80% tio&olo 70% 13% olodaterol global pharmaceuticals and

TRANSCRIPT

Mar 17, 2017

Global Pharmaceuticals and Biotechnology

IMS Tracker

For the Week Ended Mar 10, 2017

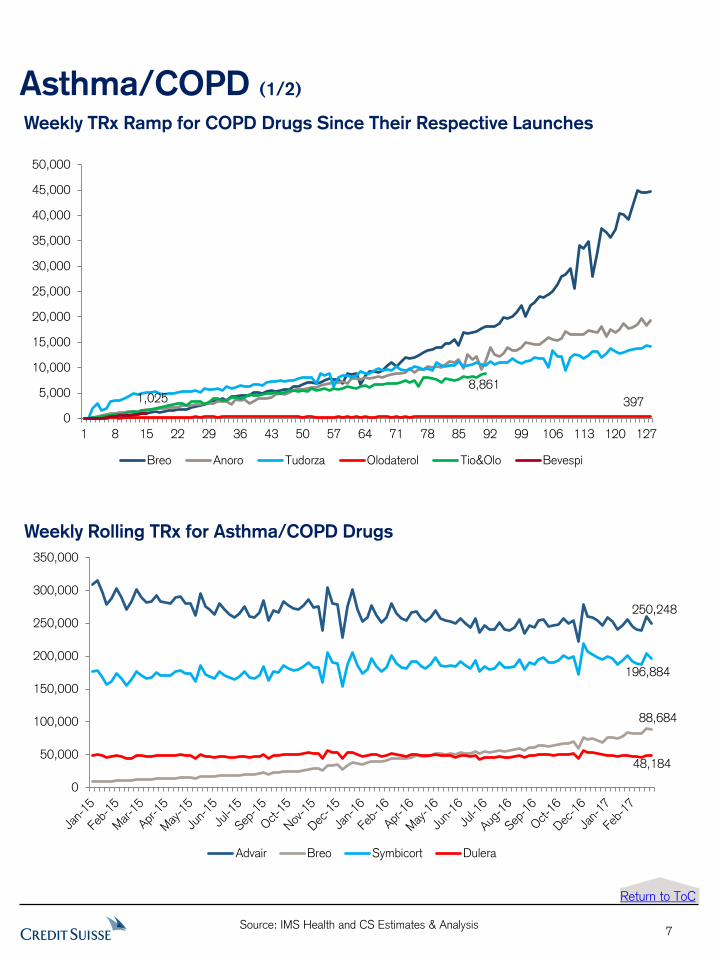

We are highlighting the asthma COPD data this week in light of the AZN deal to

effectively sell the US rights for Tudorza and follow-up combo drug Duaklir to UK

company Circassia, for up to $230m in shares and milestones. AZN will supply and

receive royalties on Duaklir post approval (2018/2019). The franchise has done little

after AZN acquired full global marketing rights in 2014 for $875m + up to $1.22b in

milestones/royalties. US sales have been stuck at around $80m of sales, with NBRx in

the first 9 weeks of 2017 running at only half the level in the same period in 2016, partly

due to loss of Medicare part B coverage. Circassia look for peak sales for Tudorza of

>$90m and Duaklir of >$180m, and believe that with 200 reps they will be effectively

providing 5x the level of US marketing support that AZN has been providing Tudorza

which is currently receiving only a tertiary detail.

Given the apparent investor disappointment over the scale of CV benefit in the FOURIER

study, it is worth noting the continued flat TRx trend for the PCSK-9 class which is

running at around 7,500 TRx and only 2000 NRx, broadly no higher than seen in

December 2016 suggesting no access improvement in 2017.

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

RESEARCH ANALYSTS

Vamil Divan, MD

(212)-538-5394

Alethia Young

(212)-538-0640

Kennen MacKay, PhD

(212)-538-5241

European Pharma Team

(44)-207-888-0304

creditsuisse.pharmateam@credit-

suisse.com

Barbara Kotei

(212)-538-8119

Eliana Merle

(212)-538-0678

Grant Hesser

(212)-325-2587

Source: IMS Health and CS Estimates & Analysis

Weekly NBRx Market Share for Asthma/COPD Drugs

Weekly NBRx Market Share for Asthma/COPD Drugs

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Arcapta

Dulera

Tio&Olo

Olodaterol

Spiriva

Bevespi

Tudorza

Daliresp

Symbicort

Arnuity

Incruse

Anoro

Breo

16%

25%

23%

7%

13%

5%5%

Source: IMS Health and CS Estimates & Analysis

Summary Table – For Week Ended Mar 10

2

Drug Name (Company) TRx % w/w NRx % w/w

Tecfidera (BIIB) 7,997 -3.0% 2,031 1.7%

Copaxone 3TW (TEVA) 9,239 -4.5% 1,865 -3.4%

Glatopa (NOVN) 697 -10.2% 196 -5.3%

Sovaldi (GILD) 208 -13.0% 61 -33.0%

Harvoni (GILD) 3,625 5.8% 1,518 5.0%

Viekira pak/Technivie (ABBV) 83 -12.6% 41 -12.8%

Praluent (SASY/REGN) 3,478 1.3% 886 -0.7%

Repatha (AMGN) 4,140 2.2% 1,370 6.4%

Enbrel (AMGN) 26,930 0.8% 8,351 0.7%

Humira (ABBV) 50,692 0.7% 15,734 -1.7%

Cimzia (UCB) 3,242 -0.9% 961 -5.6%

Imbruvica (ABBV/JNJ) 2,751 -2.4% 894 8.4%

Zydelig (GILD) 102 -13.6% 36 -26.5%

Breo (GSK) 88,684 -0.6% 39,957 -0.6%

Anoro (GSK) 26,910 0.2% 11,714 1.1%

Stribild (GILD) 7,589 -10.8% 2,634 -3.3%

Genvoya (GILD) 18,265 -1.8% 6,416 -1.1%

Triumeq (GSK/PFE) 15,724 -3.0% 5,379 2.8%

Xarelto (JNJ) 182,632 -1.9% 73,032 -1.5%

Eliquis (BMY) 190,067 -1.4% 76,282 -0.8%

Farxiga (AZN) 43,173 -0.2% 16,638 1.5%

Trulicity (LLY) 50,859 -0.9% 20,706 0.6%

Toujeo (SASY) 42,444 -1.6% 17,740 -2.5%

Januvia (MRK) 195,631 -3.1% 78,745 -0.8%

Depression Trintellix (LUN) 30,419 -1.0% 16,313 -0.2%

Prostrate Cancer Zytiga (JNJ) 1,856 -10.5% 568 -2.6%

Breast Cancer Ibrance (PFE) 3,447 -3.7% 1,260 -4.0%

Alzheimer's Disease Namenda XR (AGN) 62,632 -2.7% 22,484 -2.1%

Cardio-metabolites Entresto (NOVN) 12,246 -0.3% 5,599 0.2%

HIV

Anti-coagulants

Anti-Diabetics

Mutilple Sclerosis

HCV

HyperCholesterolae-

mia (PCSK9)

Anti-TNF

Lymphoma

Asthma/COPD

Source: IMS Health and CS Estimates & Analysis

Table of Contents (Click on Titles to Navigate Through Note)

ADHD (Pg 4)

Alzheimer’s Disease – Namenda (Pg 5)

− Weekly TRx % Shares of Namenda Franchise

− Namenda XR TRx Share of Namenda Franchise

Anti-Coagulants (Pg 6)

− Weekly TRx Shares for Anti-Coagulant Drugs

− Weekly NBRx Shares for Anti-Coagulant Drugs

Asthma/COPD (Pg 7)

− Weekly TRx Ramp for Asthma/COPD Drugs

− Weekly TRx Share for Asthma/COPD Drugs

− Weekly NBRx Share for Asthma/COPD Drugs

Autoimmune Anti-TNFs (Pg 9)

− Weekly TRx of Humira and Enbrel

− Weekly TRx of Cimzia, Remicade and Simponi

− Weekly NBRx of Anti-TNFs

Autoimmune – Psoriasis (Pg 11)

− Weekly TRx of Otezla, Xeljanz and Stelara Since

Apr, 2014

− Weekly TRx Ramp for Cosentyx, Stelara and Taltz

Since Their Respective Launches

Breast Cancer (Pg 12)

− Ibrance Weekly TRx and NRx

− Weekly TRx Ramp for Imbruvica and Ibrance

Cardio-metabolite – Entresto (Pg 13)

Cholesterol – PCSK9 (Pg 14)

Depression (Pg 15)

Diabetes (Pg 16)

− Anti-Diabetics Weekly TRx Share

− Anti-Diabetics Weekly NBRx Share

− NBRx % Shares for DPP-IV,& SGLT2 Drugs

− TRx % Shares for DPP-IV & SGLT2 Drugs

− Weekly Rolling TRx for SGLT-2 Drugs

− Weekly NBRx Shares for SGLT-2 Drugs

− Weekly TRx for DPP-4 Class

− Weekly NBRx Shares for DPP-4 Drugs

− Weekly Riolling TRx for GLP-1 Drugs

− Weekly NBRx Shares for GLP-1 Drugs

− Weekly Rolling TRx for GLP-1 Drugs

Diabetes - LA Insulins (Pg 21)

− Weekly Rolling TRx for LA Insulins

− Weekly NBRx Shares for LA Insulins

− Weekly Rolling NBRx for LA Insulins

− Weekly TRx for Tresiba Toujeo, Basglar and Soliqua

Dry Eye Disease (Pg 23)

Gastrointestinal - Constipation (Pg 24)

Gastrointestinal – IBS-D (Pg 25)

HCV (Pg 26)

HIV (Pg 28)

− Weekly TRx Ramp for HIV Drugs

− Weekly NBRx Shares for HIV Drugs

− Weekly Rolling TRx Ramp for HIV Drugs

− Weekly NBRx Shares for HIV Drugs (Company

Split)

Lymphoma (Pg 30)

− Imbruvica Weekly TRx and NRx

− Zydelig Weekly TRx and NRx

Multiple Sclerosis (Pg 31)

− Weekly NBRx % Share of Copaxone OD & 3TW

Copaxone 3TW, Glatopa OD

− Weekly TRx Market Share for Copaxone OD,

Copaxone 3TW, and Glatopa

− Weekly Rolling NRx for MS Drugs

− Weekly Rolling TRx for MS Drugs

− Weekly TRx Market Share for MS Drugs

− Weekly NBRx Market Share for MS Drugs

Opioid Dependence (Pg 34)

− Charts for Weekly NBRx (absolute scrips) and TRx

(% Share) of Opioid Dependence Drugs

Prostrate Cancer (Pg 35)

Pulmonary Arterial Hypertension (PAH) (Pg 36)

− Weekly NRx of PAH Drugs

− Weekly TRx of PAH Drugs

− Weekly NBRx of PAH Drugs

− Weekly TRx Market Share of PAH Drugs

Schizophrenia (Pg 38)

3

Source: IMS Health and CS Estimates & Analysis

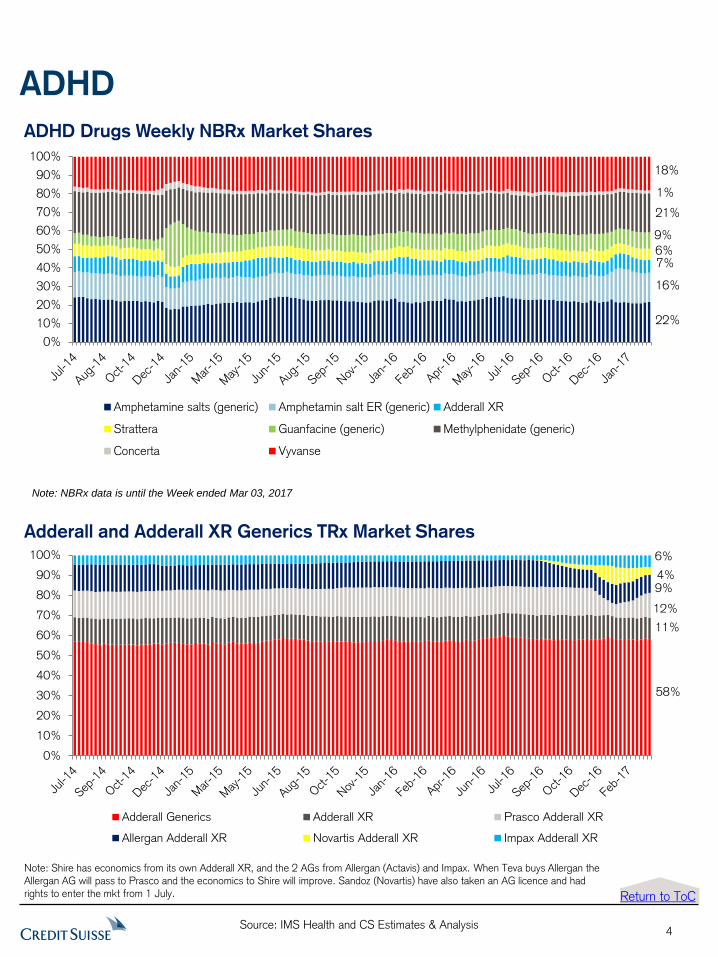

ADHD

4

ADHD Drugs Weekly NBRx Market Shares

Adderall and Adderall XR Generics TRx Market Shares

ADHD Drugs Weekly NBRx Market Shares

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Amphetamine salts (generic) Amphetamin salt ER (generic) Adderall XR

Strattera Guanfacine (generic) Methylphenidate (generic)

Concerta Vyvanse

21%

9%

22%

16%

7%6%

1%

18%

Note: NBRx data is until the Week ended Mar 03, 2017

Adderal and Adderall XR Generics TRx Market Shares

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Adderall Generics Adderall XR Prasco Adderall XR

Allergan Adderall XR Novartis Adderall XR Impax Adderall XR

9%

6%

11%

58%

12%

4%

Note: Shire has economics from its own Adderall XR, and the 2 AGs from Allergan (Actavis) and Impax. When Teva buys Allergan the Allergan AG will pass to Prasco and the economics to Shire will improve. Sandoz (Novartis) have also taken an AG licence and had rights to enter the mkt from 1 July. Return to ToC

Source: IMS Health and CS Estimates & Analysis

Alzheimer’s Disease – Namenda Franchise

Weekly TRx % Share Split of Namenda Franchise

Namenda XR Weekly TRx Share as % of Namenda Franchise

5

Weekly TRx % Share Split of Namenda Franchise

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Aug-1

3

Oct

-13

Nov-

13

Dec-

13

Jan-1

4

Feb-1

4

Mar-

14

May-

14

Jun-1

4

Jul-14

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-

15

Jun-1

5

Jul-15

Sep-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Apr-

16

May-

16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Dec-

16

Jan-1

7

Feb-1

7

Namenda IR Namenda XR Namenda IR Generic Namzaric

55%

38%

7%

Namenda XR Weekly TRx Share as % of Namenda Franchise

0%

10%

20%

30%

40%

50%

60%

Aug-1

3

Oct

-13

Nov-

13

Dec-

13

Jan-1

4

Feb-1

4

Mar-

14

May-

14

Jun-1

4

Jul-1

4

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-

15

Jun-1

5

Jul-1

5

Sep-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Apr-

16

May-

16

Jun-1

6

Jul-1

6

Aug-1

6

Sep-1

6

Oct

-16

Dec-

16

Jan-1

7

Feb-1

738%

Return to ToC

Source: IMS Health and CS Estimates & Analysis

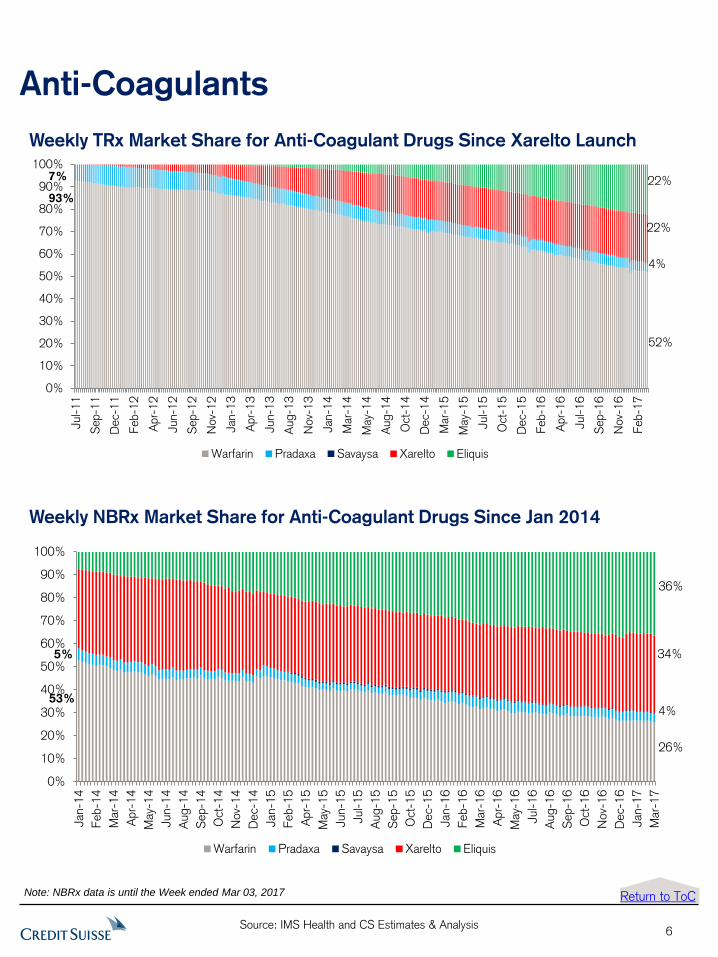

Anti-Coagulants

6

Return to ToC

Weekly TRx Market Share for Anti-Coagulant Drugs Since Xarelto Launch Weekly TRx Market Share for Anti-Coagulant Drugs Since Xarelto Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul-11

Sep-1

1

Dec-

11

Feb-1

2

Apr-

12

Jun-1

2

Sep-1

2

Nov-

12

Jan-1

3

Apr-

13

Jun-1

3

Aug-1

3

Nov-

13

Jan-1

4

Mar-

14

May-

14

Aug-1

4

Oct

-14

Dec-

14

Mar-

15

May-

15

Jul-15

Oct

-15

Dec-

15

Feb-1

6

Apr-

16

Jul-16

Sep-1

6

Nov-

16

Feb-1

7

Warfarin Pradaxa Savaysa Xarelto Eliquis

52%

4%

93%

22%

22%7%

Weekly NBRx Market Share for Anti-Coagulant Drugs Since Jan 2014

Weekly NBRx Market Share for Anti-Coagulant Drugs Since Jan, 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-

14

Jun-1

4

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Dec-

14

Jan-1

5

Feb-1

5

Apr-

15

May-

15

Jun-1

5

Jul-15

Aug-1

5

Sep-1

5

Oct

-15

Dec-

15

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-

16

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Jan-1

7

Mar-

17

Warfarin Pradaxa Savaysa Xarelto Eliquis

26%

4%

34%

36%

5%

53%

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Asthma/COPD (1/2)

Weekly Rolling TRx for Asthma/COPD Drugs

7

Return to ToC

Weekly Rolling TRx for Astham/COPD Drugs

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Advair Breo Symbicort Dulera

48,184

196,884

250,248

88,684

Weekly TRx Ramp for COPD Drugs Since Their Respective Launches

Weekly TRx Ramp for COPD Drugs Since Their Respective Launches

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120 127

Breo Anoro Tudorza Olodaterol Tio&Olo Bevespi

397

8,8611,025

Source: IMS Health and CS Estimates & Analysis

Asthma/COPD (2/2)

8

Weekly NBRx Market Share for Asthma/COPD Drugs

Weekly NBRx Market Share for Asthma/COPD Drugs

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Arcapta

Dulera

Tio&Olo

Olodaterol

Spiriva

Bevespi

Tudorza

Daliresp

Symbicort

Arnuity

Incruse

Anoro

Breo

16%

25%

23%

7%

13%

5%5%

Return to ToC

Note: NBRx data is until the Week ended Mar 03, 2017

Weekly TRx Market Share for Asthma/COPD Drugs

Weekly TRx Market Share for Asthma and COPD Drugs since Breo Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% Arcapta

Dulera

Tio&Olo

Olodaterol

Spiriva

Bevespi

Tudorza

Daliresp

Symbicort

Arnuity

Incruse

Anoro

Breo

Advair

19%

24%

30%

11%

6%4%

48%

26%

18%

Source: IMS Health and CS Estimates & Analysis

Autoimmune Anti-TNFs (1/2)

Weekly TRx of Humira and Enbrel Since Jan 2013

Weekly TRx for Cimzia, Remicade and Simponi Since Jan 2013

9

Weekly TRx of Humira and Enbrel Since Jan, 2013

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Enbrel Humira

50,692

26,930

Weekly TRx for Cimzia, Remicade and Simponi Since Jan, 2013

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Simponi Remicade Cimzia

2,623

1,604

3,242

Return to ToC

Source: IMS Health and CS Estimates & Analysis

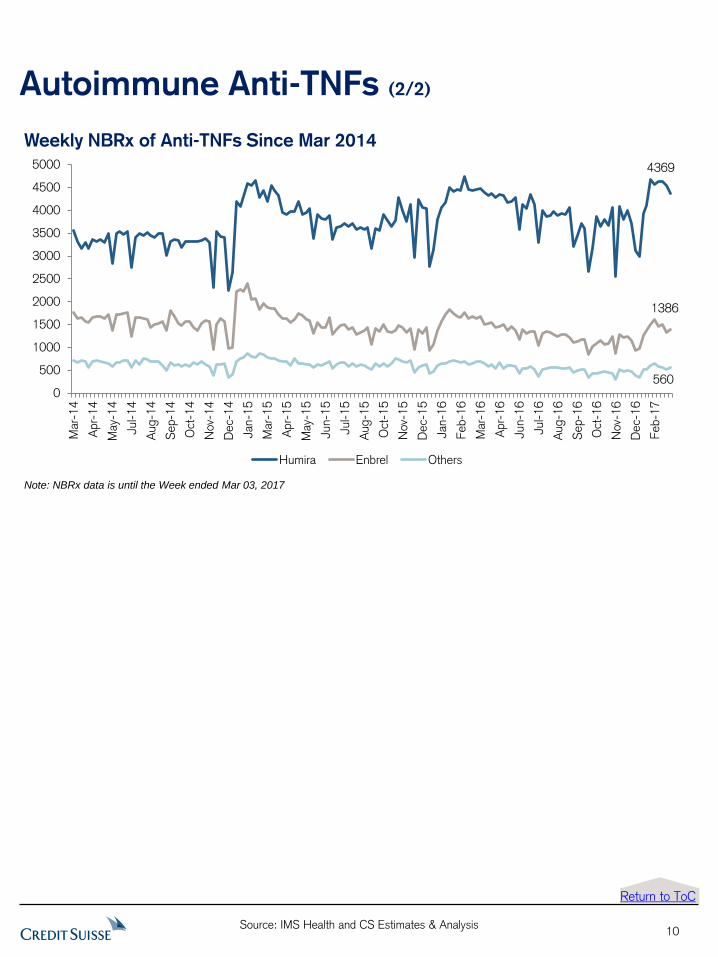

Autoimmune Anti-TNFs (2/2)

Weekly NBRx of Anti-TNFs Since Mar 2014

10

Weekly NBRx of Anti-TNFs Since Mar, 2014

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Mar-

14

Apr-

14

May-

14

Jul-1

4

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Dec-

14

Jan-1

5

Mar-

15

Apr-

15

May-

15

Jun-1

5

Jul-1

5

Aug-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Feb-1

7

Humira Enbrel Others

4369

1386

560

Return to ToC

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

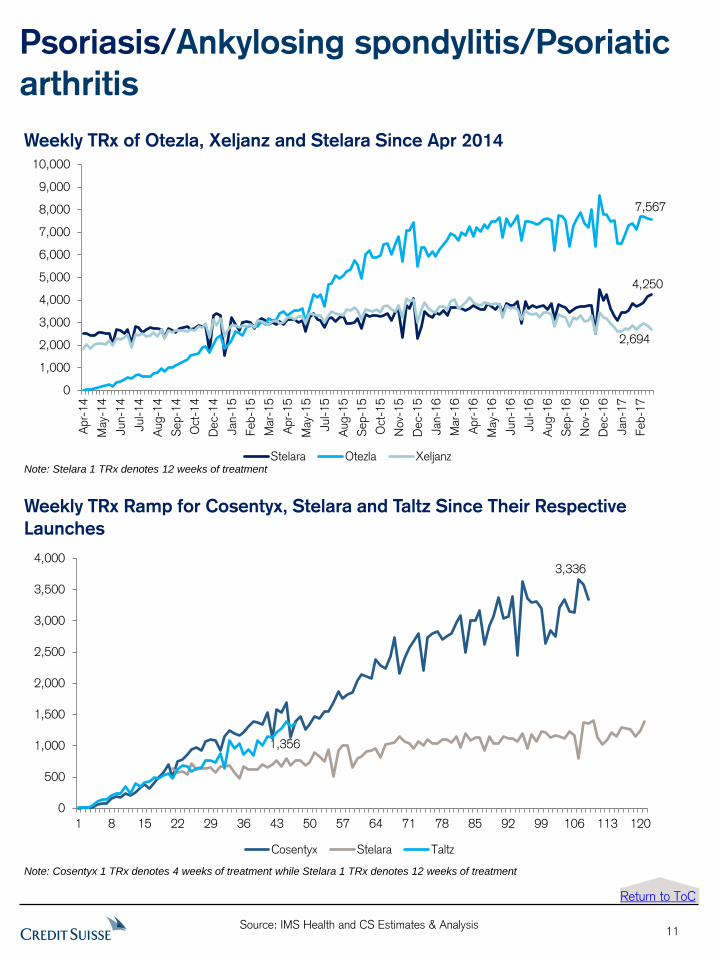

Psoriasis/Ankylosing spondylitis/Psoriatic

arthritis

Weekly TRx of Otezla, Xeljanz and Stelara Since Apr 2014

11

Weekly TRx of Otezla, Xeljanz and Stelara Since Apr, 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Apr-

14

May-

14

Jun-1

4

Jul-1

4

Aug-1

4

Sep-1

4

Oct

-14

Dec-

14

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-

15

Jul-1

5

Aug-1

5

Sep-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Mar-

16

Apr-

16

May-

16

Jun-1

6

Jul-1

6

Aug-1

6

Sep-1

6

Nov-

16

Dec-

16

Jan-1

7

Feb-1

7

Stelara Otezla Xeljanz

7,567

4,250

2,694

Return to ToC

Note: Stelara 1 TRx denotes 12 weeks of treatment

Weekly TRx Ramp for Cosentyx, Stelara and Taltz Since Their Respective

Launches

Weekly TRx Ramp for Cosentyx, Stelara and Taltz Since Their Respective Launches

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120

Cosentyx Stelara Taltz

3,336

1,356

Note: Cosentyx 1 TRx denotes 4 weeks of treatment while Stelara 1 TRx denotes 12 weeks of treatment

Source: IMS Health and CS Estimates & Analysis

Breast Cancer

Ibrance Weekly TRx and NRx Since Launch

Weekly TRx Ramp for Imbruvica and Ibrance Since Their Respective

Launches

12

Note: While not necessarily apples-to-apples, Imbruvica could be seen as a comp in light of Ibrance’s rapid uptake

Ibrance Weekly TRx and NRx Since Launch

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Ibrance TRx Ibrance NRx

1,260

3,447

2,060

Weekly TRx Ramp for Imbruvica and Ibrance Since Their Respective Launches

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120

Ibrance Imbruvica

3,447

Return to ToC

Source: IMS Health and CS Estimates & Analysis

Cardio-metabolic launch - Entresto TRx Ramp for Januvia, Brilinta, Eliquis, Xarelto, Multaq, Entresto, Repatha

and Praluent post their Respective Launches

13

TRx Ramp for Januvia, Brilinta, Eliquis, Xarelto, Multaq, Entresto post their Respective Launches

-1,500

500

2,500

4,500

6,500

8,500

10,500

12,500

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91

Januvia Brilinta Eliquis Xarelto Multaq Entresto Repatha Praluent

12,246

3,873

3,478

6,519

Weekly NBRx for Januvia, Brilinta, Eliquis, Xarelto, Multaq, Entresto,

Repatha and Praluent Since Jun 2014

Return to ToC

Weekly NBRx for Januvia, Brilinta, Eliquis, Xarelto, Multaq, Entresto Since Jun, 2014

0

5,000

10,000

15,000

20,000

25,000

Januvia Brilinta Eliquis Xarelto Entresto Repatha Praluent

15,794

4,151

19,305

17,804

647

2,108

416

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Cholesterol - PCSK9

14

Weekly TRx & NRx Ramp for PCSK9 Drugs Since Their Respective Launches

Return to ToC

Weekly NBRx Ramp for PCSK9 Drugs Since Their Respective Launches

Weekly NBRx Ramp for PCSK9 Drugs Since Their Respective Launches

0

100

200

300

400

500

600

700

800

900

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81

Repatha NBRx Praluent NBRx

725

416

Note: NBRx data is until the Week ended Mar 03, 2017

Weekly TRx & NRx Ramp for PCSK9 Drugs Since Their Respective Launches

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81

Repatha TRx Praluent TRx Repatha NRx Praluent NRx

4,140

3,478

1,370

886

Source: IMS Health and CS Estimates & Analysis

Depression

TRx Ramp for Rexulti and Trintellix post their Respective Launches

15

Weekly NBRx for Branded Anti-Depressant Drugs Since Jan 2014

Weekly NBRx for Branded Anti-Depressant Drugs Since Jan, 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Trintellix Fetzima Rexulti Viibryd

4,472

458

1,504

2,365

Trintellix Weekly TRx and NRx

0

5,000

10,000

15,000

20,000

25,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120

Trintellix TRx Trintellix NRx Rexulti TRx Rexulti NRx

9,842

6,254

Return to ToC Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes (1/6)

Anti-Diabetics Weekly TRx % Share

Weekly Rolling NBRx for Anti-Diabetics

16

Anti-Diabetics Weekly TRx % Share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Metformins Other Oral Anti-Diabetics DPP-IV SGLT-2 Insulins GLP-1

4%

5%

10%

15%

44%

22%

Return to ToC

Weekly Rolling NBRx for Anti-Diabetics

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Metformins Other Oral Anti-Diabetics DPP-IV SGLT2 Insulins GLP-1

31,506

22,52321,901

90,074

58,904

51,187

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes (2/6)

Weekly TRx % Share for DPP-IV & SGLT2 Class Drugs

Weekly NBRx % Share for DPP-IV & SGLT2 Class Drugs

17

Weekly NBRx % Share for DPP-IV, SGLT2, GLP-1 Class Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SGLT2 DPP-IV

58%

42%

Weekly TRx % Share for DPP-IV, SGLT2, GLP-1 Class Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SGLT2 DPP-IV

66%

34%

Return to ToC

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes (3/6)

Weekly NBRx Market Share for SGLT-2 Class Drugs

18

Weekly Rolling TRx for SGLT-2 Drugs

Return to ToC

Weekly Rolling TRx for SGLT-2 Drugs for Last Three Years

0

20000

40000

60000

80000

100000

120000

Farxiga Invokana/Invokamet Xigduo XR (Farxiga + Met)

Glyxambi Jardiance Synjardy (Jardiance + Met)

96,434

43,173

6,67310,962

38,707

2,161

Weekly NBRx Market Share for SGLT-2 Class Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Glyxambi Xigduo XR Jardiance Farxiga Synjardy Invokana/Invokamet

2%5%

31%

20%

39%

2%

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

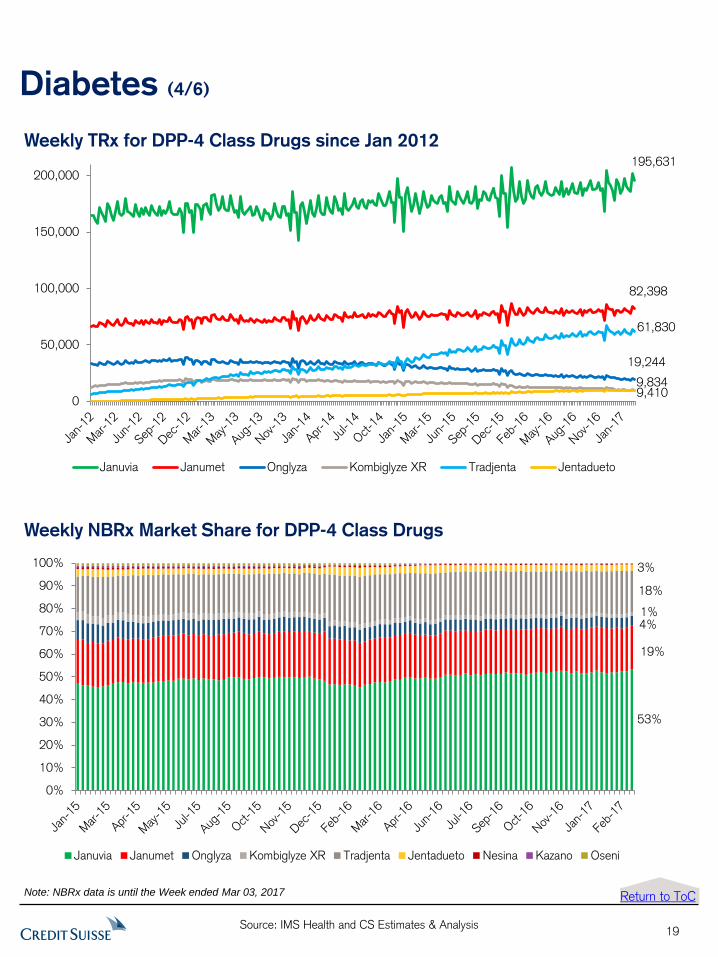

Diabetes (4/6)

Weekly TRx for DPP-4 Class Drugs since Jan 2012

Weekly NBRx Market Share for DPP-4 Class Drugs

19

Weekly NBRx Market Share for DPP-4 Class Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Januvia Janumet Onglyza Kombiglyze XR Tradjenta Jentadueto Nesina Kazano Oseni

4%

18%

53%

1%

3%

19%

Return to ToC

TRx for DPP-4 Class drugs: Januvia, Janumet, Onglyza, Kombiglyze XR and Tradjenta since 2012

0

50,000

100,000

150,000

200,000

Januvia Janumet Onglyza Kombiglyze XR Tradjenta Jentadueto

195,631

82,398

19,244

9,834

61,830

9,410

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes (5/6)

Weekly Rolling TRx for GLP-1 Class Drugs

Weekly NBRx Market Share for GLP-1 Class Drugs

20

Weekly Rolling TRx for GLP-1 Class Drugs

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Trulicity Tanzeum Victoza Bydureon Byetta

50,859

8,307

78,155

22,546

5,882

Return to ToC

Weekly NBRx Market Share for GLP-1 Class Drugs Since June, 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Byetta Victoza Bydureon Tanzeum Trulicity

4%

42%

3%

50%

2%

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes - LA Insulins (1/2)

Weekly Rolling TRx for LA Insulins

Weekly NBRx % Share of LA Insulins

21

Weekly NBRx % Share of LA Insulins

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Soliqua Toujeo Lantus Solostar Lantus Vial Tresiba Levemir Pen Levemir Vial Basaglar Kwikpen

7%

14%

8%

26%

14%

16%

16%

Weekly Rolling TRx of LA Insulins

0

50,000

100,000

150,000

200,000

250,000

300,000

Levemir Vial Levemir Pen Tresiba Lantus Vial

Lantus Solostar Basaglar Kwikpen Soliqua Toujeo

37,115

102,251

31,660

135,988

219,833

17,361

42,444

Return to ToC

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Diabetes - LA Insulins (2/2)

Weekly TRx for Tresiba, Toujeo, Basaglar and Soliqua

22

Weekly TRx for Tresiba, Toujeo, Basglar, and Soliqua

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

91

94

97

10

0

10

3

Toujeo Tresiba Soliqua Basaglar

42,444

31,660

731

17,361

Return to ToC

Weekly Rolling NBRx of LA Insulins

Weekly Rolling NBRx of LA Insulins

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Levemir Vial Levemir Pen Tresiba Lantus Vial

Lantus Solostar Basaglar Kwikpen Soliqua Toujeo

9,292

7,966

8,260

15,071

9,311

488

4,633

3,883

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Dry Eye Disease

23

Return to ToC

Weekly NBRx of Xiidra and Restasis

Weekly TRx% Share of Xiidra and Restasis

Note: NBRx data is until the Week ended Mar 03, 2017

Weekly NBRx of Xiidra and Restasis

0

5,000

10,000

15,000

20,000

25,000

30,000

Restasis Xiidra

11,961

8,530

Weekly TRX% Share of Xiidra and Restasis

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Restasis Xiidra

79%

21%

Source: IMS Health and CS Estimates & Analysis

Gastrointestinal - Constipation

24

Weekly NBRx of Constipation Drugs

Weekly TRx of Constipation Drugs

Weekly NBRx of Constipation Drugs

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Linzess Amitiza Movantik

8,634

5,400

2,620

Note: NBRx data is until the Week ended Mar 03, 2017

Weekly TRx of Constipation Drugs

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan-1

2

Mar

-12

May

-12

Jul-12

Sep-1

2

Nov-

12

Jan-1

3

Mar

-13

May

-13

Jul-13

Sep-1

3

Nov-

13

Jan-1

4

Mar

-14

May

-14

Jul-14

Sep-1

4

Nov-

14

Jan-1

5

Mar

-15

May

-15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar

-16

May

-16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar

-17

Linzess Amitiza Movantik

56,122

30,335

11,127

Return to ToC

Source: IMS Health and CS Estimates & Analysis

Gastrointestinal – IBS-D

25

Weekly NBRx of IBS-D

Weekly TRx of IBS-D

Weekly TRx of IBS-D Drugs

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Jan-1

5

Feb-1

5

Mar

-15

Apr-

15

May

-15

Jun-1

5

Jul-15

Aug-1

5

Sep-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Mar

-16

Apr-

16

May

-16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Jan-1

7

Feb-1

7

Mar

-17

Viberzi Xifaxan

5,228

16,458

Weekly NBRx of IBS-D Drugs

0

1,000

2,000

3,000

4,000

5,000

6,000

Jan-1

5

Feb-1

5

Mar

-15

Apr-

15

May

-15

Jun-1

5

Jul-15

Aug-1

5

Sep-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Mar

-16

Apr-

16

May

-16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Jan-1

7

Feb-1

7

Mar

-17

Viberzi Xifaxan

1,351

3,858

Note: NBRx data is until the Week ended Mar 03, 2017

Return to ToC

Source: IMS Health and CS Estimates & Analysis

HCV (1/2)

Weekly TRx Ramp for HCV Drugs Since Their Respective Launches

Weekly TRx Market Share for HCV Drugs Since Sovaldi Launch

26

Note: Zepatier and Viekira Pak TRx Scripts are not reflective of real world usage because of a data reporting restriction

Weekly TRx Ramp for HCV Drugs Since Their Respective Launches

0

2,000

4,000

6,000

8,000

10,000

12,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120

Incivek Epclusa Sovaldi Victrelis Harvoni Viekira Pak/Technivie Zepatier

3,625

83

1,928

1,083

Return to ToC

Weekly TRx Market Share for HCV Drugs Since Sovaldi Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sovaldi Harvoni Viekira Pak/Technivie Zepatier Epclusa

3%

52%

1%

16%

28%

Note: Zepatier and Viekira Pak TRx Scripts are not reflective of real world usage because of a data reporting restriction

Source: IMS Health and CS Estimates & Analysis

HCV (2/2)

27

Note: Zepatier and Viekira Pak TRx Scripts are not reflective of real world usage because of a data reporting restriction

Return to ToC

Weekly NBRx for HCV Drugs Since Jun 2014 Weekly NBRx for HCV Drugs Since Jun, 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Viekira Pak/Technivie Sovaldi Harvoni Epclusa Zepatier

82

1,234

660

322

41

Note: NBRx data is until the Week ended Mar 03, 2017. Also, Zepatier and Viekira Pak TRx Scripts are not reflective of real world

usage because of a data reporting restriction

Source: IMS Health and CS Estimates & Analysis

HIV (1/2)

Weekly TRx Ramp for HIV Drugs Since their Respective Launches

Weekly NBRx Market Share for HIV Drugs Since Jan 2014

28

Weekly TRx Ramp for HIV Drugs Since their Respective Launches

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120 127

Stribild Genvoya Triumeq

15,72418,265

Weekly NBRx Market Share for HIV Drugs Since Jan, 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Genvoya Stribild Complera Truvada Atripla Triumeq Tivicay Isentress Prezista

14%

11%

4%

2%3%

33%

20%

5%

9%

Return to ToC Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

HIV (2/2)

29

Weekly Rolling TRx for HIV Drugs for Last Three Years

Weekly NBRx Market Share - Company wise Split Since Jan 2014

Weekly NBRx Market Share - Company wise Split Since Jan, 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-

14

Jul-14

Aug-1

4

Sep-1

4

Oct

-14

Nov-

14

Dec-

14

Jan-1

5

Mar-

15

Apr-

15

May-

15

Jun-1

5

Jul-15

Aug-1

5

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Feb-1

7

ViiV (GSK) Gilead Others

25%

62%

14%

Note: NBRx data is until the Week ended Mar 03, 2017

Weekly Rolling TRx for HIV Drugs for Last Three Years

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Jun-1

3

Aug-1

3

Oct

-13

Nov-

13

Jan-1

4

Feb-1

4

Apr-

14

Jun-1

4

Jul-1

4

Sep-1

4

Oct

-14

Dec-

14

Feb-1

5

Mar-

15

May-

15

Jul-1

5

Aug-1

5

Oct

-15

Nov-

15

Jan-1

6

Mar-

16

Apr-

16

Jun-1

6

Jul-1

6

Sep-1

6

Nov-

16

Dec-

16

Feb-1

7

Stribild Genvoya Triumeq Isentress Tivicay

Atripla Complera Prezista Truvada

10,328

15,72413,813

5,393

10,952

35,630

18,265

Return to ToC

Source: IMS Health and CS Estimates & Analysis

Lymphoma (1/2)

Imbruvica Weekly TRx and NRx

Zydelig Weekly TRx and NRx

30

Imbruvica Weekly TRx and NRx

0

500

1,000

1,500

2,000

2,500

3,000

Imbruvica TRx Imbruvica NRx

894

2,751

Zydelig Weekly TRx and NRx

0

50

100

150

200

250

Zydelig NRx Zydelig TRx

36

102

Return to ToC

Source: IMS Health and CS Estimates & Analysis

Multiple Sclerosis (1/3)

Weekly NBRx % Share of Copaxone 20mg, Copaxone 40mg, Glatopa 20mg

Weekly TRx Market Share for Copaxone 20mg, Copaxone 40mg and

Glatopa Since Copaxone 40mg Launch

31

Weekly NBRx % Share of Copaxone OD, Copaxone 3TW, Glatopa OD

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Glatopa Copaxone 40mg Copaxone 20mg

13%

78%

10%

Weekly TRx Market Share for Copaxone OD, Copaxone 3TW, and Glatopa Since Copaxone TIW Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Feb-1

4M

ar-

14

Apr-

14

May-

14

May-

14

Jun-1

4Jul-1

4A

ug-1

4S

ep-1

4O

ct-1

4N

ov-

14

Dec-

14

Jan-1

5Feb-1

5M

ar-

15

Apr-

15

May-

15

May-

15

Jun-1

5Jul-1

5A

ug-1

5S

ep-1

5O

ct-1

5N

ov-

15

Dec-

15

Jan-1

6Feb-1

6M

ar-

16

Apr-

16

Apr-

16

May-

16

Jun-1

6Jul-1

6A

ug-1

6S

ep-1

6O

ct-1

6N

ov-

16

Dec-

16

Jan-1

7Feb-1

7M

ar-

17

Glatopa Copaxone 40mg Copaxone 20mg

6%

13%

81%

Return to ToC

Note: NBRx data is until the Week ended Mar 03, 2017. Also, Glatopa Scripts are not reflective of real world usage because of a data

reporting restriction.

Note: IMS noted a reporting restriction due to a confidential supplier agreement soon after Glatopa launch. IMS have not

estimated missing scripts and we do not know to what extent Glatopa scripts in this figure understate utilisation.

Source: IMS Health and CS Estimates & Analysis

Multiple Sclerosis (2/3)

Weekly TRx Mkt Share for MS Drugs since Tecfidera Launch

32

Return to ToC

Note: IMS noted a reporting restriction due to a confidential supplier agreement soon after Glatopa launch. IMS have not estimated missing

scripts and we do not know to what extent Glatopa scripts in this figure understate utilisation.

Weekly TRx Mkt Share for MS Drugs since Tecfidera Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Interferons Copaxone/Generics Orals Others

26%

30%

2%

42%

Weekly NBRx Mkt Share for MS Drugs

Weekly NBRx Mkt Share for MS Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Interferons Copaxone/Generics Orals Others

21%

30%

47%

3%

Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Multiple Sclerosis (3/3)

33

Weekly NBRx Market Share for MS Drugs

Weekly Rolling TRx for MS Drugs Weekly Rolling TRx for MS Drugs for Last Three Years

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jun-1

3

Aug-1

3

Oct-

13

Nov-

13

Jan-1

4

Feb-1

4

Apr-

14

Jun-1

4

Jul-14

Sep-1

4

Oct-

14

Dec-1

4

Feb-1

5

Mar-

15

May-

15

Jul-15

Aug-1

5

Oct-

15

Nov-

15

Jan-1

6

Mar-

16

Apr-

16

Jun-1

6

Jul-16

Sep-1

6

Nov-

16

Dec-1

6

Feb-1

7

Tecfidera Gilenya Aubagio Plegridy Glatopa Copaxone 40mg

7,997

4,302

3,519

778697

9,239

Return to ToC

Note: IMS noted a reporting restriction due to a confidential supplier agreement soon after Glatopa launch. IMS have not

estimated missing scripts and we do not know to what extent Glatopa scripts in this figure understate utilisation.

Weekly NBRx Market Share for MS Drugs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Copaxone 40mg Plegridy Aubagio Gilenya Tecfidera Glatopa

16%

14%

31%

33%

4%

3%

Note: NBRx data is until the Week ended Mar 03, 2017. Also, Glatopa Scripts are not reflective of real world usage

because of a data reporting restriction.

Source: IMS Health and CS Estimates & Analysis

Opioid Dependence

Weekly NBRx for Opioid Dependence Drugs Since May 14

Weekly TRx Market Share for Opioid Dependence Drugs Since May 14

34

Note: NBRx data is until the Week ended Mar 03, 2017.

Weekly TRx Market Share for Opoid Dependance Drugs Since May 14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Suboxone Film Zubsolv Bunavail

Buprenorphin/Nalox (generic) Subutex Buprenorphine (generic)

Depade (naltrexone) Naltrexone (generic)

4%1%

17%

7%

16%

56%

Return to ToC

Weekly NBRx for Opoid Dependance Drugs Since May 14

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Zubsolv Suboxone Film Buprenorphine (generic)

Bunavail Depade (naltrexone) Naltrexone (generic)

Buprenorphin/Nalox (generic)

935

148

2,410

5,253

4,123

6,094

Source: IMS Health and CS Estimates & Analysis

Prostrate Cancer (Zytiga)

Zytiga and Xtandi Weekly TRx Since Oct 2013

Zytiga and Xtandi Weekly NBRx Since Oct 2013

35

Zytiga and Xtandi Weekly TRx

0

500

1,000

1,500

2,000

2,500

3,000

Zytiga Xtandi

1,546

1,856

Weekly NBRx for Zytiga and Xtandi Since Oct, 2013

0

50

100

150

200

250

300

350

Xtandi Zytiga

148

197

Return to ToC Note: NBRx data is until the Week ended Mar 03, 2017

Source: IMS Health and CS Estimates & Analysis

Pulmonary Arterial Hypertension (PAH) (1/2)

36

Weekly NRx for PAH Drugs Since Jun 2014

Weekly TRx for PAH Drugs Since Jun 2014

Weekly NRx of PAH Drugs Since Jan, 2014

0

50

100

150

200

250

Opsumit Tracleer Adempas Uptravi Orenitram ER

177

20

107

Weekly TRx of PAH Drugs Since Jan, 2014

0

200

400

600

800

1,000

1,200

1,400

Jun-1

4

Jul-14

Aug-1

4

Sep-1

4

Oct

-14

Oct

-14

Nov-

14

Dec-

14

Jan-1

5

Feb-1

5

Mar-

15

Apr-

15

May-

15

Jun-1

5

Jul-15

Aug-1

5

Sep-1

5

Oct

-15

Oct

-15

Nov-

15

Dec-

15

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-

16

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Sep-1

6

Oct

-16

Nov-

16

Dec-

16

Jan-1

7

Feb-1

7

Opsumit Tracleer Adempas Uptravi Orenitram ER

915

136

258

Return to ToC

Source: IMS Health and CS Estimates & Analysis

Pulmonary Arterial Hypertension (PAH) (2/2)

37

Weekly TRx Market Share for PAH Drugs Since Jun 2014

Return to ToC

Weekly TRx Market Share of PAH Drugs Since Jan, 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Opsumit Tracleer Adempas Uptravi Orenitram ER

70%

10%

20%

Weekly NBRx for PAH Drugs Since Jun 2014 Weekly NBRx for PAH Drugs Since Jun, 2014

0

10

20

30

40

50

60

70

80

90

Tracleer Opsumit Uptravi Adempas Orenitram ER

52

34

7

Note: NBRx data is until the Week ended Mar 03, 2017.

Source: IMS Health and CS Estimates & Analysis

Schizophrenia

38

Weekly TRx Ramp for Schizophrenia Drugs Since their Respective Launches Vraylar Launch Performance

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120

Vraylar Rexulti Latuda Abilify Maintena Aristada

5,018

9,842

1,128

Return to ToC

Companies Mentioned (Price as of 16-Mar-2017)

AbbVie Inc. (ABBV.N, $65.9) Actelion (ATLN.S, SFr275.1) Adamas Pharmaceuticals, Inc. (ADMS.OQ, $17.49) Aimmune Therapeutics (AIMT.OQ, $22.06) Akorn (AKRX.OQ, $22.82) Alder Biopharmaceuticals (ALDR.OQ, $23.4) Alkermes plc (ALKS.OQ, $58.98) Allergan Plc. (AGN.N, $239.42) AmerisourceBergen (ABC.N, $88.0) Amgen, Inc. (AMGN.OQ, $180.11) Amphastar Pharms (AMPH.OQ, $13.35) Arena Pharmaceuticals Inc (ARNA.OQ, $1.57) AstraZeneca (AZN.L, 4866.0p) Baxter International Inc. (BAX.N, $51.43) Bayer (BAYGn.DE, €107.0) Biodelivery Sci (BDSI.OQ, $2.0) Biogen, Inc. (BIIB.OQ, $278.96) Bristol-Myers Squibb Co. (BMY.N, $57.31) CVS Health (CVS.N, $79.56) Celgene Corporation (CELG.OQ, $126.62) Cigna Corporation (CI.N, $151.79) Circassia Pharma (CIRCI.L, 87.25p) Corvus Pharmaceuticals, Inc. (CRVS.OQ, $20.42) Edge Therapeutics, Inc. (EDGE.OQ, $8.92) Eli Lilly & Co. (LLY.N, $84.99) Esperion Therapeutics (ESPR.OQ, $29.65) Express Scripts (ESRX.OQ, $64.83) Galapagos NV (GLPG.AS, €75.5) Gilead Sciences, Incorporated (GILD.OQ, $68.54) GlaxoSmithKline plc (GSK.L, 1690.5p) Impax Laboratories, Inc (IPXL.OQ, $9.55) Indivior (INDV.L, 331.9p) Ironwood Pharmaceuticals, Inc. (IRWD.OQ, $17.67) Johnson & Johnson (JNJ.N, $128.46) Lundbeck (LUN.CO, Dkr303.3) Malinckrodt (MNK.N, $47.95) Merck & Co., Inc. (MRK.N, $64.18) Mylan Inc. (MYL.OQ, $42.49) MyoKardia, Inc. (MYOK.OQ, $14.8) Novartis (NOVN.S, SFr75.3) Novo Nordisk A/S (NOVOb.CO, Dkr236.0) Orexigen Therapeutics Inc. (OREX.OQ, $4.26) Orexo (ORX.ST, Skr30.7) Otsuka Holdings (4578.T, ¥5,246) PD-Rx (PDRX.PK, $7.0) Perrigo Company plc (PRGO.N, $70.87) Pfizer (PFE.N, $34.43) Portola Pharmaceuticals (PTLA.OQ, $40.2) Reckitt Benckiser (RB.L, 7370.0p) Sanofi (SASY.PA, €83.02) Shire Pharmaceuticals (SHP.L, 4857.5p) Sucampo Pharmaceuticals (SCMP.OQ, $10.9) Sun Pharmaceuticals Industries Limited (SUN.BO, Rs710.9) Takeda Pharmaceutical (4502.T, ¥5,314) Teva Pharm Ind (TEVA.TA, agora12210.0) Teva Pharmaceutical (TEVA.N, $33.93) UCB (UCB.BR, €71.1) VIVUS, Inc. (VVUS.OQ, $1.1) Versartis, Inc. (VSAR.OQ, $18.45)

Disclosure Appendix

Analyst Certification

Vamil Divan, MD, Alethia Young, Kennen MacKay, Ph.D., Grant Hesser, Eliana Merle and European Pharma Team each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector , with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutra l may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time.

Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 45% (64% banking clients)

Neutral/Hold* 38% (61% banking clients)

Underperform/Sell* 14% (53% banking clients)

Restricted 2%

*For purposes of the NYSE and FINRA ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, a nd Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

Important Global Disclosures

Credit Suisse’s research reports are made available to clients through our proprietary research portal on CS PLUS. Credit Suisse research products may also be made available through third-party vendors or alternate electronic means as a convenience. Certain research products are only made available through CS PLUS. The services provided by Credit Suisse’s analysts to clients may depend on a specific client’s preferences regarding the frequency and manner of receiving communications, the client’s risk profile and investment, the size and scope of the overall client relationship with the Firm, as well as legal and regulatory constraints. To access all of Credit Suisse’s research that you are entitled to receive in the most timely manner, please contact your sales representative or go to https://plus.credit-suisse.com .

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: https://www.credit-suisse.com/sites/disclaimers-ib/en/managing-conflicts.html .

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

See the Companies Mentioned section for full company names

The subject company (CI.N, ESRX.OQ, GILD.OQ, GSK.L, INDV.L, LUN.CO, NOVN.S, NOVOb.CO, RB.L, SASY.PA, UCB.BR, ABBV.N, ABC.N, ADMS.OQ, AGN.N, AIMT.OQ, ALDR.OQ, AMGN.OQ, ATLN.S, AZN.L, BAX.N, BAYGn.DE, BIIB.OQ, BMY.N, CELG.OQ, JNJ.N, LLY.N, MRK.N, MYOK.OQ, TEVA.N, PTLA.OQ, PRGO.N, PFE.N, OREX.OQ, GLPG.AS, CRVS.OQ, ESPR.OQ, SHP.L, IPXL.OQ) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (ESRX.OQ, GILD.OQ, NOVN.S, ABBV.N, ABC.N, AGN.N, AIMT.OQ, AMGN.OQ, ATLN.S, BAX.N, BAYGn.DE, BMY.N, CELG.OQ, JNJ.N, LLY.N, MRK.N, MYOK.OQ, TEVA.N, PTLA.OQ, PRGO.N, PFE.N, CRVS.OQ, ESPR.OQ, SHP.L, IPXL.OQ) within the past 12 months.

Credit Suisse provided non-investment banking services to the subject company (ESRX.OQ, GILD.OQ, ABC.N, AMGN.OQ, BIIB.OQ, CELG.OQ, TEVA.N) within the past 12 months

Credit Suisse has managed or co-managed a public offering of securities for the subject company (ESRX.OQ, NOVN.S, ABBV.N, BAX.N, BAYGn.DE, BMY.N, LLY.N, MYOK.OQ, TEVA.N, PFE.N, CRVS.OQ, SHP.L) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (ESRX.OQ, GILD.OQ, NOVN.S, ABBV.N, ABC.N, AGN.N, AIMT.OQ, AMGN.OQ, ATLN.S, BAX.N, BAYGn.DE, BMY.N, CELG.OQ, JNJ.N, LLY.N, MRK.N, MYOK.OQ, TEVA.N, PTLA.OQ, PRGO.N, PFE.N, CRVS.OQ, ESPR.OQ, SHP.L, IPXL.OQ) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (CVS.N, CI.N, ESRX.OQ, GILD.OQ, GSK.L, INDV.L, LUN.CO, NOVN.S, NOVOb.CO, RB.L, SASY.PA, SUN.BO, UCB.BR, 4578.T, ABBV.N, ABC.N, ADMS.OQ, AGN.N, AIMT.OQ, ALDR.OQ, ALKS.OQ, AMGN.OQ, ATLN.S, AZN.L, BAX.N, BAYGn.DE, BIIB.OQ, BMY.N, CELG.OQ, JNJ.N, LLY.N, MRK.N, MYOK.OQ, VSAR.OQ, TEVA.N, PTLA.OQ, PRGO.N, PFE.N, OREX.OQ, GLPG.AS, CRVS.OQ, EDGE.OQ, ESPR.OQ, SHP.L, 4502.T, IPXL.OQ) within the next 3 months.

Credit Suisse has received compensation for products and services other than investment banking services from the subject company (ESRX.OQ, GILD.OQ, ABC.N, AMGN.OQ, BIIB.OQ, CELG.OQ, TEVA.N) within the past 12 months

As of the date of this report, Credit Suisse makes a market in the following subject companies (CI.N, JNJ.N, TEVA.N).

Please visit https://credit-suisse.com/in/researchdisclosure for additional disclosures mandated vide Securities And Exchange Board of India (Research Analysts) Regulations, 2014

Credit Suisse may have interest in (SUN.BO)

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (OREX.OQ, ESPR.OQ, SHP.L).

As of the end of the preceding month, Credit Suisse beneficially own between 1-3% of a class of common equity securities of (NOVN.S, ATLN.S).

Credit Suisse beneficially holds >0.5% long position of the total issued share capital of the subject company (ATLN.S, OREX.OQ).

Credit Suisse has a material conflict of interest with the subject company (CI.N) . Credit Suisse is acting as financial advisor to Anthem Inc. (ANTM) on its announced acquisition of Cigna Corporation (CI).

Credit Suisse has a material conflict of interest with the subject company (GSK.L) . "Urs Rohner, the Chairman of Credit Suisse is a non-executive Director of GlaxoSmithKline plc (LSE:GSK)"

Credit Suisse has a material conflict of interest with the subject company (ABC.N) . Credit Suisse is acting as financial adviser to PharMedium Healthcare Holdings, Inc. in relation to its definitive agreement to be acquired by AmerisourceBergen (ABC).

Credit Suisse has a material conflict of interest with the subject company (ATLN.S) . “Credit Suisse is acting as financial advisor to Actelion in relation to the proposed acquisition by Johnson & Johnson and spin out of its drug discovery operations and early-stage clinical development assets into a newly created Swiss biopharmaceutical company”

Credit Suisse has a material conflict of interest with the subject company (BAX.N) . Credit Suisse acted as the financial advisor to Claris Lifesciences Limited in relation to their announced transaction to sell their global generics injectables business to Baxter International, Inc.

Credit Suisse has a material conflict of interest with the subject company (BAYGn.DE) . Credit Suisse is acting as joint lead financial advisor to Bayer in relation to the proposed offer for Monsanto.

Credit Suisse has a material conflict of interest with the subject company (JNJ.N) . "Credit Suisse is acting as financial advisor to Actelion in relation to the proposed acquisition by Johnson & Johnson and spin out of its drug discovery operations and early-stage clinical development assets into a newly created Swiss biopharmaceutical company”

As of the date of this report, an analyst involved in the preparation of this report has the following material conflict of interest with the subject company (CVS.N). Training

As of the date of this report, an analyst involved in the preparation of this report has the following material conflict of interest with the subject company (PFE.N). As of the date of this report, an analyst involved in the preparation of this report, Vamil Divan, has following material conflicts of interest with the subject company. The analyst or a member of the analyst's household has a long position in the common stock Pfizer (PFE.N). A member of the analyst's household is an employee of Pfizer (PFE.N).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

For date and time of production, dissemination and history of recommendation for the subject company(ies) featured in this report, disseminated within the past 12 months, please refer to the link: https://rave.credit-suisse.com/disclosures/view/report?i=239614&v=1ng708dueh99sis9xuvob0psr .

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report may participate in events hosted by the subject company, including site visits. Credit Suisse does not accept or permit analysts to accept payment or reimbursement for travel expenses associated with these events.

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

The following disclosed European company/ies have estimates that comply with IFRS: (LUN.CO, RB.L, SASY.PA, UCB.BR, ATLN.S, AZN.L, BMY.N).

An analyst involved in the preparation of this report received third party benefits in connection with this research report from the subject company (CVS.N)

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (ESRX.OQ, GSK.L, NOVN.S, ABBV.N, ABC.N, ADMS.OQ, AIMT.OQ, ALDR.OQ, AMGN.OQ, AZN.L, BAX.N, BAYGn.DE, BIIB.OQ, BMY.N, CELG.OQ, LLY.N, MRK.N, MYOK.OQ, VSAR.OQ, TEVA.N, PTLA.OQ, PRGO.N, PFE.N, GLPG.AS, CRVS.OQ, EDGE.OQ, ESPR.OQ, SHP.L) within the past 3 years.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

This research report is authored by:

Credit Suisse Securities (USA) LLCVamil Divan, MD ; Alethia Young ; Kennen MacKay, Ph.D. ; Grant Hesser ; Eliana Merle ; Barbara Kotei ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Matthew Keeler ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen ; Muriel Chen

Credit Suisse International .................................................................................................................................................. European Pharma Team

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the FINRA 2241 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Credit Suisse International .................................................................................................................................................. European Pharma Team

Important disclosures regarding companies or other issuers that are the subject of this report are available on Credit Suisse’s disclosure website at https://rave.credit-suisse.com/disclosures or by calling +1 (877) 291-2683.

This report is produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who-we-are This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates.The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk.

This report is issued and distributed in European Union (except Switzerland): by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Germany: Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). United States and Canada: Credit Suisse Securities (USA) LLC; Switzerland: Credit Suisse AG; Brazil: Banco de Investimentos Credit Suisse (Brasil) S.A or its affiliates; Mexico: Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); Japan: by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau ( Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Investment Advisers Association, Type II Financial Instruments Firms Association; Hong Kong: Credit Suisse (Hong Kong) Limited; Australia: Credit Suisse Equities (Australia) Limited; Thailand: Credit Suisse Securities (Thailand) Limited, regulated by the Office of the Securities and Exchange Commission, Thailand, having registered address at 990 Abdulrahim Place, 27th Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok10500, Thailand, Tel. +66 2614 6000; Malaysia: Credit Suisse Securities (Malaysia) Sdn Bhd; Singapore: Credit Suisse AG, Singapore Branch; India: Credit Suisse Securities (India) Private Limited (CIN no.U67120MH1996PTC104392) regulated by the Securities and Exchange Board of India as Research Analyst (registration no. INH 000001030) and as Stock Broker (registration no. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th