7 fixed-income securities: characteristics and valuation ©2006 thomson/south-western

TRANSCRIPT

7

Fixed-Income Securities: Characteristics and Valuation

©2006 Thomson/South-Western

2

Introduction

This chapter focuses on the

characteristics and valuation of fixed-

income securities. Long-term debt

Preferred stock

3

Classification of Long-Term (L-T) Debt

Mortgage bonds secured

Debentures unsecured Subordinated and unsubordinated

Claims of subordinated debenture holders are considered only after the claims of unsubordinated debt holders

4

Types of L-T Debt

Equipment trust certificates

Income bonds

Collateral trust bonds

Pollution control bonds

Industrial revenue bonds

5

Characteristics of L-T Debt Indenture

covenants

Trustee

TIA 1939

Call feature

Call premium

Sinking fund

Equity-linked debt

convertible

warrant

Coupon rates

Size $25–$200 million

6

Corporate bonds

Market for corporate bonds Majority traded in the over-the-counter market Some larger issues traded on the NY Exchange

Quotations percent of par value $1000

DukeEn 63/8 08 6.8 40 93¾ –1/4

Meaning a Duke Energy bond with an interest rate (coupon rate) of 6.375 percent, maturing in 2008, yielding 6.8 percent, $40,000 dollars traded, closing price of $930.75, down $2.50 from the previous day.

Current information: http://www.etrade.com/

7

U.S. Government Debt Securities U.S. Treasury bills S-T

Maturities of 3, 6, and 12 months Minimum denominations of $10,000 Sold at a discount from maturity value

Treasury notes and bonds L-T Notes 1–10 year maturity Bonds 10–30 year maturity

8

Bond RatingsQuality S & P’s Moody’s

Highest AAA Aaa

High AA Aa

Upper Medium A A

Medium BBB Baa

Junk BB,B,CCC,CC,C

Ba,B,Caa,Ca,C

Default D

http://www.standardandpoors.com/ http://www.moodys.com/

9

Ratings

Higher rated bonds generally carry lower market yields.

Interest rate spread between ratings is less during prosperity than during recessions.

Junk bonds typically yield 3–6 percent or more.

10

International Bonds

Eurobonds Issued outside of the issuer’s country Denominated in the home currency May have less regulatory interference May have less disclosure requirements

Foreign bonds are issued in a single foreign country with interest and principal paid in that foreign currency.

11

Value of an Asset

Based on the expected future benefits over the life of the asset

Future benefits = cash flows (CFs)• Capitalization of cash flow method

– PV of the stream of future benefits discounted at an appropriate required rate of return

n

tt

t

i

CF

1 ) (1 V

0

12

Market Value of an Asset

Market price

Demand & Supply(D&S)

Approximated value

Equilibrium

D&S Intersection

Consensus Judgment

13

14

The Value of a Bond is the Present Value of its Cash Flows

nd

n

tt

d k

M

k

IP

1110

)(PVIF)(PVIFA0 k, nk, n MIP

15

16

Bond Prices and Interest Rates Relationship between P0 and kd

There is an inverse relationship between a bond’s value, P0, and its required rate of return, kd.

L-T vs. S-T Bonds A change in kd changes the value of a

long-term bond more than the value of a short-term bond.

17

18

Yield to maturity of a bond

nd

n

tt

d k

M

k

IP

1110

If the price is known, you can solve for the value of kd

which is the yield to maturity on the bond (the yield that makes the present value of the promised cash flows equal to the market price of the bond.

19

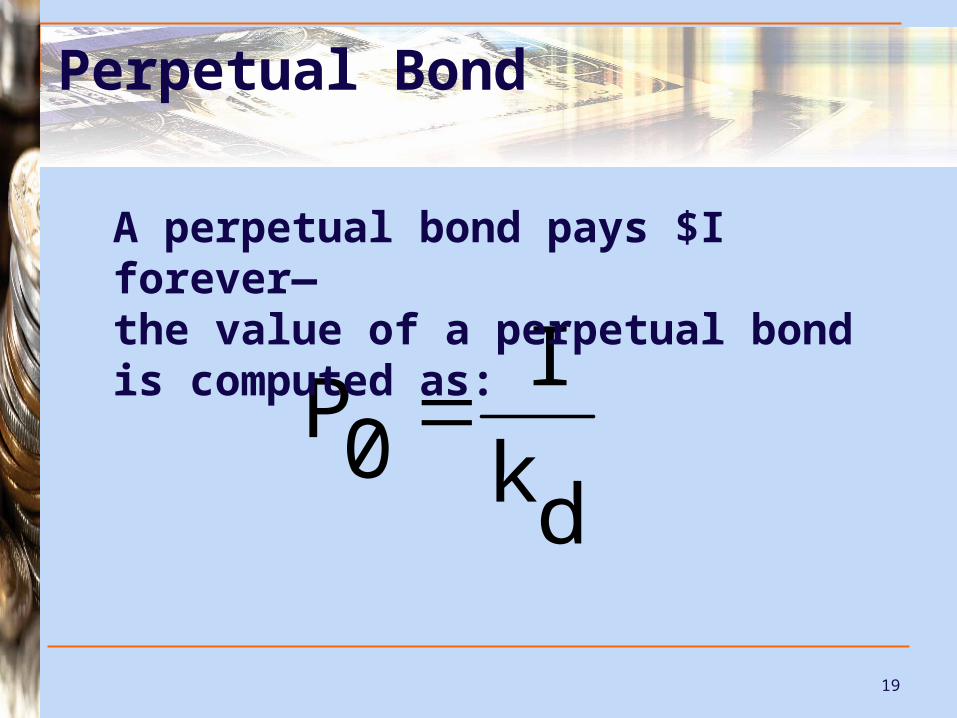

Perpetual Bond

dk

I0P

A perpetual bond pays $I forever—the value of a perpetual bond is computed as:

20

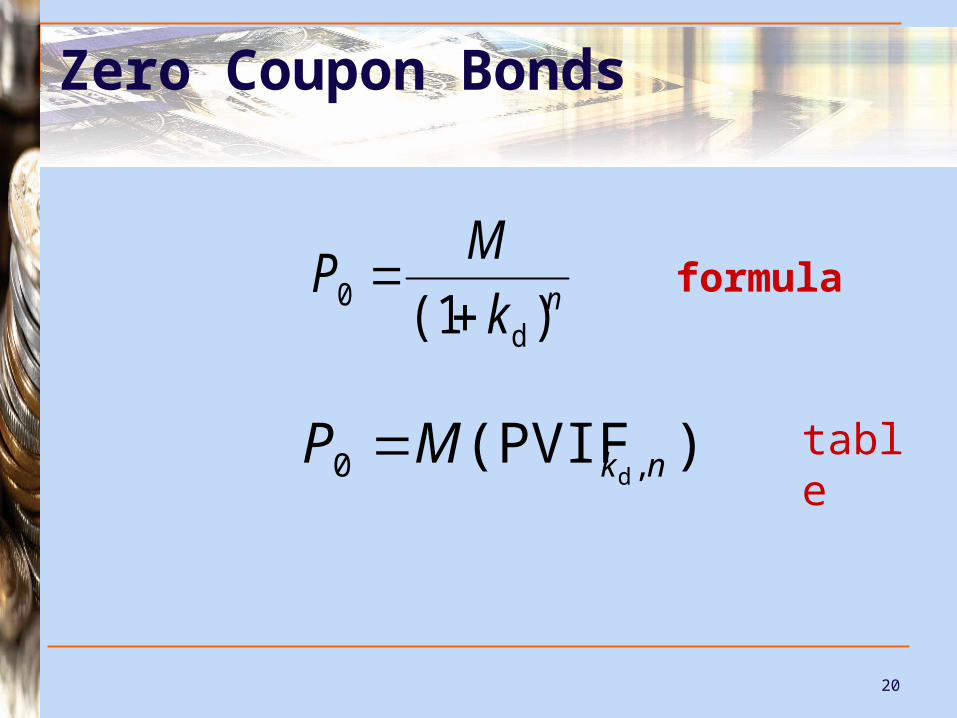

Zero Coupon Bonds

formula nk

MP

)(1 d0

)(PVIF ,0 d nkMP table

21

22

Ethical Issue

In many leveraged buyouts (LBOs), the buyer of the firm financed the purchase with a large amount of debt.

Often, stockholders made a large gain while bond prices plummeted because of the higher leverage the firm has assumed.

23

Preferred Stock (P/S)

Is in an intermediate position between C/S and L-T debt

Part of equity while increasing financial leverage Dividends on P/S are not tax deductible. Has preference over C/S with regard to earnings

and assets Dividends can not be paid on C/S unless the

preferred dividend for the period has been paid.

24

Characteristics of P/S

Selling price

Par value

Adjusted rate P/S

Cumulative

Participation

Maturity

Call feature

Voting rights

25

P/S Advantages and Disadvantages Advantages

Flexible Can increase

financial leverage

Corporate tax advantage

Disadvantages High after-tax

cost Dividends are

not tax deductible

26

Value of P/S

p

p

k

DP 0

A share of preferred stock pays $I forever—the value of a preferred share is computed as: