7y, - insurance corporation of british columbia · 2019-11-27 · 7y, information. ~l,c,{!j2_,~...

TRANSCRIPT

~ January 30, 2019

British Columbia Utilities Commission Suite 410 900 Howe Street Vancouver, BC V6Z 2N3

building trust. driving confidence.

Attention: Mr. Patrick Wruck, Commission Secretary and Manager, Regulatory Services

Re: Filing of Supplementary Information

Dear Mr. Wruck:

This letter is in further response to the British Columbia Utility Commission's (BCUC) letter dated January 28, 2019 (Exhibit A-6) extending the time for ICBC to file the redacted version of the supplementary information filed on January 24, 2019 (Exhibit B-1-3) in response to Exhibit A-5.

The supplementary information contains confidential information which, if disclosed, could influence ICBC's settlement negotiations with claimants. Disclosure of this information could therefore prejudice ICBC and its Basic insurance policyholders and thereby harm ICBC's financial interest. In addition, the supplementary information contains data that is only available on a total basis, meaning that the data set includes information about both Basic and Optional insurance. Disclosure of this information could similarly harm ICBC's economic interests. ICBC has therefore provided the supplementary information here with redactions. ICBC has separately filed the confidential version of the supplementary information with the BCUC.

Pursuant to Exhibit A-6, please find attached the redacted version of the supplementary information.

7Y, ~l,c,{!J2_,~

June Elder Manager, Corporate Regulatory Affairs gl/jb

Cc: Registered Interveners Bill Carpenter, Vice President, Insurance, ICBC

Attachment

151 West Esplanade I North Vancouver I British Columbia I V7M 3H9 I 604-661-2800 I [email protected]

Page 1 of 15

BI SEGMENTED ANALYSIS AS OF AUGUST 2018

A. EXECUTIVE SUMMARY

1. The purpose of this report is to describe the BI segmented analysis in connection with the

estimation of ICBC’s Total Bodily Injury (BI) claims costs (i.e., Basic and Optional BI). It

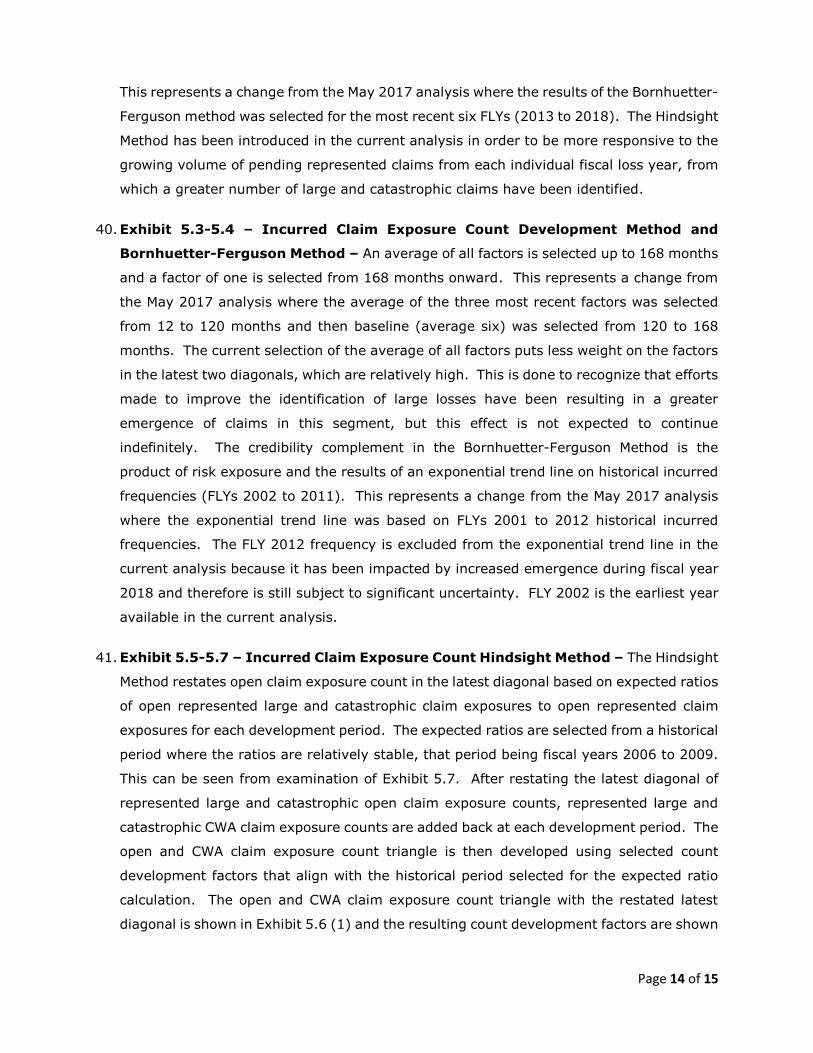

is prepared solely for that purpose and it is not intended, nor is it necessarily suitable, for

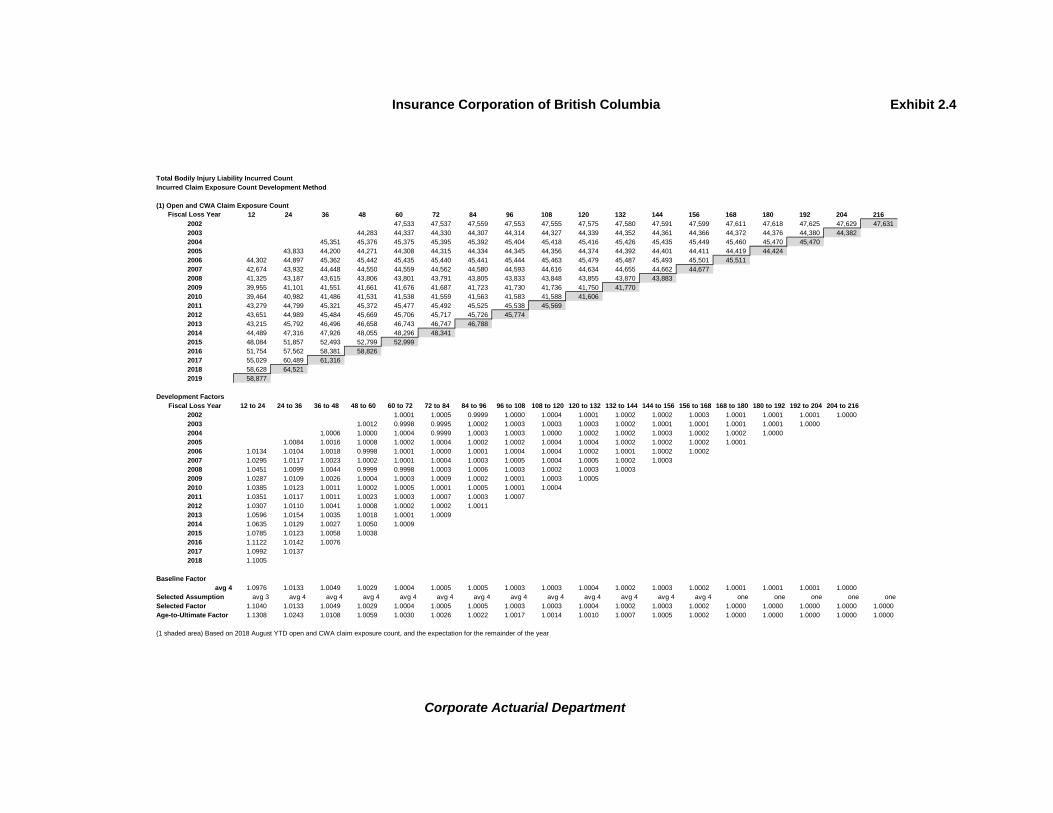

any other purpose. The intended users of this report are the Corporation, its external

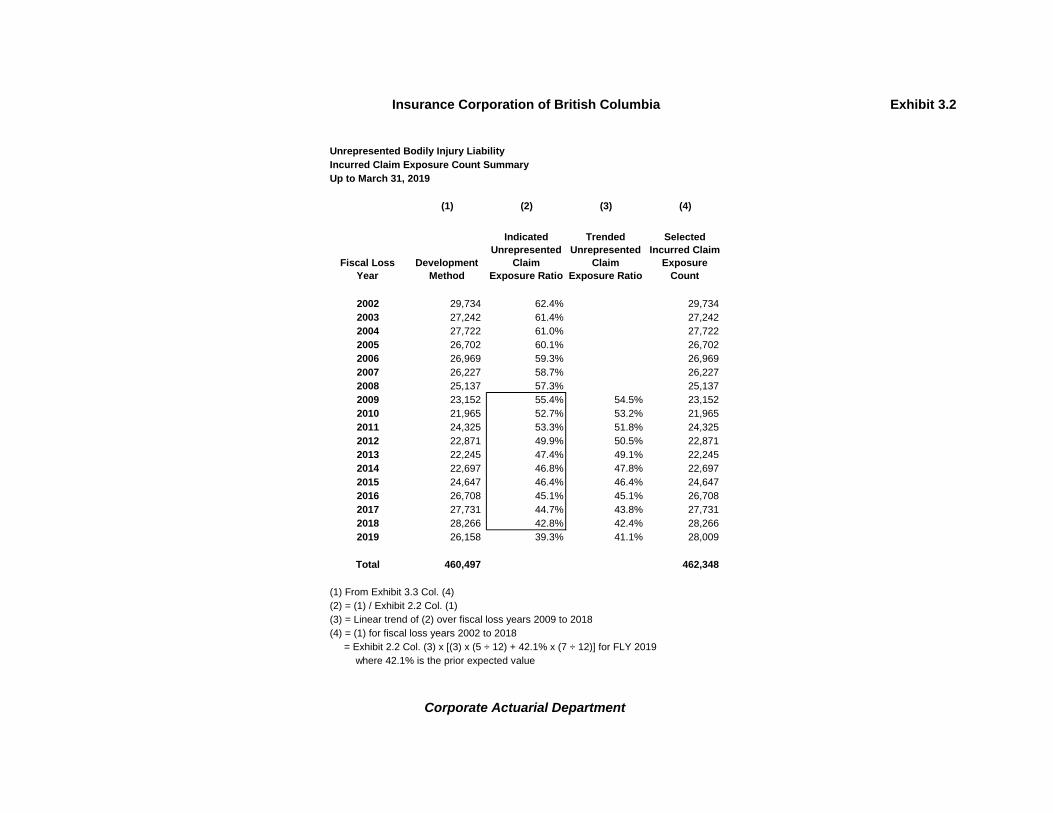

auditors, and provincial regulators of the Corporation. This report is confidential as it

contains proprietary information, which, if publicly revealed, could have material adverse

commercial consequences for the Corporation. Accordingly, neither the report nor its

content may be disclosed to any party, other than the intended users, without the prior

consent of the Corporation. Should a request for disclosure of this report or any of its

content be made by any third party, or granted to a third party under any freedom of

information legislation, then the Corporation should be notified immediately. If permission

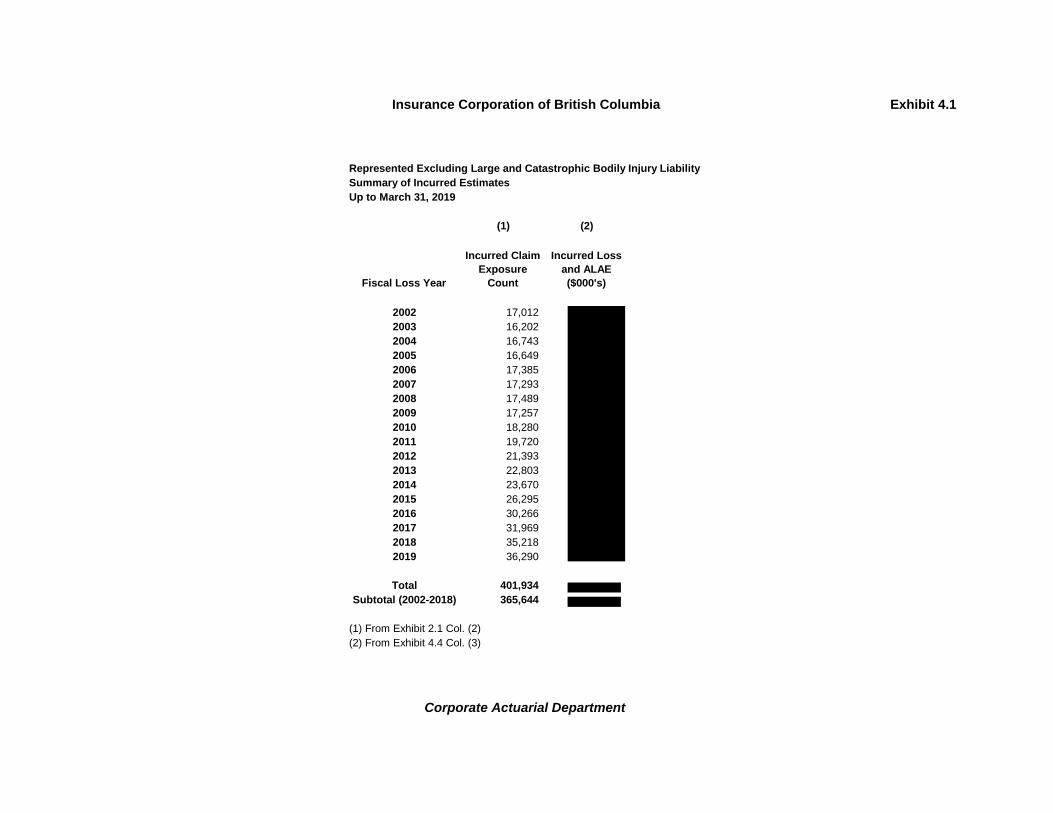

is granted for distribution of this document, it should be distributed in its entirety rather

than any excerpt thereof.

2. Unless noted otherwise, references to loss amounts within this report should be

understood as being gross of reinsurance but net of all other recovered amounts, and

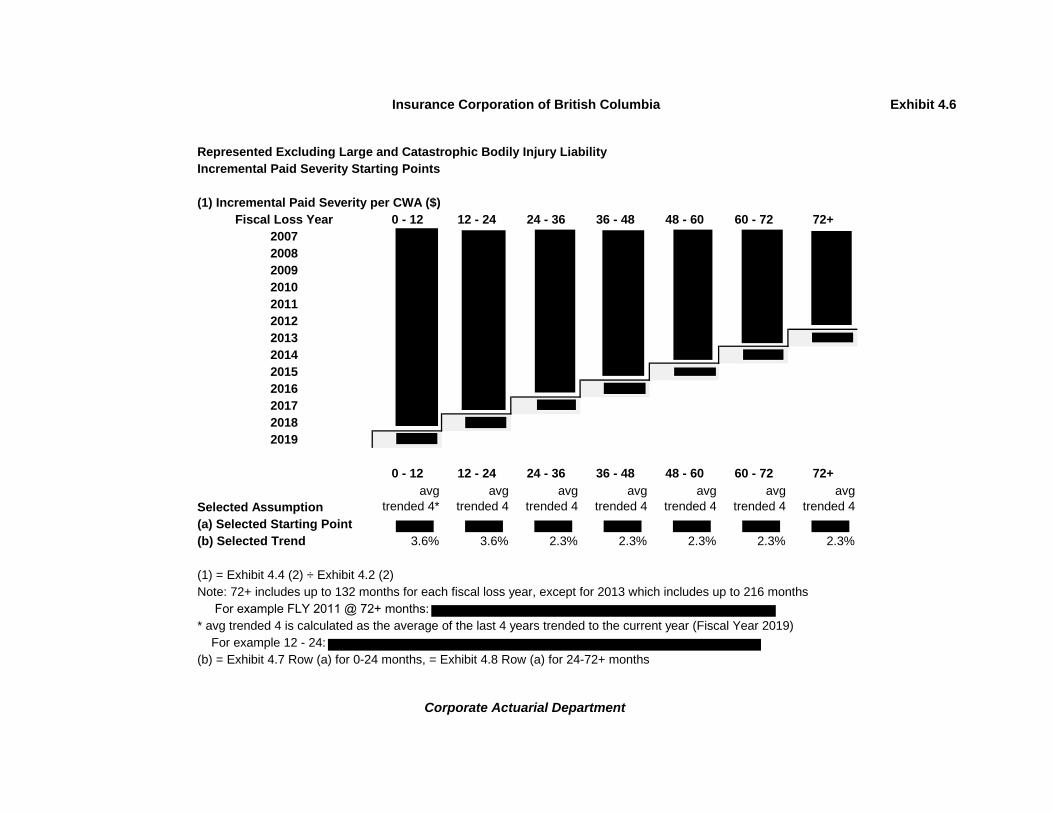

references to incurred count or incurred severity should be understood as excluding claims

completed with no amount (CNA).1

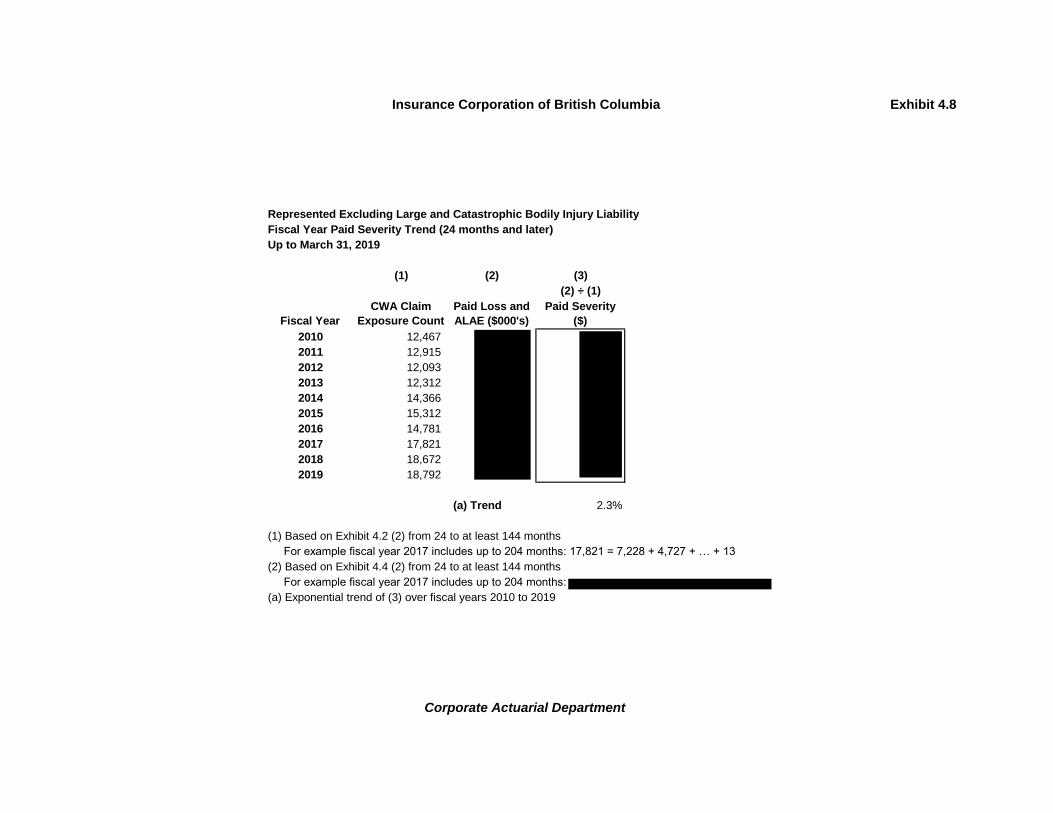

3. BI claim closure rates, which prior to fiscal year 2013 had been very stable, have

progressively fallen below their historical levels, and have not yet stabilized into a new,

steady pattern, as can be seen from Exhibits 4.3 and 5.9. ICBC actuaries are therefore

unable to rely fully on the standard Paid Development Method because a key assumption

inherent to the method is that claims closure patterns are stable over time.2 Instead,

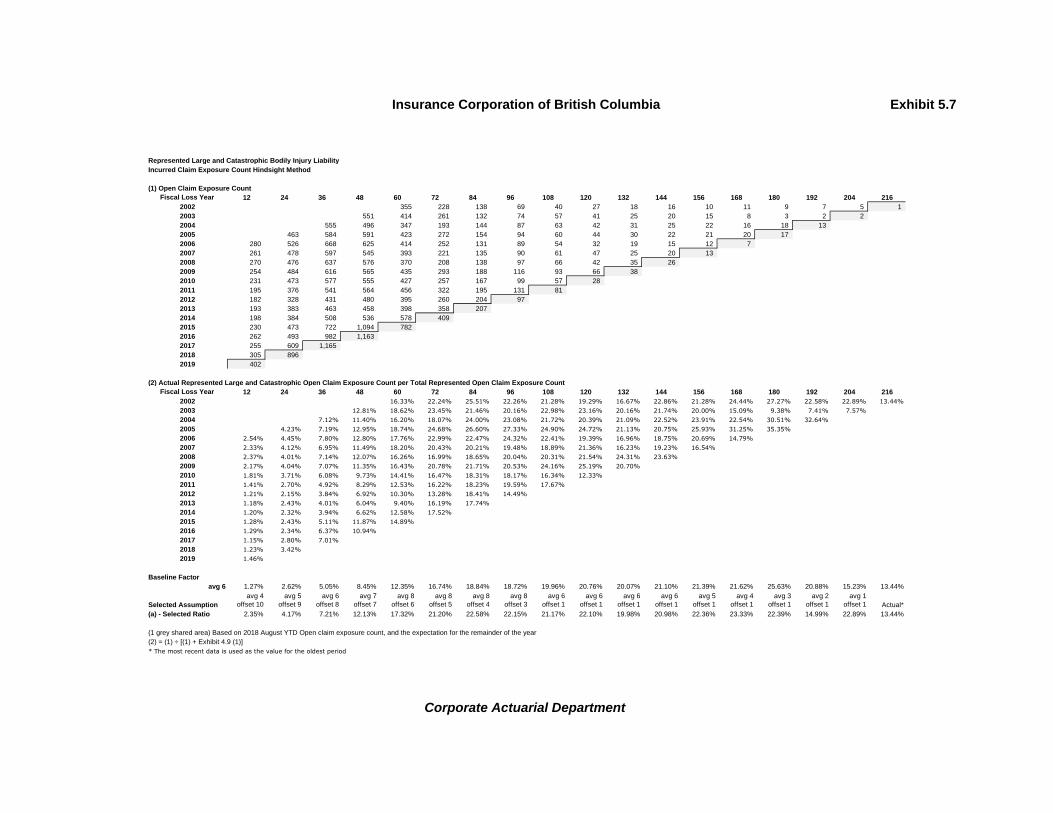

ICBC actuaries have relied on other methods. The Incurred Development Method is

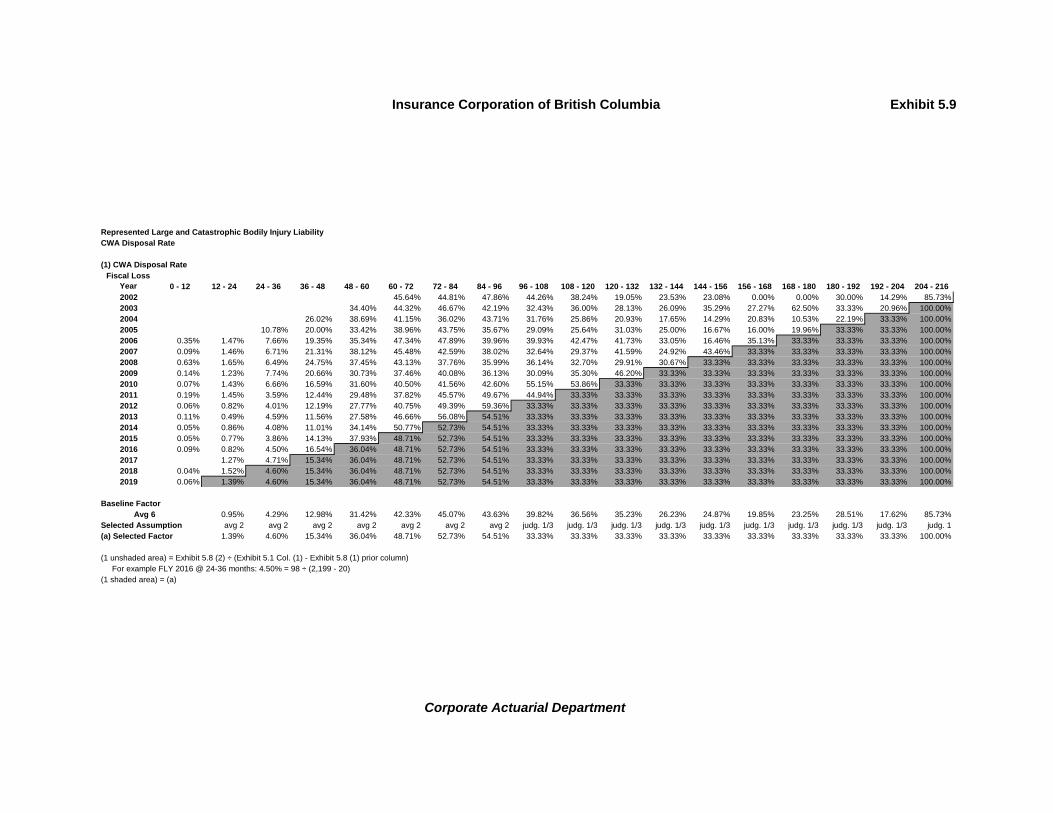

selected for fiscal loss years (FLYs) 2009 to 2011 because at this stage of their

development they are not affected to a significant extent by the changes to the closure

rates. The Hindsight Outstanding Severity Method is selected for FLYs 2012 to 2018,

which involves the estimation of “outstanding severities” (i.e., the average cost of claims

1 See paragraph 2 in Technical Appendix C.0, Chapter 3 of ICBC’s 2019 Revenue Requirements Application. 2 Since this assumption does not hold true for FLYs 2009 to 2018, the standard paid development method should only be used for FLYs prior to 2009 where there is little or no distortion from the slowdown in closures.

Page 2 of 15

that are not yet settled) by fiscal loss year, because it better accounts for the impact of

changing closure rates.

4. Outstanding severities are affected by changes in the pattern of closure rates and the mix

of claims by their level of complexity. ICBC actuaries have undertaken to refine their

estimation of outstanding severity by separating the claims data into segments of similar

complexity. The resulting three segments in the current analysis, listed in order of

increasing complexity, are: Unrepresented, Represented excluding Large and

Catastrophic, and Represented Large and Catastrophic. The frequency of claim exposures

shows different trend rates across the three segments, and recent changes in the closure

pattern of claims have not affected all segments equally. The refined segmentation of BI

claims has allowed ICBC actuaries to capture changes in the mix of the complexity of

outstanding claims that is driven by changes in the closure patterns within each segment,

and changes in the frequency of claim exposures by segment, which impacts severity

trend rates. The methodology used in this analysis, as well as changes to methodology

and assumptions from the previous analysis as of May 2017 are described in this report.

5. Key findings of the analysis are discussed below. The frequency shown is the incurred

CWA BI claim exposure frequency, which is calculated as the BI completed with amount

(CWA) claim exposure count divided by Third Party Liability earned exposure. The severity

shown is the incurred severity per BI CWA claim exposure count, which is calculated as

the BI incurred loss and allocated loss adjustment expense (ALAE) divided by the incurred

BI CWA claim exposure count.

As shown in Figure A.1, the frequency trend of represented claim exposures has turned

since FLY 2010 from a gently downward trend to a strong upward trend. In contrast,

the frequency of unrepresented claim exposures was steadily decreasing prior to FLY

2010, but while varying from year to year, has remained at a relatively consistent level

since FLY 2009. The shift in the mix of claims towards more represented claimants

has contributed to the shift in closure rates discussed above, as represented claims on

average are more complex and take longer to resolve. This has also led to a similar

shift in the mix of the pending claim inventory, which has contributed to a higher cost

of outstanding claims, as represented claims, on average, are also more costly to

resolve than unrepresented claims. Figure A.1 reflects a change in the proportion of

represented claim exposures from 47% for FLY 2010 to 57% for FLY 2018.

Page 3 of 15

Figure A.1 – BI Incurred Frequency by Legal Representation Status

As shown in Figure A.2, there has been a significant increase in the emergence of

represented large and catastrophic claim exposures from historical FLYs since the

previous analysis as of May 2017. Although these claims make up a relatively small

proportion of BI claim exposures, they can significantly influence the incurred costs,

as the average cost of these claim exposures is significantly higher than the average

cost of claim exposures in the other segments (as shown in Exhibit 5.11 for

Represented Large and Catastrophic compared to Exhibits 3.8 and 4.5 for

Unrepresented and Represented excluding Large and Catastrophic respectively). The

number of represented large and catastrophic claim exposures that emerged in fiscal

year 2018 grew by 81% from fiscal year 2017, to an unprecedented level. Many of

these claim exposures are from older FLYs: approximately one quarter of them are

from crashes occurring in FLYs 2013 and earlier, and approximately 44% of them are

from crashes occurring in FLYs 2014 and earlier. Although traditional catastrophic

injuries can often be readily identified soon after a crash occurs, some large BI claim

exposures may be the result of more complex cases that develop over time, and where

the information required to fully assess the costs becomes available many years

afterwards. The increased number of represented large and catastrophic claim

FLY 2010: 47% represented

FLY 2018: 57% represented

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Incu

rre

d F

req

eu

ncy

(C

laim

Exp

osu

re B

asis

)

Fiscal Loss YearUnrepresented Represented Long Term Trend (2002-2008)

Page 4 of 15

exposures therefore contributes to a higher cost of outstanding claim exposures that

is reflected across many FLYs.

Figure A.2 – Represented Large and Catastrophic Emergence

Even though the BI severity trend rates of represented and unrepresented claims have

been relatively mild, there is a stronger upward trend in the total severity, as shown

in Figure A.3 (+4.0% average annual growth rate from $37,000 for FLY 2011 to

$50,000 for FLY 2018). This is a direct consequence of the shift in the mix of claims

to higher complexity represented claims.

0

1,000

2,000

3,000

4,000

2014 2015 2016 2017 2018

Nu

mb

er o

f La

rge

($

20

0k+

) an

d C

atas

tro

ph

ic

Exp

osu

res

Fiscal Year

Page 5 of 15

Figure A.3 – BI Severity by Legal Representation Status

B. SUMMARY OF CHANGES FROM THE MAY 2017 ANALYSIS

6. The requirements in the Standards of Practice of the Canadian Institute of Actuaries with

respect to disclosure in an external user report (Section 1710.01) require a description

and a rationale for each assumption that is material to the results of the work, and

disclosure of any assumption (other than a model or data assumption) that is different

from the continuance of the status quo assumption. This report includes detailed

information about the basis of selection of many of the assumptions used in the derivation

of the estimation of ICBC’s Total BI claims costs. A discussion of those assumptions

considered to be of greatest relevance to the intended users of this report have been

included. ICBC believes that the disclosures made in this report comply with the spirit

and intent of Section 1710.01. A description and rationale for each and every assumption

that may be deemed to be material to the results of the estimation of Total BI claims costs

is not provided, however, ICBC considers the disclosures pertaining to the assumptions in

this report to be reasonable and appropriate to the circumstances. This section

summarizes the most significant changes to the methodology and presentation of the BI

segmented analysis in this report as compared to the May 2017 report. Other significant

Un

rep

resen

ted

In

cu

rred

Severit

y (

Cla

im E

xp

osu

re

Basis

)

Rep

resen

ted

an

d T

ota

l In

cu

rred

Severit

y (

Cla

im

Exp

osu

re B

asis

)

Fiscal Loss Year

Represented Total 2011-2018 Trend Unrepresented

Page 6 of 15

changes in the basis of selection of assumptions are identified in more detail in sections E

through H.

This analysis relies on a new and more accurate data source for the determination of

the legal representation status for claim exposures managed in the new claims

management system. Please see paragraph 14 for more detail. The impact of this

change is available.

The adjustment made in the May 2017 analysis for future closures based on the

integrated staffing model has been removed in this analysis. Closure rates have not

continued to increase, and future closure levels are now expected to be consistent with

observed closure rates from recent fiscal years. Had this adjustment not been included

in the May 2017 analysis, the BI incurred loss and ALAE estimated would have been

higher by $74 million.

The methods and summary exhibits for claim exposure counts including CNA are not

included in this analysis. Claim exposure counts including CNA do not directly impact

the loss and ALAE estimates. They were included in the May 2017 analysis to support

the adjustment for future closures based on the integrated staffing model. Since this

adjustment has been removed, as discussed in the previous paragraph, the inclusion

of claim exposure counts including CNA are no longer required.

Disposal rate selections for the Unrepresented and Represented excluding Large and

Catastrophic segments are based on longer averages compared to the May 2017

analysis. The experience has not generally shown the continuation of heightened

closure rates that were evident at that time.

Severity starting points are calculated from multi-year averages of severities, rather

than relying on the latest fiscal year value as in the May 2017 analysis. The use of

average severities will provide greater stability to the severity starting points over

time. The impact of this change is available.

Selected severity trends are based on periods that include the current fiscal year,

rather than ending in the previous fiscal year as in the May 2017 analysis. Including

the current fiscal year makes the trend more responsive to the most recent experience,

and the latest point now includes more actual data (5 months to August) as compared

to the May 2017 analysis (2 months to May). The impact of this change is available.

Page 7 of 15

As a result of the increasing emergence of large and catastrophic claims observed in

recent years, efforts have been made to improve the identification of large losses

earlier in the claims life cycle, including through reviews of pending claims. Since a

further increase in the emergence of large claims would be expected to result from

these efforts, but for only a limited period of time, the latest year’s experience is no

longer most representative of expected future experience for emergence of large and

catastrophic BI claims. Therefore, a longer experience period has been selected for

the development of large and catastrophic claim exposure counts. In addition, a new

method has been introduced in order to reflect the risk of large losses yet to emerge

from the growing volume of pending represented claims from each individual fiscal

loss year. This method is referred to as the Hindsight Method, and it assumes that at

each development age, the proportion of pending represented claim exposures that

are large and catastrophic in older, more mature fiscal loss years will hold true for the

more recent, less mature fiscal loss years. The application of the Hindsight Method is

described below in paragraph 41, and is shown in Exhibits 5.5 to 5.7.

C. OVERVIEW OF ANALYSIS

7. This analysis produces estimates of Total (Basic and Optional) BI incurred loss and ALAE,

from which Basic amounts are derived for use in the loss and ALAE estimation methods

presented in the 2019 Revenue Requirements Application (see Chapter 3, Technical

Appendix C.1.5.3).

8. The 2019 Revenue Requirements Application analysis requires Basic BI estimates of

incurred loss and ALAE. However, the amount of Basic coverage applies at the claim level

(and separately for BI and Property Damage) and not separately for each injured

claimant.3 Since this analysis requires data at the claim exposure level, Total BI data is

used. It follows that the resulting estimates of incurred loss and ALAE must be allocated

between Basic and Optional components. Therefore, to determine the Basic incurred loss

and ALAE by fiscal loss year, the Optional BI incurred loss and ALAE amounts estimated

in the August 2018 reserve analysis are subtracted from the Total BI incurred loss and

ALAE amounts estimated in this BI Segmented Analysis. The calculated BI Basic incurred

loss and ALAE amounts for each fiscal loss year from 2002 to 2018 are shown in

Exhibit 1.1.

3 See Paragraph 75 in Technical Appendix C.0, Chapter 3 of ICBC’s 2019 Revenue Requirement Application.

Page 8 of 15

9. The following describes the Total BI analysis, which is performed at the segmented level,

based on the claims closure model proposed by Adler and Kline.4 Exhibit sets 3 to 5

provide the calculations of the analysis for the Unrepresented, Represented excluding

Large and Catastrophic, and Represented Large and Catastrophic segments, respectively.

Unless noted otherwise, the analyses for each segment proceed in the same manner.

10. Within each segment, claim exposure count by FLY is first forecasted to the end of fiscal

year 2019 (i.e., to March 31, 2019), as described in paragraph 17. These forecast claim

exposure counts as of 2019 fiscal year end are then projected to their incurred values

based on historical development patterns.

11. The future closure pattern for CWA claim exposures is estimated for each segment based

on historical disposal rates, which is the ratio of the change in CWA claim exposures during

a period to the number of outstanding claim exposures at the beginning of the period.

12. The average paid loss and ALAE per CWA claim exposure (CWA severity) by FLY for each

segment is forecasted for the full 2019 fiscal year, as described in paragraph 17. CWA

severities for future fiscal years are projected at each development period based on a

historical trend rate, applied to a selected starting point (in most cases, the average of

the 2016 to 2019 fiscal years trended to the 2019 level). The future paid loss and ALAE

amounts are derived by multiplying the future CWA claim exposure counts with the

projected CWA severities in each development period. The estimated incurred loss and

ALAE for each fiscal loss year is the sum of the actual past and projected future paid loss

and ALAE amounts.

13. For Unrepresented and Represented excluding Large and Catastrophic, the baseline

selection for the claim exposure count development factors is the average of the four most

recent loss development factors, and the baseline selection for the CWA disposal rates

used for CWA exposure count closure pattern is the average of the four most recent

disposal rates. For Represented Large and Catastrophic, the baseline selection for the

claim exposure count development factors is the average of the six most recent loss

development factors, and the baseline selection for the CWA disposal rates used for CWA

claim exposure count closure pattern is the average of the six most recent disposal rates.

Final selections and departures from the baseline in the analysis are discussed below.

4 Martin Adler and Charles D. Kline Jr., Evaluating Bodily Injury Liabilities Using a Claims Closure Model, accessed August 13, 2014, http://www.casact.org/pubs/dpp/dpp88/88dpp001.pdf

Page 9 of 15

D. DATA SOURCES AND DEFINITIONS

14. Data Sources – BI loss and ALAE amounts (including paid loss and ALAE, case reserves,

and recovered amounts) and claim exposure count data are extracted from the Enterprise

Data Warehouse (for both the legacy and the new claims management systems),

organized into an appropriate format, combined, and downloaded into spreadsheets. The

data is gross of reinsurance recoveries. In the current analysis, the data source for the

legal representation status for claim exposures managed in the new claims management

system was updated. The new data source identifies the represented status at a claimant

level, as opposed to a claim exposure level, which provides greater accuracy than the old

data source. As a result of this change, the new claims management system portion of

the actuarial data triangles (FLYs 2014 and later) has been restated and differs from the

data used in the May 2017 analysis.

15. Data extracted as of August 31, 2018 is projected to March 31, 2019 as described in the

section below, and then combined with data extracted as of fiscal year-end points from

2006 to 2018.

16. The loss and ALAE data used in this analysis are verified to be consistent with other

financial records of ICBC through comparison with the actuarial loss reserving data, which

are reconciled with accounting records, as discussed in Technical Appendix C.0, Section H

of the 2019 Revenue Requirements Application.

17. Fiscal Year 2019 Expected Count and CWA Severity – Data shown in the exhibits as

of March 31, 2019 was derived based on data to August 31, 2018 and a prior expectation

of counts and payments over the course of the 2019 fiscal year, taking into consideration

relevant information from consultation with internal subject matter experts. The prior

expected values used in projecting the count and CWA severities to March 31, 2019 are

from the results of a corresponding segmented analysis as of March 31, 2018.

18. Segment Definitions – As discussed in Section A, the BI claims data are separated into

three segments. In order to achieve this, the claims data are first separated into

unrepresented and represented using the legal representation status of each claim

exposure at each point in time. Within the represented data, the claim exposures that

have either a case incurred amount greater than $200,000, or an injury results code of

010, 011, 012, 013, 020, 030, 040, 050, 051, 060, 070, 080, 090, 121, 122, 123, 130,

140, 190, or 225 and a case incurred amount greater than $10,000, are assigned to the

Page 10 of 15

Represented Large and Catastrophic segment.5 Injury result information is not recorded

in the same way in the new claims management system, and so this criteria is not applied

(only claim exposures with a case incurred amount greater than $200,000 are assigned

to the Represented Large and Catastrophic segment).6

E. SUMMARY OF TOTAL INCURRED COUNT SELECTIONS

19. Exhibit 2.1 – Incurred Claim Exposure Count Summary by Segment – This exhibit

summarizes the final selected incurred claim exposure count for each segment, and in

total, as well as calculating a representation rate (including Large and Catastrophic) for

each FLY. The representation rate is also shown in the 2019 Revenue Requirements

Application, Appendix D.0, Figure D.0.9.

20. Exhibit 2.2 – Incurred Claim Exposure Count Summary – The selected incurred claim

exposure counts are from the Development Method for FLYs 2018 and prior. The

Bornhuetter-Ferguson Method is selected for FLY 2019. This represents a change from

the May 2017 analysis where the incurred claim exposure counts for the latest two FLYs

(2017 and 2018) were calculated as the product of the FLY 2016 claim exposure to claim

ratio and the corresponding incurred claim count estimates. This calculation is no longer

required in the August 2018 analysis because the claim exposure to claim ratio for FLYs

2018 and 2019 are consistent with older FLYs.

21. Exhibit 2.3-2.4 – Incurred Claim Exposure Count Development Method and

Bornhuetter-Ferguson Method – The baseline is selected up to 168 months and a factor

of one is selected from 168 months, except for the period from 12 to 24 months where an

average of the three most recent factors is selected in order to reflect the increased level

of late reporting for BI claim exposures.

F. SUMMARY OF UNREPRESENTED BI SELECTIONS

22. Exhibit 3.1 – Incurred Summary – This exhibit summarizes the final selected incurred

claim exposure counts and incurred loss and ALAE amounts.

23. Exhibit 3.2 – Incurred Claim Exposure Count Summary – The selected incurred claim

exposure counts are from the Development Method for FLYs 2002 to 2018. For FLY 2019,

5 Injury results codes are listed in the CL314 code chart (http://icbcwebapps/corpforms/formspdf/CL314.pdf) and the data is available through the Claim Customer System (CCUS). 6 In recent years, over 95% of the claim exposures in the Large and Catastrophic segment have a case incurred amount greater than $200,000.

Page 11 of 15

the selected incurred claim exposure count is based on the total incurred claim exposure

count and a weighted average of the trended 2019 unrepresented claim exposure ratio

(five twelfths weight) and a prior expected unrepresented claim exposure ratio (seven

twelfths weight). The prior expected unrepresented claim exposure ratio is from the

results of a corresponding segmented analysis as of March 31, 2018. The weighted

average represents a balance between the prior expected unrepresented claim exposure

ratio and the trended unrepresented ratio that includes the five months of data that has

emerged since March 2018. This selection represents a change from the May 2017

analysis where the latest two FLYs (2017 and 2018) were calculated from the total incurred

claim exposure count excluding Represented Large and Catastrophic and estimates of the

unrepresented claim exposure ratio to total incurred claim exposure count excluding

represented large and catastrophic. The ratio has been simplified by the inclusion of

represented large and catastrophic claims, and FLY 2018 incurred claim exposure count

no longer relies on a trended ratio because the result from the Development Method is

reasonably consistent with the trended ratio.

24. Exhibit 3.3-3.4 – Incurred Claim Exposure Count Development Method – The

baseline is selected up to 168 months, and a factor of one is selected from 168 months

onward, except for the period from 12 to 24 months where an average of the three most

recent factors is selected in order to reflect the increased level of late reporting for BI

claim exposures.

25. Exhibit 3.5-3.6 – CWA Claim Exposure Count Closure Pattern – The average of the

three most recent disposal rates is selected up to 36 months and the baseline is selected

from 36 to 96 months. This represents a change from the May 2017 analysis where the

average of the two most recent disposal rates was selected from 12 to 96 months.

Baseline factors are now selected for the periods beyond 36 months because heightened

closure rates are no longer evident in these periods. A disposal rate of 33% is selected

from 96 to 204 months, and a disposal rate of 100% is selected from 204 to 216 months.

26. Exhibit 3.7 – Paid Loss and ALAE Development – Paid loss and ALAE amounts are

projected to their incurred values by multiplying the future incremental CWA claim

exposure counts in Exhibit 3.5 (2) by the forecasted incremental paid severities in

Exhibit 3.8 (1).

27. Exhibit 3.8 – Incremental Paid Severities – The forecasted incremental paid severities

are based on the trend in Exhibit 3.10, row (a), beginning from the selected starting points

shown in Exhibit 3.9, row (a).

Page 12 of 15

28. Exhibit 3.9 – Incremental Paid Severity Starting Points – The four most recent

points are trended to the current period, and the average of those trended points is

selected for all periods. This represents a change from the May 2017 analysis where the

latest point was selected for all periods. A trended average is selected in the current

analysis to provide greater stability to the severity starting points.

29. Exhibit 3.10 – Fiscal Year Paid Severity Trend – The selected incremental paid

severity trend for all development periods is based on an exponential trend of the fiscal

year paid severity over fiscal years 2015 to 2019. This represents a change from the May

2017 analysis where the five year exponential model did not include the current year. The

current fiscal year is included in the current analysis to be more responsive to the most

recent experience, and because it now includes more actual data (5 months) as compared

the May 2017 analysis (2 months).

G. SUMMARY OF REPRESENTED EXCLUDING LARGE AND

CATASTROPHIC BI SELECTIONS

30. Exhibit 4.1 – Incurred Summary – This exhibit summarizes the final selected incurred

claim exposure counts and incurred loss and ALAE amounts.

31. Exhibit 4.2-4.3 – CWA Claim Exposure Count Closure Pattern – The average of the

three most recent disposal rates is selected up to 36 months and then baseline is selected

from 36 to 144 months. This represents a change from the May 2017 analysis where the

average of the two most recent disposal rates was selected up to 120 months. Baseline

factors are now selected for the periods beyond 36 months because heightened closure

rates are no longer evident in these periods. A disposal rate of 33% is selected from 144

to 204 months, and a disposal rate of 100% is selected from 204 to 216 months.

32. Exhibit 4.4 – Paid Loss and ALAE Development – Paid loss and ALAE amounts are

projected to their incurred values by multiplying the future incremental CWA claim

exposure counts in Exhibit 4.2 (2) by the forecasted incremental paid severities in

Exhibit 4.5 (1).

33. Exhibit 4.5 – Incremental Paid Severity – The forecasted incremental paid severities

are based on selected trends beginning from selected starting points. The trends for the

12 to 24 month period, and the periods beyond 24 months are from Exhibit 4.7, row (a)

and Exhibit 4.8, row (a) respectively, and the selected starting points are shown in

Exhibit 4.6, row (a).

Page 13 of 15

34. Exhibit 4.6 – Incremental Paid Severity Starting Points – The four most recent

points are trended to the current period, and the average of those points is selected for

all periods. This represents a change from the May 2017 analysis where the latest point

was selected for all periods. A trended average is selected in the current analysis to

provide greater stability to the severity starting points.

35. Exhibit 4.7 – Fiscal Year Paid Severity Trend (0 to 24 months) – The selected

incremental paid severity trend for the periods up to 24 months is based on an exponential

trend of the fiscal year paid severity over fiscal years 2010 to 2019. This represents a

change from the May 2017 analysis where the ten year exponential model did not include

the current year. The current fiscal year is included in the current analysis to be more

responsive to the most recent experience, and because it now includes more actual data

(5 months) as compared to the May 2017 analysis (2 months).

36. Exhibit 4.8 – Fiscal Year Paid Severity Trend (24 months and later) – The selected

incremental paid severity trend for the periods from 24 and later is based on an

exponential trend of the fiscal year paid severity over fiscal years 2010 to 2019. This

represents a change from the May 2017 analysis where the ten year exponential model

did not include the current year. The current fiscal year is included in the current analysis

to be more responsive to the most recent experience, and because it now includes more

actual data (5 months) as compared to the May 2017 analysis (2 months).

37. Exhibit 4.9 – Open Claim Exposure Count – This exhibit shows open claim exposures

by fiscal loss year and development year. These values are used in the calculation of the

Hindsight Method estimated incurred claim exposure count for the Represented Large and

Catastrophic segment.

H. SUMMARY OF REPRESENTED LARGE AND CATASTROPHIC BI

SELECTIONS

38. Exhibit 5.1 – Incurred Summary – This exhibit summarizes the final selected incurred

claim exposure counts and incurred loss and ALAE amounts.

39. Exhibit 5.2 – Incurred Claim Exposure Count Summary - The selected incurred claim

exposure counts are from the Development Method for FLYs 2002 to 2014, the Hindsight

Method for FLYs 2015, 2016, and 2018, and the average of the Hindsight Method and the

Bornhuetter-Ferguson Method for FLY 2017. For FLY 2019, the selected incurred claim

exposure count is an average of the Hindsight Method result and a prior expected value.

Page 14 of 15

This represents a change from the May 2017 analysis where the results of the Bornhuetter-

Ferguson method was selected for the most recent six FLYs (2013 to 2018). The Hindsight

Method has been introduced in the current analysis in order to be more responsive to the

growing volume of pending represented claims from each individual fiscal loss year, from

which a greater number of large and catastrophic claims have been identified.

40. Exhibit 5.3-5.4 – Incurred Claim Exposure Count Development Method and

Bornhuetter-Ferguson Method – An average of all factors is selected up to 168 months

and a factor of one is selected from 168 months onward. This represents a change from

the May 2017 analysis where the average of the three most recent factors was selected

from 12 to 120 months and then baseline (average six) was selected from 120 to 168

months. The current selection of the average of all factors puts less weight on the factors

in the latest two diagonals, which are relatively high. This is done to recognize that efforts

made to improve the identification of large losses have been resulting in a greater

emergence of claims in this segment, but this effect is not expected to continue

indefinitely. The credibility complement in the Bornhuetter-Ferguson Method is the

product of risk exposure and the results of an exponential trend line on historical incurred

frequencies (FLYs 2002 to 2011). This represents a change from the May 2017 analysis

where the exponential trend line was based on FLYs 2001 to 2012 historical incurred

frequencies. The FLY 2012 frequency is excluded from the exponential trend line in the

current analysis because it has been impacted by increased emergence during fiscal year

2018 and therefore is still subject to significant uncertainty. FLY 2002 is the earliest year

available in the current analysis.

41. Exhibit 5.5-5.7 – Incurred Claim Exposure Count Hindsight Method – The Hindsight

Method restates open claim exposure count in the latest diagonal based on expected ratios

of open represented large and catastrophic claim exposures to open represented claim

exposures for each development period. The expected ratios are selected from a historical

period where the ratios are relatively stable, that period being fiscal years 2006 to 2009.

This can be seen from examination of Exhibit 5.7. After restating the latest diagonal of

represented large and catastrophic open claim exposure counts, represented large and

catastrophic CWA claim exposure counts are added back at each development period. The

open and CWA claim exposure count triangle is then developed using selected count

development factors that align with the historical period selected for the expected ratio

calculation. The open and CWA claim exposure count triangle with the restated latest

diagonal is shown in Exhibit 5.6 (1) and the resulting count development factors are shown

Page 15 of 15

in the bottom half of Exhibit 5.6. After 108 months, baseline count development factors

are selected.

42. Exhibit 5.8-5.9 – CWA Claim Exposure Count Closure Pattern – The average of the

two most recent disposal rates is selected up to 96 months. This represents a change

from the May 2017 analysis where the average of the four most recent disposal rates was

selected up to 96 months. A shorter-term average is selected in the current analysis to

reflect the recent closure levels that have emerged and are expected to continue. A

disposal rate of 33% is selected from 96 to 204 months and a disposal rate of 100% is

selected from 204 to 216 months.

43. Exhibit 5.10 – Paid Loss and ALAE Development – Paid loss and ALAE amounts are

projected to their incurred values by multiplying the future incremental CWA claim

exposure counts in Exhibit 5.8 (2) by the forecasted incremental paid severities in

Exhibit 5.11 (1).

44. Exhibit 5.11 – Incremental Paid Severities - The forecasted incremental paid

severities are based on the trend in Exhibit 5.13, row (a), beginning from the selected

starting points shown in Exhibit 5.12, row (a).

45. Exhibit 5.12 – Incremental Paid Severity Starting Points – The average of the six

most recent points is selected for all periods. This represents a change from the May 2017

analysis where the latest point was selected from 12 to 72 months and the average of the

four most recent points was selected from 72 months onward. A longer average is

selected in the current analysis to provide greater stability to the severity starting points.

46. Exhibit 5.13 – Fiscal Year Paid Severity Trend – The selected incremental paid

severity trend for all development periods is based on an exponential trend of the fiscal

year paid severity over fiscal years 2010 to 2019. This represents a change from the May

2017 analysis where the ten year exponential model did not include the current year. The

current fiscal year is included in the current analysis to be more responsive to the most

recent experience, and because it now includes more actual data (5 months) as compared

to the May 2017 analysis (2 months).

Insurance Corporation of British Columbia Table of Contents

Exhibit Set 1 Bodily Injury Liability Loss* and ALAE Summary and Allocation

1.1 Incurred Loss and ALAE Summary

1.2 Incurred Loss and ALAE Summary by Segment

Exhibit Set 2 Total Bodily Injury Liability Incurred Count

2.1 Incurred Claim Exposure Count Summary by Segment

2.2 Incurred Claim Exposure Count Summary

2.3 - 2.4 Incurred Claim Exposure Count Development Method and Bornhuetter-Ferguson Method

Exhibit Set 3 Unrepresented Bodily Injury Liability

3.1 Summary of Incurred Estimates

3.2 Incurred Claim Exposure Count Summary

3.3 - 3.4 Incurred Claim Exposure Count Development Method

3.5 CWA Claim Exposure Count Closure Pattern

3.6 CWA Disposal Rate

3.7 Paid Loss and ALAE Development

3.8 Incremental Paid Severities

3.9 Incremental Paid Severity Starting Points

3.10 Fiscal Year Paid Severity Trend

Exhibit Set 4 Represented Excluding Large and Catastrophic Bodily Injury Liability

4.1 Summary of Incurred Estimates

4.2 CWA Claim Exposure Count Closure Pattern

4.3 CWA Disposal Rate

4.4 Paid Loss and ALAE Development

4.5 Incremental Paid Severities

4.6 Incremental Paid Severity Starting Points

4.7 Fiscal Year Paid Severity Trend (0 to 24 months)

4.8 Fiscal Year Paid Severity Trend (24 months and later)

4.9 Open Claim Exposure Count

Exhibit Set 5 Represented Large and Catastrophic Bodily Injury Liability

5.1 Summary of Incurred Estimates

5.2 Incurred Claim Exposure Count Summary

5.3 Incurred Claim Exposure Count Development Method and Bornhuetter-Ferguson Method

5.4 Incurred Claim Exposure Count Development Method

5.5 - 5.7 Incurred Claim Exposure Count Hindsight Method

5.8 CWA Claim Exposure Count Closure Pattern

5.9 CWA Disposal Rate

5.10 Paid Loss and ALAE Development

5.11 Incremental Paid Severities

5.12 Incremental Paid Severity Starting Points

5.13 Fiscal Year Paid Severity Trend

* All loss amounts shown in the exhibits of the Injury Segment Analysis are gross of reinsurance, but net of all other recoveries

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 1.1

Bodily Injury Liability Loss and ALAE Summary and Allocation

Incurred Loss and ALAE Summary ($000's)

Up to March 31, 2019

(1) (2) (3)

(2) - (1)

Fiscal Loss

Year

Total Optional

Incurred Loss

and ALAE

from 2018

August

Reserve

Analysis

Total Incurred

Loss and

ALAE

Basic

Incurred Loss

and ALAE

2002 859,244

2003 885,134

2004 961,487

2005 1,017,810

2006 1,096,458

2007 1,099,532

2008 1,139,871

2009 1,172,359

2010 1,220,898

2011 1,372,330

2012 1,415,068

2013 1,562,194

2014 1,739,617

2015 1,932,069

2016 2,129,672

2017 2,238,578

2018 2,623,340

Total 24,465,662

(1) From ICBC's analysis of Optional Bodily Injury claims reserves as of August 31, 2018

(2) From Exhibit 1.2 Col. (4)

(3) These estimated Basic incurred loss and ALAE amounts are also provided in

Technical Appendix C.1.5.3 Col. (1) of the 2019 Revenue Requirements Application

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 1.2

Bodily Injury Liability Loss and ALAE Summary and Allocation

Incurred Loss and ALAE Summary by Segment ($000's)

Up to March 31, 2019

(1) (2) (3) (4)

(1) + (2) + (3)

Fiscal Loss

Year Unrepresented

Represented

excluding

Large and

Catastrophic

Represented

Large and

Catastrophic Total

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Total

(1) From Exhibit 3.1 Col. (2)

(2) From Exhibit 4.1 Col. (2)

(3) From Exhibit 5.1 Col. (2)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 2.1

Total Bodily Injury Liability Incurred Count

Incurred Claim Exposure Count Summary by Segment

Up to March 31, 2019

(1) (2) (3) (4) (5)

(4) - (1) - (3) [(2) + (3)] ÷ (4)

Fiscal Loss

Year Unrepresented

Represented

excluding

Large and

Catastrophic

Represented

Large and

Catastrophic Total

Rep Rate

(including

Large and

Catastrophic)

2002 29,734 17,012 885 47,631 37.6%

2003 27,242 16,202 938 44,382 38.6%

2004 27,722 16,743 1,005 45,470 39.0%

2005 26,702 16,649 1,073 44,424 39.9%

2006 26,969 17,385 1,157 45,511 40.7%

2007 26,227 17,293 1,165 44,685 41.3%

2008 25,137 17,489 1,278 43,903 42.7%

2009 23,152 17,257 1,388 41,797 44.6%

2010 21,965 18,280 1,403 41,648 47.3%

2011 24,325 19,720 1,585 45,630 46.7%

2012 22,871 21,393 1,586 45,851 50.1%

2013 22,245 22,803 1,842 46,889 52.6%

2014 22,697 23,670 2,102 48,469 53.2%

2015 24,647 26,295 2,219 53,160 53.6%

2016 26,708 30,266 2,199 59,173 54.9%

2017 27,731 31,969 2,281 61,981 55.3%

2018 28,266 35,218 2,603 66,086 57.2%

2019 28,009 36,290 2,918 67,217 58.3%

Total 462,348 401,934 29,627 893,909

(a) Trend 1.4%

(1) From Exhibit 3.1 Col. (1)

(3) From Exhibit 5.1 Col. (1)

(4) From Exhibit 2.2 Col. (3)

(a) Linear trend of (5) over fiscal loss years 2008 to 2017

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 2.2

Total Bodily Injury Liability Incurred Count

Incurred Claim Exposure Count Summary

Up to March 31, 2019

(1) (2) (3)

Fiscal Loss

Year

Development

Method

Bornhuetter-

Ferguson

Method

Selected

Incurred Claim

Exposure

Count

2002 47,631 47,631 47,631

2003 44,382 44,382 44,382

2004 45,470 45,470 45,470

2005 44,424 44,424 44,424

2006 45,511 45,511 45,511

2007 44,685 44,685 44,685

2008 43,903 43,903 43,903

2009 41,797 41,797 41,797

2010 41,648 41,648 41,648

2011 45,630 45,630 45,630

2012 45,851 45,851 45,851

2013 46,889 46,889 46,889

2014 48,469 48,471 48,469

2015 53,160 53,160 53,160

2016 59,173 59,163 59,173

2017 61,981 61,982 61,981

2018 66,086 66,110 66,086

2019 66,576 67,217 67,217

Total 893,268 893,925 893,909

(1) From Exhibit 2.3 Col. (4)

(2) From Exhibit 2.3 Col. (9)

(3) = Col. (1) for fiscal loss years 2002 to 2018

= Col. (2) for fiscal loss year 2019

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 2.3

Total Bodily Injury Liability Incurred Count

Incurred Claim Exposure Count Development Method and Bornhuetter-Ferguson Method

Up to March 31, 2019

(1) (2) (3) (4) (5) (6) (7) (8) (9)

(1) x (3) (4) ÷ (5) 1 - 1 ÷ (3)

Fiscal Loss

Year

Open and

CWA* Claim

Exposure

Count

Age-to-

Age CDF**

Age-to-

Ultimate

CDF

Incurred

Claim

Exposure

Count

Risk

Exposure

Indicated

Incurred

Frequency

Trended

Incurred

Frequency

Percentage

Unreported

Count

Incurred Claim

Exposure

Count

(Bornhuetter-

Ferguson

Method)

2002 47,631 1.0000 1.0000 47,631 2,363,098 2.016% 0.00% 47,631

2003 44,382 1.0000 1.0000 44,382 2,397,249 1.851% 0.00% 44,382

2004 45,470 1.0000 1.0000 45,470 2,438,711 1.865% 0.00% 45,470

2005 44,424 1.0000 1.0000 44,424 2,497,756 1.779% 0.00% 44,424

2006 45,511 1.0000 1.0000 45,511 2,562,601 1.776% 0.00% 45,511

2007 44,677 1.0002 1.0002 44,685 2,634,785 1.696% 0.02% 44,685

2008 43,883 1.0003 1.0005 43,903 2,709,074 1.621% 0.05% 43,903

2009 41,770 1.0002 1.0007 41,797 2,760,413 1.514% 0.07% 41,797

2010 41,606 1.0004 1.0010 41,648 2,785,866 1.495% 0.10% 41,648

2011 45,569 1.0003 1.0014 45,630 2,827,554 1.614% 0.14% 45,630

2012 45,774 1.0003 1.0017 45,851 2,862,519 1.602% 0.17% 45,851

2013 46,788 1.0005 1.0022 46,889 2,902,524 1.615% 0.22% 46,889

2014 48,341 1.0005 1.0026 48,469 2,950,153 1.643% 1.672% 0.26% 48,471

2015 52,999 1.0004 1.0030 53,160 3,008,066 1.767% 1.762% 0.30% 53,160

2016 58,826 1.0029 1.0059 59,173 3,091,385 1.914% 1.857% 0.59% 59,163

2017 61,316 1.0049 1.0108 61,981 3,169,735 1.955% 1.957% 1.07% 61,982

2018 64,521 1.0133 1.0243 66,086 3,252,816 2.032% 2.063% 2.37% 66,110

2019 58,877 1.1040 1.1308 66,576 3,317,036 2.007% 2.174% 11.56% 67,217

Total 882,364 893,268 893,925

* CWA = Completed With Amount

** CDF = Count Development Factor

(1) From Exhibit 2.4

(2) From Exhibit 2.4

(3) From Exhibit 2.4

(5) From internal ICBC database; estimated for fiscal loss year 2019

(7) Exponential trend of (6) over fiscal loss years 2014 to 2018

(9) = (4) for fiscal loss years 2002 to 2013

= (1) + (5) x (7) x (8) for fiscal loss years 2014 to 2019

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 2.4

Total Bodily Injury Liability Incurred Count

Incurred Claim Exposure Count Development Method

(1) Open and CWA Claim Exposure Count

Fiscal Loss Year 12 24 36 48 60 72 84 96 108 120 132 144 156 168 180 192 204 216

2002 47,533 47,537 47,559 47,553 47,555 47,575 47,580 47,591 47,599 47,611 47,618 47,625 47,629 47,631

2003 44,283 44,337 44,330 44,307 44,314 44,327 44,339 44,352 44,361 44,366 44,372 44,376 44,380 44,382

2004 45,351 45,376 45,375 45,395 45,392 45,404 45,418 45,416 45,426 45,435 45,449 45,460 45,470 45,470

2005 43,833 44,200 44,271 44,308 44,315 44,334 44,345 44,356 44,374 44,392 44,401 44,411 44,419 44,424

2006 44,302 44,897 45,362 45,442 45,435 45,440 45,441 45,444 45,463 45,479 45,487 45,493 45,501 45,511

2007 42,674 43,932 44,448 44,550 44,559 44,562 44,580 44,593 44,616 44,634 44,655 44,662 44,677

2008 41,325 43,187 43,615 43,806 43,801 43,791 43,805 43,833 43,848 43,855 43,870 43,883

2009 39,955 41,101 41,551 41,661 41,676 41,687 41,723 41,730 41,736 41,750 41,770

2010 39,464 40,982 41,486 41,531 41,538 41,559 41,563 41,583 41,588 41,606

2011 43,279 44,799 45,321 45,372 45,477 45,492 45,525 45,538 45,569

2012 43,651 44,989 45,484 45,669 45,706 45,717 45,726 45,774

2013 43,215 45,792 46,496 46,658 46,743 46,747 46,788

2014 44,489 47,316 47,926 48,055 48,296 48,341

2015 48,084 51,857 52,493 52,799 52,999

2016 51,754 57,562 58,381 58,826

2017 55,029 60,489 61,316

2018 58,628 64,521

2019 58,877

Development Factors

Fiscal Loss Year 12 to 24 24 to 36 36 to 48 48 to 60 60 to 72 72 to 84 84 to 96 96 to 108 108 to 120 120 to 132 132 to 144 144 to 156 156 to 168 168 to 180 180 to 192 192 to 204 204 to 216

2002 1.0001 1.0005 0.9999 1.0000 1.0004 1.0001 1.0002 1.0002 1.0003 1.0001 1.0001 1.0001 1.0000

2003 1.0012 0.9998 0.9995 1.0002 1.0003 1.0003 1.0003 1.0002 1.0001 1.0001 1.0001 1.0001 1.0000

2004 1.0006 1.0000 1.0004 0.9999 1.0003 1.0003 1.0000 1.0002 1.0002 1.0003 1.0002 1.0002 1.0000

2005 1.0084 1.0016 1.0008 1.0002 1.0004 1.0002 1.0002 1.0004 1.0004 1.0002 1.0002 1.0002 1.0001

2006 1.0134 1.0104 1.0018 0.9998 1.0001 1.0000 1.0001 1.0004 1.0004 1.0002 1.0001 1.0002 1.0002

2007 1.0295 1.0117 1.0023 1.0002 1.0001 1.0004 1.0003 1.0005 1.0004 1.0005 1.0002 1.0003

2008 1.0451 1.0099 1.0044 0.9999 0.9998 1.0003 1.0006 1.0003 1.0002 1.0003 1.0003

2009 1.0287 1.0109 1.0026 1.0004 1.0003 1.0009 1.0002 1.0001 1.0003 1.0005

2010 1.0385 1.0123 1.0011 1.0002 1.0005 1.0001 1.0005 1.0001 1.0004

2011 1.0351 1.0117 1.0011 1.0023 1.0003 1.0007 1.0003 1.0007

2012 1.0307 1.0110 1.0041 1.0008 1.0002 1.0002 1.0011

2013 1.0596 1.0154 1.0035 1.0018 1.0001 1.0009

2014 1.0635 1.0129 1.0027 1.0050 1.0009

2015 1.0785 1.0123 1.0058 1.0038

2016 1.1122 1.0142 1.0076

2017 1.0992 1.0137

2018 1.1005

Baseline Factor

avg 4 1.0976 1.0133 1.0049 1.0029 1.0004 1.0005 1.0005 1.0003 1.0003 1.0004 1.0002 1.0003 1.0002 1.0001 1.0001 1.0001 1.0000

Selected Assumption avg 3 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 one one one one one

Selected Factor 1.1040 1.0133 1.0049 1.0029 1.0004 1.0005 1.0005 1.0003 1.0003 1.0004 1.0002 1.0003 1.0002 1.0000 1.0000 1.0000 1.0000 1.0000

Age-to-Ultimate Factor 1.1308 1.0243 1.0108 1.0059 1.0030 1.0026 1.0022 1.0017 1.0014 1.0010 1.0007 1.0005 1.0002 1.0000 1.0000 1.0000 1.0000 1.0000

(1 shaded area) Based on 2018 August YTD open and CWA claim exposure count, and the expectation for the remainder of the year

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.1

Unrepresented Bodily Injury Liability

Summary of Incurred Estimates

Up to March 31, 2019

(1) (2)

Fiscal Loss Year

Incurred Claim

Exposure

Count

Incurred Loss

and ALAE

($000's)

2002 29,734

2003 27,242

2004 27,722

2005 26,702

2006 26,969

2007 26,227

2008 25,137

2009 23,152

2010 21,965

2011 24,325

2012 22,871

2013 22,245

2014 22,697

2015 24,647

2016 26,708

2017 27,731

2018 28,266

2019 28,009

Total 462,348

Subtotal (2002-2018) 434,339

(1) From Exhibit 3.2 Col. (4)

(2) From Exhibit 3.7 Col. (3)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.2

Unrepresented Bodily Injury Liability

Incurred Claim Exposure Count Summary

Up to March 31, 2019

(1) (2) (3) (4)

Fiscal Loss

Year

Development

Method

Indicated

Unrepresented

Claim

Exposure Ratio

Trended

Unrepresented

Claim

Exposure Ratio

Selected

Incurred Claim

Exposure

Count

2002 29,734 62.4% 29,734

2003 27,242 61.4% 27,242

2004 27,722 61.0% 27,722

2005 26,702 60.1% 26,702

2006 26,969 59.3% 26,969

2007 26,227 58.7% 26,227

2008 25,137 57.3% 25,137

2009 23,152 55.4% 54.5% 23,152

2010 21,965 52.7% 53.2% 21,965

2011 24,325 53.3% 51.8% 24,325

2012 22,871 49.9% 50.5% 22,871

2013 22,245 47.4% 49.1% 22,245

2014 22,697 46.8% 47.8% 22,697

2015 24,647 46.4% 46.4% 24,647

2016 26,708 45.1% 45.1% 26,708

2017 27,731 44.7% 43.8% 27,731

2018 28,266 42.8% 42.4% 28,266

2019 26,158 39.3% 41.1% 28,009

Total 460,497 462,348

(1) From Exhibit 3.3 Col. (4)

(2) = (1) / Exhibit 2.2 Col. (1)

(3) = Linear trend of (2) over fiscal loss years 2009 to 2018

(4) = (1) for fiscal loss years 2002 to 2018

= Exhibit 2.2 Col. (3) x [(3) x (5 ÷ 12) + 42.1% x (7 ÷ 12)] for FLY 2019

where 42.1% is the prior expected value

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.3

Unrepresented Bodily Injury Liability

Incurred Claim Exposure Count Development Method

Up to March 31, 2019

(1) (2) (3) (4)

(1) x (3)

Fiscal Loss

Year

Open and CWA

Claim

Exposure

Count

Age-to-Age

CDF

Age-to-Ultimate

CDF

Incurred Claim

Exposure

Count

2002 29,734 1.0000 1.0000 29,734

2003 27,242 1.0000 1.0000 27,242

2004 27,722 1.0000 1.0000 27,722

2005 26,702 1.0000 1.0000 26,702

2006 26,969 1.0000 1.0000 26,969

2007 26,225 1.0001 1.0001 26,227

2008 25,133 1.0001 1.0001 25,137

2009 23,149 1.0000 1.0001 23,152

2010 21,959 1.0001 1.0003 21,965

2011 24,315 1.0001 1.0004 24,325

2012 22,855 1.0003 1.0007 22,871

2013 22,224 1.0002 1.0009 22,245

2014 22,666 1.0004 1.0014 22,697

2015 24,603 1.0004 1.0018 24,647

2016 26,661 1.0000 1.0018 26,708

2017 27,756 0.9973 0.9991 27,731

2018 29,842 0.9480 0.9472 28,266

2019 29,657 0.9312 0.8820 26,158

Total 465,414 460,497

(1) From Exhibit 3.4

(2) From Exhibit 3.4

(3) From Exhibit 3.4

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.4

Unrepresented Bodily Injury Liability

Incurred Claim Exposure Count Development Method

(1) Open and CWA Claim Exposure Count

Fiscal Loss Year 12 24 36 48 60 72 84 96 108 120 132 144 156 168 180 192 204 216

2002 29,787 29,748 29,744 29,735 29,735 29,735 29,730 29,732 29,733 29,735 29,736 29,734 29,734 29,734

2003 27,335 27,278 27,254 27,245 27,243 27,238 27,242 27,239 27,243 27,237 27,239 27,239 27,242 27,242

2004 28,064 27,829 27,756 27,736 27,731 27,724 27,724 27,713 27,714 27,712 27,713 27,715 27,722 27,722

2005 28,366 26,942 26,737 26,737 26,714 26,713 26,710 26,703 26,698 26,700 26,701 26,701 26,702 26,702

2006 32,422 28,408 27,276 27,115 27,039 27,018 27,004 26,972 26,959 26,961 26,961 26,964 26,967 26,969

2007 30,665 27,509 26,527 26,351 26,307 26,292 26,243 26,238 26,232 26,223 26,227 26,222 26,225

2008 29,016 26,443 25,332 25,231 25,202 25,144 25,133 25,119 25,124 25,128 25,131 25,133

2009 27,438 24,319 23,331 23,248 23,162 23,154 23,142 23,141 23,137 23,142 23,149

2010 25,807 23,112 22,188 22,036 21,960 21,935 21,928 21,935 21,949 21,959

2011 28,419 25,811 24,508 24,323 24,274 24,286 24,304 24,300 24,315

2012 27,834 24,235 22,911 22,842 22,831 22,833 22,839 22,855

2013 25,882 23,335 22,305 22,184 22,190 22,200 22,224

2014 26,845 24,008 22,661 22,643 22,652 22,666

2015 29,063 26,059 24,678 24,608 24,603

2016 30,355 28,112 26,704 26,661

2017 31,383 29,177 27,756

2018 31,823 29,842

2019 29,657

Development Factors

Fiscal Loss Year 12 to 24 24 to 36 36 to 48 48 to 60 60 to 72 72 to 84 84 to 96 96 to 108 108 to 120 120 to 132 132 to 144 144 to 156 156 to 168 168 to 180 180 to 192 192 to 204 204 to 216

2002 0.9987 0.9999 0.9997 1.0000 1.0000 0.9998 1.0001 1.0000 1.0001 1.0000 0.9999 1.0000 1.0000

2003 0.9979 0.9991 0.9997 0.9999 0.9998 1.0001 0.9999 1.0001 0.9998 1.0001 1.0000 1.0001 1.0000

2004 0.9916 0.9974 0.9993 0.9998 0.9997 1.0000 0.9996 1.0000 0.9999 1.0000 1.0001 1.0003 1.0000

2005 0.9498 0.9924 1.0000 0.9991 1.0000 0.9999 0.9997 0.9998 1.0001 1.0000 1.0000 1.0000 1.0000

2006 0.8762 0.9602 0.9941 0.9972 0.9992 0.9995 0.9988 0.9995 1.0001 1.0000 1.0001 1.0001 1.0001

2007 0.8971 0.9643 0.9934 0.9983 0.9994 0.9981 0.9998 0.9998 0.9997 1.0002 0.9998 1.0001

2008 0.9113 0.9580 0.9960 0.9989 0.9977 0.9996 0.9994 1.0002 1.0002 1.0001 1.0001

2009 0.8863 0.9594 0.9964 0.9963 0.9997 0.9995 1.0000 0.9998 1.0002 1.0003

2010 0.8956 0.9600 0.9931 0.9966 0.9989 0.9997 1.0003 1.0006 1.0005

2011 0.9082 0.9495 0.9925 0.9980 1.0005 1.0007 0.9998 1.0006

2012 0.8707 0.9454 0.9970 0.9995 1.0001 1.0003 1.0007

2013 0.9016 0.9559 0.9946 1.0003 1.0005 1.0011

2014 0.8943 0.9439 0.9992 1.0004 1.0006

2015 0.8966 0.9470 0.9972 0.9998

2016 0.9261 0.9499 0.9984

2017 0.9297 0.9513

2018 0.9377

Baseline Factor

avg 4 0.9226 0.9480 0.9973 1.0000 1.0004 1.0004 1.0002 1.0003 1.0001 1.0001 1.0000 1.0001 1.0001 1.0001 1.0000 1.0000 1.0000

Selected Assumption avg 3 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 avg 4 one one one one one

Selected Factor 0.9312 0.9480 0.9973 1.0000 1.0004 1.0004 1.0002 1.0003 1.0001 1.0001 1.0000 1.0001 1.0001 1.0000 1.0000 1.0000 1.0000 1.0000

Age-to-Ultimate Factor 0.8820 0.9472 0.9991 1.0018 1.0018 1.0014 1.0009 1.0007 1.0004 1.0003 1.0001 1.0001 1.0001 1.0000 1.0000 1.0000 1.0000 1.0000

(1 shaded area) Based on 2018 August YTD open and CWA claim exposure count, and the expectation for the remainder of the year

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.5

Unrepresented Bodily Injury Liability

CWA Claim Exposure Count Closure Pattern

(1) CWA Claim Exposure Count

Fiscal Loss

Year 12 24 36 48 60 72 84 96 108 120 132 144 156 168 180 192 204 216

2001 28,668 28,737 28,784 28,799 28,815 28,826 28,828 28,836 28,840 28,841 28,843 28,844 28,844

2002 29,445 29,590 29,654 29,678 29,698 29,702 29,709 29,722 29,729 29,725 29,730 29,732 29,733 29,733

2003 26,682 26,939 27,050 27,134 27,177 27,200 27,214 27,217 27,226 27,230 27,236 27,237 27,241 27,242 27,242

2004 26,676 27,207 27,442 27,564 27,619 27,644 27,667 27,677 27,687 27,695 27,704 27,710 27,716 27,719 27,720 27,722

2005 22,711 25,822 26,200 26,428 26,513 26,596 26,635 26,664 26,675 26,685 26,694 26,696 26,699 26,699 26,700 26,700 26,702

2006 12,217 23,534 26,176 26,531 26,728 26,831 26,889 26,919 26,920 26,939 26,947 26,956 26,960 26,965 26,966 26,967 26,968 26,969

2007 13,417 23,205 25,416 25,748 25,957 26,086 26,146 26,168 26,186 26,197 26,214 26,219 26,223 26,224 26,225 26,226 26,226 26,227

2008 13,333 22,317 24,531 24,848 24,963 25,019 25,057 25,086 25,106 25,120 25,126 25,128 25,131 25,133 25,134 25,135 25,135 25,137

2009 12,026 20,446 22,565 22,833 22,965 23,029 23,082 23,104 23,115 23,137 23,139 23,144 23,147 23,148 23,150 23,151 23,151 23,152

2010 11,333 19,659 21,430 21,696 21,812 21,875 21,888 21,912 21,935 21,944 21,951 21,956 21,959 21,961 21,963 21,964 21,964 21,965

2011 14,082 21,795 23,811 24,032 24,133 24,200 24,242 24,272 24,279 24,294 24,304 24,311 24,316 24,319 24,321 24,322 24,323 24,325

2012 11,829 19,884 22,364 22,621 22,732 22,773 22,806 22,818 22,836 22,847 22,855 22,861 22,864 22,867 22,868 22,869 22,870 22,871

2013 10,082 19,770 21,772 21,978 22,080 22,144 22,164 22,188 22,207 22,219 22,228 22,233 22,237 22,240 22,241 22,242 22,243 22,245

2014 11,079 19,917 22,168 22,407 22,525 22,574 22,605 22,632 22,654 22,668 22,678 22,684 22,688 22,691 22,693 22,694 22,695 22,697

2015 12,313 21,716 24,295 24,438 24,498 24,547 24,573 24,594 24,612 24,623 24,631 24,636 24,640 24,642 24,644 24,645 24,645 24,647

2016 13,018 23,758 26,286 26,432 26,537 26,594 26,623 26,648 26,668 26,682 26,691 26,697 26,701 26,703 26,705 26,706 26,707 26,708

2017 14,891 25,361 27,439 27,559 27,624 27,660 27,678 27,693 27,706 27,714 27,720 27,724 27,726 27,728 27,729 27,730 27,730 27,731

2018 15,394 25,692 27,934 28,070 28,144 28,184 28,205 28,223 28,237 28,247 28,253 28,257 28,260 28,262 28,263 28,264 28,265 28,266

2019 14,960 25,399 27,673 27,811 27,886 27,927 27,948 27,965 27,980 27,990 27,996 28,000 28,003 28,005 28,006 28,007 28,008 28,009

(2) Incremental CWA Claim Exposure Count

Fiscal Loss

Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2001 69 47 15 16 11 2 8 4 1 2 1 -

2002 145 64 24 20 4 7 13 7 (4) 5 2 1 (0)

2003 257 111 84 43 23 14 3 9 4 6 1 4 1 (0)

2004 531 235 122 55 25 23 10 10 8 9 6 6 3 1 2

2005 3,111 378 228 85 83 39 29 11 10 9 2 3 (0) 1 1 2

2006 12,217 11,317 2,642 355 197 103 58 30 1 19 8 9 4 5 1 1 1 1

2007 13,417 9,788 2,211 332 209 129 60 22 18 11 17 5 4 1 1 1 0 1

2008 13,333 8,984 2,214 317 115 56 38 29 20 14 6 2 3 2 1 1 1 1

2009 12,026 8,420 2,119 268 132 64 53 22 11 22 2 4 3 2 1 1 1 1

2010 11,333 8,326 1,771 266 116 63 13 24 23 9 7 5 3 2 1 1 1 1

2011 14,082 7,713 2,016 221 101 67 42 30 7 15 10 7 4 3 2 1 1 2

2012 11,829 8,055 2,480 257 111 41 33 12 18 12 8 5 4 2 2 1 1 1

2013 10,082 9,688 2,002 206 102 64 20 23 19 13 8 6 4 2 2 1 1 1

2014 11,079 8,838 2,251 239 118 49 31 27 22 14 10 6 4 3 2 1 1 2

2015 12,313 9,403 2,579 143 60 49 25 22 17 12 8 5 3 2 2 1 1 1

2016 13,018 10,740 2,528 146 105 56 29 25 20 13 9 6 4 3 2 1 1 2

2017 14,891 10,470 2,078 120 66 35 18 16 13 8 6 4 2 2 1 1 0 1

2018 15,394 10,298 2,243 136 74 40 21 18 14 10 6 4 3 2 1 1 1 1

2019 14,960 10,439 2,274 138 76 40 21 18 14 10 6 4 3 2 1 1 1 1

(1 shaded area) = (1) prior column + (2)

For example FLY 2016 @ 60 months: 26,537 = 26,432 + 105

(2 lighter shaded area) Based on 2018 August YTD CWA claim exposure count, and the expectation for the remainder of the year

(2 darker shaded area) = Exhibit 3.6 (1) x (Exhibit 3.1 Col. (1) - (1) prior column)

For example FLY 2016 @ 48-60 months: 105 = 38.07% x (26,708 - 26,432)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.6

Unrepresented Bodily Injury Liability

CWA Disposal Rate

(1) CWA Disposal Rate

Fiscal Loss

Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2002 50.17% 44.44% 30.00% 35.71% 11.11% 21.88% 52.00% 58.33% -80.00% 55.56% 50.00% 50.00% -44.94%

2003 45.89% 36.63% 43.75% 39.81% 35.38% 33.33% 10.71% 36.00% 25.00% 50.00% 16.67% 80.00% 118.35% 100.00%

2004 50.76% 45.63% 43.57% 34.81% 24.27% 29.49% 18.18% 22.22% 22.86% 33.33% 33.33% 50.00% 51.69% 33.33% 100.00%

2005 77.95% 42.95% 45.42% 31.02% 43.92% 36.79% 43.28% 28.95% 37.04% 52.94% 25.00% 50.00% -14.98% 33.33% 33.33% 100.00%

2006 45.30% 76.72% 76.92% 44.77% 44.99% 42.76% 42.06% 37.55% 2.00% 38.85% 26.75% 41.09% 31.00% 51.61% 33.33% 33.33% 33.33% 100.00%

2007 51.16% 76.41% 73.16% 40.94% 43.63% 47.77% 42.54% 27.15% 30.49% 26.81% 56.60% 38.35% 46.84% 33.33% 33.33% 33.33% 33.33% 100.00%

2008 53.04% 76.11% 78.52% 52.34% 39.85% 32.26% 32.31% 36.43% 39.52% 45.75% 36.14% 18.78% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2009 51.94% 75.68% 78.30% 45.64% 41.35% 34.18% 43.00% 31.31% 22.79% 59.04% 15.42% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2010 51.59% 78.31% 76.79% 49.68% 43.05% 41.06% 14.38% 31.00% 43.05% 29.87% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2011 57.89% 75.30% 79.70% 43.03% 34.52% 34.98% 33.72% 36.34% 13.70% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2012 51.72% 72.95% 83.02% 50.67% 44.36% 29.45% 33.60% 18.17% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2013 45.32% 79.65% 80.90% 43.58% 38.25% 38.87% 20.24% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2014 48.81% 76.07% 80.98% 45.19% 40.71% 28.50% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2015 49.96% 76.24% 88.00% 40.67% 28.98% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2016 48.74% 78.45% 85.68% 34.47% 38.07% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2017 53.70% 81.54% 87.69% 40.98% 38.07% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2018 54.46% 80.00% 87.12% 40.98% 38.07% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

2019 53.41% 80.00% 87.12% 40.98% 38.07% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

Baseline Factor

Avg 4 79.06% 85.59% 40.98% 38.07% 32.95% 25.48% 29.20% 29.77% 40.37% 33.73% 37.79% 34.04% 46.24% 26.81% 60.56% 84.18% -44.94%

Selected Assumption avg 3 avg 3 avg 4 avg 4 avg 4 avg 4 avg 4 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1/3 judg. 1

(a) Selected Factor 80.00% 87.12% 40.98% 38.07% 32.95% 25.48% 29.20% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 33.33% 100.00%

(1 unshaded area) = Exhibit 3.5 (2) ÷ (Exhibit 3.1 Col. (1) - Exhibit 3.5 (1) prior column)

For example, FLY 2016 @ 12-24 months: 78.45% = 10,740 ÷ (26,708 - 13,018)

(1 shaded area) = (a)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.7

Unrepresented Bodily Injury Liability

Paid Loss and ALAE Development

(1) Paid Loss and ALAE ($000's)

Fiscal Loss

Year 12 24 36 48 60 72 84 96 108 120 132 144 156 168 180 192 204 216

(3) Incurred

Loss and

ALAE ($000's)

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

(2) Incremental Paid Loss and ALAE ($000's)

Fiscal Loss

Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

(1 shaded area) = (1) prior column + (2)

For example FLY 2016 @ 60 months:

(2 shaded area) = Exhibit 3.5 (2) x Exhibit 3.8 (1)

(3) From the last column of (1)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.8

Unrepresented Bodily Injury Liability

Incremental Paid Severities

(1) Incremental Paid Severity per CWA ($)

Fiscal Loss

Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

(1 lighter shaded area) Based on 2018 August YTD paid severities, and the expectation for the remainder of the year

(1 darker shaded area) Based on trend from Exhibit 3.9 Row (b) starting from Exhibit 3.9 Row (a)

Note: Same starting point used from 36 to 216 months

Note: Grey data points on graphs are actual incremental paid severities, and black data points are forecasted incremental paid severities

Fiscal Loss Year

0 - 12 Months

Fiscal Loss Year

36 - 48 Months

Fiscal Loss Year

24 - 36 Months

Fiscal Loss Year

12 - 24 Months

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.9

Unrepresented Bodily Injury Liability

Incremental Paid Severity Starting Points

(1) Incremental Paid Severity per CWA ($)

Fiscal Loss Year 0 - 12 12 - 24 24 - 36 36+

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0 - 12 12 - 24 24 - 36 36+

Selected Assumption avg trended 4* avg trended 4 avg trended 4 avg trended 4

(a) Selected Starting Point

(b) Selected Trend 2.0% 2.0% 2.0% 2.0%

(1) = Exhibit 3.7 (2) ÷ Exhibit 3.5 (2)

Note: 36+ includes up to 108 months for each fiscal loss year, except for 2016 which includes up to 216 months

For example FLY 2014 @ 36+ months:

*: avg trended 4 is calculated as the average of the last 4 years trended to the current year (FY 2019)

For example 12 - 24:

(b) = Exhibit 3.10 Row (a)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 3.10

Unrepresented Bodily Injury Liability

Fiscal Year Paid Severity Trend

Up to March 31, 2019

(1) (2) (3)

(2) ÷ (1)

Fiscal Year

CWA Claim

Exposure

Count

Paid Loss and

ALAE ($000's)

Paid Severity

($)

2010 22,728

2011 25,304

2012 21,968

2013 20,760

2014 23,750

2015 23,712

2016 25,161

2017 28,721

2018 28,854

2019 27,655

(a) Trend 2.0%

(1) Based on Exhibit 3.5 (2) from 12 up to at least 144 months

For example fiscal year 2017 includes up to 204 months: 28,721 = 14,891 + 10,740 + … + 1

(2) Based on Exhibit 3.7 (2) from 12 up to at least 144 months

For example fiscal year 2017 includes up to 204 months:

(a) Exponential trend of (3) over fiscal years 2015 to 2019

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 4.1

Represented Excluding Large and Catastrophic Bodily Injury Liability

Summary of Incurred Estimates

Up to March 31, 2019

(1) (2)

Fiscal Loss Year

Incurred Claim

Exposure

Count

Incurred Loss

and ALAE

($000's)

2002 17,012

2003 16,202

2004 16,743

2005 16,649

2006 17,385

2007 17,293

2008 17,489

2009 17,257

2010 18,280

2011 19,720

2012 21,393

2013 22,803

2014 23,670

2015 26,295

2016 30,266

2017 31,969

2018 35,218

2019 36,290

Total 401,934

Subtotal (2002-2018) 365,644

(1) From Exhibit 2.1 Col. (2)

(2) From Exhibit 4.4 Col. (3)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 4.2

Represented Excluding Large and Catastrophic Bodily Injury Liability

CWA Claim Exposure Count Closure Pattern

(1) CWA Claim Exposure Count

Fiscal Loss

Year 12 24 36 48 60 72 84 96 108 120 132 144 156 168 180 192 204 216

2001 15,761 16,210 16,420 16,494 16,556 16,603 16,637 16,660 16,677 16,695 16,711 16,724 16,734

2002 15,077 16,091 16,506 16,684 16,781 16,836 16,874 16,917 16,944 16,956 16,974 16,982 16,994 17,007

2003 12,365 14,329 15,265 15,637 15,840 15,953 16,014 16,074 16,105 16,127 16,150 16,170 16,175 16,183 16,202

2004 9,370 12,846 14,873 15,822 16,207 16,383 16,457 16,535 16,594 16,635 16,663 16,688 16,701 16,716 16,725 16,743

2005 4,504 9,000 12,647 14,739 15,730 16,140 16,328 16,417 16,483 16,517 16,551 16,581 16,601 16,618 16,629 16,635 16,649

2006 859 4,648 9,416 13,134 15,455 16,457 16,847 17,039 17,160 17,227 17,275 17,304 17,329 17,347 17,360 17,368 17,374 17,385

2007 819 4,795 9,232 13,134 15,449 16,307 16,667 16,829 16,964 17,074 17,137 17,192 17,222 17,246 17,262 17,272 17,279 17,293

2008 917 4,832 9,257 13,405 15,595 16,458 16,849 17,077 17,201 17,308 17,355 17,388 17,422 17,444 17,459 17,469 17,476 17,489

2009 830 4,772 9,387 13,050 15,173 16,169 16,587 16,802 16,942 17,033 17,088 17,135 17,176 17,203 17,221 17,233 17,241 17,257

2010 868 5,105 9,702 13,466 15,948 17,099 17,576 17,847 17,953 18,043 18,108 18,156 18,198 18,225 18,243 18,256 18,264 18,280

2011 1,031 5,014 9,731 13,976 16,908 18,213 18,880 19,142 19,298 19,432 19,511 19,570 19,620 19,654 19,676 19,691 19,701 19,720

2012 819 5,508 11,277 15,625 18,409 19,907 20,480 20,779 20,952 21,092 21,175 21,236 21,288 21,323 21,347 21,362 21,373 21,393

2013 1,042 6,655 12,561 16,599 19,595 21,090 21,816 22,148 22,332 22,481 22,570 22,635 22,691 22,728 22,753 22,770 22,781 22,803

2014 1,182 6,703 12,263 16,991 20,119 21,814 22,582 22,948 23,151 23,316 23,413 23,485 23,547 23,588 23,615 23,633 23,646 23,670

2015 1,005 6,348 13,576 18,572 22,056 24,080 24,996 25,433 25,675 25,872 25,988 26,074 26,147 26,196 26,229 26,251 26,266 26,295

2016 1,137 8,320 16,154 21,069 25,403 27,724 28,776 29,277 29,555 29,781 29,914 30,012 30,097 30,153 30,191 30,216 30,232 30,266

2017 1,557 9,566 16,804 22,680 27,057 29,402 30,464 30,970 31,251 31,479 31,613 31,713 31,798 31,855 31,893 31,919 31,935 31,969

2018 1,989 8,406 17,722 24,501 29,551 32,256 33,482 34,066 34,389 34,653 34,807 34,922 35,021 35,086 35,130 35,159 35,179 35,218

2019 1,668 9,782 18,992 25,694 30,688 33,362 34,574 35,151 35,471 35,731 35,885 35,998 36,095 36,160 36,204 36,232 36,252 36,290

(2) Incremental CWA Claim Exposure Count

Fiscal Loss

Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2001 449 210 74 62 47 34 23 17 18 16 13 10

2002 1,014 415 178 97 55 38 43 27 12 18 8 12 13

2003 1,964 936 372 203 113 61 60 31 22 23 20 5 8 19

2004 3,476 2,027 949 385 176 74 78 59 41 28 25 13 15 9 18

2005 4,496 3,647 2,092 991 410 188 89 66 34 34 30 20 17 10 7 14

2006 859 3,789 4,768 3,718 2,321 1,002 390 192 121 67 48 29 25 18 13 8 6 11

2007 819 3,976 4,437 3,902 2,315 858 360 162 135 110 63 55 30 24 16 11 7 14

2008 917 3,915 4,425 4,148 2,190 863 391 228 124 107 47 33 34 22 15 10 7 13

2009 830 3,942 4,615 3,663 2,123 996 418 215 140 91 55 47 41 27 18 12 8 16

2010 868 4,237 4,597 3,764 2,482 1,151 477 271 106 90 65 48 41 27 18 12 8 16

2011 1,031 3,983 4,717 4,245 2,932 1,305 667 262 156 134 79 58 50 33 22 15 10 20

2012 819 4,689 5,769 4,348 2,784 1,498 573 299 173 140 83 61 53 35 23 16 10 21

2013 1,042 5,613 5,906 4,038 2,996 1,496 725 332 184 150 88 65 56 37 25 17 11 22

2014 1,182 5,521 5,561 4,727 3,128 1,696 768 366 203 165 97 72 62 41 27 18 12 24

2015 1,005 5,343 7,228 4,996 3,484 2,023 917 437 242 197 116 86 74 49 33 22 15 29

2016 1,137 7,183 7,834 4,915 4,334 2,321 1,052 501 278 226 133 98 85 56 38 25 17 33

2017 1,557 8,008 7,238 5,876 4,378 2,345 1,062 506 281 228 134 99 85 57 38 25 17 34

2018 1,989 6,417 9,316 6,779 5,050 2,705 1,226 584 324 263 155 115 99 66 44 29 19 39

2019 1,668 8,114 9,211 6,702 4,993 2,674 1,212 577 320 260 153 113 97 65 43 29 19 38

(1 shaded area) = (1) prior column + (2)

For example FLY 2016 @ 60 months: 25,403 = 21,069 + 4,334

(2 lighter shaded area) Based on 2018 August YTD CWA claim exposure count, and the expectation for the remainder of the year

(2 darker shaded area) = Exhibit 4.3 (1) x (Exhibit 4.1 Col. (1) - (1) prior column)

For example FLY 2016 @ 48-60 months: 4,334 = 47.13% x (30,266 - 21,069)

Corporate Actuarial Department

Insurance Corporation of British Columbia Exhibit 4.3

Represented Excluding Large and Catastrophic Bodily Injury Liability

CWA Disposal Rate

(1) CWA Disposal Rate

Fiscal Loss Year 0 - 12 12 - 24 24 - 36 36 - 48 48 - 60 60 - 72 72 - 84 84 - 96 96 - 108 108 - 120 120 - 132 132 - 144 144 - 156 156 - 168 168 - 180 180 - 192 192 - 204 204 - 216

2002 52.40% 45.06% 35.17% 29.56% 23.80% 21.58% 31.14% 28.39% 17.62% 32.09% 21.00% 39.88% 69.53%

2003 51.19% 49.97% 39.70% 35.93% 31.22% 24.50% 31.91% 24.22% 22.68% 30.67% 38.46% 15.63% 28.50% 100.00%

2004 47.14% 52.01% 50.75% 41.80% 32.84% 20.56% 27.27% 28.37% 27.52% 25.93% 31.25% 23.64% 35.00% 33.33% 100.00%

2005 37.02% 47.68% 52.27% 51.88% 44.61% 36.94% 27.73% 28.45% 20.48% 25.76% 30.61% 29.41% 35.97% 33.33% 33.33% 100.00%

2006 4.94% 22.93% 37.43% 46.66% 54.60% 51.92% 42.03% 35.69% 34.98% 29.78% 30.39% 26.37% 30.88% 32.18% 33.33% 33.33% 33.33% 100.00%

2007 4.74% 24.13% 35.50% 48.40% 55.66% 46.52% 36.50% 25.87% 29.08% 33.41% 28.73% 35.20% 29.63% 33.33% 33.33% 33.33% 33.33% 100.00%