6.auditsdm

DESCRIPTION

elektroTRANSCRIPT

AUDITSUMBER DAYA

MANUSIA

OVERVIEW of the HUMAN RESOURCE

MANAGEMENT PROCESSThe human resource process starts

with the establishment of sound policies for hiring, training,

evaluating, counseling, promoting, compensating, and taking remedial

actions for employees

• A human resource audit evaluates the personnel activities used in an organization. The audit may include one division or entire company

• Suatu daftar periksa untuk menilai seluruh aspek dari manajemen sumber daya manusia dalam suatu perusahaan

LINGKUP AUDIT SDM

LINGKUP AUDIT SDM• Audit SDM adalah proses evaluasi

atas berbagai aktivitas manajemen SDM yang bertujuan memperbaiki aktivitas-aktivitas tersebut

• Audit SDM memberikan umpan balik mengenai seberapa baik para manajer menjalankan tugas-tugas yang terkait dengan pengelolaan SDM

• Audit SDM merupakan kontrol kualitas secara menyeluruh atas berbagai aktivitas pengelolaan SDM dalam perusahaan dan bagaimana aktivitas-aktivitas tersebut mendukung strategi perusahaan.

• Audit SDM mencakup:– Audit Strategi Perusahaan– Audit Fungsi SDM– Audit Kepatuhan Manajerial– Audit Kepuasan Karyawan

LINGKUP AUDIT SDM

It gives feedback about :1. The function of operating managers 2. The human resource specialists3. How well managers are meeting

their human resource dutiesIn short, the audit is an overall quality control check on human resource activities in a division or company and how those activities support the organization’s strategy

Flowchart for EarthWear Clothiers

OperatingHuman

Resource

DepartmentsDepartments

Payroll

Initiatespersonnelchanges

Payrollmaster filechanges

Reviewsmaster file

changereport

Review

By date

Payrollmaster filechanges

Timecards

Approvedby

supervisor

Timecards

Input

Errorcorrections

From IT

To IT

Flowchart for EarthWear Clothiers

PayrollDepartmentsDepartments

ITPayrollmaster

file

Errorreport

Payrollprocessing

Payrollchecks

Payrollregister

Errorcorrections

Payrollregister

Reviewby date

Payroll masterfile changes

report

Payrollreporting

Generalledger

Periodicpayrollreports

Tax reportsand forms

MANFAAT AUDIT SDM

• Mengidentifikasi kontribusi departemen SDM bagi organisasi.

• Meningkatkan citra profesional departemen SDM.

• Mendorong tanggung jawab dan profesionalisme yang lebih tinggi di kalangan karyawan departemen SDM

• Memperjelas tugas dan tanggung jawab departemen SDM.

• Mendorong keseragaman kebijakan-kebijakan dan praktik-praktik personalia

• Menemukan masalah-masalah personalia yang penting.

• Memastikan kepatuhan yang tinggi terhadap persyaratan legal.

• Mengurangi biaya-biaya SDM melalui prosedur personalia yang lebih efektif.

• Menciptakan penerimaan yang lebih besar akan perubahan-perubahan yang diperlukan dalam departemen SDM.

• Memberikan tinjauan yang seksama atas sistem informasi departemen SDM.

MANFAAT AUDIT SDM

• Identifies the contribution of the personnel departments to the organization

• Improves professional image of the personnel department

• Encourages greater responsibility and professionalism among members of the personnel department

• Clarifies the personnel department’s duties and responsibilities

• Finds critical personnel problems

MANFAAT AUDIT SDM

THE SCOPE of HUMAN RESOURCE AUDITS

• Audit of Corporate StrategyCorporate Strategy concerns how the organization is going to gain competitive advantage.

• Audit of the Human Resource FunctionAudit touches on Human Resource Information System, Staffing and Development, and Organization Control and Evaluation.

• Audit of Managerial ComplianceReviews how well managers comply with human resource policies and procedures.

• Audit of Employee SatisfactionTo learn how well employee needs are met.

AUDIT of CORPORATE STRATEGY (Audit Strategi Perusahaan)

• Strategi perusahaan berkaitan dengan cara perusahaan menciptakan keunggulan bersaing.

• Memahami strategi perusahaan sangat penting bagi manajemen SDM, karena MSDM bisa dikatakan ‘efektif’ hanya jika mampu berkontribusi bagi tercapainya sasaran stratejik perusahaan.

• Para karyawan departemen SDM bisa mempelajari strategi perusahaan lewat wawancara dengan para ekskutif kunci, mempelajari rencana bisnis jangka panjang, dan melakukan peninjauan lingkungan secara sistematis guna mengungkap tren-tren yang berubah.

• Departemen SDM harus mengaudit fungsinya, kepatuhan manajerial, dan penerimaan para karyawan atas kebijakan dan praktik SDM dalam kaitannya dengan rencana stratejik perusahaan.

AUDIT of CORPORATE STRATEGY (Audit Strategi Perusahaan)

AUDIT of the HR FUNCTION

1. Human Resource Information System- Human Resource Plans : Supply and

demand estimates; skill inventories; replacement charts and summaries

- Job Analysis Information : Job standards, Job descriptions, Job specifications

- Compensation Management : Wage, salary, and incentive levels; Fringe benefit package; Employer-provided services

2. Staffing and Development

• Recruiting : sources of recruits, availability of recruits, employment applications

• Selection : selection ratios, selection procedures, equal opportunity.

• Training and development : orientation program, training objectives and procedures, learning rates

• Career development : internal placement, career planning program, human resource development efforts

3. Organization Control and Evaluation

• Performance appraisals : standards and measures of performance, performance appraisal techniques, evaluation interview.

• Labor-Management Relations : Legal compliance, management rights, dispute resolution problems.

• Human Resource Controls : employee communications, disicipline procedures, change and development procedures,

AUDIT FUNGSI SDM• Merupakan penilaian atas berbagai fungsi yang

dijalankan departemen SDM.• Untuk setiap aktivitas SDM yang dinilai, tim audit

perlu melakukan hal-hal sebagai berikut:– Mengidentifikasi siapa yang bertanggung jawab– Menentukan tujuan – Meninjau kebijakan dan prosedur untuk

mencapai tujuan– Mengambil sampel arsip sistem informasi SDM

untuk menilai apakah kebijakan dan prosedur diikuti dengan benar

– Mempersiapkan laporan– Mengembangkan rencana tindakan untuk

memperbaiki kesalahan– Menindaklanjuti rencana tindakan untuk

melihat apakah permasalahan bisa terselesaikan

Berbagai Area dalam Audit Fungsi SDM

• Sistem Informasi SDM– Informasi Analisis Jabatan

• Standard jabatan• Deskripsi jabatan• Spesifikasi jabatan

– Rencana SDM• Estimasi permintaan dan penawaran• Inventori keahlian• Bagan dan ringkasan penggantian

– Administrasi Kompensasi• Tingkat gaji, upah, dan insentif• Paket tunjangan• Layanan perusahaan bagi karyawan

Berbagai Area dalam Audit Fungsi SDM

• Penyediaan dan Pengembangan Karyawan– Rekrutmen

• Sumber rekrutmen• Ketersediaan calon karyawan• Lamaran kerja

– Seleksi• Rasio seleksi• Prosedur seleksi• Kesetaraan kesempatan

Berbagai Area dalam Audit Fungsi SDM

• Penyediaan dan Pengembangan Karyawan– Pelatihan dan Orientasi

• Program orientasi• Tujuan dan prosedur pelatihan• Tingkat pembelajaran

– Pengembangan Karir• Keberhasilan penempatan internal• Program perencanaan karir• Upaya pengembangan SDM

Berbagai Area dalam Audit Fungsi SDM

• Kontrol dan Evaluasi Organisasi– Penilaian Kinerja

• Standard dan ukuran kinerja• Teknik penilaian kinerja• Wawancara evaluasi

– Hubungan Karyawan-Manajemen• Kepatuhan hukum• Hak-hak manajemen• Penyelesaian perselisihan

Berbagai Area dalam Audit Fungsi SDM

• Kontrol dan Evaluasi Organisasi– Kontrol SDM

• Komunikasi karyawan

• Prosedur kedisiplinan

• Prosedur perubahan dan pengembangan

– Audit SDM• Fungsi SDM

• Manajer operasi

• Umpan balik karyawan

THE MAJOR FUNCTIONS

PersonnelAuthorization of hiring, firing, wage-rate and salary adjustments, salaries, and payroll deductions.

SupervisionReview and approval of employees' attendance and time information; monitoring of employee scheduling, productivity, and payroll cost variances.

TimekeepingProcessing of employees' attendance and time information and coding of account distribution.

Payroll processing

Computation of gross pay, deductions, and net pay; recording and summarization of payments and verification of account distribution.

Disbursement Payment of employees' compensation and benefits.

General ledger Proper accumulation, classification, and summarization of payroll in the general ledger.

TASKS of AUDITORS• Identify who is responsible for each activity.• Determine the objectives sought by each

activity.• Review the policies and procedures used to

achieve these activities.• Prepare a report commending proper

objectives, policies, and procedures.• Develop an action plan to correct errors in

each activity.• Follow up the action plan to see if it solved

the problems found through the audit.

AUDIT of MANAGERIAL COMPLIANCE

• Compliance with laws is especially important. When safety, compensation, or labor laws are violated, the government holds the company responsible.

• If managers ignore policies or violate employee relations laws, the audit should uncover these errors so that corrective action can be started.

AUDIT of EMPLOYEE SATISFACTION

• Employee satisfaction refers to an employee’s general attitude toward his or her job.

• When employee needs are unmet, turnover, absenteeism, and union activity are more likely. To learn how well employee needs are met, the audit team gathers data from workers.

• The team collects information about wages, benefits, supervisory practices, career planning assistance, and other dimensions of job

DAFTAR PERIKSA SDM (David Stevens)

1. Struktur Organisasi2. Uraian / Deskripsi posisi3. Rencana keberhasilan manajemen4. Kebijakan rekruitmen5. Prosedur rekruitmen6. Program perkenalan7. Penilaian kinerja8. Penilaian potensi individu9. Perencanaan jenjang karier10.Program pelatihan11.Administrasi kompensasi12.Fungsi departemen SDM13.Perencanaan manusia

14. Catatan pribadi15. Relevansi aplikasi komputer16. Pemahaman iklim organisasi 17. Pembagian informasi dengan karyawan18. Desain pekerjaan19. Hubungan industrial20. Kesehatan karyawan21. Keamanan karyawan22. Pelayanan karyawan23. Pengumpulan angka statistik24. Praktek pengunduran diri25. Dokumentasi / formulir26. Keamanan 27. Interaksi sosial

Menurut Sherman & Bohlander, audit SDM memberikan peluang untuk:

1. Menilai efektivitas fungsi SDM2. Memastikan ketaatan terhadap hukum,

kebijakan, peraturan dan prosedur3. Menetapkan pedoman untuk penetapan

standar4. Memperbaiki mutu staff SDM5. Meningkatkan citra dari fungsi SDM6. Meningkatkan perubahan dan kreatifitas7. Menilai kelebihan dan kekurangan dari fungsi

SDM8. Memfokus staff SDM pada masalah penting9. Membawa SDM lebih dekat pada fungsi-fungsi

yang lain.

FINANCIAL STATEMENT ACCOUNTS AFFECTED

Type of Transaction Account AffectedPayroll transactions Cash.

Inventory.Direct and indirect labor expense accounts.Various payroll-related liabilitiy and expense accounts.

Accrued payroll liability Cash.transactions Various accruals (such as payroll taxes and pension costs).

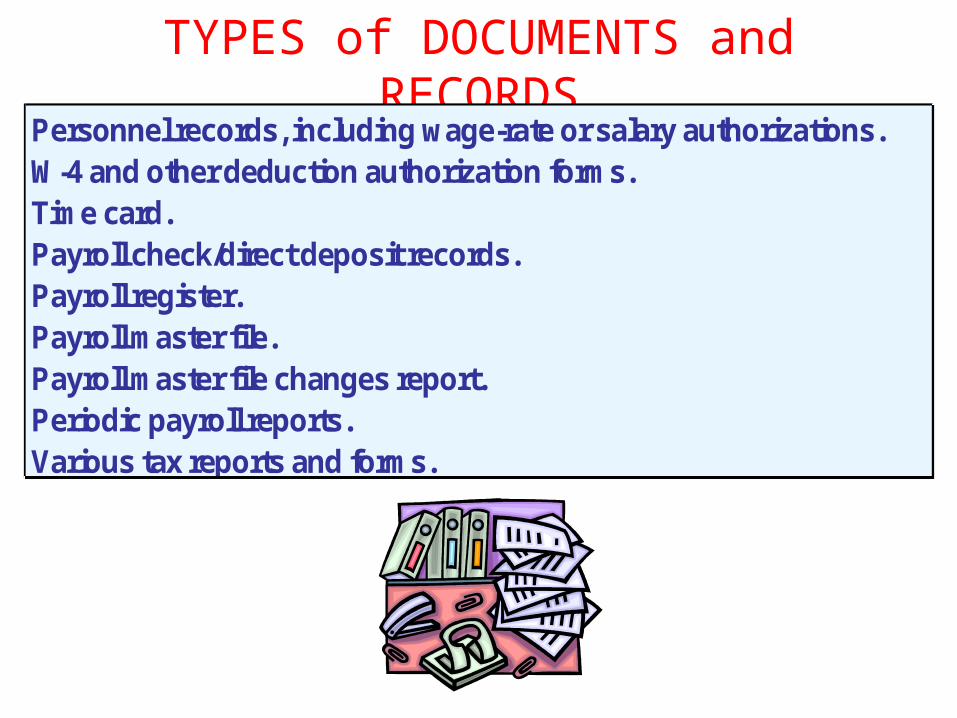

TYPES of DOCUMENTS and RECORDS

Personnel records, including wage-rate or salary authorizations.W-4 and other deduction authorization forms.Time card.Payroll check/direct deposit records.Payroll register.Payroll master file.Payroll master file changes report.Periodic payroll reports.Various tax reports and forms.

Personnel records, including wage-rate or salary authorizations.W-4 and other deduction authorization forms.Time card.Payroll check/direct deposit records.Payroll register.Payroll master file.Payroll master file changes report.Periodic payroll reports.Various tax reports and forms.

PELAKSANAAN AUDIT

– Audit dapat dilakukan oleh personel internal maupun eksternal

Langkah langkah dalam proses audit (Walter R. Mahler)

1. Memperkenalkan gagasan audit dan menekankan manfaat yang diperoleh

2. Memilih personel dengan ketrampilan yang luas dan memberikan pelatihan

3. Mengumpulkan data dari tahun yang berbeda dalam organisasi

4. Menyiapkan laporan audit untuk manager lini dan evaluasi departemen SDM

5. Mendiskusikan laporan dengan manager operasi

6. Menyatukan tindakan korektif

PENDEKATAN AUDIT SDM

1. Menetapkan ketaatan hukum dan peraturan

2. Mengukur kesesuaian program dan tujuan3. Menilai performa program

FUNGSI SDM

1. Perencanaan2. Pemilihan3. Pelatihan4. Penilaian5. Kompensasi6. Hubungan ketenagakerjaan

MEMANFAATKAN TEMUAN AUDIT– Untuk mengidentifikasi tipe tindakan

korektif yang diperlukan

METODE UNTUK MENGANALISA TEMUAN1. Membandingkan program SDM dengan

organisasi2. Berdasar audit dari beberapa sumber otoritas3. Mempercayai suatu ratio atau rata rata staf

SDM dengan total4. Menggunakan audit ketaatan untuk mengukur

aktifitas SDM apakah sesuai dengan kebijakan, prosedur dan peraturan

5. Mengelola departemen SDM berdasarkan sasaran

MENYIAPKAN LAPORAN dan REKOMENDASI

– Laporan hasil temuan, evaluasi dan rekomendasi untuk memperbaiki kekurangan dan kelemahan program SDM

THE AUDIT REPORT Findings of research are used to developed a

picture of the organization’s resource activities. For this information to be useful, it is compiled into audit report.

The audit report is a comprehensive description of human resource activities that includes both commendations for effective practices and recommendations for improving practices that are less effective.

Audit report often contain several sections. One part is for line managers, another is for manager of specific human resource function, and the final part is for the human resource manager.

REPORT for LINE MANAGERS

• How line managers handle their duties such as:– Interviewing applicants– Training employees– Evaluating performance– Motivating workers– Satisfying employee needs

• The report also identifies people problems. Violations of policies and employee relations law are highlighted

REPORT for the HR SPECIALIST

• The specialists who handle employment training, compensation, and other activities also need feedback. Such feedbacks are :

1. Unqualified workers that need for training2. Qualified workers that need for

development3. What others company are doing4. Attitude operating managers toward

personnel policies5. Workers pay dissatisfaction

REPORT for HR MANAGER

• It is contains all the information given to both operating managers and staff specialists. In addition, HR Mangers gets feedback about :

• Attitude operating managers and employees about services given by HRD

• A review of HRD plans• Human resource problems and their

implication• Recommendations for needed

changes and priorities for their implementation

RESEARCH APPROACHES to AUDITS

1. Interviews

Interviews with employees and managers are one source of information about human resource activity. Employees and managers comments help the audit team find that need improvement.

• Another useful source of information is the exit interview. Exit interview are conducted with departing employees to learn their views of the organization.

2. Questionnaires/Surveys

Because interviews are time-consuming, costly, and often to only few people, many human resource departments use questionnaires. Through questionnaire surveys, a more comprehensive picture of employee treatment can be developed. Questionnaire may also lead to more candid answers than face-to-face interviews.

- employee attitude about supervisors- Employee attitude about their jobs- Perceived effectiveness of human

resource department

3. Historical Analysis Not all the issues of interest to human

resource audit are revealed through interviews or questionnaires. Sometimes insight can be obtained by an analysis of historical records, such as:

- Safety and health records- Grievances records- Compensation studies- Scrap rates- Turnover and absenteeism records- Selection records- Affirmative action plan records- Training program records

4. External InformationOutside comparisons give the audit team a

perspective against which their firm’s activities can be judged.

Through Department of Labor, industry association, professional association numerous

statistics and report are compiled.

These organizations regularly publishes information about future employment

opportunities, employee turnover rates, work force projection, area wage and salary survey, work force demography, accident rates, and other data that can serve as benchmark for

comparing internal information.