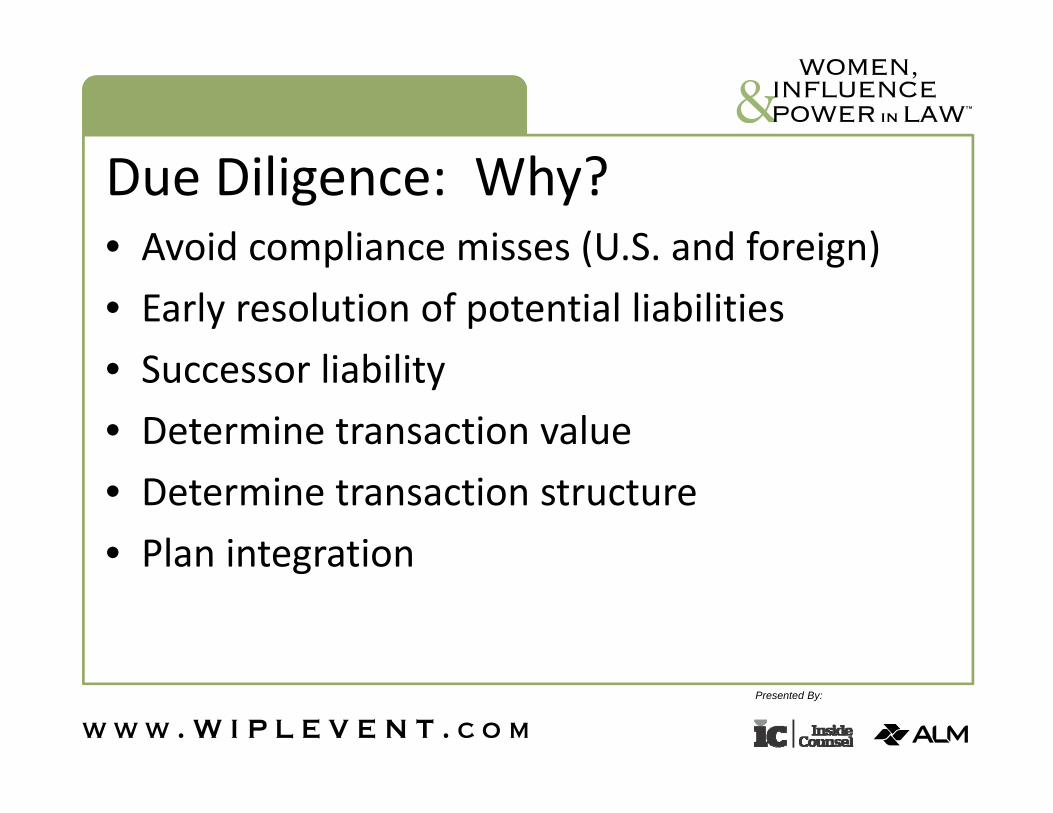

Due Diligence: Why? • Avoid compliance misses (U.S. and foreign)• Early resolution of potential liabilities• Successor liability• Determine transaction value• Determine transaction structure• Plan integration

Presented By:

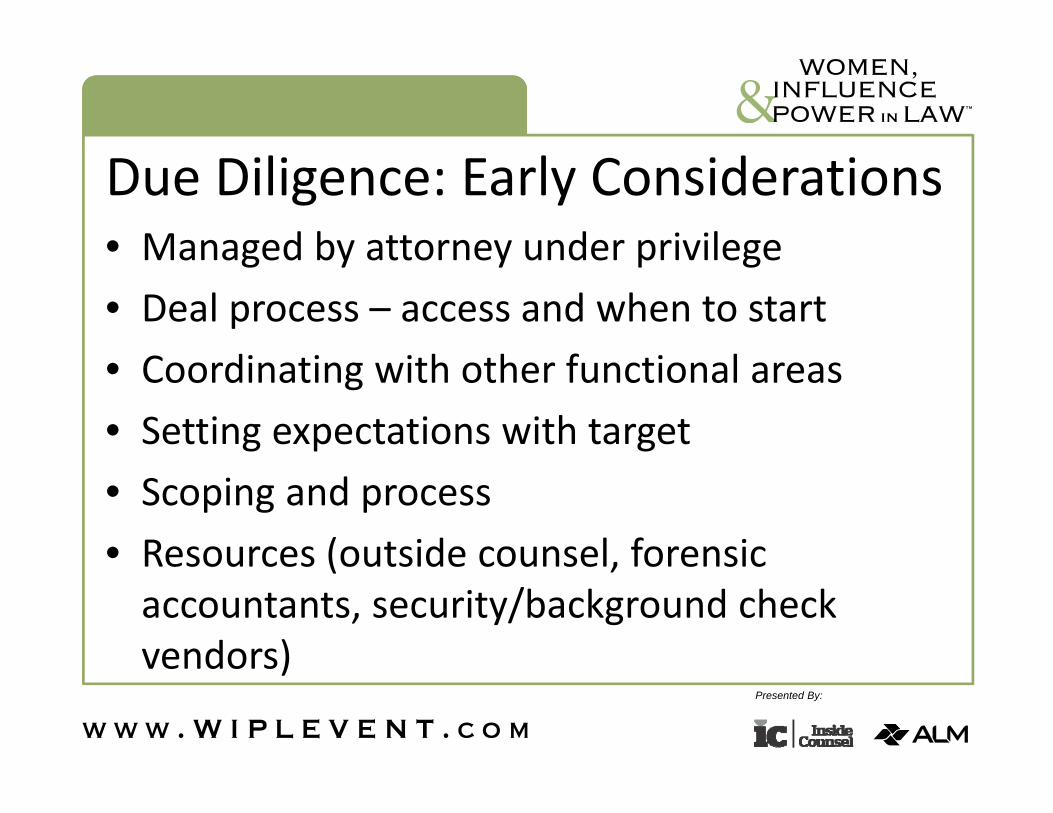

Due Diligence: Early Considerations • Managed by attorney under privilege• Deal process – access and when to start• Coordinating with other functional areas• Setting expectations with target• Scoping and process• Resources (outside counsel, forensic accountants, security/background check vendors)

Presented By:

Due Diligence: Scope/Risk Analysis Country/Revenue

CPI Score

Go‐to‐Market StrategyNature of Business

Sales to Government Customers

Presented By:

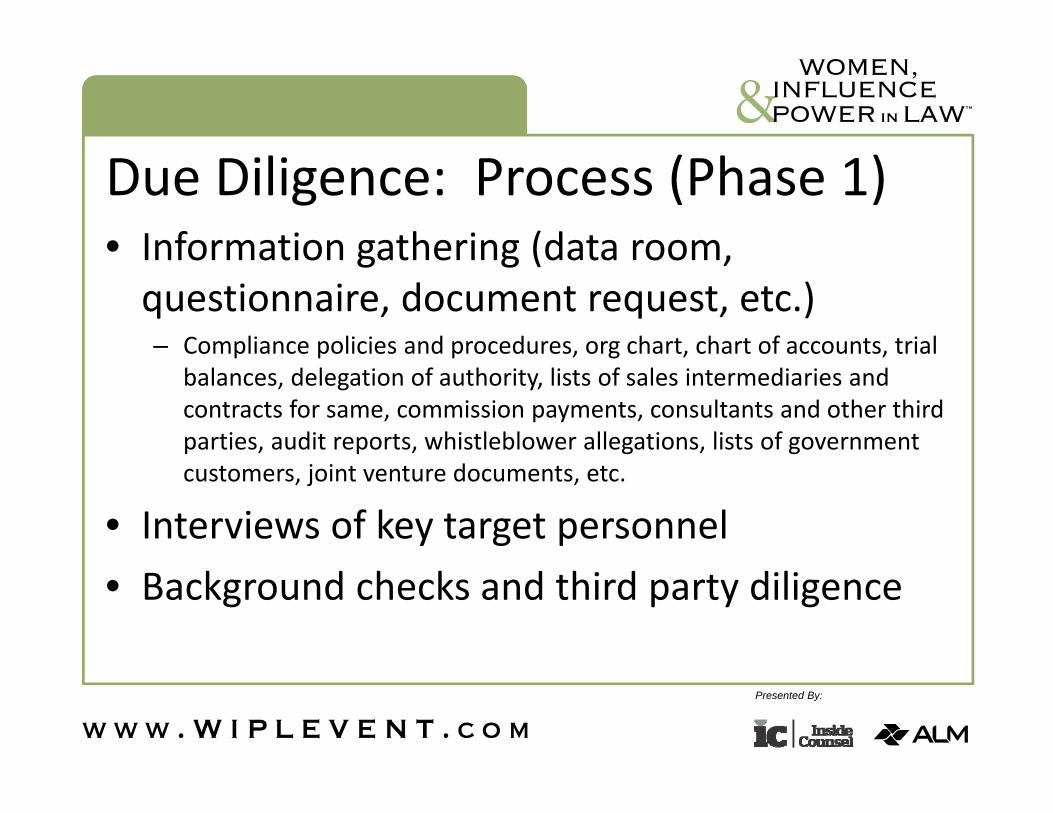

Due Diligence: Process (Phase 1) • Information gathering (data room, questionnaire, document request, etc.)– Compliance policies and procedures, org chart, chart of accounts, trial

balances, delegation of authority, lists of sales intermediaries and contracts for same, commission payments, consultants and other third parties, audit reports, whistleblower allegations, lists of government customers, joint venture documents, etc.

• Interviews of key target personnel• Background checks and third party diligence

Presented By:

Due Diligence: Process (Phase 2)• Analyze chart of accounts/trial balance data• Select transactions for testing• On‐site field work: forensic testing and interviews

• Additional procedures: investigations, confidential source inquiries, market intelligence surveys, etc.

Presented By:

Due Diligence: Focus Areas• Use of sales intermediaries• Tender participation and expenses• Pricing, commissions, discounts, rebates, free goods, credit notes

• Accounting and control environment

Revenue• Travel, entertainment, gifts• Marketing activities and donations• Consultants and other third parties (e.g., customs, product registrations, licenses)

• Employee expense reimbursements and use of cash

Expense• History of issues, violations, investigations• Tone at top; compliance policies & programs• Leadership & integrity; business practices• Tax & labor matters, accounting/controls environment

Culture

Presented By:

Due Diligence: Final Risk Analysis• Informed by all procedures and other diligence work streams (e.g., legal, tax, finance)

• Conclusions:– Legal risk– Business Impact– Pre‐closing or integration action items

Presented By:

Mitigating FCPA Risk in M&A – Documentation

Presented By:

Documentation Overview • Representations and Warranties• Covenants• Indemnification• Exit Rights

Presented By:

Representations and WarrantiesAs broad as possible (all Sellers, affiliates, directors, officers, employees, agents, etc.)• Past and present compliance with “all applicable” laws, rules or regulations

including anti‐bribery laws (specifically reference FCPA if possible)• Direct or indirect• Make, offer, promise, approve, authorize or transfer of anything of value • to a “Government Official” (includes candidates and relatives)• To obtain, influence or induce improperly• Maintain accounting standards and procedures necessary to ensure that Seller(s)

makes and keeps books, records and accounts in reasonable detail that accurately and fairly reflect the transactions and disposition of assets.

• Maintains a system of internal accounting controls• Seller(s) is not owned by a Government Official, and does not employ a

Government Official (or any relative)

Presented By:

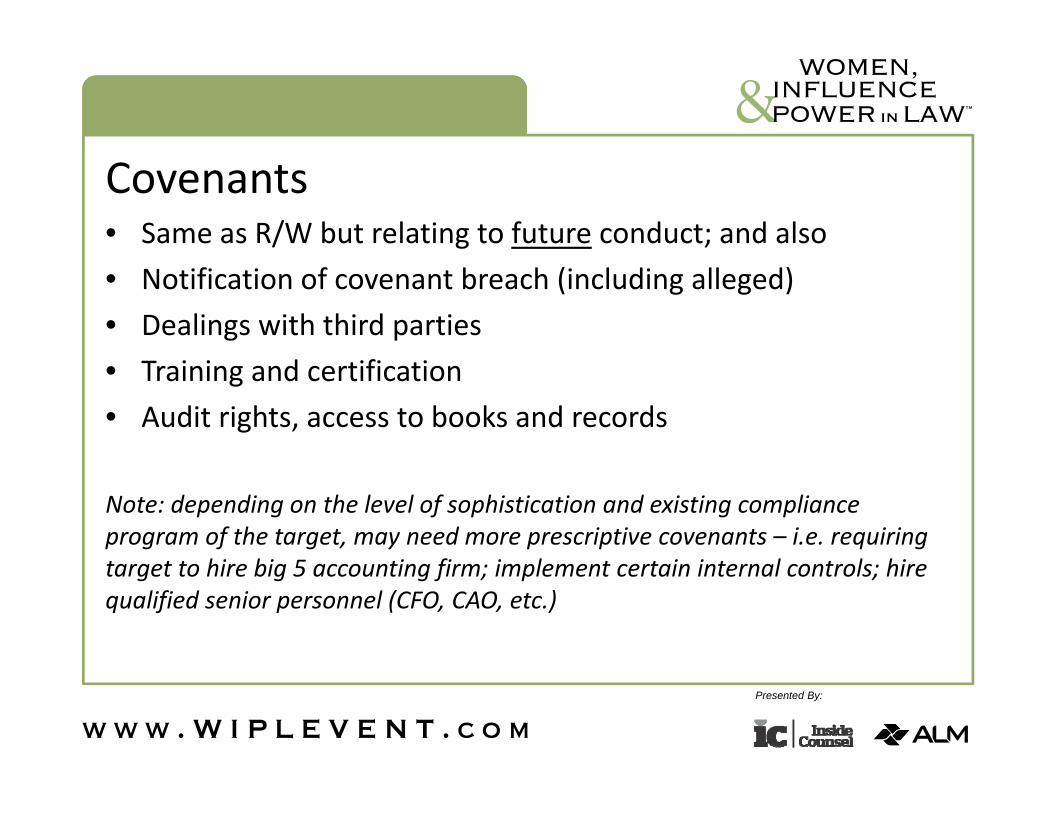

Covenants• Same as R/W but relating to future conduct; and also• Notification of covenant breach (including alleged)• Dealings with third parties• Training and certification• Audit rights, access to books and records

Note: depending on the level of sophistication and existing compliance program of the target, may need more prescriptive covenants – i.e. requiring target to hire big 5 accounting firm; implement certain internal controls; hire qualified senior personnel (CFO, CAO, etc.)

Presented By:

Indemnification• Broad definition of “Losses” – include lost profits, incidental,

consequential, attorney’s fees• Joint and several liability (in the case of multiple sellers)• Resist a “buyer’s knowledge” definition to reduce seller’s

liability• Consider restitution in addition to other remedies• De minimus, baskets (tipping), caps – consider no caps for

violation of anti‐corruption R/W/C• Survival – indefinite for violation of anti‐corruption R/W/C

Presented By:

Exit provisions• Termination rights• Put or Call option• Sale of Target (drag along)

Presented By:

Mitigating FCPA Risk in M&A – Structuring

Presented By:

Structuring Overview • Acquisition Structure • Domestic and Cross Border Transactions • Joint Ventures and Minority Investments

Presented By:

Acquisition Structure • Structure of target acquisition

– Stock versus assets – Entire company versus business area/product line

• Assumption of liabilities – Successor liability

• Impact of FCPA risk – Deal terms and price

Presented By:

Domestic and Cross Border Transactions • Acquisitions between/among US issuers• Acquisitions by US issuers of foreign companies

• Acquisition by foreign companies of US issuers

Presented By:

Joint Ventures and Minority Investments • Management and control

– Duties and responsibility – Agency relationship

• Internal policies and procedures – Practical risks and implications

• Reputation and risk by association

Presented By:

Mitigating FCPA Risk in M&A – Integration

Presented By:

The next challenge• Integration is the final stage of an FCPA compliance process that began with pre‐signing due diligence

• DOJ and SEC have issued guidance on integration in their FCPA “Resource Guide”

• DOJ also has provided a useful enforcement perspective in conditions to an advisory opinion letter and deferred prosecution agreements with major companies

Integration Overview

Presented By:

Integration goals for FCPA compliance• Mitigate business risk

– Harm to operations under acquired arrangements that may violate FCPA

– Harm to reputation and business prospects upon disclosure of violations

• Mitigate enforcement risk– Demonstrate strong commitment to uncovering and preventing FCPA

violations– “DOJ and SEC have only taken action against successor companies in

limited circumstances, generally in cases involving egregious and sustained violations or where the successor company directly participated in the violations or failed to stop the misconduct from continuing after the acquisition.” (Resource Guide, p. 28)

Presented By:

What should the buyer do?• Buyer should pursue a vigorous post‐closing FCPA compliance program

• “DOJ and SEC evaluate whether the acquiring company promptly incorporated the acquired company into all of its internal controls, including its compliance program. Companies should consider training new employees, reevaluating third parties under company standards, and, where appropriate, conducting audits on new business units.” (Resource Guide, p. 62)

Presented By:

Where does the buyer start?• The pre‐acquisition due diligence review can provide a

roadmap for integration of acquired company into buyer’s corporate control and compliance environment

• Buyer should give priority to integration workstreams that target areas of identified business and regional risk

• Resource Guide and conditions to DOJ advisory opinion and deferred prosecution agreements emphasize importance of:– Completing integration as quickly as possible (within 12‐18 months),

particularly when pre‐acquisition due diligence was not thorough– Conducting on‐site audits in appropriate cases

Presented By:

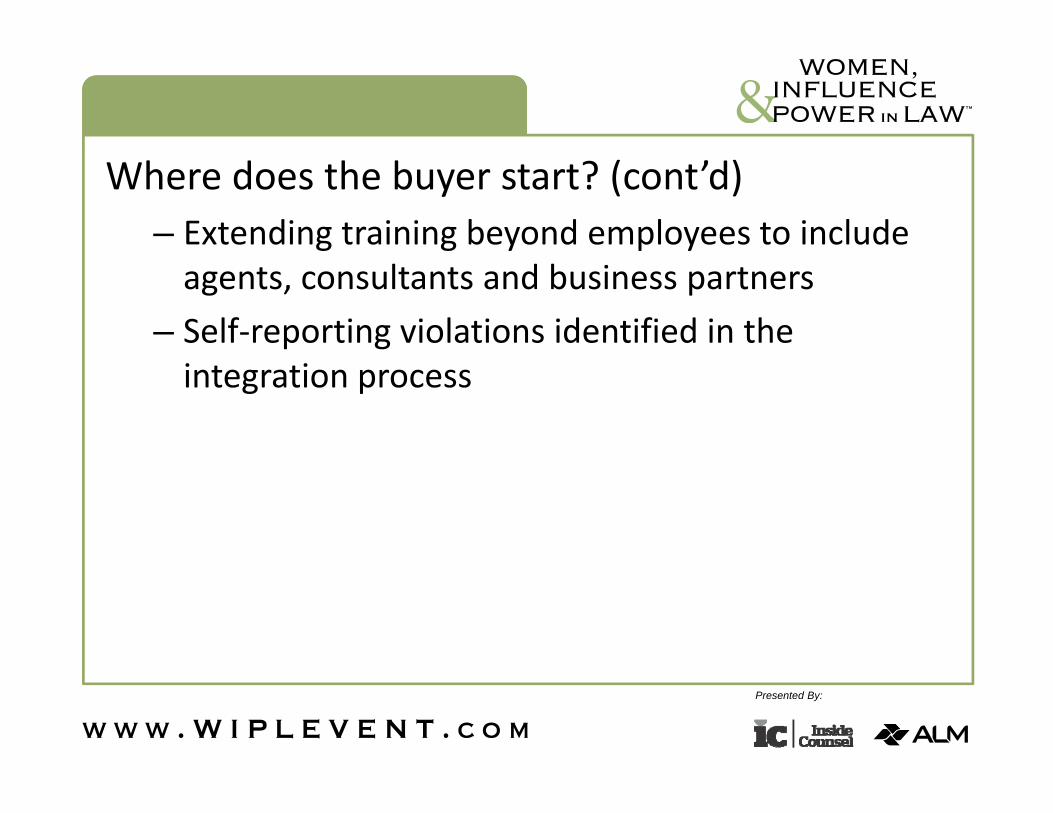

Where does the buyer start? (cont’d)– Extending training beyond employees to include agents, consultants and business partners

– Self‐reporting violations identified in the integration process

Presented By:

Key features of integration process• Here are “practical tips” from the Resource Guide (p. 29):

– Ensure that the acquiring company’s code of conduct and compliance policies and procedures regarding the FCPA and other anti‐corruption laws apply as quickly as is practicable to the newly acquired business

– Train the directors, officers and employees of the newly acquired business and, when appropriate, its agents and business partners on the FCPA and other anti‐corruption laws and the company’s code of conduct and compliance policies and procedures

– Conduct an FCPA‐specific audit of the newly acquired business as quickly as practicable

Presented By:

Key features of integration process (cont’d)– Disclose to DOJ and the SEC any corrupt payments discovered as part of post‐closing due diligence (in practice, decision whether to disclose involves weighing a variety of factors)

– On‐site compliance audits are particularly important, and reviews need to probe beyond financial statement materiality levels

Presented By:

Haliburton opinion (June 2008)• Haliburton obtained an advisory opinion letter from DOJ

before entering into an agreement to acquire a U.K. public company in circumstances that did not permit adequate pre‐signing FCPA due diligence

• Haliburton’s undertakings focused on its post‐acquisition compliance plan and provide an indication of DOJ’s perspective on integration

• Haliburton agreed to submit to DOJ within 10 business days after closing a comprehensive, risk‐based FCPA due diligence work plan addressing:– Use of agents and other third parties– Commercial dealings with state‐owned customers

Presented By:

Haliburton opinion (June 2008) (cont’d)– Joint venture, teaming and consortium arrangements– Customs and immigration matters– Tax matters– Government licenses and permits

• Haliburton agreed to an ambitious timetable to report to DOJ:– Within 90 days after closing, results of its high‐risk due diligence– Within 120 days after closing, results of its medium‐risk due

diligence– Within 180 days after closing, results of its lowest‐risk due

diligence– Within one year after closing, full remediation of any issues

identified during the one‐year period

Presented By:

Conditions to deferred prosecution agreements (DPAs)• Johnson & Johnson (J&J) (January 2011)

– Where anti‐corruption due diligence is not practicable before acquisition of a new business for reasons beyond J&J’s control, or due to any applicable law, J&J will conduct FCPA and anti‐corruption due diligence subsequent to the acquisition and report to DOJ any corrupt payments, falsified books and records or inadequate internal controls

– J&J will ensure that J&J ‘s policies and procedures regarding the anti‐corruption laws and regulations apply as quickly as is practicable, but in any event no less than one year post‐closing, to the newly acquired business

Presented By:

Conditions to deferred prosecution agreements (DPAs) (cont’d)

– For those operating companies that are determined not to pose corruption risk, J&J will conduct periodic FCPA audits or will incorporate FCPA components into financial audits

– J&J also committed to:• Train directors, officers, employees, agents, consultants, representatives, distributors, joint venture partners and relevant employees thereof, who present corruption risk to J&J, on the anti‐corruption laws and regulations and J&J’s related policies and procedures

• Conduct an FCPA‐specific audit of all newly acquired businesses within 18 months of acquisition

Presented By:

Conditions to deferred prosecution agreements (DPAs) (cont’d)• Data Systems & Solutions LLC (DS&S) (June 2012)

– If DS&S discovers any corrupt payments or inadequate internal controls as part of its due diligence of newly acquired entities, it will report that conduct to DOJ

– DS&S will ensure that its policies and procedures regarding the anti‐corruption laws apply as quickly as is practicable to newly acquired businesses and will promptly:

• Train directors, officers, employees, agents, consultants, representatives, distributors, joint venture partners and relevant employees thereof, who present corruption risk to DS&S, on the anti‐corruption laws and DS&S’s policies and procedures regarding anti‐corruption laws

• Conduct an FCPA‐specific audit of all newly acquired businesses as quickly as practicable

Presented By:

Conditions to deferred prosecution agreements (DPAs) (cont’d)• Pfizer H.C.P. Corporation (August 2012)

– When anti‐corruption due diligence is appropriate but not practicable prior to acquisition of a business for reasons beyond Pfizer’s control, or due to any applicable law, Pfizer will conduct anti‐corruption due diligence subsequent to the acquisition and report to DOJ any corrupt payments or falsified books and records

– Pfizer will ensure that Pfizer’s policies, standards and procedures regarding anti‐corruption laws and regulations apply as quickly as is practicable, but in any event no more than one year post‐closing, to newly acquired businesses, and will promptly:

• Train directors, officers and senior managers, and those employees working in positions involving activities covered by Pfizer’s policies regarding anti‐corruption and compliance with the FCPA, and, where necessary and appropriate, agents and business partners

• Include all newly acquired businesses in Pfizer’s regular anti‐corruption auditing schedule

Presented By:

Mitigating FCPA Risk in M&A – Q&A